MCAI Lex Vision: The Protect College Sports Act of 2026 — Federal NIL Salary Cap, Antitrust Immunity, and the Private Equity Blind Spot

Why Congress Fights the Last War in College Sports Antitrust

Visual Companion. Related works:

If the Protect College Sports Act Passes, Private Equity in College Sports Wins Differently (July 1, 2026) — Utah’s Crimson Brand Partners close validates the firm-formation thesis and shows why private capital migrates into compliant college-athletics operating companies whether or not the Protect College Sports Act passes.

The Protect College Sports Act of 2026 (S. 4668) Becomes a Compliance-Infrastructure Bill (June 30, 2026) — Shows how the reported Senate text hardened S. 4668 into a compliance-infrastructure bill, where clean documentation replaces the paycheck as the competitive edge and advantage keeps moving to the capital layer beneath it.

The Protect College Sports Act of 2026 — Federal NIL Salary Cap, Antitrust Immunity, and the Private Equity Blind Spot (June 2026) — Argues that the bill’s federal NIL salary cap and antitrust immunity discipline coordination among schools while leaving the private-equity capital-formation channel — the blind spot — untouched.

Private Equity, NIL, Antitrust, and the Firm-Formation Phase of College Athletics(January 2026) — Names the firm-formation phase of college athletics, forecasting advantage’s migration from coordination to capital, identifying Utah as the prototype, and projecting ten or more athletics operating companies within twenty-four months.

Executive Summary

The Protect College Sports Act of 2026 assumes college athletics remains a coordinated-association problem at the exact moment it is becoming a capital-allocation problem. The mismatch is the subject of this paper. The bill is the evidence.

Introduced May 27, 2026 as S. 4668 by Senators Cruz and Cantwell with Senators Schmitt and Coons, the bill restores coordination among institutions: a federal compensation cap, an antitrust exemption to enforce it, collective media-rights pooling, and uniform NIL and transfer rules. Every operative mechanism rests on one assumption — that competitive advantage in college sports flows from agreements among schools and conferences, and that the policy task is to discipline those agreements.

On June 18, 2026, the Senate Commerce Committee advanced the bill 19–9, as amended by a Cruz-Cantwell-Schmitt substitute, and sent it to the full Senate; a House companion, H.R. 9137, runs in parallel. Committee passage is not enactment — the Senate floor and the House still lie ahead — and the analysis below holds under every enactment outcome.

The assumption is becoming false. MindCast AI foresight modeling published in January 2026 identified a migration already underway: competitive advantage is moving from coordination to capital formation — from what schools agree to do collectively to what capitalized operating entities can finance independently. The University of Utah’s December 2025 athletics-LLC transaction, with minority private-equity participation reported above $400 million, is the prototype.

The bill governs the layer the advantage is leaving and says nothing about the layer it is entering. Worse, its media-pooling provisions may feed the very divergence it ignores. A statute that restores coordination as competitive advantage migrates away from coordination does not solve the wrong problem entirely. It solves yesterday’s problem while tomorrow’s compounds underneath it.

Five claims carry the argument, each with an explicit confidence band:

The bill confirms a MindCast AI structural prediction — the “conditional safe harbor” design principle named in September 2025 — establishing the modeling’s track record before it makes its harder claim. (Confidence ~90%.)

The bill’s operative core is a permanent, inflation-indexed federal salary cap, immunized against antitrust challenge and walled off from private enforcement: the coordination instrument, perfected. (Confidence ~95%, textual.)

The bill stays silent across all 124 sections on the capital-formation channel — athletics LLCs, private equity, firm formation — that the modeling identifies as the emerging source of divergence. (Confidence ~95% on the silence; ~75% on the framing.)

Media markets reinforce rather than offset the capital channel: collective rights pooling stabilizes distribution while audience economics concentrate value toward capitalized programs, turning a migration into a self-reinforcing equilibrium. (Confidence ~70%.)

If the athletics-LLC structure diffuses on the trajectory the modeling projects, the bill is not merely incomplete but structurally outdated on arrival, regulating a legal person the money and control will have left. (Confidence ~60%.)

The body runs the strategic game underneath the bill, traces the two reinforcing loops — capital and media — that compound competitive divergence, and shows what the migration means for each actor. Section X presents the foresight simulation that produces the paper’s predictions: seven actors, two interlocking loops, and nine forecasts run on the MindCast AI Proprietary Cognitive Digital Twin Predictive Game Theory Foresight Simulation System.

I. The Track Record, Briefly

Credibility precedes the harder argument, so establish it and move on.

In September 2025, MCAI Lex Vision: SAFE vs. SCORE Act — Which Path Should Define NCAA NIL? proposed a design principle: a conditional safe harbor, coupling antitrust immunity with enforceable equity benchmarks. The reasoning held that immunity without conditions repeats the failure of NCAA amateurism.

Section 118(c) of the bill instantiates the principle — an athletic association forfeits the antitrust exemption unless it has established rules implementing the statute’s athlete protections. Publication predated the bill by eight months and anticipated a Cruz–Cantwell compromise neither party had announced. (Confidence ~90%.)

The claim is anticipation, not influence. Whether any drafter read the report is unknowable and beside the point. Anticipation is observable and falsifiable; influence is neither, and a falsifiable-foresight practice trades only in the former.

One caveat travels with the hit, and it matters for everything below. The report framed conditional safe harbor as the athlete-first path. The enacted version adopts the conditional form while filling it with institution-favorable substance — the salary cap analyzed next. Structure predicted correctly; valence running toward institutions. Hold that tension, because it is the seam the rest of the paper opens.

