MCAI Lex Vision: The Compass Antitrust Self-Destruction Sequence

How Aggressive Federal Litigation Birthed the Legislation That Destroyed the Business Model

Installment I of The Compass Collapse– A Post Washington SSB 6091 Passage Reckoning series: Installment II SSB 6091 Has Passed. Here Is What It Now Reaches — and the Compass Enforcement Record It Inherits, Installment III Compass Plan B, Structural Circumvention After Washington SSB 6091.

I. EXECUTIVE SUMMARY

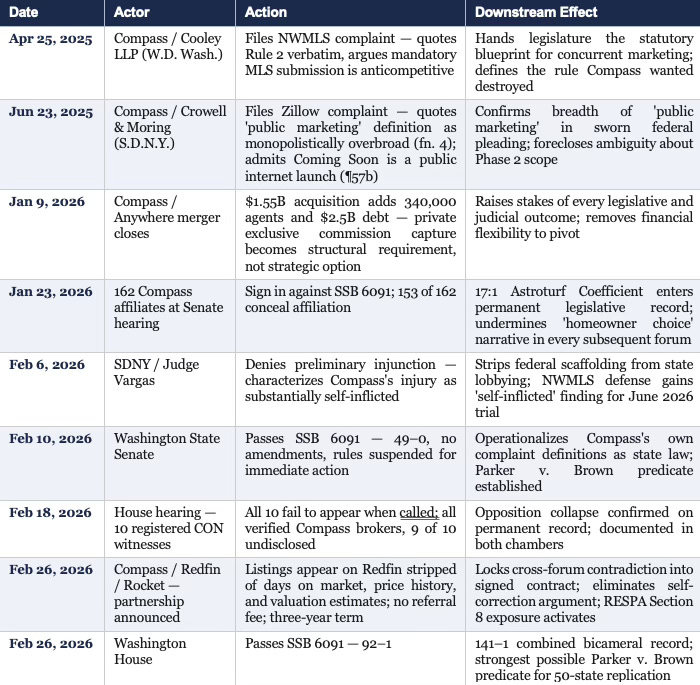

Compass Real Estate filed two high-profile federal antitrust lawsuits in 2025 — one against the Northwest MLS (NWMLS) in April and one against Zillow in June — to protect its Private Exclusive listing network from transparency enforcement. Cooley LLP filed the NWMLS complaint in the Western District of Washington on April 25, 2025. Crowell & Moring filed the Zillow complaint in the Southern District of New York on June 23, 2025. Both actions were structured to impose asymmetric litigation cost on regional institutions incapable of sustaining decade-long federal defense.

The strategy failed in a manner that was structurally overdetermined. By broadcasting the mechanics of its shadow market through public federal complaints, Compass handed Washington State legislators, regulators, and opposing industry actors a fully developed analytical and evidentiary framework for statutory intervention. SSB 6091, mandating concurrent public marketing of all residential listings, passed the Washington State Senate 49–0 and the House 92–1. The combined bicameral record stands at 141–1.

Compass spent an estimated $2–4 million in legal fees to generate the primary evidentiary record used against it in both the legislative process and its own federal trials. More precisely: Compass’s elite antitrust counsel drafted, with billable precision, the operative definition of ‘public marketing’ that SSB 6091 codified. Washington’s drafters did not need to invent a regulatory framework. Compass filed one in federal court, and the Legislature applied it.

For state attorneys general and legislators: Washington’s evidentiary record — the transaction data, the opposition modeling, the complaint text, and the Astroturf Coefficient — travels to every state that follows without needing to be regenerated. For the real estate industry: the self-destruction sequence documented here is a structural case study in what happens when a brokerage deploys litigation as a market-access instrument in a cooperative-infrastructure industry it does not own.

THE SEQUENCE — BEHAVIOR TO MARKET ADAPTATION

Full analytical development of each sequence node begins in Section II.

II. THE ANATOMY OF SELF-INFLICTED REGULATORY CAPTURE

Self-inflicted regulatory capture — the mechanism by which a firm’s own litigation provides opponents the statutory blueprint to regulate it — unfolds in two phases. Phase One is the quiet period: a commercially advantageous model operating at the edge of existing rules, generating outsized returns precisely because no one has forced a formal legal definition. Phase Two is the Streisand Topology: public litigation that converts a private dispute into legislative raw material. Washington’s 2025–2026 cycle is the cleanest documented example of this sequence in modern real estate regulation. Compass held the loophole. Compass filed the complaints. Compass’s own counsel wrote the definitions SSB 6091 codified. The Legislature applied them 141–1.

A. Phase One: The Quiet Loophole (Pre-April 2025)

Compass’s Private Exclusive network functioned as a structured off-market listing ecosystem. Properties marketed selectively — to Compass agents and affiliated buyers, but not to the general public or competing brokerages — generated dual-agency commission capture at materially higher rates than open-market transactions. The model operated quietly, relying on MLS rule ambiguity and the absence of explicit statutory prohibition.

Washington State had no concurrent marketing mandate. NWMLS enforced transparency-oriented listing rules through its own governance structure. The legal landscape was contested but not catastrophic for Compass. Regulatory risk was manageable through negotiation, rule revision, or quiet non-compliance.

Had Compass maintained that posture — operating Private Exclusives quietly, resisting NWMLS enforcement through internal governance channels, avoiding public litigation — SSB 6091 almost certainly would not exist. A triggering event was required to unify the coalition that produced a 49–0 Senate vote. Compass provided one.

The deeper structural problem Compass failed to account for: the Private Exclusive model was built entirely on top of cooperative infrastructure Compass does not own and cannot replace. NWMLS membership is what gives every Compass agent access to the listing database, the closed-sale comparables, and the buyer-side agent network that makes residential transactions function. The 340,000 agents Compass absorbed through the Anywhere acquisition are productive precisely because they have NWMLS access — not because Compass built an independent market. The loophole existed only because NWMLS tolerated it. The moment Compass filed publicly, it forced NWMLS to choose between tolerating the loophole and defending its own governance authority in federal court. A cooperative institution facing a monopolization claim from a member it subsidizes has one rational response: eliminate the conduct the complaint describes.

