MCAI Economics Vision: Washington's 'Millionaire Tax' — A State Level Framework for Preserving Innovation, Family, and Civic Capital

When Capital Meets the Realization Tax

Executive Summary

See MindCast Magazine Visual Companion

Washington’s Millionaires’ Tax may survive, or it may fall. Neither outcome decides the state’s economic future. Capital adapts faster than courts, elections, and legislatures move, and a state that fights only over legality misses the larger contest: converting mobile realization events into lasting local commitment before they reroute out of reach.

State millionaire taxes have crossed from proposal into a movement. Massachusetts proved the model with a 4 percent surtax in 2023, Washington enacted a 9.9 percent levy in March 2026, Maine added a 2 percent surcharge weeks later, and California, New York, Rhode Island, and a half-dozen other states now carry live proposals. Public debate fixes on one question for each: will the tax survive litigation, the ballot, and the courts.

MindCast forecasts that survival is the wrong variable to track. Economic systems do not wait for final rulings. Founders adjust the timing and location of liquidity events, families restructure succession and residency, and legislatures respond to the revenue signals that follow. A new equilibrium forms around the statute regardless of whether the statute itself is ever struck down.

One structural fact reframes the debate. States tax realization, not wealth. A state reaches income at the moment it is recognized at a point in time, rather than reaching a stock of assets that simply sits. The binding behavioral margin is therefore not whether the wealthy leave, but when and where they realize. The median millionaire stays rooted by community, employment, and family. The marginal realizer, the founder approaching exit and the one-time recognizer, moves freely across both timing and geography.

The governing thesis follows in one line: a state-level realization tax does not primarily decide who pays; it reprices the timing and location of taxable events, and its durable yield depends on how effectively the state converts mobile realization events into local commitment through innovation, family, and civic capital channels.

Three forms of capital absorb the adaptation, and a successful jurisdiction preserves all three at once:

1. Innovation Capital. Innovation Capital, concentrated in the founder and liquidity-event margin, where realization taxation bites hardest.

2. Family Capital. Family Capital, anchored by multi-generational stickiness yet exposed at the heir and mobile-retiree margin, and increasingly governed by transfer-tax competition rather than income-tax competition.

3. Civic Capital. Civic Capital, the binding variable, because the philanthropic and community ties that make a base sticky are themselves a form of civic investment.

Where the debate misallocates attention. Litigation and the ballot dominate public discussion, yet both decide only whether the tax exists. Long-run outcomes are set by the capital-conversion channels that decide how it behaves. Public debate concentrates on the bottom half of the policy table; durable outcomes are determined by the top half.

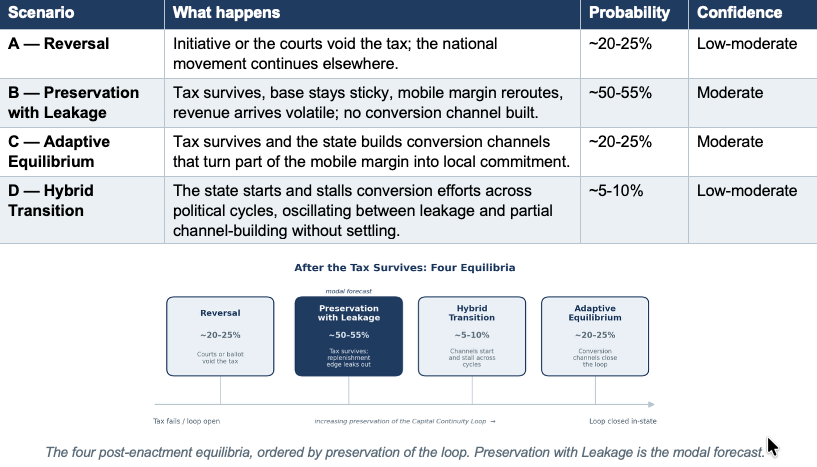

MindCast’s modal forecast for Washington, and for any state that enacts the rate without building conversion channels, is Preservation with Leakage: the tax survives, the sticky base remains, the mobile margin reroutes, and revenue arrives more volatile than projected (confidence ~50%). The more durable outcome, Adaptive Equilibrium, requires a deliberate institutional response and remains available to states that act on it (confidence the institutional leg is decisive: ~70%). Two findings run against intuition and shape everything that follows: revenue volatility shows up before any measurable out-migration, so the first signal a state sees will be misread as flight; and the first durable adaptation arrives through how the state spends the yield, not through tax relief.

Governing Structure

Taxing realization rather than wealth converts a question of legality into a control problem: the state must hold the sticky base and convert the mobile margin under a revenue stream that swings with markets. Whoever builds the conversion channel governs the outcome.

Washington serves as the worked example, not the subject. The framework is written to travel: a legislator in Sacramento, Albany, or Providence can substitute their own state and run the same analysis. Confidence bands accompany each forecast and express MindCast’s estimated probability, not certainty.

I. The Movement, Not the Statute

Washington reads as one node in a coordinated national shift, which is the first reason the analysis exports. Massachusetts voters approved the Fair Share Amendment in 2022, a 4 percent surtax on income above $1 million effective in 2023 that has since funded education and transportation. Washington followed in March 2026 with ESSB 6346, a 9.9 percent tax on income above $1 million, structured as an excise on the receipt of income so that it can survive the state’s century-old treatment of income as property. Maine layered on a 2 percent surcharge in April 2026. California advances a one-time billionaire wealth measure toward the ballot, New York debates a hike that would push the top New York City rate toward 16.8 percent, and Rhode Island, Colorado, Connecticut, Hawaii, and Michigan weigh their own versions.

Counter-evidence sharpens the picture rather than softening it. Michigan advocates suspended their 2026 campaign against organizing headwinds, a reminder that enactment is contingent and that the framework must explain failures as well as passages. Every legislature in this cohort faces the same structural choice once the rate is set, which is why a Washington-only reading would waste the lesson.

