MCAI Lex Vision: Oracle, OpenAI, and the Capacity Economy — Inside the AI Infrastructure-Financing Lawsuit

AI Accountability, When AI Promises Meet the Courts Series: When AI Promises Meet the Courts series. Why Barrows v. Oracle Tests Whether Markets Can Price the AI Buildout — Not Whether the AI Works

AI Accountability: When AI Promises Meet the Courts

Oracle, OpenAI, and the Capacity Economy — Inside the AI Infrastructure-Financing Lawsuit

Apple’s AI Illusion Narrative Control and the Law’s Search for Structural Truth

Executive Summary

Oracle spent 2025 remaking itself from a database company into one of the largest financiers of the artificial-intelligence buildout, and by December the market had begun to doubt the remake could pay for itself. A securities class action followed in February 2026, alleging that the company assured investors its enormous capital spending would convert into revenue almost immediately while playing down how much debt, how much off-balance-sheet obligation, and how much dependence on a single customer the strategy actually carried. The complaint is unproven and Oracle has not yet answered it. The significance lies elsewhere: Oracle may be the first large-scale test of whether public markets can accurately price the financing behind the AI buildout, rather than merely another dispute over whether the technology works.

AI-era securities litigation is migrating, and Oracle marks the migration’s leading edge. An earlier wave of cases policed what companies claimed their AI could do — the capability disputes that produced the Apple and Tesla matters. A newer wave polices what companies disclose about the cost of building the infrastructure that AI runs on — the capacity disputes that now reach the largest cloud operators. Read alongside its companion study of Microsoft, Oracle completes a four-part map of AI accountability: Apple’s narrative arbitrage, Tesla’s conversion of a capability claim into a hardware-substrate liability, Microsoft’s governance and forecasting failure, and Oracle’s capacity-financing exposure. The four are distinct forms of one underlying problem — a confident signal outrunning the substrate beneath it — and the map, more than any single case, is the durable contribution.

To test whether Oracle is representative or anomalous, MindCast ran the matter through its Cognitive Digital Twin foresight simulation, which classified the company not as a cloud business facing a question about AI capability but as an infrastructure-financing system facing a capacity-economy transition. The central claim follows: the operative risk for the largest AI operators is no longer whether the technology works, but whether public markets can price the financing, counterparty concentration, and revenue timing the buildout demands (confidence ~75%). The study commits that claim to a dated falsification contract, and either the docket bears it out by 2028 or MindCast revises.

Background — Oracle’s Turn Into the Infrastructure Business

Oracle built its name on database software, and for most of its history the company’s fortunes tracked enterprise licensing rather than the construction of physical plant. The cloud era reset the proposition. Through Oracle Cloud Infrastructure the company entered the business of renting computing power, and the artificial-intelligence surge of 2024 and 2025 turned that side business into the company’s defining bet. Demand for the specialized hardware that trains and serves large models ran well ahead of supply, and Oracle moved to capture it by building data centers at a scale it had never before attempted.

The bet acquired a face in 2025, and the face was OpenAI. Oracle agreed to supply the ChatGPT maker with roughly $300 billion in computing power over about five years, anchored in the Stargate buildout, and the contracted backlog the company reports as remaining performance obligations leapt to $455 billion after a single quarter’s signings. Capital expenditure climbed to match, rising from a projection near $25 billion for fiscal 2026 to roughly $35 billion by September and to approximately $50 billion by December. Executives framed the spending as nearly self-liquidating, telling investors the equipment would begin generating revenue almost as soon as it was installed.

The financing underneath the bet drew scrutiny well before the stock broke. S&P and Moody’s each moved Oracle’s outlook to negative during the summer of 2025, citing weak cash flow, rising leverage, and uncertainty about how a company would fund spending of this magnitude. By autumn Oracle carried long-term debt near $82 billion against a debt-to-equity ratio analysts placed around 450%, and its free cash flow had turned sharply negative. Management’s reassurances and the rating agencies’ warnings pointed in opposite directions, and the distance between them is where the litigation now sits.

Oracle did not reach the courthouse alone. AI-related securities suits had been accumulating for two years, most of them against smaller companies whose capability claims outran their products. The Oracle complaint, like the Microsoft complaint months earlier, signals something newer — litigation reaching the largest infrastructure operators and turning on the economics of the buildout rather than the performance of the models. Reading that shift, rather than re-trying Oracle, is the work of the study that follows.

A Note on Method — The Inversion

A single lawsuit can anchor a thesis, and a single lawsuit cannot prove one. The companion vision to this study, MindCast | The Microsoft Shareholder Suit and the Arrival of AI’s Third Phase, reasoned from one institution outward — it took the Microsoft shareholder suit and argued a general claim about AI-era accountability. The study here runs the method in reverse. Starting from the population of AI-related securities litigation and reasoning inward, it asks whether the general claim survives contact with the docket as a whole.

The two halves complete one method rather than repeating it. Reasoning from an institution risks special pleading — any one company’s troubles can be explained away as idiosyncratic. Reasoning from the docket risks pattern-hunting — any large enough pile of lawsuits will show some shape if squinted at. Run together, each checks the other: the institution supplies the mechanism, the population supplies the evidence that the mechanism recurs. Microsoft appears below only as one data point inside a wave, deliberately de-centered, because the finding that matters is invisible from inside any single case.

I. The Docket Is the Signal

AI-related allegations have become a structural feature of securities litigation rather than a novelty. Filings invoking artificial intelligence now make up a meaningful and growing share of total securities class actions, and the early entries clustered around a recognizable claim: a company broadcast a confident capability or growth narrative, an adverse reality surfaced, and the stock repriced. Through 2025, those suits largely involved relatively smaller corporate defendants.

The wave sorts into two category, and the distinction is the spine of this study. The first category is narrative arbitrage — overstatement of capability or timeline against a substrate that cannot yet deliver it. The second category is allocation and infrastructure disclosure — concealment or understatement of the capital, capacity, and execution reality beneath an AI growth story. Capability deception drives the first. Spend-and-capacity opacity drives the second.

