MCAI Lex Vision: Compass Plan B, Structural Circumvention After Washington SSB 6091

Seven Vectors, One Redfin Contract, and the NWMLS Enforcement Calculus That Changed on February 26

Installment III of the The Compass Collapse– A Post Washington SSB 6091 Passage Reckoning series:

Installment I: The Compass Self-Destruction Sequence, How Aggressive Federal Litigation Birthed the Legislation That Destroyed the Business Model

Installment II SSB 6091 Has Passed. Here Is What It Now Reaches — and the Compass Enforcement Record It Inherits.

MindCast AI’s prior Lex Vision publications established the predictive record before SSB 6091 passage. The Compass-Anywhere antitrust analysis (December 2025) predicted: “If [the Anywhere merger is] blocked: Compass pursues alternative opacity strategies through portal partnerships.” Compass was not blocked — but the prediction confirmed anyway. The evidentiary record that matters will be built in discovery, not in press releases.

I. EXECUTIVE SUMMARY

Washington State Senate Bill 6091 passed the Washington State Senate 49–0 on February 10, 2026, and the House 92–1 on March 3, 2026, eliminating Compass Real Estate’s primary market sequestration tool: the Private Exclusive. The vote was not close. The legislative record was built in public. The analytical documentation was timestamped months before either chamber cast a ballot.

Compass’s response will not be compliance.

Running a debt-constrained corporate entity with $2.6 billion in post-merger obligations through a Nash-Stigler equilibrium analysis produces one mechanically predictable result: structural circumvention designed to preserve the exclusionary advantage while appearing to satisfy the law’s surface requirements. Section II quantifies the financial and behavioral inputs that make this outcome deterministic.

On February 26, 2026 — the day the House Rules Committee held the bill’s scheduling gate — Rocket Companies, Compass, and Redfin announced a three-year strategic alliance. Plan B was not waiting for the Governor’s signature.

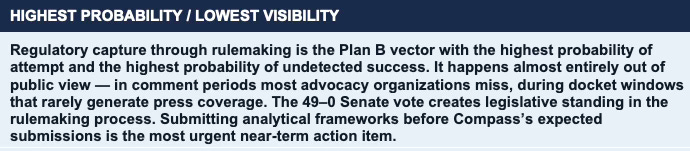

Of the seven circumvention vectors that follow, Vector D — regulatory capture through DOL rulemaking — carries the highest probability of undetected success. The DOL comment period opens the moment the Governor signs. Compass’s lobbying operation will file before most advocacy organizations learn the docket exists. Filing MindCast AI’s analytical framework before Compass’s expected submissions is the single highest-leverage action item in the ten days following signature.

sustained success probability, and the countermeasures that close each gap. Section VI details how the February 26 announcement restructured the NWMLS enforcement calculus: not by adding regulatory pressure, but by eliminating the retaliatory enforcement narrative that had constrained NWMLS’s own discretionary action for the prior ten months.

Washington’s SB 6091 and Private Real Estate Market Control (Jan 2026)

II. WHY COMPLIANCE IS NOT COMPASS’S RATIONAL OPTION

Three structural forces make compliance with SSB 6091 irrational for Compass under any standard Nash equilibrium analysis: the debt architecture left by the Anywhere merger, the pre-existing three-prong monopolization strategy already running in federal court, and a behavioral drift profile that predicts systematic circumvention regardless of stated intent. Each operates independently. Together they eliminate compliance as a viable dominant strategy.

A. The Debt-Structure Mandate

Compass’s $2.6 billion in post-merger Anywhere obligations makes inventory sequestration a survival mechanism, not a strategic preference. The Private Exclusive is not a product feature. It is the structural mechanism sustaining dual-agency commission capture at scale — the economic engine that services the debt load. SSB 6091’s concurrent marketing requirement severs that mechanism at its root.

Compliance would require surrendering the revenue architecture that makes the debt serviceable. A Nash-Stigler analysis of a regulated monopolistic actor under these financial constraints produces a single dominant strategy: redefine the law’s operational parameters rather than operate within them. Every circumvention vector identified in this analysis follows directly from that financial constraint applied to an institution whose published Behavioral Drift Factor of 0.81 marks systematic deviation between stated intent and actual conduct.

B. The Pre-Existing Three-Prong Monopolization Architecture

SSB 6091 did not catch Compass unprepared. The Compass-Anywhere antitrust analysis published in December 2025 identified a three-pronged litigation-acquisition monopolization strategy already in motion: the NWMLS lawsuit to remove MLS mandatory submission rules; the Zillow lawsuit to force portals to distribute private exclusives; and the Anywhere acquisition to provide national agent network scale through Coldwell Banker, Century 21, and Sotheby’s. SSB 6091 inserts a fourth regulatory constraint into a machine already running.

The Redfin alliance announced February 26 is the portal partnership the December 2025 analysis predicted — now operational as a signed three-year contract at zero cash cost.

C. Behavioral Drift Predicts Circumvention

MindCast AI Cognitive Digital Twin metrics, published December 2025: Causal Signal Integrity (CSI) 0.23 — lowest in the system. Behavioral Drift Factor (BDF) 0.81 — systematic deviation between stated intent and actual behavior. Coordination Tension Score (CTS) 0.88 — maximum pressure on coordination architecture. Contradiction Tolerance Coefficient (CTC) 1.62 — Compass generates contradictions faster than it resolves them.

