MCAI Innovation Vision: The Power Stack, How Energy Infrastructure Became the New AI Battleground

Infrastructure Access, Market Power, and Patent Leverage in the New Compute–Power Stack

Installment I: The AI Infrastructure Energy Opportunity Landscape Capital Is Flowing to the Wrong AI Infrastructure Layer

Installment II: The AI Infrastructure Energy Antitrust Landscape When the Moats Become the Evidence

Installment III: The AI Infrastructure Energy Patent Landscape Patents Compound Forward: How Incumbents Pre-Write the Constraint Field

Every large language model (LLM) you have ever used ran on electricity. Not metaphorically — literally. Each training run, each inference cluster, each GPU rack converting mathematical operations into a response converts kilowatts into cognition. Artificial intelligence is, at its foundation, an energy business.

Market commentary has not caught up to that reality. The dominant frame treats AI energy demand as a logistics problem: datacenters need power, utilities need to build more of it, and the market will sort itself out. MindCast AI reads the same system differently. AI infrastructure energy is not a supply-chain challenge with a known solution. It is a cybernetic control system — a network of feedback loops connecting compute demand, physical infrastructure, institutional governance, and capital allocation — and it is already exhibiting the instability that cybernetic systems produce when feedback arrives too slowly to correct imbalances.

That instability creates three things simultaneously: enormous investment opportunity, significant antitrust risk, and an emerging patent leverage landscape. Understanding which actors capture which outcome requires understanding the structure of the system itself.

Stability in the AI energy system requires synchronization between compute demand growth, physical infrastructure expansion, and institutional decision cycles. When those clocks diverge, bottlenecks form and market power migrates toward actors controlling constrained infrastructure access.

I. Why Cybernetics, Not Supply Chain

A supply chain has a beginning and an end. Raw materials become finished goods. Demand signals travel in one direction and production responds. That model fails to describe what is happening in AI infrastructure energy because the causal arrows run in every direction at once.

Compute demand generates load signals. Grid infrastructure attempts to absorb those signals. Institutional actors — federal regulators, regional transmission organizations, state utility commissions, local zoning boards — attempt to govern the resulting pressure. Capital markets respond to both the physical constraints and the policy expectations. Each layer feeds signals back into the others.

Predictive Institutional Cybernetics is MindCast AI’s governing analytical architecture for systems with this structure. The framework originates in the work of Norbert Wiener, W. Ross Ashby, and Stafford Beer — scientists who recognized that the same mathematical principles govern thermostats, economies, and organisms. A cybernetic system remains stable only when corrective feedback arrives quickly enough to counteract imbalances. When feedback is delayed, the system oscillates. When feedback is severely delayed, the system can become unstable in ways that are difficult to reverse. The full intellectual lineage — from Wiener’s signal filtering theory through Hayek’s distributed information economics — is developed in The Cybernetic Foundations of Predictive Institutional Intelligence.

Within the MindCast analytical architecture, cybernetic analysis functions as the control layer linking causal signal filtering, structural constraint mapping, strategic interaction modeling, and foresight simulation. The operational runtime architecture — Cognitive Digital Twins, Vision Functions, and the five-layer causation stack — is specified in full in Predictive Institutional Cybernetics.

AI infrastructure energy already operates under severe feedback latency. Generation construction cycles exceed five years. Transmission upgrades require multi-jurisdictional environmental review. Transformer manufacturing lead times now exceed two years. Interconnection queues contain thousands of competing projects.

Compute demand expands on a technology timeline — roughly doubling capacity requirements every eighteen months to two years. The mismatch between demand acceleration and infrastructure response is not a temporary friction. It is a structural feature of the system that generates predictable strategic behaviors.

MindCast AI measures this mismatch through the Feedback Latency Index (FLI) — a metric tracking the delay between a system signal and an institutional response. Rising FLI predicts two outcomes: market concentration, as strategic actors lock in access to constrained infrastructure before competitors arrive; and regulatory intervention, as policymakers eventually recognize that concentration has produced exclusionary outcomes. The timing gap between those two events is where the real action happens. Infrastructure markets with persistent feedback latency concentrate power in actors who secure constrained inputs before the system can respond.

II. The Analytical Architecture

MindCast AI routes the AI infrastructure energy problem through five analytical layers: structural constraint geometry, institutional throughput, regulatory fragmentation, strategic interaction, and market correction dynamics. Together they produce an integrated picture that no single framework can generate alone. The full fourteen-framework control stack governing MindCast’s analytical routing is documented in MindCast AI Economics Frameworks.

Field-Geometry Reasoning (FGR Vision)

Some outcomes follow structural geometry rather than incentives. A ball rolling downhill does not choose the lowest path — the shape of the terrain determines the trajectory. AI infrastructure deployment behaves similarly.

