MCAI Economics Vision: Where Institutional Capital Moves Under Federal Digital-Asset Control Architecture

MindCast Digital Asset Series: Prediction Markets, Stablecoins, CFTC Rule 40.11, AML/CFT, and the Bypass Geometry Driving Kalshi, Coinbase, Gemini, and GENIUS Act Corridor Consolidation

Related works: Why Kalshi, Coinbase, and Gemini Face the Same Regulatory Problem: Prediction Markets, Stablecoins, and AML/CFT as a Single Control System | The Rule 40.11 Paradox — Kalshi, the Third Circuit, and the Class Action the Ninth Circuit Cannot Ignore | Defining “Gaming” Under the Commodity Exchange Act, The Rule 40.11 Gap Driving the Nationwide Kalshi Litigation Web

Capital will concentrate in platforms and infrastructure that compress compliance latency while preserving regulatory access. Every other strategy is a bet against capital flow.

Federal digital-asset regulation has resolved into a capital routing problem, not a legality problem. The three open rulemakings — CFTC Rule 40.11, Treasury’s GENIUS Act state-regime framework, and the joint FinCEN/OFAC AML/CFT framework — no longer operate as independent dockets. They operate as a single cybernetic control architecture whose governing variable is feedback latency. Capital routes through the corridors that clear fastest under survivable enforcement exposure, regardless of classification outcomes.

Institutional capital allocates when three conditions hold simultaneously: regulatory survivability, low-latency execution, and scalable settlement rails. No platform currently satisfies all three. The unmet gap is the opportunity set.

The investable consequence is specific. Three concentrations are forming simultaneously: infrastructure dominance at the execution layer, corridor consolidation at the structure layer, and bifurcated price discovery at the market layer. Each concentration is observable, measurable, and pricable on defined time horizons. Three mispricings are open now: legal-clarity platforms overweight, compliance-speed infrastructure underweight, latency not priced as a governing variable. Entry 1 diagnosed the system. Entry 2 operationalizes the diagnosis into six allocable predictions, a cross-archetype capital view, a signal dashboard, fund-type deployment playbooks, and the first named trade.

The first trade is long the compliance-speed infrastructure layer. Five of the six predictions reward this position simultaneously. Platforms that cannot compress compliant settlement latency below the threshold institutional capital requires will not fail through regulatory attrition. Capital leaves faster than models assume. Bypass geometry operates on institutional-liquidity timescales — single reporting cycles, not multi-year corridor migration. The bypass is the investment thesis — long the infrastructure and corridors that absorb routed capital, short or avoid the platforms whose geometry forecloses it. Section XII names the 90-day watchlist: court triggers, state AG actions, class certifications, federal rulemaking dates, and capital flows into digital-asset firms.

Executive Summary

1. The system has shifted from classification to control. Entry 1 established that legality, structure, and execution operate as a single closed-loop system governed by feedback latency. Feedback latency is now the dominant variable across every enforcement, corridor, and settlement outcome. Classification battles are downstream.

2. Six falsifiable predictions anchor the 3- to 36-month window. Three primary predictions (execution dominance, corridor consolidation, latency bifurcation) and three secondary predictions (cross-domain litigation, hybrid regime, latency compression arms race) carry probability bands from 55% to 75%. Each prediction maps to observable indicators with thresholds. Each carries a falsification condition that disciplines the view.

3. Four system-level invariants hold regardless of which predictions resolve. Feedback latency governs outcomes. Corridor dominance replaces open competition. Classification deferral generates enforcement rather than suspending it. Infrastructure supersedes statute. An allocator can underwrite the invariants even if individual predictions miss.

4. The capital routing consequence is concentration. Institutional flow concentrates in three dominant stablecoin corridors, one or two compliance-acceleration vendor clusters, and a narrow set of platforms that execute the latency-compression roadmap. The concentration creates defined long positions in infrastructure and corridor incumbents, and defined short or avoid positions in platforms caught in the bypass geometry. Diversification underperforms in corridor-dominant systems.

5. The market is mispriced on three variables. Consensus is overweight legal-clarity platforms, underweight compliance-speed infrastructure, and does not price latency as a governing variable. The mispricings close as specific observable thresholds activate — most within 12 months. Section VI names the mispricings; Section XI names the first trade.

6. The first trade is long compliance-speed infrastructure. Five of the six predictions reward this position simultaneously. Falsification requires either regulatory standardization of compliance-speed technology or 18 months of vendor-market investment without latency improvement. Every other position in the framework depends on correctly sequencing prediction resolution; this one does not.

7. Observable indicators are already activating. The Ninth Circuit heard oral arguments April 16, 2026 in consolidated Kalshi/Crypto.com/Robinhood v. Nevada cases controlling a nine-state footprint. The Fourth Circuit calendars Maryland oral arguments May 7, 2026. Arizona filed the first criminal charges against a CFTC-registered prediction market operator on March 17, 2026. The New York Attorney General’s April 21, 2026 actions against Coinbase Financial Markets and Gemini Titan are the first live Stage 1 to Stage 2 convergence event in the stablecoin-adjacent ecosystem. The Kaiserman class action converts CFTC Rule 40.11 ambiguity into damages under 7 U.S.C. § 25(b) without waiting for classification resolution. Section XII carries the 90-day watchlist across court triggers, state AG actions, class actions, federal rulemakings, and capital flows.

8. Portfolio construction and fund-type playbooks translate the framework into deployment. Core (60–70%) in settlement rails and compliance infrastructure; Growth (20–30%) in hybrid execution platforms; Optionality (10–20%) in emerging corridors and compliance-speed vendors. Venture, hedge fund, private equity, and strategic corporate capital each carry distinct entry paths. Section X develops the fund-type playbooks including three ranked hedge fund trade structures with entry triggers, mechanics, and breakage paths.