An institution with this profile does not achieve compliance under regulatory pressure. It routes around constraints while generating internal inconsistency. The CTC of 1.62, published before the Redfin reversal, predicted exactly the sequence that followed: Redfin pledges to ban pre-MLS listings in April 2025, Rocket acquires Redfin, and the same platform that was the primary exhibit for voluntary market discipline becomes the primary national distribution infrastructure for the practice it pledged to ban — in one signed press release four months after the acquisition.

The output of these three forces is mechanical: a firm with this debt load, this litigation posture, and this behavioral drift coefficient does not achieve compliance under regulatory pressure. It routes around constraints while generating internal inconsistency. The seven circumvention vectors in Section III are the direct product of this structural analysis — each predicted by the financial and behavioral inputs, each now observable in Compass’s post-passage commercial conduct.

Contact mcai@mindcast-ai.com to partner with us on Law and Behavioral Economics foresight simulations.

To create your own game theory simulation of data on Compass address suppression and private exclusives, upload the URL of this publication to any LLM (ChatGPT, Claude, Gemini, Grok, Perplexity) and prompt ‘develop MindCast framework with 3 degrees of cited sub links.’ Thereafter, all new information you upload is training data for your AI system. See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure for more info.

MindCast AI’s analytical work on SSB 6091 — transaction methodology, opposition modeling, testimony framework, and game theory prediction record — is available for deployment in any state considering real estate transparency legislation. Washington’s record does not need to be rebuilt. It needs to be applied.

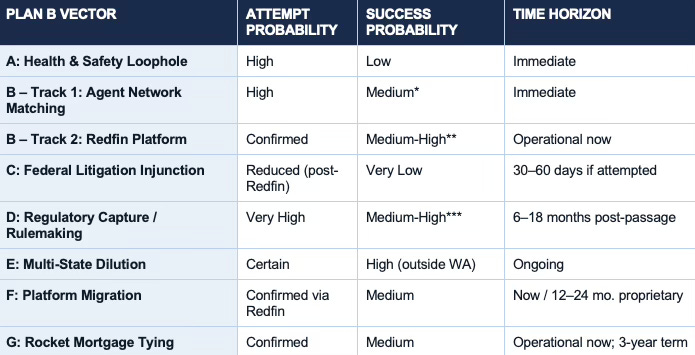

III. THE SEVEN PLAN B VECTORS

Seven circumvention vectors now operate simultaneously across different institutional surfaces. Each is assessed below for attempt probability, success probability, and the countermeasures that close each gap. Vectors B, F, and G are no longer predictions — they are signed contracts. The remaining four operate at varying stages of activation. No single vector is individually decisive. The architecture is designed so that closing one gap leaves six others open.

Compass’s Coasean Coordination Problem Part I: Private Exclusives Reshape Competition (Dec 2025)

Windermere and Compass: Two Philosophies of Real Estate (Jan 2026)

The Dual Nash-Stigler Equilibrium Architecture (Jan 2026)

The Stigler Equilibrium: Regulatory Capture and the Structure of Free Markets (Jan 2026)

The Integrated, Modernized Framework of Chicago Law and Behavioral Economics (Dec 2025)

Compass’s Coasean Coordination Problem Part II: Litigation-Acquisition Monopolization Strategy (Dec 2025)

A. Weaponizing the Health and Safety Exception

The health-and-safety carve-out is the only express exception SSB 6091 contains. Compass’s immediate post-passage play will be to systematize the exception — converting a narrow statutory safety provision into a default luxury opt-out for any high-net-worth seller who prefers privacy to competitive exposure. The countermeasure window is tight.

SSB 6091 carries a carve-out: a broker may withhold concurrent marketing when “reasonably necessary to protect the health or safety of the owner or occupant.” Among the exploitable gaps in the statute, the health-and-safety carve-out is the one most likely to be operationalized before the ink is dry on the Governor’s signature.

The Predicted Tactic

Compass legal will draft standardized “Security-Mandated Listing” addendums for high-net-worth clients in Medina and Bellevue citing “privacy concerns,” “public profile risks,” or “asset security.” Compass Teams like Team Foster are the likely immediate deployment point. The play is to convert a narrow statutory safety exception into a luxury convenience loophole, then dare the Department of Licensing to audit the “safety requirements” of ultra-wealthy sellers in gated communities.

Why It Fails at Scale

Systematization is self-defeating. A standardized security addendum becomes Exhibit A in a pattern-and-practice DOL enforcement investigation. A single discovery request pulls every addendum signed in a twelve-month period. The statistical distribution of “security concerns” among wealthy sellers is forensically damning — if 30% of Compass’s luxury listings invoke the exception while the industry average is 0.3%, the pattern defeats the pretext without additional evidence.

The client exposure problem compounds this: high-net-worth sellers are not going to want to be named deponents in a proceeding about whether their Medina estate genuinely required privacy protection from public listing. A firm whose Plan A requires publicly identifiable wealthy clients to testify that they feared their address appearing on Zillow will find its client pipeline drying before the DOL investigation concludes.

Countermeasure

DOL rulemaking should define qualifying safety circumstances narrowly — requiring documented law enforcement assessment or court order, not seller self-attestation — and establish statistical audit protocols for addendum frequency by brokerage. One enforcement action against a standardized template collapses the entire strategy. The countermeasure resource is the DOL comment process, which opens immediately after the Governor’s signature. MindCast AI’s analytical framework should be filed before Compass’s expected submissions.