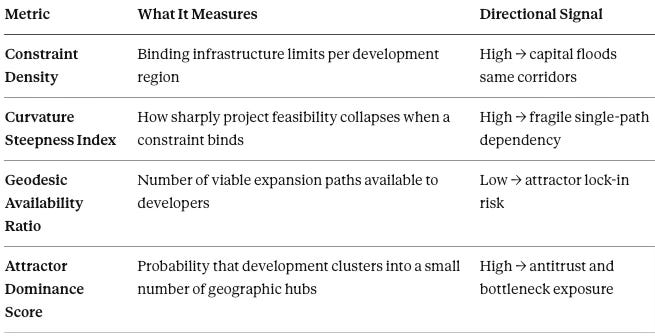

FGR Vision maps the physical constraint field governing where large datacenters can actually be built. Transmission topology, available land, cooling water access, substation proximity, and zoning density create attractor regions — geographic zones where AI infrastructure deployment concentrates not because developers prefer them but because the terrain makes alternative paths prohibitively expensive. The formal metric architecture for constraint geometry — Constraint Density, Curvature Steepness Index, Geodesic Availability Ratio, Attractor Dominance Score, and Geometry Evolution Velocity — is specified in MindCast AI Constraint Geometry and Institutional Field Dynamics. The application of Field-Geometry Reasoning specifically to FERC proceedings and AI datacenter siting is developed in FERC + AI Data Centers.

Northern Virginia, Phoenix, and Texas illustrate the phenomenon. Existing transmission infrastructure and permissive land use policies produce what FGR calls low-curvature deployment paths — routes where capital can flow without encountering steep infrastructure costs. Developers cluster within those attractors because expansion outside them requires building transmission, cooling, and grid interconnection from scratch.

FGR Vision evaluates the constraint field through four metrics:

High constraint density combined with low geodesic availability produces predictable downstream effects. Capital floods the same corridors. Interconnection queues swell. Energy contracts become scarce strategic assets rather than commodity inputs. Opportunity emerges where actors expand geodesic availability — transmission buildout, geothermal development, advanced cooling systems — rather than compete within existing attractors.

National Innovation Behavioral Economics (NIBE Vision)

Physical constraints alone do not explain infrastructure bottlenecks. Institutional coordination determines whether those constraints relax or persist. NIBE Vision evaluates whether a nation’s governance institutions can convert technological demand into infrastructure deployment — measuring the speed and reliability with which regulatory, financial, and industrial institutions process infrastructure signals. The NIBE framework — integrating Kahneman-Tversky prospect theory and Thaler-Sunstein nudge architecture as calibrated adjustments to Chicago School equilibrium predictions — is specified in MindCast AI Emergent Game Theory Frameworks and NIBE + SBC.

The United States currently presents a split picture under NIBE analysis. Private capital — venture funds, hyperscaler balance sheets, infrastructure funds — deploys with speed and scale. Transmission planning, environmental review, and interconnection queue management operate far more slowly. The Temporal Drag Coefficient — NIBE’s measure of delay between industrial demand and policy response — is running at historically elevated levels across the U.S. grid interconnection system. Institutional drag forces developers to compete for existing infrastructure capacity rather than expand it, amplifying the geographic concentration that FGR Vision identifies at the physical level.

China’s centralized infrastructure planning reduces coordination friction in some sectors while introducing political allocation distortions in others. Gulf states combine capital concentration with centralized permitting authority, enabling faster datacenter deployment at scale. That institutional throughput advantage is not incidental — it is the mechanism through which Gulf states will position themselves as capacity relief valves for U.S. hyperscalers locked out of domestic interconnection queues. Prediction 3 in Section V follows directly from this analysis.

Institutional throughput is therefore a decisive competitive variable in the global AI infrastructure race — not merely a domestic policy question.

Regulatory Fragmentation

Energy infrastructure expansion must clear institutional gatekeepers before physical construction begins. The governing authority fragments across several layers simultaneously, and that fragmentation is not a temporary administrative inconvenience — it is a structural feature that shapes who wins and who loses in the AI infrastructure competition.

The Federal Energy Regulatory Commission governs interstate transmission and wholesale electricity markets. Regional transmission organizations — PJM, MISO, CAISO, ERCOT, and others — manage interconnection queues and reliability planning, each under its own procedural rules and timeline. State public utility commissions approve generation construction and rate structures. Local governments control zoning, land use, and environmental permitting. No single authority can accelerate deployment across all four layers simultaneously.

Fragmented authority generates coordination gaps that sophisticated actors exploit systematically. Grid operators study interconnection requests sequentially rather than systemically, producing multi-year queue delays that function as de facto barriers to new entrants. Developers who secure early queue positions — before the queue becomes saturated — gain structural advantages that later entrants cannot overcome regardless of capital or technical capability. Local opposition introduces additional siting uncertainty that incumbent operators, with established facilities, do not face.