The Procedural Story, Briefly

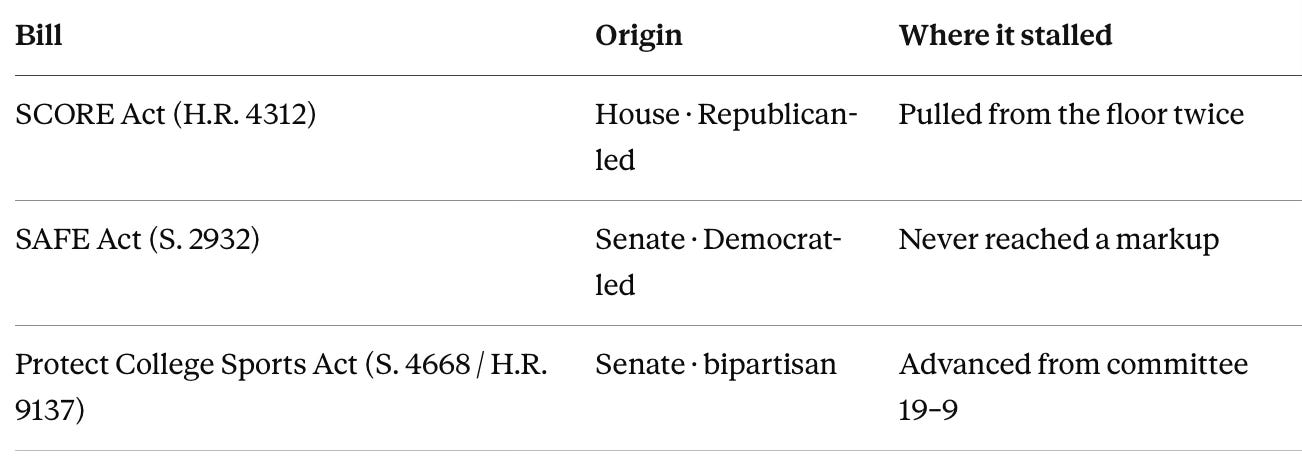

Two earlier frameworks died in the 119th Congress for opposite reasons, and the contrast explains why this one advanced. The SCORE Act (H.R. 4312), Republican-led, cleared its House committees and was pulled from the floor twice for lack of votes; the Democrat-led SAFE Act (S. 2932) never reached a markup.

The Protect College Sports Act survived because it was bipartisan from the first draft — co-authored by the committee Chair and Ranking Member, who control the markup — and because it folded the SAFE Act’s athlete protections into a SCORE-style antitrust structure, defusing both veto coalitions at once. The synthesis is the conditional-safe-harbor design this firm’s September 2025 analysis predicted. (Confidence on the bipartisan-authorship driver: ~85%.)

Committee speed is not passage: the bill still faces a sixty-vote Senate floor and a House that killed SCORE twice, the terrain Kyle Saunders’ PCSA whip-count memo maps. (Confidence the floor-and-House path stays uncertain: ~70%.) None of it changes the argument that follows. Whether the bill is enacted cleanly, attached to a vehicle, or stalls, the competitive frontier is moving the same direction — and the bill is aimed at the frontier the competition is leaving.

II. The Coordination Instrument, Perfected

The bill’s protections are real floors. The bill’s core is a ceiling. Both run on the same coordination logic, and the ceiling is the more revealing.

Sections 114 and 115 codify the “revenue share cap” — the Benefits Pool Limit from the settlement approved in In Re College Athlete NIL Legislation, No. 20-cv-03919 (N.D. Cal. June 6, 2025). Section 114 bars institutions, conferences, employees, and associated entities from arranging compensation that exceeds or circumvents the cap. Section 115 carries the cap forward with annual Consumer Price Index adjustment after the settlement expires. A ceiling born in private litigation becomes permanent federal law with an automatic escalator. (Confidence ~95%, textual.)

The cap’s genealogy is itself a MindCast AI foresight asset. In MCAI Lex Vision: the NCAA NIL Settlement, Foresight Realized (June 2025), the firm documented a May 2025 simulation that anticipated the settlement’s structure — the $2.8 billion figure, the roughly $20.5 million institutional pool, the retroactive liability to 2016 — one month before Judge Wilken’s approval. The cap the bill federalizes is the cap the report tracked at birth.

Section 118 immunizes enforcement of the cap from the antitrust laws. The grant carries the whole structure, because absent it, competing institutions collectively enforcing a ceiling on the price of labor describes a horizontal restraint — the paradigm of per se condemnation. The exemption is not incidental to athlete welfare; the exemption is the device converting a naked horizontal restraint into lawful conduct.

Section 119(b) then forecloses the private right of action from reaching that immunity. Athletes may sue to enforce the floors. Athletes may not sue to dismantle the ceiling. The cap sits doubly insulated.

Read structurally, the bargain is legible: enforceable floors traded for an antitrust-immune ceiling, with the legal channel to challenge the ceiling closed off. Calling the package “protection” is accurate on the floors and silent on the ceiling — the framing inversion MindCast AI catalogued in MCAI AI Lex Vision: Compass’ NCAA Analogy Is Backwards(September 2025), where a firm claiming the reformer’s mantle wrote itself into the gatekeeper’s role. The mechanism is identical: fairness rhetoric wrapping a control architecture.

Cap, immunity, and foreclosure all discipline what institutions do collectively. Each is the last war, fought well. The next war is not here.

III. The Last War and the Next One

The paper’s contribution begins here. Set the two battlefields side by side.

The old battleground is coordination. NCAA-wide compensation restraints, conference-wide restraints, and the settlement’s Benefits Pool Limit are each a horizontal arrangement — an agreement among competitors about the price or terms of athlete labor. Each emerges from collective rule. Antitrust plaintiffs have attacked each, in the tradition running from NCAA v. Board of Regents (1984) through NCAA v. Alston (2021), as a Sherman Act Section 1 conspiracy in restraint of trade. The Protect College Sports Act addresses the old battleground in full: it caps the restraint, immunizes the cap, and pools the media rights that fund it.

The new battleground is capital. Athletics limited-liability entities, private-equity minority capital, differential balance-sheet capacity, and firm formation share a defining trait — none is an agreement among competitors, none emerges from collective rule, and none presents a Section 1 conspiracy, because there is no conspiracy, only asymmetry. MCAI Lex Vision: Private Equity, NIL, Antitrust, and the Firm-Formation Phase of College Athletics (January 2026) modeled the migration directly. Section IV of that report forecast antitrust risk moving from horizontal wage restraints toward vertical capital stratification — durable competitive and labor-market asymmetry produced not by agreement or exclusion but by access to capital. Prediction 3 stated the litigation consequence: targets shift from the NCAA and conferences toward school-affiliated operating entities. (Original report confidence on Prediction 3: 65–75%.)