The Compass Commission Consolidation Strategy and Real Estate Marketing Transparency (Feb 2026)

B. The Shadow Market: Two-Track Architecture

Compass’s shadow market strategy runs on two parallel tracks that complement rather than substitute for each other. Track 1 operates before any listing agreement exists — moving dual-agency capture to a pre-regulatory trigger point. Track 2 is no longer a prediction: the February 26 Rocket–Compass–Redfin partnership announcement confirmed it as a signed three-year contract. Both tracks pursue the same objective through different mechanisms, and each carries distinct legal exposure.

February 26, 2026: Compass Coming Soon listings appeared on Redfin immediately. Private Exclusives to follow. 60 million monthly visitors. All buyer leads routing exclusively to Compass agents. No days on market. No price history. No valuation estimates. No referral fee. Track 2 is not a prediction. It is a signed contract.

Track 1: Pre-Listing Agent Network Matching

SSB 6091 governs the “marketing” of a property once a listing agreement is in place. Move the dual-agency capture to before any formal listing agreement is signed and the statutory prohibition may not attach. Compass leverages its internal agent network to match unlisted sellers with Compass buyers before any formal marketing period begins. The Nash-Stigler logic is clean: redefine the transaction initiation point to precede the regulatory trigger.

Track 1 carries a self-limiting constraint — insufficient internal buyer depth in markets where Compass is thin — substantially reduced once the Anywhere acquisition fully integrates Coldwell Banker, Century 21, and Sotheby’s agent networks. The integrated network creates the buyer depth the private exclusive model requires without triggering SSB 6091’s marketing definition, if that definition is not extended by DOL rulemaking to reach pre-listing agent communications.

Countermeasure

A single amendment defining “marketing” to include any agent communication about an unlisted property to a prospective buyer closes this gap in one drafting session. DOL rulemaking can accomplish the same result without legislative action.

Track 2: The Redfin Platform Architecture

The Redfin partnership moves the same dual-agency capture function from invisible agent-network matching to a signed contractual architecture at national scale. The mechanism is identical — intercept the buyer before the open market can compete — but the evidence is public, the contract runs three years, and the terms are filed in a press release authored by Compass’s own CEO.

What the Contract Terms Reveal

Per Compass’s own partnership page, Compass listings on Redfin display with no days on market, no price drop history, and no home valuation estimates. Those are the buyer’s data points. Stripping them from the buyer serves the brokerage’s commission capture architecture, not the seller’s interest in maximizing competitive exposure. All buyer inquiries route directly to Compass agents with no referral fee. One million buyer leads flow to Compass agents over the partnership term at zero acquisition cost. Rocket Mortgage preferred pricing — a 1-point first-year rate reduction or up to $6,000 lender credit — is available exclusively to Compass clients.

The Self-Correction Argument Is Now Dead

In every prior state legislative session where concurrent marketing bills faced opposition, industry opponents deployed market self-correction as the primary defense for inaction. Redfin CEO Glenn Kelman pledged publicly in April 2025 to ban listings selectively pre-marketed without MLS exposure. Compass opponents cited that pledge in Washington’s January 2026 Senate hearing as the market’s own answer to SSB 6091. On February 26, 2026, Redfin reversed that pledge and became the primary national distribution infrastructure for the practice it pledged to ban — under a three-year contract, at zero cost to Compass, four months after a corporate acquisition.

George Stigler wrote in 1971 that regulatory behavior tracks ownership, not stated mission. The mechanism confirmed in a press release. Any committee chair in any state who invokes self-correction today must defend the proposition that a pledge reversing four months after a corporate acquisition represents ongoing voluntary market discipline.

The Distribution-Side Gap SSB 6091 Doesn’t Cover

SSB 6091 governs broker listing obligations. It does not directly govern what a licensed brokerage’s search platform displays. A licensed brokerage displaying Compass listings stripped of days on market and price history — while showing all fields for every other listing on the same platform — is a two-tiered information architecture independently actionable under Washington’s Consumer Protection Act. No new statute required. A supplemental platform display provision would close the gap prospectively: licensed brokerages operating consumer-facing search platforms must display material listing data fields uniformly across all listings.

NWMLS Litigation Consequence

The Redfin deal substantially weakens Compass v. NWMLS. Compass’s antitrust theory rests on the claim that NWMLS’s restrictive listing policies exclude Compass listings from market visibility, harming consumers and constituting anticompetitive monopolization. Securing distribution to 60 million monthly Redfin visitors makes the exclusion-from-market argument difficult to sustain on any relevant market definition the Western District of Washington will apply. NWMLS’s counsel filed a Notice of Supplemental Authority following the February 6 Zillow preliminary injunction denial. The Redfin announcement is a stronger factual predicate for the same motion.

The Compass-Redfin Alliance: Market Self-Correction Is Dead (Feb 26, 2026)

Compass’s Coasean Coordination Problem Part II: Litigation-Acquisition Monopolization Strategy (Dec 2025)

The Compass Commission Consolidation Strategy and Real Estate Marketing Transparency (Feb 2026)

C. Federal Litigation — The Property Rights Injunction Play

The constitutional property rights injunction — arguing that SSB 6091 constitutes an unlawful taking or violates homeowner autonomy under substantive due process — was Compass’s litigation backstop before February 26. The Redfin partnership structurally foreclosed it. Three independent legal bars now block the play: the constitutional argument fails on the merits, the NWMLS litigation creates a cross-forum estoppel, and the Redfin contract locks the contradiction in place for three years.

