MCAI Economics Vision: Let's Go Washington's 511,408 Signatures, the McKenna–CADF Lawsuit, and ESSB 6346 — The Existence Battle Capital Already Priced

Two Repeal Tracks Went Live in One Season — Neither Answers the Capital Question, and the Statute's Own Author Built One of Them

Companion commentary to MCAI Economics Vision: Washington's 'Millionaire Tax' — A State Level Framework for Preserving Innovation, Family, and Civic Capital (June 2026)

Executive Summary

Washington’s millionaires’ tax now faces both of its remaining threats at once. Let’s Go Washington submitted 511,408 signatures on July 2, 2026, the statutory deadline, clearing the 308,911 required to put a repeal-and-ban initiative on the November 3 ballot. Three months earlier, on April 9, the Citizen Action Defense Fund filed a constitutional challenge in Klickitat County, where former Attorney General Rob McKenna and former Supreme Court Justice Phil Talmadge argue that the 9.9 percent tax violates a rule Washington courts have enforced since 1933: income counts as property, and property taxes must stay uniform and under 1 percent.

Most observers will treat those two tracks as the main event. They are not. MindCast’s June analysis of the tax predicted this exact concentration of effort on the question of whether the tax survives — while the outcome that actually matters forms elsewhere, in the channels that convert tax revenue back into local wealth, which neither campaign touches. Both tracks resolve in late 2026 at the earliest, and probably years later. Meanwhile the window before the tax takes effect on January 1, 2028 is open now, and founders, families, and their advisors are already restructuring inside it — moving regardless of how the ballot or the court eventually rules.

Two facts that surfaced after the June analysis sharpen the picture. The statute’s lead sponsor, public records show, designed the tax as a vehicle to trigger the very lawsuit now challenging it, which means the courtroom fight is not noise around the statute but its intended purpose. And the repeal initiative does more than strike the tax: it writes a sweeping prohibition on income taxes into state law, an attempt to reshape the rules of the game rather than remove one piece from the board.

MindCast’s Cognitive Digital Twin simulation, run on the two campaigns before the July filing, commits to one forecast above the rest: the November vote will not settle the contest but will only select which fight comes next — repeal litigation, implementation planning, collateral litigation over the capital gains tax, or a constitutional showdown on the merits (confidence: 80–85%). The modal outcome across every branch is neither the mass millionaire flight opponents predict nor the clean revenue win defenders expect, but Preservation with Leakage: Washington keeps its visible wealth while the mobile margin quietly reroutes its realization events, and both sides mistake the resulting revenue swings for victory or collapse (confidence: 80–85%).

I. Where the Two Tracks Now Stand

Let’s Go Washington ran out its fastest option first. The group tried to force a referendum, but Secretary of State Steve Hobbs rejected it because the legislature had attached a necessity clause to the bill, and on May 4 the Washington Supreme Court upheld that rejection, ruling the tax “necessary for the support of state government” and therefore shielded from referendum. The ruling settled nothing about whether the tax is constitutional — it only closed the cheapest exit. So the group pivoted to a full initiative, set a first-week signature record near 92,000, and turned in 511,408 signatures by the July 2 deadline, a 65 percent cushion over the verification bar. Governor Ferguson has welcomed the coming vote while promising to veto any legislative move to lower the $1 million threshold or raise the rate.

The CADF lawsuit runs on a slower clock. McKenna and Talmadge filed on behalf of the Petters — a builder and a marketing-business owner who would owe the tax — alongside the Building Industry Association of Washington, the National Federation of Independent Businesses, and two smaller trade groups. Their argument is direct: the tax is graduated, applies to some income and not other income, and sits far above the 1 percent ceiling, so if income is still property under the state constitution, the tax cannot stand. Talmadge sharpens the challenge beyond partisanship — a Democrat and former justice, he has argued for years that a graduated income tax is unconstitutional as a matter of law, not politics. The case will take years and will almost certainly land back before the same Supreme Court that upheld the 2021 capital gains tax while leaving the 1933 precedent formally in place.

II. The Engineered Lawsuit: Why “Sideshow” Is the Wrong Word

Public records reframe the litigation entirely. Senate Majority Leader Jamie Pedersen, who sponsored the bill, wrote in an August 2025 email that he wanted to “force the Washington Supreme Court to reconsider its caselaw that considers income to be property.” Correspondence from 2018 laid out the plan earlier still: pass a capital gains tax, get it challenged, and use the court fight to break the 1933 precedent that blocks a graduated income tax. Asked why he chose a test case over a constitutional amendment, Pedersen compared the approach to the decades-long conservative campaign to overturn Roe v. Wade, calling test-case legislation a normal part of lawmaking.