Old versus new is a structural split, not a cosmetic one, and three features make it so.

First, the two battlegrounds answer to different bodies of law. Coordination restraints are the natural prey of Section 1, built to detect agreements. Capital stratification produces its effects without agreement: a capitalized program gains advantage through superior capacity to offer stable, compliant, low-risk arrangements, not through any pact with rivals. Doctrine calibrated to the old battleground does not fit the new one.

Second, the bill’s cap does not bind capital. Section 114 limits what an institution may pay an athlete. The cap leaves untouched what a capitalized program may spend on the surrounding architecture — compliance systems, audit and documentation infrastructure, payment reliability, facilities, legal review — that sorts elite labor toward stable programs without any direct wage competition.

The bill’s own design widens that margin. By adding disclosure thresholds, fair-market-value review, and agent oversight, the statute converts compliance from a back-office cost into a competitive function. The January 2026 modeling forecast the shift in its Prediction 5: professionalized compliance becomes a moat, conferring financing capacity and lower enforcement risk, while informal operations carry higher exposure.

Capable record-keeping stops being overhead and starts being infrastructure. The ceiling constrains the headline number while the capital channel, armored by compliance capacity, reshapes the choice set beneath it. (Confidence ~70%.)

Third, and sharpest, capping direct pay may raise the relative value of capital-bought advantage. When every program faces the same ceiling on what it can pay, the differentiator stops being the offer and becomes the reliability and quality of everything around the offer — the things capital buys.

Section IV formalizes the mechanism; the intuition is Becker’s, that rational actors re-optimize around a price control rather than absorb it. By constraining one margin of competition, the bill intensifies competition on the unregulated margin it cannot reach. (Confidence ~60%; the second-order effect is plausible and untested.)

The migration thesis does not require the bill to fail. A bill that becomes law accelerates the relative-value dynamic. A bill that dies leaves the capital channel wholly ungoverned. The frame holds under every enactment outcome — the property that separates foresight from commentary.

Most analysis of this bill asks whether it is good for athletes. The better question is whether it is aimed at the right problem. On the evidence of its own text, it is aimed with precision at the problem of 2021.

Contact mcai@mindcast-ai.com to partner with us on Predictive Game Theory AI in Law and Behavioral Economics. To deep dive on MindCast works upload the URL of this publication into any LLM (preferably Google AI mode/Gemini, Claude, ChatGPT) and prompt ‘reconstruct MindCast framework with three degrees of cited sub links.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure.

Prior MindCast AI Work Referenced

MCAI Lex Vision: SAFE vs. SCORE Act — Which Path Should Define NCAA NIL? (September 2025)

MCAI Lex Vision: the NCAA NIL Settlement, Foresight Realized (June 2025)

MCAI Lex Vision: Private Equity, NIL, Antitrust, and the Firm-Formation Phase of College Athletics (January 2026)

MCAI AI Lex Vision: Compass’ NCAA Analogy Is Backwards (September 2025)

IV. The Strategic Structure: A Coordination Game Losing Its Focal Point

College sports has always been a coordination game, and naming the game explains why the bill faces a harder task than its drafters assume.

The NCAA served as the focal point — in Schelling’s sense, the shared expectation that let competing schools hold a cooperative equilibrium on compensation, eligibility, and transfers. The equilibrium held for one reason: every school expected every other school to comply, and the association’s authority made compliance the obvious mutual expectation.

Two shocks dissolved the focal point. Alston stripped the association’s legal authority to set compensation limits, and the House settlement converted the cap from an association norm into a litigated artifact. Once a focal point loses legitimacy, the cooperative equilibrium unravels, and players re-optimize one by one.

The bill’s project is to rebuild a focal point by statute after the original one has failed — and rebuilding a focal point is far harder than preserving one, because players who have already found a more profitable individual strategy must be persuaded to abandon it. (Confidence ~75%.)

Watch the unraveling in two games already in play.

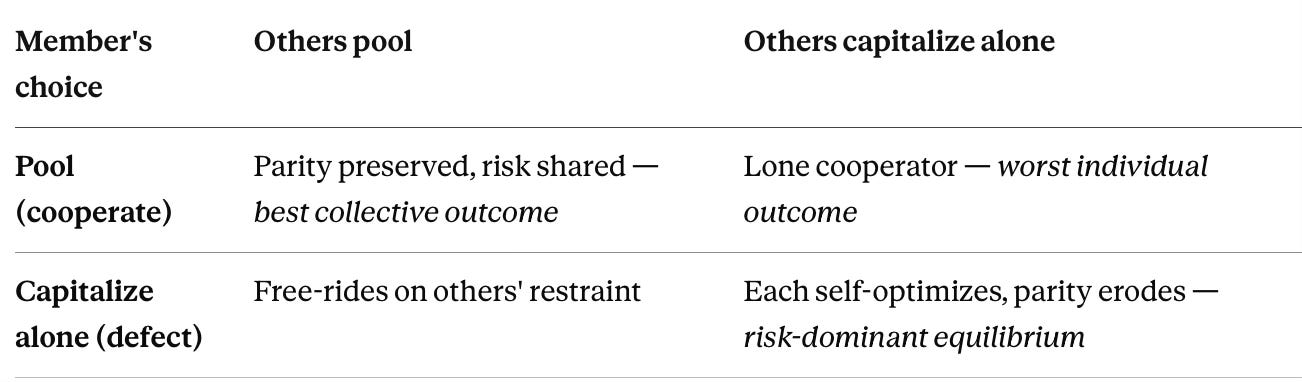

The conference-capital game is a stag hunt. Pooling capital at the conference level is the cooperative, higher-payoff outcome — it preserves competitive parity and spreads risk. Reaching it requires every member to commit at once, and members hold divergent risk profiles and balance sheets. A representative member faces this ranking of outcomes:

The lone-cooperator outcome is catastrophic: a school that commits to pooling while rivals capitalize independently absorbs the cost of parity and surrenders its own advantage. With trust low among heterogeneous members, the risk-dominant strategy is to defect to institution-level capital. The stalled Big Ten–UC Investments proposal is the stag hunt resolving toward the safe, defecting equilibrium. (Confidence ~80%.)

