MCAI Lex Vision: Defining “Gaming” Under the Commodity Exchange Act, The Rule 40.11 Gap Driving the Nationwide Kalshi Litigation Web

A Rule 40.11 Framework for the Commodity Futures Trading Commission to Stabilize Jurisdiction, Federal Preemption, and Private Liability in Prediction Markets

Submitted as a public comment to the Commodity Futures Trading Commission (CFTC) in response to the Advance Notice of Proposed Rulemaking (ANPRM) on Prediction Markets (RIN 3038–AF65), published at 91 Fed. Reg. 12516 (Mar. 16, 2026), this filing addresses Question 19 concerning the scope and public interest implications of “gaming” under CEA § 5c(c)(5)(C), and proposes targeted amendments to 17 C.F.R. § 40.11 and related provisions to define the term, restore an economic-purpose screen, require affirmative Commission approval for enumerated-activity contracts, and resolve the regulatory gap currently driving parallel federal, state, and private litigation.

CFTC ANPRM Question 19 — What factors should the Commission consider in determining the scope and public interest implications of [gaming] activity?” (including subparts 19.a through 19.f). 91 Fed. Reg. 12516, 12521 (Mar. 16, 2026).

Who the MindCast Submission is Relevant to:

CFTC Office of General Counsel: Identifies "deference vulnerabilities" under Loper Bright that could undermine the Commission's preemption cases in the Ninth and Fourth Circuits, offering a path to "harden" the agency’s position by completing the administrative record before courts define "gaming" themselves. Registered Entities (e.g., Kalshi): Highlights a "private enforcement gap" where platforms face compounding class-action damages under 7 U.S.C. § 25(b) while Rule 40.11 remains undefined and proposes a predictable "affirmative approval" framework to replace the current reactive litigation posture. State Attorneys General: Provides a functional "economic purpose" filter to separate federal risk-management tools from state-regulated "contests of chance," directly addressing the concerns raised by the 30-state amicus coalition regarding gambling enforcement. Plaintiffs' Bar: Offers firms in active litigation, such as Kaiserman v. Kalshi, a documented argument that Rule 40.11 currently imposes an affirmative prohibition that exists independently of any ongoing appellate outcomes or judicial stays. Federal Judiciary: Supplies the "reasoned deliberative record" required by administrative law standards (State Farm/Chenery) to avoid the necessity of judges making ad hoc policy decisions from the bench under the new independent judgment standards.

QUESTION PRESENTED

Whether the Commodity Futures Trading Commission may assert exclusive federal jurisdiction over event contracts as swaps, and seek preemption of state enforcement on that basis, while leaving unresolved through open rulemaking the scope of “gaming” under Commodity Exchange Act section 5c(c)(5)(C), 7 U.S.C. § 7a-2(c)(5)(C), and 17 C.F.R. § 40.11.

MindCast does not ask the Commission to answer a litigation question. MindCast identifies the single regulatory action — completing the Rule 40.11 definitional rulemaking — that resolves the structural contradiction the question above presents and that preserves the Commission’s institutional authority regardless of how any pending court proceeding resolves.

I. Summary of Comment and Proposed Rulemaking

The Commission asks, in Question 19 of the Advance Notice of Proposed Rulemaking, what factors should govern the scope and public interest implications of the “gaming” activity enumerated in CEA section 5c(c)(5)(C). Events that postdate publication of the Advance Notice have made answering that question not merely advisable but structurally necessary. The Commission filed an amicus brief on February 17, 2026 asserting exclusive federal jurisdiction over prediction market event contracts. The Commission and the Department of Justice jointly filed a Supremacy Clause action against Arizona, Illinois, and Connecticut on April 2, 2026. The Third Circuit issued a divided panel opinion on April 6, 2026 in KalshiEX LLC v. Flaherty, holding that sports-related event contracts listed on a designated contract market are swaps under the Commodity Exchange Act and that state gambling enforcement is preempted, while expressly declining to decide the scope of Rule 40.11. A private class action under 7 U.S.C. § 25(b), Kaiserman v. Kalshi Inc., was filed in the Northern District of Georgia on March 20, 2026, alleging that the registered entities violated Rule 40.11’s gaming prohibition and seeking damages for every United States trader who lost money on sports contracts. Washington Attorney General Nick Brown filed suit against KalshiEX LLC in King County Superior Court on March 27, 2026, alleging violations of the Washington Gambling Act and the Consumer Protection Act; the action has since been removed to federal court in Seattle.

Each of these developments turns on the same unresolved question: what does “gaming” mean in CEA section 5c(c)(5)(C) and Rule 40.11? The Commission is currently defending its exclusive jurisdiction in federal court while its own rulemaking docket concedes that the governing definition remains open. An agency asserting finality in litigation while soliciting public input on the same question faces a deference problem that does not turn on the statutory merits and that will compound the longer it persists.

MindCast proposes that the Commission convert the Advance Notice into a Notice of Proposed Rulemaking focused specifically on Rule 40.11 and amend that rule to: (i) adopt a textual definition of “gaming” that distinguishes contracts performing a recognized economic function — risk transfer, hedging, and price discovery — from contracts whose demand reflects consumption rather than risk transfer; (ii) revive, in modified form, the pre-2000 economic purpose test as a public interest screen; (iii) require affirmative Commission approval under 17 C.F.R. § 40.3, rather than passive non-disapproval under § 40.2(a)(2), for event contracts implicating any of the five activities enumerated in CEA section 5c(c)(5)(C); and (iv) include an express non-displacement clause clarifying that Rule 40.11’s gaming prohibition operates as an independent federal prohibition that does not turn on, and is not preempted by, any parallel state-law gambling classification. The proposed amendments supply an administrable standard, preserve the federal preemption architecture the Commission and the Department of Justice are defending, close the private enforcement gap the Third Circuit majority left open, and supply the completed deliberative record that the Commission’s pending litigation requires.