The forcing functions differ by category, and naming them sharpens the sort. A narrative-arbitrage case breaks on a capability event — an admission, a failed demonstration, a benchmark exposure. An allocation case breaks on a financial event — an earnings miss, a capex disclosure, a withdrawn backer. Each category fails in its own characteristic way, and the way it fails identifies which one it belongs to.

II. The Capability Cases — Narrative Arbitrage

Narrative arbitrage sells a future as a present. Capability that does not yet exist, or exists only in bounded conditions, gets marketed as delivered and reliable, and the arbitrage yield is the valuation premium the narrative carries until a forcing function collapses it.

Apple and Tesla define the category, and MindCast has analyzed both in full. MindCast | Apple’s AI Illusion traced the iPhone 16 “Apple Intelligence” campaign through the firm’s Cognitive Signal Integrity diagnostic, reading confident public timelines coordinated with undisclosed internal engineering limits as narrative arbitrage — the systematic exploitation of the temporal gap between a market promise and operational feasibility. The term originates there, and it governs the category. Apple’s exposure surfaced in paired forums: Tucker v. Apple, a Rule 10b-5 securities action covering June 2024 to March 2025, and Landsheft v. Apple, a California false-advertising and unfair-competition action — after roughly $900 billion in market value rode on features presented as delivery-ready that the company later deferred to 2026 or beyond. MindCast | Tesla’s Self-Driving Revolt read the Full Self-Driving cascade as the identical architecture across a longer horizon, with categorical autonomy language running ahead of a constrained engineering substrate. Both carry the same signature: the deception, if proven, concerns existence and timing, and the correction arrives when the gap between claim and substrate becomes undeniable.

Referencing rather than re-litigating the two cases is deliberate. The point here is not to re-prove either, but to fix the category clearly enough that the migration away from it becomes visible.

III. The Hinge — How Tesla Converts One Category Into the Other

Tesla matters to this study for a reason that has nothing to do with cars. Its exposure began as pure narrative arbitrage — a capability claim — and then mutated into something structurally different. The January 2025 admission that Hardware 3 vehicles cannot deliver the promised autonomy converted the dispute from “the software is not ready” into “the physical substrate sold to roughly four million owners cannot run what was advertised.” Capability deception hardened into a hardware-substrate liability.

The mutation is the migration in miniature. A claim about what the product does became a claim about what the underlying infrastructure can support, and the legal exposure shifted accordingly — from representations that might be defended as forward-looking toward a fixed physical shortfall that cannot be re-characterized. Tesla shows the mechanism by which the docket’s center of gravity moves: capability stories, pressed long enough against a hard substrate, become infrastructure stories. The hinge is not a tidy third bucket. The hinge is the process that carries cases from the first category to the second.

Contact mcai@mindcast-ai.com to partner with us on Predictive Game Theory AI in Law and Behavioral Economics. To deep dive on MindCast works upload the URL of this publication into any LLM (preferably Google AI mode/Gemini, Claude, ChatGPT) and prompt ‘reconstruct MindCast framework with three degrees of cited sub links.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure.

MindCast AI is a cybernetic, predictive game-theory AI firm specializing in law and behavioral economics, applied to complex litigation, innovation systems, and geopolitical risk intelligence. Rather than extrapolating historical patterns, the firm models the mechanisms that generate institutional behavior, running Cognitive Digital Twin simulations grounded in Nash equilibrium, Stigler information economics, and the Chicago School of law and behavioral economics.

Related series:

Cybernetic Overview of The MindCast Consumer AI Device Series

The Power Stack, How Energy Infrastructure Became the New AI Battleground

IV. The Capacity Case — Barrows v. Oracle

The allocation category does not dispute whether the AI works. It disputes whether the company told the market the truth about the spend and capacity beneath it. The concealed fact is financial and physical — capex scale, counterparty concentration, free-cash-flow strain, the timing of returns — rather than a capability claim. Oracle states the category in unusually clean form, which is why it anchors this study.

The Case and the Defendants

The case is identifiable and recent. Barrows v. Oracle Corporation (No. 1:26-cv-00127-JLH, D. Del.), filed February 3, 2026 before Judge Jennifer L. Hall, pleads Section 10(b) and Rule 10b-5 claims against all defendants and Section 20(a) control-person claims against the individuals, on behalf of investors who acquired Oracle stock between June 12 and December 16, 2025. The named defendants are the company plus its most senior leadership: Executive Chairman and Chief Technology Officer Lawrence Ellison; Safra Catz, chief executive until September 22, 2025 and Executive Vice Chair after; co-chief executives Clayton Magouyrk and Michael Sicilia; Principal Financial Officer Douglas Kehring; and Chief Accounting Officer Maria Smith. Reaching the people who set and narrated the spending strategy, rather than peripheral actors, is what gives the scienter theory its footing. The defendant itself marks the migration this study tracks. Earlier AI-related suits clustered on smaller, pure-play vendors; a complaint of this kind against an operator of Oracle’s scale signals the docket climbing toward the largest infrastructure builders — exactly the movement Section V names.

The Alleged Misrepresentation

The theory is allocation, not capability. Oracle, the plaintiffs allege, touted its contracts to build data-center capacity for AI infrastructure and assured investors the spending would convert into revenue almost immediately — Catz told analysts the company had clear line-of-sight to spend on capex “right before it starts generating revenue” and described the model as “asset-pretty-light,” while Ellison called demand “insatiable.” The complaint alleges those assurances omitted that the strategy would drive enormous capex without equivalent near-term revenue, that the spending threatened Oracle’s debt, credit rating, free cash flow, and ability to fund its projects, and — most concretely — that the “asset-light” framing concealed roughly $248 billion in off-balance-sheet lease commitments. The dispute is not whether Oracle’s cloud can run AI workloads. The dispute is whether a spend-now-earn-right-away narrative outran the financial reality, and whether the balance sheet investors saw matched the obligations the company had actually incurred.

