MCAI Lex Vision: Why Kalshi, Coinbase, and Gemini Face the Same Regulatory Problem: Prediction Markets, Stablecoins, and AML/CFT as a Single Control System

MindCast Digital Asset Series: How the GENIUS Act, CFTC Rule 40.11, and Treasury AML/CFT Framework Form Federal Digital-Asset Control Architecture

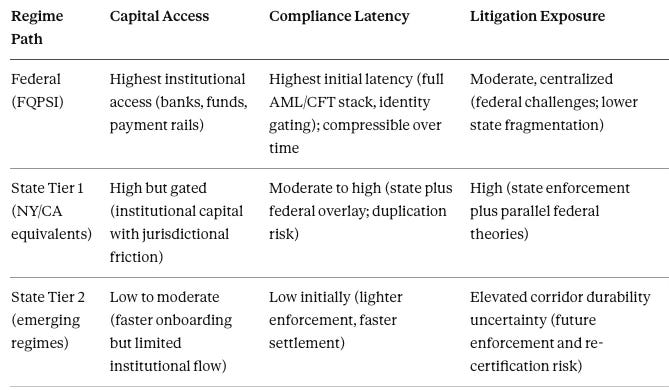

Related work: Where Institutional Capital Moves Under Federal Digital-Asset Control Architecture

Executive Summary

Prediction markets do not fail at legality. They fail at settlement under constraint.

The federal digital-asset control architecture operates as a single cybernetic system governed by feedback latency, regulatory routing, and execution constraints. The governing variable is no longer classification. Control shifts away from classification battles toward infrastructure-level dominance of transaction flow, identity gating, and latency compression. Systems that close feedback loops faster will dominate market behavior regardless of nominal legality.

Three primary predictions follow:

Prediction 1 — Execution Dominance Transition (6–12 months, 75% probability). Agencies shift enforcement from classification disputes to runtime controls: know-your-customer gating, transaction monitoring, and freeze/deny technical capabilities. Platforms redesign onboarding, order routing, and settlement to satisfy control hooks. Falsified if courts or agencies resolve classification decisively and deprioritize AML/CFT enforcement for these products.

Prediction 2 — Stablecoin Corridor Consolidation (12–24 months, 70% probability). Capital concentrates in a small set of compliant stablecoin regimes — state or federal — that offer acceptable latency and regulatory clarity. Non-aligned platforms lose institutional flow. Falsified if persistent fragmentation produces no dominant rails and institutional capital flows distribute evenly across many regimes.

Prediction 3 — Latency-Driven Market Bifurcation (9–18 months, 65% probability). Markets split into compliant high-latency venues with institutional access and low-latency offshore or lightly regulated venues with faster execution. Price discovery diverges under different latency profiles. Falsified if latency converges across venues through technology or regulatory harmonization.

Three secondary predictions extend the architecture into cross-domain litigation expansion (3–9 months, 60%), regime collapse into hybrid federal-state control structure (18–36 months, 55%), and a feedback latency compression arms race in the compliance vendor market (6–18 months, 70%). Full mechanisms, observable indicators, and falsification conditions for both tiers appear in Section VII.

The causal chain is explicit: regulatory constraint produces latency; latency reshapes firm behavior; behavior determines market outcome; market outcome becomes the input state for the next regulatory cycle. Agencies assert authority before definitional closure, creating delay-driven equilibria that firms exploit through jurisdictional routing and infrastructure selection. Stablecoin rails function as execution enablers. AML/CFT controls reshape participation and price formation through latency injection. The governing conflict moves from legality to control of infrastructure.

Three structural anchors frame the analysis:

Legality (Commodity Futures Trading Commission (CFTC) / courts)

Structure (state stablecoin regimes under the Guiding and Establishing National Innovation for U.S. Stablecoins Act (GENIUS Act))

Execution (anti-money laundering and countering the financing of terrorism (AML/CFT) controls and transaction governance)

Recent analysis by K&L Gates — Jennifer L. Crowder, Jeremy M. McLaughlin, and Joshua L. Durham, Treasury Proposes Framework for State Stablecoin Laws—Should You Issue Under a State Regime? (April 15, 2026) — correctly identifies the coordinated state-federal structure but does not model how the structure behaves under real-time market conditions. MindCast’s April 17, 2026 comment to the CFTC on RIN 3038-AF65 — MindCast Defining “Gaming” Under the Commodity Exchange Act, The Rule 40.11 Gap Driving the Nationwide Kalshi Litigation Web — reframes legality as a contested equilibrium rather than resolving it. The present publication extends that work into the structure and execution layers and converts the combined architecture into a foresight simulation.

Administrative-law constraints (Chenery, State Farm, Encino Motorcars, Loper Bright) operate as structural constraint geometry on each rulemaking, not as independent doctrinal levers. Blockchain functions as infrastructure, not control.

Section VI carries the Industry Player Routing Layer and Decision Matrix — the operational translation of the system-level analysis into corridor-selection tradeoffs, observed routing patterns across the five firm archetypes, and concrete pivot triggers that will drive corridor repositioning. Full MindCast AI Proprietary Cognitive Digital Twin (MAP CDT) Foresight Simulation output — MindCast’s predictive behavioral economics and game theory simulation architecture — and Vision Function analysis appear in the Appendix.

I. Legality as Contested Equilibrium

The CFTC layer defines whether event contracts fall within federal derivatives jurisdiction. The determination establishes the boundary between permissible and prohibited market formation. The Third Circuit’s April 6, 2026 decision in KalshiEX LLC v. Flaherty and parallel litigation confirm the boundary is not stable. Strategic forum selection, private class actions, and federal preemption claims actively contest it — including the April 2, 2026 joint U.S. Department of Justice (DOJ)-CFTC Supremacy Clause action against Arizona, Illinois, and Connecticut.

