MCAI Lex Vision: Compass’s Cross-Forum Contradictions

How Mutually Exclusive Arguments Across Federal Court, State Legislatures, Investor Communications, and Consumer Marketing Create an Exploitable Evidentiary Record

A Briefing for State Legislators, Attorneys General, and Enforcement Counsel

Companion to The Compass Narrative Inversion Playbook. See also The Compass Commission Consolidation Strategy, The Compass-Anywhere Address Suppression Calculus, State Power vs. Compass Private Exclusives, The Compass-Redfin Alliance.

This publication aggregates contradictions that surfaced across months of MindCast AI analysis spanning state and federal law forums, consumer marketing, investor communications, and public relations. The essay, in a meaningful sense, wrote itself. Each new Compass action — the Inman Connect national MLS proposal, the Q4 earnings call, the Redfin partnership, the Skillman Facebook post — arrived and slotted into a contradiction matrix that was already structurally complete. Compass keeps accelerating, and with each acceleration, the contradictions multiply.

The pattern has a name in economics. Nobel laureate Robert Shiller demonstrated in Narrative Economics (2019) that economic narratives propagate like epidemics — they spread through populations, mutate as they travel, and drive real economic behavior. Shiller observed that “new contagious narratives cause economic events, and economic events cause changed narratives” — a bidirectional feedback loop where the story and the outcome continuously reshape each other. Compass operates as a high-narrative-reliance firm. Its valuation, its agent recruitment, its legislative advocacy, its litigation posture, and its consumer marketing all depend on stories — seller choice, homeowner freedom, competitive innovation, premium revenue strategy. Shiller warned that “the human brain has always been highly tuned toward narratives, whether factual or not, to justify ongoing actions.” Compass’s problem is not that the narratives are false. The problem is that five different narratives are simultaneously true — each calibrated to a different audience, and each destroying the others on contact.

Shiller’s framework is not merely descriptive—it explains why these contradictions are exploitable in litigation and legislation. A narrative-dependent firm that tells incompatible stories to segregated audiences creates its own impeachment record the moment those audiences compare notes. Every deposition, every committee hearing, every AG investigation documented below exploits exactly that vulnerability: forcing Compass to address, in a single forum, the contradicting narrative it advanced in another.

A firm that depends on narrative coherence cannot survive narrative collision. Compass is experiencing that collision across every forum simultaneously, in a 42-day window, with each forum’s evidentiary record feeding the others. The contradictions documented below did not require investigation to discover. Compass produced them. MindCast assembled them.

How to Use This Document

Litigation partners: The six impeachment scripts in Section IX are plug-and-play deposition sequences. Each requires only public-record documents — no discovery needed. The Enforcement Charge Code Map in Section VIII provides five independent legal theories with sourced evidentiary bases.

Legislative staff: The contradiction matrix in Section I and the “For States That Have Not Yet Proposed Legislation” subsection in Section VIII provide the factual foundation for a committee memo or bill analysis. The Washington hearing record is free infrastructure — cite it directly.

State AGs: The UDAP exposure requires no new legislation. The Reffkin earnings call / Disclosure Form gap is a standalone enforcement theory under existing consumer protection statutes. The $22 billion deadweight loss and −$3.8 billion Consumer Welfare Delta figures in Section VIII supply the scale argument for prioritization.

General counsel and corporate partners: The Solvency Geometry in Section X connects every contradiction to a single balance-sheet variable: $2.6 billion in assumed Anywhere debt. The private exclusive infrastructure premium ($400–800 million) exists only if listings can be withheld from the open market. Each state that closes that window reprices the acquisition.

Executive Summary

Compass Holdings advances structurally incompatible factual claims about listing visibility depending on which institutional audience it addresses. In federal court, restricted listing visibility harms consumers and forecloses competition. In state legislatures, the same restriction becomes benign seller choice. In investor communications, private exclusives represent a premium revenue strategy driving market share. On the consumer-facing compass-homeowners.com website, listing restriction is reframed as liberation from monopolistic organized real estate. These four characterizations describe the same business practice to four different audiences, and no two can coexist without contradiction.

MindCast AI’s prior publication, The Compass Narrative Inversion Playbook, documented the core inversion: Compass’s federal pleadings and state testimony make mutually exclusive factual claims. The present essay extends that analysis across the full corpus of MindCast’s Compass publications to construct a comprehensive cross-forum contradiction matrix. Each contradiction is sourced to a specific forum, a specific date, and a specific Compass representative or document—creating an evidentiary record that legislators can cite in committee, attorneys general can deploy in enforcement actions, and opposing counsel can introduce in discovery.

**The core finding: **Compass does not merely shift emphasis across forums. Compass advances factual propositions in one venue that, if true, destroy its own claims in another. Restricted visibility either harms consumers (as Compass pleads in SDNY) or protects consumers (as Compass testified in Olympia). Private exclusives either require regulatory protection because they serve sellers (legislative argument) or require antitrust relief because competitors suppress them (litigation argument). The company’s own Disclosure Form acknowledges that private exclusive marketing “may reduce the number of potential buyers,” “may reduce the number of offers,” and may reduce “the final sale price.” CEO Robert Reffkin’s public statement: “There is no downside.” Both documents are in the public record. The gap between the CEO’s statement and the company’s own client disclosure—on the same factual question—constitutes the deceptive trade practices exposure under state UDAP statutes.

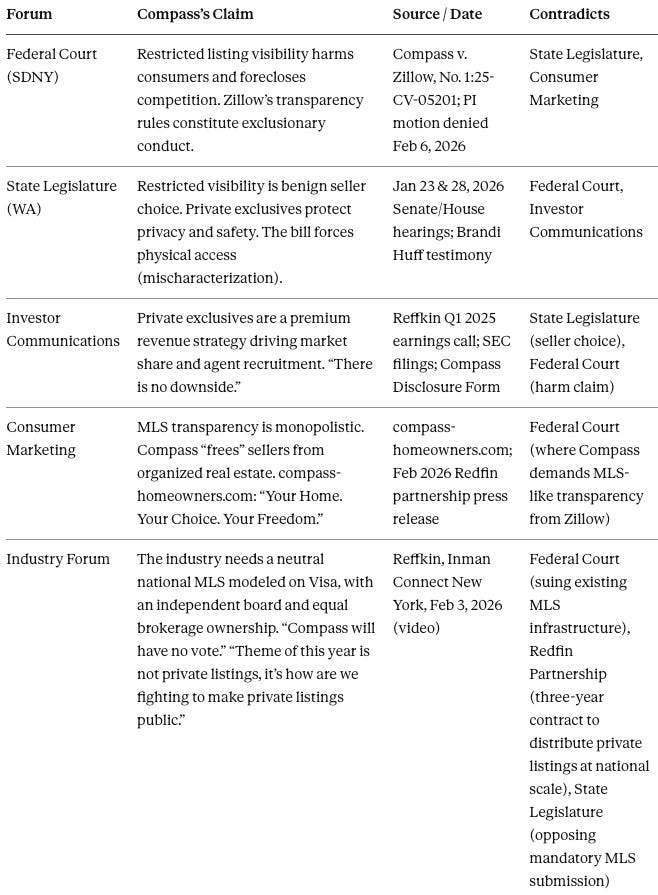

I. The Four Forums, Four Incompatible Stories

Compass operates simultaneously in at least four institutional forums, each demanding a different account of how its private exclusive model affects competition and consumer welfare. MindCast AI publications spanning January through February 2026 documented the positions Compass advanced in each. Assembled together, the contradictions form a matrix where each row cancels at least one other.

Each forum-specific position serves a rational short-term objective: the federal complaint seeks injunctive relief against Zillow; the legislative testimony seeks to defeat SB 6091; the investor communications sustain the stock price; the consumer website manufactures grassroots opposition. Assembled across forums, the positions constitute behavioral evidence that Compass’s advocacy is strategic rather than principled—the defining characteristic of what MindCast AI terms narrative arbitrage: the practice of advancing contradictory factual claims across forums whose audiences do not compare notes.

