MCAI Lex Vision: The Compass Collapse– A Post Washington SSB 6091 Passage Reckoning

How SSB 6091 Closed the Window, What Compass Did Next, and Why the Depositions Have Not Yet Begun

Washington State Legislature SSB 6091 Real Estate Marketing Transparency (with no opt-out exception) · Senate 49–0 · House 92–1 (yeas: 92; nays: 1; absent: 0; excused: 5) · Combined bicameral: 141–1

See series Installment I: The Compass Self-Destruction Sequence, How Aggressive Federal Litigation Birthed the Legislation That Destroyed the Business Model ; Installment II SSB 6091 Has Passed. Here Is What It Now Reaches — and the Compass Enforcement Record It Inherits, Installment III Compass Plan B, Structural Circumvention After Washington SSB 6091.

I. Purpose of This Document

MindCast AI’s analytical work on SSB 6091 spans three full publications, formal public comment, and testimony before both the Washington State Senate Housing Committee and the House Consumer Protection Committee. MindCast AI’s analysis and testimony are part of the official legislative record for SSB 6091 in both chambers, where we provided the law and behavioral economics, complex litigation, and consumer-welfare rationale for the transparency mandate — contributing to the environment that produced a 49–0 Senate and 92–1 House vote.

Most importantly, MindCast modeled opposition strategy end-to-end: from Compass’s federal litigation architecture, to its federal-to-state lobbying operation, to its public communications and testimony substitution playbook. MindCast is prepared to export our work on SSB 6091 to other states considering real estate transparency laws. Washington’s evidentiary record travels to every state that follows without needing to be regenerated from scratch.

Three companion publications form the analytical foundation for this umbrella. The first — The Compass Self-Destruction Sequence — is the origin story: how Compass’s own federal antitrust lawsuits handed legislators the vocabulary, evidence, and coalition to pass SSB 6091. The second — SSB 6091: What It Reaches and the Enforcement Record It Inherits — is the operational map: the transaction record, the law’s first prospective enforcement test, and the harm the new statute does not yet reach. The third — Compass Plan B: Structural Circumvention After SSB 6091 — is the forward-looking document: the seven vectors by which Compass is likely to attempt compliance theater rather than compliance, updated by the February 26, 2026 Rocket–Compass–Redfin alliance announcement.

Read individually, each paper stands on its own. Read together, they constitute a complete institutional diagnosis. The document you are reading now updates every vector in MindCast’s original eight-vector risk framework against developments through the date of this writing, identifies three new enforcement vectors the original framework did not anticipate, and introduces three forthcoming installments carrying the post-passage analysis through the federal trial calendar, the state legislative ratchet, and the goodwill impairment question none of the active proceedings have yet forced into the open.

II. The Vote and What It Proved

SSB 6091 passed the Washington State Senate 49–0 on February 10, 2026. Bipartisan. Zero amendments. Zero absences. Compass’s lobbying operation had eleven days between committee passage and the Senate floor vote to find a single sympathetic senator willing to insert the twelve-word opt-out exception that would have preserved the private exclusive model in Washington. None emerged.

The 49–0 margin is not just a legislative outcome. It is a cash constraint diagnostic. A firm with sufficient advocacy resources finds one sympathetic senator in eleven days. Compass found none — having entered the legislative fight carrying nearly $3 billion in post-merger debt, never having posted a full-year GAAP profit, and sending employees already on payroll to testify because retaining a professional lobbying operation was not an available line item.

The House passed the bill 92–1 after the Rocket–Compass–Redfin alliance was already public. Every member who read the February 26 announcement still voted yes. The combined bicameral record stands at 141–1. One hundred forty-one elected representatives of the same state from which the Western District of Washington will draw a jury for the June 2026 NWMLS trial voted to mandate exactly what Compass is suing NWMLS for enforcing.

Before the Senate vote, Compass’s primary legislative argument was that the market would self-correct. The supporting exhibit was a public pledge by Redfin CEO Glenn Kelman in April 2025 to ban listings selectively pre-marketed without MLS exposure — cited by Compass opponents in Washington’s January 2026 Senate hearing. On February 26, 2026, Rocket Companies announced a three-year strategic alliance with Compass and Redfin. The pledge reversed. Kelman departed. Redfin’s statement: “Our perspective evolved.” George Stigler wrote in 1971 that regulatory behavior tracks ownership, not stated mission. The mechanism confirmed in a press release. Any legislator in any state who invokes the self-correction argument now must defend the proposition that a pledge reversing four months after a corporate acquisition represents ongoing voluntary market discipline.

Contact mcai@mindcast-ai.com to partner with us on Law and Behavioral Economics foresight simulations. To create your own game theory simulation of data on Compass address suppression and private exclusives, upload the URL of this publication to any LLM (ChatGPT, Claude, Gemini, Grok, Perplexity) and prompt ‘develop MindCast framework with 3 degrees of cited sub links.’ Thereafter, all new information you upload is training data for your AI system. See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure for more info.