II. The Regulatory Posture Problem the Advance Notice Must Resolve

Seven public-record developments between February 6 and April 6, 2026 define the posture the Advance Notice must resolve. Each is documented in a primary public source; each pushes in a different doctrinal direction; and each compounds the legal exposure created by the absence of a completed Rule 40.11 definition.

A. February 6, 2026 — Withdrawal of the 2024 Proposed Rules

The Commission withdrew the June 10, 2024 proposed event-contract rules on February 6, 2026. See Event Contracts; Withdrawal of Proposed Regulatory Action, 91 Fed. Reg. 5386 (Feb. 6, 2026). The withdrawal notice states that the Commission acted “in light of various forms of state regulatory actions and litigation concerning the Commission’s exclusive jurisdiction over event contract derivatives listed on designated contract markets and the proper application of the swap and excluded commodity definitions.” Id. The prior proposal would have specified, by rule, which categories of event contracts the Commission considered contrary to the public interest under CEA section 5c(c)(5)(C). The withdrawal left Rule 40.11’s gaming prohibition in force but undefined.

B. February 17, 2026 — The Commission’s Ninth Circuit Amicus Brief

The Commission filed an amicus brief in the Ninth Circuit consolidated appeal, North American Derivatives Exchange, Inc. v. State of Nevada, No. 25-7187, asserting that the CEA grants the Commission exclusive jurisdiction over prediction market event contracts traded on designated contract markets and that state gambling laws are preempted as applied to such contracts. The brief was filed before the Advance Notice issued and before the comment window opened. The Commission’s jurisdictional position in the Ninth Circuit thus rests on statutory and regulatory authority whose scope the Commission itself has since opened for public comment.

C. March 12–16, 2026 — The Advance Notice of Proposed Rulemaking

The Commission published the Advance Notice on March 12, 2026, and it appeared in the Federal Register on March 16, 2026. 91 Fed. Reg. 12516 (Mar. 16, 2026). Question 19 asks the public to identify “factors” relevant to the “scope and public interest implications” of the gaming activity under CEA section 5c(c)(5)(C), with subparts 19.a (sources informing the scope of “gaming”), 19.b (contest-type distinctions), 19.c (manipulation, abusive sales practices, innovation, and fair competition), 19.d (market participant characteristics), 19.e (responsible gaming standards), and 19.f (differences among types of gaming-involving event contracts). 91 Fed. Reg. at 12521. The Commission’s request for public input on the scope of the gaming category is an explicit acknowledgment that the governing definition is not yet settled.

D. March 20, 2026 — Kaiserman v. Kalshi Inc.

On March 20, 2026, Brian Kaiserman filed a putative class action in the Northern District of Georgia, Kaiserman v. Kalshi Inc., et al., No. 1:26-cv-01525-VMC. The complaint invokes the private right of action under 7 U.S.C. § 25(b) against KalshiEX LLC, Kalshi Klear LLC, their corporate parents, and three named executive officers. The complaint alleges that Rule 40.11 prohibits the listing or clearing of event contracts that “involve, relate to, or reference . . . gaming,” that Kalshi’s sports contracts satisfy that prohibition on its face, and that section 25(b) supplies a federal damages remedy that does not require any new regulatory determination to proceed. The complaint seeks damages on behalf of every United States trader who lost money on Kalshi sports contracts.

E. March 27, 2026 — Washington v. KalshiEX LLC

Washington Attorney General Nick Brown filed a civil action against KalshiEX LLC in King County Superior Court on March 27, 2026, alleging violations of the Washington Gambling Act, the Consumer Protection Act, and the Recovery of Money Lost at Gambling Act. The complaint seeks injunctive relief to halt Kalshi’s operations in Washington, restitution for state residents who lost money on the platform, and civil penalties. Kalshi removed the action to the United States District Court for the Western District of Washington in Seattle. Three days after the state filing, Robinhood Markets, Inc. filed a preemptive federal action against the Washington Attorney General and Gambling Commission in the United States District Court for the Western District of Washington in Tacoma, seeking a declaratory judgment that federal law preempts state enforcement against its event-contract distribution partnership with Kalshi. The Washington action is materially significant for this rulemaking because the state’s complaint rests on the Washington statutory definition of gambling — “staking or risking something of value upon the outcome of a contest of chance or a future contingent event” — and because Kalshi’s federal defense depends, at the threshold, on what Rule 40.11 means by “gaming.”

F. April 2, 2026 — United States and CFTC v. Arizona, Illinois, and Connecticut

The Department of Justice and the Commission jointly filed United States and CFTC v. State of Arizona, et al., No. 2:26-cv-02246-MTL, on April 2, 2026, along with parallel actions against Illinois and Connecticut. The Arizona complaint seeks declaratory and injunctive relief under the Supremacy Clause, asserting express preemption under 7 U.S.C. § 2(a)(1)(A), field preemption, and obstacle preemption of state laws that would prohibit the listing, trading, or clearing of event contracts on CFTC-registered designated contract markets. Judge Michael T. Liburdi consolidated the federal action with the pending Kalshi preemption case, KalshiEX LLC v. Johnson, No. CV-26-01715-PHX-MTL, on the same day, with the consent of the Chief Judge and the assigned Magistrate Judge. The federal government’s preemption theory asserts the exclusivity of Commission jurisdiction over the same instruments whose Rule 40.11 treatment the Advance Notice now places before the public.

G. April 6, 2026 — KalshiEX LLC v. Flaherty

The Third Circuit issued a divided panel opinion on April 6, 2026 in KalshiEX LLC v. Flaherty, No. 25-1922, affirming a preliminary injunction that bars New Jersey from enforcing its gambling laws against Kalshi’s sports event contracts. The majority held that the contracts satisfy the CEA’s statutory definition of “swap” under 7 U.S.C. § 1a(47)(A)(ii), that the CEA grants the Commission exclusive jurisdiction over swaps traded on CFTC-licensed designated contract markets, and that both field preemption and conflict preemption shield the contracts from state regulation. The majority acknowledged Rule 40.11 and observed that the Commission “has codified this power in a regulation, 17 C.F.R. § 40.11, but it has not yet acted to review or prohibit any sports-related event contracts,” declining to reach the rule’s application. The dissent engaged Rule 40.11 directly, arguing that the Commission’s non-enforcement of its own regulation cannot preempt state law. The majority’s silence on Rule 40.11 is the doctrinal space Kaiserman now occupies.

