MCAI Lex Vision: SSB 6091 Has Passed. Here Is What It Now Reaches — and the Compass Enforcement Record It Inherits.

Pre-MLS Marketing Networks, Commission Capture, the Redfin Partnership, and a Replication Template for Every State Watching Washington

Installment II of The Compass Collapse — A Post Washington SSB 6091 Passage Reckoning, Installment I The Compass Antitrust Self-Destruction Sequence, Installment III Compass Plan B, Structural Circumvention After Washington SSB 6091.

Prior Published Analysis: The Compass-Anywhere Address Suppression Calculus | Compass Commission Consolidation Strategy and Real Estate Marketing Transparency | Chicago School Accelerated — Trust, Coordination, Narrative Power in Residential Brokerage | SSB 6091 Cross-Forum Analysis | The Compass-Redfin Alliance: Market Self-Correction Is Dead

SSB 6091 passed the Washington State Senate 49–0 on February 10, 2026, cleared the House 92–1 on March 3, 2026, and as of March 4 has been signed by the House Speaker and Senate President and delivered to the Governor. Governor Ferguson is expected to sign. On February 26 — while the House Rules Committee held the scheduling gate — Rocket Companies, Compass International Holdings, and Redfin announced a three-year strategic alliance. Compass Coming Soon listings began appearing on Redfin immediately. Private Exclusives to follow. Sixty million monthly visitors. Buyer leads flowing exclusively to Compass agents. No days on market. No price history. No valuation estimates. No referral fee.

The announcement killed the only remaining legislative argument against the bill: that the market would self-correct. Redfin’s CEO had pledged publicly in April 2025 to ban listings selectively pre-marketed without MLS exposure. Rocket acquired Redfin. The pledge reversed. The same platform that was the primary exhibit for voluntary market discipline became the primary national distribution infrastructure for the practice it pledged to ban — under a three-year contract, signed the same week the House Rules Committee decided whether to schedule SSB 6091.

Four audiences will find distinct value here: NWMLS, which now has legislative authority to enforce what its own rules and litigation posture prevented; Washington State enforcement bodies, which inherit a documented transaction record and a new distribution-side enforcement issue on the effective date; MLSs in other states, which face structurally identical governance gaps; and the legislatures and attorneys general of those states, who can use Washington’s transaction-level methodology to assess their own markets.

Every framework and concept is explained in full. Prior publications are cited for readers who want to go deeper — not as prerequisites. Analysis of Compass’s circumvention strategies and the Redfin partnership’s impact on the Compass v. NWMLS federal litigation are addressed in the companion study.

Three enforcement actions are available today without waiting for SSB 6091’s effective date. (1) Pull any active Washington listing disclosing a co-listing arrangement between a Compass brand and an Anywhere brand — Coldwell Banker Bain, Realogics Sotheby’s, RSVP Brokers ERA — and open a RCW 19.86 inquiry. Those are not competitive co-listings; they are intra-enterprise arrangements presented as independent representation. No new statute required. (2) Open Redfin, find a Compass listing, and compare the data fields to the listing next to it. If days on market, price history, or valuation estimates are missing on the Compass listing and present on the adjacent one, you have the predicate for a consumer protection inquiry under existing authority. (3) Screenshot the CDOM/DOM gap on NWMLS #2470280 — the $43.8M Clapp listing — before the effective date. That gap is Compass’s own system recording 84 days of pre-MLS marketing. It is the first prospective enforcement case under the new law if the listing closes after approximately June 11, 2026 with a Compass-affiliated buyer’s agent. The full analysis follows.

I. What SSB 6091 Does — and What It Does Not Do

SSB 6091 requires that Washington residential properties be marketed concurrently to all licensed agents through the MLS from the moment marketing begins. The law closes the pre-MLS window — the period during which a listing agent markets a property within a private network before submitting it to the database every licensed agent in Washington can access.

Before SSB 6091, that window was a legal gray zone. NWMLS rules governed listing submission timing and accuracy after a property entered the MLS. They could not reach marketing activity that occurred before submission. A listing agent could market a $43,800,000 waterfront property privately for 84 days — routing it through a brokerage’s internal network, generating buyer interest among affiliated agents, and narrowing the competitive buyer pool to people whose agents had network access — and submit a fully compliant MLS listing on day 85. Nothing in NWMLS’s rulebook had been violated. The harm was complete before enforcement authority began.

SSB 6091 moves the compliance clock to the moment marketing starts. The 84-day pre-MLS window documented in this analysis is no longer legal in Washington.

What the law does not do: SSB 6091 does not retroactively penalize transactions that closed before its effective date. The documented transactions in this analysis are not themselves subject to enforcement under the new law. Their value is evidentiary and structural — they demonstrate the mechanism the law now prohibits, identify the network that operated it, and establish the analytical template for what enforcement bodies should look for in Washington and what legislators and AGs in other states should look for in their own markets.

What the law does not yet reach: SSB 6091 targets the listing-side practice — withholding a property from concurrent MLS submission. The Compass-Redfin partnership creates a second, distribution-side harm that operates independently: a licensed brokerage displaying listings on a consumer-facing platform with selectively suppressed buyer data fields — no days on market, no price history, no valuation estimates — while displaying all three fields for every competing listing. That two-tiered information architecture is not a listing compliance issue. It is a consumer protection and fiduciary duty issue reachable under existing Washington law independent of SSB 6091. Section VI addresses it specifically.

II. Why NWMLS Could Not Enforce This Itself — and Why That Matters for Other States

Understanding why legislative action was necessary — rather than MLS rule enforcement alone — is essential context for both Washington enforcement bodies and other states assessing their own situations. Three distinct constraints prevented NWMLS from closing the gap on its own.

A. The Scope Gap

NWMLS rules are transaction-compliance rules. They require listings to be submitted accurately and on time after a property enters the system. They cannot reach the pre-submission marketing window by design — NWMLS holds jurisdiction only over listings that agents have already submitted to it. Every transaction documented in Section III reached NWMLS in full compliance. The suppression harm occurred before submission. The gap is structural, not a failure of enforcement will.

SSB 6091 fills the gap precisely because it is a statute, not an MLS rule. It applies from the moment marketing begins regardless of whether or when the listing reaches the MLS. That distinction is the central legislative lesson for every other state: MLS governance cannot close a pre-submission window. Only statutory authority can.

B. The Litigation Constraint

Compass filed a federal antitrust lawsuit against NWMLS in April 2025, alleging that NWMLS’s mandatory submission rules constitute anticompetitive monopolistic conduct. Trial is scheduled for October 2026 in the Western District of Washington. During active federal antitrust litigation, NWMLS enforcement actions against named Compass agents become exhibit material for Compass’s narrative that NWMLS selectively enforces rules to suppress Compass. The litigation posture functionally constrained NWMLS’s enforcement capacity — not because NWMLS lacked authority, but because exercising it created legal risk in the federal proceeding.

The Redfin partnership compounds this constraint in a specific way. When Compass secures distribution to 60 million monthly Redfin visitors, the “exclusion from market” argument Compass has been running against NWMLS weakens materially. NWMLS’s counsel filed a Notice of Supplemental Authority within hours of the February 6 Compass v. Zillow preliminary injunction denial. The Redfin announcement is a stronger factual predicate for the same motion. Analysis of the full litigation impact is in the companion study.

