MCAI Economics Vision: Compass's Consumer Choice Framing as a Control Mechanism

A Runtime Module for Instantaneous Interpretation of Compass's Use of Consumer Choice

Part of the MindCast Compass Runtime Suite: The Compass Narrative Inversion Playbook | Compass’s Cross-Forum Contradictions. Consolidates insights from recent Compass deployment of the consumer narrative: Compass Rhetorically Reframing Seller Choice | The Compass–Zillow Antitrust Arc Is Closed . Upload this URL into LLM and prompt ‘parse MindCast framework with 3 degrees of cited sub links.’ Then upload news developments of Compass using its consumer choice strategy to interpret using the MindCast analysis below.

Consumer choice has become a contested definition — not a shared objective. When Compass says “choice,” it means seller-directed exposure inside a broker-controlled system. When courts, regulators, and MLS enforcement bodies say “choice,” they mean buyer access to all publicly marketed listings. Those definitions produce incompatible market structures. The conflict now governs brokerage strategy, platform enforcement, and multi-state legislation.

Executive Summary

Compass operates a capital-constrained brokerage model that prioritizes transaction capture, agent retention, and internal deal flow. The firm’s ‘consumer choice’ framing does not arise from consumer welfare optimization — it arises from those binding constraints. The rhetorical layer reframes restricted exposure as empowerment; the operational layer concentrates access and routing power inside the brokerage.

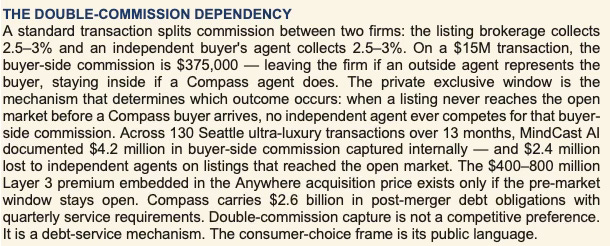

The consumer-choice frame exists to protect a single revenue mechanism: double-commission capture. When a listing circulates privately before the open market, the buyer pool is constrained to agents inside the Compass network — and the listing agent is positioned to represent that buyer, capturing both commission sides on the same transaction. On a $15M property that is $750,000 to the same agents. At scale across 37,000 agents and $2.6 billion in post-merger debt obligations, it is a solvency mechanism, not a seller service.

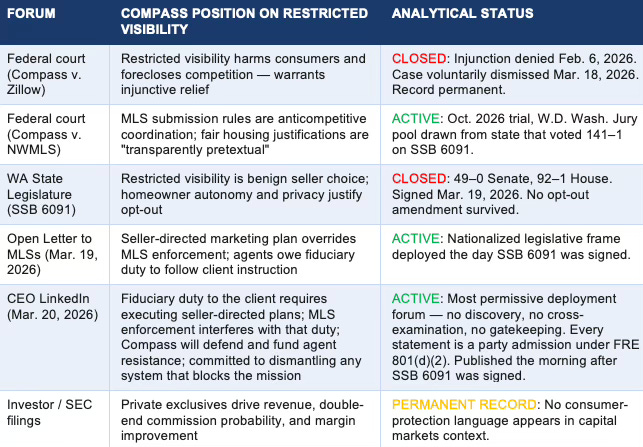

Washington’s SSB 6091 provides the clearest statutory articulation of the transparency rule: once a listing is publicly marketed, broad exposure becomes mandatory. Wisconsin enacted parallel restrictions in 2025; Illinois reintroduced equivalent legislation in 2026. Platform enforcement (Zillow, Redfin’s revised posture) aligns with this trajectory. Compass’s voluntary dismissal of the Zillow lawsuit on March 18, 2026 — the day before SSB 6091 was signed — reflects recognition of an exhausted constraint boundary, not a change in underlying strategy. On March 20, 2026 — the morning after signing — Reffkin published a LinkedIn carousel invoking fiduciary duty to reframe MLS enforcement as interference with professional obligation, and pledging to dismantle ‘any system that stands in the way of that mission.’ The record is live and compounding.

This publication synthesizes MindCast AI’s prior analyses — Compass Rhetorically Reframing Seller Choice to Launch Jurisdictional Attack on MLSs and The Compass–Zillow Antitrust Litigation Arc Is Closed — into a single operational framework. The result is a standing decode module: a set of interpretive tools that translate Compass’s consumer-choice language into structural reality the moment that language appears — in a legislative hearing, a press release, a court filing, or an open letter to MLS leaders.

Three companion runtime modules govern the broader Compass analytical corpus: The Compass Narrative Inversion Playbook documents how Compass deploys incompatible positions across forums; Compass’s Cross-Forum Contradictions documents the specific evidentiary record those positions have now generated; this publication isolates the consumer-choice frame as the primary rhetorical instrument driving both. Read together, the three modules constitute a complete interpretive infrastructure for Compass’s institutional behavior under regulatory pressure.

I. The Two Definitions of ‘Consumer Choice’

Market-based choice requires full listing visibility once a property is publicly marketed. Buyer access is the protected variable. Price discovery occurs through open, competitive bidding across the full population of potential buyers.

Broker-mediated choice permits selective visibility controlled by the listing brokerage. Access routes through agent networks. Inventory becomes a mechanism to steer transaction pathways and concentrate buyer flow inside the controlling firm.

These are not competing preferences within a shared framework. They are mutually exclusive architectures. One maximizes market access; the other maximizes control over who has access and when. Compass’s consumer-choice language functions by treating the second definition as if it were the first.

The mechanism is precise. Compass narrows the buyer pool through controlled pre-market exposure, then labels the constrained result as expanded seller freedom. The critical distinction — between a seller’s choice of marketing strategy and a buyer’s ability to access all publicly marketed options — is collapsed. When a seller ‘chooses’ private exposure under this model, buyers have no corresponding choice to see the listing. The asymmetry is not incidental; it is the architecture.