9. The entry window is weeks, not quarters. Consensus pricing still reflects the classification paradigm. The compliance-speed infrastructure re-rating activates on the first Coinbase-archetype acquisition of a category vendor or the first publicly announced sub-2-minute compliant settlement. Either event is likely within 90 to 180 days. Section XIII names the Top 5 Positions with entry triggers and falsification conditions.

10. MindCast’s position. MindCast’s Cognitive Digital Twin Foresight Simulation produced the predictions in Entry 1 and is producing the corridor-level calibration updates that will follow in subsequent entries. Institutional subscribers receive the running signal calibration, archetype-level capital views, 90-day watchlist updates, and pivot-trigger alerts as the system resolves.

I. The Capital Routing Thesis Stated

• Core claim: Capital routes through corridors that clear fastest under survivable enforcement exposure, regardless of classification.

• The three-condition opportunity set: Institutional capital allocates when (1) regulatory risk is contained, (2) latency sits below execution tolerance, and (3) settlement rails are reliable. No current platform clears all three. The unmet gap is the investable surface.

• Why now: Three rulemakings operating as one architecture; NY AG action as the first live convergence event; Third Circuit’s April 6, 2026 Flaherty decision; Kaiserman class action converting ambiguity into damages.

• Investable output: Long infrastructure and corridor incumbents; short or avoid bypass-geometry platforms; relative-value framework across the five archetypes; fund-type-specific deployment paths in Section X.

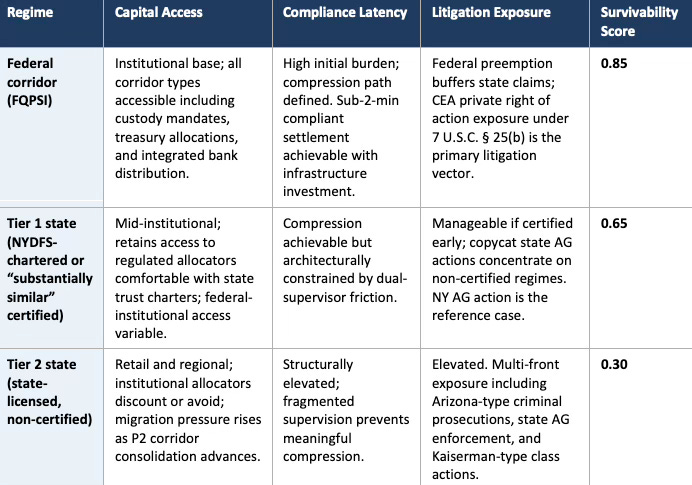

II. Issuer and Platform Decision Matrix Under Latency and Corridor Constraints

The decision surface: The three-condition test from Section I applies unevenly across regulatory regimes. Capital access, compliance latency, and litigation exposure each vary by whether an issuer or platform operates on the federal corridor (FQPSI), a Tier 1 state regime (NYDFS-chartered or Treasury “substantially similar” certified), or a Tier 2 state license. The matrix below compresses the three variables into a single survivability score across the three regimes — the decision surface allocators and counsel can apply to any specific issuer or platform.

• How to use the matrix: For any specific exposure, identify the regime, then read across to the survivability score. Scores above 0.70 clear the three-condition test; scores between 0.50 and 0.70 carry optionality with defined risks; scores below 0.50 indicate bypass candidates that should be reviewed for exit or hedge.

• Why Tier 2 sits at 0.30: The combination of elevated compliance latency (structural fragmentation), contracting institutional capital access (allocators concentrate in FQPSI and Tier 1), and multi-front litigation exposure (criminal, AG, private class) is not survivable without a defined exit path to a higher regime. Tier 2 issuers and platforms without certified migration plans trade as expiring options.

• Why FQPSI does not score 1.0: Federal corridor operators retain CEA § 25(b) private-right-of-action exposure and must still execute the latency compression build. The federal preemption buffer addresses state litigation vectors, not the full three-condition test.

• Live application: The NY v. Coinbase Financial Markets and Gemini Titan actions (April 21, 2026) test Tier 1 and federal-corridor survivability under stablecoin-adjacent stress; Arizona’s March 17, 2026 criminal prosecution tests Tier 2 survivability against criminal escalation. Both events are Section XII watchlist items.

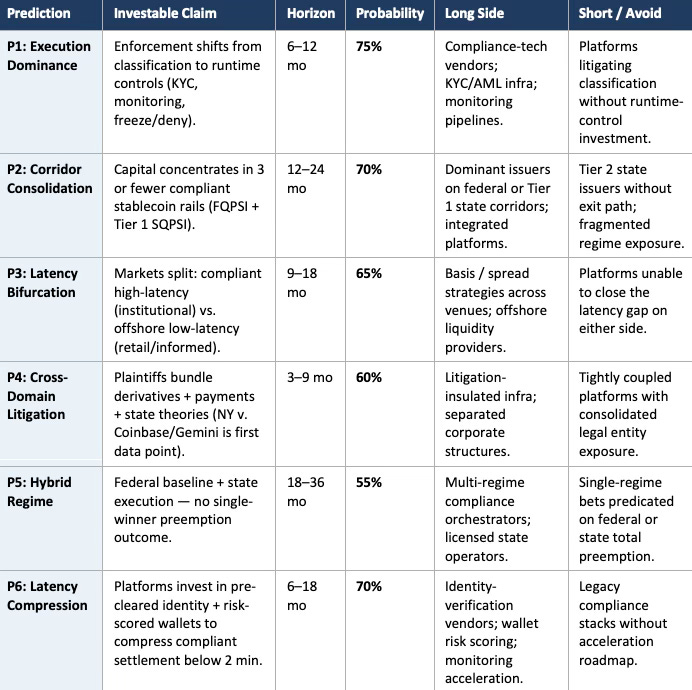

III. The Six Predictions as a Capital Allocation Framework

Each prediction converts to a specific capital position with defined entry, monitoring, and exit conditions.