That dynamic is not unique to Washington. Any state where a dominant brokerage is simultaneously litigating against the MLS faces the same enforcement paralysis. Legislative action — creating a statutory obligation enforced by state authority — is the only mechanism that escapes that constraint.

C. The Structural Conflict

NWMLS is a broker-owned MLS with six Windermere-affiliated members on its 15-seat board. Windermere is the dominant competing firm to Compass in the Seattle luxury market and appeared on the buyer side of multiple Foster/Skillman transactions in the dataset documented in Section III. Aggressive NWMLS enforcement against Compass’s top listing team directly benefits NWMLS’s own owner-brokerages. Even where enforcement is warranted on the merits, that governance structure makes NWMLS the wrong primary enforcement vehicle. State statutory authority does not carry that conflict.

For other states: before recommending that your MLS enforce its own rules against the dominant pre-MLS network operator, assess whether your MLS board includes affiliated brokers from competing firms. If it does, you have the same structural conflict. Legislative action is the appropriate path.

D. The Compass Public Record — and the Delegation Signal

Compass’s Regional Vice President for the Northwest, Cris Nelson, was the company's designated public spokesperson on pre-MLS marketing and private exclusives while the legislative debate ran in the trade press. Her public record is specific and documented across three publications.

On seller demand (Compass press release, April 25, 2025):

“We’ve seen strong demand from Seattle homeowners for pre-marketing options. When given the choice, 36% of homeowners working with a Compass agent in Seattle chose to pre-market their home as a Compass Private Exclusive.”

On seller protection (RISMedia, April 17, 2025):

“Homeowners in Washington State are asking why they are the only ones in America without a choice in how they sell their homes... Compass agents in the area have seen firsthand how these restrictions hurt sellers. Unlike in other states, Washington homeowners are forced into a one-size-fits-all approach that can weaken their negotiating power and reduce their home’s value.”

On NWMLS rules as anticompetitive (Inman, April 25, 2025):

“This is a stark example of monopolistic control, with NWMLS having 100% market share of real estate agents, that limits homeowner choice, stifles competition and sets a dangerous precedent for broker accountability and market fairness.”

Sources: Compass newsroom, April 25, 2025 | RISMedia, April 17, 2025 | Inman, April 25, 2025

At the January 23 Senate hearing and the January 28 House hearing — the two proceedings where those claims could have been cross-examined under oath — Nelson did not appear. She delegated testimony to Brandi Huff, a Compass agent. Nelson signed in CON at both hearings without disclosing her Compass affiliation, and testified at neither.

The delegation itself is an analytical signal. The executive who told RISMedia that Washington homeowners were “forced into a one-size-fits-all approach that can weaken their negotiating power” sent a subordinate to carry that argument in the only forum where it could be tested. The cross-forum pattern — senior executive for trade media, junior agent for legislative testimony — is consistent with a public relations strategy designed to shape narrative without creating an evidentiary record subject to cross-examination.

The 36% seller demand figure requires specific enforcement scrutiny. It measures Compass clients who chose a private exclusive when the option was offered by their Compass agent. It does not measure whether those sellers understood that pre-marketing within Compass’s network statistically produces a Compass agent on the buyer side — which is exactly what the transaction record in Section III documents.

The opposition witness pattern was consistent with that selective disclosure posture. MindCast AI analysis identified a 17:1 ratio of undisclosed to disclosed Compass company affiliations among opposition witnesses — 162 Compass-affiliated witnesses at the Senate hearing, only 9 of whom disclosed their affiliation. Between the Senate and House hearings, Compass-affiliated sign-ins dropped 67%, from 162 to 54, as the disclosure pattern became visible.

E. The Death of the Self-Correction Argument

The most important legislative consequence of the February 26 Redfin announcement is the destruction of the self-correction defense — not merely its credibility, but its primary evidentiary exhibit.

In every prior legislative session where legislators introduced concurrent marketing legislation, industry opponents deployed market self-correction as the procedurally defensible reason for delay: the market is already moving, voluntary action is underway, legislation is premature. Redfin CEO Glenn Kelman’s April 2025 public pledge to ban listings selectively pre-marketed without MLS exposure was the argument’s primary exhibit. Compass opponents cited it in Washington’s January 2026 Senate hearing. A sitting CEO of the second-largest portal publicly committing to ban the practice gave the self-correction argument the institutional weight it needed.

Trace what happened to that exhibit: Kelman recognized the consumer harm — the pledge itself is an admission that harm exists. Rocket acquired Redfin. The pledge reversed within months. Kelman departed. Redfin’s February 26 statement: “Our perspective evolved.” The reversal had nothing to do with new evidence about consumer welfare. Ownership changed, and the institution’s behavior followed ownership — exactly as George Stigler’s 1971 regulatory capture framework predicted.

A legislator in any state who invokes self-correction today must defend the proposition that a pledge that reversed within months of a corporate acquisition represents ongoing voluntary market discipline. No legislator can hold that position once handed the Kelman timeline in a hearing.

The Redfin partnership compounds the destruction. Redfin didn’t merely reverse its pledge. Redfin became the primary national distribution infrastructure for the practice it pledged to ban — under a three-year contract, at zero cash cost to Compass. The self-correction argument required believing that competitive market pressure would discipline information suppression. February 26 produced the largest single-day expansion of information suppression infrastructure in the industry’s history, executed by the platform that was supposed to be the market’s corrective mechanism.

References — Section II

The Compass-Anywhere Address Suppression Calculus | www.mindcast-ai.com/p/team-foster-scenario — The foundational 130-transaction simulation establishing the detection-ceiling arithmetic that explains why MLS enforcement alone cannot close the pre-submission window. Section II’s structural constraints are downstream of the game theory architecture documented there.

The Astroturf Coefficient | www.mindcast-ai.com/p/jan23-wa-senate-housing-committee — Primary source for the 17:1 undisclosed-affiliation ratio and the opposition witness methodology referenced in Section II.D.

The Compass-Redfin Alliance: Market Self-Correction Is Dead | www.mindcast-ai.com/p/compass-redfin — Primary analysis of the Kelman pledge reversal and the Stigler regulatory capture mechanism confirmed on February 26.

Contact mcai@mindcast-ai.com to partner with us on Law and Behavioral Economics foresight simulations. To create your own game theory simulation of data on Compass address suppression and private exclusives, upload the URL of this publication to any LLM (ChatGPT, Claude, Gemini, Grok, Perplexity) and prompt ‘develop MindCast framework with 3 degrees of cited sub links.’ Thereafter, all new information you upload is training data for your AI system. See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure for more info.

MindCast AI’s analytical work on SSB 6091 — transaction methodology, opposition modeling, testimony framework, and game theory prediction record — is available for deployment in any state considering real estate transparency legislation. Washington’s record does not need to be rebuilt. It needs to be applied.

