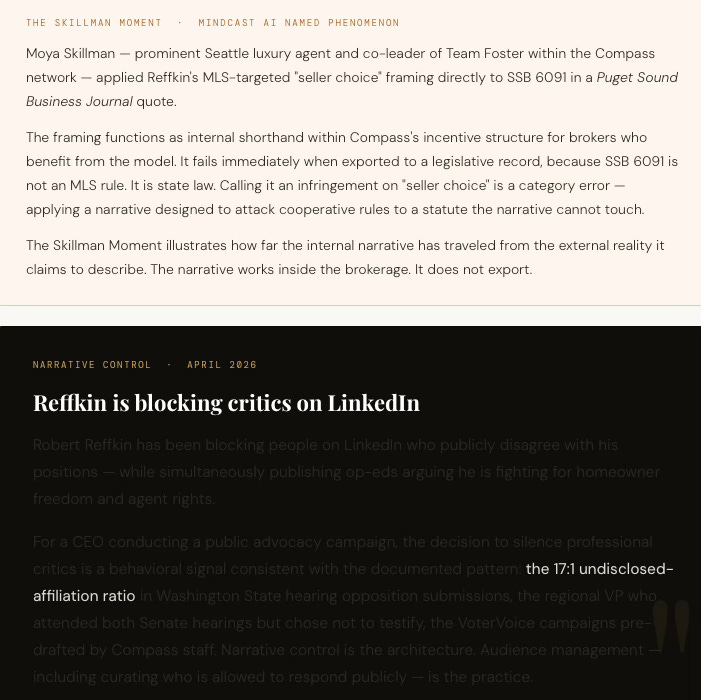

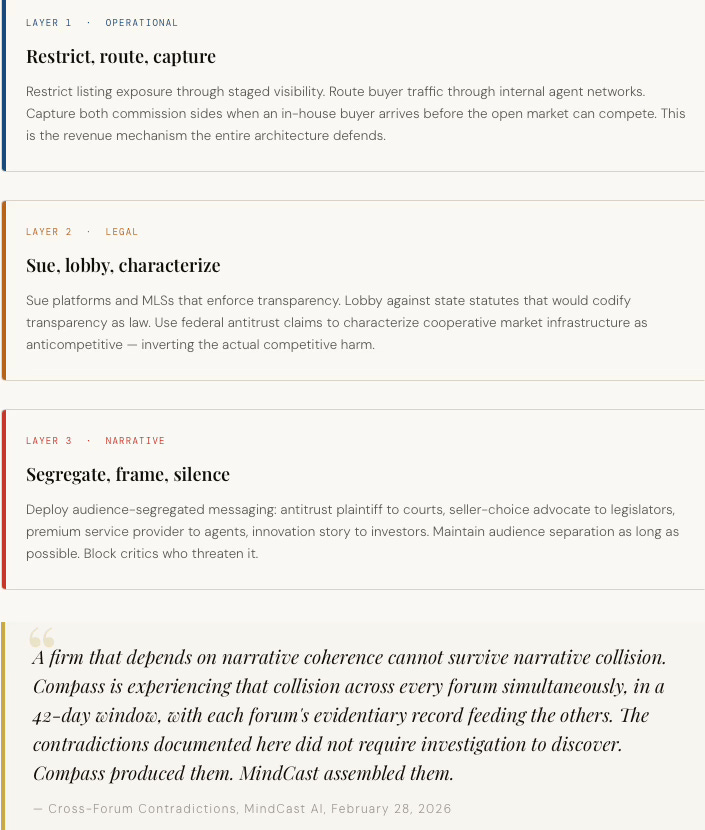

MCAI Market Vision Visual Synthesis: The Compass Narrative War Against MLSs

How America's Largest Brokerage Is Fighting the Infrastructure That Makes Home Sales Transparent — And Losing on Every Front

Visual synthesis of The Compass Commission Consolidation Strategy | The Compass Narrative Inversion Playbook | Compass’s Cross-Forum Contradictions | Compass’s Consumer Choice Framing as a Control Mechanism | The Cybernetics of Compass Holdings’ Narrative Control Architecture | Compass Holdings, Robert Reffkin’s Doctrinal Trap

I. Background on Why Compass is Controversial — and Why it Matters Now

For Readers Encountering This Story for the First Time

Compass Holdings is not a typical real estate company. Founded in 2012 and publicly traded on Nasdaq under the ticker COMP, it spent its first decade building a brand around premium technology, elite agent recruitment, and a luxury-market identity. For most of its existence the company was best known for two things: its sleek black-and-white aesthetic, and its persistent inability to post a full-year GAAP profit despite billions in venture and public capital.