Firm formation is a first-mover game. Institution-level capitalization rewards early movers and penalizes late ones. Utah moved first; every subsequent mover confronts a payoff matrix already altered, because early adopters lock in talent, compliance moats, and governance norms that later entrants must take as given. The eighteen-to-twenty-four-month path-dependency window the January 2026 report identified is the interval before the equilibrium tips. Past the tipping point, adoption becomes the dominant strategy — capitalize, or accept a structural disadvantage that compounds. (Confidence ~80%.)

A behavioral mechanism drives both games and answers the question Section III only posed. A binding compensation cap is a price control, and Becker’s account of rational response to constraint predicts the result: agents re-optimize around the cap rather than absorb it, diverting expenditure from the capped margin — direct pay — to the uncapped one — capital-funded infrastructure, stability, and facilities.

The prediction is precise. The cap does not end the arms race; it relocates the arms race to the margin the cap cannot price. (Confidence ~80%.)

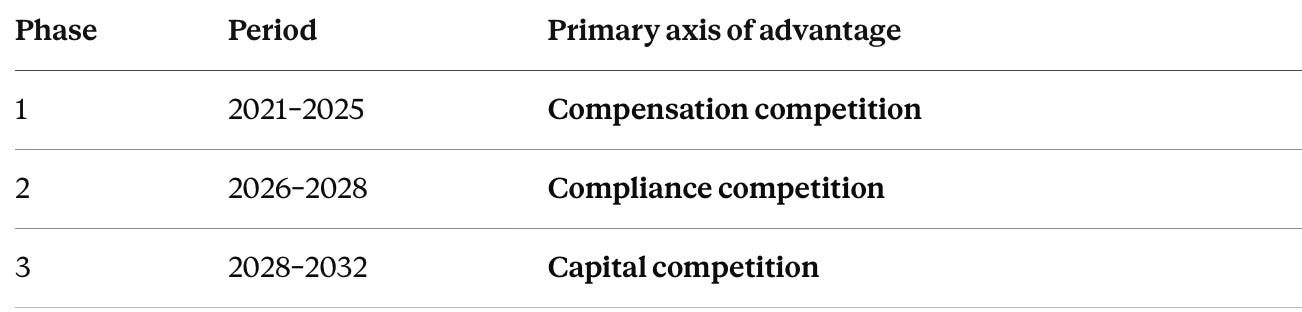

Trace the relocation across time and a three-phase migration appears — the spine of the simulation presented in Section X:

Equilibrium analysis and behavioral response converge on one forecast: schools defect from coordination toward firm-level capital, early movers tip the field, and the cap redirects rather than restrains competitive spend. The structure the game selects becomes self-reinforcing once media markets enter — the subject of the next section.

V. The Missing Reinforcement Loop: Media Markets

The bill treats media rights as a stabilizing mechanism. Title II expands collective media-rights authority on the theory that broader pooling supports conference stability, Olympic sports, and competitive balance. The theory deserves scrutiny, because media buyers do not optimize for competitive balance — media buyers optimize for audience concentration.

ESPN, Fox, NBC, Amazon, and future streaming entrants purchase inventory that maximizes viewership, subscription retention, advertising yield, and scheduling predictability. Competitive balance enters their calculus only insofar as it serves those objectives. (Confidence ~90% — the buyer objective is well established in media economics.)