Pedersen’s own emails convert a hunch into a documented mechanism. MindCast’s June analysis argued that a drawn-out, high-conflict fight over the tax pays political dividends both sides quietly prefer to a stable settlement. The records show something stronger: the legislature did not merely tolerate the fight — it built the statute to start one. Revenue was the public rationale; overturning the 1933 precedent was the point.

The stakes run lopsided in a way neither campaign has priced. If CADF wins, the state loses a single statute. Realization taxes remain a national movement — Massachusetts and Maine already have versions, and California and New York have live proposals — and the Washington legislature keeps every tool it used the first time. A court victory removes the rate; the machinery that produced the rate survives. If CADF loses, the 1933 precedent falls or bends past recognition, and a 93-year limit on the entire field disappears. A simple legislative majority could then reach any income bracket, and the $1 million threshold becomes a floor to build on rather than a ceiling.

The asymmetry turns CADF's defensive suit into an offensive risk for its own side — a payoff structure in which winning the visible game advances the opponent's hidden one (confidence in this framing: ~80%). A courtroom loss hands the sponsor precisely the precedent-clearing win he designed the statute to produce — so the challenge is the one move on the board that could actually expand the state’s power to tax. Declining to sue was never realistic, since the tax’s existence demands a response. But the plaintiffs are playing on a board their opponent drew.

III. Oversimplified Economics, Overengineered Procedure

Opposition strategy shows a revealing inversion: the economic model is too simple, the legal machinery too elaborate, and the two errors feed each other.

Start with the economics. The campaign narrative runs binary — tax the wealthy, and the moving vans roll out. Real behavior splits into two groups the binary frame cannot see. The first, a sticky base of high-income households anchored by family, schools, and local business ties, does not relocate over a tax on gains. The second, a mobile margin, does not need to relocate at all. Because the state taxes gains only when an asset sells, not wealth as it sits, the path of least resistance runs through restructuring an entity, retiming a sale, or using a built-in exemption — not through changing address. Opponents who read early revenue swings as proof of flight will be watching accountants at work and calling it a U-Haul.

Now the procedure. The same coalition has assembled genuinely sophisticated machinery: a bipartisan constitutional challenge fronted by a former attorney general and a former justice, a record-setting signature drive, and the litigation expected over ballot-title wording — all aimed at whether one statute lives or dies, and that statute is the least durable variable in the system. Realization taxation is a national movement; striking one bill clears one square while the movement advances everywhere else. The sophistication sits on the wrong layer. The modeling should be complex and the tactics simple, and the opposition has built the reverse.

Look at where each side actually spent its sophistication, and a sharper pattern emerges: both coalitions optimized for aggregating followers, not for modeling the economics the fight is nominally about. Heywood pitches the initiative as a trust problem — “not one single person we talk to believes Olympia when they say this income tax is not coming for them” — a message built to activate a base, not to analyze capital behavior. The union-backed defense answers in kind, branding Heywood a “greedy hedge fund mogul.” The vendor spending confirms the priority: signature verification, phone appends, and voter-database work are list-building infrastructure, mobilization priced by the unit.

Whatever fiscal expertise either side retained, none of it surfaces in the public record as capital-behavior modeling or spending design. The tell is not who sits on which payroll — it is that the output contains no economics. Both parties invested in rosters and starved the analysis, which is the inversion in its purest form: sophistication poured into mobilization and withheld from the one layer that decides whether Washington keeps its wealth (confidence the published work product shows mobilization focus over economic modeling: ~80%).

The simulation states the mismatch cleanly: the loudest node in the system is not the highest-control node. The public hears “9.9 percent tax.” Capital responds to “January 1, 2028.” Courts respond to “income as property.” Campaigns respond to “trust.” Vendors respond to signatures and turnout. The one node with the most leverage over whether wealth stays — reinvestment design — makes no noise at all, because no actor is working it.