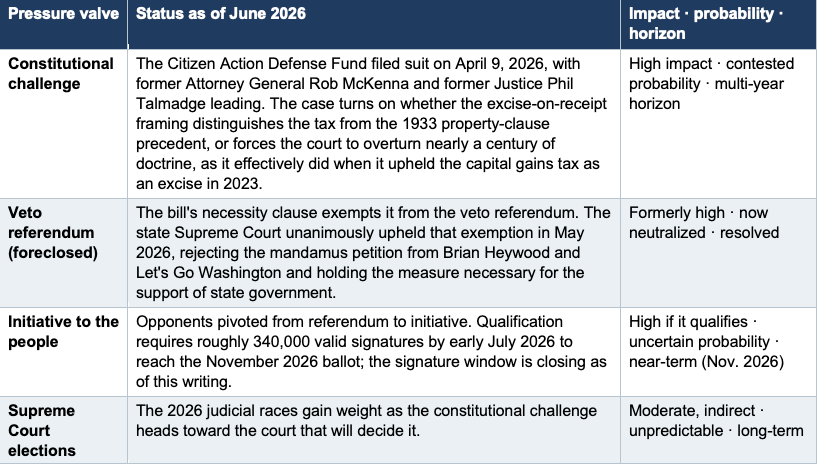

Washington’s Three Pressure Valves

Three mechanisms can still alter or end the Washington tax, and their current status matters because each operates on a different timeline and a different probability. MindCast holds the legal and political contest to roughly a fifth of the analysis, not because it is unimportant, but because none of the three decides how capital behaves around the tax. The valves below are assessed as of June 2026.

Two facts deserve emphasis. The fastest kill switch, the veto referendum, is already closed, which pushes the political fight onto the slower initiative track and the multi-year court track. Neither track answers the question a chamber, a founder, or a finance committee actually faces, which is what capital does next.

The statute is the least durable part of the tax. The rate, the exemptions, and even survival are contestable, while the movement toward realization-based taxation is the part that travels; the design choices Washington makes now set the template other states copy.

II. The Structural Reframe: States Tax Realization, Not Wealth

Flow and stock behave differently under taxation, and the distinction governs everything that follows. A wealth tax reaches a standing balance that cannot easily hide; an income tax reaches a flow the taxpayer controls in both timing and situs. State millionaire taxes are income taxes. Founders accumulate wealth through equity appreciation and recognize income only at acquisition, public offering, or sale. Taxation concentrated at the moment of recognition therefore lands on an event the taxpayer can move.

Behavioral economics predicts three responses to a repriced realization node, and observed planning already shows all three: pre-exit relocation, delayed or restructured liquidity, and entity restructuring ahead of recognition. Washington’s own statute installs escape paths directly by exempting the sale of real property and the sale of qualified family-owned small businesses, and by offering an elective pass-through entity tax. A legislature that writes exemptions writes geodesics, the lowest-cost paths through its own constraint field. Washington’s defeat of a separate bill to tax qualified small-business-stock gains left another such path open by design.

The Massachusetts Paradox, Resolved

Massachusetts supplies the proof case both sides cite, and both are correct because they measure different margins. Advocates note that the number of millionaires grew after enactment and that the surtax collected roughly $6 billion, evidence that the base is sticky. Critics note that IRS migration data showed a net adjusted-gross-income outflow near $4.2 billion in the first full year, with fewer movers carrying more income per move, evidence that the high end is mobile. Stanford data resolves the apparent conflict: only 2.4 percent of million-dollar-income households migrated, below the 2.9 percent general-population rate.

The synthesis is the exportable insight. A realization tax works on the sticky base and leaks at the mobile margin, and the net yield depends on the ratio between them. The median millionaire is anchored by community, job, and family; the marginal one-time realizer is not. Any state can run the same decomposition on its own base before it scores the revenue.

Massachusetts therefore informs the mechanism without predicting Washington by extrapolation. Enacting a tax is itself the break condition MindCast specifies, the point at which constraint stability falls below actor adaptation speed, and beyond that threshold pattern extrapolation inverts from signal to noise. Projecting one state’s collected revenue or migration figures linearly onto another mistakes recent data for structural signal. The forecasts in this document model the generating mechanism, which actors adapt, under which constraints, through which feedback loops, rather than extending a historical curve (see Appendix B).

A realization tax reprices events, it does not seize stocks. Because the taxable moment is also the mobile one, the durable question is never how much wealth sits in the state but how much of it chooses to realize there.

III. Innovation Capital

Innovation capital sits at the most mobile margin, which makes it the first test of any realization tax. Startup formation, venture investment, and the liquidity events that reward them concentrate founder wealth at discrete, plannable moments. Washington anchors a primary node of global compute and AI investment through Microsoft, Amazon, and the surrounding ecosystem, so the timing of founder liquidity carries outsized weight and stands in for every technology hub considering the same tax.

Founders who establish residency in a no-income-tax state before an exit convert relocation into the geodesic path rather than absorbing the levy, while their companies and jobs frequently remain behind. Productive capacity stays geographically concentrated even as entrepreneurial wealth distributes geographically, an equilibrium already visible in other high-cost hubs (confidence this pattern recurs in Washington: ~75%). Policymakers who want to retain the margin rather than merely tax the base can reach for several conversion mechanisms:

• Founder reinvestment incentives. rewarding capital redeployed into in-state businesses, research, and emerging industries instead of taxing the liquidity event in isolation.

• In-state investment programs. a qualified small-business-stock analog that ties favorable treatment to in-state firms, encouraging local capital retention while preserving revenue.

• Research and development expansion. enhanced credits for AI, aerospace, biotechnology, advanced manufacturing, and clean energy that strengthen position against lower-tax states.

• Strategic-industry incentives. deliberate support for sectors that generate disproportionate employment and investment, consistent with how governments have long protected strategically important industries.

Founders are taxed at the one moment they are most mobile. The liquidity event is precisely when proceeds can leave, so the policy that matters is whatever converts that exit into local reinvestment before the capital relocates.

Contact mcai@mindcast-ai.com to partner with us on Predictive Game Theory AI in Law and Behavioral Economics. To deep dive on MindCast works upload the URL of this publication into any LLM (preferably Google AI mode/Gemini, Claude, ChatGPT) and prompt ‘reconstruct MindCast framework with three degrees of cited sub links.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure.

MindCast AI is a cybernetic, predictive game-theory AI firm specializing in law and behavioral economics, applied to complex litigation, innovation systems, and geopolitical risk intelligence. Rather than extrapolating historical patterns, the firm models the mechanisms that generate institutional behavior, running Cognitive Digital Twin simulations grounded in Nash equilibrium, Stigler information economics, and the Chicago School of law and behavioral economics.

MindCast stress-tests its predictive system against live, falsifiable public events. Its sports simulations include a correct projection of the Seattle Seahawks’ Super Bowl LX victory in February 2026 and the 2026 FIFA World Cup. The vision statement that follows applies the same system to Washington’s Millionaires’ Tax.

