MCAI Lex Vision: The Rule 40.11 Paradox — Kalshi, the Third Circuit, and the Class Action the Ninth Circuit Cannot Ignore

Federal Shield, Federal Sword — How the Same Statute Drives Both Kalshi's Preemption Win and Its Class Action Exposure

On April 6, 2026, the Third Circuit affirmed a preliminary injunction barring New Jersey from enforcing its gambling laws against Kalshi’s sports event contracts. The majority held that Kalshi’s contracts are “swaps” under the Commodity Exchange Act, that the CEA grants the CFTC exclusive jurisdiction over trades on designated contract markets, and that federal field preemption and conflict preemption together shield Kalshi from state regulation. The opinion is the first federal appellate ruling on the question. The Ninth Circuit hears consolidated oral argument in eight days.

Filed on March 20 — seventeen days before the Third Circuit ruled — Kaiserman v. Kalshi Inc., et al., No. 1:26-cv-01525 (N.D. Ga.), advances a position the preemption litigation never addresses. The complaint does not argue that states can regulate Kalshi. The complaint argues that Kalshi violated federal law — specifically, CFTC Rule 40.11, which prohibits registered entities from listing or clearing event contracts that “involve, relate to, or reference gaming.” The CEA provides a private right of action for exactly this violation under 7 U.S.C. § 25(b). Plaintiff Brian Kaiserman seeks damages on behalf of every U.S. trader who lost money on Kalshi’s sports contracts.

“The system now operates in a delay-dominant equilibrium: classification deferred, liability accumulating. The Third Circuit preserved the ambiguity. The Kaiserman complaint converts ambiguity into damages.”

The paradox is structural, and the system state it produces has a name. Prediction markets litigation has entered a delay-dominant equilibrium — swap classification is deferred across every appellate court that has addressed it, regulatory determination is pending through the CFTC’s ANPRM process, and congressional action remains contested. Ambiguity at the classification layer does not freeze the system. Ambiguity at the classification layer activates the private enforcement layer. The mechanism runs on two different time axes simultaneously: appellate courts allocate authority prospectively, determining who governs future conduct; private plaintiffs enforce violations retrospectively, recovering damages for conduct that already occurred. Deferring the first does not extinguish the second. Kaiserman is not waiting for resolution. The private right of action under 7 U.S.C. § 25(b) runs directly against DCMs and DCOs for violating existing rules — no new regulatory finding required, no classification ruling needed. The same statute Kalshi wields as a federal shield contains the sword.

"The system now operates in a delay-dominant equilibrium: classification deferred, liability accumulating. The Third Circuit preserved the ambiguity. The Kaiserman complaint converts ambiguity into damages."

The paradox is structural, and the system state it produces has a name. Prediction markets litigation has entered a delay-dominant equilibrium — swap classification is deferred across every appellate court that has addressed it, regulatory determination is pending through the CFTC’s ANPRM process, and congressional action remains contested. Ambiguity at the classification layer does not freeze the system. Ambiguity at the classification layer activates the private enforcement layer. The mechanism runs on two different time axes simultaneously: appellate courts allocate authority prospectively, determining who governs future conduct; private plaintiffs enforce violations retrospectively, recovering damages for conduct that already occurred. Deferring the first does not extinguish the second. Kaisermanis not waiting for resolution. The private right of action under 7 U.S.C. § 25(b) runs directly against DCMs and DCOs for violating existing rules — no new regulatory finding required, no classification ruling needed. The same statute Kalshi wields as a federal shield contains the sword.

I. What the Third Circuit Actually Held — and What It Left Open

The majority opinion authored by Judge Porter, joined by Chief Judge Chagares, reached the following conclusions: Kalshi’s sports event contracts satisfy the CEA’s statutory definition of “swaps” because outcomes of sporting events can be “associated with a potential financial, economic, or commercial consequence” — a threshold the majority found easily met given documented economic impacts on sponsors, advertisers, broadcast networks, and franchises. Federal field preemption applies because the CEA grants the CFTC exclusive jurisdiction over swaps traded on CFTC-licensed DCMs, and Congress replaced the prior patchwork of state futures regulation when it created the CFTC. Conflict preemption independently applies because permitting New Jersey to enforce its gambling laws would directly obstruct that congressional objective. All four preliminary injunction factors favored Kalshi.