The Corrective Cascade

The correction arrived not in one stroke but as a cascade of at least five revelations across nearly three months, and the staging carries analytic weight. S&P reiterated a negative credit outlook on September 24, 2025, flagging that OpenAI — which had agreed to buy $300 billion in computing power from Oracle over roughly five years — could account for more than a third of Oracle’s revenue by fiscal 2028, and the stock fell about 2%. The next day Rothschild & Co. Redburn initiated coverage at “Sell” with a $175 target, warning the market “materially overestimates” Oracle’s contracted cloud revenues and casting the company as closer to a financier than a cloud provider, and the stock fell another 5.5%. The largest break came on December 10–11, when Oracle’s second-quarter results showed revenue below consensus, capex well above estimates, and negative free cash flow exceeding $10 billion — with Kehring disclosing fiscal-2026 capex of roughly $50 billion against unchanged revenue guidance, the cost of insuring Oracle’s debt hitting a sixteen-year high, and the stock dropping 11% from $223.01 to $198.85. The 10-Q filed the next evening revealed roughly $248 billion in off-balance-sheet lease commitments — up from under $100 billion the prior quarter, a figure analysts called a “bombshell,” with long-dated leases mismatched against shorter customer contracts — alongside Bloomberg’s report that Oracle had pushed OpenAI data-center completion dates from 2027 to 2028, and the stock fell another 4.5%. Finally, on December 17, the Financial Times reported that Blue Owl Capital, the primary backer of Oracle’s largest U.S. data-center projects, had withdrawn from funding a $10 billion facility built to serve OpenAI, and the stock fell a further 5.4%.

One Gap, Two Forcing Functions

The shape maps onto the allocation category and onto its institutional twin. Oracle’s alleged wrong — a spend-and-capacity narrative running ahead of disclosed financial exposure — is the same gap MindCast | The Microsoft Shareholder Suit and the Arrival of AI’s Third Phase names as Governance Debt at Microsoft, here visible from the market’s side as a disclosure question. The forcing functions differ in a way worth marking. Microsoft’s gap collapsed in a single session on one earnings surprise; Oracle’s bled out across a quarter through five separate revelations — a credit warning, a sell-side downgrade, an earnings miss, an off-balance-sheet lease disclosure, and a backer’s withdrawal. A multi-stage cascade is a slower-burning registration lag, and the slowness is the uncomfortable finding: the market held the capacity narrative through a ratings warning and a 40%-downside sell call in September, and only fully repriced in December when the balance-sheet reality and the financing cracks arrived together. Visible strain did not force recognition; only the hard numbers did.

The Counterparty Signature

The OpenAI concentration gives Oracle its signature. A $300 billion compute commitment from a single counterparty, projected to supply more than a third of Oracle’s revenue within a few years, is a capacity bet dressed as demand strength — committed buildout staked on one customer’s continued spending, returns deferred to fiscal years not yet arrived, and a buyer that analysts openly doubted could fund its own obligations. The registration lag here is literal: capital spent now against revenue promised later, on leases running fifteen to nineteen years against customer contracts far shorter, with the market pricing the promise before testing whether the counterparty could pay for it.

Capacity, Not Capability

Oracle sits at the opposite pole from the series’ capability cases, and the contrast sharpens both ends. MindCast | Apple’s AI Illusion and MindCast | Tesla’s Self-Driving Revolt concern features sold before they existed — a deception, if proven, about the product. Oracle concerns spending disclosed without its risk — a deception, if proven, about the balance sheet. Tesla marks the bridge between the two, where a capability claim hardened into a hardware-substrate liability; Oracle is already fully substrate-side, contesting infrastructure economics rather than product capability. The series therefore spans the whole arc, from what the model promises to what the buildout costs.

Procedural Posture

The posture is early, and the timeline disciplines any reading of the case’s strength. Lead-plaintiff contests resolved on April 27, 2026, when the court appointed two European institutional investors — Sparinvest S.A. and SEB Funds AB — as lead plaintiffs, with Kessler Topaz Meltzer & Check as lead counsel; Barrows was the named filer who started the PSLRA clock, not the steward of the operative case. Serious foreign institutional capital taking the lead against a top-tier infrastructure operator is itself a data point for the migration thesis — the allocation category now draws the kind of plaintiff that picks its targets deliberately. By stipulated order, the defendants need not respond until the lead plaintiffs file an amended or consolidated complaint, due July 14, 2026, with an answer due September 16 and any motion-to-dismiss briefing running through December 2026. Oracle has therefore entered no responsive pleading and no denial on the record; its position rests on public statements, and the absence of a reply reflects the court-ordered sequence rather than concession.

The Scienter Edge

The scienter allegations are the complaint’s hardest edge, and they are concrete rather than inferential. Oracle’s senior executives sold more than 8.85 million personally held shares during the class period for combined proceeds exceeding $1.87 billion. Catz accounts for nearly all of it — roughly 8.7 million shares for more than $1.82 billion, more than double her selling in the comparable prior period — and she relinquished the chief-executive title on September 22, 2025, weeks before the September 24 ratings warning began the repricing. Magouyrk, Sicilia, and Smith each sold shares during the period after selling none in the comparable window before it. Suspicious timing and volume of insider sales is the classic scienter booster under the governing pleading standard, and a chief executive cashing out $1.82 billion and stepping down just ahead of the first corrective disclosure is the kind of particularized fact that survives a motion to dismiss where vaguer cases fail.

Reading the Strength

Candor about the anchor strengthens the thesis, and the primary source turns out stronger than the secondary coverage implied. The “premature” critique still has a foothold — Oracle did disclose that it was spending heavily, two ratings agencies had flagged the cash-flow strain by late July 2025, and a defense will recast the optimism as protected forward-looking projection and puffery. The complaint, though, does not rest there. The roughly $248 billion in off-balance-sheet lease commitments is a concrete omission rather than a difference of opinion about strategy, and the $1.87 billion in insider sales supplies particularized scienter, so the two elements most resistant to a motion to dismiss are precisely the ones a press-release summary buried. The pleading-stage test remains genuinely unrun, with the operative complaint not due until July 2026 and no motion to dismiss yet filed (confidence ~45% that the case draws a serious pleading-stage challenge on the strategic-judgment ground, revised down from the earlier read once the lease omission and insider sales came into view). The strain is still the point: the allocation category is new enough that courts have not settled where aggressive-but-disclosed spending ends and actionable omission begins, and a case sitting on that boundary — but armed with a concrete omission and concrete insider selling — is what a maturing category looks like as doctrine begins to harden around it.