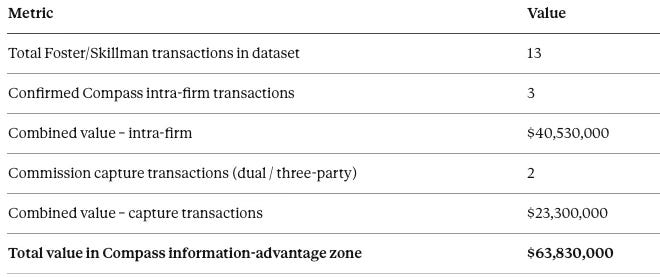

III. The Transaction Record SSB 6091 Inherits

The following 13-month dataset from Seattle Agent Magazine’s monthly Top-10 sales rankings documents the Foster/Skillman team’s luxury transaction pattern from January 2025 through January 2026 — the enforcement baseline, the documented conduct SSB 6091 was designed to prohibit, and the pattern recognition template for Washington enforcement bodies and other states’ AGs.

The full 130-transaction simulation, detection-ceiling arithmetic, and Nash-Stigler equilibrium analysis underlying this dataset are published in The Compass-Anywhere Address Suppression Calculus (www.mindcast-ai.com/p/team-foster-scenario). That publication asked whether a rational firm would scale the architecture. Section III documents what enforcement now looks like against the firm that deployed it.

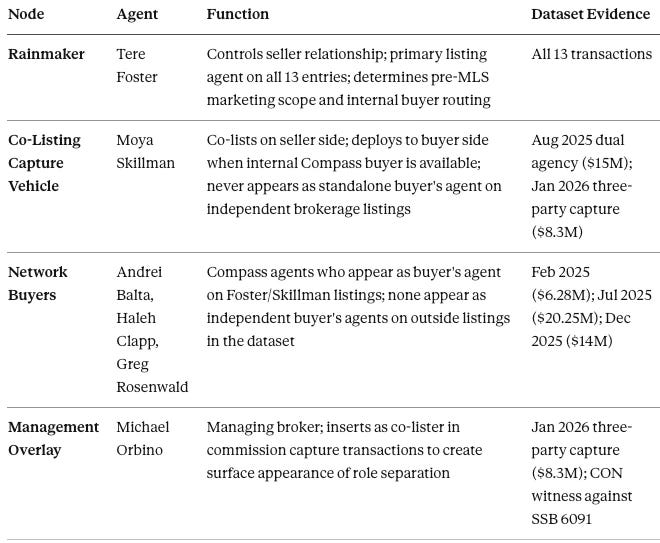

A. The Network Architecture

Pre-MLS marketing does not operate as isolated agent decisions. In the Seattle luxury market, it operates as a structured network with defined roles and predictable routing outcomes.

The pattern is structurally invariant: Foster controls access to the seller; Skillman or a network buyer captures the buyer side when an internal Compass buyer is available. Three separate intra-firm buyer routings in 13 months, with three different Compass agents, on the same waterfront corridors. That is a network operating as designed, not coincidental outcomes.

B. Anomalous Transactions — Structural Breaks Only

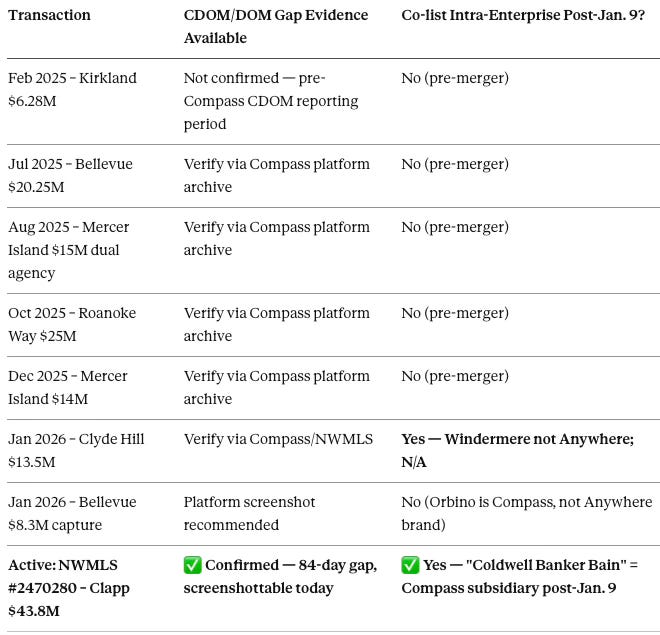

The full 13-entry transaction log is available in the prior reference publications. The table below isolates only the transactions that document the mechanism: intra-firm buyer routing, commission capture, and dual/three-party agency. Standard competitive transactions — where an independent buyer’s agent from an outside firm represented the buyer — are omitted. Their omission is the point: in a normal market, every row would look like those.

Apr 2025 ($12.5M, Coldwell Banker Bain buyer’s agent) and Sep 2025 ($10.4M, Coldwell Banker Bain buyer’s agent) are additionally flagged: Coldwell Banker Bain became a Compass International Holdings subsidiary on January 9, 2026, rendering both transactions retroactively intra-enterprise for disclosure purposes.

Dataset Summary

Investigator Triage Grid

CDOM/DOM gap evidence is self-authenticating on Compass’s own platform (Platform Self-Authentication Rule, Section IV.C). Screenshots should be taken and preserved before the effective date. Intra-enterprise co-listing status is determined by whether the co-listing firm is an Anywhere Real Estate brand post-January 9, 2026.

C. The Three Intra-Firm Transactions

February 2025 — 13415 Holmes Point Drive NE, Kirkland — $6,280,000

Listing: Tere Foster (Compass) and Shirley Shirley (RE/MAX Whatcom County). Buyer’s agent: Andrei Balta of Compass. Outside agents at Windermere, John L. Scott, and every independent firm had no equivalent access to pre-MLS marketing information. Balta’s Compass affiliation placed him inside the network the private marketing window was built to serve.

July 2025 — 9441 Lake Washington Blvd. NE, Bellevue — $20,250,000

Listing: Tere Foster and Moya Skillman of Compass. Buyer’s agent: Haleh Clapp of Compass. The highest-dollar confirmed intra-firm transaction in the dataset. Compass agents handled both sides of the Seattle area’s most expensive residential transaction that month. Clapp’s buyer-side role here is directly relevant to Section IV — six months later she listed her own property using the same pre-MLS mechanism on the same waterfront corridor.

December 2025 — 7010 N. Mercer Way, Mercer Island — $14,000,000

Listing: Kelly Weisfield and Tere Foster of Compass. Buyer’s agent: Greg Rosenwald of Compass. A third confirmed intra-firm routing on the Mercer Island waterfront corridor within twelve months. Three Compass agents, two from Team Foster’s network. The buyer-side commission stayed inside one firm.

D. The Two Commission Capture Transactions

August 2025 — 1628 72nd Ave. SE, Mercer Island — $15,000,000 — Dual Agency

Foster and Skillman represented both the seller and the buyer simultaneously. NWMLS records four role designations on a single transaction: Tere Foster — Listing Broker; Moya Skillman — Co-Listing Broker; Tere Foster — Buyer Broker; Moya Skillman — Co-Buyer Broker. No independent buyer’s agent. Total commission captured by the same two agents: $750,000. Washington law requires written, informed dual-agency consent. The structural enforcement question is not whether consent forms were signed — it is whether a seller could have understood, at engagement, that the team’s operating model systematically routes buyer-side representation back to the listing broker when an internal buyer is available.