The majority opinion runs 17 pages. Rule 40.11 appears in a single passage — acknowledged, then set aside. The court noted that the CFTC “has codified this power in a regulation, 17 C.F.R. § 40.11, but it has not yet acted to review or prohibit any sports-related event contracts.” The majority treated CFTC non-enforcement as the operative fact and moved on.

Judge Roth’s dissent engaged Rule 40.11 directly. The dissent argued that Rule 40.11(a)(1) already prohibits Kalshi’s contracts as gaming, that the CFTC’s failure to enforce its own regulation cannot preempt state law, and that agency inaction “alone cannot preempt state law, especially not when that inaction constitutes a failure to adhere to its own rules and regulations.” The dissent cited Reuters Ltd. v. FCC, 781 F.2d 946, 950 (D.C. Cir. 1986). The majority never answered that argument on the merits. The silence is the gap.

THE UNRESOLVED QUESTION

The Third Circuit majority’s preemption holding depends on the premise that Kalshi’s self-certification rendered its sports contracts presumptively approved under federal law. That premise holds only if the CFTC’s regulatory framework does not already prohibit those contracts under Rule 40.11. Judge Porter’s majority declined to decide whether Rule 40.11 applies to Kalshi’s sports contracts. Kaiserman is built on the position that Rule 40.11 does apply — and Kalshi’s own prior statements supply the evidentiary case.

Contact mcai@mindcast-ai.com to partner with us on Predictive Cognitive AI in Law and Behavioral Economics. To deep dive on MindCast Foresight Simulations upload the URL of this publication into any LLM and prompt ‘reconstruct MindCast framework with three degrees of cited sub links.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure.

MINDCAST PRIOR CORPUS — THIS PUBLICATION EXTENDS

The analytical framework applied here — the four-track enforcement hierarchy, the delay dominance function, the CFTC control-logic frame, the Trajectory A/B/C nomenclature, and the MindCast AI Proprietary Cognitive Digital Twin (CDT) Foresight Simulation methodology — was developed across nine prior MindCast publications. MindCast: Kalshi, Prediction Markets and the Conflict Architecture of Regulation established the foundational CDT architecture, the deference stack, and the Delay Dominance Function. MindCast: The National Kalshi Prediction Market Litigation Map established the four-track hierarchy and removal asymmetry. MindCast: The Ninth Circuit on April 16 as System Convergence originated the Trajectory A/B/C framework. MindCast: Prediction Markets Litigation Stack — Federal, Private, and State Enforcement Converge — this publication’s immediate predecessor — confirmed the transition to constraint-driven convergence and introduced the five-day temporal clustering analysis. The complete annotated ten-publication MindCast Kalshi corpus is indexed at www.mindcast-ai.com/p/kalshi-litigation-stack.

II. What Kaiserman Actually Does — Three Structural Moves

The Kaiserman complaint is not a generic gambling lawsuit dressed in federal pleading. Counsel at Beasley Allen constructed it around three aggressive structural choices that distinguish it from the state enforcement actions Kalshi has been battling across eleven states.

MOVE ONE: THE CEA USED AGAINST KALSHI, NOT AS PROTECTION

Every other piece of litigation in this ecosystem asks whether the CEA protects Kalshi from state gambling regulators. Kaiserman asks whether Kalshi violated the CEA. Rule 40.11 states plainly that “[a] registered entity shall not list for trading or accept for clearing . . . [a]n agreement, contract, transaction, or swap based upon an excluded commodity . . . that involves, relates to, or references . . . gaming.” The complaint alleges two independent readings of that prohibition, both of which encompass Kalshi’s sports contracts: the contracts “reference” gaming because they pay out on sports game outcomes, and the contracts “involve” gaming because they constitute gambling as defined by standard dictionaries and confirmed by prior CFTC commissioners.

The plaintiff invokes 7 U.S.C. § 25(b), which provides a private right of action against DCMs, DCOs, and their executive officers for failing to enforce — or improperly enforcing — the rules and statutory obligations the CEA requires to be enforced. The cause of action requires no new regulatory determination. Rule 40.11 is already in force. The violation, if proven, already occurred. Damages are already accruing.