MindCast AI's analytical work on SSB 6091 — transaction methodology, opposition modeling, testimony framework, and game theory prediction record — is available for deployment in any state considering real estate transparency legislation. Washington's record does not need to be rebuilt. It needs to be applied.

III. The MindCast Prediction Record

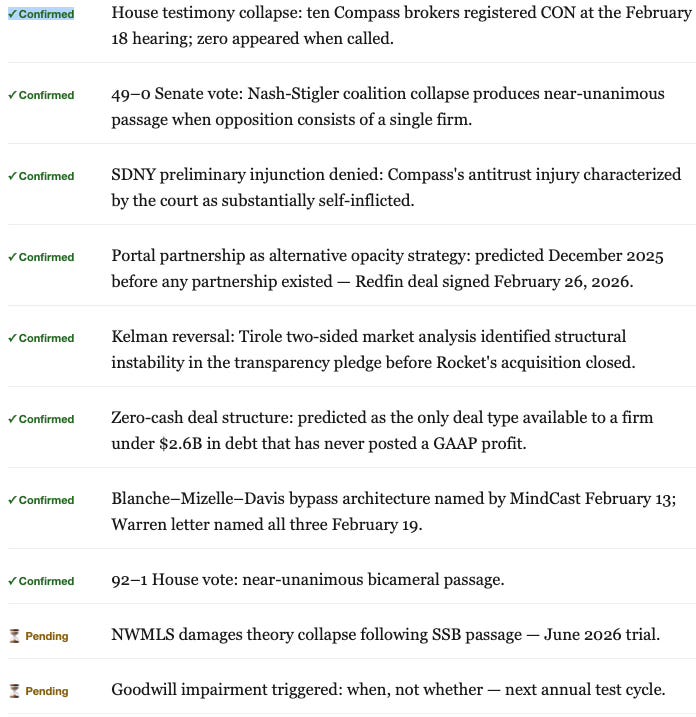

MindCast AI’s Cognitive Digital Twin methodology generates falsifiable forward predictions before outcomes materialize, published with timestamps. In December 2025 — before SSB 6091 passed, before the SDNY preliminary injunction denial, before the House hearing collapse — MindCast assigned Compass a Behavioral Drift Factor of 0.81 and a Contradiction Tolerance Coefficient of 1.62, predicting systematic deviation between stated intent and actual behavior, and an inability to maintain coherent positions across multiple institutional forums simultaneously. The following outcomes have since confirmed the model:

IV. The Opposition Architecture MindCast Documented

Understanding how Compass organized its opposition to SSB 6091 matters for two audiences: NWMLS trial counsel, who can use the legislative record to establish that Compass’s litigation was an extension of its lobbying strategy rather than a good-faith antitrust claim; and every other state legislature that will face the same playbook when a dominant brokerage opposes a concurrent marketing bill.

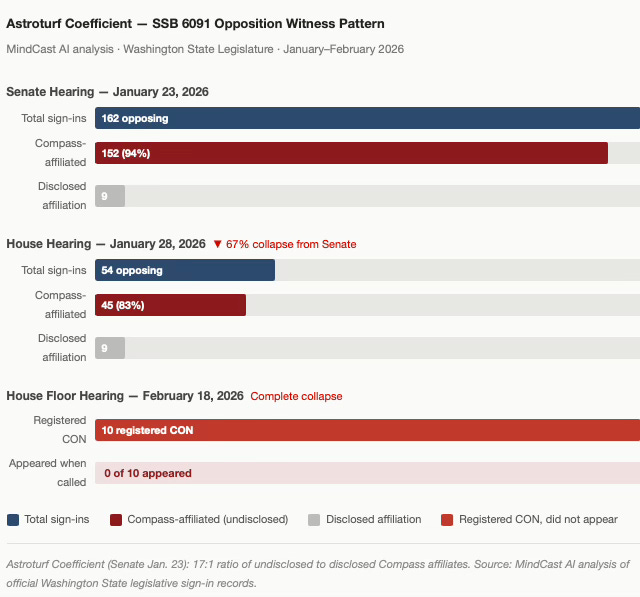

MindCast AI’s analysis of the January 23, 2026 Senate hearing documented 162 individuals opposing SSB 6091. Of those, 94% were Compass-affiliated. Only 9 disclosed that affiliation. The ratio — 17 undisclosed Compass affiliates for every 1 who disclosed — defines what MindCast formalized as the Astroturf Coefficient: a metric measuring the ratio of manufactured legislative signal to genuine constituent concern. Between the Senate and House hearings, Compass-affiliated sign-ins collapsed 67% — from 162 to 54 — as the disclosure pattern became visible to committee staff and the bill’s sponsors.