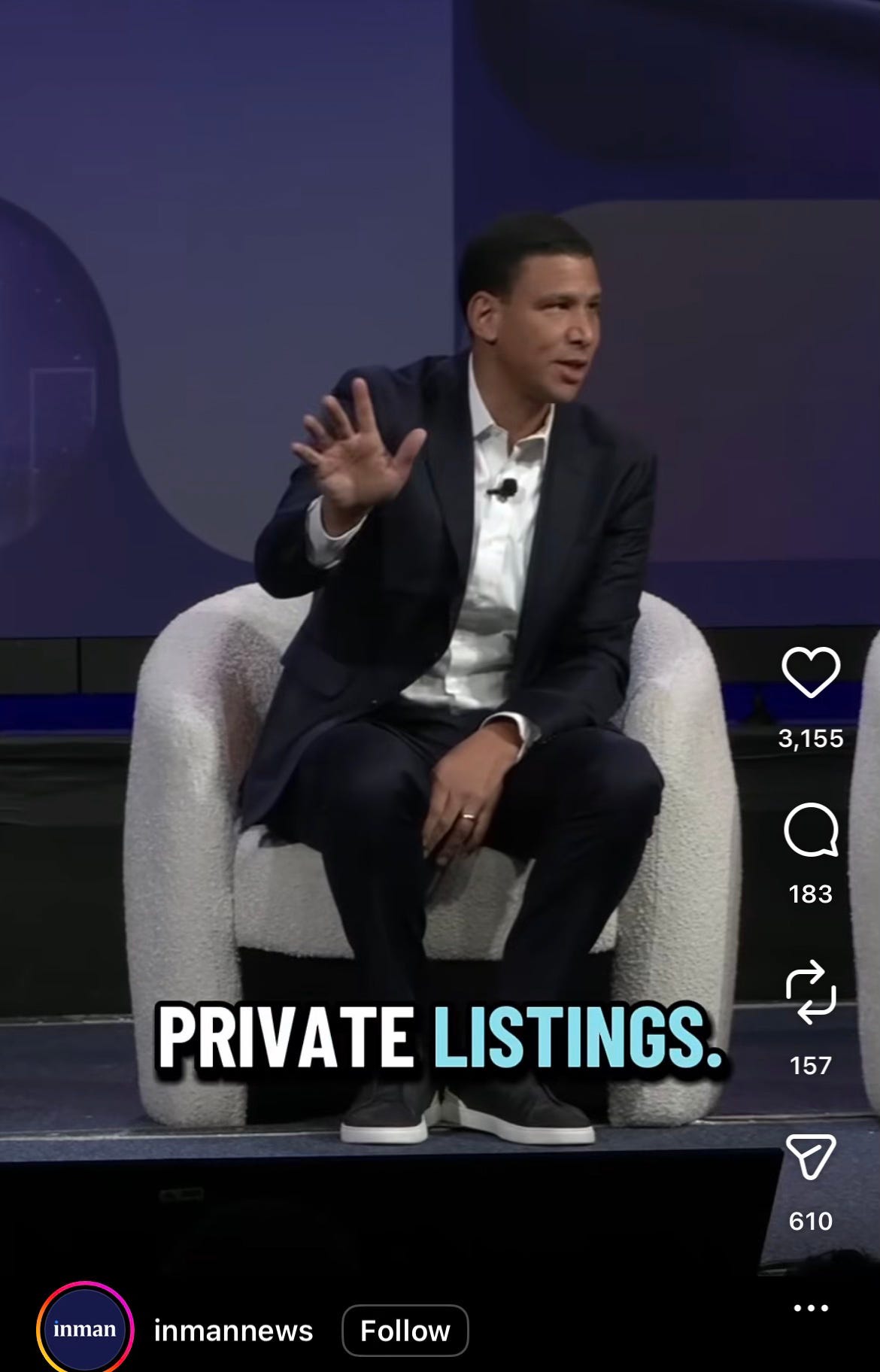

The national MLS proposal sharpens every other contradiction in the matrix. On February 3, 2026—three days before Judge Vargas denied Compass’s preliminary injunction against Zillow—Reffkin took the stage at Inman Connect New York and declared: “Theme of this year is not private listings, it’s how are we fighting to make private listings public.” He then called for a neutral national listing database modeled on Visa’s restructuring. “Compass will have no vote. Compass will have no disproportionate ownership. And it will have an independent board that will work independently in every way.” The framing positioned Compass as a champion of open, equal-access listing infrastructure. Assemble the timeline: Compass sued NWMLS in the Western District of Washington for enforcing existing MLS transparency rules.

Compass sued Zillow in the SDNY for requiring listings to appear on an open platform. Compass routed its private exclusive and Coming Soon inventory onto Redfin through a three-year exclusive partnership that bypasses MLS infrastructure entirely. Compass’s legislative witnesses in Olympia argued against mandatory MLS submission three weeks before Reffkin’s speech. A firm suing existing MLS systems, withholding inventory from them, fighting legislation that would require submission to them, building an exclusive distribution channel around them, and declaring on video that the theme of 2026 “is not private listings”—then signing the largest private listing distribution deal in the industry’s history twenty-three days later—advocates not for open infrastructure but for replacement infrastructure that the largest brokerage in the country would structurally dominate regardless of governance language.

Industry observers identified the contradiction immediately. Engel & Völkers Americas CEO Stuart Siegel noted that Reffkin’s Visa analogy carried its own antitrust history—Visa faced decades of antitrust violations as a structure that allowed thousands of independent entities to act as a single combination of interests. Oppenheim Group founder Jason Oppenheim stated the inference plainly: “Every CEO pretends like they’re trying to fight for the consumer, but give me a break.” The Q4 2025 earnings call, delivered February 26, removed any remaining ambiguity. Reffkin told investors that with Rocket and Redfin aligned, “I don’t see a scenario where the MLSs will continue to enforce these restrictive rules with Rocket and Redfin on our side because we now have more resources.” The framing shifted from “neutral infrastructure” to resource-based coercion in twenty-three days. A firm that proposes a neutral national MLS on February 3 and announces it will overpower existing MLSs through “more resources” on February 26 has disclosed, on the public record, that the proposal was a negotiating position, not a structural commitment.

II. The Federal-State Inversion: Transparency as Both Weapon and Threat

The sharpest contradiction runs between Compass’s federal litigation posture and its state legislative testimony—and it is exploitable under both antitrust and UDAP frameworks because the two positions are not merely inconsistent but mutually destructive: affirming either one supplies the evidentiary foundation to defeat the other. In the Southern District of New York, Compass argues that Zillow’s listing-visibility standards—which require listings to appear on Zillow’s platform to receive full distribution—constitute exclusionary conduct that harms consumers. Compass characterizes itself as a pro-competitive innovator fighting for open access. Judge Vargas denied the preliminary injunction on February 6, 2026, finding Compass had not demonstrated likelihood of success on its Section 1 conspiracy claim, Section 2 monopolization claim, or its assertion that transparency rules cause competitive harm. The court found Compass’s perceived harm self-inflicted.

Three weeks earlier in Olympia, Compass’s Managing Director testified against SB 6091—a bill requiring concurrent public marketing of residential listings—arguing that restricted visibility serves seller privacy and constitutes benign homeowner autonomy. Managing Director Brandi Huff served as Compass’s sole witness at both the January 23 Senate and January 28 House hearings. Under neutral questioning, Huff could not answer whether transparency impacts Compass’s business model, could not articulate buyer-side effects, and reduced fair-housing compliance to “education” rather than enforceable mechanisms.

Regional VP Cris Nelson signed into both hearings but declined to testify at either—a deliberate executive buffer. Nelson’s silence carried strategic weight: by positioning a subordinate as the sole witness, Compass insulated its Pacific Northwest leadership from the legislative record while ensuring the narrative failures landed on Huff’s testimony, not Nelson’s. Nelson witnessed the Senate committee’s reception on January 23—where senators pressed Huff on cross-forum inconsistencies she could not resolve—and chose silence again at the House five days later. The pattern signals corporate calculation, not scheduling conflict. A Regional VP present in the hearing room who declines to defend the company’s position leaves only one interpretation: the position cannot survive executive-level questioning.

MindCast AI’s State Power vs. Compass Private Exclusives predicted this pattern as a Delegation Downshift: Compass sends mid-level managers who lack authority to address business-model questions rather than the regional executives who speak freely in press forums. The prediction confirmed in real time. When senators asked Huff whether Compass’s private exclusive model affects the company’s revenue structure, Huff responded that the question was “probably above what I feel comfortable speaking to.” The admission entered the permanent legislative record—a Compass representative, on the record, conceding that the company’s sole witness lacked authority to explain how the business model works. Nelson sat in the hearing room and let the concession stand. The Delegation Downshift serves Compass’s short-term interest by preventing executive-level admissions, but creates a long-term evidentiary problem: a firm that refuses to explain its own model under neutral questioning invites every enforcement sovereign to draw the inference that the explanation would be adverse.