MOVE TWO: KALSHI’S OWN PRIOR JUDICIAL ADMISSIONS AS THE EVIDENTIARY CORE

Before Kalshi entered the sports market in January 2025, Kalshi’s lawyers told a federal court the opposite of what Kalshi now argues. The complaint quotes extensively from KalshiEX LLC v. CFTC, No. 23-cv-3257 (D.D.C. 2024), where Kalshi argued that gaming contracts should not be listed on exchanges:

“The classic example is a contract on the outcome of a sporting event; as the legislative history directly confirms, Congress did not want sports betting to be conducted on derivatives markets.”

Football, horseracing, and golf are gaming contracts: “They’re all games. It’s something that has no inherent economic significance. It’s something done for amusement.”

“The ‘gaming’ category reaches contracts contingent on games — for example, whether a certain team will win the Super Bowl. It thus functions as a check on attempts to launder sports gambling through the derivatives markets.”

“Contracts that involve games are probably not the types of contracts that we want to be listed on an exchange, because they don’t have any real economic value to them.”

Kalshi made these admissions while litigating against the CFTC to win approval for political election contracts. Having drawn the legal line at sports in 2024, Kalshi crossed it in January 2025 — and by September 2025, sports contracts represented 90% of the platform’s volume, approximately $2 billion. By February 2026, Super Bowl trading alone surpassed $1 billion. The complaint documents that progression as evidence of bad faith, not regulatory uncertainty. MindCast: Kalshi Found the One Gap in American Gaming Law Nobody Closeddocumented the four extraction mechanisms — Kalshi Platinum, tribal-market NFL advertising, 18–21 demographic capture, and quantified revenue displacement — that the Kaiserman complaint now converts into a federal evidentiary record.

THE BAD FAITH RECORD

The Kaiserman complaint introduces into a second federal court record the documented sequence: Kalshi’s lawyers told a federal judge that Super Bowl outcome contracts are “gaming” prohibited by Rule 40.11. Kalshi’s lawyers told the same court that such contracts have “no inherent economic significance.” Seventeen months later, Kalshi’s marketing materials advertised itself as “the first federally regulated exchange where you can legally bet on the NFL in all 50 states.” Screenshots of targeted Georgia advertising, a “College Ambassadors” campus recruitment program, and Kalshi’s own New York Times-sourced volume chart showing sports markets consuming nearly all platform activity after September 2025 are all exhibited in the complaint.

A Supreme Court that eventually reads this record will not be reading a close regulatory question. It will be reading a documented pivot — made with full knowledge of the legal risk — in pursuit of revenue.

MOVE THREE: VERTICAL INTEGRATION THEORY EXPANDING THE LIABILITY SURFACE

The complaint names not only KalshiEX LLC (the DCM) and Kalshi Klear LLC (the DCO), but also Kalshi Inc. (the parent holding company), Kalshi Klear Inc. (the clearing parent), CEO Tarek Mansour, COO Luana Lopes Lara, and CCO Joshua Beardsley — individually. Beasley Allen’s pleading theory holds that the entire Kalshi corporate structure operates as a single integrated enterprise in which “each entity performs indispensable, sequential functions . . . interdependent and inseparable, all for a common benefit.”

Personal officer liability under 7 U.S.C. § 25(b)(3) for willfully aiding and abetting CEA violations creates a risk profile qualitatively different from regulatory enforcement. Mansour, Lopes Lara, and Beardsley face individual damages exposure grounded in their documented public statements, board-level governance authority, and knowledge of prior CFTC litigation where Kalshi itself characterized sports contracts as prohibited gaming. The complaint’s veil-piercing counts (Counts VII and VIII) further preserve full corporate liability in the event any operating subsidiary proves inadequately capitalized to satisfy judgment.