H. The Resulting Posture

Each of these seven developments traces back to a single unresolved question: what is the scope of “gaming” in CEA section 5c(c)(5)(C) and Rule 40.11? The Commission is asserting preemption in three appellate circuits and two federal district courts while acknowledging, on the face of the Advance Notice, that the governing definition is open. Private plaintiffs now invoke the same undefined rule as the basis for federal damages claims that do not depend on any appellate outcome. State attorneys general are filing in their own courts rather than awaiting federal resolution, inverting the procedural leverage that had previously favored the platforms. The current regulatory posture creates a multi-forum strategic equilibrium in which each actor — the Commission, registered entities, state attorneys general, and private plaintiffs — rationally exploits the absence of a Rule 40.11 definition, producing simultaneous federal preemption assertions, state enforcement actions, and private damages claims in parallel rather than in sequence. Completing the Rule 40.11 definitional rulemaking is the single action capable of stabilizing the Commission’s jurisdictional posture across all of these proceedings.

III. The Statutory and Regulatory Framework

A. CEA Section 5c(c)(5)(C) and the Five Enumerated Activities

CEA section 5c(c)(5)(C)(i), 7 U.S.C. § 7a-2(c)(5)(C)(i), authorizes the Commission to determine that an agreement, contract, transaction, or swap in an excluded commodity listed by a designated contract market or swap execution facility is contrary to the public interest if it involves: (I) activity unlawful under federal or state law; (II) terrorism; (III) assassination; (IV) war; (V) gaming; or (VI) other similar activity determined by the Commission by rule or regulation to be contrary to the public interest. CEA section 5c(c)(5)(C)(ii) provides that no contract determined to be contrary to the public interest under clause (i) may be listed or made available for trading or clearing on a registered entity. The statute supplies the enumerated categories; it delegates to the Commission the authority to define their scope.

B. Rule 40.11 and the Self-Certification Pathway

The Commission adopted 17 C.F.R. § 40.11 in 2011 to implement CEA section 5c(c)(5)(C). See Provisions Common to Registered Entities, 76 Fed. Reg. 44776 (July 27, 2011). Rule 40.11(a)(1) provides that a registered entity “shall not list for trading or accept for clearing” any agreement, contract, transaction, or swap based on an excluded commodity that involves, relates to, or references any of the activities enumerated in the statute, including gaming. The rule does not define “gaming.” Rule 40.2(a)(2), the parallel self-certification provision, permits a designated contract market to list a new derivative contract for trading by providing the Commission with a written certification at least one business day before listing, and the contract takes effect upon the next business day absent Commission action. Rule 40.3 preserves a voluntary prior-approval pathway that registered entities rarely invoke.

C. The Interaction Between Rule 40.11 and Rule 40.2

Rule 40.2(a)(2) permits passive approval through non-disapproval. Rule 40.11 imposes an affirmative prohibition. The statutory structure assumes that a registered entity will decline to self-certify a contract that Rule 40.11 prohibits, and that the Commission will act to review and prohibit any contract that crosses the line. When the Commission has not defined the line — and when a registered entity reads the line one way and a federal court is being asked to read it another way — the self-certification pathway operates without the affirmative review the underlying statute contemplates. The structural point at which the current posture breaks down is precisely that one.

D. The 2012 Further Definition Line

In the 2012 joint further-definition rulemaking, the Commission and the Securities and Exchange Commission distinguished swaps and security-based swaps from “customary consumer and commercial agreements, contracts, or transactions” that are not intended to fall within the swap definition. See Further Definition of “Swap,” “Security-Based Swap,” and “Security-Based Swap Agreement”; Mixed Swaps; Security-Based Swap Agreement Recordkeeping, 77 Fed. Reg. 48208, 48246 (Aug. 13, 2012). The distinction recognizes that a contract can satisfy the literal statutory swap definition while lacking the economic characteristics — price discovery, hedging utility, financial-market risk transfer — that justify treatment as a derivative. The 2012 rulemaking drew that line at the threshold of swap classification. The Commission now faces an analogous question at the threshold of the public interest determination: can a contract that satisfies the swap definition nonetheless involve an activity — gaming — that places it outside the federal derivatives regulatory perimeter? The answer is yes. Rule 40.11 exists precisely to draw that line. The 2012 analytical framework supplies the structure for doing so.

IV. Why the Current Posture Cannot Hold

Four independent administrative-law principles, together with one associated private-enforcement consequence, indicate that the Commission cannot maintain the current posture — amicus filings asserting exclusive jurisdiction and preemption of state law on one track, and an open Advance Notice asking the public to define the governing regulatory term on another — without creating a deference vulnerability that will compound across every proceeding in which the Commission appears. Completing the Rule 40.11 rulemaking resolves all four administrative-law problems and closes the private-enforcement exposure prospectively.

A. State Farm and the Reasoned Decision-Making Standard

Motor Vehicle Manufacturers Association v. State Farm Mutual Automobile Insurance Co., 463 U.S. 29 (1983), requires an agency to examine the relevant data and articulate a satisfactory explanation for its action, including a rational connection between the facts found and the choice made. Id. at 43. An agency that asserts a final jurisdictional answer in federal litigation while its own rulemaking docket invites public input on the definition of the governing term has not supplied the rational connection the standard requires. The Commission’s amicus position in the Ninth Circuit and its complaint in the District of Arizona depend on the premise that the scope of “gaming” under Rule 40.11 is settled enough to support preemption. The Advance Notice affirmatively acknowledges that the scope is not settled. Both things cannot be true simultaneously. Completing the rulemaking resolves the inconsistency; leaving it open does not.