The testimony substitution pattern carries its own analytical weight. Cris Nelson — Compass’s Regional Vice President for the Northwest and its most media-credible spokesperson — signed in CON at both hearings without disclosing her Compass affiliation and testified at neither, delegating to a Compass agent with no published record of market analysis and no credibility capital that cross-examination could damage. A firm that believes its argument wins sends its best witness. Compass sent a substitute. Nelson’s media value derives precisely from the absence of adversarial questioning — she had publicly told RISMedia that Washington homeowners were “forced into a one-size-fits-all approach that can weaken their negotiating power.” The transaction record MindCast documented directly contradicts that claim. Nelson did not appear to defend it under oath, in a forum where the contradiction was permanently discoverable.

V. The February 26 Confirmation: What the Redfin Deal Proves

On February 26, 2026 — the same week the House Rules Committee held the scheduling decision on SSB 6091 — Rocket Companies, Compass International Holdings, and Redfin announced a three-year strategic alliance. Compass Coming Soon listings appeared on Redfin immediately, with Private Exclusives to follow. Sixty million monthly visitors. Buyer leads flowing exclusively to Compass agents. No days on market. No price history. No valuation estimates. No referral fee.

Three background facts are necessary to understand why the deal’s structure — not just its terms — is analytically significant. First, Compass assumed approximately $2.6 billion in debt through the Anywhere merger and has never posted a full-year GAAP profit. Second, Compass’s business model depends on capturing both the listing-side and buyer-side commission on luxury transactions, a mechanism requiring buyers to be routed through Compass’s internal network before the open market can compete. Third, MindCast’s three-layer acquisition hierarchy identified a “Layer 3 premium” — estimated at $400–800 million of the $1.6 billion acquisition price — representing the value that exists only if listings can be withheld from the open market long enough for an internal buyer to arrive first.

Against that background, the deal’s zero-cash structure is the most important fact in the announcement. A firm with strategic options writes a check. Compass traded listing inventory access for national distribution reach at zero cash cost because that is the only kind of deal available to a firm carrying $2.6 billion in debt that has never been profitable. The merger created the debt. The debt requires the dual commissions. The dual commissions require the private exclusive window. The Redfin deal is what a firm does when the window starts closing — not a strategic pivot, a last available play.

What the Contract Terms Reveal

Per Compass’s own partnership page, Compass listings on Redfin display with no days on market, no price drop history, and no home valuation estimates. Those are not the seller’s data points. They are the buyer’s. Stripping them from the buyer serves the brokerage’s commission capture architecture — not the seller’s interest in maximizing competitive exposure. Richard Posner’s Economic Analysis of Law (1973) provides the welfare framework: the test is not whether the seller consented, but whether the practice produces a net welfare gain or loss across all parties to the transaction. A brokerage that controls buyer access then captures the buyer-side commission when an internal agent closes the deal benefits twice from a single information asymmetry. The Redfin architecture scales that mechanism to 60 million monthly visitors.