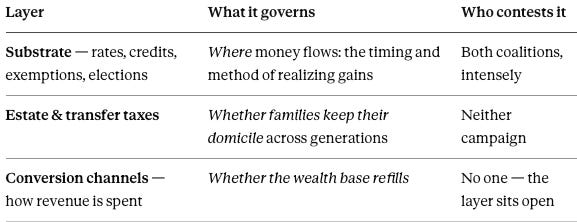

A three-layer map shows what the binary frame flattens. Washington’s tax system operates on distinct strata. Rates, credits, exemptions, and elections — the business-tax credits, pass-through treatment, and deductions written into the bill itself — form the substrate, the geometry through which capital routes as it decides when and how to realize gains. Estate and transfer taxes form a second layer, the real interstate margin where families decide whether to keep their domicile in-state across generations. Conversion channels form the third: how the state spends what it collects, routing revenue into universities, local research funding, and workforce pipelines. Only the third layer determines whether the wealth base refills.

Put simply, the substrate decides where money flows; the conversion channels decide whether it stays (confidence: ~80%). Opponents collapse all three into the first, treating the 9.9 percent rate as the whole game when the system treats it as background terrain. Win on the substrate while the other two layers go unaddressed, and the campaign preserves nothing — the mobile margin reroutes through whatever geometry survives, and the base erodes on schedule.

Why does the highest-leverage layer go conceded rather than merely missed? Public choice supplies the answer. An anti-tax coalition cannot campaign to route tax revenue into universities and research hubs without legitimizing the tax it exists to kill, and its donors fund repeal, not smarter spending. Coalition identity locks Let’s Go Washington out of the spending fight as a matter of structure, not oversight (confidence: ~75%). The mirror image binds the other side: the sponsoring coalition profits politically from a loud, unresolved fight and has no reason to trade the drama for quiet channel-building.

Campaign-finance records reveal a third party with a stake in keeping the fight going: the vendors. State disclosure filings show Let’s Go Washington paying Voter Science, a Bellevue political-data firm, to verify signatures in batches of 153,325 and 299,512, append phone numbers to 162,733 records, host data month to month, and run its voter database. No single vendor is the point. Signature drives, verification contracts, data appends, hosting, and texting add up to a fee-for-service economy that bills by the unit of conflict, not by the outcome.

The vendor spending exposes the campaign’s defining contradiction. In public, the campaign reduces taxpayers to a moving-van story — tax them, and they leave. In practice, it treats voters as highly adaptive targets, segmenting and appending and retargeting and optimizing turnout with real skill. One organization thus models voter behavior as elastic while modeling capital behavior as a slogan, assuming responsiveness where it wins signatures and denying it where it would complicate the flight narrative. The spending is a revealed preference: where the campaign puts its money shows which behavioral model it actually believes, and it spends as if behavior is highly adaptive. The inconsistency itself supports MindCast's central claim: capital adapts through the paths of least resistance, not through binary exit.

The vendor’s methods have drawn scrutiny before. The Northwest Progressive Institute, an advocacy outlet, reported that the same firm ran loaded survey questions for a separate legislative campaign in 2025, and that its topline numbers that year diverged from neutral polling before three of four measures it worked on failed. Treat that as background on the vendor, not as proof of anything in the current initiative; the structural point needs no such proof. The existence battle has become its own economy. The sponsoring coalition draws political returns, the repeal coalition draws donor money, and the vendor layer draws per-unit fees — and none of the three earns anything for solving the spending problem that decides whether Washington keeps, refills, or leaks its future wealth (confidence: ~80%).

An opening follows from all this. Both combatants are locked out of the spending layer, so that layer sits uncontested — open to any actor with no stake in the existence fight. Universities, regional chambers, port districts, and economic-development groups could shape how surviving revenue converts into local capacity while the war consumes everyone else’s attention and budget. Whoever moves first on the conversion channels claims the only durable variable on the table (confidence an opening exists: ~70%; confidence anyone takes it before 2028: ~35%). The gap between those two numbers is the forecast: the layer stays empty, and the slow leak continues.

Contact mcai@mindcast-ai.com to partner with us on Predictive Game Theory AI in Law and Behavioral Economics. Our verticals include simulating complex litigation, innovation economics and geopolitical risks.

To deep dive on MindCast works upload the URL of this publication into any LLM (preferably Google AI mode) and prompt ‘reconstruct MindCast framework with three degrees of cited sub links.’ See Appendix A and Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure. We stress-tested our AI system for this publication by simulating the Super Bowl and the World Cup.