IV. Family Capital

Family decision-making revolves around continuity rather than annual return, a fact public debate routinely misses. Families build wealth to create stability and opportunity across generations, and that horizon shapes residency, education, retirement, trust structures, philanthropy, and business succession. The levers a state actually controls here are familiar tax instruments: residency and sourcing rules, trust and pass-through treatment, the interaction with the estate tax, and exemptions for family businesses and primary residences. How a state sets them determines whether families plan to stay or plan to leave, because multi-generational rootedness is precisely what keeps the base sticky.

Exposure concentrates at two points. The heir and the mobile retiree recognize income as portfolio realization untethered from a job or a community, which makes them mobile in the same way founders are. Retention-minded policy can recognize the long horizon directly:

• Long-term residency and wealth preservation. structures that reward decades-long commitment to a state reduce the incentive to relocate ahead of a transfer or a sale.

• Family-business continuity. succession-friendly treatment of family-owned businesses preserves local employment and community stability, which Washington’s qualified-family-business exemption begins to do.

• Human-capital incentives. incentives tied to education and workforce investment compound human capital that stays in place far longer than financial capital.

Millionaire Taxes Compete With Estate Taxes, Not Income Taxes

Wealthy households at the family-capital stage rarely optimize annual income. They optimize trusts, heirs, succession, charitable vehicles, and family governance, all of which are transfer-tax questions. A state-level millionaire income tax therefore competes for the same planning attention as the estate tax, and the binding interstate competition increasingly runs not between high-income-tax and low-income-tax states but between wealth-transfer states and wealth-preservation states (confidence this reframing strengthens over the decade: ~60%).

Washington dramatizes the tension inside a single jurisdiction. The state raised its estate tax to a nation-leading 35 percent top rate in 2025, then reversed the increase back to 20 percent in 2026 through SB 6347, with the governor explaining that the change keeps Washington from being a significant outlier. The state retreated on transfer-tax competition to slow estate flight even as it advanced the realization tax on income. Two structural features deepen the exposure: Washington allows no portability of the estate-tax exemption between spouses, unlike the federal system, and Washington imposes no gift tax, which leaves lifetime gifting open as a preservation channel.

The destinations are well established. No-estate-tax, no-income-tax states such as Florida, Texas, Nevada, Wyoming, Alaska, and South Dakota function as wealth-preservation jurisdictions, and a family deciding where to be domiciled at death weighs the transfer-tax differential more heavily than any single year’s income tax. A state that wants to keep its multi-generational families must therefore manage income and transfer taxes jointly, because it can win the income-tax argument and still lose the family on the estate side.

What Actually Transmits: Architecture Over Estate

The deeper version of the transfer-tax point dissolves a common assumption: what carries advantage across generations is inherited reasoning, not inherited capital. MindCast’s recognition-architecture model holds that the durable transmitted unit is a recursive pattern-recognition grammar, the installed reflex for reading an institutional field before it resolves, and that capital only amplifies execution once a successor reads the field correctly. The estate is downstream; the grammar is the variable. Migration families show it plainly: when a household loses its savings, property, and credentials in a single border crossing, the advantage that reappears a generation later cannot be transmitted capital, because none survived (confidence this mechanism generalizes: ~65%).

The policy implication is concrete. A retention strategy aimed only at the after-tax estate targets the amplifier, not the mechanism; strong schools, durable institutions, and civic environments that reward accurate reading of the field do more to keep multi-generational families than estate-rate management alone. Family Capital and Civic Capital converge at exactly this point, which the Legacy Innovation corpus formalizes (Appendix B).

Families optimize continuity, not the current year. They weigh transfer taxes and the conditions for transmission over decades, so retention turns on the institutions that anchor a family far more than on any single year’s income-tax rate.

V. Civic Capital

Civic capital is not a third co-equal pillar; it is the binding variable, and naming it as such is the analysis’s sharpest move (confidence this reframing holds: ~70%). Stickiness and civic investment are the same phenomenon viewed from two angles. People stay where they have built schools, hospitals, universities, and institutions, and they invest in those institutions because they intend to stay. A deep philanthropic and community infrastructure is therefore the mechanism that makes the sticky base dominate the mobile margin.

Philanthropic activity rises as families shift from accumulation toward legacy, which gives a state a window to anchor capital exactly when it would otherwise become most mobile. Washington’s mature philanthropic ecosystem is an underpriced asset in the millionaire-tax debate. The vehicles are concrete, not abstract: university endowments, hospital systems, community foundations, donor-advised funds, and place-based community investment funds each convert private wealth into rooted local capacity. Policy can widen the channel:

• Philanthropic capital formation. matching incentives that route legacy-stage giving into university endowments and hospital systems keep large gifts in state at the moment wealth turns mobile.

• Community investment partnerships. community foundations and place-based investment funds let public-private structures leverage private capital toward local objectives without eroding competitiveness.

• Legacy capital development. recognition for donor-advised funds and endowed legacy vehicles deepens the civic ties that keep both capital and talent rooted across generations.

Civic institutions convert mobile wealth into rooted wealth. Endowments, hospitals, universities, and foundations are the channel through which a liquidity event becomes a permanent local commitment, which makes them retention infrastructure rather than charity.

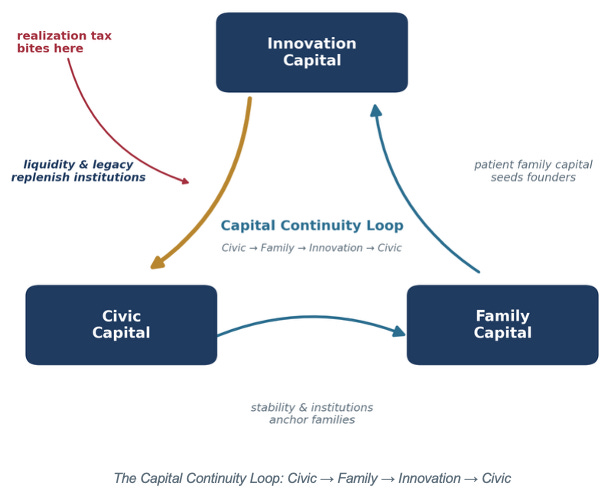

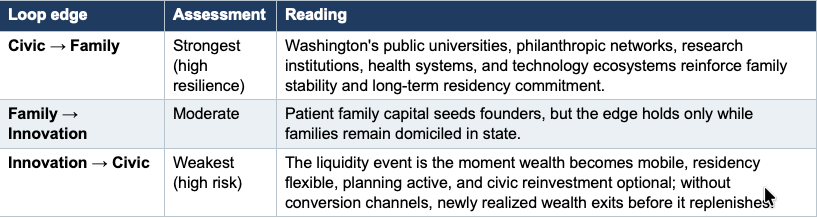

VI. The Capital Continuity Loop

The three forms of capital are not a list. They are a closed loop, and seeing the loop is what turns a taxonomy into a framework. Civic capital transmits advantage across generations through institutions and stability, sustaining family capital. Family capital supplies the patient, risk-tolerant capital that seeds founders, producing innovation capital. Innovation capital, at the liquidity and legacy stage, replenishes the endowments, hospitals, and foundations that constitute civic capital. Each form feeds the next, and the cycle closes.