• Correlation structure: P1, P2, and P6 are positively correlated — all three drive capital toward dominant infrastructure and corridors. P3 and P4 are partially uncorrelated hedges. P5 is the terminal-state view that re-prices the entire book if the hybrid regime resolves faster than the 18 to 36 month horizon implies.

• Falsification discipline: Each prediction carries an explicit falsification condition. Positions unwind when observable indicators cross falsification thresholds, not when narrative sentiment shifts.

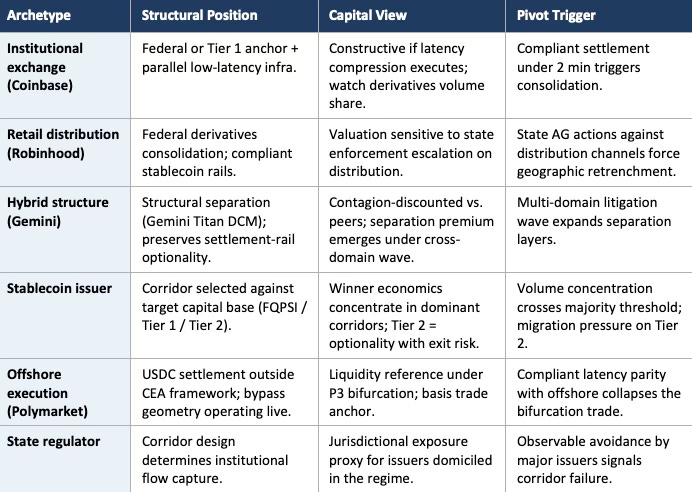

IV. Archetype-Level Capital View

The five firm archetypes from Entry 1 translate into a relative-value map: structural position, capital view, and pivot trigger.

• The governing tradeoff: Latency versus capital density under enforcement uncertainty — not federal versus state. Archetypes that optimize for the right side of the tradeoff at the right horizon capture the routing flow. Archetypes that misprice the tradeoff face bypass.

Contact mcai@mindcast-ai.com to partner with us on Predictive Law and Behavioral Economics + Game Theory Foresight Simulations. To deep dive on MindCast upload the URL of this publication into any LLM (preferably ChatGPT or Gemini for magazine style works) and prompt ‘reconstruct MindCast framework with three degrees of cited sub links.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure.

About MindCast AI

MindCast is a predictive behavioral economics and game theory artificial intelligence firm specializing in complex litigation, geopolitical risk intelligence, and innovation ecosystems. MindCast publishes falsifiable institutional foresight analysis at mindcast-ai.com.

V. The Bypass Trade and Portfolio Construction

• The live demonstration: Polymarket’s offshore USDC settlement is the bypass geometry operating in production. Every domestic platform without a latency-compression roadmap faces the same bypass regardless of regulatory standing. Capital bypass replaces gradual underperformance.

• The long side: Identity verification vendors; risk-scored wallet infrastructure; monitoring acceleration; compliant stablecoin issuers on dominant corridors; regulated platforms executing the compression roadmap. The rationale is mandatory spend across every compliant platform, producing durable demand and pricing power.

• The short or avoid side: Platforms focused on legal positioning without infrastructure investment; offshore-only venues without compliant bridges; fragmented state-only strategies without scale; tightly coupled corporate structures exposed to cross-domain contagion; Tier 2 state issuers without a defined exit path.

• The hedge: Basis and spread strategies across compliant and offshore venues during high-volatility events monetize Prediction 3 directly while hedging Prediction 6 downside.

Portfolio Construction

Corridor-dominant systems reward concentration, not diversification.

• Core (60–70%): Settlement rails and compliance infrastructure — the mandatory-spend layer underwriting every compliant platform.

• Growth (20–30%): Hybrid execution platforms combining regulated infrastructure with parallel low-latency execution — optionality under regulatory convergence.

• Optionality (10–20%): Emerging corridors, compliance-speed vendors, and latency-compression startups — asymmetric exposure to the arms race identified in Prediction 6.

Diversification underperforms in corridor-dominant systems. The four invariants in Section VIII specify why.

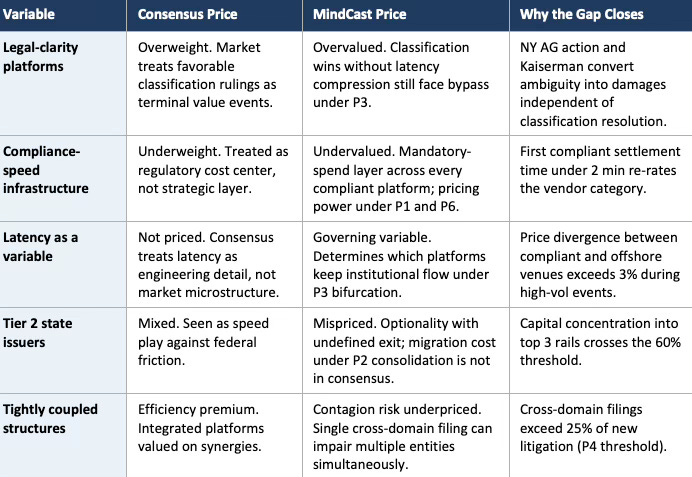

VI. Where Capital Is Mispriced Today

The framework creates urgency because the current market is wrong on three variables. Consensus pricing reflects the legality paradigm the paper replaces; capital allocated on the old paradigm is mispriced in the new one.