B. Chenery and the Contemporaneous-Record Requirement

SEC v. Chenery Corp., 318 U.S. 80 (1943), confines judicial review of agency action to the grounds the agency invoked at the time it acted. Id. at 87. A reviewing court evaluates the coherence of the agency’s reasoning as of the date of the action, not the aspirational authority of a later-completed docket. The Commission’s amicus brief was filed on February 17, 2026. The Advance Notice was published on March 12, 2026 — twenty-three days later — and expressly solicits public input on the scope of the regulatory term on which the amicus brief’s preemption theory depends. Under Chenery, a reviewing court asked to evaluate the amicus position looks to the record available on February 17. The available record includes the withdrawn 2024 proposed rules and the unamended Rule 40.11. Completing the rulemaking supplies the contemporaneous record Chenery requires for any future Commission assertion of the same position.

C. Encino Motorcars and the Unexplained-Departure Problem

Encino Motorcars, LLC v. Navarro, 579 U.S. 211 (2016), held that an agency must provide a reasoned explanation when it departs from a prior position, and that unexplained inconsistency with past practice is arbitrary under State Farm. Id. at 221–22. The withdrawal of the 2024 proposed rules on February 6, 2026 was a departure from the prior Commission’s position that sports and political event contracts should be identified by rule as contrary to the public interest under CEA section 5c(c)(5)(C). The withdrawal notice offered a single sentence of explanation pointing to pending state litigation. 91 Fed. Reg. at 5386. The explanation does not address the merits of the prior proposal’s public-interest analysis; it addresses the posture of the litigation surrounding it. Encino Motorcars requires more. Completing the Rule 40.11 rulemaking supplies the reasoned explanation the departure standard requires.

D. Loper Bright and the Elimination of Chevron Deference

Loper Bright Enterprises v. Raimondo, 603 U.S. 369 (2024), held that courts must exercise independent judgment when interpreting ambiguous statutes and may no longer defer to an agency’s reasonable interpretation under Chevron U.S.A. Inc. v. Natural Resources Defense Council, Inc., 467 U.S. 837 (1984). The consequence for the current posture is direct. The Commission’s amicus position in the Ninth Circuit asks the panel to accept the Commission’s interpretation of “swap” under 7 U.S.C. § 1a(47)(A)(ii) and, by extension, the Commission’s implicit interpretation of the scope of “gaming” under CEA section 5c(c)(5)(C). Under Loper Bright, the panel owes no deference to either interpretation. The panel decides both questions independently. The Commission’s best available posture, after Loper Bright, is to supply a completed rulemaking record that reflects reasoned agency judgment on the statutory question — not to rely on deference that is no longer available. Completing the Rule 40.11 rulemaking is the institutional action that converts the Commission’s litigation position from a deference claim the doctrine no longer supports into a reasoned rulemaking record courts will credit on its merits.

E. The Private Enforcement Track the Current Posture Leaves Open

The four administrative-law problems above concern the Commission’s appellate posture. The fifth problem concerns private litigation the Commission cannot preempt. CEA section 22 provides a private right of action — codified at 7 U.S.C. § 25(b) — against registered entities and their officers for failing to enforce, or improperly enforcing, the rules and statutory obligations the CEA requires. The Kaiserman complaint invokes that private right of action to seek damages for alleged violations of Rule 40.11. The Third Circuit’s preemption ruling does not reach private federal claims; it preempts state gambling enforcement. A ruling by the Ninth Circuit that preempts state law, however robust, likewise does not reach section 25(b). Damages accrue in federal district court under an unamended federal rule whose governing definition the Advance Notice acknowledges is open. Every day the Rule 40.11 definition remains open, the damages exposure under section 25(b) compounds. Completing the rulemaking is the only Commission action that can close that exposure prospectively and supply the defendants with a rule against which compliance can be measured.

V. Proposed Rulemaking Structure

The Commission should convert the Advance Notice to a Notice of Proposed Rulemaking focused on CEA section 5c(c)(5)(C) and Rule 40.11. The proposed rulemaking should comprise four coordinated elements. Each element is drafted to be legally self-sufficient; together, the four resolve the deference problem identified in Part IV, close the private-enforcement gap identified in Part IV.E, and preserve the federal preemption architecture the Commission and the Department of Justice are defending.

A. A Textual Definition of “Gaming” in Rule 40.11

Rule 40.11 should be amended to add a definition of “gaming” that provides objective criteria the Commission, registered entities, courts, and private litigants can apply. The proposed definition reads:

“Gaming, for purposes of CEA section 5c(c)(5)(C) and this section, means any activity in which the outcome of a contest, game, match, competition, or similar occurrence is treated as the subject of, or the referent for, a payoff to a participant or counterparty, where (1) the contest, game, match, or competition is conducted primarily for entertainment, amusement, or sport; and (2) the outcome lacks a demonstrable, non-incidental connection to the production, distribution, consumption, or hedging of an economic or commercial good, service, interest, or risk. A contract that satisfies both elements is a contract that ‘involves, relates to, or references gaming’ within the meaning of paragraph (a)(1) of this section, regardless of whether the contract otherwise satisfies the statutory definition of ‘swap’ or ‘contract of sale of a commodity for future delivery.’”