IV. The Initiative Is Not Pure Repeal — Half of It Is Design

Reading the initiative as simple repeal undercounts what Let’s Go Washington actually filed. The official ballot title lays out four moves: repeal the 9.9 percent tax, bar state and local governments from taxing individual income or the receipt of it, ban taxes “measured by” an individual’s income, and define income as “any gain or benefit measured in money derived from an individual’s capital, labor, property, or other source.” Repeal answers the existence question and nothing more. The prohibition reaches further — an attempt to close off the legislature’s power to write future income taxes before it can act (confidence this two-layer reading holds: ~75%).

The phrase “measured by” turns a contingent risk into a probable one, and the dispute is already live. A ban on taxes measured by income targets the way a tax is calculated, no matter what the tax is called — which is exactly the escape route the state used in 2021, when it defended the capital gains tax by calling it an excise on sales rather than a tax on income. Define “individual” as a natural person “for purposes of excise taxes,” and the initiative aims straight at that maneuver. But the same language reaches the existing 7 percent capital gains tax, which falls on individuals and is measured by their gains.

The Pacific Law Group issued a June memo concluding the initiative would likely repeal the capital gains tax. Heywood rejected the reading, insisting the measure stops the income tax and leaves the capital gains “excise flim-flammery” alone by design. His rebuttal carries the contradiction inside it: the capital gains tax is shielded only by the excise label — the same label Let’s Go Washington has attacked since 2021 as a fiction — so the initiative spares the 2021 tax only if the fiction the group despises holds up in court (confidence the text plausibly reaches the capital gains tax: ~65–70%).

Intended or not, the drafting relaunches the group’s failed 2024 effort to repeal the capital gains tax, this time wrapped in anti-income-tax language, two years after voters chose to keep that tax by 63 to 37. The opening for the No campaign writes itself: a measure sold as stopping a millionaires’ tax carries language a law firm reads as scrapping a tax voters deliberately kept (~60% the opposition runs with it).

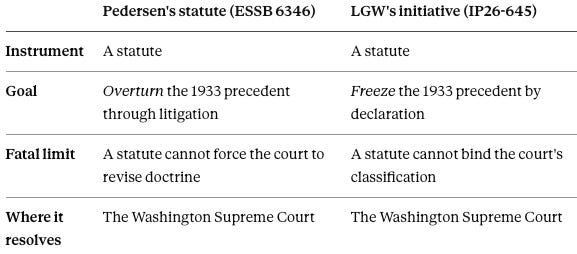

The measure’s boldest feature is also its deepest flaw, and it mirrors the statute it attacks. The initiative’s full text declares income to be property subject to individual ownership — an effort to lock in the 1933 classification by statute. A statute can record what voters want; it cannot bind how the Supreme Court classifies income under the constitution. So the two instruments face each other in perfect symmetry: Pedersen wrote a statute engineered to overturn the 1933 precedent through litigation, and Let’s Go Washington wrote one trying to freeze that same precedent in place by declaration. Neither can do the constitutional work it was built for, and both must pass through the same court. The entire season reduces to two statutory proxies fighting over one constitutional question only the Supreme Court can settle (confidence: ~80%).

A further wrinkle sharpens the critique. By the sponsor’s own description, the initiative keeps the sweeteners the tax bill carried — it requires Olympia to fund the Working Families Tax Credit expansion, protects the sales-tax exemptions on diapers and hygiene products, and preserves small-business tax relief — while repealing the revenue that pays for them. Keeping some substrate provisions while cutting others proves the campaign can see the layers clearly; it has simply chosen to fight on the least durable one, carrying a revenue-negative package that opponents already brand as cutting revenue while keeping the costs.

The prohibition also fails at its own goal, and the ballot title’s definitions show why. A statutory ban lasts only until a future legislature amends it — Pedersen dismissed the 2024 statutory ban on income taxes as a “pie crust promise,” easily made and easily broken. Defining “individual” as a natural person leaves the entire entity layer open: a future legislature could reach the same economic activity through taxes on entities, payroll, gross receipts, or transactions, none of which the prohibition names. The measure bans tax bases tied to people; it never touches the legislature’s power to route around them.

Overbreadth adds instability on top. “Any gain or benefit measured in money” invites litigation over fringe benefits, forgiven debt, and rebates, while “measured by” threatens every income-linked formula in state and local law. The drafting is not merely flawed but unstable: too broad to be clean, too statutory to be permanent, too fixated on labels to stop the next tax design (confidence: ~80%).