Why the loop matters for a realization tax: the tax bites precisely at the innovation-to-civic edge, the liquidity event at which new wealth would otherwise convert into legacy and civic investment. Taxed without a conversion channel, that edge does not simply yield revenue; it can reroute the replenishing flow out of state, starving the civic capital that sustains the next turn of the loop. A state that taxes the realization node and builds no channel collects once and weakens the cycle that generates future realizations to tax.

The conversion mechanisms in the preceding sections are, in this light, loop-repair tools. Founder reinvestment incentives keep the family-to-innovation and innovation-to-civic edges in state; family-capital incentives protect the civic-to-family edge against transfer-tax competition; civic-capital incentives strengthen the replenishment edge directly. One repair tool sits outside the tax code entirely: how the state spends the yield. Revenue routed visibly into infrastructure, research hubs, and public universities rebuilds civic capital directly, repairing the replenishment edge without a single bespoke credit (Section IX). A jurisdiction reaches Adaptive Equilibrium when the loop stays closed inside its borders; it settles into Preservation with Leakage when one edge, almost always the replenishment edge, leaks across the state line (confidence the loop framing predicts retention better than any single-pillar view: ~65%).

Wealth creation is not the risk; replenishment is. A state that taxes the realization node without rebuilding the innovation-to-civic edge collects once and weakens the loop that generates the next realization to tax (confidence the loop framing outpredicts single-pillar views: ~65%).

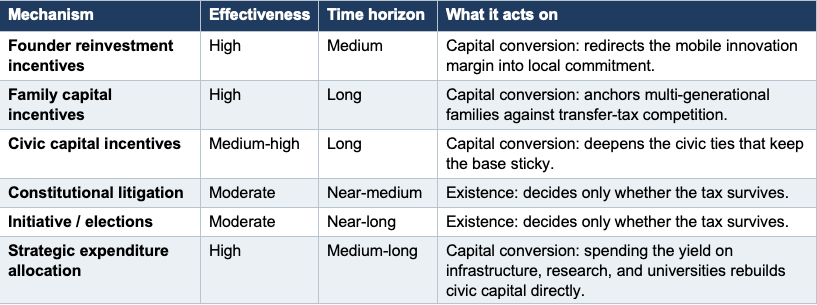

VII. The Five Policy Paths After Enactment

Five paths remain available once a realization tax is law, and ranking them by expected effectiveness exposes where the public conversation goes wrong. Two paths decide only whether the tax exists. Three decide how capital behaves around it, and those three carry the durable leverage.

The core argument: public debate concentrates on the bottom half of this table, while long-term outcomes are likely determined by the top half. A state that wins in court and at the ballot but builds no conversion channel still settles into Preservation with Leakage. A state that loses the rate but has built reinvestment, family, and civic channels keeps the capital those channels anchor. Effort follows headlines toward the existence question; leverage sits in the conversion question.

Most of the paths decide design; only one decides existence. The design choices, above all how the yield is spent, do more to set the long-run take than the up-or-down fight over whether the tax survives.

VIII. MindCast AI Proprietary Cognitive Digital Twin Foresight Simulation

MindCast models the tax as a constraint field and the affected population as a set of actor classes, then runs each class to behavioral convergence. Raising the rate increases constraint density at the realization node, and actors reroute toward the lowest-cost available path. The simulation tracks which paths the statute leaves open and which it closes.

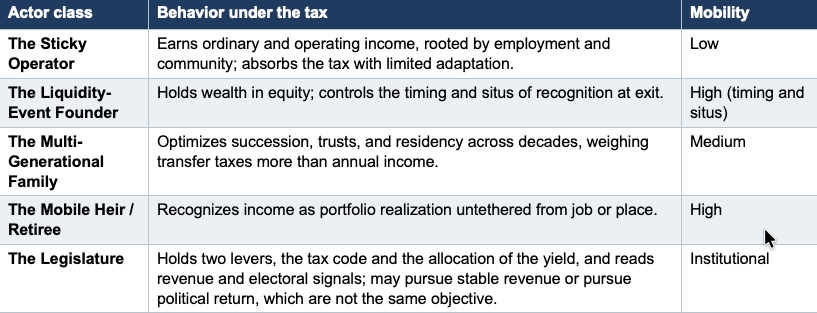

Actor Classes

Constraint Geometry and Dual-Equilibrium Closure

Field-geometry reasoning locates the binding pressure at the recognition event, not at residency in general. Pre-cut geodesics already run through the field: Washington’s exemptions for real-property and qualified-family-business sales, the pass-through entity election, untaxed qualified small-business stock, and residency change in advance of a one-time realization. Predictive closure under MindCast’s Dual-Equilibrium Termination Architecture requires two conditions together. Nash behavioral convergence arrives when actors settle into a dominant adaptation, which the simulation resolves to retiming and restructuring rather than mass flight. Stigler institutional sufficiency arrives only when the legislature builds the conversion channels. Behavioral convergence without the institutional leg yields Preservation with Leakage, not equilibrium. The architecture is not bespoke to this paper: it applies MindCast’s published Dual Nash–Stigler measurement standard, in which Nash decides where the system settles and Stigler decides when analysis stops, and its Field-Geometry Reasoning treatment of structural constraint (see Appendix B).

Simulation Outputs

A multi-layer foresight run stress-tests the loop, the governance system, and the long-horizon balance among the three capitals. The headline is reassuring and sharp at once: the run surfaces no evidence of imminent large-scale millionaire flight, and strong evidence that realization events, succession, and institutional response speed will decide the long-run outcome. The risk is not a sudden loss of the tax base; it is the slow weakening of the innovation-to-civic replenishment channel until the state’s future capacity to create wealth declines faster than policymakers notice.

Output 1: Loop Stress Test

Stress-testing each edge of the Capital Continuity Loop locates the strongest and weakest links.

The replenishment edge is the system’s primary vulnerability, and the tax falls precisely on it. Failing to build conversion channels weakens future civic capacity and, in time, reduces future innovation generation.