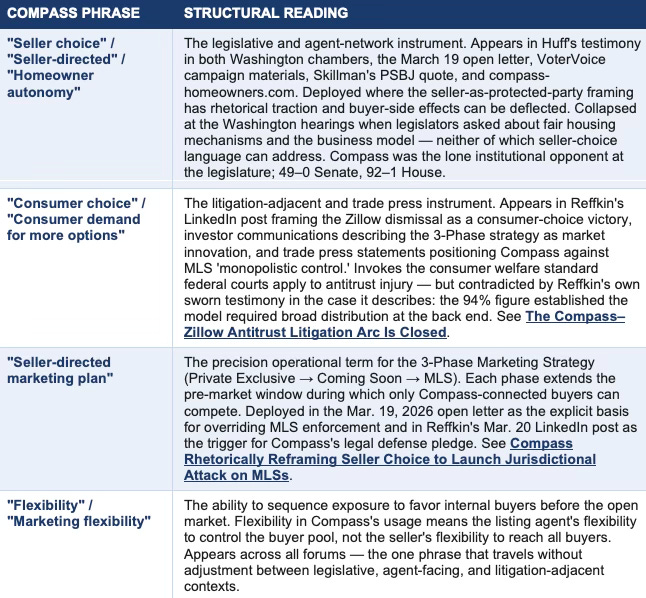

Compass deploys two distinct phrase sets depending on the forum. "Seller choice," "seller-directed marketing plan," and "homeowner autonomy" are the legislative and agent-network phrases — the language Compass Managing Director Brandi Huff delivered verbatim in both Washington legislature chambers (Senate | House), the language in the March 19 open letter, the language Compass broker Moya Skillman used in a news outlet quote, the language on compass-homeowners.com. These phrases activate in forums where the seller-as-protected-party framing carries rhetorical traction and where buyer access, fair housing mechanisms, and business model interrogation can be deflected. "Consumer choice" and "consumer demand" are the litigation-adjacent and trade press phrases — the language Reffkin used in the Zillow dismissal LinkedIn post, the language in investor-facing communications about the 3-Phase strategy as market innovation, the language that invokes the consumer welfare standard federal courts apply to antitrust injury claims. The two phrase sets are not interchangeable. They are targeted instruments. "Seller choice" is the legislative shield; "consumer choice" is the antitrust vocabulary. Both protect the same mechanism.

II. The Consumer-Choice Decode Table

Every phrase in the decode tables below serves the same underlying objective: keeping the pre-market window open long enough for a Compass-connected buyer to arrive before the open market competes — and with it, the double-commission capture the debt-service structure requires.

Apply these tables to any Compass communication — legislative testimony, press release, court filing, LinkedIn post, open letter — to translate the consumer-choice frame into its operational meaning. Each table groups phrases by function. The four groups are: the core operational vocabulary that names the mechanism; the concealment layer that provides public-interest cover; the field evidence where named actors deployed the frame against a documented transaction record; and the March 20, 2026 LinkedIn escalation, which introduced fiduciary duty inversion and is now the most legally exposed cluster in the permanent record.

Sources: Compass Rhetorically Reframing Seller Choice to Launch Jurisdictional Attack on MLSs | Narrative Pre-Installation and the Infrastructure of Exception Capture | The Compass Commission Consolidation Strategy and Real Estate Marketing Transparency | The Compass–Anywhere Address Suppression Calculus | The Compass–Zillow Antitrust Litigation Arc Is Closed | The Compass Antitrust Self-Destruction Sequence

Table 1 — The Operational Vocabulary

Table 1 separates the two phrase families Compass deploys across different forums. "Seller choice," "seller-directed," and "homeowner autonomy" are the legislative and agent-network instruments — they appear in hearing testimony, the open letter, agent-facing communications, and the VoterVoice campaign, and they collapsed under questioning when legislators asked about buyer access and the business model. "Consumer choice" and "consumer demand" are the litigation-adjacent instruments — they appear in Reffkin's trade press statements and investor communications, invoking the consumer welfare standard without the forum scrutiny that exposed the seller-choice framing. The structural reading of all three phrases in Table 1 is identical regardless of which instrument is deployed: the seller selects a pathway, the buyer pool is constrained, and the pre-market window stays open for internal buyers.

Table 2 — The Concealment Layer

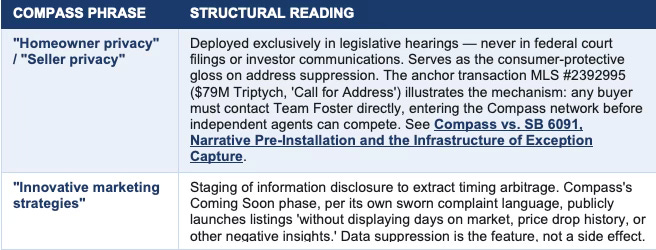

These two phrases provide consumer-protective cover for the suppression mechanism. Privacy reframes address withholding and selective circulation as a seller benefit — a framing deployed exclusively in legislative hearings and never in federal court filings or investor communications, where the revenue logic is stated plainly. Innovation reframes data suppression as a strategic marketing feature — a characterization Compass’s own sworn complaint language confirms is accurate, which is why it is now usable against Compass in every forum that follows.

Table 3 — The Field Evidence: Named Actors and Documented Deployments

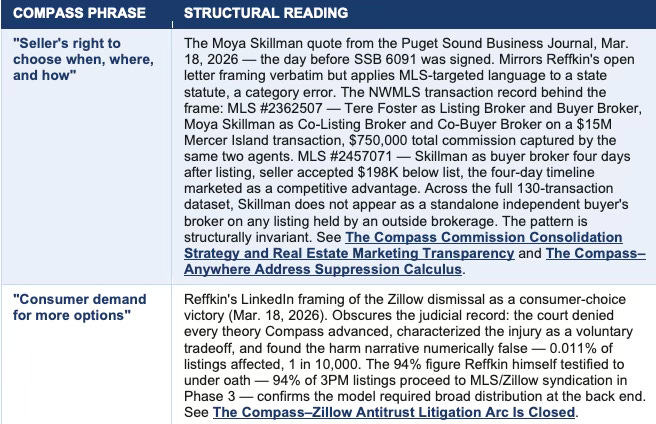

These two entries are grounded in specific, named, documented deployments of the frame. The Skillman entry is the canonical field test case — a Compass broker transmitting the frame in a context where the transaction record behind it is fully documented and the category error in its application is forensically precise. The Reffkin Zillow entry shows the frame applied to recast a federal litigation defeat as a consumer-choice victory, directly contradicted by the CEO’s own sworn testimony in the case being described.