Legality is a contested equilibrium reached through litigation, delay, and jurisdictional conflict rather than a fixed state.

Causal chain at the legality layer: Definitional gap (”gaming” undefined) → CFTC asserts jurisdiction without completing rulemaking → private plaintiffs and state attorneys general exploit the gap → enforcement multiplies across forums → classification question migrates to courts under Loper Bright independent judgment.

The private enforcement track illustrates why legality is insufficient. Kaiserman v. Kalshi Inc., No. 1:26-cv-01525-VMC (N.D. Ga., filed March 20, 2026), invokes the Commodity Exchange Act (CEA) private right of action under 7 U.S.C. § 25(b) against KalshiEX LLC, its corporate parents, and three named executive officers, alleging direct violations of CFTC Rule 40.11 regardless of the outcome of pending preemption appeals. Damages accrue under an unamended federal rule whose governing definition the CFTC itself acknowledges is open. MindCast’s analysis of the private enforcement architecture appears in MindCast: The Rule 40.11 Paradox — Kalshi, the Third Circuit, and the Class Action the Ninth Circuit Cannot Ignore (April 9, 2026), which documents how the Third Circuit’s April 6 preemption holding preserves the ambiguity Kaiserman converts into damages.

State-level enforcement against distribution partners operates on the same track. On April 21, 2026, New York Attorney General Letitia James filed parallel actions in Manhattan state court against Coinbase Financial Markets, Inc. and Gemini Titan LLC, seeking $2.2 billion in damages from Coinbase and a minimum of $1.2 billion from Gemini for operating prediction markets without New York State Gaming Commission licenses. Press Release, Office of the New York State Attorney General, Attorney General James Sues Coinbase and Gemini for Running Illegal Gambling Platforms in New York (April 21, 2026). The actions target the parent cryptocurrency exchanges and their CFTC-registered affiliates simultaneously. The New York theory does not require the state to prevail on swap classification. The theory requires only that the state’s gambling licensing framework reach the platforms operating without it — a theory preemption doctrine may address but cannot foreclose.

Falsification condition at the legality layer: If the Ninth Circuit or the Supreme Court resolves swap classification decisively and forecloses parallel state and private federal enforcement, the legality layer stabilizes and the contested-equilibrium framing weakens.

Even if the CFTC prevails in asserting jurisdiction, the outcome answers only whether prediction markets can exist. It does not determine whether those markets can clear, scale, or function in real time.

Legal permission does not produce operational capacity.

II. Structure as Constraint Geometry

Treasury’s stablecoin framework — anchored by the GENIUS Act — adopts coordination across state regimes rather than categorical federal preemption. The choice creates a constrained competitive landscape in which firms select jurisdictional pathways based on licensing friction, compliance cost, and regulatory posture.

The architecture is not harmonization. It is managed fragmentation.

Causal chain at the structure layer: Dual-regime architecture (federal plus state) → “substantially similar” standard still under construction → state regulators design corridors → firms route through corridors based on capital-access calculation → corridor dominance emerges as smaller set of states captures majority flow.

Under the structure, firms do not choose legality. They choose paths through regulatory geometry. Each state regime defines a corridor of permissible operation, and firms route through corridors that minimize constraint while preserving access to institutional capital. New York’s April 21, 2026 enforcement action against Coinbase and Gemini Titan demonstrates the corridor mechanism operating in real time: the state has defined its permissible corridor to exclude prediction markets operating without Gaming Commission licensing, regardless of CFTC registration status, and has priced the exclusion at $3.4 billion in combined sought damages.

Prediction markets follow the same logic. Platforms that align with compliant stablecoin regimes gain access to settlement infrastructure. Platforms that do not lose access to scalable capital flows regardless of legal classification.

Structure therefore determines not just where firms operate, but which firms survive. For issuers and platforms, the choice of state regime is not a compliance decision. It is a capital-access decision that determines whether the platform can integrate with compliant settlement rails and onboard institutional liquidity.

K&L Gates identified the DASP consolidation advantage as the most operationally consequential strategic reason for the state pathway: existing state digital asset service provider licenses can function as GENIUS Act-compliant pathways once Treasury certifies the state law as substantially similar, allowing vertically integrated virtual currency platforms to consolidate regulatory oversight rather than navigate parallel federal and state regimes for different components of the same business. The managed-fragmentation framework extends that insight by mapping why the resulting equilibrium favors corridor selection over race-to-the-bottom competition: Treasury’s “substantially similar” requirement forecloses standards-lowering while state DASP architecture forecloses issuer-by-issuer federalization, producing a geometry in which a small number of well-administered state corridors will capture disproportionate issuer volume.

Falsification condition at the structure layer: If stablecoin issuers voluntarily choose federal qualified payment stablecoin issuer (FQPSI) charters early and avoid state-qualified payment stablecoin issuer (SQPSI) pathways, the managed-fragmentation thesis weakens and the corridor-routing prediction fails under observed market behavior.

III. Execution as Feedback Loop Driver

The AML/CFT framework functions as runtime control over the financial system. Treasury’s April 8, 2026 joint Financial Crimes Enforcement Network (FinCEN) / Office of Foreign Assets Control (OFAC) Notice of Proposed Rulemaking (NPRM) — Docket FINCEN-2026-0100, RIN 1506-AB73 — governs identity, transaction approval, monitoring, and reporting for permitted payment stablecoin issuers (PPSIs). The controls slow capital movement by design.

In traditional financial systems, friction is a compliance cost. In real-time probabilistic markets, friction is a behavioral variable.

Causal chain at the execution layer: AML/CFT controls impose identity verification and transaction monitoring → latency enters the settlement path → information incorporation slows → liquidity fragments → price formation reflects regulatory structure rather than underlying information → platforms unable to compress latency lose institutional capital.