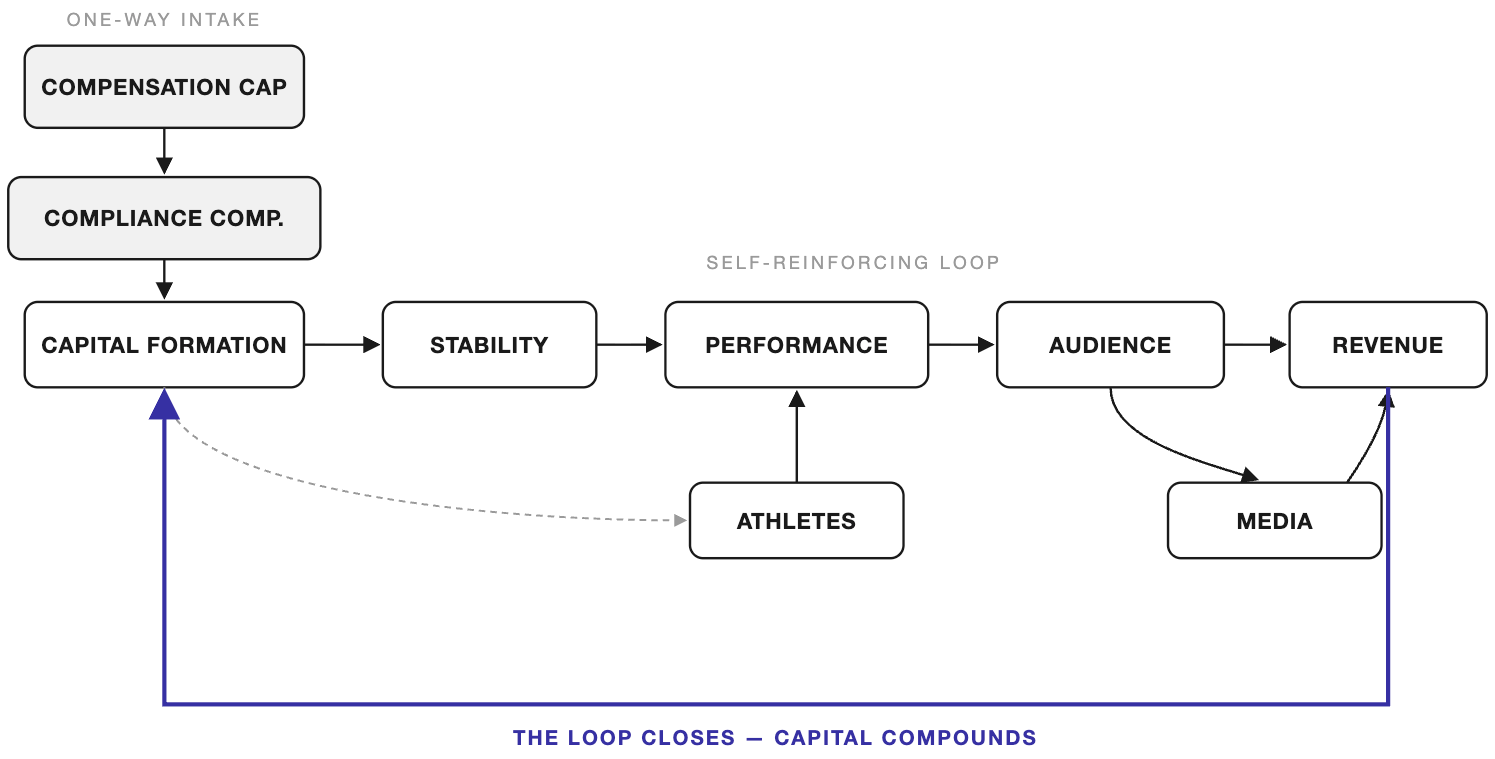

Figure 1. A one-way intake — compensation cap to compliance competition to capital formation — feeds a self-reinforcing loop. Capital funds stability and attracts athletes; stability and athletes drive performance; performance builds audience; media converts audience to revenue; revenue returns to capital. The accent arrow is the closure that turns a migration into an equilibrium.

A Cognitive Digital Twin of the media buyer produces a different equilibrium than the statute contemplates. Capitalized programs field more stable rosters, stronger compliance systems, greater payment certainty, and more consistent competitive performance. Consistent performance produces larger audiences, larger audiences command premium windows and promotional investment, and premium exposure produces revenue that attracts further capital.

The result is recursive:

Capital → Stability → Performance → Audience → Revenue → Capital

The media loop runs alongside the capital-formation loop of Sections III and IV, and the two interlock — both pass through stability and performance, and both terminate in capital. Two reinforcing loops, sharing nodes, compounding each other. (Confidence ~75%.)

The loop matters because it operates entirely outside the bill’s compensation architecture. A federal ceiling constrains direct payments. Media markets keep rewarding institutions that concentrate attention. Collective rights authority may therefore stabilize distribution while amplifying valuation differences inside the distribution system.

The distinction is decisive. Revenue floors are not competitive parity. Media pooling can preserve participation — every member keeps a check — while leaving audience economics untouched, and audience economics is where capital concentration compounds.

A migration thesis says capital can become the new source of divergence. An equilibrium thesis says the divergence becomes self-reinforcing. The media loop supplies the second. The bill assumes coordination restores balance; the simulation suggests coordination becomes the platform on which capital concentration compounds. (Confidence ~70%.)

Two loops now run together, sharing nodes and compounding each other:

Loop 1 — Capital formation. Compensation constraint → universities seek alternative advantages → capital funds them → athletes select capitalized programs → recruiting improves → performance improves → revenue rises → capital returns rise → more capital enters.

Loop 2 — Media reinforcement. Capital → stability → performance → audience → revenue → capital.

The loops interlock at stability and performance and both terminate in capital, so motion in either accelerates the other. A compensation cap touches neither.

The June 18 markup added a broadcaster amendment requiring at least one free local-market option for football and basketball games. The provision widens distribution; it does not reach the audience economics the loop runs on, because concentrated national windows — not free local access — are what premium rights value and capital chase. (Confidence the amendment leaves the loop intact: ~85%.)

VI. If the Athletics LLC Succeeds: College Athletics by 2030

The equilibrium has a destination, and the destination has a starting point.

Utah formed the first athletics-affiliated commercial entity with outside equity in December 2025. Ohio State’s athletic director has forecast further announcements. The Big Ten’s $2.4 billion proposal with UC Investments sits in a holding pattern after member opposition — the conference-level stall analyzed above, pushing capital toward the institution level where the coordination problem does not bind.

The January 2026 modeling projected a tier of ten to fifteen capitalized programs consolidating advantage within thirty-six to sixty months, with at least ten athletics-LLC formations inside twenty-four months (confidence 70–80% on formations).

Project the equilibrium to 2030 and a structure comes into view the bill does not anticipate:

Member schools of the dominant conferences operate athletics through capitalized LLCs, not athletic departments.

Private-equity minority capital — time-bounded, governance-constrained, structured to survive Title IX and tax scrutiny as the Utah deal was — funds the highest-revenue programs.

A meaningful share of athlete compensation, activation, and support flows through the affiliated operating entity rather than the university directly.

Media value concentrates toward the capitalized programs that produce consistent performance, widening the revenue gap the pooling provisions were meant to narrow.

Employment and antitrust litigation names the operating entities, where control and payment concentrate, rather than the conferences or the NCAA.

Overlay the bill on the 2030 structure, and the mismatch becomes a defect. The bill regulates the association layer — the NCAA, conferences, member institutions — and the direct institution-to-athlete relationship. Should compensation, control, and integration migrate into affiliated operating entities, the bill’s cap and its enforcement regime may not reach the entity where the money and the control actually sit. The statute would be addressed to the wrong legal person. (Confidence ~60%.)

The anti-circumvention language is the obvious rejoinder, and it does not close the gap. Section 114 bars an “associated entity” from arranging compensation that circumvents the cap, and an athletics LLC may well qualify. But the LLC’s competitive advantage is not paying above-cap compensation. The advantage is capital-funded stability and infrastructure — a margin the anti-circumvention language, built to catch disguised pay, does not price.

The capital channel slips the cap not by violating it but by competing where the cap is silent. A circumvention rule aimed at booster collectives writing inflated NIL checks does not reach an operating entity competing on balance-sheet capacity. (Confidence ~65%.)