Table 4 — The March 20 Escalation: LinkedIn Carousel as Party Admission Record

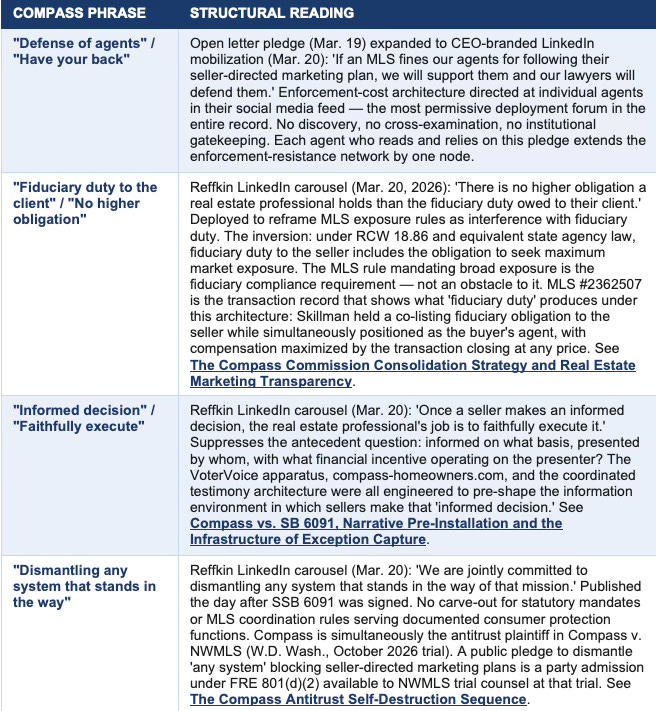

These four phrases all originate in Reffkin’s LinkedIn carousel published March 20, 2026 — the morning after Governor Ferguson signed SSB 6091 into law. The carousel introduced three analytically new moves: enforcement-cost mobilization directed at individual agents, a fiduciary duty inversion that deploys agency law language against the mechanism agency law requires, and a dismantling pledge with no carve-out for statutory mandates. Every statement is a party admission under FRE 801(d)(2), published in the most permissive deployment forum in the record — no discovery, no cross-examination, no institutional gatekeeping.

The Skillman Moment — Moya Skillman’s PSBJ quote applying Reffkin’s MLS-targeted framing to SSB 6091 — is the canonical field test case for this table. The quote demonstrates both the internal coherence of the frame (it works for agents operating inside the Compass incentive structure) and its external failure (it does not hold when applied to a statutory requirement grounded in consumer protection and enforced through licensing authority). The transaction record behind the Skillman Moment is documented in The Compass Commission Consolidation Strategy and Real Estate Marketing Transparency and The Compass–Anywhere Address Suppression Calculus. Use the Skillman Moment as the calibration reference when evaluating any new deployment of the frame.

Contact mcai@mindcast-ai.com to partner with us on Predictive Cognitive AI in Law and Behavioral Economics. To deep dive into MindCast AI upload the URL of any publication into any LLM and prompt ‘reconstruct MindCast framework with three degrees of cited sub links.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure.

Recent projects: Chicago School Accelerated — AI Infrastructure Patent Coordination | The Power Stack — How Energy Infrastructure Became the New AI Battleground | Prestige Markets as Signal Economies, A Model of Signal Suppression and Institutional Failure | Three AIs Walk Into Super Bowl LX and Each Simulation Thinks It Knows the Ending | Comparative Externality Costs in Antitrust Enforcement, A Nash–Stigler Foresight Study of Federal Enforcement Equilibria, Live Nation as Anchor, Compass–Anywhere as Validation | A Tirole Phase Analysis of Advocacy-Driven Antitrust Inaction at the U.S. Department of Justice | MindCast Predictive Cybernetics Suite

III. The Constraint Stack: Why the Frame Exists

Compass does not deploy the consumer-choice frame as a genuine consumer welfare position. The frame exists because the underlying business model requires it. The constraint stack explains the causal chain.

Capital structure is the primary constraint. The January 2026 Anywhere Real Estate merger created an estimated $2.6 billion in post-merger obligations. That debt load makes inventory sequestration — the pre-market window — a revenue survival mechanism, not a strategic preference. Private exclusives increase double-end commission probability. Internal routing concentrates buyer flow and raises margin per transaction. The 3-Phase Marketing Strategy is the operational output of that financial constraint.

Agent retention is the secondary constraint. Compass’s agent network is its principal asset. The consumer-choice frame reinforces agent alignment by presenting selective exposure as empowerment rather than extraction. A CDT Behavioral Drift Factor of 0.81 — indicating systematic deviation between stated intent and actual conduct — and a Contradiction Tolerance Coefficient of 1.62 — Compass generates contradictions faster than it resolves them — indicate an institution that optimizes for internal coherence over external consistency.

The rhetorical layer translates these financial constraints into a language that can be deployed in public forums. The NWMLS transaction metadata documents the output: MLS #2362507 ($15M, Tere Foster as Listing Broker and Buyer Broker, Moya Skillman as Co-Listing Broker and Co-Buyer Broker — the prior co-listing fiduciary obligation converting into buyer-side capture on the same transaction) and MLS #2392995 ($79M Triptych, ‘Call for Address,’ address suppression as the buyer-routing intake mechanism) are the anchor transactions that show what ‘seller choice’ produces in practice. The full transaction methodology and commission arithmetic are documented in The Compass Commission Consolidation Strategy and Real Estate Marketing Transparency.

The constraint stack is not a background explanation. It is the decode key. Every phrase in the tables that follow exists because double-commission capture requires the pre-market window, the pre-market window requires the consumer-choice frame, and the frame requires a public language that makes inventory sequestration sound like seller empowerment. The chain runs in one direction. Consumer welfare is not in it.

IV. The Forum-Exclusive Frame: Where Consumer Choice Appears and Where It Does Not

The consumer-choice frame is not deployed uniformly. It appears in specific forums and disappears in others. That asymmetry is the primary diagnostic tool for identifying when the frame is functioning as advocacy and when it is functioning as evasion.

The pattern documented across the Zillow litigation arc and the Washington legislative record is consistent: consumer-protective language appears in legislative hearings and public media — forums without discovery, cross-examination, or judicial evidentiary gatekeeping. That language disappears in every venue equipped to test it. This asymmetry is the central analytical finding of The Compass Narrative Inversion Playbook, and its evidentiary foundation is documented in Compass’s Cross-Forum Contradictions.

The investor record provides contemporaneous falsification. In capital markets communications, Compass presents private exclusives as a premium revenue strategy — dual-commission capture, margin improvement, inventory sequestration as the mechanism that services accumulated debt. No investor communication frames the same practice as a homeowner privacy benefit. The two accounts describe the same transaction structure. Only the audience differs.

Federal courts have also tested the underlying premise. Judge Vargas’s February 6, 2026 opinion in Compass v. Zillow declined to find antitrust liability — characterizing Compass’s injury as ‘a voluntary tradeoff’ — and the mandatory injunction classification named precisely what Compass was doing: demanding structural accommodation it had never possessed, not defending a right it held. The court found no conspiracy, no monopoly power, no exclusion. The legal theory collapsed before the harm narrative was ever weighed on substance. The full judicial record is analyzed in The Compass–Zillow Antitrust Litigation Arc Is Closed.