The logical structure is irreconcilable. If restricted visibility harms consumers (the federal claim), then SB 6091 remediesconsumer harm by mandating concurrent public marketing. If restricted visibility is benign (the state claim), then Compass has no standing to argue that Zillow’s visibility requirements harm competition. Compass cannot simultaneously be the victim of forced transparency (in New York) and the defender of voluntary opacity (in Olympia) without admitting that its position in at least one forum is instrumentally false.

The One Question That Ends the Conversation

“Do you stand by your federal complaint’s claim that restricted visibility harms consumers? If yes, then this bill remedies that harm. If no, withdraw the complaint.”

No third option exists. Every subsequent argument is a deflection from this binary.

III. The Investor-Consumer Inversion: Revenue Strategy Marketed as Liberation

Compass’s investor communications and consumer-facing marketing present the same practice through two lenses calibrated to opposite audiences. On earnings calls and in SEC filings, private exclusives are a premium competitive strategy: they drive agent recruitment, capture dual commissions, and generate revenue that justifies the $1.6 billion Anywhere acquisition premium. CEO Robert Reffkin’s Q1 2025 earnings call framed the model in explicit financial terms, asserting “there is no downside” to private exclusive marketing.

Compass’s own Disclosure Form—the document clients sign before opting into private exclusive marketing—directly contradicts the CEO. The Disclosure Form acknowledges that private exclusive marketing “may reduce the number of potential buyers,” “may reduce the number of offers,” and may reduce “the final sale price.” MindCast AI’s analysis of the Commission Consolidation Strategy documented this gap as the threshold exposure for UDAP enforcement: the CEO told investors there is no downside; the company told clients the downside is reduced offers, reduced buyers, and reduced price. On the same factual question—whether private exclusives affect sale outcomes—Compass advanced opposite answers to investors and clients. Neither document is internal. Both are in the public record. Washington’s AG Civil Rights Division confirmed enforcement authority exists for exactly that conduct in the January 2025 Senate hearing transcript.

Meanwhile, compass-homeowners.com presents private exclusives as consumer liberation. The site frames MLS transparency requirements as monopolistic control by “organized real estate” and positions Compass as the insurgent freeing sellers from an exploitative system. “Your Home. Your Choice. Your Freedom.” The site claims private listings achieve 2.9% higher prices—but the fine print reveals the study compares Compass listings to other Compass listings, not to the broader market, and disclaims that “correlation does not necessarily equal causation.”

The inversion crystallizes: in investor forums, private exclusives capture commissions; in consumer forums, private exclusives protect homeowners. The financial mechanism—routing buyers through Compass’s internal network to capture both commission sides—is the same in both frames. Only the audience-specific label changes. MindCast AI’s Transaction Evidence from Seattle’s ultra-luxury market quantified the mechanism: $4.2 million in captured buyer-side commission across 130 transactions over thirteen months, from a single metro’s monthly top-10 record. Scaled to 35 major markets, the same architecture implies $400–800 million of the $1.6 billion acquisition premium depends on keeping the private exclusive window open.

Contact mcai@mindcast-ai.com to partner with us on Law and Behavioral Economics foresight simulations. To create your own game theory simulation of data on Compass address suppression and private exclusives, upload the URL of this publication to any LLM (ChatGPT, Claude, Gemini, Grok, Perplexity) and prompt ‘develop MindCast framework with 3 degrees of cited sub links.’ Thereafter, all new information you upload is training data for your AI system. See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure for more info.

IV. The Redfin Partnership: Self-Correction’s Obituary

The February 26, 2026 Rocket-Compass-Redfin partnership announcement destroyed the final procedural argument available to Compass in state legislative hearings: that the market would self-correct without legislation. Redfin CEO Glenn Kelman pledged publicly in April 2025 to ban listings selectively pre-marketed without MLS exposure, setting a September 2025 enforcement date. Rocket’s $1.75 billion acquisition of Redfin closed. Kelman departed. The pledge reversed within months. Redfin’s February 26 statement: “Our perspective evolved.”

George Stigler’s 1971 framework predicted the sequence precisely: regulatory behavior tracks ownership, not stated mission. Redfin did not abandon its transparency pledge because its values changed. Rocket acquired the institution, and the institution’s behavior realigned with Rocket’s interest structure. Compass Coming Soon listings now appear on Redfin immediately, with Private Exclusives to follow. Sixty million monthly visitors. Leads flowing exclusively to Compass agents. No days on market. No price history. No valuation estimates. No referral fee.

The contract terms reveal the architecture in Compass’s own commercial language. All buyer inquiries route directly to Compass agents. Rocket Mortgage preferred pricing—a 1-point first-year rate reduction or up to $6,000 lender credit—is available exclusively to Compass clients. The partnership strips from buyers the very data points that protect them—days on market, price drop history, valuation estimates—while routing all leads into Compass’s internal commission capture infrastructure at national scale, for zero cash cost.

A committee chair who invokes self-correction today must defend the proposition that a pledge which reversed four months after a corporate acquisition represents ongoing voluntary market discipline. The second-largest real estate search portal became the primary distribution infrastructure for the practice it pledged to ban—under a three-year contract, in the opposite direction, published by the exhibit itself. The self-correction argument does not lose credibility. The argument loses its primary exhibit and acquires a contradicting one.

Ready Response for Committee Chairs

“If the market is self-correcting, why did the second-largest search portal abandon its pledge to ban off-market listings and sign a three-year contract to become the primary distribution infrastructure for them?”

The Fifth Forum: When the Consumer Welfare Framing Drops

Within hours of the Redfin partnership announcement, Moya Morgan Skillman—co-listing broker and co-buyer broker on the Mercer Island Exhibit Transaction (MLS #2362507, 1628 72nd Ave. SE, four role designations recorded at close alongside Tere Foster)—published a public Facebook post celebrating the deal. Read the post carefully, because every legislative and litigation filter Compass maintains in other forums drops away entirely.

Moya Morgan Skillman public Facebook post, February 27, 2026

Skillman opens by calling Reffkin “our fearless leader”—linking herself directly to the CEO’s corporate strategy, not to independent agent behavior or homeowner autonomy. The possessive framing throughout confirms the audience: “More exposure for your listings, more choices for your seller, and more direct buyer inquiries — on your terms.” Your listings. Your seller. Your terms. Every possessive pronoun addresses the agent, not the consumer. In Olympia, Compass frames private exclusives as homeowner autonomy. On social media, recruiting agents to the platform, the homeowner disappears. The seller is the agent’s seller, managed on the agent’s terms.

Skillman then states the mechanism with a clarity Compass’s legislative witnesses never approached: “Syndicate their Coming Soon listings to 60 million buyers on Redfin.com with no days on market, no negative insights, and no home valuation estimates.” Three buyer-protection data points—stripped. Compass’s own Disclosure Form acknowledges that private exclusive marketing “may reduce the number of potential buyers,” “may reduce the number of offers,” and may reduce “the final sale price.” Skillman celebrates the removal of the very data that would allow buyers to detect those outcomes. Days on market reveals whether a property is overpriced. Price drop history reveals whether a seller has already tested and failed at a higher number. Home valuation estimates provide independent pricing benchmarks. Compass calls this information “negative insights.” Market participants call it price discovery.

The commission capture architecture appears next, stated without euphemism: “The listing agent’s name, photo and brokerage will remain prominently displayed, with all buyer inquiries flowing directly to the listing agent.” Every buyer who contacts a Compass listing agent through Redfin enters the dual-commission pipeline. No independent buyer’s agent intercepts the lead. No competing brokerage sees the inquiry. The mechanism that captured $4.2 million in buyer-side commission from Seattle’s ultra-luxury market—documented across 130 transactions in MindCast AI’s Commission Consolidation Strategy—now scales to 60 million monthly visitors nationally. Skillman described the Layer 3 revenue architecture—the $400–800 million slice of the Anywhere acquisition premium that exists only if listings can be withheld from the open market long enough to capture both commission sides—more clearly than Compass’s own partnership page, Compass’s legislative witnesses, or Compass’s federal complaint.