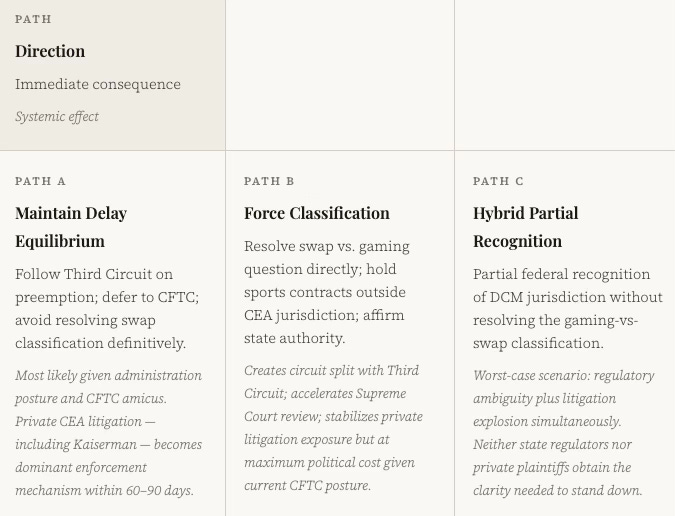

III. The Ninth Circuit Decision Node — Three Paths

The Ninth Circuit panel — Judges Ryan D. Nelson, Bridget S. Bade, and Kenneth K. Lee — hears consolidated oral argument on April 16 covering Kalshi, Robinhood, and Crypto.com against the Nevada Gaming Control Board. The district courts below ruled against all three platforms, finding sports event contracts are not swaps — a conclusion directly at odds with the Third Circuit majority. The CFTC filed an amicus brief asserting exclusive jurisdiction and supporting preemption. Now add the Third Circuit ruling and the Kaisermancomplaint to the information environment surrounding April 16. The MindCast AI Proprietary CDT Foresight Simulation framework — developed in MindCast: The Ninth Circuit on April 16 as System Convergence and extended in MindCast: Prediction Markets Litigation Stack — Federal, Private, and State Enforcement Converge — identifies three structural paths for the panel, each producing a distinct institutional consequence chain.

Path A is the dominant outcome under current institutional alignment. The current administration’s support for CFTC jurisdiction, the CFTC amicus brief, and the textualist preemption analysis the three Trump-appointed judges have signaled all point the same direction. Path A carries a consequence the Third Circuit majority never addressed: judicial restraint on classification does not insulate the system. Under Path A, Kaiserman and follow-on class actions proceed in federal district court pressing the Rule 40.11 violation theory that no appellate court has resolved. Deferring classification does not buy peace — it activates the private enforcement track.

The Ninth Circuit panel faces a choice whose consequences are asymmetric. Path B — forcing classification against Kalshi — collapses the CFTC’s control equilibrium and creates an immediate circuit split. Path C produces the worst-case outcome: ambiguity plus litigation explosion. Path A preserves appellate stability while transferring enforcement pressure to private plaintiffs. Kalshi exits April 16 with an expanded preemption win and a growing § 25(b) liability docket it cannot preempt away.

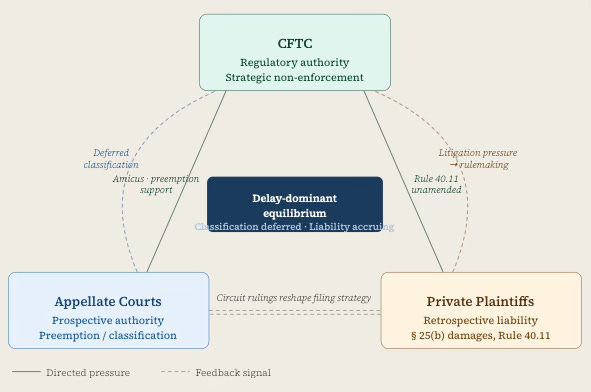

IV. The CFTC’s Posture Is Not Contradiction — It Is Control

Read superficially, the CFTC’s current posture looks inconsistent. On April 2 — four days before the Third Circuit ruled — the CFTC and DOJ jointly sued Arizona, Connecticut, and Illinois, asserting CEA preemption of state enforcement. The CFTC filed an amicus brief in the Ninth Circuit asserting exclusive jurisdiction. Chairman Michael Selig stated in January 2026 that “the CFTC has the expertise and responsibility to defend its exclusive jurisdiction over commodity derivatives.” Simultaneously, the CFTC published an advance notice of proposed rulemaking on prediction markets on March 16 — inviting public comment on the scope and public interest implications of “gaming” and “sports competition” under the very rule at the center of the Kaiserman complaint. Rule 40.11 remains on the books, unamended, unsuspended, with no guidance limiting its application to Kalshi’s sports contracts. Comments close April 30.