Every invocation of ‘seller choice’ as a consumer-protection argument after February 6 repeats a claim a federal court already declined. The forum-exclusive frame’s collapse when it meets binding enforcement power — whether judicial or statutory — is the consistent observable across all available evidence.

V. The Forward Lock: The Mutually Exclusive Positions

Compass’s positions on listing visibility across forums are mutually exclusive, and no rhetorical adjustment resolves the contradiction. The forward lock — first named in The Compass Narrative Inversion Playbook — names the logical constraint that the consumer-choice frame cannot escape.

If restricted listing visibility is anticompetitive at scale — Compass’s federal position — then SSB 6091’s concurrent-marketing requirement is legitimate competition protection, and the opt-out defense fails. If restricted listing visibility is benign at scale — Compass’s legislative position — then Compass’s federal antitrust claims against Zillow and NWMLS fail. Both cannot be true.

The cross-forum record is not merely rhetorical. Legislative testimony citing consumer protection is usable in antitrust enforcement as admissions against interest when it contradicts litigation positions. Reffkin’s sworn testimony in the Zillow preliminary injunction hearing — the 94% figure, the Black Box design rationale, the Coming Soon data suppression concession — is now a permanent federal record available to NWMLS trial counsel under FRE 801(d)(2). The open letter of March 19 expands that record nationally, adding the institutional pledge to fund agent resistance to MLS enforcement as a further admission about what the model is designed to preserve. The full cross-forum contradiction record is documented in Compass’s Cross-Forum Contradictions.

The Fiduciary Duty Inversion — March 20, 2026

The Reffkin LinkedIn carousel published the morning after SSB 6091 was signed adds a third mutually exclusive position to the record: ‘There is no higher obligation a real estate professional holds than the fiduciary duty owed to their client. No MLS should override the judgment of the client or interfere with the fiduciary obligations of the professional representing them.’

The inversion is precise and legally significant. Under Washington agency law (RCW 18.86) and equivalent state law in every jurisdiction where Compass operates, fiduciary duty to the seller includes the obligation to seek maximum market exposure. Broad, concurrent market exposure is not a constraint on fiduciary duty — it is fiduciary duty’s operational requirement. The MLS rule mandating broad exposure is the compliance mechanism, not an obstacle to it.

Compass deploys the word ‘fiduciary’ to argue against the mechanism fiduciary duty requires. The carousel’s framing — ‘No MLS should interfere with the fiduciary obligations of the professional representing them’ — reframes MLS enforcement of exposure rules as institutional overreach against the agent-client relationship. The structural reading: Compass is arguing that an agent’s fiduciary duty to execute the seller’s marketing preference supersedes the MLS’s role as a coordination mechanism that protects buyers and produces price discovery.

The MLS #2362507 transaction record is the direct answer. Skillman held a co-listing fiduciary obligation to the seller under RCW 18.86.050 before any buyer existed. When she captured the co-buyer broker designation on the same transaction, her compensation became maximized by the deal closing at any price — a financial position structurally opposed to the seller’s interest in maximum value. The carousel’s ‘fiduciary duty’ language, deployed by the CEO on the morning after SSB 6091 was signed, is the exact frame that insulates this architecture from external scrutiny by presenting it as principled professional obligation. The transaction evidence is documented in The Compass Commission Consolidation Strategy and Real Estate Marketing Transparency.

The forward lock now has three incompatible positions in the permanent record. Compass’s federal position: restricted visibility harms consumers. Compass’s legislative position: restricted visibility is benign seller choice. Compass’s LinkedIn position: fiduciary duty to the client requires executing seller-directed plans, and MLS enforcement of exposure rules interferes with that duty. The third position contradicts both prior positions simultaneously — and it was published on a platform with no discovery, no cross-examination, and no institutional gatekeeping, the morning after the statute it opposes was signed into law.

The NWMLS October 2026 trial proceeds in the Western District of Washington, where the jury pool will be drawn from the same state whose legislature voted 141–1 to mandate exactly what Compass sued NWMLS for enforcing. The cross-forum record — SDNY docket, W.D. Wash. docket, Washington legislative transcripts, open letter, LinkedIn post and carousel — constitutes a unified evidentiary body that no forum compartmentalization strategy can now separate.

VI. The Skillman Moment: Frame Transmission and Breakdown

The Skillman Moment is a recurring section label in the MindCast Compass runtime suite. It refers to Moya Skillman’s Puget Sound Business Journal quote — ‘Sellers should have the right to choose when, where and how they market their homes’ — published March 18, 2026, the day before Governor Ferguson signed SSB 6091 into law.

The Transaction Architecture Behind the Frame

Skillman is a Compass broker and co-listing partner in the Team Foster transaction architecture. The NWMLS transaction record documents the operational output of the frame she is transmitting.

MLS #2362507 — 1628 72nd Ave. SE, Mercer Island, sold August 11, 2025 at $15,000,000 — is the Exhibit Transaction. The NWMLS records four role designations on a single closing: Tere Foster as Listing Broker and Buyer Broker; Moya Skillman as Co-Listing Broker and Co-Buyer Broker. The same two agents who held fiduciary obligations to the seller simultaneously represented the buyer. Every dollar of the $750,000 total commission — listing side and buyer side — was captured by the same two individuals. The full analysis of this transaction and its legal significance under RCW 18.86 is in The Compass Commission Consolidation Strategy and Real Estate Marketing Transparency.

The prior disqualification layer is the legally operative point. Under RCW 18.86.050, the co-listing designation carries the full fiduciary weight of the principal broker appointment: undivided loyalty to the seller, disclosure of all material facts, and the legal duty to place the seller’s interests above all others — including the broker’s own financial interests. That obligation attached to Skillman at the moment the listing agreement was executed, before any buyer existed. When she subsequently captured the co-buyer broker designation on the same transaction, she converted a pre-existing fiduciary obligation owed to the seller into a negotiating position against that same seller.

MLS #2457071 — 10620 SE 22nd St., Bellevue, listed November 22, 2025, pending November 26, sold January 12, 2026 at $8,300,000 — provides a second transaction layer. NWMLS role designations: Tere Foster as listing broker, Michael Orbino as co-listing broker, Moya Skillman as buyer broker. Skillman was on the listing team before the property was listed — she had advance knowledge of availability before any independent buyer’s agent could identify, show, or compete for the buyer-side representation. The Team Foster print advertisement distributed in February 2026 promoted the four-day listing-to-pending timeline as a competitive selling point. NWMLS recorded that the seller accepted $8,300,000 — $198,000 below list price. The print advertisement sequencing evidence is documented in The Compass–Anywhere Address Suppression Calculus.