Prediction markets depend on rapid incorporation of information into prices. Price formation requires immediate capital entry, continuous position adjustment, and low-latency transaction clearing. AML/CFT requirements alter each condition: identity verification gates participation, monitoring and screening introduce delays, compliance thresholds shape transaction size and frequency. The result is not neutral regulation. It modifies market microstructure.

Three specific Treasury proposals illustrate the execution-layer mechanism. First, the primary-secondary market distinction at 31 CFR 1033.320 creates asymmetric Suspicious Activity Report (SAR) filing obligations, requiring PPSIs to file SARs on primary market activity but not on secondary market activity. The on-chain transactional layer — where prediction market settlement primarily occurs — operates with reduced monitoring density compared to the issuance-redemption layer. Second, the lawful order technical capabilities requirement at 31 CFR 1033.240(b) mandates that PPSIs maintain technical capabilities, policies, and procedures to comply with the terms of any lawful order without fully defining the scope of qualifying issuing authorities. The mandate embeds federal control primitives directly into smart contract architecture while leaving the procedural architecture open. Third, the money services business (MSB) carve-out for PPSIs at 31 CFR 1010.100(ff) removes the category from the existing MSB framework while establishing PPSIs as a new type of financial institution under the Bank Secrecy Act (BSA) at 31 U.S.C. 5312(a)(2)(Y). The classification choice determines which existing BSA compliance infrastructure applies by default and which infrastructure firms must purpose-build.

Latency becomes the governing variable. Institutional capital does not outcompete slow markets — it bypasses them. When transaction latency increases, information incorporation slows. When participation is gated, liquidity fragments. When monitoring thresholds shape behavior, price formation reflects regulatory structure as much as underlying information. Compliance architecture becomes a competitive variable. AML/CFT design choices determine participation composition, liquidity depth, and therefore pricing accuracy across every platform operating or entering prediction markets.

Falsification condition at the execution layer: If compliant platforms reduce settlement latency to parity with offshore venues through pre-cleared identities, risk-scored wallets, or faster monitoring pipelines, the latency-bifurcation prediction fails and execution ceases to be the dominant control surface.

Contact mcai@mindcast-ai.com to partner with us on Predictive Law and Behavioral Economics + Game Theory Foresight Simulations. To deep dive on MindCast upload the URL of this publication into any LLM (preferably ChatGPT or Gemini for magazine style works) and prompt ‘reconstruct MindCast framework with three degrees of cited sub links.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure.

About MindCast AI

MindCast is a predictive behavioral economics and game theory artificial intelligence firm specializing in complex litigation, geopolitical risk intelligence, and innovation ecosystems. MindCast publishes falsifiable institutional foresight analysis at mindcast-ai.com.

The firm’s active docket filing on federal digital-asset rulemaking is MindCast Defining “Gaming” Under the Commodity Exchange Act, The Rule 40.11 Gap Driving the Nationwide Kalshi Litigation Web (April 17, 2026) (CFTC RIN 3038-AF65).

IV. The Closed-Loop System: Four Structural Coherence Risks Across CFTC, State-Regime, and AML/CFT Rulemakings

Stablecoin regulation and prediction market regulation operate within a shared feedback system and resist evaluation as separate domains.

Market behavior generates transaction flows. Transaction flows trigger monitoring and enforcement. Enforcement alters participant behavior. Behavioral changes reshape market outputs. The system operates as a closed loop.

Control does not arise from rules alone. Control arises from feedback capture and response speed. Treasury’s AML/CFT framework increases feedback capture. State regimes define where the feedback applies. CFTC jurisdiction determines which activities fall within the system. Together, they produce a cybernetic control architecture over probabilistic markets.

The critical variable is not rule content. The critical variable is feedback latency.

Four structural coherence risks appear across the three federal rulemakings currently open. Each rulemaking can avoid the risk by addressing it in the final rule. Each rulemaking will produce the risk if the final rule leaves the coherence question unaddressed.

First, the definitional risk transfers across statutes. “Gaming” under CFTC Rule 40.11 remains undefined while the CFTC asserts jurisdiction — the governing defect MindCast addressed in MindCast Defining “Gaming” Under the Commodity Exchange Act, The Rule 40.11 Gap Driving the Nationwide Kalshi Litigation Web (April 17, 2026) (CFTC RIN 3038-AF65). “Substantially similar” under the state-regime NPRM remains under construction while Treasury invites states to pursue certification. “Lawful order” under the AML/CFT NPRM specifies federal issuing authorities without fully resolving the status of state-law orders.

Second, the approval-architecture risk transfers. The CFTC’s Rule 40.2(a)(2) passive non-disapproval mechanism, Treasury’s proposed state-regime certification through substantially-similar principles, and Treasury’s proposed MSB carve-out for PPSIs each establish regulatory authority over a novel category of activity through a passive or architectural mechanism rather than affirmative case-by-case review. Architectural approval mechanisms create predictable enforcement gaps that compound as the regulated activity scales.

Third, the non-displacement risk transfers. The CFTC’s Rule 40.11 prohibition operates alongside state gambling law; the relationship between them is the core question in the Kalshi litigation web. The Treasury state-regime certification operates alongside state digital asset service provider (DASP) and money transmitter law; the relationship between them is the institutional question identified by K&L Gates in Crowder, McLaughlin, and Durham, Treasury Proposes Framework for State Stablecoin Laws—Should You Issue Under a State Regime?. The Treasury AML/CFT program requirements operate alongside state consumer protection and financial services law; follow-on enforcement litigation will test that relationship directly.

Fourth, administrative-law constraint geometry governs each rulemaking. Chenery, State Farm, Encino Motorcars, and Loper Bright operate as structural constraints on the deference available to any completed rule. The deference posture each agency takes in the final rule, including the completeness of the deliberative record, determines how judicial review treats the rule.

V. Firm-Level Behavior: How Actors Adapt

Firms are already adapting to the three-layer system. Each adaptation is a routing decision, not a compliance decision.