Treating that posture as contradiction misses the mechanism. The CFTC is not failing to resolve Rule 40.11 — the CFTC is strategically preserving Rule 40.11’s ambiguity because ambiguity preserves control. Leaving the gaming prohibition unresolved while defending exclusive jurisdiction gives the CFTC simultaneous leverage over the litigation calendar, the rulemaking process, and any congressional intervention. A CFTC that resolved Rule 40.11 definitively — either by formally clearing Kalshi’s contracts or by enforcing the prohibition — would forfeit that optionality. Non-resolution is not agency drift. Non-resolution is the governing strategy. MindCast: Kalshi, Prediction Markets and the Conflict Architecture of Regulation established the full deference stack — Loper Bright, Chenery, State Farm, Encino Motorcars, Gregory v. Ashcroft, and Montana v. Blackfeet Tribe — showing how each case independently breaks the CFTC’s institutional posture, and named the Delay Dominance Function: delay becomes rational when rule mutation outpaces enforcement in multi-forum litigation environments. MindCast: Prediction Markets Litigation Stack — Federal, Private, and State Enforcement Converge confirmed closed-loop feedback entry through the five-day temporal clustering in late March and early April 2026 — four major enforcement developments across four forums in five days, each triggering immediate counter-action before the prior action was legally processed.

Kalshi’s Kaiserman exposure follows directly from that control posture. The dissent in the Third Circuit held that agency inaction cannot preempt state law. Kaisermanadvances the parallel federal claim: agency inaction cannot render compliant a registered entity that knowingly violated the operative rule. Kalshi self-certified compliance with Rule 40.11 when it launched sports contracts in January 2025. The CFTC’s silence since that self-certification is not affirmative approval — it is the CFTC preserving its enforcement option while extracting maximum jurisdictional benefit from the litigation Kalshi is winning on its behalf.

CONTROL MECHANISM — SYSTEM STATE

The CFTC holds three levers simultaneously: (1) litigation support for Kalshi’s preemption defense, buying time for the DCM market to develop; (2) the unamended Rule 40.11, preserving the option to enforce against Kalshi or any successor platform whenever political conditions change; (3) the ANPRM, creating a rulemaking record that pre-positions the CFTC to redraw the gaming definition under any administration. Resolving any one of these levers collapses the others. The CFTC’s apparent inconsistency is the equilibrium, not a deviation from it.

The MindCast Prospective Repeated Game Architecture (PRGA) — developed in MindCast: Kalshi, Prediction Markets and the Conflict Architecture of Regulationand applied in MindCast: Prediction Markets Litigation Stack — Federal, Private, and State Enforcement Converge — reads private probability assessments from observable platform conduct rather than stated litigation posture. Kalshi’s voluntary March 2026 contract screening — accepting behavioral constraints no court ordered — reveals that internal probability of the upside preemption case contracted below the strategic threshold at which continued delay generates positive expected value. Platforms confident in their preemption theory do not accept self-imposed operational constraints before a court orders them. Kalshi’s own conduct is the most credible evidence that the platform’s internal assessment of April 16 is less optimistic than its public filings suggest.

V. Forward Prediction with Falsification Conditions

MINDCAST AI PROPRIETARY COGNITIVE DIGITAL TWIN (CDT) FORESIGHT SIMULATION — FORWARD PREDICTION

Extends the CDT probability methodology established in MindCast: Prediction Markets and the Regulatory Split (P45/P35/P20 bands, four days before three of six triggers activated) and the trajectory framework from MindCast: The Ninth Circuit on April 16 as System Convergence.

Primary prediction: If the Ninth Circuit follows Path A on April 16 — affirming preemption without resolving swap classification — private CEA litigation under 7 U.S.C. § 25(b) becomes the dominant enforcement mechanism against Kalshi’s sports contracts within 60–90 days. Kaiserman triggers a filing cascade. Beasley Allen — a plaintiff firm with demonstrated multi-jurisdiction filing capacity — files follow-on actions in New York, California, and Florida within 45 days of any Path A ruling, targeting the same DCM/DCO liability theory with local trader classes. Additional plaintiff firms enter within 60 days as the 90%-sports-volume revenue figure and the prior judicial admissions record become established pleading templates. Personal officer liability claims against Mansour, Lopes Lara, and Beardsley generate settlement pressure on an independent track from the regulatory litigation — Kalshi cannot moot damages exposure through a CFTC favorable ruling.