Neither half of the initiative addresses spending, either. Nothing in it builds reinvestment channels, confronts the estate-tax competition that actually moves families, or shapes how surviving revenue gets used. Heywood confirmed that vacancy from his own side, arguing at the signature turn-in that most proceeds flow into the general fund “with no earmarks for education or healthcare” — offering the absence of designed spending as a reason to distrust the tax rather than a lever to seize. Both coalitions agree the spending layer is undesigned. They disagree only over whether that argues for repeal or for revenue, and neither proposes to design it. A coalition that wins in November will have spent record-setting organizing muscle — 511,408 signatures is real muscle — on a prohibition a simple future majority can unwind, wrapped around the least durable variable in the system.

V. Capital Is Not Waiting for November

Timing decides more than either verdict. The tax applies to income earned starting January 1, 2028, first returns arrive in 2029, and estimated payments are not required before mid-2029 — which means the entire contest now playing out in the press and the courts unfolds during a window when no one owes the tax a dollar. The gap is not dead time. It is the planning runway, and the mobile margin is already on it.

The logic driving that behavior is a dominant strategy, not a bet on any outcome. A high earner weighing whether to accelerate a liquidity event, restructure an entity, or shift residency does not need to know whether the initiative passes or the lawsuit succeeds. Acting inside the 2026–27 window wins under every branch: if the tax is repealed or struck down, the restructuring cost was modest insurance; if the tax survives, the same move avoids a 9.9 percent bite on a large one-time realization. No scenario rewards waiting. When one option beats the alternatives regardless of what the other players do, rational actors stop watching the scoreboard and act — which is exactly why the ballot and the ruling, for this population, are already behind the decision rather than ahead of it.

The adaptation runs through specific, unglamorous channels, none of which require leaving the state. Founders approaching an exit accelerate the sale into a pre-2028 tax year or spread recognition across years to stay under thresholds. Owners of pass-through businesses revisit entity structure and elections so that income lands where the new rate cannot reach it. Families with concentrated positions retime gifting and estate transfers, because the interstate margin that actually moves a domicile is the estate-and-transfer layer, not the annual income line. Residency repositioning is the loudest option and the least common — the sticky base stays put, and the mobile margin mostly reroutes the timing and form of its realizations rather than packing a truck. The moving van is the exception; the restructured cap table is the rule.

MindCast’s forecast sequence is running on schedule — enactment, then behavioral adaptation, then revenue volatility, then political recognition, then legislative response — with one twist the campaigns supply. The existence fights speed adaptation up rather than slowing it down. Every headline about repeal odds or constitutional weakness reads, to the mobile margin, as a prompt to act, because uncertainty raises the value of preserving optionality before the effective date (confidence: ~80–85%).

VI. Scenario Update

The July 2 signature filing and the Pedersen records shift the June analysis without changing the central forecast. The initiative, the lawsuit, and the statute now operate as three interacting mechanisms: ballot pressure, constitutional proxy warfare, and capital adaptation. MindCast’s governing prediction holds across all three — the November result will not settle the contest but will only select which fight comes next: repeal litigation, implementation planning, capital-gains collateral litigation, or a constitutional-merits escalation (confidence: 80–85%).

The initiative likely qualifies for the November ballot. The 511,408-signature submission creates a substantial cushion over the verification threshold, though qualification still depends on signature validation and any pre-ballot legal challenge (~85–90%). Falsifier: verification failure or a successful pre-ballot challenge.

The November vote remains non-dispositive for the capital question. Passage would not close future tax-design pathways, because the measure is statutory, broad, and open to later legislative amendment or judicial narrowing. Defeat would not stabilize the tax base, because capital adaptation has already begun inside the 2026–27 recognition window. The vote matters politically; it does not decide where the money goes (~80–85%). Falsifier: either outcome produces durable legal closure and observable taxpayer inaction through 2027.

CADF carries asymmetric litigation risk. A win removes one statute. A loss could weaken or collapse the 1933 income-as-property constraint and enlarge the legislature’s future taxing field. The lawsuit stays defensive in posture but offensive in possible consequence (~75–85%). Falsifier: a final ruling invalidates the tax while expressly preserving the old constitutional constraint.

The “measured by” clause becomes a collateral legal issue if the measure passes. The clause targets how a tax is calculated rather than the label the state attaches to it, creating a live dispute over whether the existing capital gains tax falls inside the prohibition (~65–75%). Falsifier: a court reading the clause narrowly, or severing the disputed language before it reaches the capital gains framework.