V. The Foresight Simulation — Oracle as a Capacity Economy

MindCast ran the matter through its own foresight engine, and the question put to the simulation was deliberately not the one the Microsoft analysis asked. Microsoft tested what happens when an institution cannot forecast the consequences of AI deployment; Oracle tests what happens when an institution cannot forecast the economics of AI infrastructure buildout. The Cognitive Digital Twin foresight engine constructed three twins — an Oracle Institutional Twin, a Counterparty Concentration Twin, and an Infrastructure Economy Twin — and they converged on a single classification: a Capacity Economy Transition event (composite confidence 83%).

One caveat governs how to read the result, carried over from the Microsoft analysis because the credibility standard does not relax between installments. The twins operate on the MindCast framework’s priors, so the exercise tests internal coherence and surfaces forward stress points rather than supplying evidence independent of the framework that built it. A self-run simulation cannot confirm a thesis from outside; it can fail to break one, and it can name the risk drivers a prose argument leaves implicit.

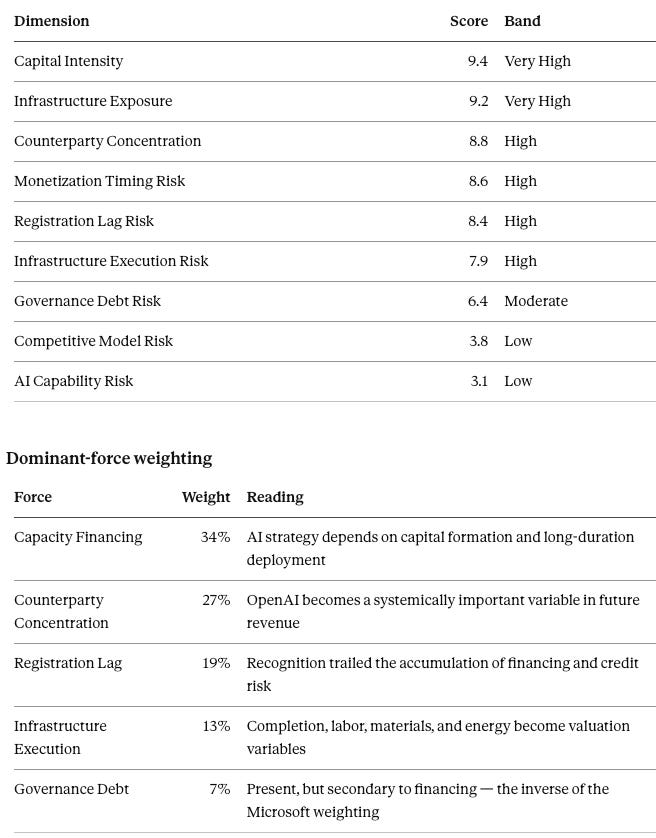

The three twins classified independently and converged. The Oracle Institutional Twin read the company less as a cloud provider than as an Infrastructure Financing System (85%), where revenue realization hangs on data-center completion, customer utilization, customer solvency, and future financing conditions rather than on AI capability. The Counterparty Concentration Twin produced a Counterparty Amplification Event (87%) and the simulation’s most distinctive signature — a Counterparty Dependency Index of 8.9, a Concentrated Dependency Regime — where the critical variable ceases to be Oracle and becomes OpenAI: Oracle’s financing, infrastructure, and revenue risk each transfer into OpenAI’s execution, funding, and adoption risk, with analysts in the complaint itself doubting the counterparty can fund its $300 billion commitment. Few infrastructure operators carry capex, spend, and financing needs; almost none stake more than a third of future revenue on a single customer who must simultaneously raise enormous capital of its own, which is what makes the dependency structure Oracle’s signature rather than a shared feature of the cohort. The Infrastructure Economy Twin generated a Capacity Economy Transition (81%), where the binding constraint migrates over time from models to GPUs to data centers to capital formation, and operators come to compete on financing, construction, energy access, and utilization rather than on capability. The two risk drivers the simulation ranked highest were the roughly $248 billion in long-duration off-balance-sheet lease commitments and the $1.87 billion in class-period insider sales — together the concrete omission and the concrete scienter a securities claim lives or dies on.

The distinctive output is the headline. Where the Microsoft simulation produced Governance Debt as its signature, Oracle’s produces the Capacity Economy Transition — the recognition that competition among the largest operators has shifted from building intelligence to financing the capacity that runs it, and that the accountability following the shift is capacity accountability rather than capability accountability. The two cases calibrate each other: Oracle’s AGE-derived governance reading registers strain rather than saturation, so Microsoft remains the cleaner Governance Debt case and Oracle the cleaner Capacity Economy case, the same gap viewed through the dominant force in each. The reading feeds directly into the migration the next section names, and it moved MindCast’s internal confidence in the capability-to-capacity thesis upward; the movement reflects strengthened internal coherence rather than external proof, held honest by the caveat above and tested only by the falsification contract that closes the study. Twin construction, the quantitative output matrix, the dominant-force weighting, and the composite indices sit in the Appendix.

VI. The Migration — The Finding the Population Reveals

No single case shows the docket moving. The migration exists only at the population level, and stating it is the contribution this study makes that the institution-anchored vision structurally could not.

The center of gravity is shifting from the first category toward the second. Early AI-era securities pressure concentrated on capability claims, often against smaller pure-play AI companies. The 2026 wave reaches the largest infrastructure operators and turns on the disclosure of spend and capacity — Oracle on capex and counterparty concentration, Microsoft on capacity rationing behind a demand narrative. The defendants are getting larger, and the concealed fact is moving down the stack, from what the model can do to what the buildout costs and whether the capacity exists to deliver it (confidence ~75%, held there because the allocation-category population is still small). The MAP CDT simulation in Section V names the destination of that movement — a Capacity Economy Transition, in which the largest operators compete on financing, construction, and capacity utilization rather than on capability itself.