A labor consequence compounds the antitrust one. As athletics LLCs coordinate schedules, channel compensation, and integrate athletic performance into entity revenue, they accumulate the factual attributes of an employer under the Fair Labor Standards Act’s economic-reality test — regardless of any statutory declaration of neutrality. The litigation the January 2026 report forecast targets these entities, and the bill’s deferral of the employment question leaves them exposed precisely where capital has concentrated.

Plausible scenarios, with the prototype already built, raise the stakes past incompleteness. The bill legislates a coordinated-association regime for a capital-allocation reality, and arrives structurally outdated. The falsification discipline cuts both ways: should fewer than five athletics-LLC formations materialize by twenty-four months despite continued capital interest, the migration thesis weakens and the bill’s coordination focus looks better calibrated than this analysis allows. (Confidence in the 2030 structure as the dominant equilibrium: ~55%. The scenario is a wager, stated as one.)

VII. The Doctrinal Hinge: Can Congress Immunize What the Court Refused?

The coordination half of the bill rests on one question: whether a statutory exemption shielding a horizontal compensation cap survives the doctrine that produced Alston. A second question hides inside the first — what legitimizes a compensation cap at all.

Start with the lineage. NCAA v. Board of Regents (1984) subjected NCAA restraints to rule-of-reason scrutiny rather than per se condemnation, while observing that college sports requires some horizontal cooperation to exist. NCAA v. Alston(2021) then applied that scrutiny to education-related compensation limits and struck them down, and Justice Kavanaugh’s concurrence questioned whether the NCAA’s remaining compensation rules could survive antitrust scrutiny at all.

The case law runs against collective limits on athlete pay. The judiciary, looking directly at the horizontal restraint, moved against it.

The bill answers by legislating around the judiciary. Congress may create antitrust exemptions the courts will not; the Sports Broadcasting Act of 1961, which Title II amends to permit collective media pooling, is itself such an exemption, enacted after a court held the NFL’s pooled-rights sale unlawful. An express statutory exemption is more durable than a judicial rule-of-reason defense, because it does not depend on a court’s case-by-case balancing. (Confidence that the §118 exemption is facially valid as an exercise of congressional power: ~80%.)

Now the concealed question surfaces, and it organizes the whole doctrinal picture. Salary caps already survive antitrust attack in professional sports — but they survive through the non-statutory labor exemption, because they emerge from bona fide, arm’s-length collective bargaining between a league and a players’ union. Brown v. Pro Football (1996) confirmed the principle: once a restraint comes out of the collective-bargaining process, labor law governs and antitrust steps aside.

Legitimacy, in other words, flows from the bargaining. Players accept the ceiling because they negotiated it and extracted consideration in return.

The Protect College Sports Act manufactures the antitrust immunity by statute while withholding the employment status — and therefore the bargaining leverage — that legitimizes compensation caps everywhere else they survive. The bill imports the professional-sports salary cap and strips out the collective-bargaining mechanism that makes the professional-sports salary cap lawful. Athletes receive the ceiling without the union that, in every professional league, is the price institutions pay for the ceiling. (Confidence in the framing as sound: ~80%.)

Game theory sharpens the stakes. A negotiated cap is a stable equilibrium: both sides consented, each holds consideration in the bargain, and the non-statutory labor exemption bars the defection path of an antitrust suit. A cap imposed by statute without bargaining is an unstable equilibrium — the bound party never consented, gained no negotiated consideration, and keeps an open defection path through employee-classification litigation.

The professional cap is self-enforcing because bargaining made it so. The bill’s cap depends on continued legal insulation to hold, and insulation is not self-enforcement. (Confidence ~75%.)

Congress need not supply the bargaining predicate to grant a valid exemption; the legislative power to immunize stands on its own. But the missing predicate opens two durable vulnerabilities that the migration thesis then exploits.

Scope is the first. Section 118 immunizes enforcement of enumerated provisions only — the cap, transfer rules, eligibility rules, agent authority. Capital stratification, athletics-LLC formation, and the labor-market effects of capital access fall outside the immunity entirely, because none is “enforcement” of an association rule. The exemption is a fence around a shrinking pasture, and the herd is moving to open range.

The monopsony theory is the second. A Sherman Act Section 2 buyer-side claim against capitalized programs or athletics LLCs draws nothing from Section 118, because it challenges no association rule. The January 2026 report assigned the theory a 20–35% probability of success, low but rising, with state unfair-competition statutes more favorable at 30–45% in receptive jurisdictions. The immunity stays silent exactly where the live exposure is migrating. (Confidence ~70%.)

Scope and the monopsony theory converge on the employment question, because a cap imposed without bargaining invites the very litigation that would supply the bargaining. Denied a seat at a negotiating table, athletes route toward employee-classification suits to win one — and a classification ruling, arriving against the capitalized operating entities, would unsettle the entire compensation structure the bill so carefully insulated. The cap’s lack of a bargaining foundation is not a cosmetic gap. It is the pressure valve through which the capital battleground gets reached.

Stated as a wager: the immunity likely survives a facial challenge to the cap and likely proves irrelevant to the vertical, labor-market, and classification theories the capital channel generates. The statute wins the case it was built to win and never reaches the cases that come to matter. (Composite confidence ~60%.)

VIII. The Quarantined Variable: Employment Status

The bill’s most consequential move on employment is the refusal to make one — and the refusal feeds both the doctrinal vulnerability and the capital channel.

Section 122 declares the title neutral on employee status. Section 116 ships the question to a twenty-member commission charged with studying collective-bargaining and employment-status alternatives, reporting within five years. The single variable governing whether the entire compensation architecture is lawful sits quarantined for half a decade.

Section 122’s neutrality changes the field even while the text claims to leave it untouched. Athletes receive a governance voice — Section 111 reserves one-third of association board seats — without the legal status that would let them bargain over the cap. A seat at the table, and no contract to negotiate. As the doctrinal analysis established, the absence of bargaining is exactly what separates this cap from the professional-sports caps that survive antitrust scrutiny, and exactly what makes it an unstable equilibrium.