Polymarket routes settlement through USDC on offshore infrastructure to preserve execution latency outside the CEA framework entirely. The adaptation prioritizes execution speed over domestic regulatory perimeter.

Kalshi operates inside the domestic regulatory perimeter but depends on U.S. dollar banking rails that cannot match the continuous-position-adjustment latency stablecoin settlement provides. The platform’s voluntary March 2026 contract screening — accepting behavioral constraints no court ordered — revealed internal recognition of the latency constraint before any regulator or court forced the issue.

Coinbase launched Coinbase Financial Markets as a separate CFTC-regulated entity to isolate prediction market exposure from the broader exchange. The adaptation segregates the high-risk product line into a regulated envelope while preserving the parent entity’s institutional standing.

Gemini spun out Gemini Titan as a CFTC-approved designated contract market in December 2025. The separation is the same move as Coinbase’s, executed through a different corporate structure.

Robinhood routes event contracts through its CFTC-registered Futures Commission Merchant to align with federal derivatives jurisdiction while preserving retail distribution. The adaptation uses federal preemption as a shield against state enforcement without subjecting the entire retail platform to derivatives-specific compliance.

Each firm faces the same system and makes the same category of routing choice: select the corridor through regulatory geometry that preserves execution capacity and minimizes identity friction at the participation gate. The choices differ in specifics but converge on a single pattern. The firms that select corridors aligned with compliant, low-latency settlement infrastructure gain access to institutional capital. The firms that cannot align with such infrastructure face bypass rather than gradual decline.

VI. Industry Player Routing Layer and Decision Matrix

The preceding sections model system-level behavior across legality, structure, and execution. Industry players — platforms, issuers, and state regulators — do not operate at the system level. They operate at the decision level under time, capital, and risk constraints. Section VI translates the structural analysis into a decision framework: routing choices, tradeoffs, and failure conditions MindCast observes across the five adaptation patterns in Section V. The patterns describe observed market behavior under the constraint geometry Sections I through IV map, not legal advice.

Issuer Decision Matrix Under Latency and Corridor Constraints

Markets select regulatory pathways based on capital accessibility at acceptable latency under survivable litigation risk, not formal legality.

Observed Routing Patterns by Platform Type

MindCast observes five routing patterns across the firm archetypes analyzed in Section V. Each pattern carries a governing rationale, a pivot trigger, and a failure mode.

Coinbase-type institutional exchange. The observed pattern anchors in a federal or State Tier 1 corridor while maintaining parallel low-latency infrastructure. The governing rationale is that institutional capital requires regulatory credibility while execution competitiveness requires latency hedging. The pivot trigger is compliant settlement latency compressing below roughly two minutes, at which point the anchor consolidates and the parallel infrastructure retires. The failure mode under wrong routing is overcommitting to a high-latency compliant stack without latency compression, producing institutional retention but loss of price leadership, user migration to faster venues, volume share erosion, and revenue compression across the derivatives product line.

Robinhood-type retail distribution platform. The observed pattern consolidates under federal derivatives jurisdiction and compliant stablecoin rails. The governing rationale is that retail scale depends on regulatory clarity and trust rather than marginal latency advantage. The pivot trigger is escalation of state enforcement against distribution channels, at which point the consolidation may require geographic retrenchment. The failure mode under wrong routing is fragmenting across state corridors, which introduces compliance drag and litigation exposure that erodes user trust, reduces retail funnel conversion, compresses customer lifetime value, and translates into valuation multiple contraction across the core brokerage platform.

Gemini-type hybrid structure. The observed pattern maintains structural separation between the regulated derivatives entity and the broader platform, preserving optionality to shift settlement rails as conditions evolve. The governing rationale is that cross-domain litigation will target interfaces between entities rather than entities themselves; separation preserves adaptability and reduces contagion risk. The pivot trigger is emergence of multi-domain litigation spanning derivatives, payments, and securities, at which point the separation may require additional layers. The failure mode under wrong routing is tight coupling of entities, which exposes the entire platform to cross-domain enforcement, increases systemic legal risk, depresses enterprise valuation through contagion pricing, and reduces access to the settlement fee pool that cross-product integration otherwise unlocks.

Stablecoin issuer routing. The observed pattern selects the corridor based on target capital base. Institutional-capital targets route through the federal FQPSI pathway. Hybrid targets route through State Tier 1 SQPSI pathways. Speed-first targets route through State Tier 2 with a defined exit strategy to a higher tier as volume crosses thresholds. The governing rationale is that the dominant issuer minimizes latency while preserving access to the capital corridor matching its target base. The pivot trigger is capital concentration into a small number of compliant rails, at which point Tier 2 issuers face migration pressure. The failure mode under wrong routing is selecting a low-latency corridor without long-term regulatory durability, producing forced migration under enforcement pressure, destruction of network effects accumulated in the original corridor, float revenue loss during transition, and token valuation compression as reserve-asset confidence and settlement-layer utility both degrade.

State regulator competitive positioning. The observed pattern designs corridors with clear rules and faster approval cycles to attract issuer capital. The governing rationale is that capital flows toward predictable and efficient regulatory pathways, and well-administered corridors capture disproportionate issuer volume. The pivot trigger is observable avoidance by major issuers or platforms, at which point the regime may require substantive recalibration. The failure mode under wrong positioning is overly restrictive or ambiguous regime design, which causes capital bypass, erodes the state’s digital-asset tax base, reduces jurisdictional standing in future federal-state regulatory coordination, and forfeits the compounding financial-services cluster benefits that dominant state corridors will accumulate over the 12 to 36 month corridor consolidation window.

The Governing Tradeoff

Federal pathways maximize capital density and long-term stability but impose early latency costs. State pathways offer initial flexibility and speed but carry higher long-term enforcement and fragmentation exposure.