Tesla explains why the migration happens rather than merely that it does. Capability narratives are defensible as forward-looking right up until they meet a hard substrate — unbuilt hardware, finite compute, committed-but-unbuilt data centers. Once the substrate binds, the claim stops being about the future and becomes about a fixed, present shortfall, and the exposure converts from the narrative category to the allocation category. The AI industry is now spending hundreds of billions against substrates that bind in exactly that way, which is why the docket should be expected to keep migrating in the same direction.

VII. What the Migration Means

The migration carries a lesson past any of the four companies. Capability litigation polices what a company claims about its technology; allocation litigation polices what a company discloses about the institution running it. The second is harder to manage, because it requires a firm to forecast and disclose its own spend-and-capacity trajectory accurately — continuously, against a quarterly reporting rhythm, while the operating reality moves underneath it.

Forecasting accuracy becomes the operative capability, and the conclusion holds independent of any verdict. Whether Oracle’s case proves premature, whether Microsoft prevails, whether Apple and Tesla settle, the docket has already shifted its weight from capability toward capacity. Companies that deploy AI into infrastructure-heavy operations now carry an exposure that no amount of model performance retires — the exposure of a spend-and-capacity reality outrunning the disclosure that describes it. The instrument for managing that exposure is foresight applied as a disclosure-integrity layer, the subject of the companion vision.

VIII. Forecast and Falsification Contract

The study commits its central finding to a dated, falsifiable forecast.

Forecast. Through the end of 2028, the AI securities docket’s center of gravity continues migrating from narrative-arbitrage cases against smaller capability vendors toward allocation-and-infrastructure-disclosure cases against the largest compute and cloud operators. Probability 70–80%.

Confirms. A majority of new large-capitalization AI-related securities actions through the window turn on capex scale, lease and financing-structure disclosure, counterparty concentration, capacity utilization, or ROI-timing disclosure rather than on capability or benchmark misstatement; and the named infrastructure operators face disclosure suits at a higher rate than capability suits.

Falsifies. Capability and AI-washing claims remain the dominant category across the window, the largest infrastructure operators avoid allocation-disclosure suits, and no migration in defendant size or concealed-fact type is observable in the filing record.

Measurement window. Through December 31, 2028, scoped to AI-related securities actions against operators with material compute or cloud-infrastructure exposure.

A second forecast follows from the same logic and is stated separately because it concerns valuation rather than litigation. Through the end of 2028, the largest AI infrastructure operators will increasingly be valued as financing systems rather than software systems — priced on capital intensity, counterparty concentration, free-cash-flow trajectory, and the spread between committed obligations and contracted revenue, with model capability receding as a valuation driver among this cohort. Probability 65–75%. The forecast confirms if sell-side and credit coverage of these operators measurably shifts weight toward financing and capacity metrics over capability metrics across the window; it falsifies if capability and benchmark narratives continue to set the valuations of the largest operators with no observable move toward financing-system framing.

MindCast either meets the falsification standard or does not publish.

Appendix — Foresight Simulation (Oracle): Construction and Quantitative Signatures

The simulation summarized in Section V rests on three twins and a set of composite signatures, specified below. Confidence figures, dimension scores, and indices are the simulation’s own outputs rather than external measurements: they represent relative dominance rankings the Cognitive Digital Twin simulation produced across the modeled forces, not financial ratios measured from Oracle’s statements. The decimal precision reflects the model’s internal scaling, not surveyed data, and the shared-priors caveat from Section V governs all of them. Read the numbers as ordered signatures — which forces dominate, which risks rank highest, how Oracle sits relative to Microsoft — rather than as calibrated quantities.

Twin 1 — Oracle Institutional Twin. Inputs: OCI growth, OpenAI contracts, RPO expansion, data-center commitments, and capex escalation across the class period from roughly $25 billion to $35 billion to approximately $50 billion. Dominant force: capacity financing. Finding: Oracle increasingly resembles a financing vehicle attached to AI infrastructure, with revenue realization contingent on data-center completion, customer utilization, customer solvency, and future financing conditions rather than on capability. Classification: Infrastructure Financing System (85%).

Twin 2 — Counterparty Concentration Twin. Inputs: OpenAI commitments, revenue projections, capacity commitments. Dominant force: dependency risk. Finding: the critical variable migrates from Oracle to OpenAI, with Oracle’s financing, infrastructure, and revenue risk transferring into OpenAI’s execution, funding, and adoption risk — a single counterparty projected to supply more than a third of revenue against a $300 billion commitment the counterparty may be unable to fund. Classification: Counterparty Amplification Event (87%).

Twin 3 — Infrastructure Economy Twin. Participants: Oracle, Microsoft, Amazon, Google, OpenAI. Dominant force: capacity arms race. Finding: the binding constraint migrates from models (2023) to GPUs (2024) to data centers (2025) to capital formation (2026 forward), and operators come to compete on financing, construction, energy access, and capacity utilization rather than on capability. Classification: Capacity Economy Transition (82%).

Composite. System classification: Capacity Economy Transition event. Dominant forces: capacity financing, counterparty concentration, and registration lag, with the roughly $248 billion in off-balance-sheet lease commitments and the $1.87 billion in class-period insider sales ranked as the highest concrete risk drivers. Composite confidence: 83%.

Quantitative output matrix

The matrix carries the thesis in one view: the two highest-scored dimensions are financial, and the two lowest are about the technology itself.

IV. The Capacity Case — Barrows v. Oracle

The allocation category does not dispute whether the AI works. It disputes whether the company told the market the truth about the spend and capacity beneath it. The concealed fact is financial and physical — capex scale, counterparty concentration, free-cash-flow strain, the timing of returns — rather than a capability claim. Oracle states the category in unusually clean form, which is why it anchors this study.

