MCAI Lex Vision: The Routing Layer Is the Antitrust Trigger

CPI Antitrust Chronicle, April 2026, publishes the MindCast structural argument — and it reframes where AI infrastructure enforcement should originate.

Hyperscaler dedicated generation agreements, transformer supply concentration, interconnection queue preemption, and cooling architecture commitments now foreclose mid-tier developers from AI infrastructure markets — before any application-layer dominance becomes measurable. Antitrust analysis built around monopoly thresholds misses the conduct entirely.

The April 2026 Competition Policy International (CPI) Antitrust Chronicle publishes a MindCast argument that names the operative trigger: routing control at the compute-energy stack, not downstream monopoly.

The MindCast article, “Infrastructure Routing Control: The Operative Antitrust Trigger in AI Energy Markets,” runs alongside Gibson Dunn’s analysis of the DOJ Antitrust Division’s electricity and digital infrastructure focus, Charles Whiddington and Domniki Mari on AI data centers and the energy challenge, and Benjamin Huffman, Ann O’Brien, and Josh Sturtevant on antitrust guardrails for energy infrastructure collaborations.

Read it at CPI: Infrastructure Routing Control: The Operative Antitrust Trigger in AI Energy Markets

The post below explains how the CPI argument extends the MindCast structural method across industry verticals and what it predicts about the next AI infrastructure enforcement action. CPI carries the full analysis — citations, doctrine, enforcement architecture.

The Thesis in Brief

Monopoly-threshold doctrine fits industries where competitive harm crystallizes at the application layer, late in the buildout cycle, after dominance becomes measurable. AI infrastructure does not behave that way.

