MCAI Lex Vision: If the Protect College Sports Act Passes, Private Equity in College Sports Wins Differently

Utah's Crimson Brand Partners Deal and the New Private-Equity Playbook for College Sports

Visual Companion. Related works:

If the Protect College Sports Act Passes, Private Equity in College Sports Wins Differently (July 1, 2026) — Utah’s Crimson Brand Partners close validates the firm-formation thesis and shows why private capital migrates into compliant college-athletics operating companies whether or not the Protect College Sports Act passes.

The Protect College Sports Act of 2026 (S. 4668) Becomes a Compliance-Infrastructure Bill (June 30, 2026) — Shows how the reported Senate text hardened S. 4668 into a compliance-infrastructure bill, where clean documentation replaces the paycheck as the competitive edge and advantage keeps moving to the capital layer beneath it.

The Protect College Sports Act of 2026 — Federal NIL Salary Cap, Antitrust Immunity, and the Private Equity Blind Spot (June 2026) — Argues that the bill’s federal NIL salary cap and antitrust immunity discipline coordination among schools while leaving the private-equity capital-formation channel — the blind spot — untouched.

Private Equity, NIL, Antitrust, and the Firm-Formation Phase of College Athletics(January 2026) — Names the firm-formation phase of college athletics, forecasting advantage’s migration from coordination to capital, identifying Utah as the prototype, and projecting ten or more athletics operating companies within twenty-four months.

Executive Summary

Utah just answered the question every athletic director is asking. On June 12, the University of Utah and its foundation closed a first-of-its-kind private-equity-backed operating-company deal — the first built around a major public university’s athletics department. The University of Utah Growth Capital Partners Foundation partnered with Otro Capital to form Crimson Brand Partners, the operating company designed to manage and monetize Utah’s athletics commercial rights, with Otro taking a minority stake and the foundation the majority. Private capital entered college athletics not by buying a team or professionalizing athletes, but through a governance-constrained operating company that monetizes the commercial surface while leaving coaching, recruiting, and student-athlete support inside the university.

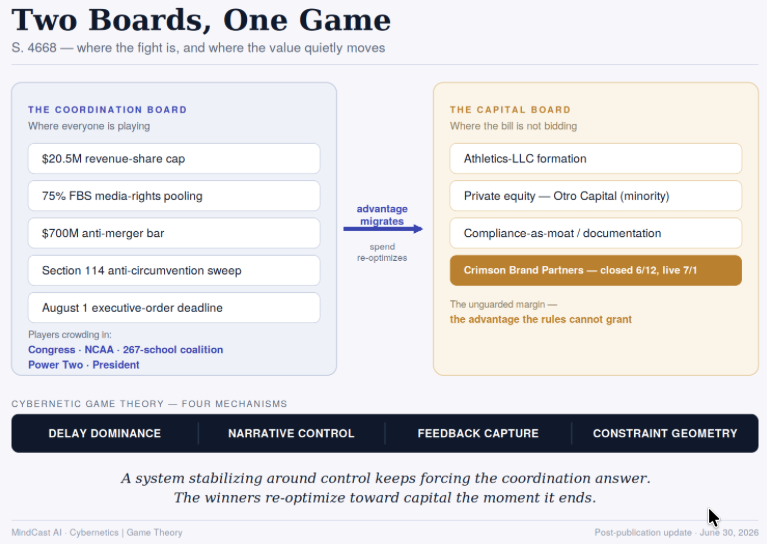

The Protect College Sports Act does not reverse that move. S. 4668 regulates the coordination layer — the compensation cap, the disclosure regime, media pooling, the anti-merger bar. Utah built beneath that layer, in the capital layer where statutory control maps less cleanly.

Passage would not kill private equity in college sports. Passage would professionalize the channel. A national cap and disclosure regime shifts competition from the size of the check to the integrity of the record behind it, and a compliant operating company becomes the machine that produces new revenue, cleaner commercial records, and better valuation evidence. Failure leaves schools inside a fragmented, litigious market that makes the same operating company a hedge against chaos. Both branches raise demand for the Utah model.

One caveat sits at the center of the structure, and honest analysis names it. Utah’s own state auditor warns the foundation holding the rights is not legally controlled by the university. The arm’s-length design is what admits capital and answers the political objections — and the same design is what a public audit flags as a governance gap. The tension is the story, not a footnote to it.

I. The Better Question

Most coverage asks whether the Protect College Sports Act stops private equity. The sharper question asks whether the bill converts private capital from a risky workaround into a sanctioned compliance-and-commercial layer.

The Utah deal does not prove that private equity can buy college athletics. The deal proves something more durable: private capital can enter through a university-adjacent commercial operating company that converts athletic demand into financeable revenue while leaving the most politically sensitive functions inside the institution. PCS would regulate the compensation and coordination layer; Crimson Brand Partners sits beneath it, in the commercial-infrastructure layer where schools now need capital, data, sponsorship execution, and compliance-grade records.