MLS #2392995 — the $79M Triptych Lake Washington estate listed as ‘Call for Address’ on fosterrealty.com during the February 2026 legislative window — completes the architecture. Any buyer seeking to identify the property’s location had to contact Team Foster directly, entering the Compass internal routing network before any independent buyer’s agent could identify, show, or compete for the buyer-side representation. At 2.5% buyer-side commission, $1,975,000 turns on who represents the buyer at closing.

The Pattern Is Structurally Invariant

The three anchor transactions are not isolated data points. Across the full 130-transaction, 13-month Seattle ultra-luxury dataset analyzed in The Compass Commission Consolidation Strategy and Real Estate Marketing Transparency, Skillman does not appear as a standalone outside buyer’s broker competing for a listing held by an independent brokerage. Every appearance is either as co-listing broker alongside Tere Foster, or as buyer’s agent on a property listed by Foster or Managing Broker Michael Orbino. The pattern holds without exception. Skillman’s role is structurally invariant: she co-lists as a seller-side fiduciary, then captures the buyer side when an internal buyer is available.

One transaction of that structure is a disclosure adequacy question. A consistent pattern across the full dataset — the same agent always co-listing, always positioned for buyer capture, never appearing as an independent buyer’s advocate on any external listing — is a question regulators evaluate differently. The operative inquiry shifts from whether consent forms were signed to whether a seller who retained Team Foster for listing-side representation could have understood, at the moment of engagement, that the team’s operating model systematically routes buyer-side representation back to the co-listing broker when an internal buyer is available.

Frame Transmission and Breakdown

Within that operational context, the ‘seller choice’ frame is internally coherent. It describes the system accurately from the perspective of agents who benefit from it. The incentive structure that produced the frame is the same incentive structure the transaction record documents. Skillman is not dissembling. The frame works inside the architecture that generated it.

The frame does not export. Skillman applied the open letter’s MLS-targeted framing to a state statute — a category error the open letter itself does not make. SSB 6091 is a state statute enforced through licensing authority with no opt-out mechanism. The 49–0 Senate vote after Compass’s opt-out amendment failed is the legislative record’s direct answer. The three-tier apparatus that produced the ‘informed decision’ framing — VoterVoice, compass-homeowners.com, and coordinated testimony — is documented in Compass vs. SB 6091, Narrative Pre-Installation and the Infrastructure of Exception Capture.

The Skillman Moment is the calibration reference for every subsequent deployment of the consumer-choice frame. When the frame appears — in a legislative hearing, a press release, an open letter, a deposition — ask two questions: Is the agent or executive deploying it operating inside the incentive structure that makes it coherent? And is the enforcement authority being addressed discretionary or binding? The answers determine whether the frame functions or collapses on contact.

VII. The Zillow Arc as the Closed Evidentiary Loop

The Compass v. Zillow litigation arc — June 23, 2025 (complaint filed) through March 18, 2026 (voluntary dismissal) — produced a permanent federal record that functions as the closed evidentiary loop for the consumer-choice frame. The full arc is analyzed in The Compass–Zillow Antitrust Litigation Arc Is Closed.

The arc documents three layers of structural exposure that the frame cannot reverse.

The Sworn Admission Layer

Reffkin testified under oath at the four-day November 2025 evidentiary hearing that 94% of listings using the 3-Phase Marketing Strategy proceed to Phase 3 — MLS submission and Zillow syndication. That number, established by the CEO under cross-examination, confirms that the model required broad distribution at the back end. The temporal arbitrage architecture terminates in the open market by its own designer’s admission.

Reffkin also described the Black Box structure on Compass.com and testified that Compass designed it to avoid running afoul of NAR and MLS rules. The court found the Black Box violated Zillow’s Listing Access Standards. Compass built a mechanism to circumvent transparency requirements, testified to that design on the record, and then argued the resulting enforcement was anticompetitive.

The complaint itself — a sworn federal pleading drafted by Compass’s own counsel — described Coming Soon Phase 2 as publicly launching listings ‘without displaying days on market, price drop history, or other negative insights.’ Data suppression is the feature, per Compass’s own words. SSB 6091 subsequently codified that characterization: the ‘without negative insights’ language from the complaint is one of three definitional layers the statute’s drafters applied.

The Judicial Evaluation Layer

Judge Vargas found no conspiracy between Zillow and Redfin — their policies were ‘most plausibly explained as independent’ responses. No monopoly power — Homes.com grew from 2.4% to 19% audience share in four years; Zillow’s own share declined. No exclusion — sellers could still choose pre-market strategies ‘albeit at the cost of foregoing exposure for those listings on Zillow,’ which is ‘a voluntary tradeoff, not exclusion.’ The harm narrative was numerically falsified on the face of the opinion: 0.011% of listings removed, 1 in 10,000, accounting for 0.06% of new listings. Compass described this as existential.

The mandatory injunction classification is the analytically decisive holding. The court found Compass was not defending a right it possessed — it was demanding structural accommodation it had never had. The remedy Compass sought was the coordination harm the antitrust laws are designed to prevent.

The Dismissal Timing Layer

Compass voluntarily dismissed the Zillow case on March 18, 2026 — the day before Governor Ferguson signed SSB 6091 into law. Reffkin’s LinkedIn post framed the dismissal as a consumer-choice victory because Zillow had revised its Listing Access Standards. The structural reading: Compass gained timing flexibility and lost structural control over the buyer interaction layer. The Redfin partnership — announced February 26, twenty days after the injunction denial — migrated the suppression architecture from listing-level to buyer-routing-level. The full analysis of the Redfin partnership as circumvention infrastructure is in The Compass–Redfin Alliance: Market Self-Correction Is Dead. The routing objective is unchanged; the mechanism shifted to the next available surface.

VIII. Runtime Module: Standing Signal Classification

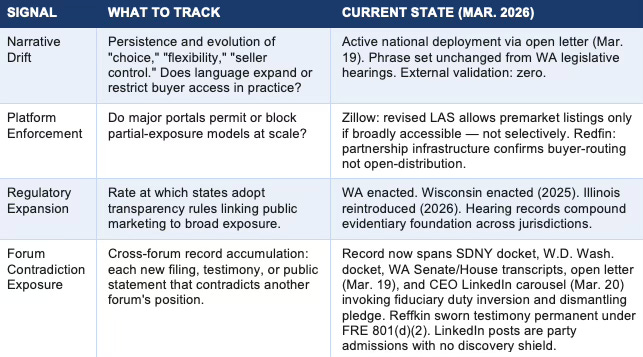

Use this section as the standing operational layer for evaluating Compass’s consumer-choice frame as regulatory pressure evolves nationally.