January 2026 — 10620 SE 22nd St., Bellevue — $8,300,000 — Three-Party Capture

Listed by: Tere Foster and Michael Orbino of Compass. Bought with: Moya Skillman of Compass. Foster controls the seller relationship. Orbino — a managing broker — inserts as co-lister, creating the surface appearance of role separation. Skillman is then deployed to the buyer side. Seller’s representation, co-listing fee, and buyer’s commission all flow to the same Compass team while presenting the appearance of separate representation.

NWMLS sequence: listed November 22, 2025; pending November 26, 2025; sold January 12, 2026 at $8,300,000 — $198,000 below list. The buyer’s agent had advance knowledge the property would be listed before any independent agent, because she was on the listing team.

Nelson told RISMedia that Compass’s pre-marketing approach existed because Washington homeowners were “forced into a one-size-fits-all approach that can weaken their negotiating power.” The January 2026 Bellevue transaction documents the opposite: a seller whose buyer’s agent was on the listing team, whose property went pending in four days, who accepted $198,000 below list. The private network did not protect this seller’s negotiating power. It determined who the buyer would be before any independent agent knew the property existed — and Nelson sent Brandi Huff to the Capitol rather than defend that outcome herself.

References — Section III

The Compass-Anywhere Address Suppression Calculus | www.mindcast-ai.com/p/team-foster-scenario — The complete 130-transaction dataset, detection threshold analysis, and Nash-Stigler equilibrium modeling from which the 13-entry enforcement record above is derived. The revenue-ceiling finding — that no price threshold simultaneously generates material revenue and avoids the Stigler detection threshold — establishes why the architecture cannot scale and why SSB 6091 was the necessary instrument to close it.

Compass Commission Consolidation Strategy and Real Estate Marketing Transparency | www.mindcast-ai.com/p/compass-private-exclusives-monopoly — Documents the three-node routing architecture (rainmaker / co-lister capture vehicle / management overlay) and the Layer 3 private exclusive infrastructure premium that the transaction record in this section instantiates at the team level.

IV. The Active Listing: SSB 6091’s First Prospective Enforcement Case

The transactions in Section III closed before SSB 6091’s effective date. They are the historical record the law inherits. The following listing is the prospective enforcement test — Washington’s highest-priced active residential listing, marketed for 84 days before MLS submission, whose continued pre-MLS marketing window after the Governor’s signature is subject to enforcement under the new law.

A. Why Price Tier Defines the Enforcement Stakes

At the trophy asset tier ($15M–$20M+), buyer pools often shrink to single digits. Transactions resemble private placements. Price discovery does not emerge from market competition — it depends entirely on which buyers are introduced to the property and in what sequence. MindCast AI’s Chicago School Accelerated analysis documents the nonlinear risk structure across luxury price brackets: at the entry tier, enough buyers exist that the market clears despite pre-MLS marketing. At the trophy tier, pre-MLS marketing does not inconvenience outside agents. It structurally determines who the buyer pool is.

At $43.8M, the Clapp listing is beyond that tier. Pre-MLS marketing at this price is buyer pool selection — and SSB 6091 prohibits exactly that.

B. The “Call for Address” Mechanism — and Why Agent Access Doesn’t Cure It

Compass will argue — and has argued — that any licensed agent could show a suppressed listing. The argument is technically accurate and strategically irrelevant.

On NWMLS listings with suppressed public addresses, the address suppression operates only on consumer-facing portals — Zillow, Redfin, Realtor.com, and Compass’s own public pages. Inside the NWMLS agent portal, licensed members see private remarks, showing instructions, lockbox access, and sufficient location detail to contact the listing agent and schedule a showing. No licensed agent is locked out of the property itself.

The suppression serves one primary function: it prevents buyers from identifying the property independently. A buyer who cannot find the address cannot bring it to their own agent, cannot run their own comparable sales analysis, cannot research prior ownership or tax history, and cannot approach the transaction with the same informational baseline the listing agent’s network already has from 84 days of pre-MLS marketing.

By the time an outside agent’s client arrives through the public MLS, the Compass network has already had the pre-MLS window to route an internal buyer. The “any agent could show it” argument describes access at the end of the sequence. The suppression operates at the beginning — during buyer discovery, when the network forms the buyer pool and anchors price expectations. On MLS #2392995 — the $79M Lake Washington estate listed without an address — a buyer the Compass network routes during the pre-MLS window is not competing on equal terms with a buyer whose agent discovers the listing after MLS submission. The network already selected the first buyer before the second buyer knew the property existed.

SSB 6091 reaches this mechanism precisely. The concurrent marketing requirement eliminates the pre-MLS window during which buyer pool selection occurs — not merely the point at which a licensed agent can schedule a showing.

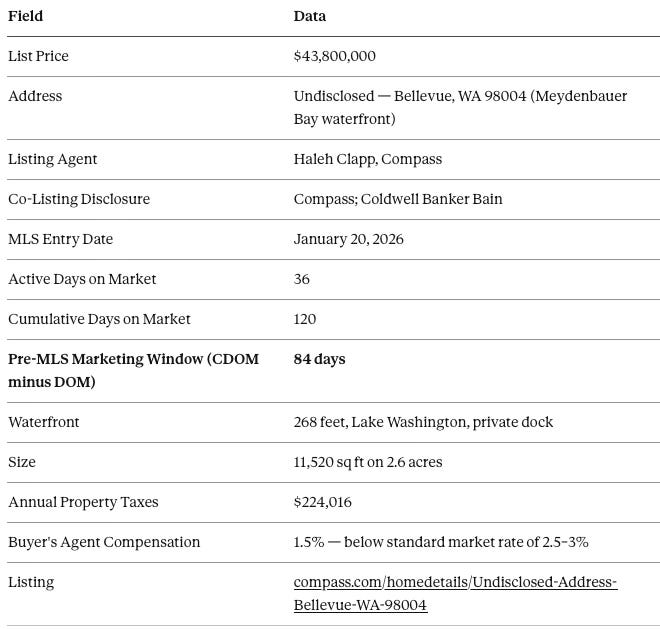

C. NWMLS #2470280 — Haleh Clapp, Compass — Active as of February 2026

Platform Self-Authentication Rule: When a brokerage platform publishes both Cumulative Days on Market (CDOM) and Days on Market (DOM), the delta between them is the platform’s own admission of pre-MLS marketing duration. Compass’s own platform supplies the 84-day pre-MLS window figure: Compass reports both “Days on Market” (time since MLS submission) and “Cumulative Days on Market” (total tracked marketing period including pre-MLS activity). The gap between those two figures is the platform’s own record that marketing began before MLS submission — not an inference. Compass’s own system recorded Compass’s own conduct. Don’t subpoena. Screenshot.

D. The Network Connection and the Post-Merger Disclosure Problem

The July 2025 transaction establishes Haleh Clapp’s position in the Foster/Skillman network: she acted as buyer’s agent on the $20,250,000 confirmed intra-firm transaction on the same waterfront corridor. Six months later, she listed her own property using the same pre-MLS mechanism.