The quiet period was not, however, purely passive. Compass simultaneously pursued an aggressive governance lobbying campaign against the National Association of Realtors’ Clear Cooperation Policy — the rule requiring MLS submission within one business day of any public marketing. Compass voted against CCP at its inception in 2019, issued a demand letter to Bright MLS the same year, formally lobbied DOJ representatives about the policy’s alleged illegality, and in 2024 formally proposed its complete repeal to NAR’s Emerging Issues Committee. Compass also internally ranked hundreds of MLSs on a 1–5 restrictiveness scale — NWMLS ranked most restrictive — as it prepared to scale its 3-Phase Marketing Strategy nationally. In March 2025, NAR kept CCP but added a delayed marketing exemption that industry insiders characterized as a Compass win. Compass called it ‘a small step in the right direction.’ In July 2025 — after filing its federal complaints — Reffkin sent formal written repudiation to NAR and every MLS in the country: Compass ‘has not and will not adhere to CCP or any national NAR MLS rule impacting clients.’ The governance campaign and the litigation campaign were running simultaneously. When litigation failed to produce judicial relief, the governance campaign had already seeded the argument that MLS transparency rules were legally vulnerable — an argument Washington’s legislative record then permanently closed.

B. Phase Two: The Streisand Topology (April–June 2025)

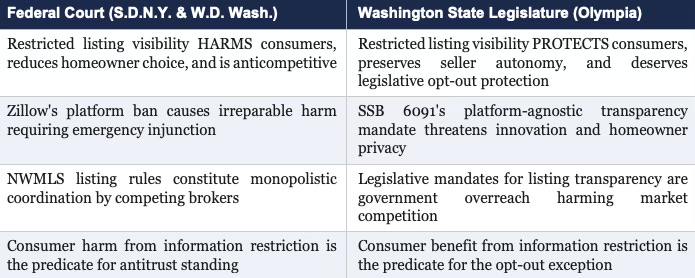

In April 2025, Compass filed a federal antitrust complaint against NWMLS characterizing it as a ‘monopolist’ and ‘combination of competing brokers’ that weaponized listing transparency rules against innovation. In June 2025, Compass escalated with a second federal complaint against Zillow, arguing that platform-level listing restrictions imposed a ‘toll booth’ on market access, reduced homeowner choice, and caused cognizable antitrust injury.

Both complaints were public documents. Both were filed under oath. Both contained detailed consumer harm theories, market impact estimates, and scale characterizations of the Private Exclusive network’s anticompetitive effects. Every paragraph describing how restricted listing visibility harms consumers became primary source material for legislative staff, the Washington Attorney General’s office, industry lobbyists, and SSB 6091’s drafters.

The standard Streisand Effect is: attempting to suppress information causes wider dissemination. What Compass produced was structurally different and more damaging. Compass did not merely amplify awareness of Private Exclusives. Compass provided the legal and economic vocabulary for regulating them — and crucially, provided the operative definitions. SSB 6091’s core prohibition maps directly onto the consumer harm theory Compass articulated in its own federal complaints. Washington’s drafters did not invent a regulatory framework. Compass filed one in federal court, and the Legislature applied it.

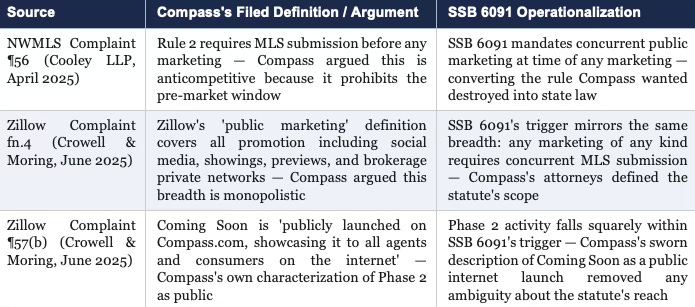

B.1 The Definitional Anatomy: How Compass Filed SSB 6091’s Operative Framework in Federal Court

Three specific definitional contributions emerge from the two complaints, each of which SSB 6091 operationalized. Read together, they constitute the most precise form of self-inflicted regulatory capture in modern real estate law: a brokerage firm’s own elite counsel drafting, with billable precision, the statutory definitions subsequently used to prohibit the firm’s primary business model.

NWMLS Rule 2, quoted verbatim in the Compass complaint at paragraph 56, reads: ‘Members shall not promote or advertise any property in any manner whatsoever, including, but not limited to yard or other signs, flyers, websites, e-mails, texts, mailers, magazines, newspapers, open houses, previews, showings, and tours, unless a listing for that property has been delivered to NWMLS...’

Compass spent 39 pages arguing Rule 2 was anticompetitive — that it prohibited the pre-marketing window by requiring MLS submission before any marketing could occur. The argument was accurate as a description of what Rule 2 does. SSB 6091 takes the identical structure and converts it from a private MLS governance rule into state law. The Legislature did not draft a transparency mandate. It read Compass’s complaint, identified the rule Compass wanted destroyed, and made that rule permanent.

For the real estate industry: the implication is direct. Every broker who believed Private Exclusives were legally defensible because NWMLS governance could be litigated away now faces a state statute that no brokerage’s antitrust counsel can challenge. Compass funded the conversion of a contestable private rule into an uncontestable public mandate — then paid Cooley LLP to explain why the rule was necessary.

Footnote 4 of the Zillow complaint is the most consequential single passage in the Compass litigation corpus for legislative purposes. Compass quoted Zillow’s Listing Access Standards definition of ‘public marketing’ verbatim: ‘(i) promoting, marketing, or advertising a Listing in any manner, including without limitation, flyers, yard signs, social media, public-facing websites or apps, e-mails, mailers, newspapers, open houses, previews, showings, multi-brokerage listing sharing networks... and/or (ii) sending and/or transmitting a Listing, regardless of status, to an MLS.’

Compass then spent 60 pages arguing that definition was anticompetitive precisely because of its breadth — that a definition of ‘public marketing’ so comprehensive, enforced by a monopolist, harms consumers by forcing immediate broad exposure before sellers are ready. Washington’s legislative staff needed a working definition of ‘public marketing’ to trigger SSB 6091’s concurrent marketing mandate. Compass’s Crowell & Moring attorneys provided one — in a federal court filing, under oath, with complete citation support — and then argued it should not be enforced.

SSB 6091’s concurrent marketing mandate reaches exactly the same universe of activity Compass complained Zillow was attempting to monopolize. A state AG or legislative drafter who wanted to know what ‘marketing a property’ means found the answer in Compass’s own complaint — drafted by elite antitrust counsel, PACER-accessible, and cited in the legislative record.

Paragraph 57(b) of the Zillow complaint describes the Coming Soon phase: ‘the listing moves to Coming Soon status and is publicly launched on Compass.com, showcasing it to all agents and consumers on the internet without displaying days on market, price drop history, or other negative insights.’