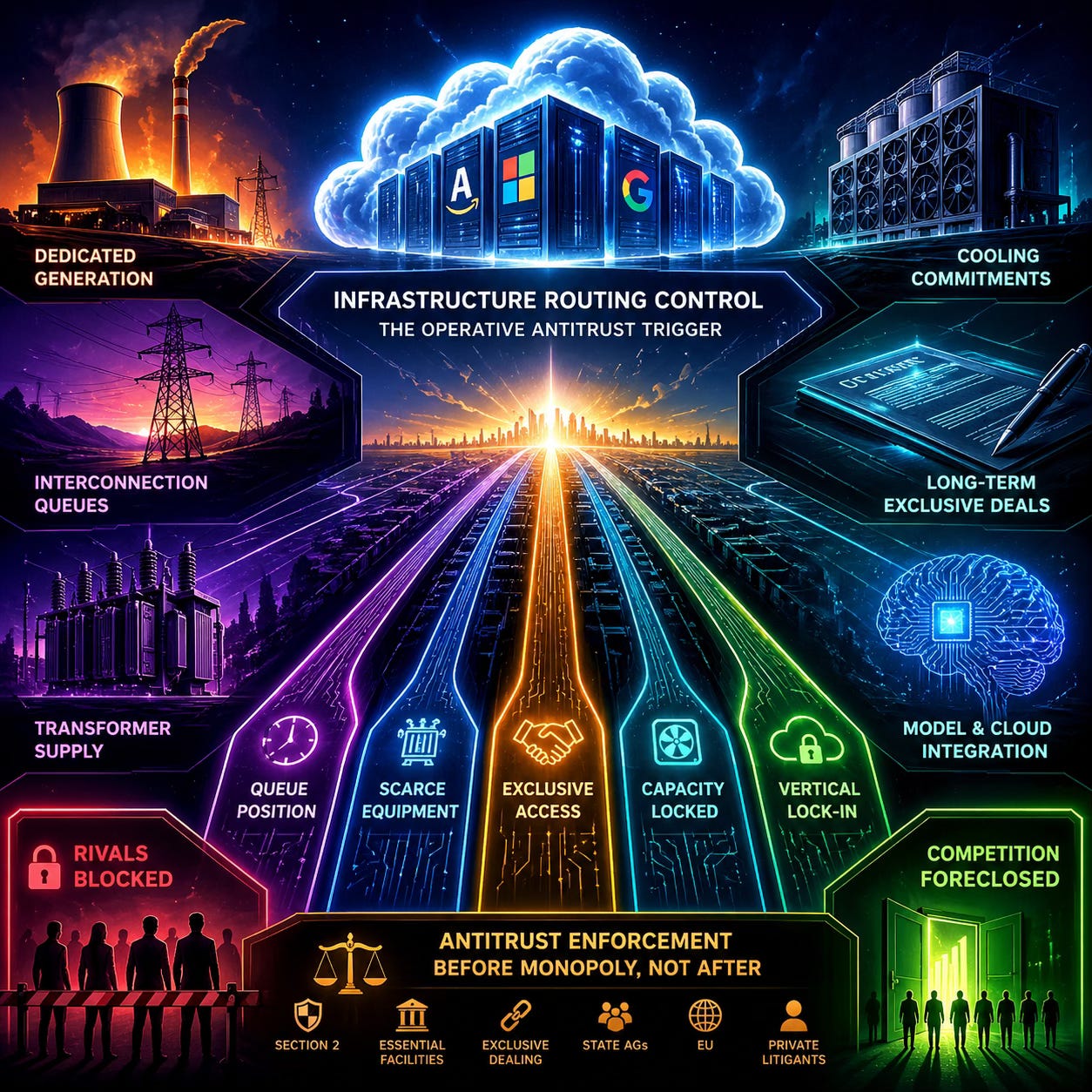

Foreclosure operates upstream of the application layer. Foreclosure happens at the routing layers of the compute-energy stack — the points where mid-tier developers must traverse infrastructure controlled by hyperscalers to participate in AI deployment at all. Queue position in public interconnection grids. Dedicated generation agreements. Transformer supply. Cooling architecture commitments. None of these qualify as downstream product markets. Each functions as a physical and contractual precondition through which any AI product reaches market.

Control of those layers forecloses competition before market share in AI applications becomes measurable.

The CPI article argues for a single doctrinal correction: enforcement should calibrate to routing control, not to monopoly threshold. Railroads, electric utilities, and telecommunications support the move directly. Regulators in each prior infrastructure cycle eventually intervened at the routing layer — but only after delay made structural remedies more disruptive than earlier action would have required.

AI infrastructure is traversing the same sequence now.

Why the CPI Argument Matters for the MindCast Corpus

Readers following the MindCast publication arc will recognize the structural method. The same analytical frame mapped Compass v. NWMLS as a narrative control architecture, traced the Kalshi prediction markets litigation web through the Rule 40.11 definitional gap, and read the Vail/Alterra dynamic as a Signal Suppression Equilibrium. The frame applies to AI infrastructure with no modification.

The recurring move stays constant: identify the routing layer, identify the conduct that captures it, identify the field geometry that results, and predict where enforcement will arrive once the Becker phase of tolerated rational accumulation closes.

The industry vertical changes across publications. The geometry does not.

The CPI article extends the frame to one of the largest infrastructure buildouts in modern economic history — and arrives at a moment when the European Commission has formally activated proceedings on AI stack control, when state attorneys general have already demonstrated willingness to pursue structural remedies independent of federal enforcement posture, and when the mid-tier developer class that will eventually constitute the complainant pool takes shape in real time.

Three Structural Moves Worth Highlighting

The article develops several arguments at length. Three deserve attention here for readers tracking the analytical method.

First, the efficiency defense fails structurally. The standard Chicago School response to infrastructure concentration claims holds that vertical integration and long-term contracting produce efficiency gains that benefit consumers. The defense carries weight in most infrastructure markets. In AI infrastructure, the gains from dedicated generation agreements accrue exclusively to the contracting hyperscaler and its downstream customers — while queue congestion, capacity reduction, and higher effective interconnection costs fall onto the mid-tier developer class. Locally efficient. Field-negative. The efficiency framing does not close the antitrust inquiry; it reframes the inquiry as a quantification question.

Second, the buyer-side monopsony theory compounds the seller-side foreclosure analysis. Hyperscalers dominate not only the deployment of AI infrastructure but also the purchasing of the inputs that infrastructure requires — large power transformers, dedicated generation capacity, advanced cooling equipment. When three buyers control enough purchasing volume to set effective market terms, supplier investment incentives align to hyperscaler demand rather than to total addressable market demand. The transformer supply bottleneck stops functioning as a shared constraint and becomes a buyer-induced entry barrier. The shift produces a materially stronger theory of harm.

Third, distributed enforcement architecture changes the timeline. Federal settlement no longer guarantees closure. The Live Nation litigation demonstrated the pattern: federal regulators negotiated settlement terms while a coalition of state attorneys general continued pursuing independent structural claims. The enforcement field now includes federal agencies, state AGs, congressional investigations, federal and state courts, private litigants, and — since March 2026 — the European Commission. Each node responds to local incentives. No single actor controls the sequence. Firms designing antitrust governance strategy around the assumption of sustained federal enforcement restraint are missing where the action will actually originate.