• The central mispricing: Compliance-speed infrastructure is treated as a cost center when it is a strategic layer with mandatory spend, pricing power, and the only category that wins under five of the six predictions simultaneously. The re-rating activates when the first regulated platform compresses compliant settlement below 2 minutes.

• Why consensus is stuck: Public debate sits inside the classification paradigm — preemption, jurisdiction, Rule 40.11 scope. The governing variable is feedback latency, which does not appear in the classification frame. The gap between public framing and governing variable is the source of the mispricing.

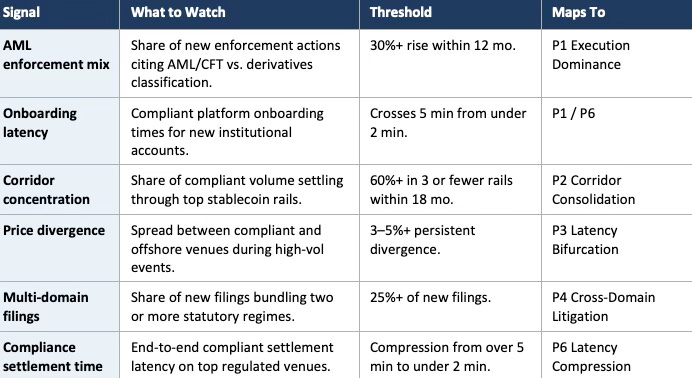

VII. The Signal Dashboard

Observable indicators activate the predictions and close the mispricings. Each signal maps back to the prediction it validates or falsifies.

• Refresh cadence: Quarterly full calibration; event-driven updates on appellate resolutions, NPRM final-rule publication, and large enforcement actions.

• Leading vs. lagging: Onboarding latency and compliance settlement time are leading indicators of P1 and P6. Corridor concentration and price divergence are lagging indicators that confirm P2 and P3.

VIII. Four System-Level Invariants and Why They Underwrite the Book

• Feedback latency governs all outcomes. The dominant variable across every prediction path.

• Corridor dominance replaces open competition. A small number of administered corridors capture disproportionate institutional flow.

• Classification deferral generates enforcement rather than suspending it. Private, state, and federal tracks operate independently of classification resolution.

• Infrastructure supersedes statute. Settlement, identity, and monitoring infrastructure determine outcomes inside any regulatory perimeter.

The invariants hold even if all six predictions fail simultaneously. Any alternate resolution must satisfy the four structural claims or reveal an unanticipated system state. Allocators underwrite the invariants; positions express the predictions.

IX. Catalyst Calendar and Deployment Phasing

Catalyst Calendar

• Near-term catalysts (0–6 months): CFTC RIN 3038-AF65 comment period closes (April 30, 2026); Kaiserman class certification docket; further NY AG actions and copycat state filings; first final-rule publications across the three rulemakings.

• Mid-term catalysts (6–18 months): Ninth Circuit Kalshi resolution or cert petition; first compliant settlement latency compression below 2 minutes; initial corridor concentration signal crossing the 60% threshold.

• Terminal catalysts (18–36 months): Hybrid regime codification; interagency MOU or joint guidance across CFTC, Treasury, and state regulators; appellate confirmation or rejection of the managed-fragmentation outcome.

Deployment Phasing

Catalyst resolution maps to three deployment phases. The phasing is additive: positions taken in Phase 1 remain in place through Phase 3 unless observable indicators cross falsification thresholds.

• Phase 1 — Accumulate (0–6 months): Build positions in infrastructure and compliance-speed exposure. Catalyst path is unchanged by regulatory noise because the mandatory-spend layer absorbs flow under every scenario.

• Phase 2 — Monitor and Select (6–12 months): Track enforcement shift indicators (AML mix, onboarding latency) and signal activations. Begin selective platform exposure as archetype pivot triggers activate.

• Phase 3 — Concentrate (12–24 months): Concentrate into dominant rails and execution leaders as corridor consolidation completes and latency compression separates winners from bypass candidates.

X. Fund-Type Deployment Playbooks

The framework holds for mixed institutional capital; deployment paths differ by fund type.

Venture Capital

• Focus: Early-stage infrastructure and compliance-speed layers — identity, monitoring acceleration, latency compression, wallet risk scoring.

• Strategy: Seed the mandatory-spend layer before consolidation; avoid pure application-layer bets that lack an infrastructure moat against the bypass geometry.

• What NOT to fund: Consumer prediction-market applications without an infrastructure moat; legal-optimization or classification-arbitrage plays whose value depends on classification wins; application-layer wrappers over offshore settlement without a compliant bridge roadmap. The application layer is structurally bypassed under the three-layer architecture; capital routes around it.

• Edge: Capture foundational infrastructure positions before Prediction 2 corridor consolidation and Prediction 6 vendor-market concentration compress entry points.

Hedge Funds

• Focus: Timing, arbitrage, and cross-venue inefficiencies produced by the bifurcation dynamic.

• Strategy: Three executable trade structures, ranked by conviction.