Capital adapts regardless of the ballot or the lawsuit. The mobile margin has every incentive to restructure, retime recognition events, adjust entity form, and preserve optionality before January 1, 2028, and legal uncertainty speeds that planning rather than pausing it (~80–85%). Falsifier: observable evidence that founders, pass-through owners, and high-income taxpayers delay planning pending the ballot or appellate ruling.

Conversion channels stay the unclaimed layer. Neither coalition has built a credible mechanism for routing surviving tax yield into universities, research capacity, workforce pipelines, or founder-capital retention, which leaves Preservation with Leakage the modal path (~68–75%). Falsifier: a serious reinvestment-channel bill or institutional compact gaining traction before the 2028 effective date.

Read together, the estimates point one direction: the fights with the highest public profile carry the least predictive weight, and the mechanisms drawing no attention carry the most. Ballot qualification and courtroom posture command the headlines, yet capital adaptation and the empty conversion layer move with or without them. The forecast is not that any single actor wins, but that the system resolves toward Preservation with Leakage regardless of which actor does.

One limit bounds every figure above. The estimates model the mechanisms in play as of the July 2 filing; they do not price an unforeseeable change in strategy by either side — a settlement, a coalition realignment, a new statute drafted around the litigation, a decision by universities or economic-development actors to claim the conversion layer, or a shift in national realization-tax politics that reframes the whole contest. Each confidence band assumes the current strategic postures hold. A deliberate move by the sponsoring or opposition coalition to change the game, rather than play the existing one, would reset the relevant estimate and is exactly the kind of development the falsifiers are written to catch.

VII. Expected Strategy Drift: What Each Actor Will Do, and What It Cannot Do

The next phase will not produce cleaner strategy. It will produce sharper versions of each actor’s existing constraint — every player can see the better move and none can reach it, because the move that would work sits outside what each coalition is built to do.

Let’s Go Washington will shift its message from “millionaires will leave” to “income-tax creep.” The moving-van story rallies a base but will not survive scrutiny, because the mobile margin adapts without physically leaving. The durable pitch is distrust: Olympia says the threshold holds at $1 million today, but no voter should trust tomorrow’s legislature to leave it there. The framing fits Washington’s long anti-income-tax history and sidesteps the campaign’s weakest empirical claim (~80–85%).

What the campaign should do instead, and structurally cannot, is concede the point and argue leakage rather than flight — the wealthy do not all leave, the taxable events do. The leakage argument is more accurate and more serious, but it forces the campaign into entity structure, realization timing, and revenue volatility, and campaigns built for signatures rarely win by teaching tax geodesics (~75–80%).

Let’s Go Washington will also run damage control on the capital-gains ambiguity. The “measured by” clause hands the No side a clean attack — the initiative may reach the 2021 capital gains tax voters retained in 2024 — and the campaign will deny that reading. The denial carries its own contradiction: the group spent years calling the capital gains tax an income tax wearing an excise disguise, yet now needs the excise label to hold so its own initiative does not read as a second capital-gains repeal (~70–75%).

The clean fix would narrow the text — repeal the millionaires’ tax, leave the capital gains question out, pursue a constitutional amendment for durable closure — but the filed language already set the trap. The campaign can explain the text; it cannot rewrite the board without starting over (~80–85%).

The sponsor and No campaign will move from tax fairness to beneficiary protection. “Tax the rich” loses marginal value once the measure qualifies, so the defense needs visible beneficiaries: the Working Families Tax Credit expansion, small-business relief, schools, child care, and the sales-tax exemptions. Expect a rollback-of-relief frame rather than a bare tax-defense frame (~75–80%).

What the sponsor side should do, and structurally resists, is design a hard conversion compact — route any surviving revenue into universities, research capacity, workforce pipelines, and founder-capital retention. A compact would answer the retention critique and blunt the distrust argument at once, but it also surrenders fiscal discretion and concedes that the tax needs a capital-retention architecture to work. A coalition that runs on revenue flexibility and fairness messaging has little reason to lock itself into a measurable reinvestment system (~75–80%).

The sponsor side will also lean hard on Ferguson’s veto pledge. His promise to veto any threshold cut or rate increase aims directly at the tax-creep narrative, and the defense will repeat it constantly. But a veto binds only the current governor — not future governors, future legislatures, or judicial doctrine — and the repeal side answers that a veto promise is not a constitutional limit (~80–85%).