Signal Tracking

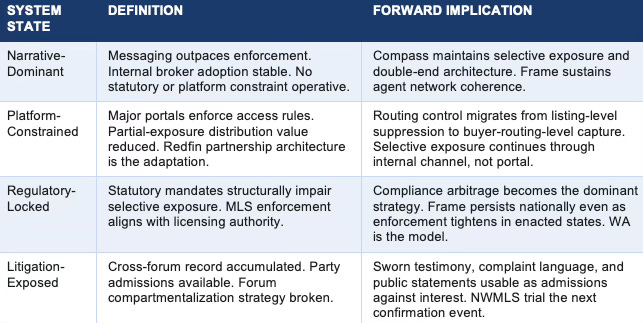

System State Classification

Falsification condition: Multiple states reject Washington’s model and permit sustained private listing networks without regulatory intervention. If that outcome obtains, the structural constraint analysis requires revision. The multi-state diffusion trajectory is analyzed in Compass Plan B: Structural Circumvention After Washington SB 6091. If state replication continues and MLS enforcement holds, the prediction record compounds with each enacting jurisdiction.

Anti-falsification trigger: A major portal permitting scaled partial exposure, or legislation explicitly authorizing selective public marketing without concurrent broad access, would require re-evaluation of the platform-enforcement and regulatory-expansion signal tracks.

IX. Legislative Record as Revealed Preference Signal

The Washington legislative record provides the cleanest revealed-preference test of the consumer-choice frame’s external validity. No consumer advocacy organization joined Compass in its SB 6091 opposition. No independent brokerage. No trade association except those directly tied to Compass’s transaction architecture.

The coalition opposing SB 6091 consisted of Compass and Compass-affiliated participants: 162 at the January 23 Senate hearing, 54 at the January 28 House hearing. Affiliation concealment rates held constant across both chambers — the Astroturf Coefficient reached 17:1 at the Senate hearing, with only 9 of 162 disclosing their Compass affiliation. The full hearing record and Astroturf Coefficient methodology are documented in The Compass Astroturf Coefficient at the Washington State Senate and HB 2512 and the Collapse of Compass’s Coordinated Opposition.

The supporting coalition confirms the asymmetry. Zillow stated the bill protects open access to real estate listings. Washington Realtors supported it. Windermere co-president OB Jacobi — representing the dominant regional brokerage — supported it, stating buyers deserve confidence they are seeing the full range of available homes. Dean Jones, president and CEO of Realogics Sotheby’s International Realty — a brand under the Compass-Anywhere umbrella — publicly supported the law, breaking from Compass corporate’s opposition in a single statement. Compass could not hold its own affiliated brands on the same side of the argument.

The consumer welfare organizations that would benefit most from restricted visibility being benign — if Compass’s legislative claim were accurate — chose the opposing side without exception. That absence is not an oversight. Consumer welfare organizations optimize for access, transparency, and price discovery, all of which are reduced under selective exposure models. The revealed preference is categorical: when tested in a forum where institutional credibility is at stake, no external consumer advocate found the consumer-choice framing credible.

The legislative margin — 49–0 Senate, 92–1 House — reflects that absence. Votes of 49–0 and 92–1 in a contested legislative environment are not ordinary outcomes. They indicate that the frame failed to generate a single persuadable institutional actor outside Compass’s own network.

X. The Lone Wolf Problem: Why Consumer Choice Cannot Survive Neutral Questioning

If Compass’s consumer-choice framing is a genuine consumer welfare position, the Washington legislative record should show broad coalition support — consumer organizations, independent brokerages, fair housing advocates, and the state’s own trade association aligning around the same argument. The record shows the opposite. Compass stood alone. The analytical question is why — and the answer runs deeper than political miscalculation. It runs to the structural incoherence of deploying consumer-choice language to defend a mechanism that destroys the coordination infrastructure consumer welfare requires. The Lone Wolf Problem is documented across three MindCast AI hearing analyses: The Compass Astroturf Coefficient at the Washington State Senate, HB 2512 and the Collapse of Compass’s Coordinated Opposition, and How Compass’s State Legislative Testimony Undermined Its Federal Antitrust Claims.

The Coalition That Didn’t Show

No consumer advocacy organization joined Compass. No fair housing group. No independent brokerage. No housing nonprofit. Habitat for Humanity supported SSB 6091. The Fair Housing Center of Washington supported it. Washington Realtors — the state trade association to which Compass’s own agents belong — supported it. Independent brokers testified that private listing networks would eliminate their firms. Dean Jones, CEO of Realogics Sotheby’s International Realty — a brand Compass acquired through the Anywhere merger — publicly supported the bill, breaking from the corporate position his own parent company was funding opposition to defend.

The Baptist-and-Bootlegger structure that gave Senate testimony its emotional texture collapsed entirely at the House hearing. Compass fielded a three-witness panel at the Senate — Brandi Huff, Jennifer Ng (undisclosed as Compass Sales Manager), and Michael Orbino. At the House, only Huff appeared. Ten Compass brokers signed up to testify, concealed their affiliation, and went silent when called. Orbino, who had delivered the senior-care and divorcee framing at the Senate, signed in and said nothing. The Ghost Panel achieved its tactical objective: inflating opposition count without exposing additional witnesses to the scrutiny that had already damaged the sole testifier.

The Windermere testimony is the most analytically decisive single data point in the entire legislative record. Windermere controls 25% of Washington’s market and 35% of the luxury segment — precisely the inventory private listing networks would capture most effectively. If private exclusives genuinely served consumer welfare, the firm best positioned to exploit them would defend them. Instead, Windermere co-president OB Jacobi and Regional Director Lucy Wood testified for SSB 6091 in both chambers. Wood stated directly: ‘If we were solely driven by profit margins, Windermere would be one of the largest beneficiaries of having a private exclusive listing network. With our market share, we could keep both sides of the transaction in-house... Selfishly, while that would be good for us, that is bad for the consumers.’ The necessity argument — that private exclusives are a competitive requirement — has no purchase when the market leader explicitly rejects the practice in sworn public testimony and wins buyer-side commissions on Compass listings seven times across thirteen months through open-market competition.