The constitutional property rights argument — that SSB 6091 constitutes a taking or violates homeowner autonomy protected by substantive due process — was available before February 26. After February 26, it is structurally foreclosed by Compass’s own commercial conduct.

The Constitutional Argument Fails

Federal courts have consistently declined to frame MLS participation rules or listing disclosure mandates as constitutional property rights violations. A disclosure mandate doesn’t take property — it restricts one method of sale while leaving all others intact. State police power over broker licensing is among the most robust categories of state legislative authority, and the current federal judicial climate’s hostility to administrative agency overreach does not translate into hostility to state legislative authority over professional licensing. The Western District of Washington will not be the court to chart that doctrinal expansion.

The NWMLS Forward Lock

Compass is already litigating in federal court against NWMLS arguing that mandatory MLS submission rules are anticompetitive restrictions on seller choice. A simultaneous injunction against SSB 6091 would require arguing the opposite proposition: that the state’s mandatory concurrent marketing requirement violates homeowner property rights. Both arguments dress in seller-choice language. The underlying ask is structurally inverted. A federal judge in the Western District of Washington who has already seen the NWMLS complaint will see it immediately.

The Redfin Contract Locks the Contradiction for Three Years

The SDNY denied Compass’s Zillow preliminary injunction on February 6, finding the platform exclusion theory insufficient. The Redfin deal confirms that Compass can secure national platform distribution independently. A party demonstrating it can reach 60 million monthly visitors through a single portal partnership cannot simultaneously argue that concurrent marketing mandates constitute market exclusion sufficient to warrant injunctive relief. The cross-forum contradiction is now a three-year business obligation. Compass cannot settle its way out of it while the contract runs.

Federal litigation is not Compass’s primary post-passage play. The SDNY’s February 6 denial of the Zillow preliminary injunction, followed immediately by the Redfin partnership announcement, signals that Compass has already pivoted from litigation-as-leverage to partnership-as-circumvention. Vector C’s attempt probability is reduced precisely because Compass’s commercial conduct has made the constitutional argument untenable. The real action is in the administrative rulemaking process.

Compass’s Coasean Coordination Problem Part III: Coordination Costs, MLS Governance and the Litigation (Dec 2025)

Brief of MindCast AI LLC as Amicus Curiae in Support of Defendant NWMLS (May 2025)

D. Regulatory Capture Through Rulemaking

Regulatory capture through DOL rulemaking is simultaneously the highest-probability circumvention vector and the lowest-visibility one. The legislative fight is over. The administrative fight begins the moment the Governor signs. Compass’s lobbying operation — the same infrastructure that generated a 17:1 Astroturf Coefficient in the Senate hearing — will shift from the legislative chamber to the DOL comment process immediately, in proceedings that generate no floor votes, no public testimony lists, and no press coverage.

SSB 6091 passes the Legislature and reaches the Governor’s desk. DOL then writes the implementing rules. Compass’s lobbyists — the same operation that coordinated the seventeen-to-one undisclosed Astroturf Coefficient in the January Senate hearing — shift from the legislative chamber to the administrative rulemaking comment process immediately after passage. The definitions of “marketing,” “health or safety,” and enforcement thresholds get shaped in that process through comment letters and ex parte meetings that rarely surface in legislative reporting.

Compass will seek interpretive guidance that: (a) defines “concurrent marketing” narrowly to exclude pre-listing agent communications; (b) expands the “health or safety” exception broadly through self-attestation; (c) creates compliance safe harbors that functionally permit phased marketing under alternate terminology; or (d) delays enforcement timelines to extend the pre-MLS window into the post-signature period.

The Wisconsin Comparison

The opt-out language Compass sought throughout the SSB 6091 hearings — “or if the homeowner requests otherwise in writing” — mirrors Wisconsin’s AB 456. Wisconsin’s implementing regulations interpreted the opt-out broadly, functionally preserving the pre-MLS window for any willing seller. Compass will deploy the Wisconsin framework as a model for DOL interpretive guidance, arguing that Washington’s statute contains analogous flexibility. The analytical response: SSB 6091’s 49–0 Senate and 92–1 House votes with no opt-out amendment — after multiple attempts to insert one failed — is the clearest possible statement of legislative intent.

Countermeasure

Filing analytical frameworks in the DOL rulemaking comment docket before Compass’s expected submissions is the immediate deliverable. The 49–0 Senate vote creates explicit legislative standing. The MindCast AI publication record — timestamped before passage, in the official legislative record of both chambers — is the credentialed voice in that proceeding. Every state AG who engaged with the Washington record has an interest in how DOL interprets the statute, because narrow interpretation becomes the precedent Compass imports to the next state.

Nineteen Senators, Seventeen Questions: How Compass Bought Its Antitrust Clearance (Feb 2026)

The Astroturf Coefficient: Compass’s Coordinated Opposition to SB 6091 (Jan 2026)

The Geometry of Regulatory Capture at the DOJ Antitrust Division (Jan 2026)

The Tirole Phase Analysis of Advocacy-Driven Antitrust Inaction (Jan 2026)

E. Multi-State Dilution Strategy

Surface compliance in Washington while doubling down in forty-four unregulated states is Compass’s lowest-friction response to a single-state mandate. The Redfin partnership — structured nationally, not Washington-specifically — is already executing this vector at scale. The counterstrategy requires making Compass’s Washington conduct visible to every state legislature simultaneously, and the five-state legislative ratchet now underway creates exactly that visibility.