The governing tradeoff is not federal versus state. The governing tradeoff is latency versus capital density under enforcement uncertainty.

Concrete Pivot Triggers

Four observable market events will trigger corridor repositioning across the five adaptation patterns:

Latency Compression Event. Compliant settlement latency falls below roughly two minutes. Trigger response: consolidation into regulated rails as the execution penalty for compliance disappears.

Enforcement Convergence Event. Simultaneous federal and state actions against the same platform or product category. Trigger response: collapse of weaker corridors and acceleration of capital into stronger ones.

Capital Concentration Event. Majority issuance volume concentrates in a small number of issuers or rails. Trigger response: corridor lock-in, with late entrants facing increasing friction to access institutional flow.

Judicial Clarification Event. Appellate resolution stabilizes the swap-classification question. Trigger response: execution layer becomes the dominant control surface as the legality layer stabilizes.

The framework converts system description into decision infrastructure. Institutional readers can map regulatory corridors against measurable tradeoffs, anticipate the conditions under which firm strategy must pivot, and identify failure conditions before they materialize.

VII. Foresight Simulation Predictions

MindCast produces the foresight predictions in this section through the MindCast AI Proprietary Cognitive Digital Twin (MAP CDT) Foresight Simulation architecture — a predictive behavioral economics and game theory framework that integrates three analytical traditions.

The first is law and behavioral economics (MindCast Chicago School Accelerated — The Integrated, Modernized Framework of Chicago Law and Behavioral Economics), which treats institutional actors — agencies, courts, firms, plaintiffs — as rational agents responding to incentive structures under information constraints.

The second is strategic game theory applied to multi-agent regulatory environments, which identifies equilibrium behaviors under rule mutability, forum selection, and delay dominance rather than within fixed statutory regimes (MindCast Predictive Game Theory AI vs. Market Predictive AI— Structural Foresight in Institutional Systems).

The third is cybernetic control theory (MindCast Predictive Cybernetics Suite | Cybernetic Game Theory), which models how feedback loops capture, process, and act on signals to shape system behavior over time.

The combination produces falsifiable predictions with specified timelines, probability bands, mechanisms, and observable indicators. Each prediction carries an explicit falsification condition against which market behavior can be measured. The methodology disclosure appears in the Appendix; the Vision Function outputs — four parallel analytical routings that measure feedback capture, strategic delay dynamics, constraint geometry, and regime classification — document the analytical pathway that produced each prediction.

Applied to the federal digital-asset control architecture, the framework yields six falsifiable predictions — three primary, three secondary — that together describe how the system resolves over the next 6 to 36 months. Four system-level invariants hold across the six prediction paths. Each invariant describes structural behavior that emerges regardless of which specific prediction resolves which way:

Feedback latency governs all outcomes. Whether enforcement migrates to runtime controls (Prediction 1), markets bifurcate by compliance latency (Prediction 3), or vendors compress settlement times through latency-compression infrastructure (Prediction 6), feedback latency operates as the dominant control variable. Statutory classification is downstream of feedback latency dynamics.

Corridor dominance replaces open competition. Firms navigate constrained regulatory corridors rather than optimize freely across a fragmented regime map. A small number of well-administered corridors — federal, state, or hybrid — capture disproportionate institutional flow. The corridor geometry persists regardless of whether federal preemption wins, hybrid resolution emerges, or persistent fragmentation continues.

Classification deferral generates enforcement rather than suspending it. Private plaintiffs under 7 U.S.C. § 25(b), state attorneys general under gambling licensing frameworks, and federal preemption litigation all operate independently of classification resolution. Deferral generates liability on parallel tracks; resolution would merely redistribute it. The Kaiserman and NY v. Coinbase/Gemini Titan actions demonstrate the invariant in live operation.

Infrastructure supersedes statute. Settlement rails, identity verification architecture, transaction monitoring pipelines, and lawful-order technical capabilities determine platform outcomes regardless of statutory perimeter. The regulated entity that controls superior execution infrastructure dominates the regulatory regime it operates within; the regulated entity with inferior infrastructure is bypassed regardless of nominal legality.

The invariants hold even if all six predictions fail simultaneously. Any alternate resolution must satisfy the four structural claims or reveal an unanticipated system state.

The invariants produce a single directional conclusion. The governing conflict will move from legality to control of infrastructure. Capital does not wait for regulatory clarity; it routes to execution environments that already function.

The bypass prediction is the consequential one. Platforms that cannot reduce execution latency below the threshold institutional capital requires will not fail gradually through regulatory pressure — capital will route to settlement infrastructure that can, bypassing the slower platforms entirely. Polymarket’s offshore USDC settlement already operates as the live demonstration. Every domestic platform unable to integrate compliant stablecoin settlement faces the same bypass geometry regardless of legal classification. Markets that cannot clear at the speed institutional liquidity requires do not win delayed fights over jurisdiction; they lose the liquidity itself.

The forward equilibrium resolves through a two-stage convergence loop. Stage 1 is the current fragmentation: states experiment at the structure layer through GENIUS Act certification while federal agencies assert at the legality layer through CFTC preemption litigation. Stage 2 is collapse into one of two terminal configurations — either one layer wins preemption outright, or a hybrid regime emerges with federal baseline and state execution. The Kalshi litigation web is running Stage 1 to Stage 2 convergence in derivatives. The GENIUS Act rulemakings are the Stage 1 setup for the same convergence in stablecoins. The same platforms — Coinbase, Robinhood, Gemini — sit in both systems and will face both convergence trajectories simultaneously. New York’s April 21, 2026 actions against Coinbase Financial Markets and Gemini Titan are the first observable Stage 1 to Stage 2 acceleration event in the stablecoin-adjacent ecosystem.

Primary Predictions

Three primary predictions anchor the 6 to 24 month resolution window. Each operates on a different time horizon and tests a different layer of the three-layer control architecture. Each carries a specific mechanism, observable indicators, and falsification condition that market behavior will either validate or refute on a measurable timeline.