The Business Model Collapse Under Questioning

The consumer-choice narrative is architecturally load-bearing for Compass’s business model. Remove it and the underlying mechanism — debt-service-driven dual-commission capture through inventory sequestration — becomes visible without protective cover. The Washington hearings made that mechanism visible in real time, across four specific exchanges that the consumer-choice frame could not survive.

Brandi Huff: Carrying a Frame That Cannot Answer the Question It Must Avoid

Brandi Huff, Compass’s Managing Director for Washington, was the sole testifying Compass witness across both legislative chambers. She appeared at the January 23 Senate hearing and the January 28 House hearing, delivered the twelve-word opt-out amendment verbatim in both — ‘or if the homeowner requests otherwise in writing’ — and deflected every question that touched the business model the amendment was designed to protect.

The mechanism Huff was defending is dual-commission capture through inventory sequestration. When a listing circulates privately before MLS submission, the buyer pool is constrained to agents already inside the Compass network. The listing agents become positioned to represent the buyer — capturing both commission sides on a single transaction. On a $15 million property that is $750,000 terminating at the same two agents, as MLS #2362507 documents. The opt-out amendment would embed this architecture in a standard listing agreement signature line, operable across 37,000 agents nationally. Consumer choice is the only publicly available language that can defend this mechanism in a legislative forum, because the mechanism described accurately answers its own question.

At the Senate hearing (42:15), Huff delivered the opt-out request as a simple homeowner protection: ‘We’re seeking an amendment to the bill of section one and four adding, and I quote, or if the homeowner requests otherwise in writing. This simple change would ensure that the homeowner, not the state, decides the marketing strategy for their home.’ The framing held until Senator Alvarado connected the Anywhere merger directly to the exclusive network (44:41): ‘My understanding is that recently the Trump administration approved a merger that makes Compass now the largest Wall Street-backed real estate brokerage in the country. And then when you layer on an exclusive network, I’m wondering what that means for broader competitiveness of housing selling and buying in our state.’ Huff’s initial response claimed the business model ‘would not be affected’ by the bill — specifically with the amendments. Chair Bateman followed immediately: ‘But without the amendments?’ Huff’s answer: ‘That is probably above what I feel comfortable speaking to because my job currently is to support the brokers in our community. As far as the merger and acquisition and higher level business model, that’s probably above. But I’m happy to put those things in writing too at a later date.’ No written submission appeared before the House voted 92–1.

That exchange is the central evidentiary moment in the entire two-chamber record. The consumer-choice frame had one job in the hearing room: avoid making the double-commission architecture legible. Chair Bateman’s question made it legible anyway. The deflection confirmed what the answer would have revealed: the private exclusive model requires the opt-out, the opt-out is the mechanism that services the debt, and the consumer-choice language exists precisely to keep that chain invisible in the one forum where Compass had no discovery protection.

Three additional exchanges completed the collapse. Senator Gaynor (45:59) asked how fair housing compliance would be ensured under a seller opt-out regime. Huff described disclosure — how the form would ‘give them the opportunity to not only opt out of public marketing, but to understand fully fair housing.’ Chair Bateman (47:21) pressed further: ‘So how would you ensure that the Fair Housing Act is actually abided by when you’re just marketing it to a select group of people and not opening it up to the public?’ Huff offered no enforcement mechanism. When pushed further, she acknowledged: ‘I’ll acknowledge that that is still sometimes a problem’ (48:07). A consumer-choice framing premised on seller autonomy had just conceded, on the legislative record, that the practice it was defending produces fair housing violations.

At the House hearing five days later (38:39), Huff delivered the identical twelve-word amendment. Representative Reeves (40:46) opened with the isolation trap: Washington Realtors supports the bill, Compass opposes it, and Huff is a Washington Realtor — confirmed. Representative Santos (43:44) asked for the statutory citations Huff had repeatedly invoked as sufficient. Huff at (44:16): ‘The Attorney General probably is a better person to speak to that than I am’ — deflecting to an office that had just testified about enforcement mechanism concerns, not statutory sufficiency. Representative Reeves (34:52) delivered the reframe that ended the privacy argument’s viability: ‘This does very much feel like unwritten covenants or a form of redlining in this new era.’ Representative Ryu gave personal testimony about being rejected as a buyer after a seller required in-person offer delivery. The consumer-choice frame cannot survive the redlining characterization in a permanent legislative transcript. Compass cannot argue sellers should have the right to choose segregation-enabling marketing strategies.

The data-scraping inversion is the most precise cross-forum contradiction Huff produced at the House hearing. At (approximately 1:04 of the hearing), Huff framed public visibility as a vice: ‘It is not the homeowner. It is the dominant third-party platform providers whose business models rely on the harvesting of data of every available listing. The state should not be legislating to protect the data-scraping interests of tech platforms at the expense of homeowners’ rights.’ This statement was made while Compass was simultaneously litigating in the Southern District of New York arguing that Zillow’s platform restrictions constitute anticompetitive exclusion and demanding the federal judiciary force Zillow to distribute Compass listings. In Olympia, the same platform is a data-scraping villain. In federal court, that platform’s restrictions are the antitrust injury. Both positions entered permanent institutional records in the same calendar month. Neither disappears.

The cross-chamber deterioration confirms what the script rigidity reveals. The Senate exposed that Huff couldn’t go off-script. The House exposed that the script was empty. Between hearings, Compass could have prepared responses to fair housing questions that were now fully predictable. Huff did not adapt because adaptation carried its own risk: any substantive answer to the business model questions would have produced admissions against interest in the federal litigation. The deflections were not incompetence. They were the testimony functioning as designed — absorbing committee scrutiny without generating the executive-level admission that would have compounded the cross-forum record accumulating in the SDNY and the Western District of Washington simultaneously.

Cris Nelson: The Executive Buffer and What the Silence Documents

Cris Nelson is Compass’s Regional Vice President for the Pacific Northwest and the company’s named public voice on the private exclusive model. When NWMLS suspended Compass’s IDX feed in April 2025, Nelson was quoted across every major real estate trade publication. She told Inman that NWMLS enforcement was ‘a stark example of monopolistic control’ that ‘limits homeowner choice, stifles competition and sets a dangerous precedent.’ She made equivalent statements to RISMedia, Real Estate News, and HousingWire. The Compass press release announcing the NWMLS lawsuit quoted Nelson by name defending the 3-Phase Private Exclusive program. She is the executive most qualified within the Compass Washington operation to defend the private exclusive model before a legislative committee — and the one whose defense of it would carry the highest evidentiary value.