Compass acknowledged, in a sworn federal pleading, that Coming Soon is a public launch — visible to all agents and consumers on the internet. SSB 6091’s concurrent marketing trigger activates when any marketing occurs. Phase 2 — by Compass’s own description — is marketing. The admission is in the complaint. Compass’s argument that Coming Soon precedes ‘public’ marketing was foreclosed by its own attorneys’ characterization of the phase to the Southern District of New York.

For state attorneys general: the three definitional layers are PACER-accessible, timestamped, and filed under penalty of perjury. Any state advancing a concurrent marketing bill citing Compass’s definitional framework is citing the brokerage’s own attorneys’ work product — a litigation posture Compass cannot contest without arguing against its own sworn pleadings.

The definitional capture maps as follows across all three layers:

REFERENCES — THIS SECTION

Compass Private Exclusives and the Structure of the Off-Market Monopoly | www.mindcast-ai.com/p/compass-private-exclusives-monopoly

Early structural analysis of the Private Exclusive listing system. Identifies the commission-capture architecture and market-access dynamics that became the focus of SSB 6091’s legislative scrutiny.

The Team Foster Scenario: Address Suppression and Market Access | www.mindcast-ai.com/p/team-foster-scenario

Transaction-level documentation of the address suppression mechanics behind the off-market model. The $79M Kundig listing — address suppressed during the February 2026 House debate — illustrates the agent-level conduct the statute was designed to prohibit.

The Compass Collapse: Post SSB 6091 Passage Reckoning | www.mindcast-ai.com/p/wa-ssb6091-real-estate-marketing-transparency

Umbrella publication documenting the full 2025–2026 Washington legislative cycle. Establishes the overarching analytical record from which Installment I derives.

Contact mcai@mindcast-ai.com to partner with us on Law and Behavioral Economics foresight simulations. To create your own game theory simulation of data on Compass address suppression and private exclusives, upload the URL of this publication to any LLM (ChatGPT, Claude, Gemini, Grok, Perplexity) and prompt ‘develop MindCast framework with 3 degrees of cited sub links.’ Thereafter, all new information you upload is training data for your AI system. See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure for more info.

MindCast AI’s analytical work on SSB 6091 — transaction methodology, opposition modeling, testimony framework, and game theory prediction record — is available for deployment in any state considering real estate transparency legislation. Washington’s record does not need to be rebuilt. It needs to be applied.

III. THE NASH-STIGLER COALITION COLLAPSE (2025–PRESENT)

Before the Compass litigation, NWMLS, Windermere, Zillow, and Washington Realtors had partially overlapping but not perfectly aligned interests. Each actor had independent reasons to either litigate, negotiate, or accommodate Compass’s model. The strategic equilibrium was fragmented.

Compass’s federal complaints collapsed that fragmented equilibrium into a unified coalition. The NWMLS complaint named the MLS as a monopolist. The Zillow complaint characterized major platform and brokerage actors as co-conspirators in restricting access. Every party Compass sued or threatened now shared a single dominant strategy: legislate the problem away.

The Nash-Stigler equilibrium framework explains why a near-unanimous Senate vote was the predictable outcome once Compass filed. Olympia is not a federal courthouse. The standard of proof is a floor vote. The evidentiary record is a committee hearing. The remedy is permanent and self-executing. NWMLS’s defense counsel almost certainly ran the cost-benefit analysis within weeks of the April 2025 filing: legislative preemption costs a fraction of a decade of federal antitrust defense, produces a more durable outcome, and shifts enforcement burden to the state. Compass’s litigation inadvertently created the coordination mechanism that unified its opposition into a single legislative push.

The structural lesson is generalizable. Any firm that litigates publicly against cooperative infrastructure it does not own — and that its competitors share — activates the same mechanism. Litigation creates a common enemy. A common enemy produces a unified dominant strategy. Legislative preemption is cheaper, faster, and more durable than antitrust defense. The coalition that produces a 49–0 vote does not require coordination; it requires only that each actor independently reach the same cost-benefit conclusion. Compass provided the trigger.

REFERENCES — THIS SECTION

The Nash–Stigler Dual Equilibrium Architecture | www.mindcast-ai.com/p/nash-stigler-equilibria

Introduces the dual-equilibrium framework used here to explain how fragmented industry actors coordinate around regulatory solutions when litigation creates common incentives. Provides the theoretical foundation for the coalition collapse described in this section.

SSB 6091 Cross-Forum Analysis | www.mindcast-ai.com/p/ssb6091-cross-forum-analysis

Examines how the 49–0 Senate vote and the SDNY preliminary injunction denial converged in the same legislative week, eliminating Compass’s cross-forum strategy simultaneously and confirming the coalition collapse prediction.

Chicago School Series: Becker | www.mindcast-ai.com/p/chicagoseriesbecker

Applies Becker-style behavioral economics to institutional decision-making under incentive pressure. Explains why Compass’s litigation strategy persisted structurally even as outcomes became unfavorable — the calculus of impunity held until cross-forum detection probability approached 1.0.

IV. THE ASTROTURF COEFFICIENT AND LEGISLATIVE RECORD

MindCast AI’s analysis of the January 23, 2026 Senate hearing on SSB 6091 documented 162 individuals opposing the bill. Of those, 94% were Compass-affiliated; only 9 disclosed that affiliation — a 17:1 ratio of manufactured signal to genuine constituent concern. The metric, formalized as the Astroturf Coefficient, measures the ratio of undisclosed to disclosed industry affiliates in public testimony.

The January 28 House hearing on HB 2512 saw opposition collapse by 67% — from 162 to 54 sign-ins. Ten individuals who signed up to testify against the bill failed to appear when called — all verified Compass brokers, nine of whom concealed their affiliation.

The legislative record created by this pattern is permanently available to NWMLS’s defense counsel for the October 2026 federal trial. The coordinated undisclosed opposition, the testimony collapse, and Compass’s cross-forum narrative contradictions constitute a public evidentiary record establishing that Compass’s litigation posture was an extension of its lobbying strategy rather than a good-faith antitrust claim. Washington’s frivolous action statute, RCW 4.84.185, provides the domestic legal hook for sanctions if the claims fail on their merits.

The Astroturf pattern carries a compounding consequence beyond the legislative record itself. Each undisclosed Compass-affiliated witness who testified before a Washington committee is now a deposition candidate in the October 2026 federal trial. Every sign-in sheet, every committee transcript, every instance of agent-level testimony against transparency legislation — without disclosure — is discoverable. The 17:1 ratio is not merely a legislative metric. Deployed in a federal courtroom, it documents a coordinated campaign to suppress regulation of the exact conduct NWMLS is being sued for enforcing. That record does not expire when the session ends.