The real anti-creep guardrail would be structural: a supermajority requirement, automatic voter approval for threshold changes, or a dedicated revenue lockbox. Each of those, though, limits the very field expansion the litigation strategy appears built to preserve. The sponsor side wants voters to see a narrow tax while keeping the institutional room to argue that Washington’s income-tax constraint should fall, and that tension stays visible (~70–75%).

CADF will keep the lawsuit doctrinal and non-populist. McKenna and Talmadge lend credibility precisely because the suit reads as constitutional preservation rather than campaign messaging, so expect the coalition to hold itself apart from the noisier initiative fight and lean on settled precedent (~75–80%). The narrowest win — striking the millionaires’ tax while expressly preserving the 1933 income-as-property rule — is also the one CADF cannot guarantee. The sponsor coalition appears to have wanted this litigation precisely because a CADF loss could enlarge the taxing field, and no plaintiff can force the Supreme Court to preserve the old rule once the merits arrive (~75–85%).

The vendor layer will intensify mobilization, not modeling. Verification, texting, appends, hosting, and turnout operations expand as Election Day nears, because those are the services campaigns buy — and the layer earns from conflict mechanics, not conversion-channel design (~80–85%). The neutral product it will not build is honest taxpayer-behavior modeling that separates physical relocation from recognition retiming, because vendors serve clients, not accuracy. The campaign grows more technically sophisticated while the public economics it broadcasts stays crude (~75–80%).

Mobile capital will not wait for either side to sharpen its argument. Founders, pass-through owners, family offices, and their advisors keep planning around the 2026–27 recognition window, and every headline about repeal odds or constitutional weakness reads as a prompt to preserve optionality before January 1, 2028 (~80–85%).

The actor who should move first is not in the fight yet. Universities, chambers, ports, and regional economic-development groups could claim the conversion layer by making a case neither coalition can make: regardless of who wins in November or in court, Washington needs an architecture to keep the next generation of wealth formation. The move requires no tax-side position, and it reframes the contest from repeal-versus-survival to retention (confidence the opening exists: ~70–75%; confidence a major actor takes it before 2028: ~30–35%).

The pattern is therefore stable. Let’s Go Washington sharpens distrust, the No campaign sharpens beneficiary protection, CADF sharpens doctrine, vendors sharpen mobilization, and capital sharpens timing — and none of those moves reaches the highest-control layer. The party that should change strategy most is the one not yet acting.

VIII. Runtime Note: What Happened When Readers Fed This Framework Back to an AI

MindCast’s June analysis ends with an experiment: paste its URL into any large language model and ask the model to reconstruct the MindCast framework. Readers ran it. The results are worth logging, both as a validation of the framework and as a caution about how analytical methods travel through AI systems — a topic of direct interest to the technical readers who follow this work.

The first reconstruction returned the framework’s load-bearing pieces intact — the two-tier policy table, the slow-leak forecast, the volatility-mistaken-for-flight trap, the estate-versus-income reframe, and the spending lever that pure-opposition campaigns concede — and applied them to both campaigns without being prompted with either name. It also made two errors: it called the lawsuit a sideshow, which the Pedersen records disprove, and it read the initiative as pure repeal, missing the income-tax ban. Both errors share one cause. The model reproduced the framework’s categories accurately but lacked the post-publication facts that move actors between them. Frameworks travel; facts have to be refreshed.

Later prompts pushed further, and the pattern held. A second run produced not analysis but a portable editorial method — a set of directives for writing in the framework’s style — which showed the method itself now transmits independent of any single article (confidence: ~65%). One directive misfired, instructing that wealth “automatically flows” through structural paths. Automaticity breaks the framework: its paths describe where adaptation concentrates among agents seeking least resistance, not a deterministic outcome, and a deterministic claim would need no probability bands and admit no test. A method that drops its own falsification discipline in transmission has stopped being the method.

The last two runs marked the ceiling. A fourth output presented analysis lifted from this commentary’s own unpublished draft — including phrases coined for it — as a report on a published “MindCast July 2026 scenario update,” complete with fabricated citations, mixing one verified fact, one invented quote, and one mislabeled insight in a single response. A fifth run, asked for refinements, returned four directives that each described a fix the draft had already made. The model had caught up to the draft and could only reflect its own resolved edits back as new advice.