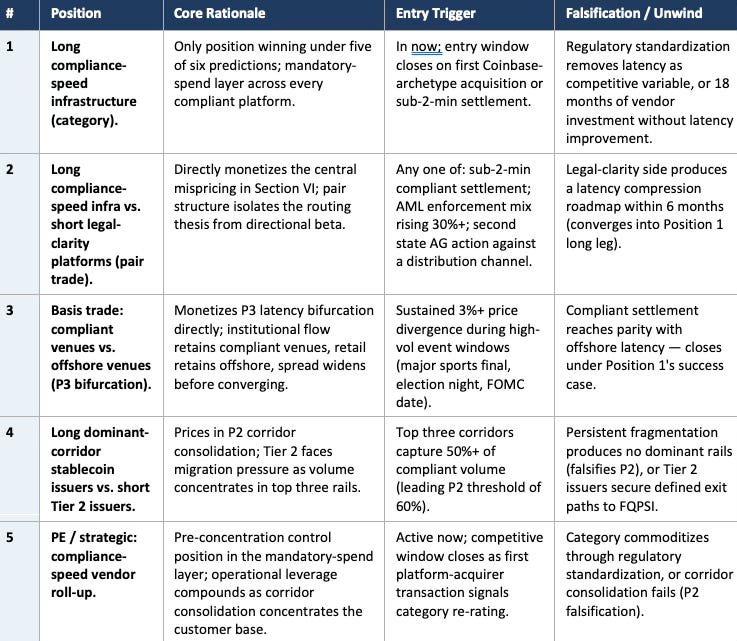

◦ Trade 1 — Long compliance-speed infrastructure vs. short legal-clarity platforms. When: enter on confirmation of any one of three triggers — first sub-2-minute compliant settlement, AML enforcement mix rising 30%+, or second state AG filing against a distribution channel. How: pair-trade structure sized to the spread between mandatory-spend durability and classification-event terminal value. What breaks first: the legal-clarity side, as classification wins fail to produce latency compression and get caught in P3 bifurcation.

◦ Trade 2 — Basis trade across compliant and offshore venues. When: enter on sustained 3%+ price divergence during any high-volatility event window (major sports final, election night, FOMC date). How: spread position across the two venue types, sized to the divergence half-life. What breaks first: the offshore side’s price, as compliant venues attract institutional flow with credibility while offshore venues retain retail flow with speed — the divergence widens before it converges.

◦ Trade 3 — Long dominant-corridor stablecoin issuers vs. short Tier 2 issuers. When: enter on confirmation that top 3 corridors capture more than 50% of compliant volume (leading P2 threshold). How: relative-value across the issuer capital stack. What breaks first: the Tier 2 float as migration pressure forces reserve-asset confidence repricing and token-layer utility degrades simultaneously.

• Edge: Exploit short-term dislocations during system convergence. The Signal Dashboard in Section VII supplies the activation thresholds; the mispricings in Section VI supply the directional bias.

Private Equity

• Focus: Control positions in scaling infrastructure — compliance vendors, identity platforms, integrated settlement and execution stacks.

• Strategy: Acquire or roll up compliance-speed vendors before corridor consolidation; build vertically integrated settlement-plus-execution stacks that capture the margin the bypass geometry strands at the platform layer.

• Edge: Scale and operational leverage in the infrastructure layer that every compliant platform must spend into.

Corporate and Strategic Investors

• Focus: Ecosystem positioning and integration across regulated platforms, settlement rails, and distribution channels.

• Strategy: Invest in or partner with dominant rails; build internal compliance-speed capabilities; secure distribution and settlement alignment ahead of corridor consolidation.

• Edge: Ecosystem control and long-term strategic positioning that survives hybrid regime codification under Prediction 5.

XI. The First Trade and Position Implications

The Highest-Conviction Position

The highest-conviction position is long the compliance-speed infrastructure layer — identity verification, risk-scored wallet infrastructure, monitoring acceleration, and latency-compression tooling. The conviction rests on a single structural claim: five of the six predictions reward this position simultaneously (P1 execution dominance, P2 corridor consolidation, P5 hybrid regime, P6 latency compression, and — through the bifurcation-closure mechanism — P3 latency bifurcation). The position also wins asymmetrically under P4 cross-domain litigation because separation-supporting vendors become acquisition targets.

Why it is the first trade: Every other position in the framework depends on correctly sequencing which prediction resolves first. The compliance-speed infrastructure position is independent of resolution order — it captures mandatory spend across every compliant platform under every prediction path except the single falsification case (P6 regulatory standardization of latency technology).

The falsification condition: The position unwinds if regulators intervene to standardize compliance-speed technology and remove it as a competitive variable, or if compliant settlement latency fails to improve despite vendor-market investment over the 18-month window.

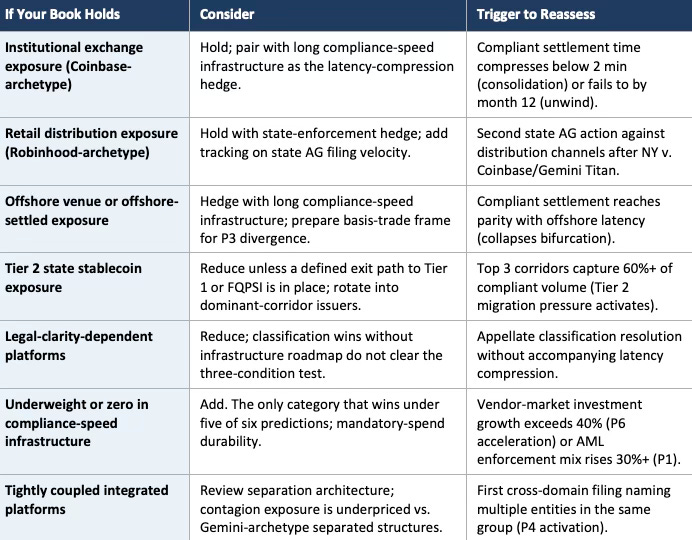

Position Implications by Current Holding

The table below translates the framework into specific actions for common institutional book compositions. Each row identifies a typical exposure, the action consistent with the three-layer control architecture, and the observable trigger that should prompt reassessment.