Washington State is not Compass’s primary market. California, New York, Texas, and Florida are. Compass’s rational response to a Washington-only mandate is to allow surface compliance in Washington while doubling down on private exclusive infrastructure in the forty-four states where no legislation is pending or enacted. Wisconsin’s Act 69 takes effect January 1, 2027; Connecticut, Hawaii, and Illinois have active bills moving; Washington is the only state with a signed law. Forty-four states remain open territory. California is the most consequential next accelerant: CAR-AG tension with Compass is active, the California market represents Compass’s largest revenue concentration, and 500,000 suppressed listings on Redfin now provides the specific legislative hook prior California sessions lacked.

The Kelman reversal timeline is now permanently in the legislative record available to every state that follows: public pledge April 2025, Rocket acquisition closes, pledge reverses within months, February 26 statement reads “Our perspective evolved.” The harm is now demonstrable with a browser and two tabs. A legislative staffer can open Redfin in any state, find a Compass listing, and show the committee the two-tiered information environment — Compass listings stripped of days on market while every other listing shows it — on a laptop, in real time, without expert witnesses.

The Active State Legislative Ratchet — March 2026

As of March 3, 2026 — the same day SSB 6091 passed the Washington House 92–1 — Inman News confirmed that four additional states have active concurrent marketing legislation in progress. The legislative ratchet is not a future scenario. It is the present state of play across five enacted or pending bills, each adding a node to the Parker v. Brown “clearly articulated state policy” defense that makes federal preemption progressively harder with every enacting state. Compass’s public response — characterizing all five as “veiled attempts by Zillow to preserve its market dominance” — is the Narrative Inversion Playbook applied to a multi-state front. Each state has independent institutional actors supporting the bills: state Realtor associations, state real estate commissions, and bipartisan legislative sponsors with no Zillow organizational affiliation. Compass cannot run the Astroturf Coefficient deflection in five states simultaneously without the pattern becoming the story.

Each of those four states — Wisconsin (Act 69, effective January 1, 2027), Connecticut (SB 340), Hawaii (SB 2806), and Illinois (HB 4964) — presents a distinct legislative design: Wisconsin’s opt-out architecture, Connecticut’s “limited access channels” framing, Hawaii’s CPA enforcement hook, and Illinois’s showing-refusal prohibition. No single bill combines all four elements. The bill-by-bill analysis, the definitional gap each drafting committee must close, and the Parker v. Brown compounding effect across enacting states are developed in full in Installment IV: The 50-State Replication Strategy.

Federal Inaction Has Elevated State Authority (Jan 2026)

Judicial Process as Competitive Federalism (Feb 2026)

See Which States Are Looking to Limit Private Real Estate Listings, Inman News (Mar 3, 2026)

F. Internal Platform Migration — Confirmed via Redfin

Platform migration — moving the private exclusive infrastructure from MLS-adjacent broker networks to consumer-facing portals — was the December 2025 MindCast AI prediction that the Redfin partnership confirmed. The mechanism is identical to the shadow market architecture: intercept the buyer before open-market competition can operate. The evidence is now public, contractual, and available to every enforcement authority watching.

Goodwill Impairment Implication

Compass just structured a three-year national platform deal anchored entirely on its exclusive listing inventory. If Rocket’s $1.75 billion acquisition of Redfin was premised on Compass’s listing inventory as the primary driver of partnership value, the market is implicitly pricing the Layer 3 private exclusive premium at the upper end of the $400–800 million range estimated in the Anywhere acquisition analysis. Anywhere executives called private listings “short-sighted” on the record. Those same brands are now enrolled in a national information suppression contract.

Auditors testing goodwill assumptions now have three evidentiary inputs simultaneously: acquired leadership skepticism timestamped on earnings calls, a signed three-year contract confirming the mechanism is the strategic rationale, and a state legislative ratchet — with multi-state replication underway — eliminating the operating condition the goodwill premium requires. The impairment question is when, not whether.

Platform migration does not require Compass to suppress a single listing under SSB 6091’s terms. The law governs broker marketing obligations. It does not govern what a licensed brokerage’s search platform displays — which is why the Washington CPA enforcement vector and the Redfin fiduciary liability theory matter independently of the statute. Closing the platform gap requires either a supplemental display provision or an AG enforcement action under existing authority.

The Compass-Redfin Alliance: Market Self-Correction Is Dead (Feb 26, 2026)

Compass’s Coasean Coordination Problem Part II: Litigation-Acquisition Monopolization Strategy (Dec 2025)

G. The Rocket Mortgage Vertical Tying Arrangement

The Rocket Mortgage tying arrangement is the newest vector and the one with the most immediate federal enforcement implications. RESPA Section 8 was specifically designed to reach exactly this three-party referral architecture. The Washington AG holds independent enforcement authority without waiting for CFPB action. One million buyer leads routed exclusively to Compass agents over three years is a quantifiable “thing of value” — not a marketing arrangement.

Rocket Companies is the nation’s largest residential lender. The referral mechanism runs in three sequential steps:

Step 1 — Lead Capture: Redfin routes all buyer inquiries on Compass listings exclusively to Compass agents. No competing brokerage receives the lead. No referral fee changes hands.

Step 2 — Agent Capture: Compass agents present Rocket Mortgage as the preferred lender, backed by exclusive buyer incentives unavailable through any other lender: a 1-point first-year rate reduction or up to $6,000 in lender credits, available only to Compass clients.

Step 3 — Lender Capture: Rocket’s mortgage products are embedded into Compass’s platform. One million buyer leads route exclusively to Compass agents over the three-year term — each one a potential Rocket mortgage origination.