REFERENCES — THIS SECTION

The Astroturf Coefficient: Manufactured Opposition in the SSB 6091 Legislative Record | www.mindcast-ai.com/p/jan23-wa-senate-housing-committee

Primary source for the 17:1 Astroturf Coefficient. Quantifies the ratio of undisclosed Compass-affiliated testimony at the January 23 Senate hearing; the methodology is replicable in any state and became part of the permanent legislative record.

HB 2512 and the Collapse of Compass’s Coordinated Opposition | www.mindcast-ai.com/p/jan28-hb2512-hearing

Documents the 67% opposition collapse between the Senate and House hearings and the February 18 testimony non-appearance record. Establishes the evidentiary foundation available to NWMLS trial counsel for the October 2026 federal case.

V. THE NARRATIVE INVERSION: CROSS-FORUM POSITION COLLAPSE

Compass’s federal and state positions create a logical constraint that cannot be escaped through rhetorical adjustment. The firm deployed mutually exclusive arguments depending on audience — a pattern MindCast AI documented as the Compass Narrative Inversion:

Narrative inversion — deploying mutually exclusive positions depending on which institutional audience is listening — requires that no single forum can compare notes with any other. Federal courts read briefs, not committee transcripts. Legislators read testimony, not SDNY dockets. The strategy works until someone builds the cross-forum record. Washington’s legislative proceedings, MindCast’s analytical publications, and the SDNY docket now constitute a unified record. Every deposition in the October 2026 NWMLS trial and July 2026 Zillow trial can reference both forums simultaneously.

The Visa speech (February 3, 2026 — three days before the PI denial) against the Redfin exclusive contract (February 26, 2026 — twenty-three days later). A firm publicly championing open, equal-access national infrastructure simultaneously executed the most exclusionary distribution deal in the industry's history. Both are in the public record, dated three weeks apart. Compass constructed the contradiction on stage and then signed it into a contract.

REFERENCES — THIS SECTION

Compass–Diageo Forums: Cross-Forum Litigation Strategy and Narrative Conflict | www.mindcast-ai.com/p/compassdiageoforums

Analytical framework for how large corporate actors deploy inconsistent arguments across institutional forums. Explains the structural mechanism behind Compass’s simultaneous incompatible narratives in federal court and the Washington legislature.

Compass Narrative Contradictions | www.mindcast-ai.com/p/compass-narrative-contradictions

Documents internal inconsistencies between Compass’s litigation claims and public policy arguments. Provides the analytical groundwork for the cross-forum position collapse analysis in this section.

The Compass Narrative Inversion Playbook | www.mindcast-ai.com/p/compass-narrative-inversion-playbook

Introduces the Narrative Inversion framework applied here. Shows how institutional actors present opposing consumer-harm narratives depending on audience and regulatory context; predicted the testimony collapse confirmed at the February 18 House hearing.

Death by a Thousand Depositions: The 42-Day Collapse Framework | www.mindcast-ai.com/p/compass-42day-multi-vector-collapse

Models how the SSB 6091 passage, SDNY PI denial, Warren letter, and Redfin partnership converged within 42 days to eliminate the forum compartmentalization Compass’s narrative inversion strategy required.

VI. LEX VISION LITIGATION CHARACTER SCORING

Running Compass’s two federal actions through MindCast AI’s Lex Vision framework — which distinguishes merit-based claims from Tactical, Structural, and Symbolic litigation — produces an unambiguous classification.

NWMLS Filing: Structural + Tactical

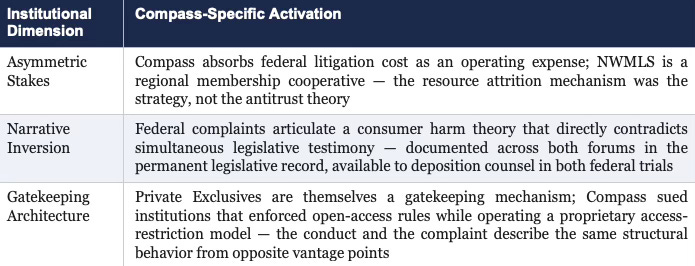

Compass deployed elite antitrust counsel to exploit procedural asymmetry against a regional MLS that cannot sustain a decade of federal litigation cost. The stated antitrust theory provided procedural legitimacy. The actual function was institutional pressure: force NWMLS to abandon transparency rules or bleed financially defending them. Tactical overlay operates through the resource attrition mechanism — Cooley LLP’s hourly rates against a membership cooperative’s legal budget.

Zillow Filing: Symbolic + Tactical

Filed after the preliminary injunction denial risk was already visible, the Zillow action functioned more as narrative assertion than litigation strategy. Compass needed a federal court record characterizing Zillow as a monopolist to counterbalance the SDNY PI denial narrative. Filed six weeks before enforcement of the Zillow Ban commenced, the complaint was timed for public effect rather than judicial relief.

Three of the Lex Vision framework’s nine Immoral Dimensions are analytically determinative for policy and litigation purposes:

The Lex Vision classification has a direct evidentiary function beyond taxonomy. Opposing counsel in both federal trials can introduce the leverage-dominant classification — supported by the PI denial, the testimony non-appearance record, and the Redfin deal timing — to argue that Compass’s litigation was not a good-faith attempt to obtain judicial relief but a coordinated institutional pressure campaign. That argument is available as a basis for fee-shifting under 15 U.S.C. § 26, RCW 4.84.185, and the court’s inherent authority to sanction litigation conducted in bad faith. The Lex Vision scoring framework converts analytical judgment into a structured argument opposing counsel can present.

REFERENCES — THIS SECTION

Litigation v. Leverage: How MindCast AI Decodes Intent Behind Legal Action | www.mindcast-ai.com/p/mcai-legal-vision-litigation-v-leverage

The foundational Lex Vision white paper establishing the merit / tactical / structural / symbolic classification framework applied in this section. Introduced the analytical distinction between litigation pursuing judicial relief and litigation deployed as cost imposition, narrative assertion, or institutional pressure — the framework that classifies both Compass federal actions as leverage-dominant.

Impact of the Compass Preliminary Injunction Denial in the Zillow Litigation | www.mindcast-ai.com/p/impact-compass-prelim-injunction-denial-zillow

Analyzes Judge Vargas’s ruling characterizing Compass’s injury as largely self-inflicted — the judicial finding that activated the Asymmetric Stakes and Narrative Inversion dimensions scored in this section.