The January 2026 acquisition of Anywhere Real Estate — the parent of Coldwell Banker, Century 21, and Sotheby’s International Realty — changed the scale of the conversation. The deal added $2.6 billion in debt and pushed agent count to 37,000 across 35 major U.S. markets. Compass went from well-capitalized disruptor to dominant player in a single transaction. And it made the company’s underlying revenue model — one that had always been structurally dependent on a specific and controversial practice — a matter of urgent public concern.

That practice is the private exclusive listing: a home marketed for sale that is not entered into the Multiple Listing Service, circulating instead within the brokerage’s internal network before the open market ever sees it.

The Multiple Listing Service is cooperative infrastructure. Agents who join an MLS agree to list their properties in a shared database and gain access to all other listings in return. The result is price transparency: buyers can see all available homes, competitive bidding becomes possible, and sellers receive what the market will actually bear. MLSs are not government agencies — they are private cooperatives — but in most major markets they are functionally mandatory for agents who want to serve their clients fully.

Compass’s private exclusive model is structurally incompatible with MLS concurrent-marketing requirements. When an MLS requires that any publicly marketed listing be made available to all member agents simultaneously, the pre-market window — the period during which Compass can route a buyer through its internal network before open competition begins — disappears.

The commission capture mechanism depends on that window remaining open. On a $15 million Seattle-area property, capturing both the listing and buyer commission means $750,000 flowing to agents within the same brokerage from a single transaction. Scaled across 37,000 agents and $2.6 billion in post-merger debt obligations, this is not a premium amenity. As MindCast AI documented in its Commission Consolidation analysis, it is a solvency mechanism.

II. The Mechanism: Narrative Inversion, Arguing Both Sides of the Same Fact

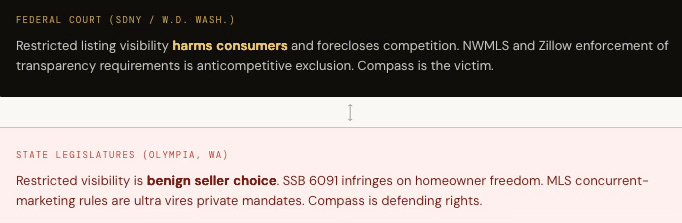

What Compass Claims About Restricted Listing Visibility Depends Entirely on Who Is Listening

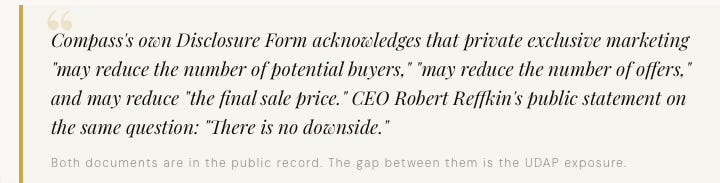

Both positions cannot simultaneously be true. Restricted listing visibility either harms consumers — as Compass pleads in federal court — or protects them, as Compass argues in state legislatures. A company cannot hold both claims across different forums without creating an evidentiary record that is exploitable in both. As MindCast AI documented in The Compass Narrative Inversion Playbook, first published February 4, 2026 as a briefing for legislators and attorneys general, this contradiction is not peripheral to Compass's strategy. It is structural.

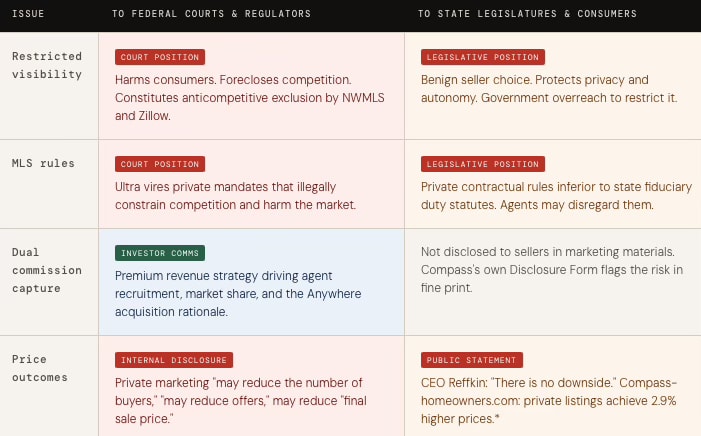

The Cross-Forum Contradiction Matrix

Each row documents the same business practice described incompatibly to four distinct audiences. Source: Compass’s Cross-Forum Contradictions, MindCast AI, Feb. 28, 2026.