Output 2: Institutional Adaptation and Governance Debt

Government response speed trails capital adaptation speed by an estimated three to five years. Adaptation runs ahead in a fixed sequence: enactment, behavioral adaptation, revenue volatility, measurable leakage, political recognition, and only then legislative response. The state’s current posture reads as managed strain; left unaddressed, the lag compounds into governance debt, the widening gap between behavior the legislature already recognizes and the political alignment required to act on it. The binding constraint is response velocity, not detection.

The sequence carries a trap worth stating plainly. Revenue volatility arrives before any measurable out-migration, because taxpayers restructure timing, entities, and recognition almost immediately while physical relocation unfolds over years. The first signal a state actually sees is therefore a wobble in receipts, not a moving van, and the political reflex is to read that wobble as flight. Acting on the misread, by softening the tax or declaring failure, would mistake ordinary behavioral adjustment for base loss, and would do so before the federal and market conditions that also move realizations have been netted out (Section IX).

Output 3: Equilibrium Reassessment

Incorporating the public-choice and governance-lag findings shifts the scenario weights. The reassessed distribution lifts Preservation with Leakage and trims Reversal, and adds a Hybrid Transition state for jurisdictions that start and stall conversion efforts across political cycles without settling.

Output 4: Family Capital Dominance Over the Long Horizon

Across a fifteen-to-twenty-five-year horizon, family-capital dynamics outweigh innovation-capital dynamics. Innovation events create wealth; family systems decide where wealth ultimately resides, through domicile, succession, philanthropy, education, and multi-generational residency. Discussions that fixate on founders underweight heirs, whose accumulated domicile decisions exert more influence over the long run than any single liquidity event.

Output 5: Expenditure Precedes Tax Relief

Likely policy responses order themselves predictably: strategic expenditure programs, research investment, and economic-development funding arrive before founder or family tax incentives. Political optics favor “we invested the revenue in growth” over “we cut taxes for high-income households,” which makes expenditure allocation the underappreciated first-mover conversion mechanism (Section IX).

The actionable consequence reframes the advocacy fight. Because spending is the politically realistic first lever, the contest that decides retention is not whether the rate is cut but where the yield goes. A chamber, a university, or an economic-development body that wants to keep capital in state gains more by shaping the expenditure toward research hubs, infrastructure, and workforce pipelines, the public goods that rebuild the replenishment edge, than by pursuing a repeal that the necessity clause and the cohort trend both make unlikely.

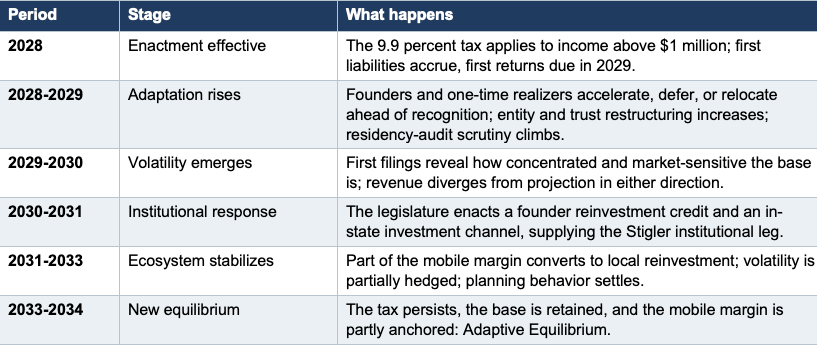

What Adaptive Equilibrium Actually Looks Like

Adaptive Equilibrium has stayed abstract in the debate, so the following sequence makes it concrete, anchored to Washington’s 2028 effective date. The lag between the revenue-volatility signal and the legislative response is not incidental; it reflects the feedback latency MindCast models in policy systems, where harm and signal arrive delayed, dispersed, and fragmented across venues, so institutions correct slowly (Appendix B). The timeline is illustrative, and the contingent step is the institutional response in years three and four; absent it, the sequence halts at revenue volatility and the state settles into Preservation with Leakage (confidence the institutional step is the hinge: ~70%).

The model converges on one warning. Capital adapts faster than the state can respond, so the modal outcome is Preservation with Leakage unless a deliberate institutional step closes the loop in years three and four (confidence the institutional step is the hinge: ~70%).

IX. Macro Boundary Conditions: Where the Micro-Model Ends

The constraint-geometry model above resolves behavior at the level of actors and realization events. Four macro forces sit outside that resolution, and naming them protects the framework against misuse before chambers, legislatures, and institutional advisors. Each is a boundary condition the micro-model holds constant; each can dominate the micro-mechanics in a given year.

The expenditure side: spending as a conversion channel

Tax analysis treats the legislature as a collector and an incentive-setter, and stops there. The sticky base, however, prices the use of the yield, not only its size. A state that routes revenue visibly into world-class infrastructure, targeted research hubs, and top-tier public universities is building civic capital directly, which repairs the loop’s replenishment edge without bespoke credits or exemptions. Expenditure quality is therefore a conversion lever in its own right, and a poorly spent yield leaks retention even when the rate and the credits are well designed. Treating spending as a black box understates the legislature’s most powerful tool (confidence expenditure quality materially affects retention: ~65%).

Cohort convergence and the network-effects moat

The exportability thesis cuts both ways. When most high-productivity states adopt comparable realization surtaxes, as Massachusetts, Washington, and the live California and New York proposals suggest, the relative tax differential between innovation hubs flattens. The binding retention variable then shifts from the tax differential to network-effect density: a founder weighing departure from a compute-and-talent ecosystem like Seattle finds the low-tax alternatives in Florida or Texas lack the network effects that make the hub productive in the first place. A convergent cohort behaves like an oligopoly over innovation ecosystems, and oligopoly reduces the near-term pressure to build conversion channels, because the founder’s outside option is weaker than the headline rate implies. The relief is conditional: it holds only while the cohort holds and while the network moat holds, and it erodes if either fragments (confidence the moat dampens flight under cohort convergence: ~65%).

The federal and monetary interface

Realization events are bound to federal conditions the state does not control: the federal long-term capital-gains rate, the interest-rate environment set by the Federal Reserve, and the liquidity cycle that governs whether the IPO and acquisition windows are open. A founder’s decision to exit in 2028 responds to all three at once, not to Washington’s 9.9 percent in isolation. The analytic hazard is attribution. A frozen IPO market or a high-rate environment can depress realizations statewide, and a naive reading will charge that decline to local leakage or planning adaptation when the cause is macro weather. The model’s leakage estimates are valid only after federal and market conditions are netted out, which is itself the identification problem the Prediction Table flags.