• The live-book reality: Most institutional books are long the wrong side of the mispricings in Section VI — overweight legal-clarity platforms, underweight compliance-speed infrastructure, with Tier 2 state exposure carried as speed optionality. The actions above rebalance against the three mispricings without requiring a single view on classification outcomes.

• What to cut to fund the first trade: Legal-clarity-dependent platforms (the first row of the mispricings table) and Tier 2 state issuers without exit paths. Both are mispriced in the same direction for the same reason — consensus still operates on the classification paradigm the framework replaces.

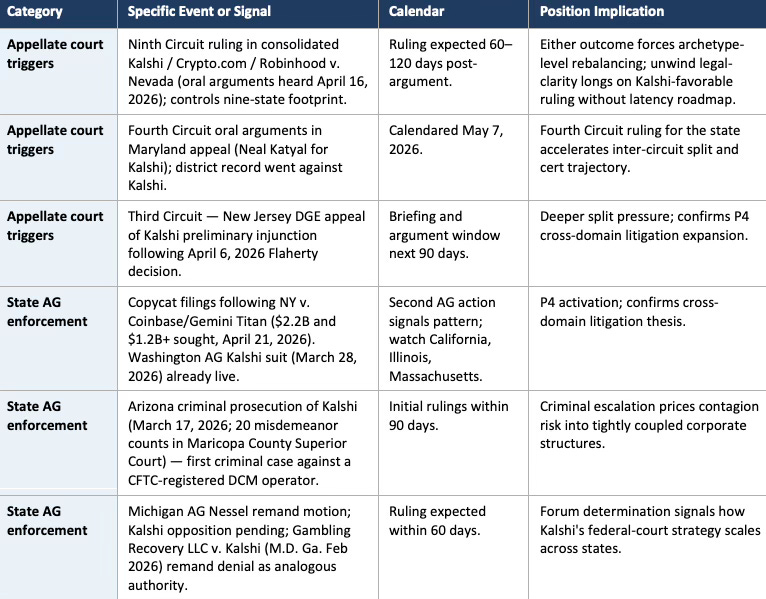

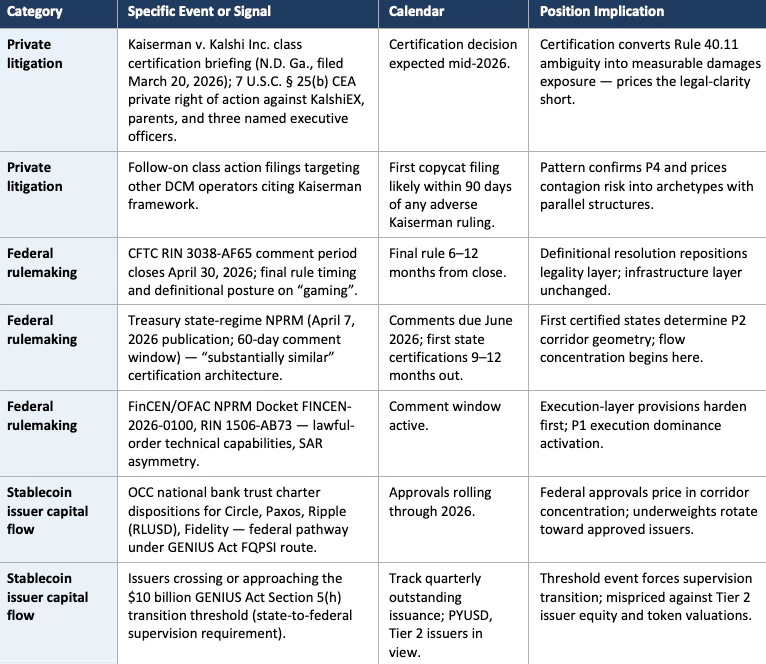

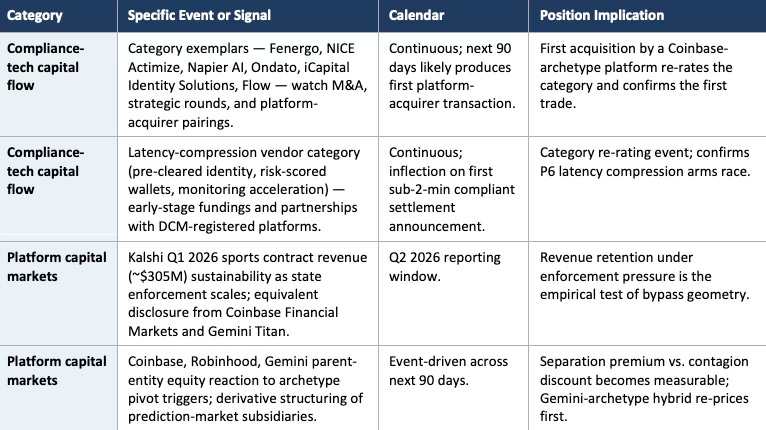

XII. Where to Look First (Next 90 Days)

The critique of any routing thesis is “what, specifically, and when.” Section XII translates the framework into a 90-day watchlist organized by category: appellate court triggers, state AG enforcement, private litigation, federal rulemaking, and capital flows into digital-asset firms. Each line is a specific, live event or signal, with its calendar and the position implication it carries. Institutional subscribers receive event-driven updates as each line activates.