Deferral also relocates the question rather than resolving it. The January 2026 report names employment classification a falsification trigger: two or more circuit rulings finding employee status, or National Labor Relations Board certification at five or more Football Bowl Subdivision programs within thirty-six months.

Congressional silence does not freeze the question; it hands the question to the courts and the Board — the actors whose rulings the report flagged as decisive — and hands it to them just as compensation and control migrate into the operating entities most exposed to an economic-reality test. (Confidence that LLC structures accumulate employer-like attributes regardless of §122: ~80%.)

Deferral, in short, is a decision to let the most important question be answered elsewhere, later, by institutions other than Congress — while the firm-formation channel drafts the answer in operational fact.

IX. What the Migration Means for Each Actor

The shift from coordination to capital reaches every institution in the field, and each faces a different decision. The simulation in Section X models each actor’s adaptation; the strategic implications follow. The reads below are foresight, not advice; each actor should model its own posture against its own exposure.

Universities and athletic directors. The compliance burden the bill creates is real and arriving — disclosure thresholds, fair-market-value review, agent oversight, an append-only record of every deal that withstands audit. Two responses tempt and both fail: absorb the burden as paperwork through existing staff, or wait for peers to move first. The burden is the entry cost to the capital era, not a clerical chore. Programs that document, review, and audit at scale carry lower enforcement risk and present better to capital — compliance capacity now helps determine what makes a program financeable. The strategic question underneath the burden is capital structure: whether to partition athletics into a financeable entity, and on what governance and tax terms. (Confidence ~70%.)

Conferences. The bill closes the consolidation path — Section 205 bars conferences from mergers or asset acquisitions that would build a closed top tier (the markup substitute recast the provision in conference-neutral terms, dropping the introduced version’s framing that singled out the SEC and Big Ten) — while the capital path stays blocked by the collective-action failure modeled above. Caught between a legal bar on combining and a stag-hunt bar on pooling capital, conferences face the prospect of being bypassed by institution-level capital that needs neither. The media loop deepens the exposure: pooled rights stabilize the conference’s distribution while audience value concentrates toward its capitalized members. The conference as the unit of competition is the structure most exposed to the migration. (Confidence ~65%.)

Capital providers. The bill leaves the firm-formation channel unregulated, and the Utah template — minority stake, defined buyback, majority university control, Title IX and tax structured around — is replicable. The first-mover window runs roughly eighteen to twenty-four months: early structures set the governance norms and the switching costs later entrants must accept. Opportunity and antitrust exposure occupy the same window. (Confidence ~65%.)

Athlete representation and agents. The bill reshapes the agent market through registration, certification, and a five-percent fee cap, compressing margins and formalizing the role. The deeper shift is leverage: a compensation cap imposed without bargaining moves the fight for athlete leverage to employment-classification litigation, not the negotiating table. Representation that understands the capital-stability tradeoff — capitalized programs offer lower individual risk at the cost of bargaining room — will steer clients more precisely than representation chasing headline numbers. (Confidence ~65%.)

Regulators and state attorneys general. The Section 118 immunity is scoped narrowly to association rules, leaving the entity layer open to enforcement under Sherman Act Section 2 and state unfair-competition statutes. Enforcement calibrated to the old battleground — NCAA and conference coordination — will miss the layer where money and control are concentrating. The signal to watch is narrative inversion: fairness rhetoric deployed to insulate a control structure, the pattern MindCast AI has documented across both college sports and adjacent markets. (Confidence ~70%.)

X. The Simulation: Seven Actors, Two Loops, Nine Predictions

The argument above is the output of a formal simulation, not an impression. The MindCast AI Proprietary Cognitive Digital Twin Predictive Game Theory Foresight Simulation System models seven actors under the bill and checks whether their independent optimizations converge. They do. Each actor, optimizing rationally under the statute, pushes competitive advantage from coordination toward capital, and the two loops compound the result.

The seven twins’ adaptive moves follow, with the load-bearing two elaborated in Sections IV and V:

The convergence produces nine predictions, each with a confidence band and a falsification condition.

Prediction 1 — The cap holds facially and leaks structurally. Section 118 survives most direct legal challenges while capital-mediated differentiation increasingly determines competitive outcomes. Confidence: 65%. Falsified if federal courts invalidate the immunity within 36 months, or no observable capital-driven divergence emerges.

Prediction 2 — Litigation migrates to operating entities. Athletics LLCs, affiliated entities, and capitalized programs increasingly replace the NCAA and conferences as primary litigation targets. Confidence: 65%. Falsified if major litigation keeps focusing on association coordination through 2029.

Prediction 3 — Employment status resolves outside Congress. Courts, agencies, or labor regulators resolve the athlete-employment question before the Section 116 commission produces meaningful recommendations. Confidence: 55%. Falsified if congressional action arrives first.

Prediction 4 — Athletics-LLC adoption accelerates. Ten or more significant athletics-affiliated operating entities emerge within twenty-four months of the Utah prototype. Confidence: 60%. Falsified if fewer than five formations occur despite continued investor interest.

Prediction 5 — Compliance becomes a recruiting asset. Elite programs market payment reliability, NIL administration, audit readiness, and governance as recruiting advantages; compliance evolves from overhead into infrastructure. Confidence: 65%. Falsified if recruiting competition remains overwhelmingly compensation-driven through 2029.

Prediction 6 — Capital replaces compensation as the primary sorting mechanism. Athlete placement increasingly correlates with institutional capitalization rather than nominal compensation; capital-rich programs attract disproportionate elite talent under identical ceilings. Confidence: 70%. Falsified if recruiting outcomes remain primarily compensation-driven.

Prediction 7 — Conference power erodes relative to operating entities. Operating entities gain influence over compensation administration, NIL activation, athlete services, and commercial operations, while conferences retain mainly regulatory functions. Confidence: 60%. Falsified if conferences remain the dominant operational centers through 2032.