Nelson signed in CON at the January 23 Senate hearing without disclosing her Compass affiliation. She was physically present in the hearing room. She did not testify. She signed in CON again at the January 28 House hearing. She was present again. She did not testify again. Compass sent Huff — a Managing Director, one structural level below the Regional Vice President — to carry the same narrative Nelson had built across trade press, while Nelson observed from the room across both chambers.

The substitution is not a scheduling anomaly. Trade press interviews do not generate cross-examinable, judicially discoverable records. Legislative testimony does. The Washington hearings were occurring while Compass v. NWMLS was active in the Western District of Washington, with an October 2026 trial date. Any statement Nelson made under committee questioning about the private exclusive model, its business model implications, or its relationship to the NWMLS enforcement dispute would have entered a permanent legislative transcript — available to NWMLS trial counsel as a party admission under FRE 801(d)(2) at trial. The statements she made freely to Inman — characterizing NWMLS enforcement as monopolistic control — were made in a forum that carries no discovery exposure. Her silence in the hearing room was not modesty. It was the corporate legal strategy operating through personnel assignment.

Huff’s deflections confirm this reading. ‘That is probably above what I feel comfortable speaking to’ is not the answer of an unprepared witness. It is the answer of a witness who has been instructed precisely what she is and is not authorized to say, by an executive who is watching from the room and cannot say it herself. The delegation preserved the executive record while the Managing Director absorbed the cross-examination. That is what the Ghost Panel strategy looks like at the witness level — and what the Nelson substitution looks like at the executive level. One firm, two tiers of insulation, both operating simultaneously across both chambers.

The documentation is in the public record. Skillman posted photographs from the January 28 House hearing, tagging @compasswashington, with the caption: ‘Thank you to our EXTRAORDINARY leadership team at @compasswashington for pushing against extremely strong headwinds in Olympia right now.’ Nelson is in the building. Nelson is the leadership. Nelson is silent in the transcript. The consumer-choice frame is carried by the Managing Director, deflected when it meets the business model question, and protected at the executive level by the Regional VP who built it in trade press. That architecture is documented across the hearing records in The Compass Astroturf Coefficient at the Washington State Senate and HB 2512 and the Collapse of Compass’s Coordinated Opposition.

The structural diagnosis behind these exchanges is named Narrative Arbitrage in How Compass’s State Legislative Testimony Undermined Its Federal Antitrust Claims: framing the same business practice as pro-competitive innovation, consumer privacy protection, or anti-monopoly rebellion depending on which story serves the immediate objective. Narrative arbitrage works only when forums remain siloed. The Washington hearings collapsed the silo — placing Compass’s federal litigation posture and its state legislative testimony in the same public record simultaneously. Every state that holds hearings generates the same collapse.

The Coasean Foundation: Why the Frame Is Structurally Incoherent

The deepest problem with the consumer-choice frame is not rhetorical. It is analytical. MindCast AI’s Chicago School Accelerated Part I: Coase and Why Transaction Costs ≠ Coordination Costs establishes the foundational distinction: transaction costs and coordination costs are analytically independent categories. Zero transaction costs do not guarantee efficient outcomes when coordination architecture is absent. The distinction is directly applicable to the MLS debate.

Federal antitrust analysis — and Compass’s own litigation framing — treats MLS rules as friction-generating cartels. The implicit theory: MLS submission requirements create transaction costs; removing them liberates markets. That theory is wrong, and Compass’s Coasean Coordination Problem Part I: How Private Exclusives Reshape Competition and Threaten MLS Stability formalizes why. MLS systems do not create transaction costs. MLS systems solve a coordination cost problem: they provide the focal point (shared reference for where listings appear), trust infrastructure (verified data, professional accountability), and narrative alignment (common understanding of how markets operate) that enable millions of one-time participants to match efficiently in a compressed timeframe.

The consumer-choice frame, translated into Coasean terms, argues that reducing the focal point constraint liberates buyers and sellers to bargain more efficiently. The coordination cost framework shows the opposite: removing the focal point does not reduce friction within the bargaining mechanism — it destroys the mechanism’s ability to engage at all. Buyers who cannot know whether their search is complete cannot make efficient decisions. Sellers who cannot assess full market exposure cannot price accurately. Price discovery degrades. Search friction rises. The market fragments into incompatible private networks where inventory access is a function of brokerage affiliation rather than market participation.

This is precisely the outcome the Washington legislative record documented in real time. The independent brokers who testified for SSB 6091 were not arguing ideology. They were identifying the coordination cost effect: private listing networks drive consolidation that eliminates the firms that sustain broad market participation. Nicole Bascom-Green stated it directly — Compass wants to control all the flow of information for specific spaces. Tracy Choate stated it directly — private exclusive networks are poised to drive brokerage consolidation that eliminates small brokerages. Both observations follow from the coordination cost framework: once inventory is sequestered behind a proprietary network, access to the focal point is a function of firm size, not market participation.

The consumer-choice frame therefore fails not just empirically — as the hearing record demonstrates — but analytically. It treats what destroys coordination architecture as if it were the exercise of market freedom. The MLS is not a restriction on consumer choice. The MLS is the infrastructure that makes competitive consumer choice possible by ensuring all buyers see all publicly marketed listings at the same time. Consumer choice, properly understood, requires the focal point. Compass’s model destroys it.

The Washington Senate voted 49–0. The House voted 92–1. Those margins do not reflect a close call on a contested consumer welfare question. They reflect institutional actors evaluating a claim about consumer welfare against the coordination cost reality the claim obscures — and finding the claim analytically empty on every forum where it was tested under neutral questioning.

XI. Conclusion: Consumer Choice as Control

Consumer choice is not the governing objective within the Compass model. It is the language used to defend a system optimized for control over transaction pathways.

The decode table in Section II, the forum matrix in Section IV, and the forward lock in Section V provide the tools to identify and evaluate every future deployment of this frame. The Skillman Moment in Section VI provides the field-test calibration reference. The Zillow arc in Section VII provides the closed evidentiary foundation. The runtime module in Section VIII provides the standing classification architecture. The Lone Wolf analysis in Section X provides the legislative and Coasean proof that the frame is not just rhetorically defeated but analytically incoherent.

Multi-state legislative momentum, platform enforcement, and litigation scrutiny are converging on a single definition of choice: access. Washington has enacted that definition into statute and enforced it through the most decisive bicameral vote in the SB 6091 legislative record. Wisconsin and Illinois are in the diffusion sequence. The NWMLS trial in October 2026 is the next confirmation event.

The outcome will be determined by which definition becomes enforceable at scale. Washington shows where the conflict resolves. Seller choice does not govern listing exposure once public marketing begins. Market structure does.

Whoever governs listing exposure governs the structure of the housing market itself.