The co-listing disclosure reads “Compass; Coldwell Banker Bain.” Before January 9, 2026, that represented two independent firms. After January 9 — eleven days before this listing entered the MLS — Coldwell Banker Bain became a Compass International Holdings subsidiary. What presents as competitive co-listing is structurally single-enterprise representation. The MLS disclosure framework has not caught up to the corporate consolidation.

E. The Below-Market Co-op Fee — Now a Two-Layer Signal

The 1.5% buyer’s agent compensation on a $43.8M transaction creates a $438,000 gap versus the standard 2.5% rate. Under the Redfin partnership terms — which strip days on market, price history, and valuation estimates from Compass listings — an independent buyer’s agent now faces both an information disadvantage and an economic signal simultaneously. The fee structure that makes sense only if Compass expects to control the buyer side operates in tandem with a platform architecture that routes buyer inquiries to Compass agents first. The two suppression mechanisms — fee and data — now compound each other at national scale.

F. What Enforcement Looks Like if This Listing Closes Under the New Law

If the Clapp listing closes after SSB 6091’s effective date with a Compass-affiliated buyer’s agent, Washington enforcement authorities have a complete record:

84 days of pre-MLS marketing documented by Compass’s own platform

Listing agent confirmed in the Foster/Skillman network who previously bought a Foster listing as buyer’s agent on the same corridor

Co-listing disclosure presenting two entities now under a single corporate parent

Below-market co-op fee operating alongside Redfin’s information-suppressed display architecture

Buyer’s agent, if Compass-affiliated, completing the same intra-firm circuit documented three times in the prior 12 months

If the buyer’s agent is independent, the enforcement question becomes the pre-MLS window alone — 84 days of marketing to a network that excluded every independent agent in Washington’s largest luxury market, with Compass’s own platform as the evidentiary source.

The enforcement pathway. Washington’s Department of Licensing (DOL) enforces SSB 6091 through RCW 18.85, which regulates real estate licensees. A violation of the concurrent marketing requirement triggers DOL’s Real Estate Program via complaint, investigation, and license discipline. The AG’s consumer protection division holds parallel authority under RCW 19.86 — particularly where the pre-MLS window operates alongside the post-merger disclosure failures documented in Section V. NWMLS retains authority to enforce its own listing rules independently and may move against the “Call for Address” mechanism as a separate MLS governance matter now that the Redfin partnership has substantially weakened the litigation-constraint argument. All three enforcement tracks — DOL licensing, AG consumer protection, and NWMLS governance — run independently and simultaneously. SSB 6091 creates the predicate for all three. The Clapp listing, if it closes under statutory coverage with a Compass-affiliated buyer’s agent, activates all three simultaneously for the first time.

References — Section IV

The Compass-Anywhere Address Suppression Calculus | www.mindcast-ai.com/p/team-foster-scenario — The detection calculus showing why the trophy-asset tier ($20M+) was the only price range where Nash stability held for address suppression, and why the Clapp listing’s profile fits that tier precisely.

Chicago School Accelerated — Trust, Coordination, Narrative Power in Residential Brokerage | www.mindcast-ai.com/p/chicago-accelerated-compass-trust — Nonlinear risk structure across luxury price brackets; establishes the trophy-asset buyer pool selection dynamic that makes pre-MLS marketing at $43.8M categorically distinct from pre-MLS marketing at lower tiers.

V. The Post-Merger Disclosure Problem

The Compass–Anywhere merger closed January 9, 2026. Anywhere’s portfolio includes Coldwell Banker, Sotheby’s International Realty, Century 21, Corcoran, ERA, Better Homes and Gardens Real Estate, and Christie’s International Real Estate. Combined: approximately 340,000 agents, $415 billion in combined 2024 sales volume, operating under Compass International Holdings.

The disclosure form was not redesigned when the merger closed. That is the problem. State-level real estate disclosure frameworks require agents to identify their firm affiliation — not their corporate parent’s ownership structure. When two brands merge under a common parent, the disclosure form continues to list two different brand names, creating the visual appearance of independent competitive representation that no longer exists. The form that described a genuinely competitive co-listing arrangement before January 9 describes an intra-enterprise commission split after it, in identical language, with no indication to the seller that the competitive dynamic has changed.

In April 2025, a Foster/Skillman listing at 3252 Hunts Point Road ($12,500,000) had a Coldwell Banker Bain buyer’s agent. In September 2025, a Foster/Skillman listing at 8620 N. Mercer Way ($10,400,000) had a Coldwell Banker Bain buyer’s agent. Both recorded as genuinely competitive transactions at the time of closing. As of January 9, 2026, both would be intra-enterprise. The commission that appeared to cross a competitive boundary now stays inside the same corporate parent.

Sellers engaging Compass-affiliated agents in Washington today who receive a co-listing disclosure naming any Anywhere brand are not receiving disclosure of a competitive arrangement. They are receiving disclosure that two divisions of the same parent company are splitting the listing commission. The disclosure form says “Compass; Coldwell Banker Bain.” What it does not say is that both entities now report to the same board, share the same ultimate parent, and that the buyer-side commission flowing to “Coldwell Banker Bain” stays inside Compass International Holdings. Under RCW 19.86, a representation that creates a false impression of independent competitive representation — when the two named parties are divisions of the same enterprise — satisfies the unfair or deceptive act standard without requiring proof of intent. The structural deception is facially apparent from the disclosure form itself, read against the publicly available merger record.

For Washington DOL enforcement: every listing in Washington disclosing a co-listing arrangement between a Compass brand and an Anywhere brand after January 9, 2026 is a candidate for disclosure review. The question is not whether the individual agents are aware of the corporate relationship — awareness is irrelevant to the structural analysis. The question is whether a reasonable seller, reading the disclosure, would understand that both agents represent the same corporate enterprise and that buyer-side commission flowing to either party stays inside that enterprise. The answer is no. The disclosure framework has not caught up to the merger.

Out-of-state AG investigator script. For any state AG office examining this issue in their jurisdiction, the three-step inquiry is: (1) Pull all co-listed residential transactions in your market from January 9, 2026 forward where both the listing brokerage and the buyer’s brokerage are Compass-family or Anywhere-family brands — NWMLS field designations and equivalent MLS records provide this data without subpoenas. (2) Compare the co-listing disclosure language against the post-merger corporate ownership chart — if the disclosure names two brands without disclosing common ultimate ownership, test it against your state’s UDAP standard for material omission or misrepresentation. (3) For any active listing meeting that pattern, treat it as a live enforcement candidate under your state’s consumer protection statute: the violation is ongoing, accruing on every new seller who signs an engagement letter without accurate disclosure of common control.

For state AGs in every state where Compass and Anywhere brands now operate under a single corporate parent — California, Illinois, New York, Florida, Texas — the same analysis applies in every jurisdiction. Each co-listing disclosure naming a Compass brand alongside any Anywhere portfolio brand, presented to a seller as a competitive arrangement, is a candidate for the same consumer protection inquiry Washington can now pursue under RCW 19.86.

References — Section V

Compass Commission Consolidation Strategy and Real Estate Marketing Transparency | www.mindcast-ai.com/p/compass-private-exclusives-monopoly — Documents the Layer 1/2/3 acquisition hierarchy and the brand portfolio that makes the post-merger disclosure problem structurally universal across all Compass-Anywhere operating markets.