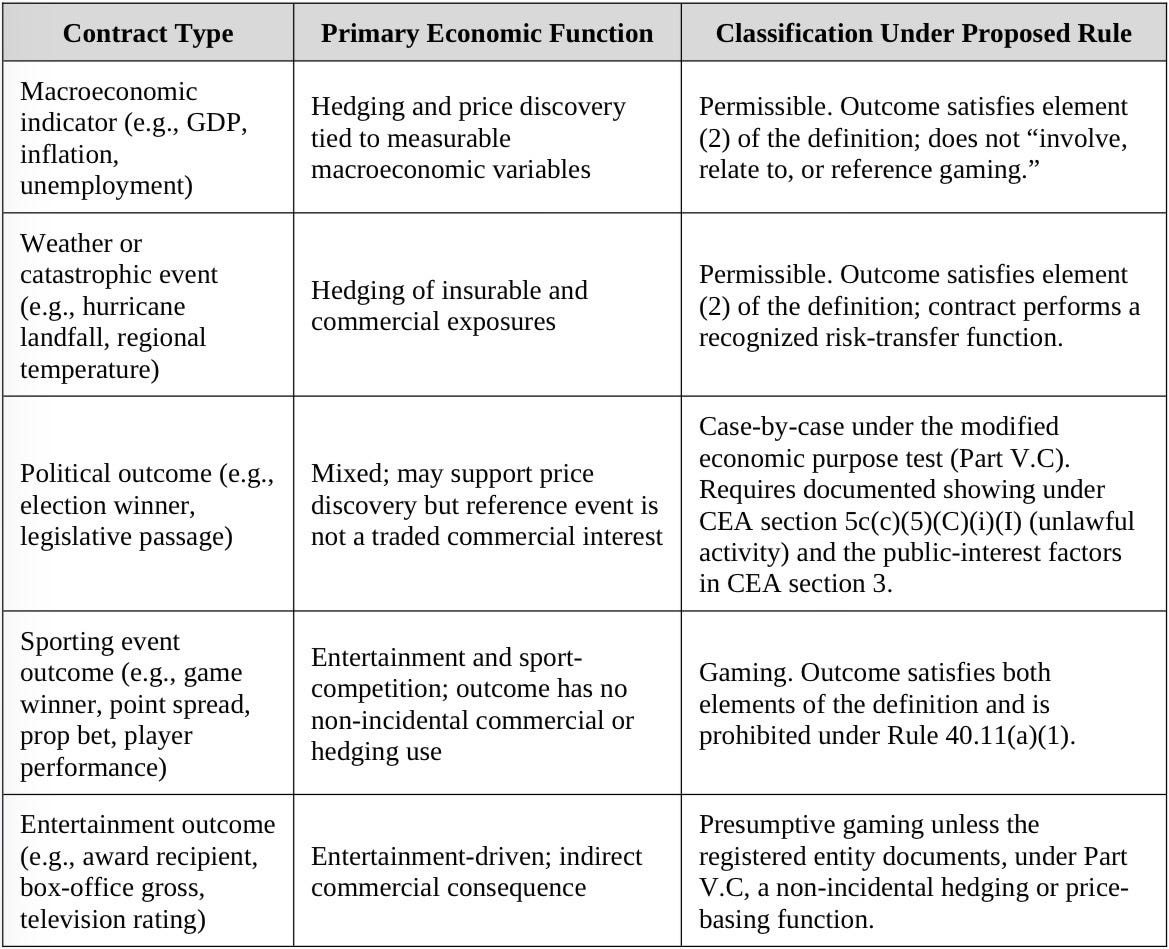

The definition answers the six subparts of Question 19 directly. Subpart 19.a asks what sources should inform the scope of the term. The proposed definition draws on the 2012 joint further-definition rulemaking’s economic-consequence analysis, the CEA’s own public-interest purposes in section 3, and the plain meaning of “gaming” as reflected in federal and state gambling statutes. Subpart 19.b asks how the Commission should distinguish among types of contests. The two-element structure does the work: the first element captures the entertainment or sport-competition character of the contest; the second element excludes contests whose outcomes carry genuine economic or commercial consequence. Subpart 19.c asks about manipulation, abusive sales practices, and responsible innovation; the definition’s second element channels the public interest inquiry to the structural economic function the CEA exists to protect. Subparts 19.d through 19.f — participant characteristics, responsible gaming standards, and differences among contract types — inform the application of the definition to specific products but do not require the Commission to resolve those questions before completing the definition itself. The definition supplies an administrable standard that the Commission, registered entities, and courts can apply consistently across contract types and across forums.

B. Application of the Proposed Definition

The following table illustrates how the proposed definition applies across representative event-contract categories. The illustrations are not exhaustive and are not a substitute for contract-level analysis under the modified economic purpose test proposed in Part V.C below; they show that the definition produces administrable distinctions at the level of regulatory application.

C. A Modified Economic Purpose Test as a Public Interest Screen

Question 9 of the Advance Notice asks whether any elements of the pre-2000 economic purpose test should inform the Commission’s public interest determination under CEA section 5c(c)(5)(C). The answer is yes, but in a modified form calibrated to the specific structure of event contracts. The Commission should adopt a rule requiring that a designated contract market seeking to list an event contract that references or potentially involves any of the activities enumerated in CEA section 5c(c)(5)(C) include, as part of its self-certification or prior-approval submission, a written explanation of:

(1) The reasonable expectation that the contract will be used for hedging or price-basing purposes on more than an occasional basis, supported by identification of the commercial or financial interests whose risk the contract is designed to transfer;

(2) The economic or commercial consequences with which the reference event is associated, and the mechanism by which the contract’s payoff structure transmits information about those consequences to market participants;

(3) The extent to which the contract’s function in price discovery, risk management, or hedging is non-incidental to any entertainment, amusement, or sport-outcome characteristics of the reference event; and

(4) The registered entity’s analysis of whether the contract “involves, relates to, or references” any activity enumerated in CEA section 5c(c)(5)(C), including gaming, under the definition proposed in Part V.A above.

The screen does not categorically prohibit any contract. The screen requires that the registered entity supply the economic analysis the Commission needs to make the public interest determination that CEA section 5c(c)(5)(C) contemplates. The structure operates as a functional filter: markets that aggregate economically relevant information and transfer commercial or financial risk satisfy the screen, while markets whose demand derives primarily from participant behavioral motivations — entertainment utility, sport-outcome engagement, and consumption-driven risk-seeking rather than hedging — do not. The analysis distinguishes contracts that aggregate economically relevant information from contracts whose demand is primarily driven by entertainment utility and well-documented behavioral biases, including overconfidence, loss-chasing, and preference for outcome-based wagering rather than risk transfer. The resulting distinction is not an ad hoc classification choice; the distinction reflects a predictable behavioral response to contract design, one that courts, regulators, and registered entities can apply with consistency because the inputs — contract structure, demand patterns, participant use — are observable on the record of any submission. The screen also creates a documentary record against which Rule 40.11 compliance can be evaluated, both by the Commission and by any court reviewing either Commission enforcement or a private action under 7 U.S.C. § 25(b).