MindCast AI’s January analysis, Private Equity, NIL, Antitrust, and the Firm-Formation Phase of College Athletics, argued that college athletics had entered a firm-formation phase driven by regulatory stasis. Utah served as the prototype: the school approved an athletics-affiliated commercial entity, then structured outside capital as minority, time-bounded, and governance-constrained rather than as permanent ownership of the department. Asset partitioning was the decisive mechanism — the operating company becomes the economic firm while the university keeps control of the athletic functions.

Utah’s June close validates the mechanism. The university and its foundation finalized the partnership with Otro Capital, renaming the entity Crimson Brand Partners — the vehicle the Board of Trustees authorized on December 9, 2025 as Utah Brands & Entertainment — and naming a leadership team drawn from professional sports. Crimson runs commercial operations: stadium and arena events, branding, licensing, sponsorships, ticketing, and digital media. Coaching, recruiting, scheduling, student-athlete support, private fundraising, and facilities stay with the university.

Separation is the point. Utah did not sell college athletics. Utah converted athletics-adjacent commercial activity into an operating company held at arm’s length.

II. Utah as Validation, Not Just News

The close moves Utah from thesis to operating reality, and three forecasted features now appear in the finalized structure.

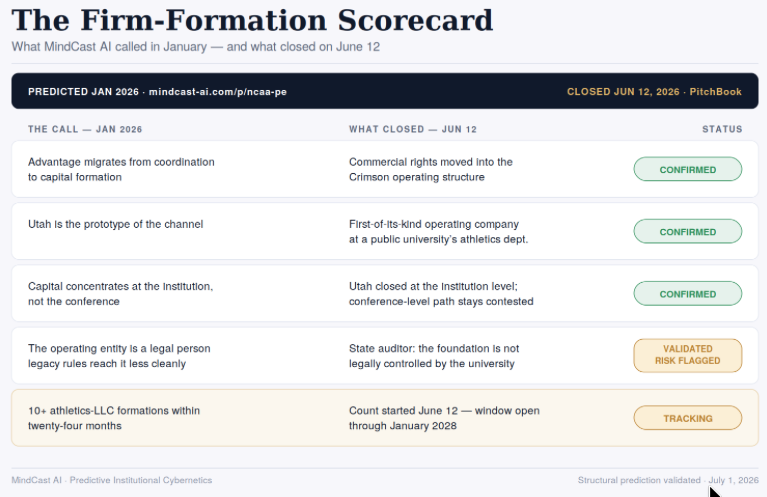

Figure 1. The firm-formation scorecard. Four structural calls from the January analysis confirmed at close; the diffusion count opened and is tracking.

Revenue concentration came first. Crimson Brand Partners controls the commercial surface — sponsorships, licensing, ticketing, digital media, and venue events — pulling functions that usually sit with four separate outside partners into one company under one agenda.

Institutional control held where it is most politically sensitive. Utah kept coaching, recruiting, scheduling, student-athlete support, private fundraising, and facilities, and athletic director Mark Harlan chairs the new company’s board. Harlan told reporters that management of coaches, athletes, and NCAA and Big 12 work still reports through the athletic director, president, and board.

Professional operating discipline arrived with the leadership team. CEO Matt Webb spent eight years running corporate partnerships for the New Orleans Saints and Pelicans and built commercial platforms for the Browns and Padres before that; the group adds a chief commercial officer, a chief ticketing officer, and a chief financial officer drawn from the NFL, NBA, MLB, NASCAR, and private-equity-backed finance. Crimson folds in roughly 15 Utah Athletics employees at launch and scales toward 70. Utah did not disclose the partnership’s financial terms.

Now the tension the structure cannot hide. Utah State Auditor Tina Cannon warned in a May 2026 letter that the foundation holding the transferred rights is intentionally structured so the university does not legally control it, citing governance and transparency risks alongside the department’s deficits and debt.

The warning cuts toward the firm-formation thesis rather than against it. An entity a school does not fully control is precisely the legal person the January analysis flagged — the commercial layer the department’s legacy rules reach less cleanly (~85%). Utah’s control is real over the athletic functions and deliberately arm’s-length over the commercial ones, and the arm’s-length design both admits the capital and draws the auditor’s objection.

III. What S. 4668 Actually Regulates

The Protect College Sports Act reshapes the rules schools play by, not the businesses they build. The Senate Commerce Committee advanced the bill 19–9 on June 18, 2026, sending it to a floor vote that the sixty-vote threshold and Power Two opposition leave far from certain.