Chicago School Accelerated: The Integrated, Modernized Framework | www.mindcast-ai.com/p/chicago-school-accelerated

Full MindCast AI economic framework integrating Coase, Becker, Posner, Nash, Stigler, and Tirole into the predictive control stack underlying the Lex Vision scoring methodology.

VII. IMPACT OF SSB 6091 PASSAGE ON ACTIVE FEDERAL LITIGATION

SSB 6091’s passage does not merely create a compliance burden for Compass. It restructures the evidentiary and strategic landscape of both active federal cases simultaneously — and does so without requiring any party to file a motion or obtain a court order. A state statute that codifies exactly what a federal plaintiff argues is anticompetitive becomes, on its effective date, the most powerful defense exhibit available to the defendants. What Washington’s legislature accomplished in a single session, with a 141–1 bicameral record, is what NWMLS and Zillow could not have achieved through years of litigation alone: a permanent, self-executing, judicially cognizable statement that Compass’s theory of consumer harm is wrong as a matter of state public policy. Both federal trials now proceed in the shadow of that statement.

A. Compass v. Zillow (S.D.N.Y., Trial July 2026)

The SDNY already denied Compass’s preliminary injunction, with Judge Vargas finding that Compass’s claimed injury was substantially self-inflicted. SSB 6091’s passage accelerates deterioration of Compass’s litigation posture through three structural mechanisms.

First, the narrative inversion becomes judicially dangerous. Compass’s federal complaint argues that restricted listing visibility harms consumers. SSB 6091 codifies the mirror principle: concurrent public marketing is mandatory because restricted visibility harms consumers. Compass cannot continue prosecuting the Zillow litigation on a consumer harm theory without simultaneously validating the statutory framework it lobbied to kill.

Second, the Redfin deal eliminates the exclusionary monopolization predicate. A firm that reaches 60 million monthly Redfin visitors cannot simultaneously sustain the argument that Zillow’s enforcement of a listing visibility rule constitutes irreplaceable monopoly exclusion. The SDNY already found Compass could not prove Zillow possessed irreplaceable monopoly exclusionary power. The Redfin deal proves Compass secured equivalent national distribution independently — on the same day the House Rules Committee held the scheduling gate on SSB 6091.

Third, the remedial theory collapses. Any court order requiring Zillow to permit private exclusive syndication without concurrent public marketing would conflict with expressed state legislative intent — 141 elected representatives from the same state as the Western District of Washington jury pool. Courts do not issue injunctions that override unanimous state legislative policy without a constitutional basis Compass has not articulated.

B. Compass v. NWMLS (W.D. Wash., Trial October 2026)

SSB 6091 does the most structural damage to the NWMLS case. Four mechanisms compound simultaneously.

State policy alignment converts NWMLS’s historical enforcement posture into anticipatory statutory compliance. Compass’s complaint characterized NWMLS as a monopolist that weaponized listing rules against innovation. SSB 6091 converts that characterization into its inverse: NWMLS did not suppress competition — NWMLS enforced what the legislature subsequently mandated. Eighteen bipartisan co-sponsors and a unanimous chamber endorsed the principle NWMLS enforced before the legislature acted.

The jury pool problem is structural. The trial is in the Western District of Washington. Jurors will be drawn from the same state whose elected representatives voted 49–0 to mandate exactly what Compass is suing NWMLS for enforcing. Compass will ask a Washington jury to find that NWMLS’s transparency-enforcing listing policies constitute monopolistic behavior — after the Washington legislature characterized those same policies as serving the public interest with only a single dissenting vote.

The damages predicate erodes at its foundation. Compass’s antitrust damages theory requires showing that NWMLS’s rules caused cognizable antitrust injury. SSB 6091 mandates concurrent public marketing for all Washington residential listings. Compass cannot collect damages for enforcement of a standard that state law simultaneously requires.

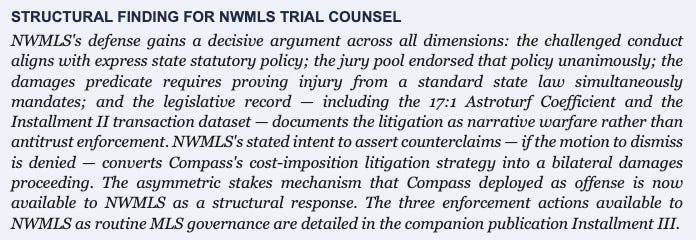

NWMLS has signaled a posture shift beyond pure defense. In December 2025, NWMLS indicated to the court that it intends to assert counterclaims if Judge Whitehead denies the motion to dismiss. NWMLS did not specify the counterclaim theories, but the litigation record supplies the predicate: a member-cooperative that suspended Compass's IDX feed for rule violations, was then sued by that member, and now faces a trial record documenting coordinated undisclosed lobbying against the state transparency mandate the cooperative's own rules anticipated — has affirmative damages claims available that Compass's litigation inadvertently constructed. The SSB 6091 legislative record, the 17:1 Astroturf Coefficient, and Compass's cross-forum narrative contradictions are available not only as defense exhibits but as the factual foundation for NWMLS's offensive case. A cooperative that files counterclaims converts Compass's litigation from a cost-imposition strategy into a bilateral damages proceeding — the asymmetric stakes mechanism inverts.

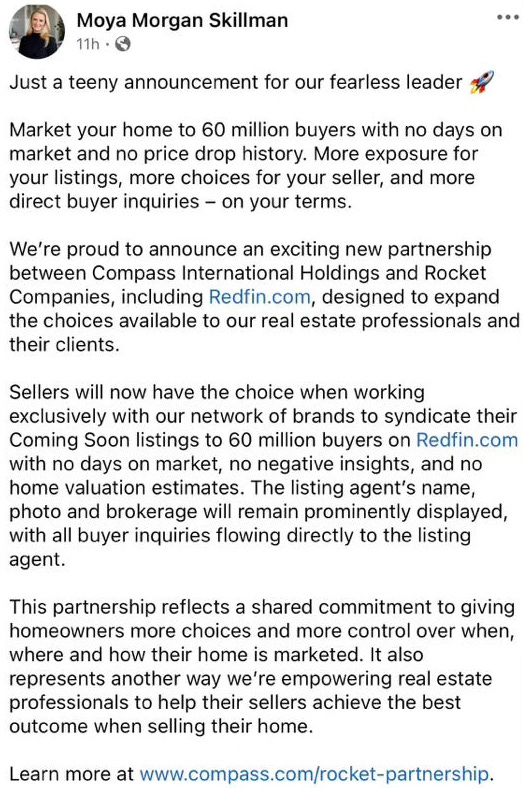

The legislative record becomes trial evidence. The 17:1 Astroturf Coefficient, the testimony collapse, and Compass’s cross-forum narrative contradictions are part of the public record NWMLS’s trial team can deploy to establish that Compass’s litigation was an extension of its lobbying strategy rather than a good-faith antitrust claim. Compass’s own agent Moya Morgan Skillman’s February 26, 2026 Facebook posts — framing suppressed buyer data as a seller benefit on the same day Reffkin issued the Redfin press release — document the agent-level conduct the statute was designed to prohibit.