Agent-Level Confirmation

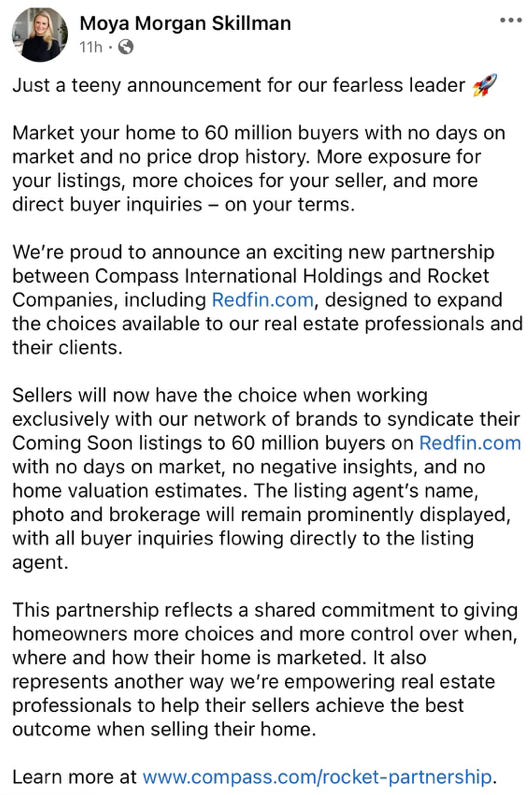

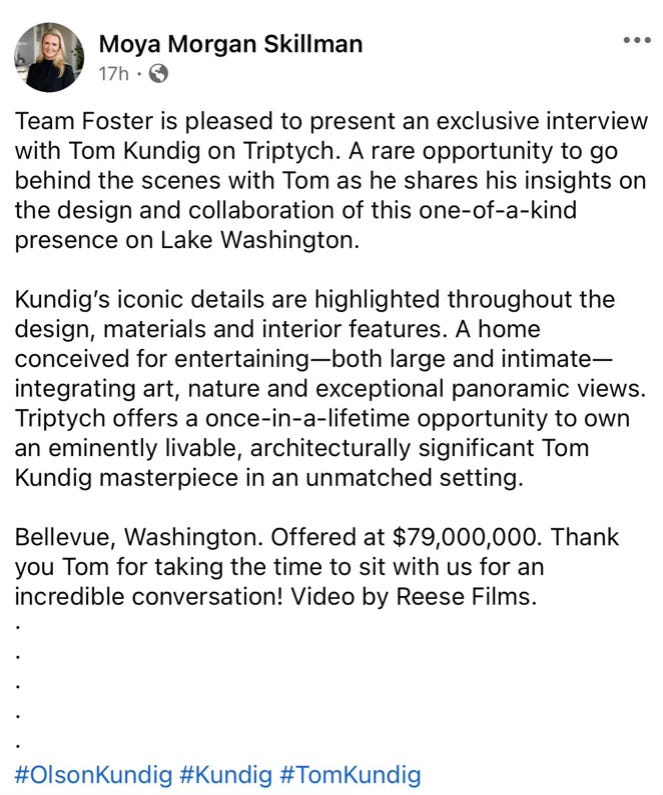

On the same day Compass issued a press release framing the partnership as a seller-choice initiative, Compass broker Moya Morgan Skillman — whose role as Team Foster co-lister and buyer-side capture vehicle is documented across thirteen months of Seattle luxury transaction data in the companion publications — posted the announcement to her public social network with this framing: “More direct buyer inquiries — on your terms. No days on market. No price drop history. No negative insights.” Sellers seeking maximum competitive exposure do not need to be told their listing will display without negative insights. Agents seeking to control buyer information do. The same day, Skillman posted content marketing for the $79 million Lake Washington estate documented in MindCast’s Address Suppression Calculus as Team Foster’s anchor suppression listing — a property catalogued in the NWMLS without a street address, marketed through an exclusive architect interview designed to generate internal buyer inquiry before broad market exposure.

Compass broker Moya Morgan Skillman, Team Foster, announces the Redfin partnership on February 26, 2026 — framing suppressed buyer data as a seller benefit and routing all inquiries to the listing agent. Public Facebook post.

Skillman markets MLS #2392995 — the $79 million Lake Washington estate documented in the Address Suppression Calculus as Team Foster's anchor suppression listing — through an exclusive architect interview designed to generate internal buyer inquiry before broad market exposure. Public Facebook post, February 26, 2026.

What the Deal Does to the NWMLS Litigation

Compass’s antitrust theory against NWMLS rests on one factual predicate: that NWMLS’s listing rules restrict Compass’s market access sufficiently to constitute exclusionary conduct under Section 2 of the Sherman Act. A firm that reaches 60 million monthly Redfin visitors cannot simultaneously sustain that argument. NWMLS’s counsel will file a Notice of Supplemental Authority on the Redfin announcement before the June 2026 trial, following the same playbook they ran within hours of the February 6 SDNY preliminary injunction denial.

More fundamentally, the deal converts the cross-forum contradiction from rhetorical problem to contractual obligation. Compass is now bound by signed agreement for three years to display listings stripped of the exact buyer data fields its federal complaints identify as essential to consumer welfare. Every deposition in both the Zillow trial (July 2026, SDNY) and the NWMLS trial (June 2026, W.D. Wash.) can reference the contract. Compass cannot settle its way out of the contradiction while the contract runs.

VI. Risk Vector Assessment

MindCast AI’s 42-Day Collapse Framework, published February 21, 2026, benchmarked eight compounding risk vectors active within six weeks of the Anywhere merger close. The framework’s core thesis: the danger to Compass is not any single proceeding. A firm the size of the combined Compass-Anywhere entity can survive a federal antitrust case, a legislative defeat, or a congressional inquiry in isolation. What it cannot survive without structural recalibration is all of those things activating simultaneously — feeding each other’s evidentiary records, with each adverse development strengthening multiple other attack surfaces at once.

No vector has improved since February 21. Three original vectors have upgraded significantly. Three new vectors have emerged that the original framework did not anticipate because the Redfin partnership did not exist when the framework was published. The eleven vectors organize into two groups by mechanism: the six vectors Compass created through its own conduct, and the five external pressure vectors the environment is now applying regardless of what Compass argues in court.