Every core instrument governs coordination among schools. A federal revenue-share cap aligns with the House settlement’s $20.5 million ceiling. A Section 118 antitrust shield protects institutions, but only for conduct the bill blesses. Mandatory NIL disclosure, a fair-market-value database, and a clearinghouse police individual deals. A high-revenue conference-consolidation bar aimed at superleague formation freezes the top of the realignment ladder, with reported thresholds varying by bill version. A Section 125 floor protects women’s and Olympic programs, and the bill stays neutral on employee status.

Congress can legislate caps, disclosures, eligibility, transfers, and media pooling. Congress does not build the revenue engines schools need to survive those rules. Utah built the missing layer.

MindCast AI’s June update, The Protect College Sports Act Becomes a Compliance-Infrastructure Bill, framed the bill as compliance infrastructure, and the same logic reaches private capital: a cap and disclosure regime shifts competition from the size of the check to the integrity of the record behind it. Crimson Brand Partners is not merely a revenue vehicle; the company is the commercial data layer that makes sponsorship value, ticketing demand, licensing performance, media inventory, and brand activation legible inside a capped-compensation regime.

Contact mcai@mindcast-ai.com to partner with us on Predictive Game Theory AI in Law and Behavioral Economics. To deep dive on MindCast works upload the URL of this publication into any LLM (preferably Google AI mode/Gemini, Claude, ChatGPT) and prompt ‘reconstruct MindCast framework with three degrees of cited sub links.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure.

MindCast AI is a cybernetic, predictive game-theory AI firm specializing in law and behavioral economics, applied to complex litigation, innovation systems, and geopolitical risk intelligence. Rather than extrapolating historical patterns, the firm models the mechanisms that generate institutional behavior, running Cognitive Digital Twin simulations grounded in Nash equilibrium, Stigler information economics, and the Chicago School of law and behavioral economics.

Recent projects: When a FIFA World Cup Model Picks France and the Economist Picks Argentina |

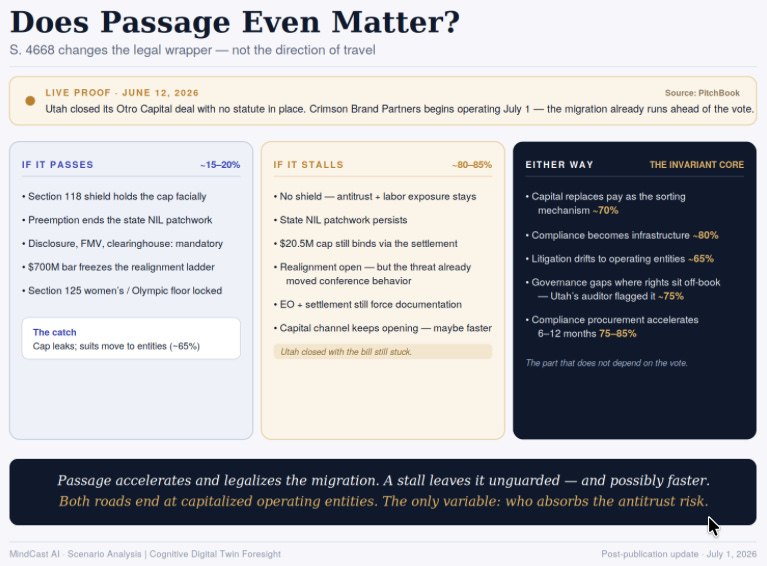

IV. If PCS Passes

Passage would likely produce four effects, with early signals observable within a year of enactment.

Compliance becomes a monetizable moat. The bill preempts conflicting state NIL, transfer, and eligibility laws and sets one federal standard, so programs with stronger intake systems, valuation records, agent verification, associated-entity mapping, and audit trails move faster and defend decisions better (~80%).

Capital shifts from “pay players” optics toward infrastructure. Investment funds ticketing systems, sponsorship teams, premium seating, venue events, content studios, compliance tooling, brand licensing, and fan data — the lanes the bill narrows least (~75%).

Utah becomes a model rather than an outlier. Crimson Brand Partners hands every athletic director a clean public answer — a controlled operating company that stabilizes funding, reduces debt pressure, and protects women’s and Olympic programs — and imitation follows a working template (~70%).

Power Two resistance intensifies. The Big Ten and SEC oppose the bill as drafted, arguing it under-preempts state law, under-protects enforcement, hands ongoing rulemaking to Congress, and could shrink athlete revenue-share. Opposition reinforces the Utah thesis rather than undercutting it — sophisticated actors do not wait for stable rules, they build infrastructure that survives multiple regimes (~75%).