The Case and the Defendants

The case is identifiable and recent. Barrows v. Oracle Corporation (No. 1:26-cv-00127-JLH, D. Del.), filed February 3, 2026 before Judge Jennifer L. Hall, pleads Section 10(b) and Rule 10b-5 claims against all defendants and Section 20(a) control-person claims against the individuals, on behalf of investors who acquired Oracle stock between June 12 and December 16, 2025. The named defendants are the company plus its most senior leadership: Executive Chairman and Chief Technology Officer Lawrence Ellison; Safra Catz, chief executive until September 22, 2025 and Executive Vice Chair after; co-chief executives Clayton Magouyrk and Michael Sicilia; Principal Financial Officer Douglas Kehring; and Chief Accounting Officer Maria Smith. Reaching the people who set and narrated the spending strategy, rather than peripheral actors, is what gives the scienter theory its footing. The defendant itself marks the migration this study tracks. Earlier AI-related suits clustered on smaller, pure-play vendors; a complaint of this kind against an operator of Oracle’s scale signals the docket climbing toward the largest infrastructure builders — exactly the movement Section V names.

The Alleged Misrepresentation

The theory is allocation, not capability. Oracle, the plaintiffs allege, touted its contracts to build data-center capacity for AI infrastructure and assured investors the spending would convert into revenue almost immediately — Catz told analysts the company had clear line-of-sight to spend on capex “right before it starts generating revenue” and described the model as “asset-pretty-light,” while Ellison called demand “insatiable.” The complaint alleges those assurances omitted that the strategy would drive enormous capex without equivalent near-term revenue, that the spending threatened Oracle’s debt, credit rating, free cash flow, and ability to fund its projects, and — most concretely — that the “asset-light” framing concealed roughly $248 billion in off-balance-sheet lease commitments. The dispute is not whether Oracle’s cloud can run AI workloads. The dispute is whether a spend-now-earn-right-away narrative outran the financial reality, and whether the balance sheet investors saw matched the obligations the company had actually incurred.

The Corrective Cascade

The correction arrived not in one stroke but as a cascade of at least five revelations across nearly three months, and the staging carries analytic weight. S&P reiterated a negative credit outlook on September 24, 2025, flagging that OpenAI — which had agreed to buy $300 billion in computing power from Oracle over roughly five years — could account for more than a third of Oracle’s revenue by fiscal 2028, and the stock fell about 2%. The next day Rothschild & Co. Redburn initiated coverage at “Sell” with a $175 target, warning the market “materially overestimates” Oracle’s contracted cloud revenues and casting the company as closer to a financier than a cloud provider, and the stock fell another 5.5%. The largest break came on December 10–11, when Oracle’s second-quarter results showed revenue below consensus, capex well above estimates, and negative free cash flow exceeding $10 billion — with Kehring disclosing fiscal-2026 capex of roughly $50 billion against unchanged revenue guidance, the cost of insuring Oracle’s debt hitting a sixteen-year high, and the stock dropping 11% from $223.01 to $198.85. The 10-Q filed the next evening revealed roughly $248 billion in off-balance-sheet lease commitments — up from under $100 billion the prior quarter, a figure analysts called a “bombshell,” with long-dated leases mismatched against shorter customer contracts — alongside Bloomberg’s report that Oracle had pushed OpenAI data-center completion dates from 2027 to 2028, and the stock fell another 4.5%. Finally, on December 17, the Financial Times reported that Blue Owl Capital, the primary backer of Oracle’s largest U.S. data-center projects, had withdrawn from funding a $10 billion facility built to serve OpenAI, and the stock fell a further 5.4%.

One Gap, Two Forcing Functions

The shape maps onto the allocation category and onto its institutional twin. Oracle’s alleged wrong — a spend-and-capacity narrative running ahead of disclosed financial exposure — is the same gap MindCast | The Microsoft Shareholder Suit and the Arrival of AI’s Third Phase names as Governance Debt at Microsoft, here visible from the market’s side as a disclosure question. The forcing functions differ in a way worth marking. Microsoft’s gap collapsed in a single session on one earnings surprise; Oracle’s bled out across a quarter through five separate revelations — a credit warning, a sell-side downgrade, an earnings miss, an off-balance-sheet lease disclosure, and a backer’s withdrawal. A multi-stage cascade is a slower-burning registration lag, and the slowness is the uncomfortable finding: the market held the capacity narrative through a ratings warning and a 40%-downside sell call in September, and only fully repriced in December when the balance-sheet reality and the financing cracks arrived together. Visible strain did not force recognition; only the hard numbers did.

The Counterparty Signature

The OpenAI concentration gives Oracle its signature. A $300 billion compute commitment from a single counterparty, projected to supply more than a third of Oracle’s revenue within a few years, is a capacity bet dressed as demand strength — committed buildout staked on one customer’s continued spending, returns deferred to fiscal years not yet arrived, and a buyer that analysts openly doubted could fund its own obligations. The registration lag here is literal: capital spent now against revenue promised later, on leases running fifteen to nineteen years against customer contracts far shorter, with the market pricing the promise before testing whether the counterparty could pay for it.

Capacity, Not Capability

Oracle sits at the opposite pole from the series’ capability cases, and the contrast sharpens both ends. MindCast | Apple’s AI Illusion and MindCast | Tesla’s Self-Driving Revolt concern features sold before they existed — a deception, if proven, about the product. Oracle concerns spending disclosed without its risk — a deception, if proven, about the balance sheet. Tesla marks the bridge between the two, where a capability claim hardened into a hardware-substrate liability; Oracle is already fully substrate-side, contesting infrastructure economics rather than product capability. The series therefore spans the whole arc, from what the model promises to what the buildout costs.

Procedural Posture

The posture is early, and the timeline disciplines any reading of the case’s strength. Lead-plaintiff contests resolved on April 27, 2026, when the court appointed two European institutional investors — Sparinvest S.A. and SEB Funds AB — as lead plaintiffs, with Kessler Topaz Meltzer & Check as lead counsel; Barrows was the named filer who started the PSLRA clock, not the steward of the operative case. Serious foreign institutional capital taking the lead against a top-tier infrastructure operator is itself a data point for the migration thesis — the allocation category now draws the kind of plaintiff that picks its targets deliberately. By stipulated order, the defendants need not respond until the lead plaintiffs file an amended or consolidated complaint, due July 14, 2026, with an answer due September 16 and any motion-to-dismiss briefing running through December 2026. Oracle has therefore entered no responsive pleading and no denial on the record; its position rests on public statements, and the absence of a reply reflects the court-ordered sequence rather than concession.