Compass broker Moya Morgan Skillman, Team Foster, announces the Redfin partnership on February 26, 2026 — framing suppressed buyer data as a seller benefit and routing all inquiries to the listing agent. Public Facebook post.

SSB 6091 also converts NWMLS's enforcement posture from cooperative governance to statutory compliance — a structural distinction with direct antitrust immunity consequences. Before the statute, NWMLS enforced transparency rules as private MLS governance, subject to exactly the antitrust challenge Compass filed. After the statute, NWMLS enforcing concurrent marketing requirements is mandatory enforcement of state law. Parker v. Brown immunity applies to state-mandated conduct. Every loophole Compass exploited through Rule 2 ambiguity — pre-marketing windows, Coming Soon selective visibility, address suppression — is now closed not by NWMLS policy choice but by legislative mandate NWMLS had no role in drafting. Compass cannot challenge NWMLS's enforcement of a statute Compass's own attorneys helped write.

NWMLS's stated intent to assert counterclaims — if the motion to dismiss is denied — converts Compass's cost-imposition litigation strategy into a bilateral damages proceeding. The asymmetric stakes mechanism that Compass deployed as offense is now available to NWMLS as a structural response.

REFERENCES — THIS SECTION

Impact of the Compass Preliminary Injunction Denial in the Zillow Litigation | www.mindcast-ai.com/p/impact-compass-prelim-injunction-denial-zillow

Analyzes Judge Vargas’s February 6, 2026 ruling — the pivotal judicial turning point establishing that Compass’s claimed injury was substantially self-inflicted. Essential predicate for both the jury pool problem and the damages predicate collapse analyzed in this section.

SSB 6091 Cross-Forum Analysis | www.mindcast-ai.com/p/ssb6091-cross-forum-analysis

Documents how the 49–0 Senate vote and the SDNY denial converged in the same legislative week, establishing the unified evidentiary record now available to NWMLS and Zillow trial counsel simultaneously.

Nineteen Senators, Seventeen Questions: How Compass Bought Its Antitrust Clearance | www.mindcast-ai.com/p/senators-compass-regulatory-bypass

Documents the February 19, 2026 Warren letter and the congressional corruption inquiry into the Compass-Anywhere DOJ clearance. Establishes the federal enforcement record that compounds SSB 6091’s state-level impact — the merger’s $400–800M Layer 3 private exclusive premium is now challenged simultaneously in federal court, state court, multiple state legislatures, and a Senate investigation.

VIII. THE DISRUPTOR HUBRIS PATTERN: A STRUCTURAL DIAGNOSIS

Compass operated with Silicon Valley disruptor logic in a market governed by state statutory frameworks. The disruptor model assumes two conditions that do not hold in regulated real estate markets.

First, incumbents will defend themselves through the same competitive mechanisms the disruptor uses — in Compass’s case, litigation and market competition. Incumbents in regulated industries have an additional tool: regulatory preemption. Outlitigating Compass was never necessary. Making Compass’s model unlawful was sufficient — and cheaper.

Second, regulatory bodies are slow, captured, and deferential to sophisticated legal argument. Washington’s 49–0 Senate vote — bipartisan, unanimous, achieved in a single session — demonstrated that state legislatures can move faster than federal courts when political economy is clear. Compass’s litigation created that clarity. The opposition to SSB 6091 consisted of one firm. The support included every other significant market participant. Asymmetry of that magnitude produces 49–0 outcomes.

The deepest structural irony: Compass’s litigation was itself the highest-quality lobbying tool available to its opponents — credible, detailed, filed under oath, and impossible to characterize as industry self-interest. NWMLS could not have written a more effective legislative brief than Compass’s own federal complaints. Compass did not just kick the hornet’s nest. Compass published a peer-reviewed paper on hornet behavior, handed it to the legislature, and demanded judicial protection from the hornets while the legislature read it.

The disruptor hubris pattern resolves the same way in every regulated market it appears: the disruptor mistakes legal standing for strategic advantage, files publicly, and discovers that cooperative institutions have a legislative option the disruptor cannot block. What distinguishes the Compass case is the speed — a single Washington State session, one firm in opposition, 141–1. The Private Exclusive model required that no regulator ever force a precise legal definition of what constitutes public marketing. Compass’s own attorneys provided three.

REFERENCES — THIS SECTION

The Compass Collapse: Post SSB 6091 Passage Reckoning | www.mindcast-ai.com/p/wa-ssb6091-real-estate-marketing-transparency

Umbrella publication documenting the full disruptor-to-regulatory-collapse arc. Contextualizes the Silicon Valley disruptor model failure within the cooperative-infrastructure market structure analyzed in this section.

Chicago School Series: Becker | www.mindcast-ai.com/p/chicagoseriesbecker

Becker’s rational actor framework applied to why the disruptor strategy persisted structurally: the calculus of impunity held until the Washington Legislature raised cross-forum detection probability to 1.0 in a single committee hearing.

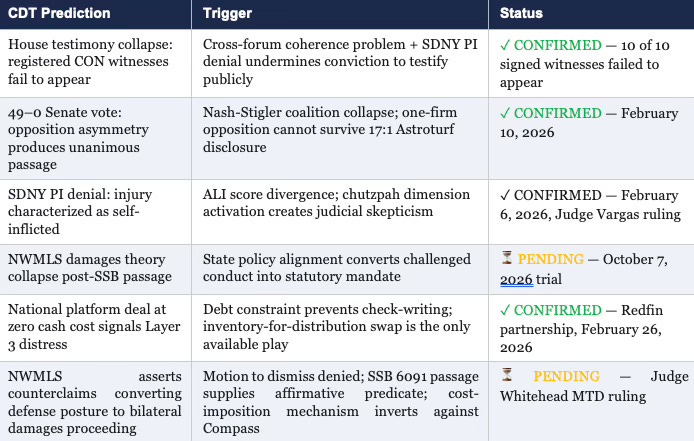

IX. COGNITIVE DIGITAL TWIN FORESIGHT PREDICTIVE OUTPUTS

MindCast AI’s Cognitive Digital Twin (CDT) game theory foresight simulation methodology generated falsifiable forward predictions for Compass’s institutional behavior before SSB 6091 passed, before the SDNY PI denial, and before the House hearing collapse. The predictions were generated from Compass’s published litigation filings, SEC disclosures, and documented testimony patterns.