Each step transfers value between parties in the referral chain. Under RESPA Section 8, a “thing of value” includes any referral of settlement service business — not merely cash payments. One million exclusive buyer leads over three years, structured in a signed contract, satisfies that standard on its face. The question for enforcement counsel is not whether the structure fits RESPA — it does — but which agency files first: CFPB, the Washington AG, or a plaintiff’s class.

Washington State Enforcement — Independent of CFPB

Washington’s Consumer Loan Act and mortgage broker regulations give the AG’s office enforcement authority over this referral structure without waiting for federal action. Washington’s AG is simultaneously a plaintiff against Redfin in federal court (the FTC–Redfin rental market antitrust action, September 30, 2025) and now watching Redfin become the primary distribution infrastructure for the information suppression SSB 6091 was designed to prevent. That dual position gives Washington’s AG a structural enforcement advantage no other state AG currently holds. State AG consumer finance divisions should examine whether the Rocket–Compass–Redfin referral structure satisfies state anti-kickback and anti-tying provisions independent of CFPB’s posture.

Redfin Fiduciary Liability

Redfin operates in Washington as a licensed brokerage. Redfin buyer’s agents showing clients Compass listings stripped of days on market and price history — data the agent knows exists because every other listing on the same platform displays it — are systematically positioned to breach RCW 18.86 disclosure obligations at platform scale. Systemic fiduciary breach at platform scale is not an individual case management question. It is a regulatory enforcement action, and one the AG’s office can open under existing authority today, before SSB 6091’s effective date.

The Compass-Redfin Alliance: Market Self-Correction Is Dead (Feb 26, 2026)

IV. PROBABILITY MATRIX — UPDATED FEBRUARY 26, 2026

The consolidated probability matrix reflects conditions as of February 26, 2026 — the date the Redfin partnership was announced. Three vectors shifted materially on that date: Vector B Track 2 moved from prediction to confirmed; Vector C attempt probability dropped because the Redfin contract makes the constitutional market-exclusion argument untenable; and Vector G became operational. All probabilities assume no active countermeasures unless otherwise noted.

* Elevated post-Anywhere merger. Coldwell Banker, Century 21, and Sotheby’s networks extend internal buyer depth substantially.

** Medium-High but legally exposed. Washington CPA provides an independent enforcement vector against the two-tiered information display architecture under current law.

*** Medium-High only if uncontested. Active MindCast AI engagement in DOL rulemaking process substantially reduces this probability.

The probability matrix reveals a structural asymmetry: the highest-probability vectors (D, E, B Track 2) are also the least visible to the public record, while the lowest-probability vector (C) would have generated the most press coverage. Compass’s Plan B is designed to operate beneath the enforcement threshold of any single actor. The countermeasure logic runs in the opposite direction: the vectors with the highest uncontested success probability are the ones that require the most immediate institutional response.

V. THE NWMLS LITIGATION TRAP — THE SELLER CHOICE INVERSION

The Compass v. NWMLS litigation dynamic cuts both ways on Plan B. The federal litigation prong is not merely a constitutional long shot — it is actively constrained by Compass’s existing federal posture, and the Redfin partnership locks that constraint in for three years.

The Forward Lock. In Compass v. NWMLS, Compass argues NWMLS’s mandatory submission rules are anticompetitive restrictions on seller choice. Any injunction against SSB 6091 would require arguing the opposite: that a mandatory concurrent marketing requirement violates homeowner property rights. Both arguments dress in seller-choice language. The underlying ask is structurally inverted. The Redfin contract is now the third document in that record — a three-year business obligation that cannot be unwound while the NWMLS and Zillow trials run.

The Narrative Inversion Playbook documented the foundational contradiction across five argument pairs with pinpoint federal complaint citations. The Redfin partnership converts that rhetorical contradiction into a contractual one. Compass is now obligated — by contract — for three years to display listings with no days on market and no price history: the exact data fields Reffkin named as “misleading insights that damage value.” Every deposition in the Zillow and NWMLS trials can reference it. Every state legislative hearing during that window can reference it. Compass cannot settle its way out of the contradiction while the contract runs.

The common variable across all three forums is not seller choice. The common variable is Compass’s pre-MLS window. Anything that closes it is anticompetitive or unconstitutional. Anything that preserves it is seller autonomy. The MindCast AI three-prong monopolization analysis, published December 2025 and timestamped before these events, is the predicate record state AG defense counsel can walk into any courtroom with.

Compass’s Coasean Coordination Problem Part III: Coordination Costs, MLS Governance and the Litigation (Dec 2025)

The Compass Narrative Inversion Playbook (Feb 2026)

SSB 6091 Cross-Forum Analysis (Feb 2026)

Brief of MindCast AI LLC as Amicus Curiae in Support of Defendant NWMLS (May 2025)

VI. THE REFFKIN GIFT — HOW COMPASS DESTROYED ITS OWN ANTITRUST DEFENSE

On February 26, 2026, Compass eliminated its own antitrust defense. The Rocket–Compass–Redfin partnership announcement — 60 million monthly visitors, exclusive lead routing, zero referral fee — gave NWMLS something no court ruling had yet delivered: Compass’s own confirmation that NWMLS listing rules don’t restrict its market access. A firm that reaches more consumers through a single portal partnership than through any regional MLS cannot simultaneously argue that MLS listing requirements constitute exclusionary conduct. Compass signed the press release that destroys its own Compass v. NWMLS theory.