The Scienter Edge

The scienter allegations are the complaint’s hardest edge, and they are concrete rather than inferential. Oracle’s senior executives sold more than 8.85 million personally held shares during the class period for combined proceeds exceeding $1.87 billion. Catz accounts for nearly all of it — roughly 8.7 million shares for more than $1.82 billion, more than double her selling in the comparable prior period — and she relinquished the chief-executive title on September 22, 2025, weeks before the September 24 ratings warning began the repricing. Magouyrk, Sicilia, and Smith each sold shares during the period after selling none in the comparable window before it. Suspicious timing and volume of insider sales is the classic scienter booster under the governing pleading standard, and a chief executive cashing out $1.82 billion and stepping down just ahead of the first corrective disclosure is the kind of particularized fact that survives a motion to dismiss where vaguer cases fail.

Reading the Strength

Candor about the anchor strengthens the thesis, and the primary source turns out stronger than the secondary coverage implied. The “premature” critique still has a foothold — Oracle did disclose that it was spending heavily, two ratings agencies had flagged the cash-flow strain by late July 2025, and a defense will recast the optimism as protected forward-looking projection and puffery. The complaint, though, does not rest there. The roughly $248 billion in off-balance-sheet lease commitments is a concrete omission rather than a difference of opinion about strategy, and the $1.87 billion in insider sales supplies particularized scienter, so the two elements most resistant to a motion to dismiss are precisely the ones a press-release summary buried. The pleading-stage test remains genuinely unrun, with the operative complaint not due until July 2026 and no motion to dismiss yet filed (confidence ~45% that the case draws a serious pleading-stage challenge on the strategic-judgment ground, revised down from the earlier read once the lease omission and insider sales came into view). The strain is still the point: the allocation category is new enough that courts have not settled where aggressive-but-disclosed spending ends and actionable omission begins, and a case sitting on that boundary — but armed with a concrete omission and concrete insider selling — is what a maturing category looks like as doctrine begins to harden around it.

V. The Foresight Simulation — Oracle as a Capacity Economy

MindCast ran the matter through its own foresight engine, and the question put to the simulation was deliberately not the one the Microsoft analysis asked. Microsoft tested what happens when an institution cannot forecast the consequences of AI deployment; Oracle tests what happens when an institution cannot forecast the economics of AI infrastructure buildout. The Cognitive Digital Twin foresight engine constructed three twins — an Oracle Institutional Twin, a Counterparty Concentration Twin, and an Infrastructure Economy Twin — and they converged on a single classification: a Capacity Economy Transition event (composite confidence 83%).

One caveat governs how to read the result, carried over from the Microsoft analysis because the credibility standard does not relax between installments. The twins operate on the MindCast framework’s priors, so the exercise tests internal coherence and surfaces forward stress points rather than supplying evidence independent of the framework that built it. A self-run simulation cannot confirm a thesis from outside; it can fail to break one, and it can name the risk drivers a prose argument leaves implicit.

The three twins classified independently and converged. The Oracle Institutional Twin read the company less as a cloud provider than as an Infrastructure Financing System (85%), where revenue realization hangs on data-center completion, customer utilization, customer solvency, and future financing conditions rather than on AI capability. The Counterparty Concentration Twin produced a Counterparty Amplification Event (87%) and the simulation’s most distinctive signature — a Counterparty Dependency Index of 8.9, a Concentrated Dependency Regime — where the critical variable ceases to be Oracle and becomes OpenAI: Oracle’s financing, infrastructure, and revenue risk each transfer into OpenAI’s execution, funding, and adoption risk, with analysts in the complaint itself doubting the counterparty can fund its $300 billion commitment. Few infrastructure operators carry capex, spend, and financing needs; almost none stake more than a third of future revenue on a single customer who must simultaneously raise enormous capital of its own, which is what makes the dependency structure Oracle’s signature rather than a shared feature of the cohort. The Infrastructure Economy Twin generated a Capacity Economy Transition (81%), where the binding constraint migrates over time from models to GPUs to data centers to capital formation, and operators come to compete on financing, construction, energy access, and utilization rather than on capability. The two risk drivers the simulation ranked highest were the roughly $248 billion in long-duration off-balance-sheet lease commitments and the $1.87 billion in class-period insider sales — together the concrete omission and the concrete scienter a securities claim lives or dies on.

The distinctive output is the headline. Where the Microsoft simulation produced Governance Debt as its signature, Oracle’s produces the Capacity Economy Transition — the recognition that competition among the largest operators has shifted from building intelligence to financing the capacity that runs it, and that the accountability following the shift is capacity accountability rather than capability accountability. The two cases calibrate each other: Oracle’s AGE-derived governance reading registers strain rather than saturation, so Microsoft remains the cleaner Governance Debt case and Oracle the cleaner Capacity Economy case, the same gap viewed through the dominant force in each. The reading feeds directly into the migration the next section names, and it moved MindCast’s internal confidence in the capability-to-capacity thesis upward; the movement reflects strengthened internal coherence rather than external proof, held honest by the caveat above and tested only by the falsification contract that closes the study. Twin construction, the quantitative output matrix, the dominant-force weighting, and the composite indices sit in the Appendix.

VI. The Migration — The Finding the Population Reveals

No single case shows the docket moving. The migration exists only at the population level, and stating it is the contribution this study makes that the institution-anchored vision structurally could not.