* Fine print discloses the 2.9% figure compares Compass listings to other Compass listings — not to the broader market — and that "correlation does not necessarily equal causation."

III. Rhetorical Architecture "Consumer Choice" as a Control Mechanism

The Frame That Protects the Commission Capture Model

Of all the frames Compass deploys, the most durable is consumer choice. It appears in legislative testimony, consumer marketing, broker talking points, and in CEO Reffkin’s public communications. Understanding why requires understanding what the frame actually does, as distinct from what it appears to say.

When Compass says “choice,” it means seller-directed exposure inside a broker-controlled system. The seller chooses to market privately. The seller limits buyer access. The seller exercises autonomy. When courts, regulators, and MLS enforcement bodies say “choice,” they mean buyer access to all publicly marketed listings — the competitive environment in which a seller’s choice produces accurate price discovery.

These definitions produce incompatible market structures. Compass’s “seller choice” is, in operational terms, brokerage routing control: the ability to direct which buyers see a listing, in which order, through which agent network, before the open market is allowed to compete. The commission capture mechanism is the commercial function the frame protects.

As MindCast AI’s consumer choice analysis documents, this framing does not arise from consumer welfare optimization. It arises from Compass’s binding financial constraints: $2.6 billion in debt against a history of never having posted a full-year GAAP profit. At scale, the double-commission mechanism is not a seller service. It is how the Anywhere acquisition premium was priced.

IV. Analytical Framework The Three-Layer Control Architecture

From The Cybernetics of Compass Holdings' Narrative Control Architecture, MindCast AI, March 21, 2026

Any individual piece of Compass's conduct — a lawsuit here, a lobbying campaign there, a consumer website with contested footnotes — can be explained away in isolation. The coherence of the pattern across all forums simultaneously is what the cybernetics framework captures. Eight emergent patterns become visible only when all prior publications are read together. No single publication establishes them independently.

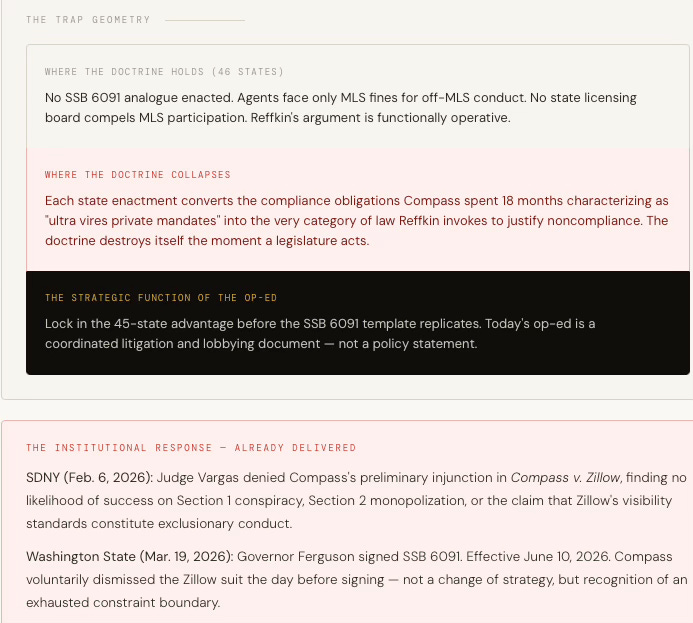

V. The Endgame Reffkin's Doctrinal Trap: Law vs. Rule

Why the Fiduciary-Duty Argument Destroys Itself the Moment a Legislature Acts

On March 25, 2026, Compass CEO Robert Reffkin published an op-ed in Inman formalizing what MindCast AI had been tracking in incipient form for months. The headline stated the claim directly: MLS mandates are private contractual rules, not law, and state fiduciary duty statutes supersede them. Agents who follow seller-directed off-MLS instructions face MLS fines, not regulators, because the MLS is not the government.