The public-choice legislature

The Dual-Equilibrium architecture treats Stigler institutional sufficiency as a condition the legislature can satisfy by building conversion channels. Public-choice theory complicates the assumption. A legislator’s payoff often runs on electoral return rather than on a quietly stabilized tax base, and the narrative of fighting capital flight can be worth more politically than the closed loop is worth fiscally. Under those incentives, Preservation with Leakage is not a failure to act; it is a stable political equilibrium that a rational legislator may prefer and sustain. The implication tilts the scenario weights: the institutional leg of Adaptive Equilibrium is harder to reach than the micro-model alone suggests, and the modal outcome leans further toward Leakage wherever the political return on conflict exceeds the fiscal return on stability (confidence public-choice incentives raise the probability of durable Leakage: ~60%). MindCast’s enforcement-capture metrics, which track whether institutional behavior survives leadership turnover, supply the instrumentation for this leg (Appendix B).

The micro-model can be right and still be overwhelmed. Expenditure quality, cohort convergence, federal cycles, and political incentives each can dominate the actor-level mechanics in a given year, which is why the forecast names them rather than quietly absorbing them.

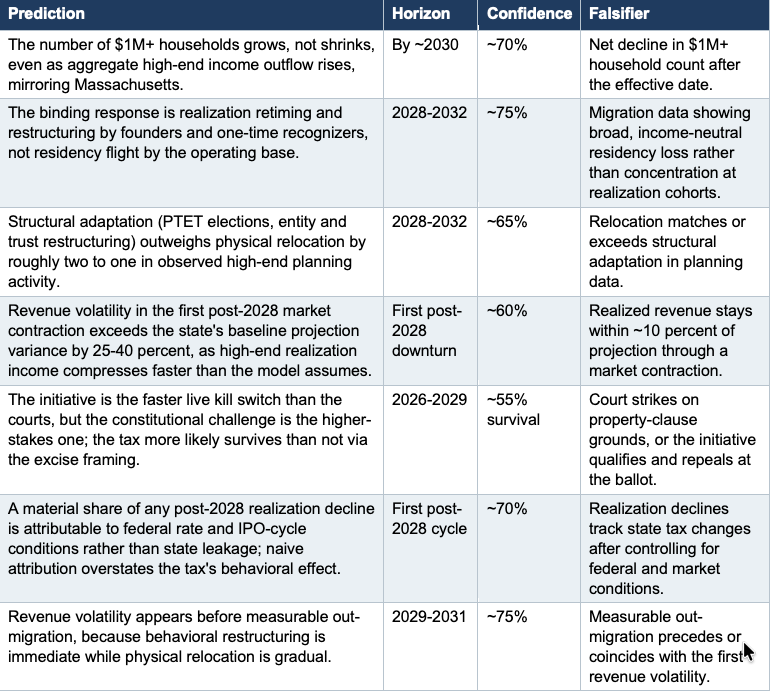

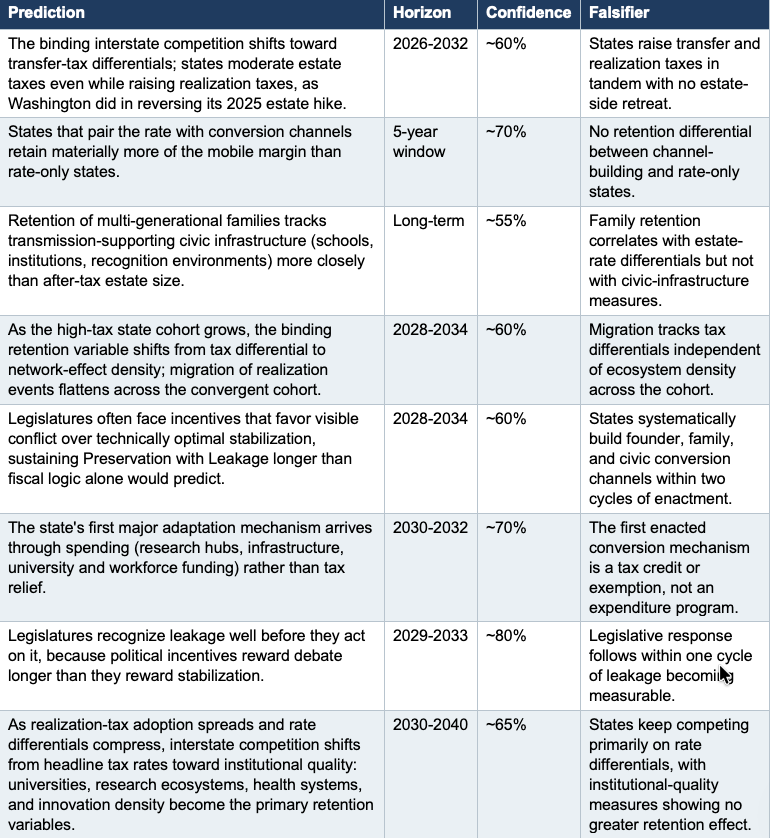

X. MindCast Prediction Table

Each prediction below is falsifiable, carries a horizon and a confidence band, and names the observation that would refute it, applying the falsification-contract standard MindCast set out in its federal Nash–Stigler comment (Appendix B). Predictions are stated for the general case and illustrated with Washington.

First-Order Predictions — Volatility, Migration, Litigation

Direct, near-term consequences that register in revenue, residency, and the courts within the first cycles after enactment.

Second-Order Predictions — Institutional Quality, Estate-Tax Competition, Civic Capital

Structural, longer-horizon dynamics that decide retention after the first-order effects register, driven by institutions rather than by the rate.

Each claim is built to be proven wrong. The value of the table lies less in the probabilities than in the falsifiers, which let a reader hold the framework accountable as Washington’s data arrives.

XI. The Capital Adaptation Index

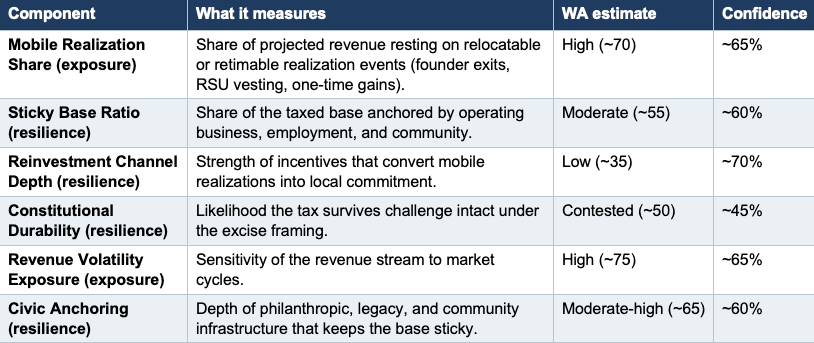

MindCast proposes a State Capital Adaptation Index (SCAI) to score how well a jurisdiction will hold capital under a realization tax, instantiated here as the Washington Capital Adaptation Index (WCAI). Six components each score from 0 to 100. Three measure resilience directly and three measure exposure, which the composite inverts. Scores below are MindCast estimates for illustration, not measured values, and the methodology appears in Appendix A so the numbers can be inspected rather than taken on faith.