VI. The Redfin Partnership: A Distribution-Side Enforcement Issue SSB 6091 Does Not Fully Reach

The February 26 Compass-Redfin announcement creates a second category of enforcement exposure that operates on a different legal track than SSB 6091’s listing-side requirement. Understanding the distinction is essential for Washington enforcement bodies and for other states’ AGs assessing their own exposure.

What the Redfin partnership actually does: Per Compass’s own partnership page, Compass listings on Redfin display with no days on market, no price drop history, and no home valuation estimates. All buyer inquiries route directly to Compass agents with no referral fee. Rocket Mortgage preferred pricing is available exclusively to Compass clients. One million buyer leads flow to Compass agents over the partnership term at zero acquisition cost.

Those stripped fields — days on market, price history, valuation estimates — are not the seller’s data points. They are the buyer’s. Stripping them serves the brokerage’s commission capture architecture, not the seller’s interest in maximizing competitive exposure.

A. The Washington Consumer Protection Act — RCW 19.86

Redfin operates in Washington as a licensed brokerage — not merely a passive platform. A licensed brokerage actively curating a two-tiered information environment — Compass listings stripped of buyer data while every other listing on the same platform displays it — is participating in information suppression, not merely hosting it.

The Kelman reversal is the evidentiary anchor. Redfin’s own prior leadership recognized the consumer harm publicly and pledged to prohibit it, then reversed course after a corporate acquisition. Defending that sequence under RCW 19.86’s unfair or deceptive acts or practices standard is a difficult task. Washington’s AG Civil Rights Division confirmed UDAP enforcement authority for this category of structural conduct on the legislative record — a permanently discoverable transcript available to every AG office examining the same business model.

The disparate treatment is the legal hook, not just the omission itself. Washington courts have found CPA violations where the deceptive act is structural. Showing Compass listings stripped of buyer data on a platform that displays that data for every other listing is structural deception built into the platform architecture itself. The enforcement predicate does not require proving intent — the two-tiered display is facially apparent from a browser, and the Kelman timeline establishes that the distinction between Compass listings and all other listings is a deliberate contractual choice, not a technical limitation.

B. Fiduciary Duty to Buyer Clients — RCW 18.86

Redfin buyer’s agents in Washington are now structurally positioned to breach their RCW 18.86 disclosure duty on every Compass listing they show. The information suppression is built into the platform infrastructure — the agent may be unaware they’re showing a client a listing missing data fields that exist and are visible on every adjacent listing. Unawareness does not eliminate liability. It amplifies the issue as a systemic practice rather than individual agent error.

Systemic fiduciary breach at platform scale — 60 million monthly visitors, all Compass listings uniformly stripped — is a regulatory enforcement action, not individual case management. Washington’s real estate licensing board has oversight authority that operates independently of SSB 6091 and independently of the AG’s CPA jurisdiction.

C. The Rocket Mortgage Integration — RESPA Section 8 and Washington Consumer Lending Law

The Rocket Mortgage integration creates a three-party referral arrangement in settlement services that RESPA Section 8 was specifically designed to reach: Redfin routes buyer leads exclusively to Compass agents; those agents connect buyers to Rocket’s preferred pricing bundle; Rocket’s products are embedded into Compass’s platform.

RESPA Section 8 risk analysis should examine whether one million buyer leads routed exclusively to Compass agents over three years may be characterized as a “thing of value” depending on the consideration exchanged, affiliate structure, and the actual routing and compensation terms in the partnership agreement. CFPB enforcement authority is the federal instrument. But Washington’s Consumer Loan Act and mortgage broker regulations provide independent state enforcement authority over settlement service referral arrangements. Washington’s AG consumer finance division should examine whether the Rocket-Compass-Redfin referral structure satisfies state anti-kickback and anti-tying provisions before CFPB acts. Filing a state inquiry establishes independent enforcement posture and creates a coordination vehicle with other state AGs examining the same contract.

References — Section VI

The Compass-Redfin Alliance: Market Self-Correction Is Dead | www.mindcast-ai.com/p/compass-redfin — Primary analysis of the partnership structure, Kelman pledge reversal, and Stigler capture confirmation. The RCW 19.86 hook in Section VI.A builds directly on the consumer harm framework established there.

Runtime Analysis of the Compass-Redfin-Rocket Alliance | www.mindcast-ai.com/p/runtime-compass-redfin-rocket — Structural breakdown of the three-party alliance; documents Redfin’s acknowledgment that SSB 6091 may exclude Compass listings from the partnership display in Washington — confirming the statute’s immediate market effect and the enforcement predicate for Sections VI.A and VI.B.

Compass Commission Consolidation Strategy and Real Estate Marketing Transparency | www.mindcast-ai.com/p/compass-private-exclusives-monopoly — Layer 3 framework and the $400–800M private exclusive infrastructure premium estimate.

VII. The Antitrust Theory of Harm: A Framework for State AGs

A. Why Agent Indifference Disappears Inside a Private Network

In a fully competitive, transparent real estate market, a buyer’s agent is indifferent to which brokerage holds the listing. All agents search the same MLS simultaneously. Brokerage affiliation is irrelevant when all agents see the same inventory at the same time.

Inside a pre-MLS private marketing network, that indifference completely evaporates. A network-affiliated buyer’s agent operating within the pre-MLS window has exclusive access to inventory no outside agent can see. Their clients can make offers on properties that buyers represented by independent firms do not know exist. The advantage is not superior service or market expertise. It is an engineered information asymmetry — a structural head start built into the marketing architecture.

A market outcome produced by superior competition is the system working correctly. A market outcome produced by foreclosed access to information is exclusionary conduct — regardless of whether the foreclosing party characterizes it as “seller’s choice.”

B. The Three Enforcement Components

The artificial inventory moat. Restricting listings to the internal network during the pre-MLS window creates a barrier to entry not based on competitive merit. The moat is an engineered feature of the marketing architecture — the three intra-firm transactions in Section III are outcomes the architecture produced by design. Compass’s standard counterargument — that any licensed agent could schedule a showing through the private remarks field — describes access at the end of the sequence. The suppression operates at the beginning: during buyer discovery, when the network forms the buyer pool and anchors price expectations. A buyer whose agent finds the listing after MLS submission is not competing on equal terms with a buyer the Compass network routed during the pre-MLS window. They are competing against someone the network already selected.

The steering premium. The structural setup creates a powerful economic incentive for network-affiliated buyer’s agents to direct clients toward internal listings. The advantage is not a reward for better work. It is a reward for network membership. The steering premium converts information asymmetry into commission routing — documented in NWMLS’s own field designations.

The compounded exclusion. A below-market co-op fee functions as a second-layer exclusionary mechanism. Under the Redfin partnership, that second layer now compounds with a third: information-stripped platform display that routes all buyer inquiries to Compass agents before an independent agent can respond. Three suppression mechanisms — pre-MLS window, fee, and data stripping — now operate in sequence on the same listing inventory.