The center of gravity is shifting from the first category toward the second. Early AI-era securities pressure concentrated on capability claims, often against smaller pure-play AI companies. The 2026 wave reaches the largest infrastructure operators and turns on the disclosure of spend and capacity — Oracle on capex and counterparty concentration, Microsoft on capacity rationing behind a demand narrative. The defendants are getting larger, and the concealed fact is moving down the stack, from what the model can do to what the buildout costs and whether the capacity exists to deliver it (confidence ~75%, held there because the allocation-category population is still small). The MAP CDT simulation in Section V names the destination of that movement — a Capacity Economy Transition, in which the largest operators compete on financing, construction, and capacity utilization rather than on capability itself.

Tesla explains why the migration happens rather than merely that it does. Capability narratives are defensible as forward-looking right up until they meet a hard substrate — unbuilt hardware, finite compute, committed-but-unbuilt data centers. Once the substrate binds, the claim stops being about the future and becomes about a fixed, present shortfall, and the exposure converts from the narrative category to the allocation category. The AI industry is now spending hundreds of billions against substrates that bind in exactly that way, which is why the docket should be expected to keep migrating in the same direction.

VII. What the Migration Means

The migration carries a lesson past any of the four companies. Capability litigation polices what a company claims about its technology; allocation litigation polices what a company discloses about the institution running it. The second is harder to manage, because it requires a firm to forecast and disclose its own spend-and-capacity trajectory accurately — continuously, against a quarterly reporting rhythm, while the operating reality moves underneath it.

Forecasting accuracy becomes the operative capability, and the conclusion holds independent of any verdict. Whether Oracle’s case proves premature, whether Microsoft prevails, whether Apple and Tesla settle, the docket has already shifted its weight from capability toward capacity. Companies that deploy AI into infrastructure-heavy operations now carry an exposure that no amount of model performance retires — the exposure of a spend-and-capacity reality outrunning the disclosure that describes it. The instrument for managing that exposure is foresight applied as a disclosure-integrity layer, the subject of the companion vision.

VIII. Forecast and Falsification Contract

The study commits its central finding to a dated, falsifiable forecast.

Forecast. Through the end of 2028, the AI securities docket’s center of gravity continues migrating from narrative-arbitrage cases against smaller capability vendors toward allocation-and-infrastructure-disclosure cases against the largest compute and cloud operators. Probability 70–80%.

Confirms. A majority of new large-capitalization AI-related securities actions through the window turn on capex scale, lease and financing-structure disclosure, counterparty concentration, capacity utilization, or ROI-timing disclosure rather than on capability or benchmark misstatement; and the named infrastructure operators face disclosure suits at a higher rate than capability suits.

Falsifies. Capability and AI-washing claims remain the dominant category across the window, the largest infrastructure operators avoid allocation-disclosure suits, and no migration in defendant size or concealed-fact type is observable in the filing record.

Measurement window. Through December 31, 2028, scoped to AI-related securities actions against operators with material compute or cloud-infrastructure exposure.

A second forecast follows from the same logic and is stated separately because it concerns valuation rather than litigation. Through the end of 2028, the largest AI infrastructure operators will increasingly be valued as financing systems rather than software systems — priced on capital intensity, counterparty concentration, free-cash-flow trajectory, and the spread between committed obligations and contracted revenue, with model capability receding as a valuation driver among this cohort. Probability 65–75%. The forecast confirms if sell-side and credit coverage of these operators measurably shifts weight toward financing and capacity metrics over capability metrics across the window; it falsifies if capability and benchmark narratives continue to set the valuations of the largest operators with no observable move toward financing-system framing.

MindCast either meets the falsification standard or does not publish.

Appendix — Foresight Simulation (Oracle): Construction and Quantitative Signatures

The simulation summarized in Section V rests on three twins and a set of composite signatures, specified below. Confidence figures, dimension scores, and indices are the simulation’s own outputs rather than external measurements: they represent relative dominance rankings the Cognitive Digital Twin simulation produced across the modeled forces, not financial ratios measured from Oracle’s statements. The decimal precision reflects the model’s internal scaling, not surveyed data, and the shared-priors caveat from Section V governs all of them. Read the numbers as ordered signatures — which forces dominate, which risks rank highest, how Oracle sits relative to Microsoft — rather than as calibrated quantities.

Twin 1 — Oracle Institutional Twin. Inputs: OCI growth, OpenAI contracts, RPO expansion, data-center commitments, and capex escalation across the class period from roughly $25 billion to $35 billion to approximately $50 billion. Dominant force: capacity financing. Finding: Oracle increasingly resembles a financing vehicle attached to AI infrastructure, with revenue realization contingent on data-center completion, customer utilization, customer solvency, and future financing conditions rather than on capability. Classification: Infrastructure Financing System (85%).

Twin 2 — Counterparty Concentration Twin. Inputs: OpenAI commitments, revenue projections, capacity commitments. Dominant force: dependency risk. Finding: the critical variable migrates from Oracle to OpenAI, with Oracle’s financing, infrastructure, and revenue risk transferring into OpenAI’s execution, funding, and adoption risk — a single counterparty projected to supply more than a third of revenue against a $300 billion commitment the counterparty may be unable to fund. Classification: Counterparty Amplification Event (87%).

Twin 3 — Infrastructure Economy Twin. Participants: Oracle, Microsoft, Amazon, Google, OpenAI. Dominant force: capacity arms race. Finding: the binding constraint migrates from models (2023) to GPUs (2024) to data centers (2025) to capital formation (2026 forward), and operators come to compete on financing, construction, energy access, and capacity utilization rather than on capability. Classification: Capacity Economy Transition (82%).

Composite. System classification: Capacity Economy Transition event. Dominant forces: capacity financing, counterparty concentration, and registration lag, with the roughly $248 billion in off-balance-sheet lease commitments and the $1.87 billion in class-period insider sales ranked as the highest concrete risk drivers. Composite confidence: 83%.

Quantitative output matrix

The matrix carries the thesis in one view: the two highest-scored dimensions are financial, and the two lowest are about the technology itself.

Oracle litigation facts are drawn from public filings and reporting on Barrows v. Oracle Corporation, No. 1:26-cv-00127-JLH (D. Del.), and describe unproven allegations; Oracle has not yet responded on the record, and its position rests on public statements. Structural readings are MindCast analysis, labeled with confidence bands and committed to the falsification contract above.