Composite WCAI: roughly 48-55, “Adaptive-Contingent.” Washington holds a strong civic-anchoring and operating base against high realization-margin and volatility exposure, with a thin reinvestment channel and contested constitutional footing. The composite lands near the midpoint because the outcome turns on one buildable component: deepen Reinvestment Channel Depth and the score moves toward Adaptive Equilibrium; leave it thin and the state settles into Preservation with Leakage (confidence this single lever is decisive: ~70%).

Washington scores adaptive-contingent, not adaptive. The ingredients for retention are present, but the index turns on conversion channels the state has not yet built, so the rating is a forecast conditioned on action rather than a verdict.

XII. What Each Audience Should Weigh

The migration from a legality contest to a capital-adaptation problem reaches every actor in the field, and each faces a different decision. The following is foresight, not advice; each reader should model their own posture against their own exposure.

Chambers of commerce

Opposition alone leaves the outcome to the courts and the ballot and concedes the conversion question. The higher-leverage move is to model members’ mobile-margin exposure and to advocate for conversion channels, so that capital adapting around the tax adapts toward the local economy rather than away from it.

Businesses assessing the tax

Operating income and one-time realization sit in different risk classes and demand different responses. For most operating businesses the pass-through entity election and entity structure matter far more than relocation, because the sticky base rarely gains from a move that disrupts the enterprise itself.

Founders approaching exit

Realization timing and residency relative to the liquidity event are the binding variables, not residency in the abstract. Planning windows open well before an exit, the qualified-small-business and real-property exemptions reward structure over flight, untaxed qualified small-business stock remains a live channel, and rising residency-audit scrutiny raises the cost of a poorly documented move (confidence audit scrutiny intensifies as effective dates approach: ~75%).

Wealthy families, family offices, and advisors

Multi-generational rootedness is an asset to protect rather than a constraint to escape. Income and transfer taxes optimize jointly, the interaction with Washington’s estate regime and its no-portability, no-gift-tax structure rewards integrated planning, and the wealth-transfer-versus-preservation contest, not the annual income tax, is the variable most likely to move a family’s domicile. Family offices at institutional scale carry a distinct exposure: operating with institutional impact but without institutional accountability, they accumulate correction lag, errors compound quietly until they surface at succession, the moment that tests coordination architecture most severely. The retention question for these families is less the estate rate than whether the conditions that transmit advantage across generations remain intact.

Foundations and universities

Civic institutions are active retention infrastructure, not passive beneficiaries of the tax debate. Pathways that channel legacy-stage wealth toward local endowments, research, and community investment convert the most mobile capital at the moment it turns mobile, which serves both the institution and the state’s retention goal. Universities, hospitals, and foundations that frame themselves as the replenishment edge of the loop, rather than as grantees, position themselves at the center of the policy conversation.

State legislatures

The modal outcome of enacting the rate alone is Preservation with Leakage, and durability requires the institutional leg. Budgeting against volatile high-end realization income, designing exemptions as deliberate geodesics rather than accidental ones, managing transfer and income taxes jointly, and building conversion channels are the levers that separate Adaptive Equilibrium from leakage.

Every audience faces the same question from a different seat: whether, and how, to convert mobile realization events into local commitment, which is why the loop, not the litigation, is the thread common to all of them.

XIII. Conclusion

Washington’s Millionaires’ Tax will generate years of legal and political contest, and the initiative, the courts, and the judicial elections will shape the headline. Durable prosperity rarely follows from a legal victory alone. Jurisdictions that hold capital are the ones where people keep building companies, raising families, supporting institutions, and committing to place.

The foresight run finds no sign of imminent large-scale flight, which makes the real risk easy to miss. The danger is not losing the tax base overnight; it is letting the innovation-to-civic replenishment edge weaken gradually until the state’s capacity to create new wealth declines faster than policymakers recognize. Slow erosion rarely triggers a political response until the governance debt has already accumulated.

The decisive question is therefore not whether any single tax survives. The decisive question is how innovation capital, family capital, and civic capital evolve around it, and whether the state builds the channel that converts a mobile margin into local commitment before it reroutes. States that ask the realization question early, manage transfer and income taxes together, and answer institutionally will export the lesson Washington is now teaching in real time.

Appendix A: WCAI Methodology

The index exists to discipline judgment, not to manufacture precision. The mechanics below let a reader reconstruct any score and substitute their own state.

Step 1 — Score six components from 0 to 100

Three components measure resilience (Sticky Base Ratio, Reinvestment Channel Depth, Constitutional Durability, Civic Anchoring) and two measure exposure (Mobile Realization Share, Revenue Volatility Exposure). Each component is scored on observable proxies: realization-heavy share of high-end AGI, operating-versus-portfolio income mix, presence and size of reinvestment credits, litigation posture and precedent, capital-gains share of the base, and philanthropic-asset density.

Step 2 — Invert the exposure components

Exposure scores enter the composite as their complement, so that a high Mobile Realization Share or high Revenue Volatility Exposure reduces resilience. An exposure score of 70 contributes 30 to the composite, computed as 100 minus the exposure value.

Step 3 — Weight and combine

MindCast applies a base weighting that reflects how decisive each component is to retention: Reinvestment Channel Depth and Sticky Base Ratio carry the heaviest weight because they most directly govern whether the mobile margin converts; Mobile Realization Share and Revenue Volatility Exposure follow; Constitutional Durability and Civic Anchoring round out the set. A reader who disputes a weight can reset it and recompute, which is the point of publishing the mechanics.

Applying the weights to Washington’s illustrative component scores, with exposure components inverted, yields a composite in the high-40s to mid-50s, the Adaptive-Contingent band. The single largest lever on the result is Reinvestment Channel Depth, which is also the component a legislature can most readily change, which is why the index treats it as the decision variable rather than a descriptor.