Prediction 1 — Execution Dominance Transition (6–12 months, 75% probability). Agencies will shift enforcement from classification disputes to runtime controls: know-your-customer gating, transaction monitoring, and freeze/deny technical capabilities. The shift occurs because classification litigation produces contested outcomes while execution-layer enforcement produces measurable compliance behavior — regulators optimize for enforcement mechanisms that produce reliable outputs. Platforms redesign onboarding, order routing, and settlement architectures to satisfy the control hooks rather than continue litigating definitional questions.

Mechanism. The CFTC’s Rule 40.11 posture, Treasury’s AML/CFT lawful-order mandate at 31 CFR 1033.240(b), and FinCEN’s SAR asymmetry at 31 CFR 1033.320 each push enforcement weight toward transaction-layer controls. Agency attention follows enforcement leverage. As the three rulemakings complete their comment windows and move toward final rules, the execution-layer provisions harden faster than the classification-layer provisions because execution provisions are technical specifications while classification provisions are doctrinal determinations subject to judicial review.

Observable indicators. At least a 30% increase in enforcement actions citing AML/CFT compliance failures rather than derivatives classification failures within 12 months; compliant venues extend platform onboarding times from under two minutes to over five minutes as identity verification requirements harden; regulated platforms push settlement latency to at least two times baseline as screening and monitoring requirements compound; agency guidance — speeches, no-action letters, enforcement manuals — emphasizes “lawful order” compliance and technical capabilities rather than swap-classification doctrine.

Falsification. Prediction 1 fails if courts or agencies resolve swap classification decisively and then deprioritize AML/CFT enforcement for these products, or if measurable identity-gating and transaction-delay increases fail to materialize on compliant platforms within the 12-month window.

Prediction 2 — Stablecoin Corridor Consolidation (12–24 months, 70% probability). Capital will concentrate in a small set of compliant stablecoin regimes — federal FQPSI or State Tier 1 SQPSI — that offer acceptable latency combined with regulatory clarity. Non-aligned platforms lose institutional flow regardless of nominal legality. Institutional capital drives the consolidation through its preference for corridors that provide both settlement infrastructure and litigation predictability, and only a handful of regimes will supply both at scale.

Mechanism. The GENIUS Act’s “substantially similar” certification architecture produces a state-level equilibrium in which a small number of well-administered regimes capture disproportionate issuer volume — the Delaware-style regulatory competition K&L Gates identified. Institutional capital routes through these dominant corridors because corridor dominance itself reduces the risk of forced migration under enforcement pressure. The corridor selection operates as a capital-access decision rather than a compliance decision.

Observable indicators. At least 60% of compliant prediction market and payment volume concentrates in three or fewer stablecoin rails within 18 months; exclusive or preferred settlement partnerships form between top platforms and dominant issuers; at least 50% of new entrants select two or three dominant state or federal regimes rather than distributing across the full available regime map; regulatory capital (examiner expertise, supervisory technology investment, enforcement staff) concentrates in the same dominant corridors.

Falsification. Prediction 2 fails if persistent fragmentation produces no dominant rails and institutional capital flows distribute evenly across many regimes, or if the K&L Gates DASP consolidation advantage fails to produce observable corridor concentration within 24 months. Prediction 2 also fails if stablecoin issuers voluntarily choose federal FQPSI charters early and avoid state SQPSI pathways, which would falsify the managed-fragmentation thesis from the structure side.

Prediction 3 — Latency-Driven Market Bifurcation (9–18 months, 65% probability). Markets will split into compliant high-latency venues with institutional access and low-latency offshore or lightly regulated venues with faster execution. Price discovery diverges between the two market tiers under different latency profiles, and the bifurcation becomes self-reinforcing as liquidity migrates toward the corridor that matches the specific capital type seeking execution. The bypass geometry identified in Section III produces the split as its direct observable consequence.

Mechanism. AML/CFT friction operates as a latency injection that modifies market microstructure rather than as a compliance cost borne equally across venues. Institutional capital tolerates latency when paired with regulatory credibility and capital density; retail and informed-trader capital tolerates compliance minimalism when paired with execution speed. The two capital types segregate to the corridors matching their latency preferences, producing two distinct price discovery processes operating on the same events.

Observable indicators. Price divergence of 3% to 5% or greater between compliant and offshore markets during high-volatility events such as major sports finals, election nights, or macroeconomic release dates; at least 20% user migration to lower-latency platforms within 12 months of stricter compliance rollout on regulated venues; measurable increase in slippage and reduced liquidity depth on compliant venues at settlement windows; growth of derivative products (basis trades, spread positions) that arbitrage the latency gap between compliant and non-compliant venues.

Falsification. Prediction 3 fails if latency converges across venues through technology compression (the Prediction 6 scenario) or through regulatory harmonization that reduces compliance friction, or if no sustained price divergence emerges despite differing compliance frictions during the 18-month observation window.

Secondary Predictions

Three further predictions follow from the same system architecture. Each tests a different consequence of the Stage 1 to Stage 2 convergence dynamic on a distinct time horizon.

Prediction 4 — Cross-Domain Litigation Expansion (3–9 months, 60% probability). Plaintiffs’ bars and state attorneys general will file cases that bundle derivatives, payments, and securities theories to exploit definitional seams across agencies. A single digital-asset platform operates under the CFTC for derivatives, Treasury for stablecoins, and state authorities for consumer protection; each statutory regime carries its own enforcement mechanism independent of the others, and cross-domain complaints convert that structural independence into parallel litigation exposure. The NY v. Coinbase/Gemini Titan action filed April 21, 2026 is the initial data point. Cross-domain filings become the dominant enforcement pattern as plaintiffs recognize that definitional ambiguity across three rulemakings creates arbitrage across statutory regimes.