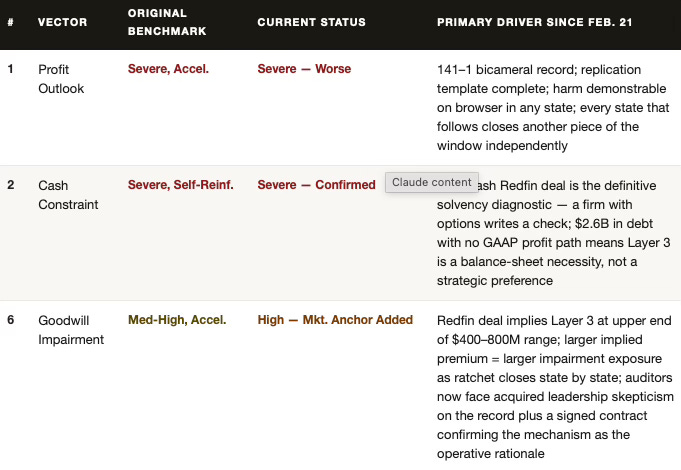

Table A-1 — Financial Vectors (1, 2, 6): The Balance Sheet Trap

Vectors 1, 2, and 6 are all downstream of the same operating condition failure: Layer 3 cannot survive at the scale the acquisition required. Profit deteriorates as the window closes state by state. Cash constraint explains why the advocacy operation that might have slowed the ratchet was underfunded from the start. Goodwill impairment is the accounting consequence when auditors can no longer treat the Layer 3 premium as a recoverable asset. No enforcement sovereign needs to act for these three vectors to cause damage — the balance sheet does the work.

Vector 6 in detail. MindCast’s original framework estimated the Layer 3 private exclusive infrastructure premium at $400–800 million of the $1.6 billion Anywhere acquisition price. The Redfin deal adds a market-implied valuation anchor the original framework lacked. If Rocket’s $1.75 billion acquisition of Redfin was premised on Compass’s exclusive listing inventory as the primary driver of partnership value — which the press release structure strongly implies — the market is pricing Layer 3 at the upper end of the range. A larger implied premium means a larger impairment exposure when the regulatory ratchet closes the window state by state. Auditors testing the goodwill assumptions recorded at close now face three compounding facts simultaneously: acquired leadership skepticism on the record, a signed contract confirming the mechanism as the strategic rationale, and a state legislative ratchet eliminating the operating condition the premium requires. The impairment question is when — not whether.

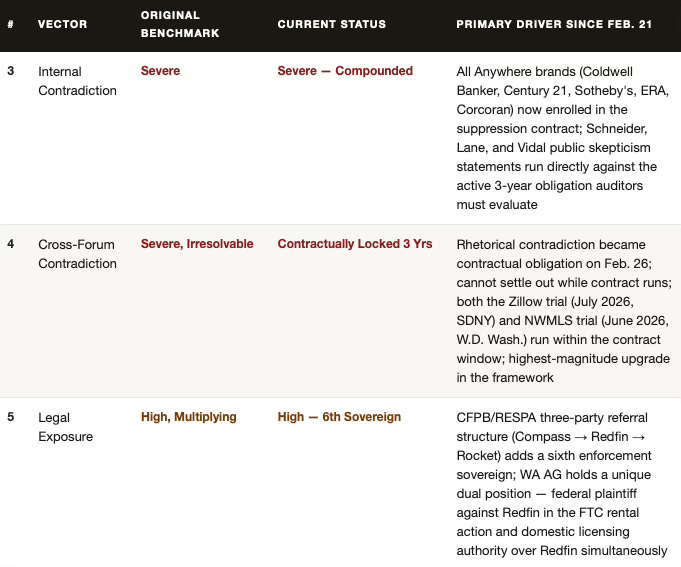

Table A-2 — Legal and Evidentiary Vectors (3, 4, 5): The Record Trap

Vectors 3, 4, and 5 are downstream of Compass’s own filings, statements, and contracts being used against it across simultaneous proceedings. Anywhere’s leadership publicly doubted the private exclusive model before the merger closed — that skepticism is now auditor-facing evidence. Compass’s federal complaints argued that restricted listing visibility harms consumers — that argument now runs directly against the Redfin contract Compass signed. Five separate legal proceedings draw from the same evidentiary substrate, and each new sworn statement in any one of them narrows the factual space available in every other.

Vector 4 in detail. Before February 26, the cross-forum contradiction was a rhetorical constraint that counsel could attempt to manage through forum separation — arguing different things to different institutional audiences without a single venue forcing simultaneous accountability. After February 26, the contradiction is a contractual obligation. Compass is bound by signed agreement for three years to display listings stripped of days on market and price history — the exact data fields its federal complaints identify as essential to consumer welfare. The irresolvable contradiction became irresolvable by contract, in a press release Compass authored and timestamped on the same day the House Rules Committee held the scheduling gate on the bill Compass lobbied to kill.