C. The Platform API Parallel

Technology antitrust law offers the directly applicable structural analogue. In foundational platform competition cases, antitrust regulators examined situations where dominant platform operators gave internal developers privileged access to system interfaces unavailable to external developers. The competitive harm was not that internal developers were more skilled. External developers were structurally foreclosed from competing on equal terms because the platform controlled access to the infrastructure that determined competitive outcomes.

A pre-MLS private network operates on the same structural principle. Internal agents have privileged access. External agents do not. The competitive foreclosure is not incidental to the system’s design. It is the system’s design. The Redfin partnership extends this architecture to the distribution layer — 60 million monthly visitors routing buyer inquiries to Compass agents first, before any independent agent can respond.

D. Nash-Stigler Framework for State AG Assessment

Nash Equilibrium identifies the stable outcome in a multi-player decision environment where no participant can improve their result by changing strategy while others hold theirs constant. In a transparent MLS market, equilibrium produces competitive outcomes. Inside a private network, the equilibrium shifts artificially: the dominant strategy for a network-affiliated buyer’s agent is to direct clients toward internal listings where they have an informational advantage. The three intra-firm transactions in the dataset are the stable equilibrium output of that manipulated environment — rational responses to a structurally engineered incentive system.

Stigler Equilibrium identifies the information sufficiency threshold — the point at which regulators possess enough documented evidence to act without further investigation. Before the Washington transaction record existed publicly, the pre-MLS marketing pattern operated below the interpretive threshold. The Washington record demonstrates that the Stigler threshold can be crossed using publicly available data — MLS field designations, agent roster lookups, brokerage CDOM/DOM platform data — without subpoenas or discovery.

For state AGs and legislatures: If your market has a dominant brokerage with a private listing network, a rainmaker team structure with recurring intra-firm buyer routing, and a below-market co-op fee pattern on suppressed listings, the Nash equilibrium has already shifted. If your dominant portal has now joined the Redfin partnership, the Stigler threshold is crossed at the platform level. Washington’s methodology shows exactly how to assess both.

E. Market Definition for AG Analysis

Washington’s dataset suggests this template: luxury residential real estate transactions above a defined price threshold (in Washington, $6M+) in a defined geography (King County), facilitated through a single dominant MLS with no meaningful competitor, where one brokerage’s agents appear disproportionately in both listing and buyer roles across a defined time window.

The Washington record documents: 13 top-ten transactions involving one team over 13 months, three confirmed intra-firm buyer routings with three different Compass buyer’s agents, $63.8M concentrated within one firm’s information advantage zone. State consumer protection statutes typically provide an independent enforcement pathway that does not require satisfying Sherman Act standards. State AGs should assess both the federal antitrust theory and state UDAP exposure simultaneously.

References — Section VII

The Nash-Stigler Dual Equilibrium Architecture | www.mindcast-ai.com/p/nash-stigler-equilibria — Formal equilibrium framework underlying the AG assessment template in Section VII.D. Establishes why the three-transaction intra-firm routing pattern constitutes a shifted Nash equilibrium rather than coincidental outcomes.

The Compass-Anywhere Address Suppression Calculus | www.mindcast-ai.com/p/team-foster-scenario — The Stigler equilibrium analysis demonstrating that Washington’s transaction record crossed the information sufficiency threshold using publicly available data alone. The methodology is directly replicable in any state with a functioning MLS and a regularly published luxury transaction ranking.

VIII. The Replication Template: Six Steps for Every State

Washington’s experience is a complete case study for replication. Here is the methodology, step by step.

Step 1: Identify your data source. Every state with a functioning MLS has the equivalent of Seattle Agent Magazine’s monthly top-10 sales data. Look for regularly published sales rankings identifying listing agent, buyer’s agent, brokerage affiliation, sale price, and closing date. The entire Washington transaction record was assembled from public data. No subpoenas required.

Step 2: Build a 12-month transaction matrix. For your state’s largest luxury market, build a transaction matrix covering 12 months of top-tier sales. Flag every transaction where the listing agent and buyer’s agent share brokerage affiliation. Flag every dual-agency transaction. Flag every transaction where the listing agent’s team member appears on the buyer side through a co-lister insertion. The three-party capture architecture — rainmaker lists, co-lister inserts, team member buys — is not unique to Washington. It is a structural feature of how pre-MLS networks monetize information asymmetry, and it appears in MLS field designations without additional investigation.

Step 3: Pull CDOM/DOM data on active suppressed listings. For any brokerage operating a private listing network, the gap between Cumulative Days on Market and Days on Market on the brokerage’s own platform is a direct record of pre-MLS marketing activity. Compass’s own system documented the 84-day window on the Clapp listing. No whistleblower required. Also check whether your state’s dominant portal has signed the Redfin-style partnership — if Compass Coming Soon listings are appearing without days on market or price history, the platform suppression layer is already operating in your market.

Step 4: Cross-reference agent roles. Build a role matrix: for each agent on the top listing team, how often do they appear as buyer’s agent on their own team’s listings versus as standalone buyer’s agent on independent brokerage listings? Structural invariance — an agent who never appears as standalone buyer’s agent on independent listings — is the signature of a co-listing capture vehicle.

Step 5: Assess your MLS’s litigation and governance exposure. Before recommending MLS enforcement against the dominant pre-MLS network operator, evaluate: Is the MLS currently in litigation with the brokerage? If so, enforcement creates exhibit risk. Does the dominant competing brokerage have board representation on the MLS? If so, enforcement directly benefits owner-competitors. Either condition establishes the need for statutory authority. Both conditions together make legislative action the only viable path.

Step 6: Draft the statute — and add the distribution-side provision. SSB 6091’s operative requirement — concurrent marketing from the moment marketing begins, no opt-out — is the listing-side template. The Redfin partnership makes a second provision necessary: licensed brokerages operating consumer-facing search platforms must display material listing data fields uniformly across all listings. No field suppression for preferred partner inventory. Adding that provision closes the Redfin architecture before it replicates in the next partnership Compass signs. SSB 6091 closes the listing window. A platform display uniformity provision closes the distribution window. Both are necessary.

Falsification condition. The Platform Self-Authentication Rule — CDOM/DOM gap as admission of pre-MLS marketing — depends on Compass continuing to publish both fields. If, after the effective date, Compass listings in Washington show no CDOM/DOM gap on Compass’s own platform (or Compass removes the CDOM field entirely) while still marketing “Coming Soon” or “Private Exclusive” inventory, the enforcement predicate shifts from platform self-authentication to subpoenaed marketing logs, portal timestamps, and third-party showing records. That is not a defeat — it is the expected response of a network that knows the gap is discoverable. Removal of the field is itself a signal. Document the current data now, before the effective date.

What good faith compliance looks like. The statute does not require abandoning seller optionality. It requires concurrent marketing. Good faith compliance design: marketing begins → immediate MLS submission, same timestamp. Where a documented seller health or safety exception applies → written certification, defined time limit, audit trail available on request. Platform display → uniform data fields across all listings; no field suppression by brokerage affiliation. Co-listing disclosure → identifies common corporate control, not just brand names, where common control is the economic fact. Any firm that designs to these specifications has no SSB 6091 exposure. The statute targets timing advantage, not seller choice.

IX. Day-One Enforcement Watch List for Washington

For NWMLS and Washington enforcement authorities, these are the first-generation enforcement indicators beginning on SSB 6091’s effective date of approximately June 11, 2026.