D. Affirmative Approval Under Rule 40.3 for Enumerated-Activity Contracts

Rule 40.2(a)(2) should be amended to provide that passive non-disapproval through self-certification is unavailable for event contracts that reference or potentially involve any of the five activities enumerated in CEA section 5c(c)(5)(C). Registered entities seeking to list such contracts should be required to proceed under Rule 40.3, which provides for affirmative Commission approval and preserves the ninety-day review period specified in CEA section 5c(c)(5)(C)(iv). The amendment carries three benefits. First, it aligns the procedural pathway with the substantive character of the contracts at issue: contracts that may be contrary to the public interest under a statutory enumeration should receive affirmative agency attention, not passive approval. Second, it converts the Commission’s current reactive posture into a structured review process that generates the contemporaneous record Chenery and State Farm require. Third, it supplies registered entities with a predictable procedural framework that eliminates the current ambiguity about when a self-certified contract may be deemed to have received Commission approval.

E. An Express Non-Displacement Clause

Rule 40.11 should be amended to include an express clause clarifying that the rule’s prohibition operates independently of state-law gambling classifications. The proposed clause reads:

“The prohibition in paragraph (a)(1) of this section operates as an independent federal prohibition applicable to registered entities and is not contingent upon, and is not preempted or displaced by, any classification of the underlying activity as lawful or unlawful under the law of any State. Compliance with this section is required of every registered entity regardless of the status of the underlying activity under State law.”

The clause performs three functions simultaneously. First, it preserves the federal preemption architecture the Commission and the Department of Justice are defending, because it confirms that the federal regulatory regime — of which Rule 40.11 is part — occupies the field of event-contract regulation on designated contract markets. Second, it forecloses the argument raised in the Third Circuit dissent that the Commission’s non-enforcement of Rule 40.11 signals that federal law is indifferent to gaming-referenced contracts, by making clear that the rule’s prohibition is affirmative and operates regardless of state-law developments. Third, it closes the private-enforcement gap under 7 U.S.C. § 25(b) prospectively, because it supplies registered entities with a clear federal rule against which compliance can be measured and provides reviewing courts with a completed rulemaking record that satisfies Loper Bright independent statutory analysis.

VI. How the Proposed Rulemaking Resolves the Current Litigation Conflict

The proposed rulemaking is not a retreat from the federal preemption position. The proposed rulemaking is the administrative-law predicate the preemption position requires. Four consequences follow.

First, the rulemaking preserves federal exclusive jurisdiction. The Commission and the Department of Justice have asserted, in the District of Arizona and in three appellate circuits, that the CEA occupies the field of event-contract regulation on designated contract markets. A completed rulemaking under CEA section 5c(c)(5)(C) strengthens that assertion by demonstrating that the Commission is exercising the regulatory authority the statute grants it. Field preemption is most defensible when the federal agency occupying the field is actively regulating it. The current posture — amicus filings paired with an open rulemaking docket — is the weakest available configuration. Completing the rulemaking is the strongest.

Second, the rulemaking closes the private enforcement gap under 7 U.S.C. § 25(b) prospectively. The Kaiserman complaint and any follow-on actions depend on the proposition that Rule 40.11 prohibits conduct that registered entities engaged in without Commission correction. A completed rulemaking that defines “gaming,” adopts a modified economic purpose screen, and requires affirmative approval under Rule 40.3 for enumerated-activity contracts supplies registered entities with a rule against which compliance can be measured on a forward-going basis. The rulemaking does not resolve the retrospective liability question the Kaiserman complaint raises — no rulemaking can — but it closes the forward-going exposure that will otherwise compound for every month the Rule 40.11 definition remains open.

Third, the rulemaking supplies the Ninth Circuit, the Fourth Circuit, and any reviewing Supreme Court with the reasoned deliberative record Loper Bright, Chenery, and State Farm require. A panel exercising independent judgment on the scope of “gaming” under CEA section 5c(c)(5)(C) will read a completed rulemaking record as the Commission’s best statement of its reasoned agency judgment on the statutory question. The same panel, faced with an open Advance Notice and an amicus brief, will read the two as incompatible — and will resolve that incompatibility against the agency, because Loper Bright removes the deference that would otherwise have shielded the inconsistency.

Fourth, the rulemaking provides the reasoned explanation Encino Motorcars requires for the February 6, 2026 withdrawal of the prior proposed rules. A Notice of Proposed Rulemaking that addresses the Rule 40.11 definitional question, the economic purpose screen, and the Rule 40.2 procedural pathway is, on its face, the completed replacement for the withdrawn proposal. The withdrawal notice’s reference to pending state litigation as the reason for reconsideration becomes retrospective justification for the Commission’s decision to replace an incomplete proposal with a more precisely targeted one — rather than a standalone explanation that Encino Motorcars would find insufficient.

The Forward Consequence of Non-Action

The converse of the preceding analysis is equally structural. If the Commission does not complete this rulemaking, three consequences follow, each of which the record of the past sixty days has already begun to demonstrate. Private liability under 7 U.S.C. § 25(b) will expand as additional plaintiffs’ firms replicate the Kaiserman pleading template in other federal districts, and damages will accrue under an unamended rule the Commission acknowledges lacks a completed definition. State enforcement actions will proliferate, as the Washington, Arizona, Nevada, Massachusetts, Ohio, and Maryland filings have already shown, with state attorneys general increasingly filing in their own courts rather than awaiting federal resolution. Courts — not the Commission — will define “gaming” under CEA section 5c(c)(5)(C) and Rule 40.11, either through the Ninth Circuit, Fourth Circuit, and Supreme Court preemption dockets or through the Kaiserman and follow-on private dockets. Each of those courts will decide the question de novo under Loper Bright, without the deference the Commission has historically relied on and without the completed rulemaking record that is the agency’s only remaining source of institutional authority on the question. The administrative-law framework the Commission invokes in its amicus filings assumes that the agency is the primary interpreter of its own enabling statute. The assumption is sustainable only if the agency acts.