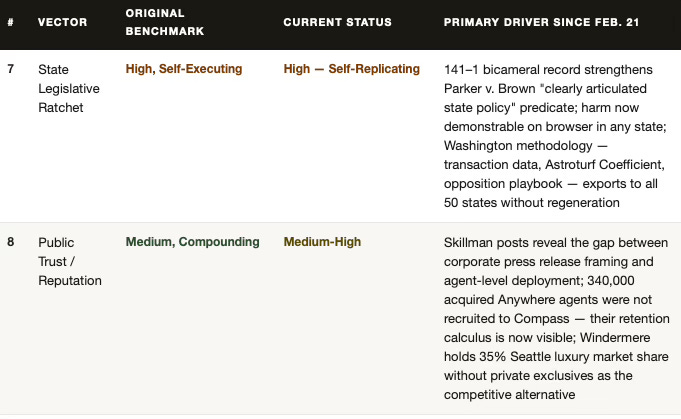

Table B1 — Market & Reputational Pressure (7–8): Original Vectors Now Accelerating

Vectors 7 and 8 were in the original February 21 framework. Both have worsened. The state legislative ratchet was always self-executing — the Redfin deal made it self-replicating by converting the harm from a theoretical argument into something demonstrable on a browser in any state capital. The reputational vector was always a lagging indicator — the Skillman posts moved it from abstract brand risk to documented agent-level conduct, with a named competitive alternative already operating at 35% luxury market share without the mechanism Compass is defending.

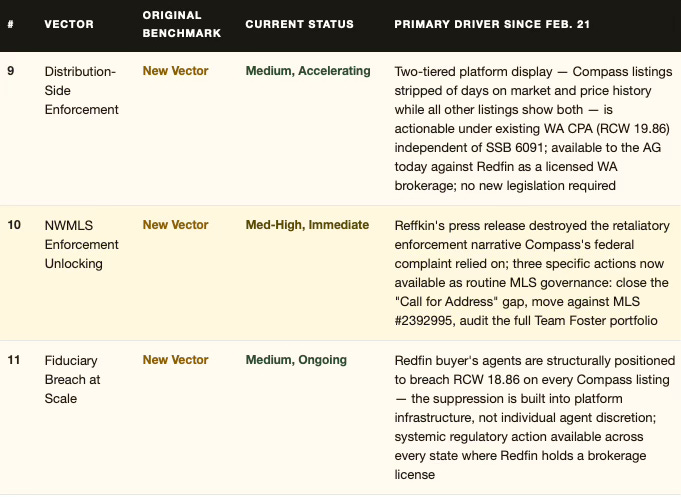

Table B2 — New Enforcement Vectors (9–11): Created by the Redfin Deal

Vectors 9, 10, and 11 did not exist on February 21. All three emerged from the Redfin partnership announcement. None require SSB 6091 to take effect, none require federal cooperation, and none require a new statute. Vector 9 is actionable today under existing Washington CPA law. Vector 10 became available the moment Reffkin’s press release destroyed the retaliatory enforcement narrative. Vector 11 operates across every state where Redfin holds a brokerage license — independently of anything happening in Washington.

The feed relationships between all three groups run in both directions. The legislative ratchet (Vector 7) tightens the cash constraint (Vector 2) by closing the Layer 3 window state by state — and the cash constraint explains why the advocacy operation failed, confirming the ratchet’s self-executing character. The NWMLS enforcement unlocking (Vector 10) generates evidentiary material that flows directly into the legal exposure vector (Vector 5). The goodwill impairment trigger (Vector 6) is fed by every state that adopts the Washington replication template. None of the eleven vectors stop running independently of each other.

VII. What NWMLS Can Now Do

Before February 26, NWMLS’s rational enforcement posture was restraint. During active federal antitrust litigation in which Compass alleged that NWMLS’s listing rules constitute exclusionary monopolistic conduct, every discretionary enforcement action NWMLS took against a Compass agent became potential exhibit material for the retaliatory enforcement narrative — the argument that NWMLS was selectively targeting Compass to suppress competition. That narrative required one factual predicate: that NWMLS rules restricted Compass’s market access in a way that harmed competition.

Compass’s own press release destroyed that predicate. The institutional cover NWMLS needed did not come from Olympia. It came from Robert Reffkin. Three specific enforcement actions are now available as routine MLS governance that were previously constrained by litigation-cost asymmetry:

Action 1 — Close the “Call for Address” Gap. NWMLS rules require an address field but do not prohibit a “Call for Address” entry. Team Foster’s address suppression architecture exploits exactly this gap — listing properties with full photographs, pricing, and specifications but no street address, preventing buyers from independently locating, researching, or approaching a property outside the Compass network. Updating the address disclosure rule is routine MLS governance after February 26. A firm with 60 million monthly Redfin visitors is not competitively harmed by an address disclosure requirement, and cannot argue otherwise in active federal litigation without immediately undermining its own antitrust theory.

Action 2 — Move Against MLS #2392995. The $79 million Lake Washington estate — the anchor listing in Team Foster’s documented suppression portfolio — carries a complete evidentiary record: the listing, the address suppression, the pattern across Team Foster’s active inventory. The enforcement predicate existed before February 26. The litigation-cost asymmetry that made exercising it irrational did not survive Reffkin’s press release.