As MindCast AI’s doctrinal analysis documents, the structural failure is precise: fiduciary duty governs an agent’s loyalty to a specific client in a specific transaction. MLS rules govern the cooperative market infrastructure that makes competitive transactions possible in the first place. These are not the same decision layer.

An agent who withholds a listing from the MLS to protect a seller’s stated privacy preference has made a transaction-level decision. An agent who systematically routes listings through off-MLS channels to maximize dual-sided commission capture has made a market-level decision. Fiduciary duty governs the first. It has never authorized the second. Reffkin’s doctrine conflates them — and that conflation is the mechanism by which a legal obligation to a client becomes legal cover for conduct that harms the market the client depends on for price discovery.

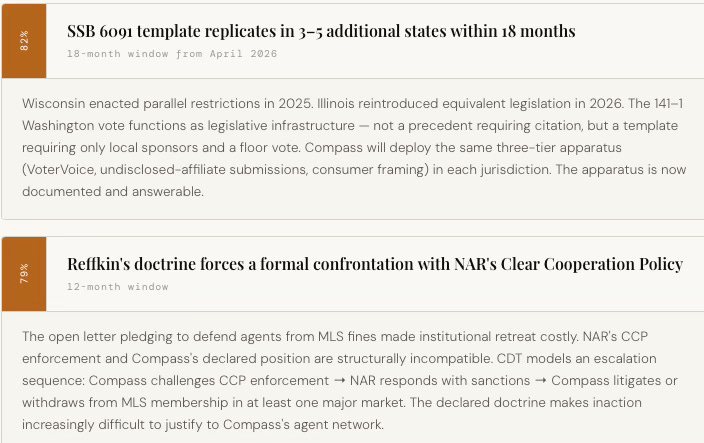

The Compass-Rocket-Redfin open letter pledging to defend agents from MLS fines made institutional retreat from this position costly. NAR’s Clear Cooperation Policy enforcement and Compass’s declared position are now structurally incompatible. CDT models a formal confrontation as a near-term probability.

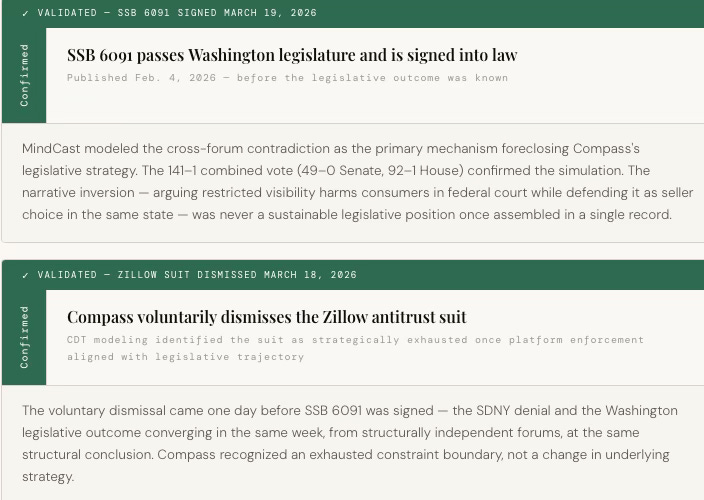

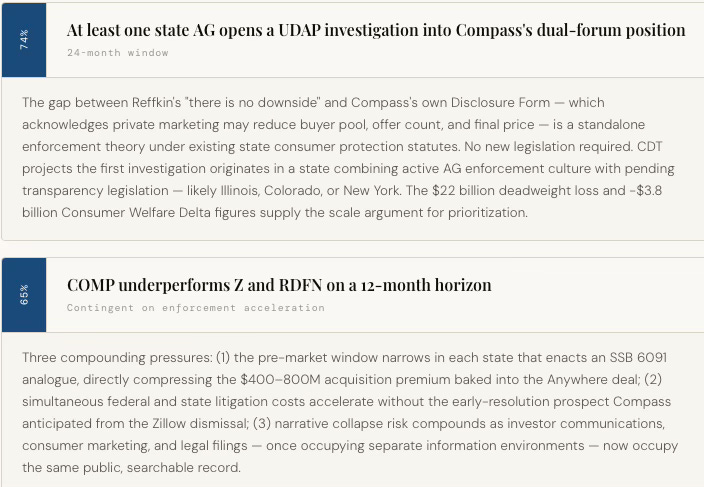

VI. CDT Foresight Simulation MindCast AI Falsifiable Predictions

Generated by MindCast's Cognitive Digital Twin architecture. Predictions are grounded in Nash-Stigler Equilibrium modeling, Tirole Phase frameworks, and Chicago School institutional economics. Two predictions have already been validated against observed outcomes.