VII. The Ninth Circuit Decision Space and the Structural Consequences That Follow

The analysis in this comment does not assume a particular outcome in the consolidated Ninth Circuit appeal or in any other pending matter; it identifies the structural consequences that follow from each legally available path. The United States Court of Appeals for the Third Circuit has articulated one view of Commission authority over event contracts under the Commodity Exchange Act. The forthcoming ruling from the United States Court of Appeals for the Ninth Circuit will operate within a constrained legal space defined by the statutory interpretation of “swap” under 7 U.S.C. § 1a(47)(A)(ii), the scope of Commission exclusive jurisdiction under 7 U.S.C. § 2(a)(1)(A), the preemption framework the Commission and the Department of Justice have asserted in United States and CFTC v. Arizona, and the unresolved definitional status of “gaming” under 17 C.F.R. § 40.11. Each of those boundaries is a fixed feature of the record; their combined effect defines the space within which any ruling must fall.

Two structural paths exhaust that space. Any ruling must either (1) reinforce federal exclusivity under the Commodity Exchange Act and the Commission’s preemption theory, or (2) impose limiting principles that permit overlapping state enforcement, private federal enforcement under 7 U.S.C. § 25(b), or both. The two paths are not predictions; they are the only legally available outcomes given the statutory and regulatory record before the panel. Each path carries distinct structural consequences for the Commission, for registered entities, for state regulators, and for private plaintiffs. Each path also produces a different record for any subsequent petition for a writ of certiorari to the Supreme Court of the United States. The Commission can prepare for both paths through a single administrative action: completing the Rule 40.11 rulemaking.

A. The Reinforcement Path

A ruling that reinforces federal exclusivity does not close the definitional question this comment addresses. A ruling of that character affirms the Commission’s jurisdictional authority over event contracts on designated contract markets without resolving what “gaming” means under CEA section 5c(c)(5)(C) and Rule 40.11. The Third Circuit majority in KalshiEX LLC v. Flaherty reached exactly that configuration: preemption of state gambling enforcement affirmed, Rule 40.11’s scope left undecided. Under the reinforcement path, the private right of action under 7 U.S.C. § 25(b) operates as the residual enforcement mechanism, because preemption of state law does not reach federal damages claims against registered entities. The Kaiserman complaint occupies that residual space now. Follow-on filings in other federal districts occupy it on a forward-going basis. Every day the Commission does not define the scope of the rule the private plaintiffs are suing under, the residual enforcement pathway expands. Completing the Rule 40.11 rulemaking closes the residual pathway prospectively by supplying registered entities with a definitional standard against which compliance can be measured.

B. The Limiting-Principles Path

A ruling that imposes limiting principles — on the scope of the swap definition, on the reach of field preemption, or on the self-certification mechanism under 17 C.F.R. § 40.2(a)(2) — preserves or expands the authority of state regulators, private plaintiffs, or both to enforce independently. Under the limiting-principles path, state attorneys general operating in their own courts become primary interpreters of the line between federally regulated event contracts and state-regulated gambling. Private plaintiffs operating under 7 U.S.C. § 25(b) continue to press the Rule 40.11 theory now before the Northern District of Georgia. Courts in both forums will be required to define “gaming” under Rule 40.11 on their own initiative, because Rule 40.11 imposes an affirmative prohibition that registered entities may violate, 7 U.S.C. § 25(b) supplies a private right of action for such violations, and under Loper Bright Enterprises v. Raimondo no deference is available to fill the definitional gap. The Commission’s institutional authority over the definition of its own regulatory term transfers by default to the judiciary. Completing the Rule 40.11 rulemaking preserves the Commission’s primacy on the definitional question regardless of how the preemption question resolves.

C. The Certiorari Posture

Any divergence between the Third Circuit’s reasoning in Flaherty and the Ninth Circuit’s reasoning in the consolidated appeal will produce a record that state attorneys general, affected tribal governments, registered entities, and the Solicitor General will evaluate for certiorari purposes. The same is true of any divergence between either of those circuits and the Fourth Circuit, which is scheduled to hear argument in a parallel matter, or the Sixth Circuit, which faces an intra-circuit conflict on the underlying statutory question. The Commission’s institutional position in any such petition is materially stronger if the agency can point to a completed Rule 40.11 rulemaking record than if the agency must rely on an amicus brief filed during a period when its own rulemaking docket was open. A completed rulemaking supplies the reasoned deliberative record that Motor Vehicle Manufacturers Association v. State Farm Mutual Automobile Insurance Co. and SEC v. Chenery Corp. require; it supplies the reasoned explanation for departure that Encino Motorcars, LLC v. Navarro requires; and it supplies the institutional predicate that preserves the Commission’s interpretive position under Loper Bright. An open Advance Notice paired with an amicus brief supplies none of those records.

D. What the Commission Cannot Outrun

The circuit courts, the Supreme Court, state attorneys general, and private plaintiffs will continue to act on the record as it stands. The Commission cannot control the timing of those actions. The Commission can, however, control whether the record those actors are acting upon includes a completed Rule 40.11 rulemaking or does not. The single variable within the Commission’s control determines whether the Commission enters the post-ruling environment — under either structural path — as the primary interpreter of its own regulatory term or as an agency whose definitional authority has already transferred to the courts by default. The Advance Notice comment period closes April 30, 2026. The Ninth Circuit oral argument was heard April 16, 2026. The window in which the Commission can still act before the appellate record closes is narrow and is narrowing.