• What has already moved: State AG enforcement has priced in for Kalshi directly (Nevada, New Jersey, Massachusetts, Arizona, Washington, Michigan). The Third Circuit April 6, 2026 Flaherty decision and the April 21, 2026 NY v. Coinbase/Gemini Titan filing are reflected in affected equity marks.

• What has not priced yet: The compliance-speed infrastructure re-rating — Section VI’s central mispricing. Category exemplars continue to trade on legacy compliance-vendor multiples rather than on the mandatory-spend thesis the three-layer architecture implies. The window for entering at consensus pricing closes on the first Coinbase-archetype platform acquisition of a category vendor or the first publicly announced sub-2-minute compliant settlement. Either event is likely within 90 to 180 days.

• The late-entry penalty: Corridor-dominant systems produce compressed entry windows because capital concentration is itself self-reinforcing. Waiting for P2 corridor consolidation to be obvious in market data means paying post-concentration prices for pre-concentration exposures. The first trade is sized against the 90-day window, not the 18-month horizon.

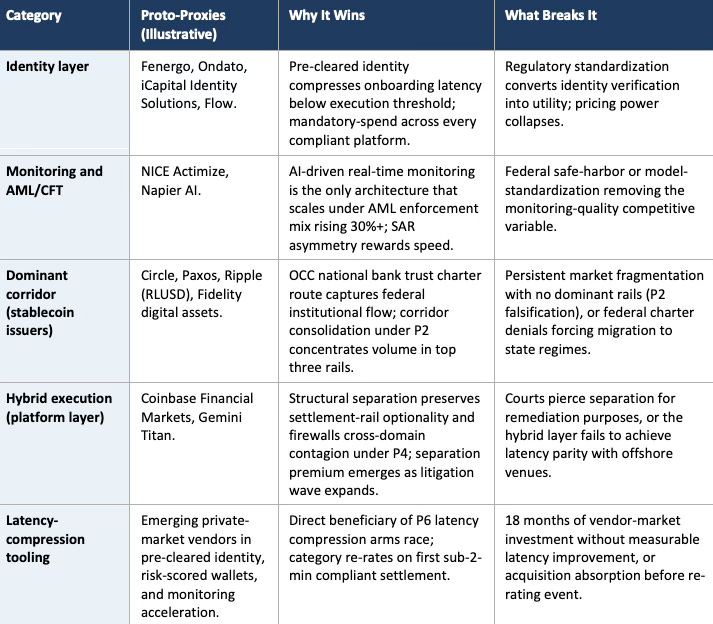

Named Categories and Proto-Proxies

The investable categories below identify where capital routing lands. Named firms are proto-proxies — illustrative exemplars showing the shape of the exposure allocators can map against public and private comparables — not recommendations. Each category carries a structural reason it wins and a defined condition that breaks it.

• What not to fund (VC specific): Consumer prediction-market applications without infrastructure moat; legal-optimization platforms whose value proposition depends on classification wins; application-layer wrappers over offshore settlement without a compliant bridge roadmap. The application layer is structurally bypassed under the three-layer architecture; capital routes around it.

XIII. Top 5 Positions Right Now

The framework compresses to five named positions, ranked. Position 1 is the first trade. Positions 2 through 4 are the three ranked hedge fund structures from Section X. Position 5 is the PE and strategic opportunity. Each position carries a core rationale, an entry trigger, and a falsification condition. Allocators size at their own discretion; the framework supplies direction and conviction, not book construction.

• Correlation across the five: Positions 1, 2, and 5 share the compliance-speed infrastructure long leg and are positively correlated. Position 3 is a partially uncorrelated hedge against Position 1’s success case. Position 4 is orthogonal to the other four and functions as an independent expression of P2 corridor consolidation.

• Sequencing: Positions 1 and 5 are active now. Position 2 activates on the first of three discrete triggers. Positions 3 and 4 activate on observable market thresholds. The framework does not require entering all five simultaneously.

• What the five positions share: Every falsification condition in the table is specific, observable, and time-bounded. Positions unwind on data, not on sentiment. The discipline is the product.

XIV. Implications by Reader Type

The framework produces different consequences for readers in different institutional roles. The allocator implications run through Sections X, XI, and XII. The translations below serve the other institutional audiences that read MindCast’s work — counsel advising regulated digital-asset operators, strategy consultants engaged on transformation and operating-model work, and regulatory advisors positioning clients against live rulemakings.

For Counsel

The framework reframes client strategy without reframing the law. The three-layer control architecture diagnosed in Entry 1 and operationalized here describes the institutional dynamics counsel’s clients face; it does not make legal claims counsel is better positioned to make. Three uses follow.

• Client-strategy intelligence beyond the classification frame: Client briefings that focus exclusively on preemption, Rule 40.11 scope, or state gambling licensing address only the legality layer. Clients facing the full three-layer control architecture also need counsel aware of the structure and execution layers where the bypass geometry operates. The archetype view in Section IV and the Section VI mispricings supply the frame for those conversations.

• Practice-area pipeline anticipation: The 90-day watchlist in Section XII identifies the dockets and rulemakings that will drive billable work in 2026–2027. Cross-domain litigation defense (bundled derivatives, payments, and state theories) expands under Prediction 4. Private CEA class actions following Kaiserman expand on a separate track. Compliance-speed vendor M&A activity under Prediction 6 creates transactional demand. State AG defense work scales as copycat filings follow NY v. Coinbase/Gemini Titan. Firms that staff and market against these vectors 12 to 24 months ahead of the wave capture the matters; firms that wait enter the pipeline at consensus pricing.