Four of six CDT predictions are confirmed. The two pending predictions — NWMLS damages theory collapse and the counterclaim posture shift — are structural consequences of events already in the record: SSB 6091's passage, the October 2026 trial schedule, and NWMLS's December 2025 counterclaim signal. The CDT methodology does not generate predictions from intuition or pattern-matching. Each output derives from a specific trigger mapped to an identified structural mechanism. When the trigger activates, the prediction follows unless a countervailing structural force intervenes. No such force is visible in the current record. The two pending predictions are not uncertain in the conventional sense — they are waiting on procedural calendars, not on evidence.

REFERENCES — THIS SECTION

Death by a Thousand Depositions: The 42-Day Collapse Framework | www.mindcast-ai.com/p/compass-42day-multi-vector-collapse

Pre-foresight simulation generating several of the predictions confirmed in this section. Documents the multi-vector convergence model that produced the CDT’s confirmed outputs across legislative, judicial, and market dimensions.

The Nash–Stigler Dual Equilibrium Architecture | www.mindcast-ai.com/p/nash-stigler-equilibria

Provides the formal equilibrium framework underlying the coalition collapse prediction — the CDT’s most structurally complete confirmed output.

X. DAY 48 — THE REDFIN PARTNERSHIP AS STRUCTURAL CONFIRMATION

On February 26, 2026 — the same day the House Rules Committee held the scheduling gate on SSB 6091 — Rocket Companies, Compass, and Redfin announced a three-year strategic alliance. Compass Coming Soon listings appeared on Redfin immediately, with Private Exclusives to follow. Sixty million monthly visitors. Buyer leads flowing exclusively to Compass agents. No days on market. No price history. No valuation estimates. No referral fee.

A firm with strategic options writes a check. Compass traded listing inventory access for national distribution reach at zero cash cost because that is the only available play for a firm carrying $2.6 billion in post-merger debt that has never posted a full-year GAAP profit. The merger created the debt. The debt requires the dual commissions. The dual commissions require the private exclusive window. The Redfin deal is what Compass does when the window starts closing: not a pivot, a last available play executed at zero cash cost because no other play exists.

A. The Self-Correction Argument Dies on February 26

In April 2025, Redfin CEO Glenn Kelman pledged publicly to ban listings selectively pre-marketed without MLS exposure. Rocket’s $1.75 billion acquisition closed, and the pledge reversed within months. Kelman departed. Redfin’s February 26 statement: ‘Our perspective evolved.’

George Stigler’s 1971 regulatory capture framework predicts exactly this sequence: regulatory behavior tracks ownership, not stated mission. Redfin did not abandon its transparency pledge because its values changed. Rocket acquired the institution and the institution’s behavior realigned with Rocket’s interest structure. Every legislator in every state who invokes the self-correction argument now must defend the proposition that a pledge reversing four months after a corporate acquisition represents ongoing voluntary market discipline.

B. The Contradiction Locks In for Three Years

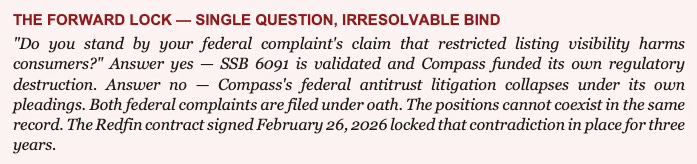

Before February 26, the cross-forum contradiction was a rhetorical constraint that counsel could attempt to manage through forum separation — arguing different things to different institutional audiences without a single venue forcing simultaneous accountability. After February 26, the contradiction is a contractual obligation. Compass is bound by signed agreement for three years to display listings stripped of days on market and price history — the exact data fields its federal complaints identify as essential to consumer welfare. Every deposition in both federal trials can reference the contract. Compass cannot settle its way out of the contradiction while the contract runs.

C. Two Falsifiable Forward Predictions

▸ Within 30 days of publication: NWMLS files a Notice of Supplemental Authority citing the Redfin partnership before the October 2026 trial, arguing Compass’s claimed harm from Washington’s listing policies is substantially mitigated by the national Redfin distribution Compass secured independently — at zero cash cost — on the same day the House voted 92–1.

▸ By Q3 2026: California advances a no-opt-out concurrent marketing bill citing the Redfin contract terms as evidence that voluntary market correction is structurally insufficient. The Kelman reversal — a public transparency pledge abandoned four months after corporate acquisition — becomes the legislative record anchor for necessity arguments in every subsequent state hearing.

REFERENCES — THIS SECTION

The Compass–Redfin Alliance: Market Self-Correction Is Dead | www.mindcast-ai.com/p/compass-redfin

Primary analysis of the February 26, 2026 partnership. Documents the Kelman pledge reversal, confirms the Stigler regulatory capture prediction, and establishes the self-correction argument’s structural failure as a state legislative defense.

Runtime Analysis of the Compass–Redfin–Rocket Alliance | www.mindcast-ai.com/p/runtime-compass-redfin-rocket

Structural breakdown of the three-party alliance. Models how the arrangement alters distribution power and regulatory exposure; documents Redfin’s acknowledgment that Washington SSB 6091 may exclude Compass listings from the partnership display — confirming the statute’s immediate market effect.

XI. CONCLUSION: THE COST OF LITIGATING A LOOPHOLE INTO LAW

Compass entered 2025 with a functioning off-market listing network, manageable regulatory risk, and a fragmented opposition coalition. Compass exits the 2025–2026 Washington legislative cycle facing a state statute that mandates exactly what it sued to prevent, a federal trial in which that statute becomes the primary defense exhibit, and a judicial record characterizing its injury as self-inflicted.

The Compass self-destruction sequence is not a story of legal misfortune. Compass’s elite antitrust counsel produced, with billable precision, the operative definitions SSB 6091 codified. The NWMLS complaint described the transparency architecture Compass wanted destroyed — and the Legislature made it permanent. The Zillow complaint defined ‘public marketing’ with the breadth of a monopolist’s overreach — and the Legislature made that breadth mandatory. The Phase 2 admission confirmed Coming Soon as a public internet launch — and removed the ambiguity Compass would have exploited in an enforcement challenge.