Absent a completed definition, the regulatory system governing event contracts does not converge to a stable equilibrium. The system produces parallel and conflicting enforcement across federal, state, and private actors, with the courts forced to supply the definition in the Commission’s place. Completing the Rule 40.11 rulemaking is not only the institutional action that preserves the Commission’s authority; completing the rulemaking is the action that allows the regulatory system itself to resolve, rather than to continue producing the multi-forum conflict the current posture has already generated.

VIII. Specific Rulemaking Requests

Based on the foregoing, MindCast AI LLC respectfully requests that the Commission take the following actions:

1. Convert the Advance Notice of Proposed Rulemaking to a Notice of Proposed Rulemaking focused on CEA section 5c(c)(5)(C) and 17 C.F.R. § 40.11 within ninety days of the close of the comment period on April 30, 2026;

2. Amend 17 C.F.R. § 40.11 to include the textual definition of “gaming” proposed in Part V.A above, or a materially equivalent definition that distinguishes contest-referenced contracts lacking demonstrable economic function from contracts whose reference events are associated with measurable economic or commercial consequence;

3. Amend 17 C.F.R. § 40.2(a)(2) to provide that passive non-disapproval through self-certification is unavailable for event contracts that reference or potentially involve any of the five activities enumerated in CEA section 5c(c)(5)(C), and require registered entities to proceed under 17 C.F.R. § 40.3 for such contracts;

4. Adopt the modified economic purpose test proposed in Part V.C above as a written component of every Rule 40.3 submission for event contracts referencing or potentially involving any of the enumerated activities; and

5. Amend 17 C.F.R. § 40.11 to include the express non-displacement clause proposed in Part V.E above.

Commission staff may contact the undersigned for any clarification concerning this comment. MindCast AI LLC welcomes the opportunity to supply additional analysis at the Commission’s request.

APPENDIX: LITIGATION POSTURE ADDENDUM

Live Proceedings Implicating the Rule 40.11 Definitional Gap

The administrative-law argument above is not hypothetical. The definitional gap identified in this comment is currently being adjudicated in parallel federal and state proceedings. The Commission’s completion of the Rule 40.11 rulemaking would materially affect the record available to every court in the following matters.

A. Active Federal Proceedings

North American Derivatives Exchange, Inc. v. State of Nevada, No. 25-7187 (9th Cir.) — Consolidated appeal on preemption of state gambling enforcement; Commission participating as amicus asserting exclusive federal jurisdiction. Oral argument held April 16, 2026.

KalshiEX LLC v. Flaherty, No. 25-1922 (3d Cir.) — Divided panel opinion issued April 6, 2026; majority declined to decide scope of Rule 40.11; dissent engaged the rule directly.

United States and CFTC v. State of Arizona, et al., No. 2:26-cv-02246-MTL (D. Ariz.) — DOJ-CFTC Supremacy Clause action filed April 2, 2026; consolidated same day with KalshiEX LLC v. Johnson, No. CV-26-01715-PHX-MTL. Parallel federal actions filed against Illinois and Connecticut.

Kaiserman v. Kalshi Inc., et al., No. 1:26-cv-01525-VMC (N.D. Ga.) — Putative class action filed March 20, 2026 under 7 U.S.C. § 25(b), alleging direct violations of Rule 40.11 by registered entities and named executive officers.

B. Active State and Removed Proceedings

Washington v. KalshiEX LLC — Civil action filed by Washington Attorney General Nick Brown in King County Superior Court on March 27, 2026, alleging violations of the Washington Gambling Act, Consumer Protection Act, and Recovery of Money Lost at Gambling Act. Removed to the United States District Court for the Western District of Washington in Seattle.

Robinhood Markets, Inc. v. Washington State Gambling Commission, et al. (W.D. Wash., Tacoma)— Preemptive federal declaratory-judgment action filed March 30, 2026 by a CFTC-registered Futures Commission Merchant that routes event contracts through Kalshi, seeking a ruling that federal law preempts state enforcement against the distribution partnership.

Arizona v. KalshiEX LLC, No. CR 2026-173-001 — Criminal Information filed by Arizona Attorney General on March 16, 2026, charging twenty counts including election-wagering counts, based on individual bets as small as one dollar.

Additional state enforcement actions — Active proceedings in Nevada, Massachusetts, Ohio, Maryland, and New Jersey. Coordinated amicus coalition of more than thirty state attorneys general filed in support of state enforcement authority in the Ninth Circuit and Third Circuit appeals.

C. Cross-Proceeding Significance

Each of the proceedings above will address, directly or indirectly, the scope of “gaming” under CEA section 5c(c)(5)(C) and Rule 40.11. The definitional gap identified in this comment is now being adjudicated in parallel federal and state proceedings. The Commission retains the institutional authority to resolve that gap through the rulemaking process this Advance Notice initiated. Every day the Commission declines to complete the rulemaking, that authority transfers by default to courts operating under Loper Bright independent judgment and to private plaintiffs operating under 7 U.S.C. § 25(b). The choice the Commission faces is not whether the gap will be filled; the choice is whether the Commission or the judiciary fills it.

MindCast AI LLC is a predictive behavioral economics and game theory artificial intelligence firm specializing in complex litigation, geopolitical risk intelligence, and innovation ecosystems. MindCast publishes falsifiable institutional foresight analysis at mindcast-ai.com. The firm’s prediction-markets analytical corpus includes a detailed examination of the interaction between 17 C.F.R. § 40.11, Commission litigation posture, and the private right of action under 7 U.S.C. § 25(b). See

MCAI Lex Vision: The Rule 40.11 Paradox — Kalshi, the Third Circuit, and the Class Action the Ninth Circuit Cannot Ignore

On April 6, 2026, the Third Circuit affirmed a preliminary injunction barring New Jersey from enforcing its gambling laws against Kalshi’s sports event contracts. The majority held that Kalshi’s contracts are “swaps” under the Commodity Exchange Act, that the CEA grants the CFTC exclusive jurisdiction over trades on designated contract markets, and that…