• Regulatory engagement positioning: The structural coherence risks identified in Entry 1 Section IV — definitional transfer, approval-architecture risk, non-displacement risk, and administrative-law constraint geometry — supply the substantive frame for comment letters, agency engagement, and amicus work across the three open rulemakings (CFTC RIN 3038-AF65, Treasury state-regime NPRM, FinCEN/OFAC Docket FINCEN-2026-0100). Counsel filing on any of the three dockets within the next 90 days can cite or build on the structural analysis without restating it.

For Strategy Consultants

The framework supplies scenario-planning inputs, operating-model diagnostics, and board-level framing that translate directly into transformation and strategy engagements.

• Scenario-planning inputs: The six predictions in Section III carry probability bands, timelines, observable indicators, and falsification conditions — the exact structure scenario teams build around. The four system-level invariants in Section VIII hold across any prediction path and anchor the base-case scenario. Client engagements that require 12- to 36-month regulatory scenarios for digital-asset operators can use the framework as the outside view complementing proprietary client data.

• Operating-model implications by archetype: The archetype-level view in Section IV and the observed routing patterns in Entry 1 Section V specify what different client types should build, acquire, or partner for. A Coinbase-type institutional exchange client needs latency-compression infrastructure and settlement-rail integration. A Gemini-type hybrid client needs separation architecture extension and cross-domain contagion firewalls. A Robinhood-type retail distribution client needs state-enforcement hedging and geographic retrenchment planning. The archetypes map onto live client portfolios with minimal translation.

• The C-suite diagnostic: The three-condition opportunity-set test from Section I — regulatory survivability, low-latency execution, scalable settlement rails — functions as a single-slide diagnostic for client board presentations. The question “which of the three conditions does the current strategy fail” structures the transformation engagement that follows. No platform currently satisfies all three; the gap is where the engagement value sits.

• Benchmarking: The five firm archetypes in Section IV function as competitive-peer benchmarks. Consultants evaluating client positioning on corridor selection, separation architecture, or settlement-rail integration can map clients directly against the observed patterns rather than against a theoretical framework. The archetype view is the benchmark.

For Regulatory Advisors

Counsel and strategy advisors positioning clients against the three open federal rulemakings operate at the intersection where the framework has its sharpest immediate application. Three uses follow.

• Comment-letter positioning across the three dockets: The Entry 1 Section IV coherence risks identify where final rules will face Loper Bright, Chenery, State Farm, and Encino Motorcars challenges. Comment letters that frame client positions around the structural coherence risks carry more weight on the deliberative record than comment letters that restate classification arguments. MindCast’s own CFTC comment (RIN 3038-AF65, published April 17, 2026) demonstrates the structural approach applied to one of the three dockets.

• Cross-docket coordination: Clients whose business touches all three rulemakings — which describes every Coinbase-archetype, Gemini-archetype, and Robinhood-archetype platform — benefit from coordinated engagement across CFTC, Treasury, and FinCEN/OFAC rather than independent single-docket responses. The three-layer control architecture supplies the framework for coordinated engagement because it diagnoses why the three rulemakings operate as one system.

• State-regime certification strategy: Treasury’s “substantially similar” architecture under the GENIUS Act (NPRM published April 7, 2026) creates a competitive positioning opportunity for state regulators and state-domiciled clients. Counsel and strategy advisors helping states design or clients navigate certification should treat corridor dominance as the governing outcome — dominant state regimes capture disproportionate institutional flow, which compounds into financial-services cluster benefits over the corridor consolidation window. The Section IV archetype view supplies the framework for predicting which states will administer dominant corridors.

XV. MindCast’s Role for Institutional Subscribers

MindCast serves allocators, counsel, and strategy advisors with a single analytical output calibrated to each reader type’s needs.

• Running calibration: Quarterly prediction calibration and probability updates as observable indicators activate.

• Archetype-level coverage: Capital view updates by archetype as routing behavior and separation architecture evolve — used by allocators for position sizing, by counsel for client-strategy briefings, and by strategy consultants for peer benchmarking.

• Pivot-trigger alerts: Event-driven notifications when corridor repositioning becomes likely across the five archetypes.

• 90-day watchlist updates: Event-driven updates as each line in the Section XII watchlist activates, including appellate rulings, class certification decisions, state AG filings, and category-level capital flow events.

• Comment-letter and amicus support: Structural coherence analysis supplied to counsel filing on CFTC, Treasury, and FinCEN/OFAC dockets, including non-confidential framing suitable for incorporation into client engagement materials.

• Scenario-planning and board-level framing: Single-slide and single-page translations of the framework for strategy-consultant use in C-suite and board presentations.

• Custom institutional analysis: Bespoke Cognitive Digital Twin Foresight Simulation applied to subscriber-specific questions — live dockets, client portfolios, regulatory engagement strategies.

XVI. Closing Position

The regulatory conversation is not the investment conversation. Regulatory outcomes determine which statutes apply. Feedback latency, corridor selection, and infrastructure dominance determine which platforms receive institutional capital. Entry 1 made the system-level case. Entry 2 converts the case into five named positions, three mispricings, a 90-day watchlist, and a signal dashboard that says when to move.

The asymmetry is the trade. If the thesis is wrong, positions unwind against specific falsification conditions over months as each threshold fails to activate — losses accumulate slowly, on measurable data, with time to reposition. If the thesis is right, capital exit from bypassed platforms compresses into single reporting cycles, compliance-speed infrastructure re-rates on a single announcement, and corridor concentration locks in pricing before post-concentration entrants can access the flow. The losses are slow and bounded; the gains are fast and structural. The asymmetry is what makes the first trade worth taking at size.

The direction of the system is decided. The five positions are named. The watchlist is active. Bypass is not a slow process — it is a discontinuity. The entry window is measured in weeks, not quarters.