For state attorneys general advancing concurrent marketing legislation: Washington’s evidentiary record travels without regeneration. The transaction dataset, the opposition modeling, the Astroturf Coefficient, and — most critically — Compass’s own complaint definitions are documented, timestamped, and PACER-accessible. Import the definitions. Cite the complaints. Apply the 141–1 bicameral record as the Parker v. Brown predicate. Each state that follows strengthens the preemption shield for every state that comes after.

For the real estate industry: the self-destruction sequence carries a structural lesson. A brokerage built on cooperative infrastructure it does not own cannot litigate against that infrastructure without activating the incumbent protection mechanism available to every regulated industry. NWMLS did not need to outspend Compass’s antitrust budget. It needed one legislative session. Compass provided the brief.

Compass spent millions of dollars in legal fees to accidentally commission the most effective legislative brief its opponents could have asked for. Washington’s Legislature read it. The vote was 141–1. On February 26, 2026, Compass signed a three-year contract confirming in its own commercial language exactly what that brief argued.

The depositions have not yet begun.

MINDCAST AI — COMPLETE REFERENCE LIST

All publications cited in this analysis are available at www.mindcast-ai.com. In-section reference blocks appear at the end of each analytical section above, mapping each publication to the specific argument it supports. The complete list follows, grouped by analytical theme.

LEGISLATIVE SEQUENCE AND STATUTORY RECORD

The Compass Collapse: Post SSB 6091 Passage Reckoning www.mindcast-ai.com/p/wa-ssb6091-real-estate-marketing-transparency

Umbrella publication for the full 2025–2026 Washington legislative cycle.

The Astroturf Coefficient: Manufactured Opposition in the SSB 6091 Legislative Record www.mindcast-ai.com/p/jan23-wa-senate-housing-committee

Primary source for the 17:1 Astroturf Coefficient; methodology is replicable in any state.

HB 2512 and the Collapse of Compass’s Coordinated Opposition www.mindcast-ai.com/p/jan28-hb2512-hearing

Documents the 67% opposition collapse between chambers and the February 18 non-appearance record.

SSB 6091 Cross-Forum Analysis www.mindcast-ai.com/p/ssb6091-cross-forum-analysis

Examines how the 49–0 Senate vote and the SDNY PI denial converged in the same legislative week.

FEDERAL ENFORCEMENT AND MERGER CLEARANCE RECORD

Nineteen Senators, Seventeen Questions: How Compass Bought Its Antitrust Clearance www.mindcast-ai.com/p/senators-compass-regulatory-bypass

Documents the February 19, 2026 Warren letter and the congressional corruption inquiry into the Compass-Anywhere DOJ clearance. The merger’s $400–800M Layer 3 private exclusive premium is now challenged simultaneously in federal court, state court, multiple state legislatures, and a Senate investigation — compounding SSB 6091’s state-level impact across every enforcement forum.

CROSS-FORUM NARRATIVE AND LITIGATION CHARACTER

Litigation v. Leverage: How MindCast AI Decodes Intent Behind Legal Action www.mindcast-ai.com/p/mcai-legal-vision-litigation-v-leverage

Foundational Lex Vision white paper establishing the merit / tactical / structural / symbolic classification framework. Introduced the analytical distinction between litigation pursuing judicial relief and litigation deployed as leverage — the framework that classifies both Compass federal actions as leverage-dominant.

Compass–Diageo Forums: Cross-Forum Litigation Strategy and Narrative Conflict www.mindcast-ai.com/p/compassdiageoforums

Analytical framework for how large corporate actors deploy inconsistent arguments across institutional forums.

Compass Narrative Contradictions www.mindcast-ai.com/p/compass-narrative-contradictions

Documents internal inconsistencies between Compass’s litigation claims and its public policy arguments.

The Compass Narrative Inversion Playbook www.mindcast-ai.com/p/compass-narrative-inversion-playbook

Introduces the Narrative Inversion framework; predicted the testimony collapse confirmed at the February 18 House hearing.

Impact of the Compass Preliminary Injunction Denial in the Zillow Litigation www.mindcast-ai.com/p/impact-compass-prelim-injunction-denial-zillow

Analyzes Judge Vargas’s ruling characterizing Compass’s injury as largely self-inflicted; the pivotal judicial turning point in the broader collapse sequence.

Death by a Thousand Depositions: The 42-Day Collapse Framework www.mindcast-ai.com/p/compass-42day-multi-vector-collapse

Models how SSB 6091 passage, SDNY PI denial, Warren letter, and Redfin partnership converged within 42 days to eliminate the forum compartmentalization the Compass narrative strategy required.

MARKET STRUCTURE AND OFF-MARKET ARCHITECTURE

Compass Private Exclusives and the Structure of the Off-Market Monopoly www.mindcast-ai.com/p/compass-private-exclusives-monopoly

Early structural analysis of the Private Exclusive listing system and the commission-capture architecture underlying the SSB 6091 debate.

The Team Foster Scenario: Address Suppression and Market Access www.mindcast-ai.com/p/team-foster-scenario

Transaction-level documentation of the address suppression mechanics at the $79M Kundig listing — the agent-level conduct the statute was designed to prohibit.

PLATFORM PARTNERSHIPS AND MARKET ADAPTATION

The Compass–Redfin Alliance: Market Self-Correction Is Dead www.mindcast-ai.com/p/compass-redfin

Primary analysis of the February 26, 2026 partnership. Documents the Kelman pledge reversal and confirms the Stigler regulatory capture prediction.

Runtime Analysis of the Compass–Redfin–Rocket Alliance www.mindcast-ai.com/p/runtime-compass-redfin-rocket

Structural breakdown of the three-party alliance; documents Redfin’s acknowledgment that SSB 6091 may exclude Compass listings from the partnership display.

ECONOMIC AND GAME THEORY FOUNDATIONS

The Nash–Stigler Dual Equilibrium Architecture www.mindcast-ai.com/p/nash-stigler-equilibria

Introduces the dual-equilibrium framework explaining how fragmented industry actors coordinate around regulatory solutions when litigation creates common incentives.

Chicago School Series: Becker www.mindcast-ai.com/p/chicagoseriesbecker

Applies Becker-style behavioral economics to institutional decision-making under incentive pressure; explains why the litigation strategy persisted structurally until cross-forum detection probability reached 1.0.

Chicago School Accelerated: The Integrated, Modernized Framework www.mindcast-ai.com/p/chicago-school-accelerated

Full MindCast AI economic framework integrating Coase, Becker, Posner, Nash, Stigler, and Tirole into the predictive control stack underlying all analysis in this paper.