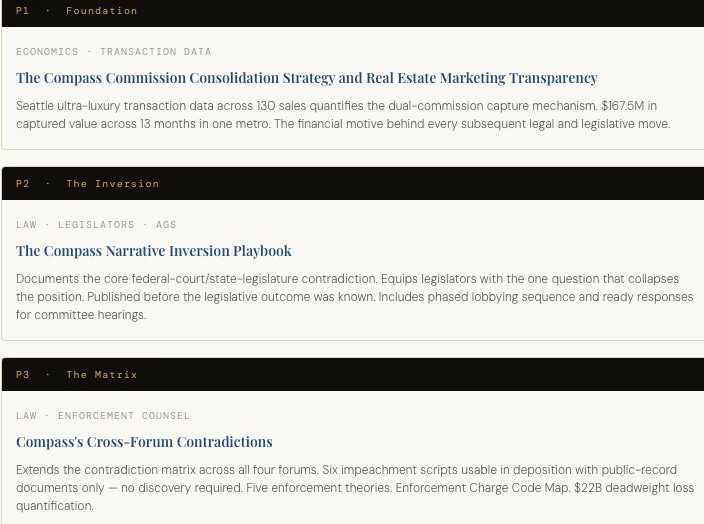

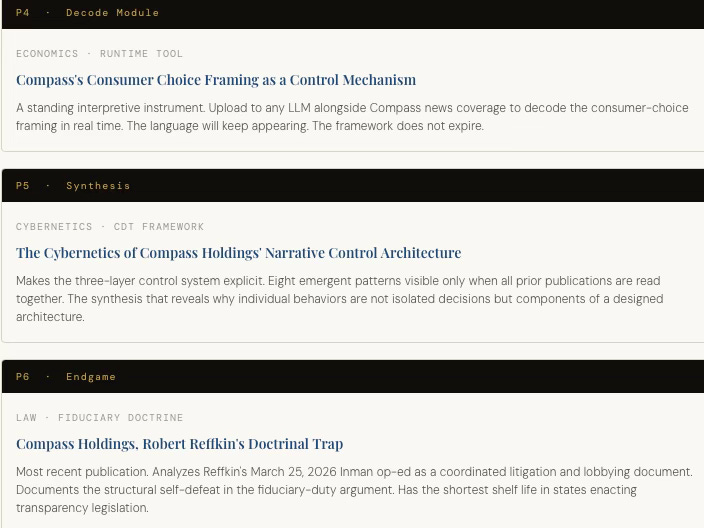

VII. The MindCast Compass vs MLSs Corpus

Six Publications, One Analytical Architecture Each Publication Isolates a Different Surface of the Same Underlying Control Architecture. Each publication below isolates a different surface of the same underlying control architecture. Read individually, each identifies a mechanism, a language pattern, a forum strategy, or an evidentiary record. Read together, they reveal patterns no single publication establishes independently.

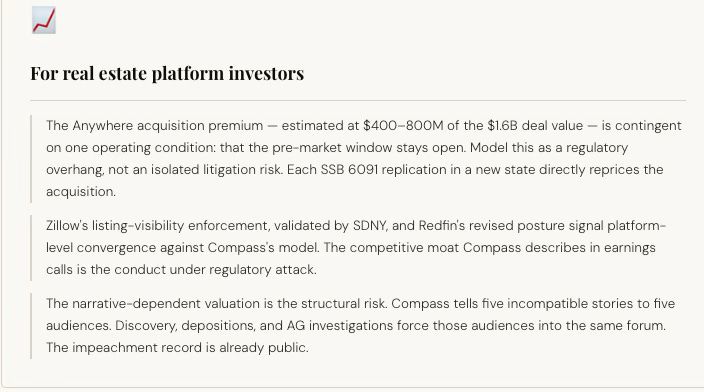

VIII. Audience Briefings What This Means for Each Audience

Contact mcai@mindcast-ai.com to partner with us on Predictive Cognitive AI in Law and Behavioral Economics. To deep dive on MindCast work in Cognitive AI upload the URL of this publication into any LLM and prompt ‘reconstruct MindCast framework with three degrees of cited sub links.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure.