MCAI Economics Vision: The Cybernetics of Compass Holdings' Narrative Control Architecture

Inventory Restriction, Commission Capture, and the Collapse of Audience Separation

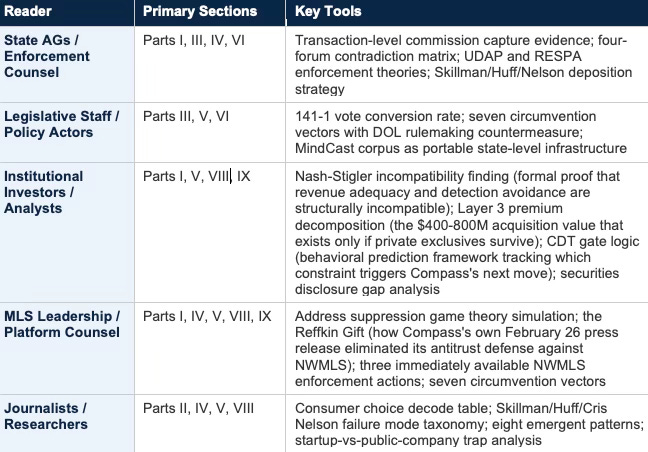

Primary series publications: The Compass Commission Consolidation Strategy and Real Estate Marketing Transparency | The Compass Narrative Inversion Playbook | Compass Cross-Forum Contradictions | Compass Consumer Choice Framing as a Control Mechanism

The publication is extensive. Upload the URL to any LLM, then prompt the AI system to ‘assess MindCast frameworks with degrees of cited sub links.’ Thereafter, upload any Compass news developments into the LLM chat to apply this publication’s frameworks. Compass news is now training data for your personal Compass behavioral economics + game theory simulator.

EXECUTIVE SUMMARY

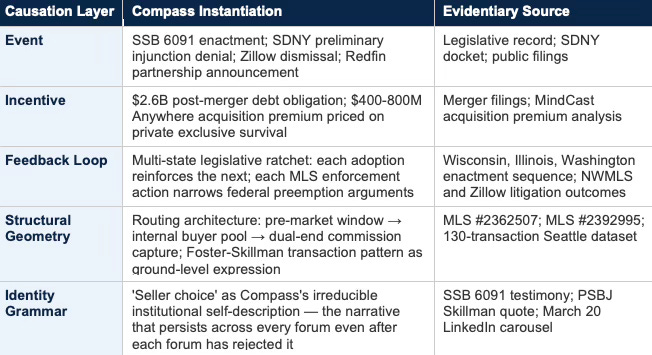

Compass Holdings is the largest residential real estate brokerage in the United States by agent count, with approximately 37,000 agents across 35 major markets following its January 2026 acquisition of Anywhere Real Estate — the parent company of Coldwell Banker, Century 21, and Sotheby’s International Realty. Compass’s core business model centers on capturing both the listing-side and buyer-side commission on luxury transactions — a dual-commission capture — by routing buyers through its internal agent network before the open market can compete. CEO Robert Reffkin has led the firm since its founding. Compass is publicly traded on Nasdaq (COMP) and carries approximately $2.6 billion in post-merger debt following the Anywhere acquisition, against a history of never having posted a full-year GAAP profit.

Washington State SSB 6091 — the Real Estate Marketing Transparency Act — passed both chambers of the Washington legislature on a combined 141-1 vote and was signed by Governor Ferguson on March 19, 2026. The law requires brokers to market residential properties concurrently to the general public through the MLS (Multiple Listing Service) from the moment any marketing begins, eliminating the pre-market window Compass’s commission capture model depends on. The Northwest MLS (NWMLS) is the primary MLS serving the greater Seattle region. Compass sued NWMLS in federal court in April 2025, alleging that its listing transparency rules constituted anticompetitive conduct, and filed a parallel lawsuit against Zillow — the dominant residential listing portal — in June 2025. Both suits were part of a coordinated strategy to protect the private exclusive model from platform and MLS enforcement simultaneously. The Zillow case was voluntarily dismissed on March 18, 2026 — the day before SSB 6091 was signed.

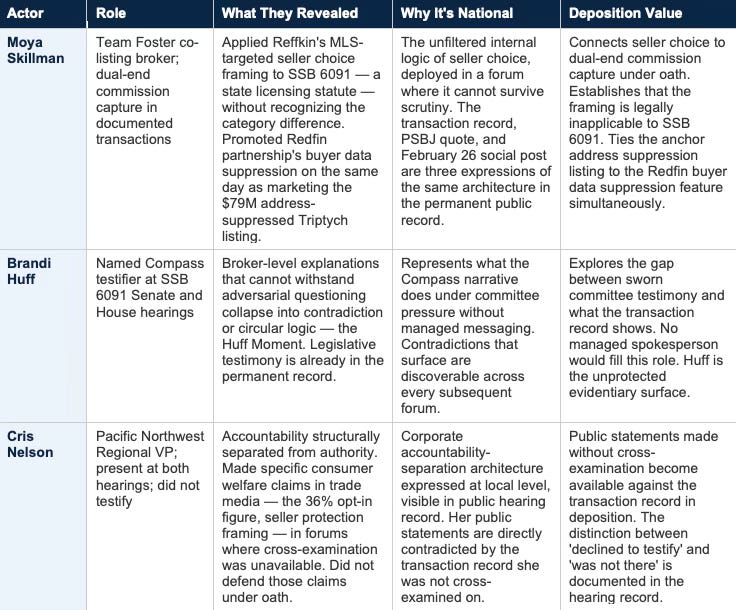

Three individuals whose conduct is central to this analysis appear throughout the document. Moya Skillman and Tere Foster co-lead Team Foster, a high-volume luxury brokerage team within the Compass network in Seattle whose transactions form the ground-level evidentiary core of MindCast’s transaction dataset. Brandi Huff is the Compass broker who served as the company’s named witness at both the January 23 and January 28, 2026 Washington State legislative hearings on SSB 6091. Cris Nelson is Compass’s Pacific Northwest Regional Vice President — the senior Compass executive present at both hearings — who was present but chose not to testify. All three are analyzed in depth in Part IV.

Four MindCast AI publications each isolate a different surface of the same underlying control architecture. Read individually, each piece identifies a mechanism, a language pattern, a forum strategy, or an evidentiary record. Read together, they reveal eight emergent patterns that no single publication establishes independently. Those patterns are the analytical contribution of this synthesis.

Compass operates a three-layer control system. Layer 1 is operational: restrict listing exposure through staged visibility, route buyer traffic through internal networks, and capture both commission sides when an in-house buyer arrives during the pre-market window. Layer 2 is linguistic: translate that restriction into consumer-facing language — seller choice, privacy, flexibility, innovation — so the constraint reads as empowerment. Layer 3 is institutional: calibrate the language by forum, so courts hear one account, legislatures hear another, investors hear a third, and consumers hear a fourth. The system holds as long as those audiences do not compare notes. They now are comparing notes.

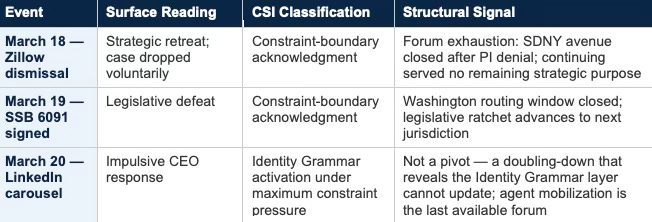

Three events in a 72-hour window collapsed the audience separation the architecture requires. On March 18, 2026, Compass voluntarily dismissed its antitrust lawsuit against Zillow — one day before Governor Ferguson signed SSB 6091, Washington State’s real estate marketing transparency statute, into law. On March 20, CEO Robert Reffkin published a LinkedIn carousel invoking fiduciary duty language against the statute he had just failed to block, pledging to dismantle ‘any system that stands in the way.’ All three forums — federal court, state legislature, social media — now feed a single evidentiary corpus. MindCast’s four prior publications tracked the architecture in real time as each contradiction compounded. This document names the patterns, connects the mechanisms, and builds the runtime decode infrastructure for interpreting whatever Compass does next.

Eight patterns surface through cross-corpus analysis that no individual publication establishes independently:

The Debt-Narrative Correlation. Compass’s rhetorical intensity tracks balance-sheet constraints, not market conditions. The $2.6B debt assumed through the Anywhere Real Estate acquisition converted private exclusive revenue into a solvency mechanism. Narrative escalation — including the March 20 fiduciary duty inversion — marks the sequential exhaustion of forums as each closes.

The Self-Disclosure Trap. Compass’s most damaging evidence is self-generated. The client Disclosure Form, the CEO’s public statements, the federal antitrust complaint filed in the Southern District of New York (SDNY), and the Q4 earnings guidance make mutually exclusive factual claims about the same business practice. The exposure under Unfair and Deceptive Acts and Practices (UDAP) statutes requires no investigation — only compilation.

The Astroturf Coefficient. The 17:1 undisclosed-to-disclosed affiliation ratio in Washington SSB 6091 testimony reflects deliberate apparatus design, not compliance failure. Compass operated coordinated lobbying infrastructure — including pre-drafted agent messaging campaigns and a consumer-facing website framing inventory restriction as homeowner freedom — to manufacture the appearance of independent opposition. Every future deployment of this infrastructure now carries the documented prior record.

The Structural Ratchet. Each state adopting concurrent marketing requirements reinforces the ‘clearly articulated state policy’ standard, compounds the cross-forum evidentiary corpus, and narrows Compass’s federal preemption arguments. Wisconsin, Illinois, and Washington are the leading edge of a compounding cascade, not isolated actions.

Timing as Strategic Signal. The March 18 Zillow dismissal, March 19 SSB 6091 signing, and March 20 LinkedIn carousel reflect a pre-sequenced escalation architecture. Future Compass moves can be anticipated by mapping which forums remain open and which debt-service constraints are binding.

The Public Company Trap. Compass communicates like a startup defending a pre-revenue thesis — in the legal and financial context of a post-IPO, post-acquisition, debt-loaded public company. Startup narrative discipline earns the benefit of the doubt before capitalization. Deployed after a $1.6B acquisition and $2.6B in debt obligations, the same language generates party admissions under Federal Rule of Evidence 801(d)(2) and UDAP exposure. Reffkin is applying founder discipline in a post-IPO evidentiary environment. The March 20 carousel is the clearest expression of that mismatch in the permanent record.

The Agent as Enforcement Vector. Individual agents operating the routing architecture face the same UDAP, fiduciary, and licensing exposure as the firm — without Compass’s legal resources. The March 20 carousel directed enforcement-cost risk toward agents rather than absorbing it at the corporate level. Compass captures the revenue upside of the architecture; agents absorb the compliance downside. The point at which agents recognize that dynamic and modify their behavior is an additional gate condition for the CDT — the Cognitive Digital Twin behavioral model used in Part VIII to predict Compass’s next institutional moves.

The Local Forum as Behavioral Baseline. Moya Skillman (Team Foster luxury broker), Brandi Huff (Compass’s named SSB 6091 legislative witness), and Cris Nelson (Compass’s Pacific Northwest Regional VP) were local actors in a regional legislative fight — not national strategists managing enterprise exposure. That context is precisely what makes them analytically valuable: the Washington record captures the Compass institutional system operating without its managed messaging layer. The same apparatus, seller choice framing, and accountability-separation architecture will appear in every state advancing concurrent marketing legislation. Their depositions in Compass v. NWMLS carry specific strategic value. MindCast’s analytical corpus — built before SSB 6091 passed, timestamped throughout — is the ready infrastructure for every state that follows.

The document closes with a CDT Foresight Simulation applying the MindCast cybernetics suite to Reffkin as a modeled decision system (Part VIII), testable predictions with gate logic (Part IX), and a full one-degree citation map (Part VII).

CORE THESIS

Compass operates a unified control strategy that only appears inconsistent when each forum is read in isolation. Cross-forum analysis reveals coherence: inventory restriction, buyer-pathway control, and narrative variation function as a single system designed to preserve commission capture, internal routing, and premium valuation positioning under increasing regulatory constraint. Language does not describe the system. Language protects it.

I. The Mechanism — Inventory Restriction as Revenue Architecture

The Compass Commission Consolidation Strategy and Real Estate Marketing Transparency documents the operational foundation of the firm’s entire strategic architecture. Restricted listing exposure is not a consumer feature. Restricted listing exposure is the revenue mechanism.

The 3-Phase Marketing Strategy — Private Exclusive, Coming Soon, MLS — stages information access to constrain the buyer pool to Compass-connected agents during the pre-market window. An internal buyer arriving before the open market competes eliminates the bid competition that price discovery requires. When the listing agent also represents that buyer, both commission sides consolidate.

The NAR commission bundling settlement, finalized in 2024, is the upstream structural event that changed the environment in which this mechanism now operates — and that the document record does not adequately account for. The settlement disaggregated buyer-side commission from the listing process in a way that made dual-end capture more visible and more legally contestable than it had been under the prior bundled structure. Before the settlement, industry-wide commission bundling obscured the buyer-routing economics: the buyer-side commission was embedded in the transaction architecture in a way that made its capture less legible to sellers, buyers, and regulators. After the settlement, every transaction where Compass represents both sides is more visibly a conflict of interest — the buyer-side commission is no longer structurally hidden, and its capture by the same agent who represents the seller is more readily identifiable as a dual-representation problem. The settlement did not create the Compass routing architecture. It stripped away the industry-wide bundling that previously made the problem harder to see, observe, and quantify. That context makes the Washington ultra-luxury transaction dataset — 16 of 130 transactions with commission flows remaining inside Compass — more significant as an evidentiary instrument than it would have been before the settlement, not less.

The Transaction Record

MindCast’s analysis of 130 Seattle-region ultra-luxury transactions over 13 months produced a precise quantification:

16 of 130 transactions produced commission flows that remained entirely inside the combined Compass-Anywhere entity

8 were confirmed dual-end captures — Compass represented both buyer and seller

8 additional cross-brand transactions became internal revenue the moment the merger closed, with no agent behavior change required

Total: $167.5M in transaction value; $4.2M in captured buyer-side commission from one metro market’s monthly top-10 record alone

Scaled across Compass’s 35 major markets, the same mechanism implies $600M to $1.5B of the Anywhere acquisition premium depends on one operating condition: listings can be withheld from the open market long enough for an internal buyer to arrive first. Concurrent marketing requirements eliminate that condition. That arithmetic explains every subsequent Compass institutional action — legislative, litigational, and narrative.

The Foster-Skillman Architecture — Mechanism at the Transaction Level

The Seattle ultra-luxury dataset is not an abstraction. The routing architecture operates through named agents on documented transactions. Team Foster — Tere Foster and Moya Skillman, operating within the Compass network — represents the mechanism at its most legible: the same agents appearing as both listing broker and buyer broker across repeated high-value transactions, capturing both commission sides on listings that circulated internally before reaching the open market.

Two anchor transactions define the evidentiary core. MLS #2362507 — a $15M Mercer Island property — produced a dual-end capture in which Tere Foster and Moya Skillman represented both the seller and the buyer, consolidating the full commission inside the same team. MLS #2392995 — the $79M Triptych estate, listed on the Team Foster website as ‘Call for Address’ — withheld the property address entirely, requiring any prospective buyer to contact Compass first. The address suppression is not a privacy feature. It is a funnel. Every buyer who wants to know where the property is must route through Compass to find out, positioning Compass to capture the buyer-side commission before any outside agent can establish a relationship.

The same Moya Skillman who operates this architecture at the transaction level is the Moya Skillman who applied Reffkin’s ‘seller choice’ framing to SSB 6091 in the Puget Sound Business Journal. The connection is not incidental. An agent whose compensation depends on the pre-market routing window has a direct financial stake in the narrative that protects it. The Skillman Moment in Part IV is not merely a messaging error — it is the point at which the agent operating the mechanism publicly deploys the language designed to protect it, in a forum where the mechanism’s transaction record is already documented. The quote and the transaction are the same system, visible from two different angles.

A third data point completes the evidentiary picture. On February 26, 2026 — the same day Compass issued its Redfin partnership press release framing the arrangement as a seller-choice initiative — Skillman posted the announcement to her public social network with this framing: ‘More direct buyer inquiries — on your terms. No days on market. No price drop history. No negative insights.’ That framing is analytically precise in a way the corporate press release is not. Sellers seeking maximum competitive exposure do not need to be told their listing will display without negative insights. Agents seeking to control buyer information do. On the same day, Skillman posted content marketing for the $79M Lake Washington estate — MLS #2392995, the anchor suppression listing in the Address Suppression Calculus, the property catalogued in the NWMLS without a street address. The co-occurrence is not coincidental. The transaction record, the PSBJ quote, and the February 26 social post are three expressions of the same agent operating the same architecture and deploying the same language to protect it — across three different forums, on a documented timeline, in the permanent public record.

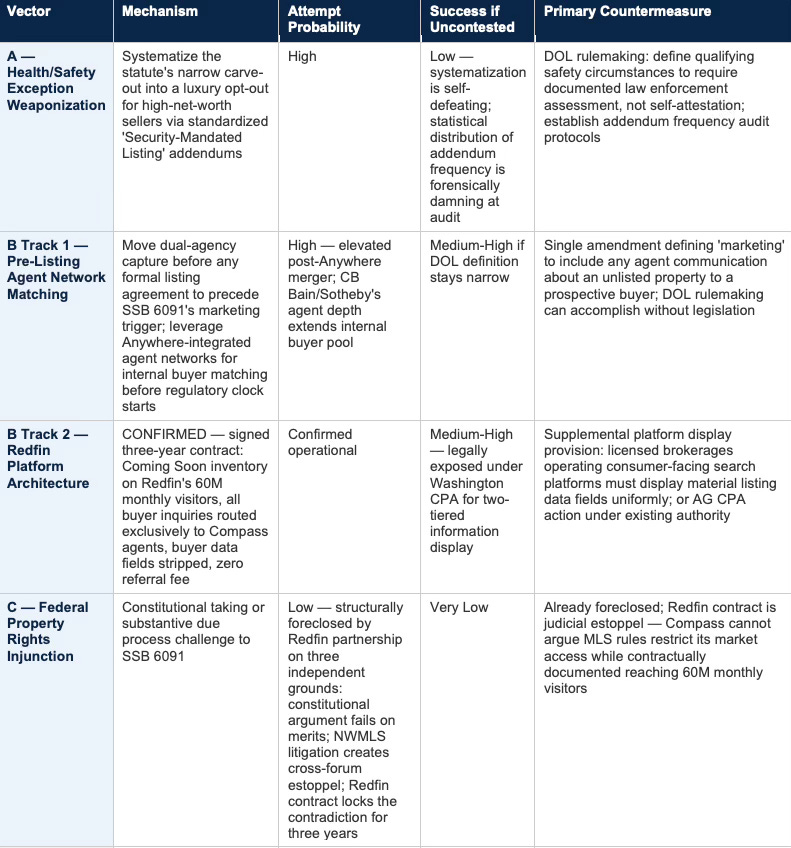

The address suppression practice carries a fair housing dimension that the transaction-level and antitrust analysis does not fully surface — and that state AGs with fair housing jurisdiction will find independently actionable. A listing withheld behind a ‘Call for Address’ requirement does not restrict access equally. Access depends on knowing which Compass agent to contact, which depends on having the social and professional network to identify that agent, which is itself a function of prior market participation, income level, and community connection. In a luxury market already stratified by network access, mandatory contact-first discovery is a structural filter on who participates in the buyer pool — before any showing, before any offer, before any price negotiation. The buyers who route through the filter are disproportionately those already connected to the Compass agent network. The buyers excluded from the pre-market window are disproportionately those without it. Whether that distribution produces a disparate impact on protected classes under the Fair Housing Act is a legal determination this document does not make. The question is worth raising in any jurisdiction where a state AG with fair housing authority is evaluating the routing architecture — because ‘Call for Address’ is not a neutral privacy feature. It is a gatekeeper mechanism whose gatekeeping effects follow the contours of existing network inequality.

The Anywhere Premium — A Locked Bet on Regulatory Outcomes

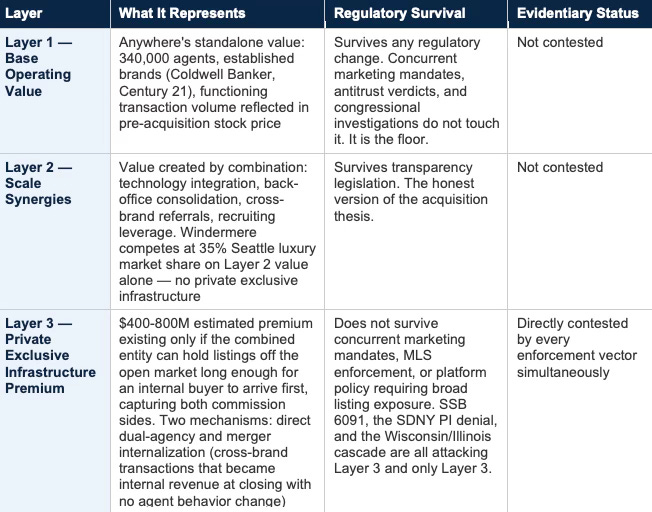

The January 2026 Anywhere Real Estate merger is the financial event that makes every subsequent Compass institutional action intelligible. Understanding the acquisition premium is not background context. It is the linchpin argument.

Compass acquired Anywhere at a valuation that priced in the continuation of private exclusive infrastructure. MindCast estimates $400-800M of the $1.6B acquisition premium exists only if the pre-market routing window survives — meaning listings can be withheld from broad market exposure long enough for internal Compass buyers to arrive first, producing the dual-end commission captures the transaction record documents. Remove that operating condition and the premium paid for Anywhere is not recoverable. The acquisition has already closed. The debt — estimated at $2.6B in post-merger obligations — is fixed. The revenue assumption underneath it is not.

That asymmetry is what makes buyer routing through private exclusives an existential question rather than a strategic preference. A brokerage that prefers internal routing but can survive without it behaves differently from a brokerage that acquired $1.6B in assets on the assumption that the routing infrastructure would remain intact. Compass is the second type. Every SSB 6091-style statute, every MLS enforcement action, every platform policy requiring concurrent listing exposure is not merely a competitive inconvenience — it is retroactively repricing a transaction Compass cannot unwind. The pressure is not prospective. It is compounding against a fixed liability.

This is why the legislative, litigational, and narrative responses to transparency requirements have the character they do. Compass sued NWMLS and Zillow simultaneously. It deployed a coordinated three-tier opposition apparatus at SSB 6091 hearings with a 17:1 undisclosed affiliation ratio. It announced the Redfin exclusive partnership — routing private inventory around MLS infrastructure entirely — on the same day it told investors it would overpower MLS enforcement through superior resources. These are not the actions of a firm defending a preferred business model. They are the actions of a firm defending the revenue assumption embedded in a closed acquisition at a fixed price against a debt load that does not flex.

THE REPRICING LOGIC

Each state that enacts a no-opt-out concurrent marketing requirement closes a piece of the conversion frontier that justified the Anywhere acquisition premium. Wisconsin, Illinois, and Washington have already moved. The cascade compounds: each adoption creates a discoverable legislative record that the next state’s drafters cite, each MLS enforcement action narrows the federal preemption arguments Compass relies on, and each judicial ruling against Compass’s exclusivity positions — including the SDNY preliminary injunction denial — removes a pillar of the legal architecture the premium assumed would hold. The debt is fixed. The pillars are not.

The Foster-Skillman transaction architecture is the ground-level expression of this premium dependency. MLS #2362507 and MLS #2392995 are not isolated data points — they are the mechanism operating at the individual transaction level that, aggregated across 35 major markets and 37,000 agents, produces the revenue numbers the Anywhere acquisition premium assumed. When Moya Skillman applies ‘seller choice’ language to SSB 6091 in the Puget Sound Business Journal, she is not making an abstract policy argument. She is an agent whose compensation depends on the routing window defending the regulatory condition that makes the architecture work — in a forum where the transaction record behind that defense is already in the public domain.

The Address Suppression Calculus — Nash-Stigler Incompatibility

The Compass-Anywhere Address Suppression Calculus provides the formal proof that the Anywhere premium was structurally unrecoverable through address suppression alone — independent of any regulatory action. The publication constructs a full Nash-Stigler game theory simulation using the 130-transaction Seattle dataset and a single optimization problem: at what price threshold should the combined entity deploy address suppression across its 54-listing portfolio to maximize dual-commission capture while remaining below the detection threshold that triggers NWMLS enforcement, competitor complaints, and regulatory scrutiny?

The Dual Nash-Stigler Equilibrium Architecture | The Stigler Equilibrium- Regulatory Capture and the Structure of Free Markets

The finding is unambiguous: no such threshold exists. Revenue adequacy and detection avoidance are structurally incompatible objectives across every price tier modeled. The simulation’s core logic runs as follows. Of the 54 Compass-controlled listings in the Seattle dataset, independent brokerages captured the buyer side on 32 — $281.4M in transaction value, representing $7.04M in buyer-side commission that left the combined entity’s network. Address suppression targets that $7.04M. Full-portfolio deployment across all 54 listings generates the maximum conversion opportunity but immediately exceeds the Nash-Stigler detection threshold — the Stigler boundary at which the evidentiary record becomes sufficient for NWMLS enforcement, competing brokers, and regulators to act without additional investigation. Concentrating deployment at $20M and above, where privacy framing remains credible, compresses recoverable revenue to approximately $500,000 per market annually from the sampled data.

THE NASH-STIGLER INCOMPATIBILITY FINDING

Scaled nationally under generous assumptions about comparable transaction density across Compass’s 35 major markets, full-portfolio address suppression produces a scenario-output range of $70-140M annually — stated explicitly in the publication as a scenario output, not a projection, given unverified assumptions about cross-market density. Against $2.6B in post-merger debt obligations, $70-140M is not debt service. It is noise. And it is only achievable at deployment volumes that immediately trigger institutional detection. The mechanism cannot simultaneously generate revenue at the scale the acquisition premium requires and avoid the detection level that activates enforcement. The Anywhere premium was not merely threatened by SSB 6091. It was arithmetically unrecoverable from the moment the merger closed.

The simulation also establishes why MLS #2392995 — the $79M Triptych estate listed as ‘Call for Address’ — operates at the precise price point where privacy framing remains credible. At $79M, the suppression is defensible as a seller preference for high-net-worth privacy. Below $20M, the same mechanism reads as straightforward buyer-pool restriction with no privacy rationale. The Triptych listing is not a random data point. It represents the upper end of the zone where detection avoidance and commission-capture motive can coexist without immediate institutional response. The simulation predicted that targeting precisely that zone was the rational deployment strategy. The MLS record confirmed it in real time.

The simulation’s Windermere finding carries a separate analytical value. Windermere appears most frequently among the independent brokerages capturing buyer-side commissions on Compass-controlled listings — consistent with Windermere’s 35% Seattle luxury market share. Windermere competes entirely on Layer 2 value: service quality, agent talent, local market knowledge, and operational depth. No private exclusive infrastructure. No address suppression. No dual-end routing architecture. The Windermere contrast is not incidental context. It is the falsification of the claim that private exclusive infrastructure is necessary to compete in luxury markets. A firm with no routing architecture and no address suppression wins buyer-side commission on Compass-controlled listings at the highest frequency in the dataset.

II. The Language Layer — Consumer Choice as Control Architecture

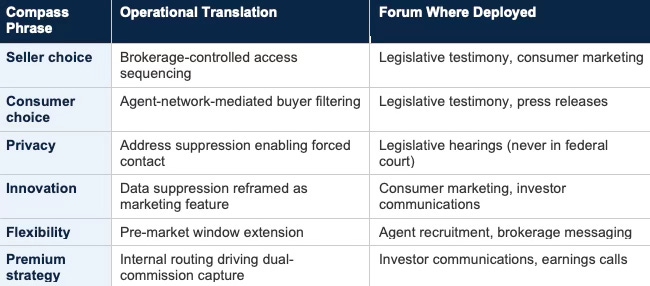

Consumer choice, seller choice, privacy, flexibility, innovation. Compass Consumer Choice Framing as a Control Mechanism establishes that these phrases are not descriptions of consumer welfare positions. They are load-bearing translation infrastructure that converts a revenue-extraction mechanism into a public-interest narrative.

The Two Definitions of Consumer Choice

Two structurally incompatible definitions compete in every Compass communication:

THE ASYMMETRY

When a seller ‘chooses’ private exposure under Compass’s model, buyers have no corresponding choice to see the listing. The asymmetry is not incidental. It is the architecture. Compass collapses this distinction — treating a seller’s choice of marketing strategy as equivalent to a buyer’s ability to access all publicly marketed options.

The Decode Function

Compass’s consumer-choice vocabulary operates as a translation layer across four functional categories. Each phrase serves the same underlying objective: keeping the pre-market window open long enough for a Compass-connected buyer to arrive before the open market competes.

The March 20 Escalation

Reffkin’s LinkedIn carousel, published the morning after Governor Ferguson signed SSB 6091, introduced three analytically new moves: enforcement-cost mobilization directed at individual agents, a fiduciary duty inversion deploying agency law language against MLS enforcement obligations, and a dismantling pledge with no carve-out for statutory mandates.

Every statement in the carousel is a party admission under FRE 801(d)(2), published in the most permissive deployment forum in the record — no discovery, no cross-examination, no institutional gatekeeping. The March 20 carousel is the most legally exposed cluster in the permanent Compass record.

III. The Forum Strategy — Narrative Inversion and Audience Calibration

The Compass Narrative Inversion Playbook establishes the structural architecture: Compass does not maintain a single description of its conduct. Messaging shifts across forums based on evidentiary pressure and audience incentives. Each forum receives the version of reality that optimizes for that forum’s decision-makers.

The Four-Forum Contradiction Matrix

THE CORE CONTRADICTION

Restricted visibility either harms consumers (as Compass pleads in SDNY) or protects consumers (as Compass testified in Olympia). Private exclusives either require regulatory protection because they serve sellers (legislative argument) or require antitrust relief because competitors suppress them (litigation argument). No two of these positions can coexist without contradiction.

The Three-Tier Opposition Apparatus

Compass’s legislative engagement operates through a documented infrastructure designed to manufacture the appearance of independent consumer concern. MindCast analysis of SSB 6091 opposition testimony documented:

162 individuals affiliated with Compass submitted opposition

Only 9 disclosed that affiliation — a 17:1 undisclosed-to-disclosed ratio

VoterVoice campaigns provided pre-drafted messaging and collected agent mobile numbers for coordinated activation

compass-homeowners.com framed inventory sequestration as ‘Your Home. Your Choice. Your Freedom.’

The site’s claimed 2.9% price premium compares Compass listings to other Compass listings — not to the broader market — and disclaims that ‘correlation does not necessarily equal causation’

The vote outcome measures the apparatus’s actual persuasive conversion rate. SSB 6091 passed the Washington legislature on a combined 141-1 vote — 49-0 in the Senate, 92-1 in the House. The opposition apparatus — 162 coordinated witnesses, pre-drafted messaging infrastructure, a consumer-facing website, a regional vice president in the hearing room — produced exactly one opposing vote across both chambers of a closely divided legislature, a 162:1 witness-to-vote ratio that is itself a documented policy outcome. In a chamber where partisan coalitions routinely fracture on land use, housing, and consumer protection issues, a 141-1 result means Compass’s arguments found no traction with any member of either party, in either chamber.

That conversion rate travels to every subsequent state. The record available to future legislatures is not merely that Compass opposed the bill. It is that Compass deployed a large, coordinated, substantially undisclosed opposition apparatus and failed to persuade a single member of the opposing party — and only one member of any party — across the entire bicameral process. The apparatus generated noise at scale. The vote quantified exactly how much signal it produced.

The Inman Contradiction — 23 Days

The national MLS proposal timeline sharpens every forum contradiction simultaneously. On February 3, 2026, Reffkin declared at Inman Connect New York: ‘Theme of this year is not private listings, it’s how are we fighting to make private listings public.’ He proposed a neutral national listing database with no Compass vote, no disproportionate ownership, and an independent board.

On February 26 — 23 days later — Reffkin told investors that with Rocket and Redfin aligned, ‘I don’t see a scenario where the MLSs will continue to enforce these restrictive rules with Rocket and Redfin on our side because we now have more resources.’ The framing shifted from neutral infrastructure to resource-based coercion in three weeks. The Compass-Redfin exclusive partnership was signed the same day. A firm that proposes neutral infrastructure on February 3 and announces it will overpower existing MLSs through resources on February 26 has disclosed, on the public record, that the February 3 proposal was a negotiating position, not a structural commitment.

The Redfin Partnership as Antitrust Self-Incrimination

The Redfin exclusive partnership is not merely a forum contradiction — it is self-incriminating on the specific antitrust theory Compass was advancing in federal court. Compass’s SDNY complaint argued that Zillow’s listing visibility requirements constitute anticompetitive exclusionary conduct: requiring listings to appear on an open, multi-party platform as a condition of access was, in Compass’s framing, an illegal restriction on competition. The Redfin partnership, signed 23 days after Reffkin’s neutral infrastructure speech, routes Compass private exclusive and Coming Soon inventory through a single competing portal under an exclusive three-year arrangement — precisely the structure Compass characterized as anticompetitive when Zillow was the beneficiary.

The legal exposure compounds further. If restricting listing visibility to a single platform is exclusionary conduct when a dominant portal requires it, the same structural analysis applies when a dominant brokerage does it. Compass’s own complaint language — drafted by counsel, filed under penalty of Rule 11 — is now available as a template for characterizing the Redfin arrangement. The arguments Compass made against Zillow’s listing requirements are directly portable against Compass’s own exclusive routing deal. Compass did not just contradict its legislative testimony with the Redfin partnership. It handed every MLS, every competing portal, and every state AG a ready-made antitrust theory written in Compass’s own words.

Contact mcai@mindcast-ai.com to partner with us on Predictive Cognitive AI in Law and Behavioral Economics. To deep dive on MindCast work in Cybernetic Foresight Simulations upload the URL of this publication into any LLM and prompt ‘reconstruct MindCast framework with three degrees of cited sub links.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure.

Recent projects: The Power Stack Series— How Energy Infrastructure Became the New AI Battleground | MindCast AI Emergent Game Theory Frameworks | MindCast AI Field-Geometry Reasoning | MindCast AI Installed Cognitive Grammar | Runtime Geometry, A Framework for Predictive Institutional Economics | Super Bowl LX — AI Simulation vs. Reality | The Runtime Causation Arbitration Directive | Google’s Deep-Thinking Ratio Measures Effort, Not Structure | MindCast AI Constraint Geometry and Institutional Field Dynamics | Double-Sided Rational Ignorance, How Platform Intermediaries Monetize the Measurement Gap | Executive Summary of MindCast AI Investment Series

IV. The Instability Condition — Narrative Collision and Detection Events

Compass’s control architecture depends on audience separation. Each forum must receive its calibrated narrative without comparing notes with the others. Compass Cross-Forum Contradictions identifies the structural vulnerability: Washington legislative hearings, federal court records, investor disclosures, and press records now constitute a unified evidentiary corpus that forces cross-forum comparison.

Robert Shiller’s Narrative Economics framework grounds the analysis. A narrative-dependent firm that tells incompatible stories to segregated audiences creates its own impeachment record the moment those audiences compare notes. Compass is experiencing narrative collision across every forum simultaneously, in a 42-day window, with each forum’s evidentiary record feeding the others.

The Detection Taxonomy — Three Failure Mode Categories

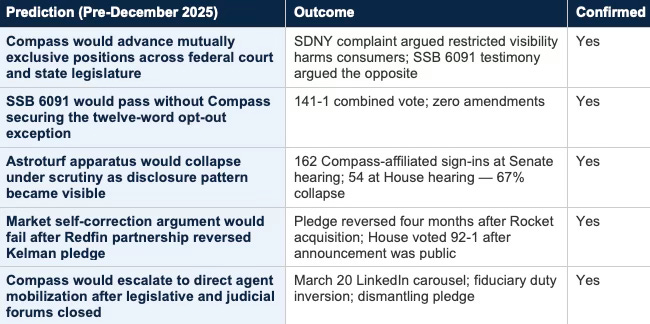

The MindCast Prediction Record — CDT Validation

The December 2025 CDT model assigned Compass a Behavioral Drift Factor of 0.81 — indicating systematic deviation between stated intent and actual conduct — and a Contradiction Tolerance Coefficient of 1.62 — indicating Compass generates contradictions faster than any single forum can absorb. The following outcomes confirm the model against published timestamps:

The Astroturf collapse warrants specific attention as a measurable policy outcome. The 67% drop — from 162 affiliated sign-ins at the January 23 Senate hearing to 54 at the House hearing — reflects the disclosure pattern becoming visible to committee staff and bill sponsors as the record accumulated. The apparatus did not become less active. It became less effective as the prior record traveled with it. Every future deployment now carries the Washington record as context.

The Redfin deal’s zero-cash structure is the definitive debt-constraint diagnostic. A firm with strategic options writes a check. Compass traded listing inventory access for national distribution reach at zero cash cost because that is the only kind of deal available to a firm carrying $2.6B in debt that has never posted a full-year GAAP profit. The Redfin CEO’s April 2025 pledge to ban selectively pre-marketed listings reversed four months after Rocket’s acquisition. George Stigler wrote in 1971 that regulatory behavior tracks ownership, not stated mission. The mechanism confirmed in a press release. Any legislator in any subsequent state who invokes the market self-correction argument now must defend the proposition that a pledge reversing four months after a corporate acquisition represents ongoing voluntary market discipline.

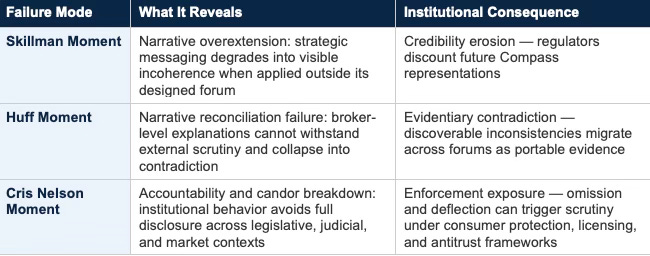

The Skillman Moment — Canonical Field Case

The Skillman Moment is the primary detection event in the MindCast Compass corpus. Moya Skillman’s Puget Sound Business Journal quote applies Reffkin’s MLS-targeted ‘seller choice’ framing to SSB 6091 — a state licensing statute — and in doing so exposes the precise boundary at which the frame ceases to function.

The category error is structural, not rhetorical. ‘Seller choice’ is a compliance argument calibrated to MLS governance: an internal rule structure where brokerages negotiate opt-in and opt-out windows, where enforcement is contractual, and where the relevant decision-maker is an industry body weighing member interests. MLS rules are discretionary instruments. Brokerages lobby against them, litigate around them, and negotiate carve-outs from them — as Compass was doing simultaneously in SDNY and in the Western District of Washington. That context is where ‘seller choice’ operates coherently. It addresses a forum whose outputs can be influenced.

SSB 6091 is categorically different. It is a state transparency statute enacted under the legislature’s police power, enforced through the Washington Department of Licensing, and backed by civil penalties and license sanctions. Noncompliance is not a matter of MLS membership consequences. Noncompliance is a licensing violation. Applying ‘seller choice’ to SSB 6091 does not engage the statute on its own terms — it imports a private governance argument into a public law forum where that argument has no operative meaning. A broker who tells a seller that ‘seller choice’ supersedes a statutory marketing obligation is not offering a legal defense. That broker is misrepresenting the law to a client.

THE ISOLATION PROBLEM

At the SSB 6091 hearings, no independent consumer group, housing advocacy organization, or unaffiliated industry body supported Compass’s seller choice narrative. The only voices advancing it were Compass representatives, Compass-affiliated agents, and Compass-funded opposition infrastructure. The 17:1 undisclosed affiliation ratio is not incidental context — it is the evidentiary record that Compass was a lone institutional actor manufacturing the appearance of broader constituency support. When a policy position attracts zero independent endorsement across two rounds of public hearings, the position is not a consumer welfare argument. It is a business interest dressed in consumer welfare language.

The isolation finding sharpens the Skillman Moment’s analytical value. Skillman’s PSBJ quote did not represent an industry consensus that legislators weighed and rejected. It represented Compass’s internal narrative, transmitted by a Compass broker, in a context where the transaction record behind the narrative — dual-end commission capture through pre-market routing — is fully documented. The quote holds internally: for agents operating inside the Compass incentive structure, ‘seller choice’ coherently describes why private exclusives serve their interests. The quote breaks externally: applied to a statutory mandate with licensing penalties, the frame does not engage the legal reality it is being used to resist.

The Skillman-to-Huff Bridge — When the Frame Cannot Answer the Question

The Skillman Moment identifies narrative overextension — the frame applied beyond the forum it was designed for. The Huff Moment identifies what happens next: when the overextended frame is pressed with a direct question it cannot answer without exposing the mechanism underneath.

The bridging question is simple and has never received a direct answer: Is the seller choice narrative related to Compass’s business interest in capturing double commissions through private exclusives?

The question cannot be answered honestly within the seller choice frame. Confirming the relationship collapses the consumer welfare argument — it converts ‘seller choice’ from a neutral preference principle into disclosed self-interest, which is a different and weaker position in both legislative and judicial forums. Denying the relationship contradicts the transaction record, the earnings guidance, the acquisition premium arithmetic, and Compass’s own Disclosure Form. Deflecting or reframing the question — which is what the Huff Moment documents — is itself behavioral evidence that the frame cannot survive adversarial scrutiny on its foundational premise.

THE STRUCTURAL EXPOSURE

A consumer welfare argument that cannot withstand a single direct question about the business interest it serves is not a consumer welfare argument. It is a business interest that has been translated into consumer welfare language for forum-specific deployment. The translation breaks down under cross-examination — and the breakdown is the Huff Moment.

The Cris Nelson Moment — Accountability Architecture in Practice

The detection taxonomy defines the Cris Nelson Moment as accountability and candor breakdown at the institutional level. The SSB 6091 hearing record provides its most precisely documented instantiation. Nelson, Compass’s Pacific Northwest Regional Vice President, was present at both the January 23 and January 28 hearings. Brandi Huff testified as Compass’s named representative at both. Nelson did not testify at either.

Presence without testimony in a public legislative proceeding is not absence. It is a documented strategic choice: maintain physical presence to monitor proceedings and signal institutional weight while avoiding the sworn testimonial record that creates personal accountability for specific factual representations. The representations were made — by Huff, by affiliated brokers, by the coordinated opposition apparatus — while Nelson preserved the executive buffer that keeps institutional leadership outside the direct evidentiary record. When those representations are tested in subsequent proceedings, Huff carries the exposure. Nelson’s conduct at the hearings is the Cris Nelson Moment made visible: the institutional behavior pattern in which accountability is structurally separated from authority.

For enforcement purposes, the distinction between ‘declined to testify’ and ‘was not there’ matters significantly. Nelson’s presence is documented in the hearing record. The decision not to testify while a subordinate made representations on the firm’s behalf is an institutional conduct choice, not an absence of knowledge. That record is available in any subsequent proceeding — deposition, regulatory investigation, or legislative inquiry — where the question of what Compass’s regional leadership knew, and when, becomes relevant.

The public record Nelson did generate outside the hearings makes the testimonial absence more analytically significant, not less. Nelson told RISMedia that Washington homeowners were ‘forced into a one-size-fits-all approach that can weaken their negotiating power’ — a direct consumer welfare claim about the harm SSB 6091 would cause. Nelson stated in a Compass press release that 36% of Seattle homeowners working with a Compass agent chose to pre-market their homes as a Private Exclusive — a demand-side representation used to argue that SSB 6091 restricts consumer choice. Both statements are specific, documented, and directly contradicted by the transaction record MindCast assembled: the same agents whose pre-market architecture Nelson was defending were capturing dual-end commissions in documented transactions where seller outcomes were constrained by the restricted buyer pool. Nelson made the consumer welfare claim in trade media where cross-examination is not available. Nelson declined to defend that claim under oath in the proceeding where cross-examination was available and the transaction record was in the record. That asymmetry is the Cris Nelson Moment at its most structurally precise.

The Zillow Litigation Arc — 268 Days, Zero Relief, Permanent Record

The Compass-Zillow antitrust litigation arc is the most analytically consequential element of the Compass forum record — 268 days, zero judicial relief, and millions in legal fees spent generating a federal evidentiary record now usable against Compass across every remaining forum simultaneously.

Compass filed its complaint against Zillow on June 23, 2025 — thirty-nine days after filing against NWMLS in the Western District of Washington. MindCast identified the 39-day interval at the time as evidence of coordinated strategic pressure rather than independent grievance, and characterized the venue fragmentation — a Seattle-based company suing in New York — as a deliberate mechanism to prevent any single court from evaluating the cumulative pattern. The prediction is confirmed by the dismissal arc: 268 days from filing to voluntary withdrawal, zero judicial relief obtained at any stage.

The Mandatory Injunction Classification — Compass Was Not Defending a Right

The most analytically significant holding in the Vargas opinion received almost no public attention: the court’s classification of Compass’s request as a mandatory injunction rather than a prohibitory one. A prohibitory injunction preserves the status quo. A mandatory injunction alters it, triggering the heightened ‘clear or substantial likelihood’ standard. Judge Vargas classified Compass’s request as mandatory because directing Zillow to accommodate Compass’s premarketing strategies would alter Zillow’s and Compass’s positions vis-à-vis each other — requiring Zillow to distribute listings on terms that had never previously existed between the parties.

The classification names precisely what Compass was doing. Compass was not defending a right it possessed. It was demanding a structural accommodation it had never had. The antitrust framing — Zillow as monopolist, Compass as excluded competitor — obscured that the relief sought was not restoration but compulsion. MindCast’s

Brief of MindCast AI LLC as Amicus Curiae in Support of Defendant Zillow had argued this directly before the hearing: ‘The requested injunction is the coordination harm.’ Compass sought to compel a high-integrity coordination actor to transmit inventory that deliberately bypassed coordination requirements. Judge Vargas reached the same conclusion through mandatory injunction doctrine. Because the court found no likelihood of success on the merits, it never reached the harm narrative. Compass’s entire public case — harm to sellers, harm to agents, harm to competition — was rendered procedurally irrelevant before it was weighed on substance.

Reffkin’s Sworn Testimony — The 94% Admission

The preliminary injunction hearing was not resolved on briefs alone. From November 18 to 21, 2025, Judge Vargas held a four-day evidentiary hearing at which Reffkin testified under oath. That testimony is now permanent federal record, and it contains the most significant self-incriminating admission in the entire Compass corpus.

Reffkin testified that 94 percent of listings using Compass’s 3-Phase Marketing Strategy proceed to the third phase — MLS submission and Zillow syndication. The number is not Zillow’s characterization. It is the CEO’s sworn description of his own model under cross-examination. The temporal arbitrage architecture Compass built — restricting buyer access during the pre-market window — terminates in Zillow distribution in 94 of every 100 cases by the CEO’s own account. The model required Zillow at the back end. Reffkin established that on the record. That sworn testimony is now available in every subsequent proceeding where the relationship between Compass’s private exclusive model and its claimed harm from Zillow’s platform policies is at issue.

Reffkin also testified to the Black Box structure on Compass.com — the front-page interface advertising Private Exclusives without specific listing details, requiring buyer contact with a Compass agent to access property information — and testified that Compass structured it specifically to avoid running afoul of NAR and MLS rules. The court found the Black Box violated Zillow’s Listing Access Standards. Compass built a mechanism to circumvent MLS transparency requirements, testified to that design on the record, and then argued the resulting enforcement was anticompetitive. The complaint’s Coming Soon phase description completed the picture: Compass’s own counsel characterized Phase 2 as launching listings ‘without displaying days on market, price drop history, or other negative insights.’ That language — in a sworn federal pleading — established that buyer data suppression was the feature, not a side effect. SSB 6091 subsequently codified the concurrent marketing trigger against exactly that conduct.

THE ARC AS SELF-GENERATED EVIDENTIARY RECORD

Compass spent approximately 268 days and millions in legal fees generating a federal evidentiary record that is now usable against it across every remaining forum. The Section 1 conspiracy theory was rejected on the merits — the court found Zillow and Redfin independently developed their policies. The Section 2 monopolization theory failed — multi-homing destroyed the network effects argument, Homes.com had grown from 2.4% to 19% audience share in four years, and Zillow’s share declined during the same period. The harm narrative was never evaluated because the legal theory collapsed first. What remained when Compass filed its voluntary dismissal on March 18, 2026 was not a strategic retreat. It was the permanent federal record of every position Compass advanced and every admission Reffkin made under oath — available without subpoena to every enforcement sovereign examining Compass, simultaneously, in real time.

Three Deals, Twenty Days — Industry Consensus Against Compass’s Architecture

Zillow, eXp, and Redfin–Compass: Three Deals, Twenty Days, One Outlier establishes a finding the antitrust analysis alone cannot: Compass’s routing architecture is not an industry norm that SSB 6091 disrupted. It is a structural outlier that major competitors voluntarily rejected in the same window Compass was defending it as essential.

The sequence: Compass-Redfin announced February 26. Zillow launched Zillow Preview on March 17 — partnering with Keller Williams, REMAX, HomeServices of America, Side, and United Real Estate — making coming-soon listings publicly visible on Zillow and Trulia before MLS active status with full buyer data intact and no internal routing requirement. eXp announced a pre-marketing syndication deal with Homes.com, Realtor.com, and ComeHome.com on March 18, on explicitly non-exclusive terms. CEO Leo Pareja stated the architecture directly: any portal may receive eXp listings on equal terms. All three send listings to consumer-facing platforms before MLS active status. The surface resemblance ends there.

The non-exclusivity clause in the eXp deal is the architectural diagnostic. The Compass-Redfin structure is built around exclusivity at the inquiry layer: all buyer inquiries route to Compass agents, buyer data fields are stripped, and the arrangement is locked in a signed three-year contract at zero cash cost to a firm that has never posted a full-year GAAP profit. eXp’s architecture produces the opposite outcome by design — any portal may receive listings on equal terms, no internal routing requirement, no stripped data fields. Both brokerages describe their deals in seller-benefit language. The non-exclusivity architecture reveals which framing the underlying contract supports.

Buyer Data Suppression — Posner, Friedman, and Market Structure Failure at Platform Scale

The Compass-Redfin contract strips three specific data fields from every Compass listing on Redfin’s platform: days on market, price drop history, and home valuation estimates. Neither Zillow Preview nor eXp’s deal strips any of these fields. Understanding why those three specific fields matter — and why their suppression across 60 million monthly Redfin users constitutes a market structure failure, not a consumer preference — requires the Chicago School analytical framework Zillow, eXp, and Redfin–Compass: Three Deals, Twenty Days, One Outlier applies directly.

Richard Posner’s consumer welfare standard evaluates challenged practices not by their procedural form but by their effect on total welfare across every party the transaction touches. Applied to the Redfin contract: the seller receives early Redfin exposure and a cleaner listing presentation. The buyer negotiates without DOM data, without price history, and without valuation estimates — three inputs that directly determine the buyer’s capacity to assess leverage and form an accurate bid. The informational asymmetry transfers economic value from the buyer to the brokerage, which benefits when a less-informed buyer pays above what competitive market information would have produced and captures both commission sides when an internal agent closes. The seller’s authorization does not make the buyer’s degraded position disappear. At platform scale across 60 million monthly visitors and 35 major markets over three years, what is a bilateral consent arrangement in a single transaction becomes a systemic market distortion that no individual buyer can detect or opt out of.

Milton Friedman’s price discovery framework makes the structural harm precise. DOM data, price drop history, and valuation estimates are not buyer amenities. They are price discovery mechanisms — the means by which dispersed information held by millions of market participants gets aggregated into transaction prices that accurately reflect underlying value. A property that sat 90 days and dropped $200,000 communicates the seller’s revealed willingness to accept less, the absence of competing demand, and the cost of a failed marketing cycle. Buyers who see that data bid differently. Markets where it circulates freely generate prices that reflect actual demand. Markets where it is selectively suppressed generate prices that reflect the information advantage of whoever controls the data field. Stripping those fields from buyer view on 60 million monthly user sessions does not merely harm individual buyers in individual transactions. It degrades the price discovery function the entire market depends on to generate accurate valuations — and the party that benefits from the degraded function is the brokerage that negotiated the suppression into the platform contract.

THE MARKET CONSENSUS SIGNAL

Realtor.com CEO Damian Eales described the eXp deal architecture in terms that directly indict the Compass-Redfin structure: ‘equal access for all buyers, not a subset selected by the listing agent.’ That statement was published on March 18, 2026 — the same day Compass dismissed the Zillow lawsuit. The industry consensus that emerged across twenty days — Zillow Preview, eXp non-exclusive syndication, Realtor.com’s public positioning — establishes that open distribution with full buyer data is the voluntary competitive norm Compass’s competitors are converging toward. Compass’s exclusive routing arrangement is not a market response to consumer demand. It is an outlier architecture whose outlier status is now documented by the voluntary choices of every major competing actor in the same twenty-day window.

The Streisand Topology — How Compass Filed SSB 6091 in Federal Court

The self-destruction sequence that produced SSB 6091 is the most analytically significant element of the entire Compass corpus — and the concept that unifies the litigation strategy, the legislative outcome, and the self-disclosure trap. The standard Streisand Effect is: attempting to suppress information causes wider dissemination. What Compass produced was structurally different and more damaging. Compass did not merely amplify awareness of private exclusives. Compass’s own elite antitrust counsel provided the legal and economic vocabulary for regulating them — with billable precision — and the Washington legislature applied it 141-1.

The mechanism unfolds in two phases. Phase One — the quiet loophole: Compass’s Private Exclusive network operated at the edge of existing MLS rules, generating dual-agency commission capture at higher rates than open-market transactions. Washington had no concurrent marketing mandate. The model relied on rule ambiguity and the absence of explicit statutory prohibition. Had Compass maintained that posture — operating quietly, resisting NWMLS enforcement through internal governance channels, avoiding public litigation — SSB 6091 almost certainly would not exist. A triggering event was required to unify the coalition that produced a 49-0 Senate vote. Compass provided one.

Phase Two — the Streisand Topology: in April 2025, Compass filed a federal antitrust complaint against NWMLS characterizing it as a monopolist weaponizing listing transparency rules against innovation. In June 2025, it filed a second complaint against Zillow. Both complaints were public documents, filed under oath, containing detailed consumer harm theories, market impact estimates, and scale characterizations of the private exclusive network’s effects. Every paragraph describing how restricted listing visibility harms consumers became primary source material for legislative staff, the Washington AG’s office, and SSB 6091’s drafters. Three specific definitional contributions from the two complaints map directly onto SSB 6091’s operative framework: the characterization of pre-MLS marketing as creating an exclusive buyer pool, the quantification of harm to buyers from restricted visibility, and the characterization of public marketing as triggering concurrent disclosure obligations. Washington’s drafters did not invent a regulatory framework. Compass filed one in federal court, and the legislature applied it.

THE COOPERATIVE INFRASTRUCTURE PROBLEM

The deeper structural error Compass failed to account for: the Private Exclusive model was built entirely on top of cooperative infrastructure Compass does not own and cannot replace. NWMLS membership is what gives every Compass agent access to the listing database, closed-sale comparables, and the buyer-side agent network that makes residential transactions function. The 340,000 agents absorbed through the Anywhere acquisition are productive precisely because they have NWMLS access — not because Compass built an independent market. The loophole existed only because NWMLS tolerated it. The moment Compass filed publicly, it forced NWMLS to choose between tolerating the loophole and defending its own governance authority in federal court. A cooperative institution facing a monopolization claim from a member it subsidizes has one rational response: eliminate the conduct the complaint describes.

For other states: Washington’s evidentiary record — the transaction data, the opposition modeling, the complaint text, and the Astroturf Coefficient — travels to every state that follows without needing to be regenerated. The Streisand Topology is now a documented template. Any dominant brokerage in any state that files federal antitrust complaints against its MLS is providing that state’s legislature with the vocabulary, evidence, and coalition infrastructure to pass its own SSB 6091. MindCast is prepared to export this analytical framework to any state advancing concurrent marketing legislation.

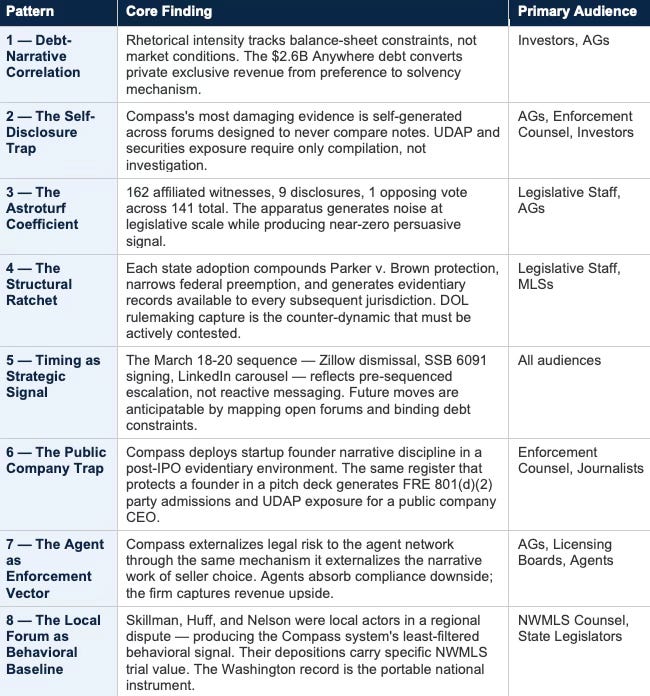

V. Emergent Patterns — What Cross-Corpus Analysis Reveals

The four primary publications, read individually, isolate discrete surfaces of the same structure. Read together, they reveal eight emergent patterns that no single publication establishes independently. These patterns are the analytical contribution of the umbrella synthesis.

Pattern 1: The Debt-Narrative Correlation

Compass’s rhetorical intensity does not correlate with market conditions or competitive pressure. It correlates with balance-sheet constraints. The $2.6B post-merger debt load created by the Anywhere acquisition converted private exclusive revenue from a strategic option into a solvency dependency. Narrative escalation tracks debt exposure: as each forum’s evidentiary record narrows Compass’s viable positions, messaging shifts to the next available forum with less developed counter-evidence. The March 20 LinkedIn carousel — deploying fiduciary duty language against a statutory mandate — represents the exhaustion of legislative, judicial, and investor forums and the turn to direct agent mobilization as the last viable narrative channel.

Pattern 2: The Self-Disclosure Trap

Compass’s most legally damaging evidence is self-generated. The client Disclosure Form acknowledges that private exclusive marketing ‘may reduce the number of potential buyers,’ ‘may reduce the number of offers,’ and may reduce ‘the final sale price.’ CEO Reffkin’s public statement: ‘There is no downside.’ The SDNY complaint argues restricted visibility harms consumers. Q4 earnings guidance describes private exclusives as a premium revenue strategy. Each document was produced in a forum where its audience would not encounter the others. Assembled, they constitute a UDAP exposure that requires no new investigation — only compilation. Compass produced its own impeachment record across audiences that were designed to never compare notes.

The same gap carries a securities disclosure dimension that the UDAP framing does not fully capture — and that the institutional investor audience will find directly relevant. If Compass’s public investor communications represented private exclusives as a durable premium revenue strategy driving superior market share and supporting the Anywhere acquisition premium, while the firm’s own client-facing Disclosure Form simultaneously acknowledged the practice may reduce sale prices and buyer pools, the question of whether the investor communications were materially accurate is a securities disclosure issue. The materiality threshold is whether a reasonable investor would consider the Disclosure Form language significant in evaluating the premium revenue thesis. Given that the premium revenue thesis is load-bearing for the $1.6B Anywhere acquisition valuation — and that $400-800M of that premium depends on the private exclusive window remaining open — the gap between the investor narrative and the client disclosure is not a technical inconsistency. It is a potential misrepresentation about the financial condition of the firm’s core revenue architecture to the investors who funded it.

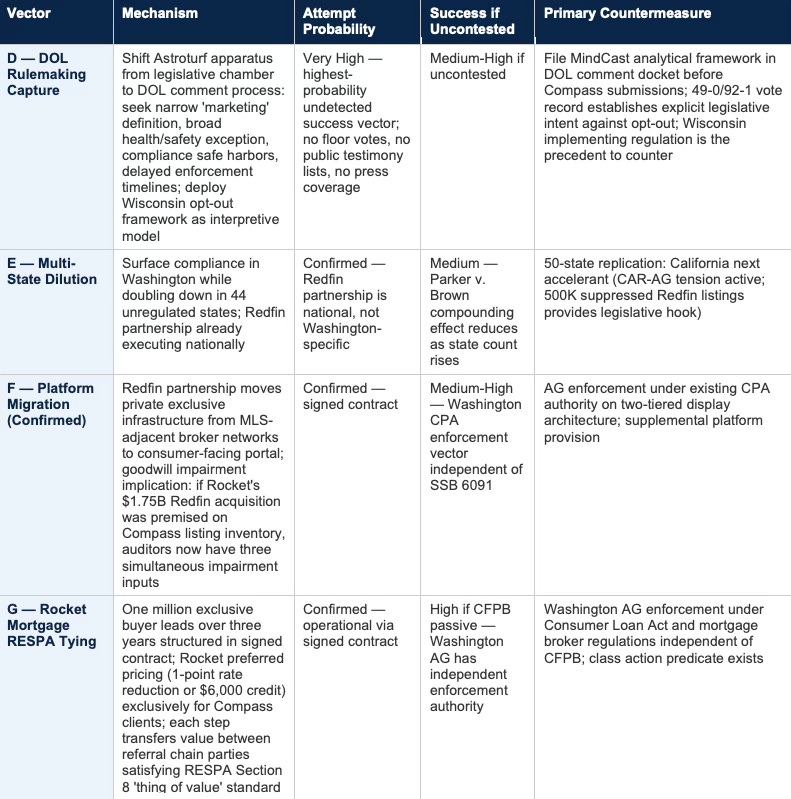

The Rocket-Compass-Redfin partnership adds a further securities dimension through the goodwill impairment question. If Rocket’s $1.75B acquisition of Redfin was premised on Compass’s listing inventory as the primary driver of partnership value, auditors testing goodwill assumptions now have three simultaneous evidentiary inputs: acquired Anywhere leadership skepticism timestamped on earnings calls, a signed three-year contract confirming the private exclusive mechanism is the strategic rationale, and a state legislative ratchet — with multi-state replication underway — eliminating the operating condition the goodwill premium requires. The impairment question is when, not whether. The Rocket Mortgage tying arrangement compounds this: one million exclusive buyer leads over three years, structured in a signed contract, with preferred Rocket Mortgage pricing exclusively for Compass clients — a structure satisfying RESPA Section 8’s ‘thing of value’ standard on its face. The Washington AG holds independent enforcement authority under the Consumer Loan Act without waiting for CFPB action.

Pattern 3: The Astroturf Coefficient

Compass’s legislative opposition infrastructure exhibits a documented coordination pattern: 162 affiliated individuals submitting opposition testimony with only 9 disclosing affiliation. The 17:1 undisclosed-to-disclosed ratio is not incidental — it reflects a deliberate apparatus design. VoterVoice provides pre-drafted messaging. compass-homeowners.com provides consumer-protective framing. Named brokers — Jennifer Ng testifying about seniors without disclosing her Compass Sales Manager role — provide the appearance of independent constituent concern. The apparatus manufactures the signal that grass-roots opposition is generating. When the affiliation architecture is documented, as it now is, every future deployment of the apparatus carries the prior record as context.

Pattern 4: The Structural Ratchet — Multi-State Cascade

Each state that adopts concurrent marketing requirements reinforces the ‘clearly articulated state policy’ standard, narrows Compass’s federal preemption arguments, and creates a new jurisdictional evidentiary record available to every subsequent legislature and enforcement body. Wisconsin enacted listing transparency restrictions in December 2025. Illinois reintroduced equivalent legislation in February 2026. Washington enacted SSB 6091. The cascade is not a trend. It is a structural ratchet: adoption reinforces adoption, each hearing generates permanently discoverable records, and the cross-forum contradiction matrix compounds with each new jurisdiction.

The ratchet has a counter-dynamic that the legislative record alone does not resolve: regulatory capture through administrative rulemaking. The same Astroturf apparatus that generated a 17:1 undisclosed affiliation ratio in the SSB 6091 hearings shifts to the DOL comment docket after each state’s bill passes — a proceeding generating no floor votes, no public testimony lists, and no press coverage. Wisconsin’s implementing regulations interpreted the opt-out language broadly, functionally preserving the pre-MLS window for any willing seller. Compass will deploy the Wisconsin framework as a model for interpretive guidance in every subsequent state, seeking narrow ‘marketing’ definitions and broad health/safety exception interpretations that restore the practical effect of the private exclusive window after the legislative fight is over. The structural ratchet only compounds if the administrative rulemaking vector is contested in each jurisdiction with the same analytical rigor that the legislative record was built with. The SSB 6091 record — timestamped, bicameral, 141-1 — is the template for every subsequent state’s DOL proceeding, but it must be actively deployed rather than assumed to travel automatically.

Pattern 5: Timing as Strategic Signal

Compass’s major institutional actions cluster in ways that reveal strategic rather than reactive decision-making. The Zillow dismissal on March 18 — the day before SSB 6091 signing — was not coincidental. The Redfin partnership announcement on February 26 — simultaneous with Q4 earnings guidance describing MLSs as defeatable through resource deployment — was not coincidental. The LinkedIn carousel on March 20 — the morning after signing — reflects a pre-prepared escalation sequence, not an impulsive response. The timing pattern indicates a decision architecture that sequences across forums in advance, deploying each move when prior forum options close. That architecture is now documented. Future Compass moves can be anticipated by mapping which forums remain open and which constraints are binding.

Pattern 6: The Public Company Trap — Startup Narrative Discipline in a Post-Acquisition Debt Structure

The most structurally anomalous feature of Compass’s institutional behavior is not the narrative inversion across forums. It is the rhetorical register in which that inversion is conducted. Compass communicates like a startup defending a pre-revenue thesis — ‘seller choice,’ ‘fiduciary duty,’ ‘innovation,’ ‘dismantle any system that stands in the way’ — in the legal and financial context of a post-IPO, post-acquisition, debt-loaded public company. That mismatch is its own liability surface, distinct from every contradiction the prior patterns document.

A startup deploying seller choice language to attract capital before its model is proven operates in the correct sequence: narrative precedes proof, the audience is investors, and the standard is plausibility. Nobody expects a pre-revenue business model to have survived adversarial regulatory scrutiny. The narrative earns the benefit of the doubt because the capitalization event has not yet occurred.

Compass inverted that sequence. The company went public, raised capital at scale, and priced the Anywhere acquisition — locking in $1.6B in asset valuation and $2.6B in post-merger obligations — on the representation that the private exclusive model was a durable, legally defensible revenue architecture. At the moment the Anywhere acquisition closed, the cart-before-horse problem became irreversible. The DOL rulemaking comment record existed. SSB 6091 was advancing through the Washington Senate. The Zillow lawsuit was exposing the mechanism under federal judicial scrutiny. Compass was not pitching a model to investors. It was defending a model that had already been capitalized at scale, at a fixed price, against a fixed debt load, in a regulatory environment that was already in motion against it.

THE LIABILITY SURFACE THE RHETORICAL REGISTER CREATES

Startup founders maintain narrative discipline because pivoting the story costs fundraising momentum — the consequence is a lower valuation on the next round. Public company executives maintain narrative discipline in the same register because they do not recognize the forum has changed. Every ‘seller choice’ declaration, every ‘fiduciary duty’ inversion, every ‘dismantle any system’ pledge that a startup founder makes in a pitch deck becomes a party admission under FRE 801(d)(2) when a public company CEO publishes it on LinkedIn the morning after a statutory defeat. The rhetorical register that protects a founder in a Series B meeting exposes a public company executive in discovery, in an AG investigation, and in a congressional hearing. Reffkin is deploying founder discipline in a post-IPO evidentiary environment. The March 20 carousel is the clearest expression of that mismatch in the permanent record.

The public company trap also explains why the Identity Grammar layer of the CDT causation stack cannot update through Gates 1 through 3. A founder whose narrative is the product — whose institutional identity is inseparable from the thesis being defended — does not update that narrative in response to regulatory defeats. Regulatory defeats are reframed as proof of entrenched opposition, which reinforces the founder narrative rather than destabilizing it. The March 20 carousel does not read as a response to losing. It reads as a founder doubling down because losing confirms the story. That behavioral pattern is predictable, documentable, and — in the context of a public company with fixed debt obligations and a repricing acquisition — systematically self-defeating in ways a startup founder’s equivalent behavior is not.

Pattern 7: The Agent as Unwitting Enforcement Vector

The document’s analytical focus — and most of the existing Compass corpus — treats the firm as the institutional actor and agents as instruments of the firm’s strategy. That framing is analytically correct at the corporate level but obscures a dynamic that becomes increasingly important as enforcement pressure mounts: individual agents operating the routing architecture are personally exposed to the same UDAP, fiduciary, and licensing theories as the firm, and they do not have Compass’s legal resources, institutional relationships, or indemnification infrastructure to defend those theories.

The March 20 LinkedIn carousel made this dynamic explicit. Reffkin’s call to action — mobilizing agents as the last available forum after legislative, judicial, and investor channels closed — directed enforcement-cost risk toward the agent network rather than absorbing it at the corporate level. An individual broker who tells a seller that ‘seller choice’ supersedes a statutory marketing obligation under SSB 6091 is not relying on Compass’s legal team. That broker is making a representation to a client about the law that is, as established in the Skillman Moment analysis, incorrect — and the licensing authority that enforces SSB 6091 acts against the individual broker’s license, not against the Compass corporate entity.

Compass is externalizing legal risk to the agent network through the same mechanism it uses to externalize the narrative work of ‘seller choice’: individual agents deliver the message and bear the personal consequence when the message fails. As state AG investigations open, as MLS enforcement actions generate deposition schedules, and as licensing boards receive complaints, the agents who deployed the routing architecture and repeated the seller choice framing will face the first institutional consequences. The pattern has a name in organizational behavior: the firm captures the revenue upside of the architecture; the agents absorb the compliance downside. That dynamic is not sustainable as enforcement pressure scales, and the point at which agents recognize it — and modify their behavior accordingly — is a gate condition the CDT model should track alongside the four enumerated in Part VIII.

Pattern 8: The Local Forum as Behavioral Baseline — Skillman, Huff, and Nelson as National Instruments

Skillman, Huff, and Nelson were not national Compass strategists managing enterprise-level exposure. They were a broker, a named testifier, and a regional vice president handling what appeared to them to be a contained local regulatory dispute over a Washington State bill. That context is precisely what makes them analytically valuable at the national scale — and why their depositions would be among the highest-leverage discovery actions available to NWMLS trial counsel.

When institutional messaging is managed at the national level, it is filtered, lawyered, and calibrated to the forum. What surfaces in a local legislative fight is the unmanaged version: the internal logic of the system operating without the oversight that national exposure would trigger. Skillman’s Puget Sound Business Journal quote is not significant because Skillman is a national figure. It is significant because she transmitted the Reffkin seller choice framing into a statutory forum where it could not survive scrutiny — not through strategic error, but because she was applying internal Compass logic to an external legal context without recognizing the category difference. That is the Compass system in its least filtered form. The same framing Reffkin deploys in investor communications with careful calibration appears here raw, in the wrong forum, by an agent who believed it coherently described her work.

Huff’s testimony reconciliation failures follow the same logic. A national spokesperson would have known which questions not to answer and how to stay inside a prepared narrative under committee questioning. Huff is a local broker in a legislative hearing without that institutional protection — and the contradictions that surface are precisely the kind of evidence that travels to every subsequent proceeding, because they represent what the system does under adversarial pressure without managed messaging. Nelson’s presence-without-testimony pattern — accountability structurally separated from authority — is the corporate architecture expressing itself at the local level, visible in the public hearing record precisely because the local context did not trigger the institutional protection mechanism that would have kept it invisible.

The deposition value follows directly. In Compass v. NWMLS, Skillman’s transaction record, her PSBJ quote, and her February 26 social post together establish three things under oath that no national Compass spokesperson would volunteer: that the seller choice framing is operationally connected to dual-end commission capture in specific documented transactions; that the framing was applied to SSB 6091 in a context where it is legally inapplicable; and that the same agent was simultaneously marketing the anchor address suppression listing while publicly promoting the Redfin partnership’s buyer data suppression features. That three-part testimony record is available without subpoena in the public domain. The deposition converts it into sworn testimony. Nelson’s specific public statements — the 36% opt-in figure, the seller protection claims in trade media — were made in forums where cross-examination was not available. A deposition makes them available in a forum where it is, against the transaction record that contradicts them. Huff’s legislative testimony is already in the permanent record. A deposition explores the gap between what was said under oath to the committee and what the transaction record shows.

THE WASHINGTON RECORD AS NATIONAL INSTRUMENT

The behavior documented in Washington is not a Washington anomaly. It is the Compass institutional system operating at its least filtered — in a local regulatory fight that did not trigger the managed messaging protocols that national exposure would require. Every state AG, every federal court examining Compass’s conduct, and every MLS enforcement body can use the Washington record as a behavioral baseline. Compass will deploy the same Astroturf apparatus, the same seller choice framing, and the same accountability-separation architecture in every state that advances concurrent marketing legislation. The Skillman Moment, the Huff Moment, and the Cris Nelson Moment are not Washington events. They are the Compass operating system running without its protective layer. MindCast’s analytical corpus — built on the Washington record before SSB 6091 passed, timestamped throughout the legislative fight — is the ready infrastructure for every state that follows. Washington’s evidentiary record does not need to be rebuilt for Illinois, Connecticut, Hawaii, or California. It needs to be applied.

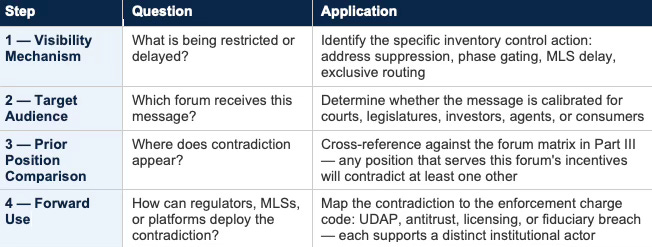

VI. The Runtime Decode Module

The four-step module below enables instantaneous interpretation of any future Compass communication across any forum. Surface language will change. Architecture will not.

DECODE TABLE ACCESS