Action 3 — Audit the Full Team Foster Portfolio. Pattern-and-practice enforcement is the correct instrument — it establishes systemic conduct, eliminates the isolated-incident defense, and creates the evidentiary record that travels directly into the June 2026 NWMLS trial as affirmative evidence of the conduct NWMLS’s listing rules were designed to prevent. When each listing in the portfolio closes, NWMLS records will document who represented the buyer. If the intra-firm routing pattern repeats, the Layer 3 model holds. If independent brokers win the buyer side at open-market rates, the regulatory pressure is already reshaping behavior before SSB 6091 formally takes effect.

VIII. The 50-State Replication Argument

Washington’s experience is a complete case study for export. Before the Redfin announcement, every state legislature that advanced a concurrent marketing bill faced the same primary obstacle: the harm was diffuse and difficult to demonstrate concretely to a committee. The Redfin partnership eliminated that obstacle. Open the Redfin website. Find a Compass listing. Compare it to any adjacent listing on the same page. The two-tiered information environment — Compass listings stripped of days on market, price history, and valuation estimates while every competing listing displays all three — is demonstrable with a browser and two tabs. A legislative staffer can show it in committee with a laptop.

Washington’s evidentiary record travels to every state that follows without regeneration: the 13-month transaction dataset documenting intra-firm buyer routing, the Astroturf Coefficient measuring coordinated undisclosed opposition, the Kelman reversal timeline, the Nelson delegation pattern, and the twelve-word opt-out amendment Compass sought across multiple hearings. Each element is documented, timestamped, and permanently accessible to any legislative staff, AG investigator, or opposing counsel that requests it.

The Parker v. Brown doctrine amplifies the ratchet’s durability. Each state that enacts a no-opt-out concurrent marketing requirement reinforces the “clearly articulated state policy” standard, making federal preemption challenges progressively weaker as the state count rises. Washington’s 141–1 bicameral record is the strongest possible predicate in a single state. A third state becomes a pattern. A fifth becomes a standard. States that move early shape the preemption landscape for every state that follows.

California is the most likely next accelerant. The California Association of Realtors and the state AG already have active tension with Compass over Private Exclusives, and 500,000 suppressed listings now appearing on Redfin provides the specific legislative hook prior California sessions lacked. Illinois matters because Chicago is Compass’s second-largest market and @properties — now a Compass International Holdings subsidiary following the Anywhere merger — carries deep political connections in Springfield. Legislators who previously deferred to @properties on local real estate matters must now reckon with the fact that @properties is part of a national information suppression architecture controlled from New York.

IX. The Three Forthcoming Installments

Three companion publications carry the post-passage analysis forward. Each addresses a distinct dimension of what SSB 6091’s passage set in motion. Brief descriptions follow for readers encountering this series for the first time.

INSTALLMENT I FORTHCOMING

The Compass Self-Destruction Sequence: How Aggressive Federal Litigation Birthed the Legislation That Destroyed the Business Model

In April 2025, Compass filed a federal antitrust complaint against the Northwest MLS characterizing it as a monopolist that weaponized transparency rules against innovation. In June 2025, Compass escalated with a second federal complaint against Zillow, arguing that platform-level listing restrictions harmed consumers and foreclosed competition. Both complaints were public documents filed under oath, containing detailed consumer harm theories and market impact estimates. Every paragraph describing how restricted listing visibility harms consumers became primary source material for Washington legislative staff, the AG’s office, and SSB 6091’s drafters. Compass did not merely amplify awareness of its private listing network — it provided the legal and economic vocabulary for regulating it. Installment I documents the full anatomy of that sequence, including the coalition dynamics that produced the 49–0 Senate vote, the documented pattern of coordinated undisclosed opposition, and why the legislative record now functions as trial evidence in the June 2026 NWMLS proceeding.

INSTALLMENT II FORTHCOMING

SSB 6091: What It Reaches and the Enforcement Record It Inherits

SSB 6091 closes the pre-MLS marketing window — the period during which a listing agent markets a property within a private network before submitting it to the database every licensed Washington agent can access. Installment II documents thirteen months of Seattle luxury transaction data establishing the mechanism the law now prohibits: three confirmed transactions where the listing agent’s own firm represented the buyer, two transactions where the same agents represented both buyer and seller simultaneously, and $63.8 million in transactions concentrated within one firm’s information-advantage zone. It also examines Washington’s highest-priced active listing — a $43.8 million Meydenbauer Bay waterfront property that Compass’s own platform recorded as having been privately marketed for 84 days before MLS submission — as the law’s first prospective enforcement test. Critically, the installment maps the enforcement harm SSB 6091 does not yet reach: the Compass-Redfin partnership’s two-tiered information display architecture on a licensed brokerage’s platform, which is actionable under existing Washington consumer protection law independently of the new statute.