V. If PCS Fails or Stalls

Failure makes the thesis more urgent, not weaker. Schools without a federal framework stay inside a fragmented regime — House settlement implementation, clearinghouse practice, conference enforcement, state NIL laws, private litigation, Title IX pressure, and unresolved employment status. Legal-risk discounts rise, and demand for outside capital, compliance systems, and professionalized operations rises with them.

Utah becomes a chaos hedge in that branch. Crimson Brand Partners lets the school generate revenue and professionalize operations without waiting for Congress, the NCAA, the conferences, or the courts to settle the market.

Symmetry is the point. Passage rewards compliance infrastructure; failure rewards institutional self-help. Both roads lead to firm formation.

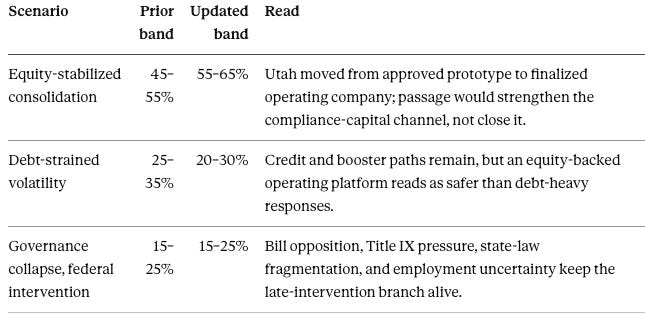

VI. Updated MindCast AI Forecast

The forecast tracks how college athletics resolves its capital structure over the next several years, across three competing scenarios. Utah’s finalized operating model shifts the bands — raising the odds of equity-stabilized consolidation and trimming the debt-strained path, while the late-intervention scenario holds. The table sets each prior read against the updated one.

Bands are independent likelihoods for each scenario, not a single partition summing to 100 percent. Overall confidence: 80–85 percent.

Timing drives the upward shift for equity-stabilized consolidation. Utah finalized the operating model before the statute resolved, and firm formation is no longer waiting on legislation — capital architecture is moving ahead of federal coordination.

VII. Cognitive Digital Twin: Actor Read

The MAP Cognitive Digital Twin runs each actor forward on its own incentives. Five reads follow.

University of Utah optimizes for solvency, institutional control, reputational protection, and competitive relevance. Crimson Brand Partners lets the school monetize commercial operations without making the department look like a privately owned franchise. Forecast: Utah presents the company as a sustainability and Olympic-sport-preservation structure, not a private-equity transaction (~85%).

Private capital — Otro Capital and peers — optimizes for control rights, growth channels, downside protection, and regulatory survivability. Commercial operations offer a broader, more defensible return than athlete-compensation vehicles or booster collectives. Forecast: investors prefer operating-company exposure over direct NIL exposure, more so if the bill passes (~80%).

Congress optimizes for visible stability, athlete-protection narratives, Olympic-sport preservation, and antitrust containment. Statutory actors legislate caps, disclosures, and eligibility more easily than business models. Forecast: Congress keeps stabilizing the top layer while schools innovate below it (~75%).

The Power Two optimize for autonomy, revenue retention, and media-rights leverage. Opposition to the bill fits a rational-actor read — resistance to a statute that limits scale advantages and forces coordination. Forecast: SEC and Big Ten schools build their own infrastructure even while opposing the federal framework (~80%).

Athletes optimize for compensation, eligibility stability, transfer optionality, and payment reliability. Capitalized programs offer lower documentation risk and steadier payments even when headline pay stays capped. Forecast: athlete decisions increasingly price institutional stability, not raw NIL dollars alone (~65%).

VIII. The Bottom Line

Passage would not stop private equity in college athletics. Passage would change where private equity wins.

The bill attempts to stabilize college sports through national rules, caps, disclosures, transfer limits, media pooling, and antitrust protection. Utah’s Crimson Brand Partners shows the parallel move: schools are not waiting for a national settlement, they are building commercial firms around athletics that survive multiple legal regimes.

The next phase of college athletics will not hinge only on whether athletes become employees, whether the cap survives, or whether Congress passes the bill. The deeper shift sits in capital architecture. Schools with financeable commercial platforms gain compliance, revenue, documentation, and adaptability advantages; schools without them face higher volatility, higher legal exposure, and weaker bargaining power.

Utah did not sell college athletics. Utah built the operating company for the post-amateurism era — and whether S. 4668 becomes law decides the wrapper around that fact, not the fact itself.

Sources & Primary Documents

Methods Note

The forecast issues from the MAP Cognitive Digital Twin foresight simulation, which routes each event through cybernetic and game-theoretic lenses to separate the coordination layer — what schools and conferences do together — from the capital layer, where a capitalized operating company builds advantage the coordination rules reach less cleanly. Scenario bands are independent likelihoods rather than a partition, and the analysis states the undisclosed-terms limit rather than filling it with an unverified figure. Foresight analysis, not legal or investment advice.