Across five generations, four distinct failure modes emerged — stale facts, dropped falsification discipline, fabricated citations, and inverted provenance — against a hit rate high enough that every early run contributed at least one usable insight after checking. The operating rule follows, and it is not abstract: verify every factual claim at its source, and re-derive every analytical claim from the mechanism rather than borrowing a pattern. Two obligations in this very draft remain open under that rule — the “income is property” language in Section IV, which needs confirmation against the initiative’s filed text, and the vendor relationship in Section III, drawn from disclosure filings that predate the July signature drive. Neither claim reaches publication grade until its source is pulled directly. The rule binds the author exactly as it binds the machine.

Conclusion

November will deliver a verdict on the initiative, and the courts will eventually deliver one on the 1933 precedent. Neither decides Washington’s economic future. Opposition strategy in 2026 runs on an inverted allocation of effort — a crude behavioral model paired with elaborate legal machinery, both trained on the least durable variable in the system. Coalition identity forces the inversion: a repeal campaign cannot design spending without legitimizing the tax, and the sponsoring coalition profits from the drama, so both sides wage an expensive war over a statute capital has already learned to route around. The spending layer — the one place long-term wealth is kept or lost — sits open to whoever claims it first.

One symmetry captures the whole season: one side wrote a statute to overturn a constitutional precedent through litigation, and the other wrote a statute to freeze that precedent by declaration. Two proxies, one question, one court. The taxpayers all of this is supposedly about, meanwhile, have spent the 2026–27 window quietly restructuring — and by the time either side wins, the money will have finished adapting to a tax that has not yet taken effect.

Appendix: MindCast Source Citations

MCAI Economics Vision: Washington’s ‘Millionaire Tax’ — A State Level Framework for Preserving Innovation, Family, and Civic Capital — Parent framework paper; supplies the policy-path table, Capital Continuity Loop, Preservation with Leakage forecast, and public-choice analysis this commentary extends.

MCAI Innovation Vision: Cybernetic Game Theory — Control, Not Choice — Grounds the treatment of the high-conflict existence battle as a stable equilibrium both sides prefer.

MCAI Economics Vision: MindCast Dynamic Game Theory — Competing Inside a System That Rewrites Itself — Underpins the design-layer reading of the initiative’s income-tax ban as an attempt to rewrite the constraint field.

MCAI Economics Vision: MindCast Runtime Narrative Control Cybernetics — Supports treating repeal-odds and constitutional-vulnerability headlines as planning signals for the mobile margin.

Appendix: External Source Citations

Ballotpedia News, “Signatures submitted for Washington initiative to repeal legislation establishing an income tax...” — Records the May 4 Heywood v. Hobbs referendum ruling, the signature threshold, and the initiative’s income-tax-ban scope.

“Opponents file 511K signatures to repeal WA millionaire tax”, FOX 13 Seattle, July 2, 2026 — Confirms the July 2 filing date and 511,408-signature total, and records the Pacific Law Group memo reading the initiative as likely repealing the capital gains tax alongside Heywood’s rebuttal.

“New lawsuit challenges constitutionality of Washington’s ‘millionaires tax’”, KNKX Public Radio, April 9, 2026 — CADF filing details, lead plaintiffs, and the Culliton uniformity argument.

The Startup Law Blog, “What the Author of ESSB 6346 Said He Was Actually Trying to Do” — Documents the Pedersen 2018 correspondence describing the capital gains tax as the path toward a graduated income tax through litigation.

MyNorthwest, “Public records show WA’s millionaires’ tax crafted to overturn 1933 income tax ruling” — The August 2025 Pedersen email and the Roe v. Wade test-case comparison.

Washington State Standard, “Foes of WA income tax race to collect initiative signatures” — The ballot title’s “measured by” language and the statutory income definition.

Washington State Standard, “WA income tax foes file signatures to get repeal measure on ballot” — The retained sweeteners, the No on 645 committee, and Heywood’s general-fund characterization.

The Seattle Times, “Initiative 2109: Voters keep WA capital gains tax on state’s richest” — The 63–37 vote retaining the capital gains tax in 2024.

Andrew Villeneuve, “Chad Magendanz and Voter Science LLC are writing push polls instead of adhering to the scientific method, screenshots show”, NPI’s Cascadia Advocate, August 19, 2025 — Advocacy-outlet reporting on Voter Science’s survey design and the 2024 gap between its topline numbers and initiative outcomes; cited as background on vendor methods, not as evidence of conduct in the current initiative.

Washington State Public Disclosure Commission, campaign finance records — Voter Science expenditure detail for the Let’s Go Washington initiative-to-legislature track.