Prediction 8 — Congress triggers a second reform cycle. Lawmakers revisit the statute as capital-driven divergence persists, with future reform aimed at operating entities, private equity, labor classification, and governance transparency rather than compensation ceilings. Confidence: 65%. Falsified if competitive balance stabilizes without additional federal intervention.

Prediction 9 — Media value increasingly tracks capitalization. Audience share, premium windows, and rights value increasingly track institutional capitalization alongside brand strength and audience history — capitalization joins the established drivers rather than displacing them, widening rather than narrowing the gap the pooling provisions were meant to close. Confidence: 70%. Falsified if capitalization shows no growing relationship to media value through 2032.

Two disciplines frame the set. The first is self-policing: the bill’s introduction starts a clock against MindCast AI’s own prior work, which named a comprehensive NIL and antitrust statute “enacted and operative for 24 months without injunction, material amendment, or adverse appellate ruling” as a falsification trigger. Introduction is not enactment, and a voluntary pooling regime may not be the coordination restoration the trigger contemplates — but a foresight practice that hides its own falsification conditions is marketing, and one that publishes them is intelligence.

The second is observation. The following signals will confirm or break the thesis as it unfolds:

Athletics-LLC formations with outside capital, by count and structure.

Disclosure of buyback windows, control provisions, profit-allocation terms.

Transfer-portal sorting correlated with program payment reliability.

Circuit rulings or NLRB certifications involving revenue-sport athletes.

State attorney general enforcement differentiated by program structure.

Media-rights valuations and audience share tracked against program capitalization.

The Section 116 commission’s composition, timeline, and treatment of collective bargaining.

Any antitrust challenge testing the scope — not the validity — of the Section 118 immunity.

XI. Conclusion: From Coordination to Capital

The Protect College Sports Act of 2026 restores coordination among institutions at the exact moment competitive advantage is migrating from coordination to capital formation. The bill is a precise instrument aimed at a receding target. It advanced from committee 19–9 on June 18, 2026; whether it clears the Senate floor and the House or stalls as its predecessors did, the target keeps receding either way.

The coordination war was real, and the bill largely wins it — the compensation cap immunized, made permanent, and shielded from challenge; the media rights pooled; the rules made uniform. The athlete protections inside that settlement are genuine and worth defending.

But the competitive frontier has already moved to a battleground the statute never names: the capitalized operating entity, financed by patient equity, competing on the margins a compensation cap cannot price — and amplified by media markets that reward concentrated attention rather than competitive balance. Run the structure forward and the bill governs a legal person the money and control will have left, while two reinforcing loops, capital and media, compound the divergence underneath it.

The cap it so carefully insulated rests on no bargaining, and the missing bargaining is the pressure valve through which the capital battleground gets reached.

The central policy question is no longer whether Congress can restore coordination. Congress can, and in this bill largely has. The open question is whether anyone will govern the capital-driven divergence that coordination restoration was meant to prevent — or whether it hardens, unregulated, into the operating system of college sports while the statute stands guard over a war that is already ending.

Congress is fighting the last war while capital markets and media markets jointly finance the next one. The bill is a map of where the fighting was; this paper, a map of where it is going.

Methods Note

MindCast AI conducts this analysis through the MindCast AI Proprietary Cognitive Digital Twin Predictive Game Theory Foresight Simulation System — the firm’s umbrella foresight architecture. Cognitive Digital Twins model how institutions, regulators, capital providers, media buyers, and athlete labor markets perceive risk, update strategy, allocate resources, and respond under stress.

The seven actor twins, their adaptations, and the two interlocking reinforcement loops — set out in Sections IV, V, and X — are components of the system, and behavioral economics and predictive game theory are its analytical engines — a Chicago-school lens (Coase on coordination capacity, Becker on rational response to constraint, Posner on the lag between behavior and legal correction) coupled with focal-point coordination, collective-action and first-mover dynamics, and equilibrium stability.

Predictions issue only where multiple Vision Functions converge on a directional outcome and remain stable under stress testing, and each prediction pairs with predefined, observable falsification conditions.

Statutory analysis draws from the bill text as introduced May 27, 2026 (S. 4668). Section citations are to the introduced text; the Cruz-Cantwell-Schmitt substitute adopted at the June 18 markup revised several provisions — notably the super-league section — and may renumber others, so cited sections should be reconfirmed against the engrossed text once it posts. Capital-structure analysis builds on the firm’s published NCAA NIL corpus, verified against primary sources.

MindCast AI partners with universities, conferences, capital providers, and counsel on foresight simulations for complex litigation, antitrust, and institutional strategy. Inquiries: mcai@mindcast-ai.com.

Appendix — Legislative Dossier & Primary Sources

The bill

Protect College Sports Act of 2026 — full text as introduced (PDF)

Cruz-Cantwell-Schmitt substitute, as adopted at markup (PDF)

S. 4668, 119th Congress (Congress.gov) · H.R. 9137 — House companion (Congress.gov)

Committee action — June 18, 2026 markup

Markup announcement · Introduction release (Cantwell, Cruz, Schmitt, Coons)

Adopted amendments (PDFs): Budd 1 · Budd 5 · Budd 7 · Capito 1 · Curtis 1 · Duckworth 1 · Duckworth 4 · Duckworth 6 · Kim 1 · Lujan 1 · Rosen 1 · Rosen 2 · Sheehy 1 · Sullivan 1 · Wicker 2

Predecessor legislation

Underlying settlement

In re College Athlete NIL Litigation, No. 4:20-cv-03919-CW (N.D. Cal.) — final approval June 6, 2025 (Wilken); ~$2.8B in back damages and the ~$20.5M per-school revenue-share cap codified by the bill. Approval reported (ESPN)

Complementary analysis

Kyle L. Saunders, “The PCSA Targeting Memo: Data & Methods” — Senate whip count and vote math; the political-feasibility companion to this structural analysis.

Prior MindCast AI work (foresight record)

SAFE vs. SCORE Act (Sept 2025) · the NCAA NIL Settlement, Foresight Realized (June 2025) · Private Equity, NIL, and the Firm-Formation Phase (Jan 2026) · Compass’ NCAA Analogy Is Backwards (Sept 2025)