Active listing watch. NWMLS #2470280 — the Clapp listing at $43.8M — remains active. If it closes after SSB 6091’s effective date, the buyer’s agent affiliation is the first enforcement data point under the new law. A Compass-affiliated buyer’s agent completes the documented network circuit under statutory coverage for the first time.

CDOM/DOM gap monitoring. Any Compass listing in Washington that shows a CDOM/DOM gap after SSB 6091’s effective date is a presumptive violation. The gap is self-documenting on Compass’s own platform. DOL investigators do not need to subpoena internal records — the evidentiary predicate is on the brokerage’s public-facing website.

Redfin display audit. Any Compass listing appearing on Redfin without days on market, price history, or valuation estimates — while adjacent listings display all three fields — is the predicate for a RCW 19.86 consumer protection inquiry independent of SSB 6091. Run the side-by-side comparison. The two-tiered display is facially apparent from a browser.

Redfin buyer’s agent disclosure tracking. Washington real estate licensing enforcement should assess whether Redfin buyer’s agents are disclosing to buyer clients when a listing’s data fields have been suppressed by platform agreement. Systemic failure to disclose is a RCW 18.86 violation at platform scale.

Post-merger disclosure audits. Every listing in Washington disclosing a co-listing arrangement between a Compass brand and an Anywhere brand after January 9, 2026 requires review under the Consumer Protection Act. Those are not competitive co-listings. They are intra-enterprise arrangements presented as independent representation.

Network role tracking. Any transaction where the buyer’s agent is a member of the listing agent’s team, or a confirmed network participant who previously purchased a listing from that team, is a priority enforcement review.

Below-market co-op fee flagging. Any active luxury listing with buyer’s agent compensation below 1.8% — materially below the standard 2.5–3% range — warrants review as a potential secondary exclusionary mechanism operating alongside pre-MLS marketing or Redfin data suppression.

Supplemental: What the Redfin Partnership Confirms for Goodwill Impairment Analysis

Auditors, equity analysts, and M&A counsel examining the $1.6 billion Anywhere acquisition premium will find the relevant analysis here. Washington enforcement bodies and state AG investigators can proceed directly to Section X.

MindCast AI’s Layer 3 framework — developed in the Compass Commission Consolidation Strategy — decomposed the Anywhere acquisition premium into three value layers. Layer 3 is the private exclusive infrastructure premium, estimated at $400–800 million, which exists only if listings can be withheld from the open market long enough for an internal buyer to arrive first.

Robert Reffkin’s Redfin partnership statement — framing the arrangement as protecting sellers from “misleading insights that damage value” — is not brand consolidation language. It is Layer 3 language, simultaneously available to every auditor testing goodwill assumptions, every state legislature advancing concurrent marketing bills, and every federal court examining Compass’s antitrust claims. Compass confirmed Layer 3 in its own commercial language, in a signed contract, published in a press release.

The impairment calculus runs in both directions. The partnership gives Compass a new revenue stream — one million buyer leads, Rocket mortgage integration — that auditors can treat as partial substitute for Private Exclusive Infrastructure Premium. But a firm that outsources its listing suppression infrastructure to a third-party platform for a three-year term because it can no longer operate it internally at scale has not recovered Layer 3. It has documented that Layer 3 can no longer be operated internally — which is precisely what goodwill impairment review examines.

X. Conclusion: The Law Inherits the Record

SSB 6091 did not create the enforcement problem. It created enforcement authority over a problem the transaction record had already documented in full.

Thirteen months of Seattle luxury data establish the mechanism: a network with defined roles, predictable routing, and a structural signature visible in publicly available MLS field designations — no subpoenas, no whistleblowers, no discovery required. The Clapp listing is the law’s first prospective enforcement test, carrying an 84-day pre-MLS window self-documented by Compass’s own platform, a co-listing disclosure masking single-enterprise representation as competitive collaboration, and a below-market co-op fee that makes sense only if Compass expects to control the buyer side. Three enforcement tracks — DOL licensing, AG consumer protection, and NWMLS governance — are now available simultaneously, each triggered by the same conduct on the same listing.

The Redfin partnership added a fourth enforcement dimension SSB 6091’s drafters did not need to anticipate, because it did not exist when the bill was introduced. A licensed brokerage displaying two tiers of information on the same platform — Compass listings stripped of the exact buyer data fields its own federal complaints call essential to consumer welfare, while every competing listing displays all three — is the most precisely self-defeating commercial act in the series. Compass signed a three-year contract confirming that the mechanism is structural, deliberate, and national in scope. Every state legislature that was waiting for concrete evidence that voluntary market correction had failed now has it, time-stamped and browser-accessible.

Washington’s transaction record travels to every state that follows without regeneration. The methodology is public. The dataset is verifiable. The enforcement template is documented step by step. The only thing each subsequent state needs to supply is a 12-month luxury transaction matrix from its own MLS.

The depositions have not yet begun.

XI. References

MindCast AI Publications

The Compass-Anywhere Address Suppression Calculus — www.mindcast-ai.com/p/team-foster-scenario

Compass Commission Consolidation Strategy and Real Estate Marketing Transparency — www.mindcast-ai.com/p/compass-private-exclusives-monopoly

Chicago School Accelerated — Trust, Coordination, Narrative Power in Residential Brokerage — www.mindcast-ai.com/p/chicago-accelerated-compass-trust

SSB 6091 Cross-Forum Analysis — www.mindcast-ai.com/p/ssb6091-cross-forum-analysis

The Compass-Redfin Alliance: Market Self-Correction Is Dead — www.mindcast-ai.com/p/compass-redfin

Runtime Analysis of the Compass-Redfin-Rocket Alliance — www.mindcast-ai.com/p/runtime-compass-redfin-rocket

The Nash-Stigler Dual Equilibrium Architecture — www.mindcast-ai.com/p/nash-stigler-equilibria

The Astroturf Coefficient — www.mindcast-ai.com/p/jan23-wa-senate-housing-committee

The Compass Collapse — A Post Washington SSB 6091 Passage Reckoning (umbrella) — www.mindcast-ai.com/p/wa-ssb6091-real-estate-marketing-transparency

Primary Sources

Haleh Clapp Active Listing (NWMLS #2470280) — compass.com listing page

Compass Newsroom: Cris Nelson on private exclusive demand — compass.com, April 25, 2025

RISMedia: Cris Nelson on seller negotiating power — rismedia.com, April 17, 2025

Inman: Cris Nelson on NWMLS monopolistic control — inman.com, April 25, 2025

Real Estate News: Compass-Redfin Partnership Announced — realestatenews.com, February 26, 2026

Compass Partnership Page — compass.com/rocket-partnership

Inman: Compass–Anywhere Merger Closes Jan. 9, 2026 — inman.com, January 9, 2026

HousingWire: Compass v. NWMLS Trial Delayed to Oct. 2026 — housingwire.com, December 9, 2025

RISMedia: NWMLS Signals Intent to Countersue Compass — rismedia.com, December 5, 2025

Transaction Data: Seattle Agent Magazine, Top-10 Monthly Sales, January 2025–January 2026