Part 1: The Antitrust Predicate Destruction

Section 2 monopolization claims under the Sherman Act require actual or threatened exclusion from a relevant market. Compass v. NWMLS rests on one essential factual predicate: that NWMLS listing rules deny Compass market access sufficient to constitute exclusionary conduct. Strip that predicate and the antitrust theory collapses before discovery closes.

The Redfin press release strips it — in Compass’s own language, signed by Compass’s own CEO, published simultaneously to every investor, every court, and every opposing counsel. A firm reaching 60 million monthly visitors through a single portal partnership cannot simultaneously argue that regional MLS submission requirements constitute exclusionary restriction on market access. The numbers don’t permit it.

NWMLS serves the Pacific Northwest. Redfin serves the nation. Compass just documented, contractually, that its market reach exceeds anything NWMLS rules could restrict. The geographic scope alone defeats the antitrust premise before Compass’s own counsel can reframe it. Under the relevant market definition framework the Western District of Washington will apply, Compass has now provided affirmative evidence of non-exclusion: national distribution, 60 million monthly visitors, zero cash cost, exclusive lead routing. The exclusionary conduct theory requires the defendant’s conduct to foreclose competitive opportunity. Compass’s own press release forecloses the foreclosure argument.

The Self-Inflicted Estoppel. Compass v. NWMLS requires Compass to prove NWMLS rules restrict its market access. The Redfin partnership proves the opposite — in Compass’s own commercial language, in a binding contract, in a press release Compass authored and published. Judicial estoppel doesn’t require a court ruling to apply. It requires a party to take a position inconsistent with a position previously taken. Compass took both positions on the same day.

Part 2: The Retaliatory Enforcement Calculus Inversion

NWMLS has been waiting — rationally — for antitrust finality before moving against listings such as Team Foster’s address suppression architecture. The retaliatory enforcement narrative had two components: (1) NWMLS selectively targeting Compass while ignoring identical conduct by smaller brokerages, and (2) the selective targeting occurring because NWMLS member brokerages feared Compass’s competitive entry. Both components required the market access predicate to be live.

If NWMLS rules restrict Compass’s market access, then enforcement of those rules against Compass looks like weaponization of regulatory authority for competitive advantage. Compass’s counsel was prepared to run that argument — it is exactly the kind of counterclaim that creates litigation cost asymmetry in favor of a deep-pocketed plaintiff. NWMLS’s rational response was to minimize discretionary enforcement actions that could be characterized as selective targeting while the antitrust proceeding was live.

Compass’s own press release killed the predicate. The retaliatory enforcement narrative is now factually unmoored. NWMLS’s rational restraint before February 26 was not weakness — it was game-theoretically correct play. The restraint is no longer rational.

Part 3: Three Enforcement Actions Now Available to NWMLS

Three specific enforcement actions the changed calculus makes available — each previously constrained by litigation-cost asymmetry, each now executable as routine MLS governance:

Action 1: Close the “Call for Address” Gap

NWMLS rules require an address field but do not prohibit a “Call for Address” entry. The Team Foster address suppression architecture exploits exactly this gap: MLS #2392995, the $79 million Lake Washington estate, is listed without a street address — technically compliant on the face of the current rule text, structurally suppressive in effect. NWMLS updating its address disclosure rules — replacing “Call for Address” with mandatory address disclosure — is routine MLS governance after February 26. Before February 26, the same rule amendment risked characterization as targeted rule-tightening against Compass mid-litigation. Compass’s own press release eliminated that characterization. A firm with 60 million monthly Redfin visitors is not harmed by an address disclosure requirement.

Action 2: Move Against MLS #2392995

The $79 million Lake Washington estate listed without an address is the flagship entry in the Team Foster suppression portfolio documented in the Address Suppression Calculus (February 19, 2026). The evidentiary record is built: the listing, the address suppression, the pattern across seven active Team Foster listings totaling $136 million in inventory. The enforcement predicate existed before February 26. The litigation-cost calculus that made enforcement asymmetric did not survive Reffkin’s press release. NWMLS can move against MLS #2392995 without handing Compass a single usable defense.

Action 3: Audit the Full Team Foster Portfolio

Seven active Team Foster listings documented February 19 — $136 million in inventory, $3.4 million in buyer-side commission at stake — represent a pattern-and-practice enforcement target, not an individual transaction challenge. Pattern-and-practice enforcement establishes systemic conduct, removes the “isolated incident” defense, and creates the evidentiary record that travels into the Compass v. NWMLS proceeding as affirmative evidence of the conduct NWMLS’s listing rules were designed to prevent.

When each Team Foster listing closes, the NWMLS records will document who represented the buyer. If the internalization pattern documented in the Mercer Island Exhibit Transaction repeats — Compass holding both sides — the Layer 3 model confirms. If independent brokers win the buyer side at open-market rates, the enforcement pressure is already reshaping behavior before SSB 6091 formally takes effect.

The Reffkin Gift resolves the central strategic uncertainty that has defined the post-Anywhere period. NWMLS no longer needs to calculate the retaliatory enforcement risk. Every enforcement action it takes after February 26 is routine MLS governance, not litigation-cost asymmetry. The three enforcement actions identified in Part 3 are available today, executable under existing authority, and each one builds the evidentiary record that travels into the Compass v. NWMLS proceeding as affirmative evidence of the conduct the listing rules were designed to prevent.