Observable indicators. At least 25% of new litigation filings include multi-domain claims spanning two or more statutory regimes; parallel filings target both platform operators and payment/settlement affiliates simultaneously; plaintiffs’ firms develop template complaints that bundle CFTC Rule 40.11, state gambling licensing, and state consumer protection theories.

Falsification. Prediction 4 fails if litigation remains siloed within single statutes without cross-domain claims, or if the NY v. Coinbase/Gemini Titan action produces an early settlement that deters rather than encourages follow-on filings.

Prediction 5 — Regime Collapse into Hybrid Control Structure (18–36 months, 55% probability). Federal baseline standards on AML/CFT compliance and core definitions will combine with state execution on licensing and corridor enforcement to produce a layered control structure rather than a single-winner outcome. Preemption disputes resolve into layered authority because neither pure federal preemption nor pure state preservation satisfies the institutional actors operating the system — federal agencies want baseline control over digital-asset architecture while state regulators want jurisdictional authority over activities inside their borders. The hybrid outcome is the Nash equilibrium of the federal-state negotiation, not an idealized regulatory design.

Observable indicators. Federal rulemaking explicitly incorporates state certification frameworks under the GENIUS Act “substantially similar” mechanism; at least two appellate decisions affirm partial state authority within a federal baseline rather than displacing state authority entirely; interagency coordination frameworks (MOUs, joint guidance, shared examination programs) emerge between federal and state regulators on digital-asset issues.

Falsification. Prediction 5 fails if clear federal preemption displaces state regimes entirely (single-winner federal outcome), or if state authority preservation displaces federal authority on digital-asset activities (single-winner state outcome). Prediction 5 also fails if the federal-state negotiation collapses into sustained jurisdictional conflict with no convergence on layered authority within 36 months.

Prediction 6 — Feedback Latency Compression Arms Race (6–18 months, 70% probability). Platforms will invest in compliance-speed infrastructure — pre-cleared identities, risk-scored wallets, faster monitoring pipelines — to reduce effective latency while remaining compliant. The investment reshapes the compliance vendor market and determines which platforms survive the bypass geometry identified in Section III. Platforms that succeed at latency compression inherit institutional capital that would otherwise route offshore; platforms that fail become bypassed venues regardless of regulatory standing.

Observable indicators. Reduction in compliant settlement latency from over five minutes to under two minutes during the observation window; at least 40% growth in the AML/CFT acceleration and identity verification vendor market as platforms purchase the infrastructure to compress latency; platform marketing materials explicitly highlight “instant compliant settlement” or equivalent language as a competitive differentiator; vendor acquisitions by regulated platforms accelerate as speed becomes the decisive capability.

Falsification. Prediction 6 fails if no measurable improvement in compliant settlement times occurs despite vendor-market investment, and the latency gap between compliant and offshore venues widens rather than compresses. Prediction 6 also fails if regulators intervene to standardize latency-compression technology and remove it as a competitive variable.

Regulatory Implications

Four structural priorities emerge for the three open rulemakings:

Define key terms before operational mandates (e.g., complete the scope of “lawful order” prior to imposing technical capabilities requirements).

Replace passive or architectural approval with targeted affirmative review for novel activities that affect system stability.

Clarify non-displacement between federal AML/CFT obligations and state financial and consumer protection law to reduce cross-forum conflict.

Evaluate latency impacts of monitoring and reporting on real-time market microstructure and price formation.

VIII. Conclusion

Federal digital-asset regulation has stopped operating as three separate rulemakings and started operating as one control architecture. The CFTC prediction markets docket, the Treasury GENIUS Act state-regime NPRM, and the Treasury FinCEN/OFAC AML/CFT NPRM govern the same platforms, address the same institutional actors, and produce the same structural defect — authority asserted before deliberation completes. Kalshi, Coinbase, and Gemini face the same regulatory problem not because the three rulemakings coordinate their approach, but because the three platforms route through a single closed-loop system governed by feedback latency, corridor selection, and execution infrastructure.

The legality layer establishes whether markets may exist. The structure layer determines which corridors firms route through. The execution layer determines whether markets can clear under real-time institutional demand. Together, the three layers produce a cybernetic control architecture in which classification battles are downstream of feedback dynamics. The framework identifies four system-level invariants that hold regardless of which specific prediction resolves which way: feedback latency governs all outcomes; corridor dominance replaces open competition; classification deferral generates enforcement rather than suspending it; and infrastructure supersedes statute. The six falsifiable predictions in Section VII — three primary, three secondary, across 3 to 36 month horizons — describe how the system resolves under those invariants.

The behavioral observation is already empirically visible. Polymarket routes settlement offshore through USDC to preserve execution latency outside the CEA framework. Kalshi operates inside the domestic regulatory perimeter but depends on U.S. dollar banking rails that cannot match stablecoin settlement latency — the voluntary March 2026 contract screening reveals the internal recognition of that constraint. Coinbase isolated prediction market exposure in Coinbase Financial Markets. Gemini spun out Gemini Titan as a designated contract market. Robinhood routes event contracts through its CFTC-registered Futures Commission Merchant. Each adaptation is the same move: select the corridor through regulatory geometry that preserves execution capacity and minimizes identity friction at the participation gate. The corridor-routing behavior Section II predicts is not a forecast. It is the current state of the system, now accelerating as the three rulemakings move toward final rule and enforcement.

What Completes the Architecture

Four structural priorities follow for the three open rulemakings. Each maps to a coherence risk identified in Section IV and to a structural condition under which federal digital-asset regulation survives the judicial scrutiny Loper Bright, Chenery, State Farm, and Encino Motorcars will apply to any subsequent enforcement action:

Define key terms before operational mandates. Complete the scope of “gaming” under CFTC Rule 40.11, “substantially similar” under the state-regime NPRM, and “lawful order” under the AML/CFT NPRM prior to issuing final rules that impose compliance obligations against those terms. Deferral generates litigation; definitional completion reduces it.