Appendix B: Methodological Foundations

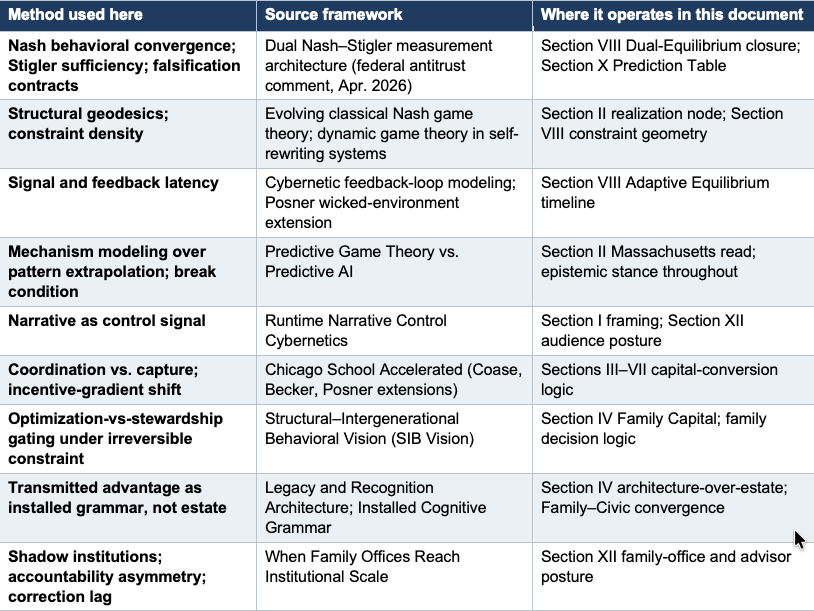

The machinery in this document is not assembled for the occasion. The wealth-migration analysis applies a standing MindCast methodology developed across a published corpus on cybernetics, game theory, and Chicago School behavioral economics. Three load-bearing methods do the work, and each traces to a specific source.

Nash behavioral convergence and Stigler sufficiency

The Dual-Equilibrium framing in Section VIII applies MindCast’s Dual Nash–Stigler measurement architecture, formalized in its April 2026 federal antitrust comment. Nash equilibrium serves as the behavioral termination condition: the system settles where no actor improves by unilateral deviation, which the scenario model resolves to retiming and restructuring rather than mass flight. Stigler equilibrium serves as the inquiry sufficiency condition: analysis stops when added evidence yields less verified signal than it costs, which here marks the point at which the institutional response is the only remaining variable. Both must fire before a prediction is committed, and each prediction carries an explicit falsification contract, the same standard that governs the Prediction Table.

Structural geodesics and Field-Geometry Reasoning

The constraint-geometry analysis treats the realization event as the binding pressure point and the statute’s exemptions as pre-cut geodesics, the lowest-cost paths through the field. The treatment draws on MindCast’s work evolving classical Nash game theory with real-world parameters, which introduces cross-forum interaction, signal latency, and structural constraint geometry as first-class variables rather than abstractions, and on the dynamic game-theory work on competing inside a system that rewrites its own constraints over time.

Feedback latency and narrative as control signal

The lagged legislative response in the Adaptive Equilibrium timeline reflects the feedback-latency problem MindCast adapts from Posner: institutional self-correction stalls in environments where harm and signal arrive delayed, dispersed, and fragmented across venues. The companion cybernetic work models public and market narratives, such as the recurring “millionaire flight” and “fair share” frames, as runtime control signals inside institutional systems rather than as background noise, which is why narrative framing appears in this analysis as a steering variable.

Family-capital and legacy foundations

The Family Capital pillar rests on MindCast’s Legacy Innovation corpus. Structural–Intergenerational Behavioral Vision supplies the gating logic that determines when families exit optimization and enter stewardship under irreversible constraint and long horizons, which is the behavior the estate-versus-income reframe depends on. The recognition-architecture model specifies what actually transmits across generations, recursive pattern-recognition grammar rather than the estate, and converts the unexplained complementarity in Becker’s intergenerational-mobility theory into a named mechanism. The family-office analysis adds the coordination-economics frame for private capital at institutional scale, where accountability asymmetry produces correction lag that surfaces at succession.

Lineage map

Appendix C: MindCast Source Citations

Every MindCast publication cited in this document appears below with its full title linked and a one-line note on its role in the analysis.

MCAI Cybernetics & Game Theory: Strategic Logic Hub — Provides the cybernetics-and-game-theory foundation beneath the paper’s constraint-geometry and equilibrium analysis.

MCAI Innovation Vision: Cybernetic Game Theory — Control, Not Choice — Supplies the control-not-choice account of how institutions stabilize around suboptimal equilibria such as Preservation with Leakage.

MCAI Innovation Vision: How MindCast Evolves the Structural Gaps in Classical Nash Game Theory — Grounds the treatment of realization events as geodesics through a constraint field and the rerouting of capital when low-cost paths close.

MCAI Economics Vision: MindCast AI Economics Frameworks — Anchors the Chicago-School behavioral-economics basis the paper applies to taxpayer and legislative behavior.

MCAI Economics Vision: MindCast Dynamic Game Theory — Competing Inside a System That Rewrites Itself — Underpins the claim that enacting a tax changes the game itself, so static optimization misreads behavior.

MCAI Economics Vision: MindCast Runtime Narrative Control Cybernetics — Supports treating the millionaire-flight and fair-share framings as runtime control signals rather than background noise.

MCAI Economics Vision: Chicago School Accelerated — Coase, Becker, and Posner as a Single Analytical System — Supplies the Coase-Becker-Posner engine behind the conversion logic and the feedback-latency account of slow legislative response.

MCAI Legacy-Cultural Innovation Vision: Structural Intergenerational Behavioral Economics (SIB Vision) — Grounds the Family Capital claim that families optimize continuity rather than annual income under long horizons and irreversible constraint.

MCAI Legacy Innovation Vision: Legacy and Recognition Architecture — Supplies the architecture-over-estate insight and the convergence of Family and Civic Capital.

MCAI Legacy Innovation Vision: When Family Offices Reach Institutional Scale — Informs the family-office and advisor guidance and the long-horizon dominance of Family Capital.

MCAI Market Vision: MindCast Predictive Game Theory vs. Predictive AI — Structural Foresight in Institutional Systems — Justifies forecasting Washington from the generating mechanism rather than extrapolating Massachusetts’ figures.

MindCast AI LLC — Public Comment, DOJ/FTC Docket ATR-2026-0001: A Nash–Stigler Measurement Architecture for Dynamic Coordination Analysis — Provides the Dual Nash–Stigler measurement architecture and falsification-contract standard behind the simulation’s closure logic and the Prediction Table.