The Compass-Redfin Alliance: Market Self-Correction Is Dead (Feb 26, 2026) — www.mindcast-ai.com/p/compass-redfin

The Compass Narrative Inversion Playbook (Feb 2026) — www.mindcast-ai.com/p/compass-narrative-inversion-playbook

The Compass-Anywhere Address Suppression Calculus (Feb 2026), The Compass Commission Consolidation Strategy and Real Estate Marketing Transparency

VII. MINDCAST AI STRATEGIC POSITIONING

MindCast AI’s post-passage positioning spans three simultaneous fronts: the DOL rulemaking process, where the analytical record must be filed before Compass’s expected submissions; the Washington AG enforcement surface, where the Redfin two-tiered display architecture is independently actionable under current CPA law; and the 50-state replication strategy, where Washington’s evidentiary record travels to every state legislature that follows. Each front has a distinct timeline and a distinct set of institutional actors.

Immediate Priority: DOL Rulemaking and Redfin Enforcement

Two urgent near-term engagement surfaces define the ten-day sprint following the Governor’s signature: DOL rulemaking comment windows, and Washington AG’s enforcement authority over Redfin’s two-tiered information display architecture under current CPA law — independent of SSB 6091’s effective date.

Research items for the ten-day sprint:

DOL rulemaking timeline and comment period schedule post-signing.

Redfin’s Washington brokerage licensing status and any enforcement inquiries triggered by the February 26 announcement.

Compass-Zillow litigation settlement terms — any provision creating national private exclusive distribution infrastructure.

Multi-state inventory of pending real estate transparency legislation. California most likely next accelerant.

Wisconsin AB 456 implementing regulations — how the opt-out language was administratively interpreted.

Rocket–Compass–Redfin contract terms under Washington Consumer Loan Act and mortgage broker regulations.

Publication Sequencing

The analytical record is positioned for the trial calendar and the state legislative ratchet:

The Narrative Inversion Playbook — established the contradiction during the legislative fight. Published.

The Compass-Redfin Alliance: Market Self-Correction Is Dead — published February 26, 2026.

The Compass Antitrust Self-Destruction Sequence (Installment I) — how aggressive federal litigation birthed the legislation that destroyed the business model. Published.

SSB 6091: What It Reaches and the Enforcement Record It Inherits (Installment II) — operational map, transaction record, first prospective enforcement test. Published.

Compass Plan B: Structural Circumvention After SSB 6091 (this document, Installment III) — publish within 48 hours of Governor’s signature.

The Seller Choice Inversion — post-passage federal court implication analysis. Publish before Compass files anything.

NWMLS Enforcement Action Analysis — Section VI as a standalone briefing for NWMLS counsel and Pacific Northwest brokerages. Publish immediately.

The 50-State Replication Argument

SSB 6091 is the proof of concept. Five states now have enacted or active concurrent marketing legislation as of March 3, 2026: Washington (passed 141–1), Wisconsin (Act 69, effective January 1, 2027), Connecticut (SB 340, pending), Hawaii (SB 2806, pending), and Illinois (HB 4964, pending). The Redfin partnership accelerates legislative activity in each through a mechanism prior sessions lacked: the harm is now demonstrable with a browser and two tabs. Washington’s evidentiary record — the Astroturf Coefficient, the Kelman reversal timeline, the Reffkin earnings call versus the Compass Disclosure Form contradiction — travels to every state that follows without needing to be regenerated from scratch.

Each state that enacts a no-opt-out concurrent marketing requirement reinforces the “clearly articulated state policy” standard under Parker v. Brown, making federal preemption challenges progressively weaker as the state count rises. The Parker defense compounds with each enacting state. Compass’s multi-state dilution strategy (Vector E) relies on regulatory fragmentation to survive. The replication strategy closes that gap state by state. California remains the most consequential next state: CAR-AG tension with Compass is active, Compass’s largest revenue concentration is in California, and 500,000 suppressed listings on Redfin provides the specific legislative hook prior California sessions lacked.

The publication record is positioned for the trial calendar, the DOL rulemaking process, and the state legislative ratchet simultaneously. Each document in the sequence is timestamped before the events it predicted. That record is the institutional credibility that makes MindCast AI’s DOL submissions, AG briefings, and multi-state legislative analysis actionable rather than academic.

Death by a Thousand Depositions: The 42-Day Collapse Framework (Feb 2026)

Federal Inaction Has Elevated State Authority (Jan 2026)

Judicial Process as Competitive Federalism (Jan 2026)

VIII. CONCLUSION

SSB 6091’s 141–1 bicameral passage represents the most significant regulatory constraint on Compass’s core revenue architecture since the company’s founding. The legislative record is built. The analytical documentation is timestamped. The prediction is on record.

Compass’s Plan B is not a single move. It is a seven-vector circumvention architecture operating simultaneously across different institutional surfaces — administrative rulemaking, pre-listing agent networks, a national portal partnership, federal litigation positioning, and a vertical tying arrangement in settlement services — each designed to preserve the pre-MLS window through mechanisms that appear, individually, like technical compliance.

The February 26, 2026 Rocket–Compass–Redfin announcement resolved the central uncertainty: the portal partnership MindCast AI’s December 2025 framework predicted is operational today — a signed three-year contract at zero cash cost to a firm that has never posted a full-year GAAP profit. The merger created the debt. The debt requires the dual commissions. The dual commissions require the pre-MLS window. The Redfin deal is what a firm does when the window starts closing and cash is unavailable. The depositions have not yet begun.