Replace passive or architectural approval with targeted affirmative review for novel activities that affect system stability. The CFTC’s Rule 40.2(a)(2) passive non-disapproval mechanism, Treasury’s state-regime substantially-similar certification, and Treasury’s PPSI MSB carve-out each establish regulatory authority through passive architecture rather than affirmative case-by-case review. Affirmative approval for novel activities closes the enforcement gaps that passive architecture leaves open.

Clarify non-displacement between federal AML/CFT obligations and state financial and consumer protection law. The NY v. Coinbase/Gemini Titan action demonstrates the cross-forum conflict that emerges when federal and state regulatory frameworks operate against the same activity without explicit non-displacement language. Each final rule should specify what the federal framework preempts and what it leaves to state authority.

Evaluate latency impacts of monitoring and reporting on real-time market microstructure and price formation. The primary-secondary market SAR asymmetry at 31 CFR 1033.320, the lawful-order technical capabilities mandate at 31 CFR 1033.240(b), and the PPSI identity-gating architecture each inject latency into settlement paths. Agency rulemaking that evaluates the microstructure consequences of latency injection will produce better-calibrated final rules than rulemaking that treats latency as a compliance cost alone.

The Governing Question

The regulatory question is no longer whether prediction markets are legal or whether stablecoins require oversight. The live question is control:

Who commands the feedback loops through which markets form, settle, and execute — and how latency, enforcement, and jurisdiction shape the information those markets produce.

No single agency can answer the question. Only the system level can. The three federal rulemakings currently open represent a coordinated opportunity to establish that system-level foundation. The same three rulemakings also represent a coordinated risk: if the coherence gaps remain unaddressed across all three dockets, the institutional output will be a federal digital-asset control architecture that fails the administrative-law standards the agencies themselves invoke when defending it — and the bypass geometry identified in Section III will accelerate through platforms and capital flows the federal system no longer governs.

The direction of the system is decided. The structural shape of it is not.

Appendix: Cognitive Digital Twin Foresight Simulation Output

The analysis above derives from MindCast’s MAP CDT Foresight Simulation architecture. The following appendix discloses the signal intake, triadic calibration, and vision function routing that produced the six predictions in Section VII.

Cognitive Digital Twin Flow

Signal Intake. Multi-agency rulemaking (CFTC prediction markets ANPRM RIN 3038-AF65; Treasury state-regime NPRM; FinCEN/OFAC AML/CFT NPRM Docket FINCEN-2026-0100). Parallel litigation (Kalshi appellate docket, Kaiserman class action, NY v. Coinbase/Gemini Titan, Arizona consolidated federal docket). Stablecoin regime fragmentation across GENIUS Act-authorized pathways. AML/CFT execution constraints at the primary-secondary market interface.

Triadic Calibration. Legal signals: unresolved definitions (”gaming”, “substantially similar”, “lawful order”). Behavioral signals: firm routing (Polymarket offshore, Coinbase subsidiary isolation, Kalshi contract screening), latency avoidance, jurisdictional arbitrage. Structural signals: state corridor selection, enforcement asymmetry across dockets, removal-and-consolidation procedural patterns.

Causal Signal Integrity (CSI). High. Consistent pattern across agencies — authority asserted before definitional completion. Reinforced by litigation behavior across Third Circuit, Ninth Circuit, and N.D. Ga. dockets, and by enforcement timing (NY AG action filed April 21, 2026 during active federal rulemakings).

Vision Function Routing. Cybernetic Control Vision (dominant). Chicago Strategic Game Theory (co-dominant). Field Geometry Reasoning (structural overlay). Game Regime Identification (classification layer).

Vision Function Outputs

Cybernetic Control Vision (CCV). CCV evaluates how feedback loops capture, process, and act on signals to shape system behavior over time by measuring feedback speed, adaptation, and behavioral lock-in.

Feedback Capture Rate (FCR): High — broad monitoring and enforcement signals across federal and state actors.

Adaptation Velocity (AV): Moderate — rulemaking incomplete, enforcement active.

Loop Closure Index (LCI): Partial — loops forming but not synchronized.

Behavioral Lock-In Coefficient (BLIC): Increasing — firms adapting observable routing choices to constraint.

Feedback Latency Index (FLI): Elevated — delay between rule issuance and enforcement activation.

Classification: Semi-closed loop trending toward closed-loop control.

Chicago Strategic Game Theory (CSGT). CSGT models strategic interaction under delay, rule mutability, and incomplete information where actors optimize across forums rather than within fixed rules.

Strategic Delay Preference Index (SDPI): High — agencies and firms exploit delay.

Rule Mutability Score (RMS): High — rules actively evolving across three rulemakings.

Information Set Resolution (ISR): Moderate — definitions incomplete.

Equilibrium Persistence Under Loss (EPUL): High — conflict persists despite inefficiency.

Equilibrium: delay-dominant system.

Field Geometry Reasoning (FGR). FGR detects when structural constraint geometry governs outcomes rather than intent or incentives.

Constraint Density (CD): High — dense regulatory constraints across federal and state layers.

Geodesic Availability Ratio (GAR): Low — few viable compliant paths.

Attractor Dominance Score (ADS): High — dominant corridors form around compliant low-latency settlement.

Intent-Outcome Decoupling Index (IODI): High — firm intent decoupled from outcome under constraint density.

Game Regime Identification (GRI). GRI classifies the operating environment based on constraint, latency, and feedback stability into regimes such as Arena, Fog, Labyrinth, or Trap.

Feedback Stability (FS): <1.5 — not fully stabilized.

Feedback Latency Index (FLI): High.

Corridor Width (CW): Narrow.

Regime: Labyrinth approaching Trap conditions.