Secondary prediction: The Supreme Court grants certiorari before December 2026 if the Ninth Circuit and Fourth Circuit (oral argument May 7) reach divergent results on the preemption question. MindCast assigns 70–75% probability to Supreme Court review, conditional on Ninth Circuit divergence from the Third Circuit framework. The 64% market-implied probability understates the effect of 34-state amicus opposition, which gives the Court a political basis for review independent of doctrinal circuit split.

Falsification conditions — prediction is falsified if:

(1) The Ninth Circuit classifies Kalshi’s sports contracts as lawful swaps within CFTC exclusive jurisdiction and explicitly holds that CEA swap status supersedes Rule 40.11’s gaming prohibition — closing the liability gap the Kaiserman complaint occupies; OR

(2) The CFTC issues binding rulemaking before May 15 explicitly limiting Rule 40.11’s gaming prohibition as applied to sports contracts on licensed DCMs — forfeiting the control optionality identified in Section IV; OR

(3) The Kaiserman complaint is dismissed on standing or ripeness grounds before merits briefing, temporarily sealing the private enforcement escape valve and restoring the pure delay equilibrium.

VI. The Road to the Supreme Court

The multi-circuit litigation map is now dense. The Third Circuit has ruled for Kalshi. Two Nevada district courts ruled against Kalshi on the swap definition question. The Middle District of Tennessee ruled for Kalshi. The District of Maryland, the Southern District of Ohio, and two Nevada district courts ruled against Kalshi. The Fourth Circuit hears oral argument on May 7. The Sixth Circuit faces an intra-circuit conflict between Tennessee and Ohio. MindCast: The National Kalshi Prediction Market Litigation Map documents the removal asymmetry and cascade mechanic across sixteen active enforcement actions. The Paul Weiss litigation map documents suits against eleven states. The Holland & Knight alertplaces Supreme Court certiorari petitions as early as Q1 2027.

Senators John Curtis and Adam Schiff introduced the Prediction Markets Are Gambling Act on March 23, 2026 — a bipartisan legislative intervention that would amend the CEA to reclassify sports and casino-style event contracts as gambling outside CFTC jurisdiction, analyzed in MindCast: Prediction Markets — Legislative Regime Conversion and the Collapse of Preemption as the cross-trajectory invariant whose relevance increases regardless of which path April 16 signals. A bipartisan coalition of over 20 senators has urged the CFTC to abstain from intervening in prediction market litigation. More than 34 states, the District of Columbia, and the Northern Mariana Islands filed amicus briefs asserting state regulatory authority in the Third Circuit — a level of opposition the Supreme Court will find difficult to ignore even absent a formal circuit split.

Whatever the Ninth Circuit does on April 16, two federal records now contain Kalshi’s own lawyers telling a federal judge that football and golf contracts are gaming prohibited by Rule 40.11 — and Kalshi’s own platform data showing $2 billion in sports contracts launched seventeen months later. Preemption doctrine protects Kalshi from state enforcement. Preemption doctrine does not reach the federal liability claim building in the Northern District of Georgia. The delay-dominant equilibrium that protects Kalshi at the appellate level is the same equilibrium that makes the § 25(b) damages track inevitable. Deferral produces accumulation; they are the same mechanism. The system is not waiting for resolution — the system is resolving through parallel tracks simultaneously, and one of those tracks names Tarek Mansour, Luana Lopes Lara, and Joshua Beardsley as individual defendants.

The Control Triangle: Three Enforcement Tracks, One System

Each enforcement track operates on a different time axis, answers to a different principal, and produces a different form of resolution pressure. The feedback loop running between them — not any single track — drives the system toward eventual clarity.

MINDCAST ANALYTICAL NOTE

The Kaiserman complaint was filed March 20 — three weeks before the Third Circuit ruled. Beasley Allen constructed the Rule 40.11 private action theory independently, without the benefit of the appellate outcome. Two separate legal actors, working without coordination, reached the same conclusion: Rule 40.11 prohibits Kalshi’s sports contracts as currently structured. The Third Circuit majority’s silence on that question is not an answer. Silence on a dispositive regulatory question, in a 2-1 opinion issued under appellate time pressure, is a deferred question — now accumulating as liability in federal district court in Georgia.