INSTALLMENT III FORTHCOMING

Compass Plan B: Structural Circumvention After SSB 6091

SSB 6091’s passage did not end Compass’s effort to preserve the pre-MLS window. Running Compass’s debt-constrained institutional profile through a Nash-Stigler equilibrium analysis — where no firm surrenders a survival mechanism voluntarily — produces one mechanically predictable result: structural circumvention designed to preserve the exclusionary advantage while appearing to satisfy the law’s surface requirements. Installment III maps seven circumvention vectors Compass is likely to deploy, from weaponizing the statute’s health-and-safety exception, to pursuing regulatory capture through DOL rulemaking, to the national portal architecture that was a prediction in the December 2025 analysis and is now a signed three-year contract. The installment also documents how the Redfin deal simultaneously confirmed Compass’s circumvention strategy and destroyed its antitrust defense — eliminating the market exclusion theory Compass needs for June 2026 in the same press release in which it announced the partnership. Three specific enforcement actions now available to NWMLS as routine MLS governance are detailed, along with countermeasures available to state enforcement authorities before any of the seven circumvention vectors reaches operational scale.

X. Conclusion: The Unacquirable Premium

The 42-day collapse is not the story of a firm that made strategic errors after a reasonable acquisition. Layer 3 — the private exclusive infrastructure premium estimated at $400–800 million of the acquisition price — was not acquirable at any price that required it to survive. The mechanism’s value derived entirely from its ability to route premium inventory through internal networks before open market exposure. Deploying that mechanism at national scale — across 35 major markets, with 340,000 agents, under the institutional visibility a $1.6 billion acquisition creates — generated the legislative coordination, federal judicial scrutiny, and congressional attention that closed the window the mechanism required.

The Compass-Anywhere acquisition premium and the acquisition risk were not separable.

Acquiring the premium activated the risk. The larger the premium, the more aggressively the mechanism needed to be deployed. The more aggressively it was deployed, the faster the enforcement vectors activated. That is what an unacquirable premium looks like under Chicago School analysis: not a bad bet that happened to lose, but a structural configuration in which acquiring the asset activated the forces that destroyed it — predictably, compoundingly, and without a recovery path that did not require repricing the transaction before it closed.

Eleven compounding vectors. No exits. The internal architecture confirms the solvency constraint. The external architecture confirms the enforcement trajectory. The Redfin partnership moved all eleven simultaneously — buying narrative cover while accelerating the rest. February 26 is not Day 48 of a countdown. It is the day the countdown became a contract.

The depositions have not yet begun.

THE SINGLE QUESTION

Ask any Compass representative in any forum, at any stage of the post-passage circumvention effort: “Do you stand by your federal complaint’s claim that restricted listing visibility harms consumers?” Yes validates SSB 6091. No collapses Compass’s federal antitrust litigation. The Redfin contract makes both sides of that contradiction irresolvable for three years. Both cannot be true.

Prior MindCast Publications Referenced

The Compass-Redfin Alliance: Market Self-Correction Is Dead — www.mindcast-ai.com/p/compass-redfin

Death by a Thousand Depositions: The 42-Day Collapse Framework — www.mindcast-ai.com/p/compass-42day-multi-vector-collapse

The Compass Narrative Inversion Playbook — www.mindcast-ai.com/p/compass-narrative-inversion-playbook

The Compass-Anywhere Address Suppression Calculus — www.mindcast-ai.com/p/team-foster-scenario

The Compass Commission Consolidation Strategy and Real Estate Marketing Transparency — www.mindcast-ai.com/p/compass-private-exclusives-monopoly

Nineteen Senators, Seventeen Questions: How Compass Bought Its Antitrust Clearance— www.mindcast-ai.com/p/senators-compass-regulatory-bypass

The Astroturf Coefficient — www.mindcast-ai.com/p/jan23-wa-senate-housing-committee

SSB 6091 Cross-Forum Analysis — www.mindcast-ai.com/p/ssb6091-cross-forum-analysis

The Dual Nash-Stigler Equilibrium Architecture — www.mindcast-ai.com/p/nash-stigler-equilibria

The Tirole Phase Analysis of Advocacy-Driven Antitrust Inaction — www.mindcast-ai.com/p/tirole-advocacy-arbitrage

The Stigler Equilibrium: Regulatory Capture and the Structure of Free Markets — www.mindcast-ai.com/p/stigler-equilibrium

Federal Inaction Has Elevated State Authority — www.mindcast-ai.com/p/state-ag-federal-inaction

Judicial Process as Competitive Federalism — www.mindcast-ai.com/p/judicial-process-competitive-federalism

Chicago School Accelerated: The Integrated, Modernized Framework — www.mindcast-ai.com/p/chicago-school-accelerated