What the CPI Placement Means

The article carries the MindCast structural method into peer-reviewed antitrust scholarship at the moment its doctrinal questions become operative.

The Trinko preemption question — whether FERC Order 2023’s interconnection reforms displace antitrust liability — sits as the threshold legal issue any first significant enforcement action in this space will need to resolve. Cross-jurisdictional propagation between EU findings and domestic state-level enforcement is not prospective; the dynamic is precedented and active. Mid-tier developers accumulating standing through documented queue exclusion now constitute the complainant base that state coalition actions require.

The article does not predict a specific enforcement date. It maps the structural conditions that make enforcement likely from at least one institutional node, identifies the doctrinal theories available to that node, and locates the conduct record that will define the evidentiary core when the action arrives.

The Forward Hook

If routing control persists at current trajectory, public interconnection access for sub-500 MW developers becomes structurally nonviable within two to three buildout cycles. The mechanism runs on arithmetic, not conspiracy: each hyperscaler dedicated generation agreement that exits the public queue removes capacity the queue cannot replace at the rate mid-tier developers require it. Once queue depth falls below the threshold at which mid-tier developers can reliably project interconnection timelines, the entry decision becomes irrational independent of capital availability. Consolidation follows from the aggregate structural effect of parallel rational conduct — not from any single firm’s market share.

The prediction is falsifiable, not commentary. PJM and MISO interconnection withdrawal data already document the structural conditions. Regulatory intervention, grid expansion, and technological substitution will determine the timeline — but the conduct already on record discloses the structural direction.

Foresight built on routing geometry produces predictions of this kind. Market-share extrapolation does not.

Who Should Read This

State attorneys general and their antitrust divisions. The Live Nation template — federal settlement followed by independent state structural claims — applies directly here. PJM and MISO data document mid-tier developer queue exclusion. The complainant class takes shape now. State coalition formation, not federal agency initiation, sits as the enforcement path of least resistance.

Mid-tier AI infrastructure developers and their counsel. CoreWeave, Applied Digital, Crusoe Energy, and the broader sub-500 MW developer class have standing arguments accumulating in real time. The conduct record — interconnection withdrawal data, hyperscaler procurement filings, earnings call disclosures — is largely public and growing. Documenting exclusion now matters more than waiting for a federal initiation that may not arrive on the relevant competitive timeline.

FERC and state public utility commissions. Whether FERC Order 2023’s interconnection reforms constitute a sufficient regulatory regime for Trinko purposes is the threshold legal question any first significant enforcement action will need to resolve. The answer determines whether antitrust liability operates at the federal level or routes around Trinko through state and private channels.

Hyperscaler general counsel and antitrust compliance functions. The conduct categories the article maps — dedicated generation agreements, transformer procurement, cooling architecture commitments — were individually rational when formed. The aggregate pattern now constitutes the evidentiary core that enforcement actors across nodes will target. Governance strategy built on the assumption of sustained federal enforcement restraint underweights the distributed enforcement risk.

Institutional investors with AI infrastructure exposure. The investment corollary tracks the legal corollary directly. Positions that expand system capacity — transformer manufacturing, advanced transmission, next-generation generation — reduce both physical constraint and legal exposure simultaneously. Positions that capture existing scarcity without expanding it accumulate antitrust exposure at the same rate they reduce competitive availability for the developers who will eventually constitute the complainant class.

EU competition counsel and policy advisors. The European Commission’s March 2026 formal activation on AI stack control creates an evidentiary record that domestic state-level enforcement and private litigation can incorporate without waiting for federal agency initiation. Cross-jurisdictional propagation is precedented and active, not prospective.

Read the Full Article

Infrastructure Routing Control: The Operative Antitrust Trigger in AI Energy Markets — CPI Antitrust Chronicle, April 2026

The article develops the four conduct categories (queue preemption, transformer supply concentration, dedicated generation lock-in, cooling architecture commitment), the five doctrinal theories (Section 2 monopoly maintenance, essential facilities, de facto exclusive dealing, Section 1 concerted refusal, refusal to deal), the buyer-side monopsony theory, the efficiency-defense critique, the distributed enforcement architecture analysis, and the full-stack vertical foreclosure theory connecting infrastructure routing control to model partnership and enterprise distribution layers.

The article also flags two dimensions left for future development: state public utility commission rate cases as antitrust-relevant evidence, and environmental review and permitting timelines as a structural weakness in any Trinko defense.