The three enforcement tracks — appellate preemption litigation, CFTC regulatory action, and private § 25(b) damages claims — do not run in isolation. Private litigation pressure increases the probability of CFTC regulatory intervention, which reshapes the incentives facing appellate courts in subsequent circuit proceedings. Running that feedback loop accelerates system resolution independent of any single actor’s preferred timeline. The CFTC preserves its control leverage precisely because the loop keeps running. MindCast publishes post-argument simulation output the day of April 16 oral argument. Institutional subscribers receive same-day delivery.

KEY CITATIONS & SOURCES

KalshiEX LLC v. Flaherty, No. 25-1922 (3d Cir. Apr. 6, 2026) — Third Circuit majority opinion and Roth dissent.

Kaiserman v. Kalshi Inc., et al., No. 1:26-cv-01525-VMC (N.D. Ga. Mar. 20, 2026) — Class action complaint filed by Beasley Allen on behalf of Brian Kaiserman.

17 C.F.R. § 40.11 — CFTC Rule prohibiting registered entities from listing or clearing event contracts involving, relating to, or referencing gaming.

7 U.S.C. § 25(b) — CEA private right of action against DCMs, DCOs, and executive officers.

KalshiEX LLC v. CFTC, No. 23-cv-3257 (D.D.C. Sept. 12, 2024) — D.C. District Court opinion in which Kalshi’s prior admissions on gaming contracts appear in the record.

Prediction Markets ANPRM, 91 Fed. Reg. 12516 (Mar. 16, 2026) — CFTC advance notice of proposed rulemaking; comments due April 30, 2026.

CFTC Amicus Brief, N. Am. Derivatives Exch. v. Nevada, No. 25-7187 (9th Cir. Feb. 17, 2026) — CFTC asserting exclusive jurisdiction over DCMs.

Holland & Knight Alert (Apr. 7, 2026) — Appellate landscape and SCOTUS timeline analysis.

Paul Weiss Client Memo (Apr. 6, 2026) — Complete multi-jurisdictional litigation map with case citations.

KalshiEX LLC v. Orgel, No. 3:26-CV-00034, 2026 WL 474869 (M.D. Tenn. Feb. 19, 2026) — Pro-Kalshi district court ruling cited in Third Circuit fn. 6.

Blue Lake Rancheria v. Kalshi Inc., No. 3:25-cv-6162, 2025 WL 3141202 (N.D. Cal. Nov. 10, 2025) — Tribal gaming challenge; CFTC jurisdiction recognized.

MindCast: Kalshi, Prediction Markets and the Conflict Architecture of Regulation — Establishes the CDT architecture, deference stack, Delay Dominance Function, PRGA behavioral framework, and Trajectory A/B/C probability methodology extended in this publication.

MindCast: The National Kalshi Prediction Market Litigation Map — Four-track hierarchy, removal asymmetry, cascade mechanic, and sixteen-state enforcement map underpinning the multi-circuit analysis in Section VI.

MindCast: The Ninth Circuit on April 16 as System Convergence — Origins of the Trajectory A/B/C framework and the three-layer preemption architecture applied in Section III.

MindCast: Prediction Markets Litigation Stack — Federal, Private, and State Enforcement Converge— Immediate predecessor publication. Establishes four-track hierarchy with federal override as dominant layer, five-day temporal clustering analysis, Washington convergence node, and Arizona criminal prosecution as categorical prohibition pattern. Complete annotated ten-publication corpus indexed here.

MindCast: Kalshi Found the One Gap in American Gaming Law Nobody Closed — Documents the four extraction mechanisms (Kalshi Platinum, tribal-market NFL advertising, 18–21 demographic capture, revenue displacement) that the Kaiserman complaint converts into a federal evidentiary record.

MindCast: Prediction Markets and the Regulatory Split — Original CDT foresight simulation with P45/P35/P20 probability bands; the methodology this publication’s prediction block directly extends.

MindCast: Kalshi’s Prediction Market Federal Strategy — Three-layer litigation architecture as preemption-driven expansion engine; Big Lagoon procedural shield; supplemental authority cascade mechanic.

MindCast: Prediction Markets — Legislative Regime Conversion — Statutory Category Exclusion Mechanism (SCEM) and the Schiff-Curtis track as the cross-trajectory invariant identified in Section VI.