The evidentiary significance compounds because of who Skillman is and what role she occupies in Compass’s commission capture architecture. MindCast AI’s Address Suppression Calculus documented Team Foster’s three-node routing structure in detail: Tere Foster operates as the Contract Anchor—a high-visibility rainmaker who secures listing contracts across Seattle’s highest-value submarkets (Medina, Hunts Point, Clyde Hill, Yarrow Point, Mercer Island, Bellevue waterfront). Moya Skillman operates as the Internal Buyer Capture Node—Foster’s daughter, whose structural role captures buyer representation on properties her mother lists. Michael Orbino functions as the Management Overlay—a division-level broker coordinating inventory pipelines across the team.

The mother-daughter relationship carries structural, not merely familial, significance. Formal role separation on NWMLS records does not correspond to independent economic decision-making. Within MindCast AI’s 130-transaction sample from The Commission Consolidation Strategy, Skillman never appears as a standalone outside buyer’s broker competing for a listing held by an independent brokerage. Every appearance in the dataset positions her either as co-listing broker alongside her mother or as buyer’s agent on a property listed by Foster or Managing Broker Orbino. The pattern across thirteen months of ultra-luxury transactions is structurally invariant—Skillman functions exclusively within the Compass internal routing network, never as an independent market participant.

MLS #2362507—the Mercer Island Exhibit Transaction at 1628 72nd Ave. SE, sold August 11, 2025 at $15,000,000—records four role designations: Tere Foster as Listing Broker and Buyer Broker, Moya Skillman as Co-Listing Broker and Co-Buyer Broker. Both agents held fiduciary obligations to seller and buyer simultaneously on the same transaction. Total commission captured by the same two individuals: $750,000. No outside agent involved. No competing offer from an independently represented buyer. The MLS recorded it. The role designations are self-authenticating. No expert witness or discovery subpoena is required to interpret what four role designations on a single transaction mean.

Team Foster then deployed address suppression on MLS #2392995—“Triptych: A Tom Kundig Masterwork on Lake Washington”—listed at $79,000,000 with full photographs, specifications, and price on fosterrealty.com, and one field reading “Call for Address.” Any buyer seeking to identify the property’s location had to contact Team Foster directly, entering the Compass routing network before any independent buyer’s agent could show the property. Buyer-side commission at stake from a single transaction: $1,975,000. The listing appeared during the February 2026 legislative window—while the Washington House debated SSB 6091, the bill designed to prevent exactly this mechanism.

The Nash-Stigler constraint exposes why Team Foster’s architecture—and Skillman’s role within it—matters beyond any single transaction. MindCast AI’s Address Suppression Calculus modeled the optimization problem across four price tiers and reached a finding with no exceptions: no price threshold exists where address suppression simultaneously generates revenue sufficient to affect the Compass-Anywhere debt service obligation and avoids the detection threshold that triggers institutional response. Concentrating deployment at $20 million and above—where privacy framing remains credible and Skillman’s team operates—compresses annual revenue to approximately $500,000 per market. Full-portfolio deployment across all 54 Compass-controlled listings in the dataset produces a maximum of $7.04 million annually—but immediately exceeds detection tolerances, triggering NWMLS enforcement, competitor complaints, and regulatory scrutiny. Revenue adequacy and detection avoidance are structurally incompatible objectives at every price threshold modeled.

The constraint creates the trap Skillman’s Facebook post inadvertently documents Compass trying to escape. At the team level, the Foster-Skillman architecture generates enough dual-commission capture to matter to a team’s P&L—$750,000 on a single Mercer Island transaction—but not enough to service $2.6 billion in corporate acquisition debt. Scaling the mechanism across 35 markets requires deployment volumes that cross the Stigler information-sufficiency boundary, making the strategy visible to every enforcement sovereign simultaneously. The Redfin partnership represents Compass’s structural response: substitute Redfin’s 60 million monthly visitors for the address-field suppression that NWMLS constraints made untenable at scale. Skillman celebrates the substitution in her post—“no days on market, no negative insights” through Redfin rather than through a suppressed address field—without recognizing that the Nash-Stigler constraint does not disappear at the platform level. The constraint migrates upward. Instead of triggering NWMLS enforcement, the platform-level deployment triggers state legislative and federal enforcement responses. The 42-day multi-vector convergence documented in Section VII is that migration in action.

Skillman’s Facebook post celebrating the Redfin partnership landed eleven hours after the deal went live, connecting the team-level routing architecture she operates daily to the national distribution infrastructure Compass just acquired. The same person. The same team. The same mechanism—now scaled from a $79 million Lake Washington estate to 60 million monthly Redfin visitors across 35 markets.

Skillman’s post reveals what Compass tells agents when no legislator, judge, or regulator occupies the room. Every other forum’s framing—homeowner privacy, seller choice, consumer empowerment, competitive innovation—operates as the filtered version. The agent-facing recruitment pitch strips those filters and exposes the underlying economic proposition: capture buyer leads, eliminate competing brokerages from the inquiry flow, suppress the market data that enables informed buyer negotiation, and consolidate both commission sides inside Compass’s network. When Compass’s next legislative witness testifies that private exclusives protect homeowner autonomy, the committee can place Skillman’s post on the record and ask a single question: “Which audience received the accurate description of how this model works—the legislators, or the agents?”

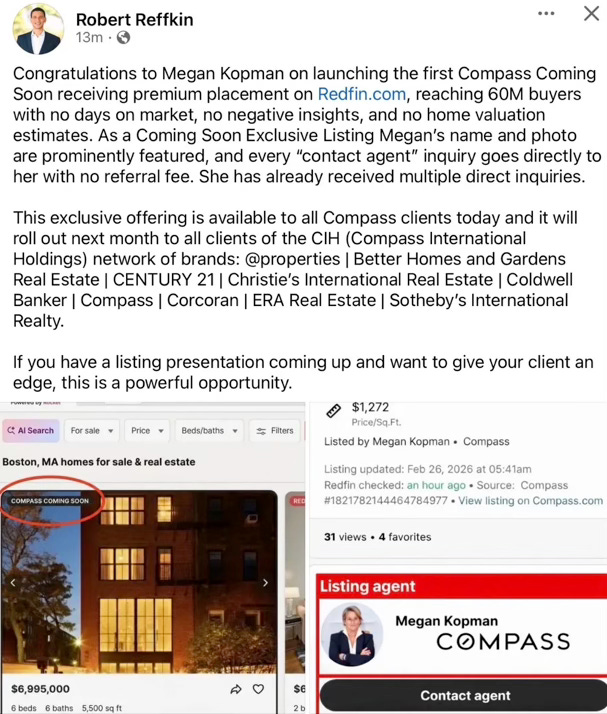

The Sixth Forum: What “Making Private Listings Public” Looks Like

Two days after the Redfin partnership announcement—and twenty-five days after declaring at Inman Connect that the “theme of this year is not private listings, it’s how are we fighting to make private listings public”—Reffkin posted the following on his personal Facebook account:

Robert Reffkin public Facebook post, February 28, 2026

The post congratulates Megan Kopman on “launching the first Compass Coming Soon receiving premium placement on Redfin.com, reaching 60M buyers with no days on market, no negative insights, and no home valuation estimates.” Every “contact agent” inquiry routes directly to Kopman “with no referral fee.” The post then announces the mechanism will “roll out next month to all clients of the CIH (Compass International Holdings) network of brands: @properties | Better Homes and Gardens Real Estate | CENTURY 21 | Christie’s International Real Estate | Coldwell Banker | Compass | Corcoran | ERA Real Estate | Sotheby’s International Realty.” The closing line: “If you have a listing presentation coming up and want to give your client an edge, this is a powerful opportunity.”

Skillman’s post and Reffkin’s post serve different analytical purposes and should be read as distinct exhibits.

Skillman is delivering the wrong framing to the wrong audience. Her Facebook post is not an internal agent communication—it is public-facing, visible to every consumer, committee staffer, and enforcement sovereign with a browser. And the language she uses—“no days on market, no negative insights, and no home valuation estimates”—describes the suppression of consumer-protective data as a selling point. Days on market, price drop history, and valuation estimates exist to protect buyers. Skillman markets their removal as a benefit—not to agents in a closed recruiting pitch, but to the public, on a platform where the consumers whose interests Compass’s legislative witnesses claim to protect can read it. The evidentiary value is not that Skillman dropped the consumer-welfare filter. The evidentiary value is that she delivered the commission capture framing directly to consumers and presented the elimination of their informational protections as a feature. “Our fearless leader.” “Your listings, your seller, your terms.” No mention of seller choice, homeowner privacy, or fair housing. The vocabulary that Compass deploys in every other forum—the vocabulary designed for consumers—is entirely absent from a post that consumers can see.

Reffkin’s post operates on three different levels, none of which overlap with Skillman’s.

First, Reffkin defines what “making private listings public” looks like in practice. Read the Inman declaration against the Kopman listing. Reffkin told the industry the theme of 2026 “is not private listings, it’s how are we fighting to make private listings public.” This post is him demonstrating exactly that—a Compass private listing, appearing on Redfin, visible to 60 million visitors. In his framing, he kept his word. The problem is what “public” now means. The Kopman listing appears on Redfin—but not on the MLS. No days on market. No price drop history. No home valuation estimates. All buyer inquiries route to the listing agent. No independent buyer’s broker intercepts the lead. No referral fee. “Premium placement”—prioritized above MLS-submitted listings from competing brokerages. Reffkin redefined “public.” A listing that appears on one affiliated platform, stripped of every data point that protects buyers, with all leads captured internally and no competing broker access, is not what any legislature, any MLS, or any consumer protection framework means by “public.” Public means MLS submission—concurrent access by all brokerages, all platforms, all buyers, with full market data. Reffkin built a private version of public: visible but informationally impoverished, structurally designed to route every buyer inquiry into Compass’s dual-commission capture pipeline.

Second, Reffkin delegitimizes the enforcement infrastructure that every state transparency bill depends on. At Inman Connect—the same appearance where he announced the “not private listings” theme—Reffkin declared: “I don’t think any agent at any company should be fined by their MLS. This doesn’t happen in any other industry. There is no association that is fining their own people. This is not normal.” On the Q4 earnings call, he escalated: “I’m going to look at that piece of paper, and the agent’s going to say, ’Can you help me?’ Yes, we will help them.” Reffkin is not merely marketing the Redfin pipeline. He is preemptively framing MLS compliance fines as illegitimate—inoculating agents against the enforcement pressure that MLS transparency rules create. Every state concurrent marketing bill relies on MLS infrastructure to function. A CEO publicly telling 340,000 agents that MLS fines are “not normal” and that the company will absorb the cost of noncompliance is a direct assault on the enforcement mechanism those bills depend on. The framing is not “we disagree with the rule.” The framing is “the institution making the rule has no legitimate authority to make it.”

Third, Reffkin announces the nine-brand CIH rollout. Skillman celebrates a team-level win in Seattle’s ultra-luxury market. Reffkin announces a corporate infrastructure deployment across the entire Anywhere acquisition portfolio: Century 21, Coldwell Banker, Sotheby’s, Corcoran, ERA, Christie’s, Better Homes and Gardens, @properties. Every brand Compass acquired with $1.6 billion in debt-financed capital now feeds into the same Redfin distribution pipeline. The Layer 3 premium—the $400–800 million slice of the acquisition price that exists only if listings can be withheld from the open market—activates across 340,000 agents nationwide. That is the scaling that crosses the Nash-Stigler detection threshold. That is the deployment volume the Address Suppression Calculus identified as structurally incompatible with detection avoidance. And the CEO announced it on Facebook as a “powerful opportunity.”

The deposition question writes itself: “Mr. Reffkin, when you told the Inman Connect audience that the theme of 2026 was making private listings public, did you mean submission to the MLS with full market data—or did you mean display on a single affiliated platform with no days on market, no price history, no valuation estimates, and all buyer inquiries routed exclusively to the listing agent?”

The Six-Forum Contradiction

Federal Court: Restricted visibility harms consumers.

State Legislature: Restricted visibility protects homeowner privacy.

Investor Communications: Restricted visibility is a premium revenue strategy with “no downside.”

Consumer Marketing: Restricted visibility is liberation from monopolistic organized real estate.

Agent Social Media (Skillman): Restricted visibility eliminates “negative insights” and “home valuation estimates”—and a Compass agent marketed the suppression of buyer-protective information directly to the public as a feature, not a risk.

CEO Social Media (Reffkin): Restricted visibility is “premium placement” on an affiliated platform—redefined as “making private listings public”—while the CEO simultaneously delegitimizes the MLS enforcement infrastructure that state transparency laws depend on, and announces the mechanism’s rollout across all nine CIH brands and 340,000 agents.

V. The Astroturf Architecture: Manufacturing Consent

Compass’s cross-forum contradictions extend beyond substantive arguments to the infrastructure of advocacy itself. MindCast AI’s analysis of the January 2026 SB 6091 hearings documented a coordinated opposition apparatus operating through three tiers: grassroots manufacturing via VoterVoice campaigns, consumer framing via compass-homeowners.com, and aligned broker testimony designed to appear as independent constituent concern.

The data exposed the coordination’s scale. Of 162 individuals affiliated with Compass who registered opposition to SB 6091 in the Senate hearing, only 9 disclosed that affiliation—a 17:1 ratio. By the House hearing, Compass sign-ins declined 67%, and brokers who registered to testify vanished once committee questioning intensified.

Jennifer Ng’s January 23 Senate testimony illustrates the apparatus at the individual level. Ng testified about seniors in crisis and vulnerable populations—framing private exclusives as a protective measure for at-risk homeowners. She listed every credential from her professional bio. She omitted one: Compass. Ng holds the title of Sales Manager at Compass Fremont, identified in Compass’s own public agent directory. Her testimony carried the emotional weight of an independent community advocate. Her employer’s identity carried the evidentiary weight of coordinated corporate messaging. The omission was not casual. Ng presented precisely the credentials that established expertise while suppressing the one affiliation that would have recharacterized her testimony from constituent concern to corporate lobbying. Multiply that pattern by 153 undisclosed affiliations, and the 17:1 ratio stops being a statistic and becomes an infrastructure.

The apparatus creates a cross-forum problem of its own. Compass markets itself to investors as a company with enough market power to capture dual commissions at scale across 35 metros. Compass presents itself to legislators as defending small homeowners exercising individual choice. The VoterVoice infrastructure—which collects mobile numbers for “periodic call to action text messages” and provides pre-drafted messaging—reveals which framing Compass actually operates under. A seller-choice movement does not require corporate-manufactured opposition with undisclosed affiliations. A revenue-protection campaign does.

VI. The Technology Trap: IPO Narrative as Antitrust Admission

A fifth forum compounds the contradiction matrix: SEC filings and IPO disclosures. MindCast AI’s analysis of Compass’s Technology Trap documented how the company spent a decade telling investors it was a technology company whose platform created switching costs, retained agents through platform dependency, and deserved software-style valuation multiples. Applying Stanford professor Mark Lemley’s 2025 labor-antitrust framework, those same disclosures describe exit barriers under Section 7 of the Clayton Act.

The documentation trap operates because securities law required Compass to explain its competitive moat. Antitrust law now uses that explanation as evidence. Every feature Compass cited as a competitive advantage—proprietary data, integrated workflows, agent lock-in, $1.5 billion in platform investment—is precisely what Lemley identifies as a barrier to exit that creates monopsony capacity over agent labor. Productivity gains that travel with the worker are efficiencies; productivity gains that remain with the platform are transfers enabled by exit barriers. Compass celebrated the barriers, quantified them, and filed them with the SEC. Discovery is unnecessary because compliance already did the work.

Applied to the cross-forum matrix, the IPO narrative creates a sixth incompatible position. In federal court against Zillow, Compass is a scrappy competitor fighting for open access. In SEC filings, Compass is a platform monopolist whose technology creates agent lock-in. In state legislatures, Compass is a defender of individual homeowner choice. On compass-homeowners.com, Compass is the insurgent fighting “organized real estate.” On earnings calls, Compass is the consolidator whose acquisition premium requires information asymmetry to pencil. After the Anywhere merger, Compass controls 340,000 agents and 20%+ of the national residential market—the consolidation that prompted nineteen senators to formally accuse the DOJ of corruption in clearing the deal.

VII. The Multi-Vector Convergence

MindCast AI’s 42-Day Collapse Framework identified the core structural insight: the danger to Compass was never any single proceeding. A firm of this size can survive a federal antitrust case, a 49-0 legislative defeat, or congressional scrutiny of its merger clearance. What a firm cannot survive is all activating simultaneously, feeding each other’s evidentiary records, with none requiring the others to succeed in order to cause damage.

Framed through MindCast AI’s Dual Nash-Stigler Equilibrium Architecture, Compass’s cross-forum strategy depended on maintaining isolated, audience-specific equilibria—feeding tailored narratives to segregated institutional audiences that never compared notes. Consumer harm from restricted visibility in the SDNY. Benign seller choice in Olympia. Premium revenue strategy on earnings calls. Liberation from organized real estate on compass-homeowners.com. Each position constituted a locally stable Nash equilibrium: rational within the forum, sustainable as long as no audience observed the contradicting position advanced in another venue. The multi-vector convergence destroyed the information asymmetry required for those isolated equilibria to function. When SSB 6091’s 49-0 passage, the SDNY preliminary injunction denial, the Warren letter, and the Redfin partnership announcement all activated within the same 42-day window, each forum’s evidentiary record became visible to every other sovereign simultaneously. The Stigler information-sufficiency threshold crossed in every forum at once. Compass’s previously rational forum-shopping became mathematically unsustainable—not because any single forum defeated the strategy, but because cross-forum visibility eliminated the compartmentalization the strategy required.

MindCast AI’s State Power vs. Compass Private Exclusives named the mechanism that sustained the compartmentalization: the Stigler Shield—the structural information asymmetry that prevents cross-forum detection of contradictory positions. Each forum operated with its own evidentiary record, its own audience, and its own standard of scrutiny. Federal courts saw the antitrust pleadings but not the state testimony. State legislators heard the seller-choice framing but not the SDNY complaint. Investors received the “no downside” earnings call but not the Disclosure Form’s contradicting language. The Shield functioned because no institution compelled simultaneous accounting across all forums. Narrative inversion persisted not because Compass’s arguments were persuasive—they were not, as the 49-0 vote and the PI denial confirm—but because the Stigler Shield prevented any single audience from observing the full contradiction set.

The Washington hearings broke the Shield. The core insight from the State Power analysis applies directly to every forum documented in this essay: testimony generates the enforcement signal, not enactment. A hearing compels the firm to address, in a single public setting, positions it has maintained in contradictory form across courts and marketing channels. A failed bill that produces testimony documenting cross-forum contradictions creates a permanent evidentiary record available to every AG in every state. Washington’s SB 6091 passed the Senate 49-0, but even a bill that dies in committee generates the same informational release—the hearing record is the mechanism; the bill is secondary. Gary Becker modeled misconduct as a rational economic calculation: misconduct persists when benefits exceed the probability of detection multiplied by the severity of punishment. Compass maintained narrative inversion because the probability of cross-forum detection historically approached zero. The Washington hearing raised that probability to 1.0 by forcing Compass’s contradictions onto a single permanent record. The hearing did not require new penalties. The hearing destroyed the calculus of impunity by making the contradictions prohibitively expensive to maintain.

Within 42 days of the Anywhere merger closing on January 9, 2026, the following converged: SSB 6091 passed the Washington State Senate 49-0. The SDNY denied Compass’s preliminary injunction against Zillow. Nineteen senators formally accused the DOJ of corruption. Wisconsin and Illinois advanced concurrent marketing requirements. COMP dropped 3.2% on the Warren letter’s publication date alone. Each vector feeds the others. The Senate hearing testimony becomes discoverable evidence in the Zillow trial. The SDNY denial becomes a legislative exhibit against the “market self-corrects” argument. The Warren letter accelerates state AG coordination. The Redfin partnership announcement on February 26 confirmed the structural logic: Compass responded to closing regulatory windows with the only distribution deal available to a firm carrying $2.6 billion in assumed Anywhere debt—one that costs zero cash while expanding the private exclusive infrastructure nationally.

The cross-forum contradiction matrix is the connective tissue. Each proceeding generates a permanently discoverable record. Each record is simultaneously available—without coordination—to every other enforcement sovereign examining Compass. The same Seattle ultra-luxury transaction dataset documenting $4.2 million in captured commission is accessible to the SDNY Zillow antitrust trial, the NWMLS antitrust case in the Western District of Washington, the Warren letter congressional inquiry, Washington’s AG Civil Rights Division, every state legislature advancing a concurrent marketing bill, and every auditor testing goodwill assumptions. No forum introduced the dataset for another forum to draw from it. The MLS recorded it. Seattle Agent Magazine published it. Every enforcement sovereign has had access since the month each transaction closed.

VIII. Practical Applications

For State Legislators

Every core claim Compass advances in state hearings—seller choice, privacy, fair-housing compliance through disclosure, harm from “data scraping” platforms—has been raised, tested under neutral questioning, and failed on the Washington record. Legislators in other states do not need to re-litigate these claims. Compass’s Managing Director could not explain how the model functions at scale without opt-outs, could not articulate buyer-side effects, and reduced fair-housing compliance to “education” rather than enforceable mechanisms. Compass’s remaining tactical play in any legislative session is introducing an opt-out amendment on the floor to consume calendar time and stall the bill past the cutoff.

For States That Have Not Yet Proposed Legislation

States that have not introduced real estate marketing transparency bills should understand why the cross-forum record documented here applies to every jurisdiction where Compass operates—not just Washington. Four structural reasons make inaction increasingly costly.

First, the mechanism operates in every Compass market. The three-node routing architecture documented through Team Foster in Seattle—Contract Anchor, Internal Buyer Capture Node, Management Overlay—replicates wherever luxury inventory concentration and thin buyer pools create the conditions for pre-market routing. Boston, Miami, Los Angeles, Chicago, New York, and every other market where Compass holds significant listing share runs the same dual-commission capture pipeline. The $4.2 million captured from Seattle’s ultra-luxury top-10 record is the calibration from a single metro. Scaled across 35 major markets, the same architecture implies $600 million to $1.5 billion in captured buyer-side commission nationally. Every state AG and every legislative committee has access to the same MLS transaction data for their jurisdiction—the same addresses, the same role designations, the same commission flows—waiting to be assembled by any analyst who knows what to look for.

Second, Washington’s evidentiary record is free infrastructure. The hearing transcripts from January 23 and January 28, 2026 are permanently discoverable legislative records. Huff’s testimony failures—the Delegation Downshift, the admission that business-model questions exceeded her authority—entered the public record under oath-equivalent conditions. The 17:1 Astroturf ratio is documented in the sign-in sheets. The Reffkin earnings call / Disclosure Form contradiction requires no investigation to surface—both documents are already public. Washington did the investigative work. States that have not proposed legislation inherit the entire evidentiary dataset at zero cost, zero discovery burden, and zero political risk of conducting their own hearings. A staff memo citing the Washington record provides the same factual foundation as a year-long committee investigation.

Third, the Parker v. Brown ratchet makes later adoption safer. Each state that enacts a concurrent marketing requirement reinforces the “clearly articulated state policy” standard under the state-action immunity doctrine, making federal preemption challenges progressively weaker. Wisconsin enacted listing transparency restrictions in December 2025. Illinois reintroduced its bill in February 2026. Washington’s Senate voted 49-0. States that introduce legislation after three or four other states have enacted carry substantially lower litigation risk than first-movers. The legal landscape improves with each adoption. Waiting is not neutral—waiting allows the private exclusive mechanism to capture dual commissions from the state’s consumers while the regulatory environment matures elsewhere.

Fourth, UDAP enforcement requires no new legislation at all. The Reffkin earnings call statement (“There is no downside”) versus the Compass client Disclosure Form (“may reduce the number of potential buyers,” “may reduce the number of offers,” may reduce “the final sale price”) constitutes a standalone deceptive trade practices exposure under every state’s existing UDAP statute. No bill required. No hearing required. The CEO’s public statement and the company’s own client disclosure contradict each other on the same factual question—whether private exclusives affect sale outcomes—and both documents are in the public record. Washington’s AG Civil Rights Division confirmed enforcement authority exists for exactly this conduct in the January 2025 Senate hearing transcript. Every other state AG possesses the same statutory authority. The question is not whether the enforcement theory exists. The question is whether the AG’s office has seen the contradiction. Forwarding this document answers that question.

For State Attorneys General

The cross-forum evidentiary record establishes a narrative inversion pattern exploitable in any enforcement theory, consent decree negotiation, or amicus filing. The Disclosure Form / earnings call gap is the threshold UDAP exposure: the CEO told investors there is no downside; the company told clients the downside exists. The Washington hearing transcript is a permanently discoverable legislative record confirming AG enforcement authority over exactly this conduct. Multi-state AG coordination becomes analytically rational with Washington’s evidentiary record as the shared foundation—the same dataset, the same contradictions, the same mechanism documented across every market Compass operates in.

MindCast AI’s State Power vs. Compass Private Exclusives quantified the national harm and supplied the orthodox free-market rationale for state enforcement. Estimated deadweight loss from the Compass-Anywhere private exclusive gatekeeping model: $22 billion—comparable to documented monopoly cases where federal enforcement did occur. Consumer Welfare Delta from price suppression in non-competitive-bid Private Exclusive transactions: −$3.8 billion. Accumulated operating losses subsidized by debt-financed market consolidation: $2.2 billion. Inherited merger debt driving dual-agency commission capture as a balance-sheet necessity: $2.5 billion. AGs should note the magnitude: these are not business-dispute numbers. These are structural antitrust figures that dwarf the enforcement thresholds applied in comparable consumer protection investigations.

The Chicago School framework supplies the enforcement rationale across every political environment. Under Coase, state transparency mandates reduce the artificial transaction costs that private exclusive networks impose—hiding inventory and price data from the open market, forcing buyers to pay an access tax through dual-agency commissions to see the product. The hearing process functions as what MindCast AI terms a Coasean Information Subsidy: the cost for any single consumer to uncover Compass’s contradictory positions across forums is prohibitively high, but the state subsidizes the production of that truth through the hearing record, reducing transaction costs for the entire market. Under Becker, the enforcement theory targets the calculus of impunity—misconduct persists when benefits exceed the probability of detection multiplied by the severity of punishment. Under Posner, state action constitutes efficiency maximization: when federal antitrust fails to correct the deadweight loss, efficient systems route the correction to the institution with lower friction—state police power. The AG functions as the marketmaker of last resort. The framing is not “we are regulating the market.” The framing is “we are removing the artificial friction that prevents the market from working.”

Multi-state coordination strengthens through the Parker v. Brown safe harbor. Each state that enacts a concurrent marketing requirement reinforces the “clearly articulated state policy” standard, making federal preemption challenges progressively weaker as the state count rises. Wisconsin enacted listing transparency restrictions in December 2025. Illinois reintroduced its bill in February 2026. Washington’s 49-0 Senate vote provides the strongest legislative signal in the cascade. The first state to enact faces the most aggressive legal challenge. By the fifth state, the challenge is virtually untenable.

A critical distinction for enforcement framing: the $4.2 million in captured buyer-side commission documented in the Seattle ultra-luxury market is not merely a wealth transfer from consumers to the brokerage. Under Chicago School price theory, routing buyers through an internal network by restricting listing visibility creates a measurable deadweight loss to consumer welfare. Reduced buyer competition produces lower sale prices for sellers. Suppressed price discovery prevents efficient allocation of housing capital. Fewer competing offers compress the quality of transaction terms available to both parties. The private exclusive mechanism does not redistribute value—the mechanism destroys value by eliminating the competitive process that generates it. Framing the enforcement theory around deadweight loss rather than transfer shifts the private exclusive model from a “premium revenue strategy” (Compass’s investor characterization) to a structural antitrust violation with quantifiable consumer harm—the distinction that separates a business dispute from an enforcement priority.

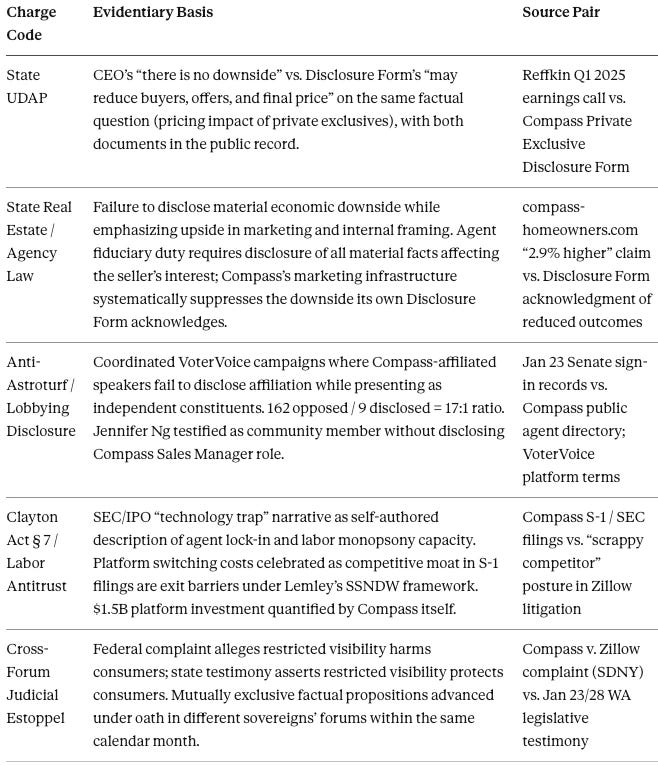

Enforcement Charge Code Map

The following consolidates the specific legal hooks available across the cross-forum record into a single reference. Each charge code maps to a documented contradiction, a public-record source pair, and the enforcement authority best positioned to act.

For Opposing Counsel

The forward lock operates as follows: if Compass maintains its federal complaint’s claim that restricted visibility harms consumers, then every concurrent marketing bill remedies that harm and Compass cannot oppose them without contradicting its own pleadings. If Compass abandons the claim to preserve legislative flexibility, it undermines its antitrust standing against Zillow. Neither path is available without concession. The cross-forum contradiction matrix converts every future Compass argument into a source of impeachment material from a different forum.

IX. Cross-Forum Impeachment Playbook

The contradiction matrix produces four ready-to-use impeachment sequences. Each follows the same structure: establish the witness’s own statement in Forum A, introduce the contradicting statement from Forum B, and force a choice. These scripts are designed for depositions, committee hearings, and AG enforcement interviews. Each question sequence is self-contained and requires no additional foundation beyond documents already in the public record.

A. Federal vs. State: Restricted Visibility

Q1: “In your federal complaint against Zillow, Compass alleges that restricted listing visibility harms consumers and forecloses competition. Do you stand by that allegation?”

Q2: “In January 2026, Compass testified before the Washington State Legislature that restricted listing visibility is benign seller choice that protects privacy. Do you stand by that testimony?”

Q3: “Which statement is accurate? On what date did the other become inaccurate?”

Effect: Affirming Q1 concedes that SB 6091 remedies the harm Compass identified. Affirming Q2 destroys the federal complaint’s standing. No third option exists.

B. Investor vs. Client: Pricing Impact

Q1: “In your Q1 2025 earnings call, you told investors ‘there is no downside’ to private exclusive marketing. Is that statement accurate?”

Q2: “Your client Disclosure Form warns that private exclusive marketing ‘may reduce the number of potential buyers,’ ‘may reduce the number of offers,’ and may reduce ‘the final sale price.’ Is that disclosure accurate?”

Q3: “Which of those statements is accurate, and on what date did the other become inaccurate?”

Effect: Affirming Q1 means the Disclosure Form’s warnings are false, exposing Compass to securities and client-protection liability for requiring clients to sign a misleading document. Affirming Q2 means the CEO misled investors. Both documents are in the public record and require no discovery to obtain.

C. Redfin Self-Correction Reversal

Q1: “In the January 2026 Washington hearings, Compass argued that legislation was unnecessary because the market was self-correcting. Redfin’s pledge to ban pre-marketed listings was cited as evidence. Is that accurate?”

Q2: “On February 26, 2026, Compass entered a three-year partnership with Redfin to distribute Coming Soon and Private Exclusive listings to 60 million monthly visitors, with all leads routed to Compass agents. Is that accurate?”

Q3: “How does a three-year contract to expand the distribution of private exclusives constitute market self-correction toward transparency?”

Effect: Destroys the self-correction defense with Compass’s own contract. The partnership press release is self-authenticating. No expert testimony required.

D. Technology Platform Lock-In vs. Scrappy Competitor

Q1: “Compass’s S-1 filing describes a proprietary platform with $1.5 billion in technology investment that creates ‘stickiness’ and switching costs for agents. Is that description accurate?”

Q2: “In your federal complaint against Zillow, Compass characterizes itself as a pro-competitive innovator fighting for open access against an entrenched monopolist. Is that characterization accurate?”

Q3: “Compass now controls 340,000 agents and 20%+ of the national residential market following the Anywhere acquisition. At what market share does a firm with $1.5 billion in platform lock-in stop being a scrappy competitor and start being the entrenched incumbent?”

Effect: Forces Compass to choose between the technology moat narrative (which sustains the stock price but creates antitrust liability) and the competitive underdog narrative (which sustains the litigation but destroys the investment thesis). The S-1 is a self-authenticating SEC filing that requires no discovery.

E. Agent Social Media vs. Legislative Testimony: The Skillman Exhibit

Q1: “In January 2026, Compass testified before the Washington Legislature that private exclusives protect homeowner privacy and safety. Is that an accurate characterization of Compass’s position?”

Q2: “On February 27, 2026, Moya Morgan Skillman—co-listing broker and co-buyer broker on the Mercer Island Exhibit Transaction—posted publicly that the Redfin partnership delivers ‘more exposure for your listings, more choices for your seller, and more direct buyer inquiries — on your terms,’ with ‘no days on market, no negative insights, and no home valuation estimates.’ Does that post describe homeowner privacy, or agent commission capture?”

Q3: “Ms. Skillman holds four role designations on a single MLS transaction—listing broker, buyer broker, co-listing broker, and co-buyer broker—under the same Compass team. She called the CEO ‘our fearless leader.’ Is the private exclusive model designed to protect consumers, or to route buyer inquiries into exactly this kind of dual-commission architecture?”

Q4: “Which audience received the accurate description of how this model works—the legislators, or the agents?”

Effect: The Skillman post is a self-authenticating public exhibit connecting the Mercer Island dual-commission transaction record, the Team Foster address suppression mechanism, and the Redfin national distribution partnership in a single document authored by a principal of the team. The post’s agent-facing language—“your listings,” “your seller,” “your terms,” “no negative insights”—eliminates every consumer-welfare filter Compass maintains in other forums. No discovery required. The exhibit is public, timestamped, and authored by someone whose MLS role designations are independently verifiable.

F. National MLS Proposal vs. Actual Conduct: The Twenty-Three-Day Collapse

Q1: “On February 3, 2026, at Inman Connect New York, your CEO stated—on video—that the ’theme of this year is not private listings, it’s how are we fighting to make private listings public.’ He then proposed a neutral national MLS with an independent board and equal brokerage ownership. Is that an accurate characterization of Compass’s position as of February 3?”

Q2: “At the time of that proposal, Compass was suing NWMLS in the Western District of Washington for enforcing MLS transparency rules, suing Zillow in the SDNY for requiring MLS submission, and your witnesses in Olympia were opposing SB 6091’s mandatory MLS concurrent marketing requirement. How does Compass reconcile advocating for a national MLS while litigating against and lobbying against the existing MLS transparency rules that a national MLS would presumably enforce?”

Q2: “Twenty-three days after declaring on video that the theme of 2026 ’is not private listings’ and proposing a neutral national MLS, your CEO told investors on the Q4 2025 earnings call: ‘I don’t see a scenario where the MLSs will continue to enforce these restrictive rules with Rocket and Redfin on our side because we now have more resources.’ Was the national MLS proposal a structural commitment, or a negotiating position that became unnecessary once the Redfin partnership provided an alternative distribution channel?”

Q4: “Your CEO stated Compass would have ‘no vote’ and ‘no disproportionate ownership’ in the proposed national MLS. Compass now controls 340,000 agents and over 700,000 listings through the Anywhere merger. Under what governance structure would the largest brokerage in the country exercise no disproportionate influence over a national listing database?”

Effect: The twenty-three-day timeline between proposal and abandonment is self-documenting. Q1 establishes the stated commitment. Q2 surfaces the simultaneous conduct that contradicts it. Q3 introduces the CEO’s own words replacing “neutral infrastructure” with “more resources”—the shift from governance framing to coercion framing, on the public record, in the CEO’s own voice. Q4 applies the market-structure arithmetic: 340,000 agents and 700,000 listings make the “no disproportionate ownership” claim structurally incredible regardless of formal governance design. The sequence demonstrates that Compass’s MLS advocacy, like its legislative testimony and federal litigation, adjusts to the audience and the moment rather than expressing a stable institutional commitment.

X. The Solvency Geometry

Every cross-forum contradiction ultimately reduces to one structural variable: the $1.6 billion Anywhere acquisition price and the debt it created. MindCast AI’s Three-Layer Acquisition Hierarchy decomposed that price into standalone brokerage value (Layer 1), scale synergies (Layer 2), and the private exclusive infrastructure premium (Layer 3)—estimated at $400–800 million. Layer 3 exists only if listings can be withheld from the open market long enough for an internal buyer to arrive first, capturing both commission sides.

The merger created the debt. The debt requires dual commissions. Dual commissions require the private exclusive window to remain open. Each state that closes that window tightens the financial constraint the merger itself created. The Redfin partnership confirmed the solvency geometry in Compass’s own press release—a three-year national platform deal anchored entirely on exclusive listing inventory, structured at zero cash cost because zero cash is what a firm carrying $2.6 billion in assumed debt can afford.

The behavioral paradox is what makes the geometry remarkable. Compass is not retrenching as the walls close. Compass is accelerating — launching new narrative positions across new forums at the exact moment when existing contradictions are converging from every direction. The Inman Connect national MLS proposal. The Q4 earnings call escalation from governance language to coercion language. The Redfin partnership. The compass-homeowners.com consumer campaign. The VoterVoice astroturf infrastructure. Each move opens a new front of contradiction while the existing fronts remain unresolved. And every move shares one structural feature: zero cash cost. The Redfin partnership is a three-year deal at zero cash. The national MLS proposal costs nothing but a conference stage. The VoterVoice campaigns cost negligible cash. The consumer website costs negligible cash. Compass funds its acceleration with narrative rather than capital — because narrative is the only currency a firm carrying $2.6 billion in debt and $2.2 billion in accumulated operating losses can deploy.

Shiller’s Narrative Economics documented this pattern across multiple asset classes: firms facing declining fundamentals do not retreat from narrative production — they escalate it, because the narrative is the asset. The story justifies the valuation. The valuation services the debt. The debt funds the story’s next iteration. When the cycle depends on audience segregation to prevent contradictions from surfacing, each new narrative play simultaneously sustains the cycle and accelerates its exposure. Compass is not funding operations with debt to service debt. Compass is funding stories with debt to service debt — and the stories are contradicting each other faster than the firm can segregate the audiences.

Shiller’s epidemic model predicts exactly what the solvency geometry produces: narratives that propagate in isolation remain locally stable, but when populations mix — when a federal court’s evidentiary record becomes visible to a state legislature, when an agent’s Facebook post reaches a committee staffer, when an earnings call transcript lands in an AG’s inbox — the contradicting strains collide and the contagion model breaks down. Shiller noted that “contagion is strongest when people feel a personal tie to an individual in or at the root of the story.” Skillman’s post works as evidence precisely because it is personal — a named agent, on a named team, delivering the commission capture framing directly to consumers without the vocabulary Compass deploys in every other forum. Reffkin’s post escalates the personal contagion to the CEO level — redefining “public” on camera while delegitimizing the enforcement infrastructure designed to prevent exactly the behavior the post celebrates. Both are narrative events in Shiller’s framework: moments where the internal stories Compass tells agents collided with the external stories Compass tells legislators, judges, and consumers. The collision is the evidence. The debt funds the next narrative. The next narrative funds the next collision.

Compass’s cross-forum contradictions are not rhetorical inconsistencies. They are the behavioral signature of a firm whose legal strategy and business model cannot occupy the same public record without collapsing each other. The contradictions persist because no single forum has had the complete picture. Assembled across forums, the record speaks for itself.

XI. Source Publications

The analysis in this essay draws on the following MindCast AI publications, all available at www.mindcast-ai.com:

The Compass Narrative Inversion Playbook (Feb 4, 2026)

How Compass’s State Legislative Testimony Undermined its Federal Antitrust Claims (Jan 31, 2026)

MindCast Testimony for WA House Hearing on SSB 6091 (Feb 18, 2026)

The Compass Commission Consolidation Strategy and Real Estate Marketing Transparency (Feb 19, 2026)

Nineteen Senators, Seventeen Questions: How Compass Bought Its Antitrust Clearance (Feb 20, 2026)

Death by a Thousand Depositions: Compass’s Multi-Vector Regulatory Collapse (Feb 21, 2026)

The Compass-Anywhere Address Suppression Calculus (Feb 22, 2026)

The Compass-Redfin Alliance: Market Self-Correction Is Dead (Feb 27, 2026)

State Power vs. Compass Private Exclusives: Legislative Testimony as a One-Way Gate (Feb 6, 2026)

Compass’s Technology Trap: How IPO Narrative Became Its Antitrust Liability (Jan 11, 2026)