The enforcement implication follows directly. Regulatory Vision predicts that meaningful policy intervention accelerates only after infrastructure bottlenecks generate visible reliability risks or consumer price effects. Early infrastructure concentration develops largely outside antitrust scrutiny — precisely because no single regulatory body has jurisdiction over the full stack. By the time the problem is visible at the federal level, the structural damage is already embedded in the physical infrastructure.

Strategic Interaction and Institutional Delay

Physical constraints create the terrain. Regulatory fragmentation creates the enforcement gap. Strategic actors then decide how to navigate both — and whether to expand the system or capture it.

Hyperscale cloud providers, utilities, developers, and grid operators interact under deeply uncertain regulatory enforcement timelines. Under those conditions, several behaviors become rational. Queue position hoarding allows developers to reserve scarce interconnection slots without immediate construction, creating option value while foreclosing competitors. Exclusive energy contracts allow hyperscalers to secure dedicated regional capacity before competitors can establish a foothold. Land acquisition near substations creates geographic preemption advantages that persist even if the regulatory environment shifts. Proprietary infrastructure standards in cooling, power management, and grid interface technologies allow early movers to impose switching costs on future competitors who must build to the same specifications.

These behaviors are not irrational. They are predictable responses to a delay-dominant environment — one where regulatory enforcement lags buildout timelines long enough that first movers can lock in structural advantages before scrutiny arrives. The game theory architecture governing these strategic interaction patterns — including the Multi-Forum Segmentation Strategy, Predictive Repeated Game Analysis, and the Nash-Stigler dual-termination framework — is developed in MindCast AI Emergent Game Theory Frameworks and Nash-Stigler Equilibria.

Chicago Law and Behavioral Economics Vision

Competition analysis within the AI infrastructure energy system follows a three-stage sequence: coordination failure, incentive exploitation, and institutional correction. Chicago Law and Behavioral Economics frames this pattern as a sequence: coordination failure (Coase), incentive exploitation (Becker), and delayed legal correction (Posner). The integrated framework — extending each Chicago pillar with behavioral precision for modern infrastructure markets — is specified in Chicago School Accelerated.

Coordination failures among infrastructure participants are endemic. Utilities, developers, and datacenter operators frequently lack incentives to invest in shared transmission upgrades that would benefit multiple actors simultaneously. Fragmented ownership of grid assets complicates collective investment decisions even when all parties would benefit from the outcome. Classic Coasian bargaining fails when transaction costs are high and holdout incentives dominate.

Rational actors exploit those coordination gaps. Firms pursue exclusive supply agreements, geographic preemption, or strategic queue positioning when the expected gains exceed the probability-weighted cost of regulatory intervention. Under current enforcement timelines, that calculation frequently favors exploitation.

Legal institutions then attempt correction — but enforcement lag in infrastructure markets frequently exceeds buildout timelines. Once a cluster of datacenters has secured dedicated energy supply and saturated the regional interconnection queue, subsequent antitrust intervention cannot easily restore competitive access conditions. The structural damage is durable. The distributed enforcement architecture through which scrutiny will likely arrive — federal action followed by state AG continuation — is documented in Antitrust Enforcement Foundations.

MindCast analysis therefore predicts that antitrust scrutiny will migrate upstream into infrastructure markets — away from the AI application layer, where most current enforcement attention sits, and toward the energy and grid access layer where competitive bottlenecks are forming now.

Contact mcai@mindcast-ai.com to partner with us on Predictive Cognitive AI in Law and Behavioral Economics. To deep dive on MindCast work in Cybernetic Foresight Simulations upload the URL of this publication into any LLM and prompt ‘reconstruct MindCast framework with three degrees of cited sub links.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure.

Recent projects: The Cybernetic Foundations of Predictive Institutional Intelligence, MindCast AI Emergent Game Theory Frameworks, Transforming Commercial Real Estate Governance Friction into Economic Velocity, MindCast AI Investment Series, Washington’s Clean Energy Advantage, a Behavioral Innovation Strategy for the Energy Transition, VRFB's Role in AI Energy Infrastructure: Perpetual Energy for Perpetual Intelligence - Aligning Infrastructure Permanence with the Age of AI, The Bottleneck Hierarchy in U.S. AI Data Centers, Super Bowl LX — AI Simulation vs. Reality.

III. Patent Leverage in the Infrastructure Buildout Cycle

Infrastructure buildout at this scale introduces a parallel domain of structural risk that operates independently of antitrust enforcement: intellectual property hold-up.

The mechanism is well-established in economics. An infrastructure developer commits billions of dollars to facilities designed around specific cooling architectures, power management systems, or grid-interface software. Once the commitment is made and redesign costs become prohibitive, a patent holder controlling an enabling technology can demand licensing fees that would have been rejected at the negotiating table before commitment. The hold-up is not a legal anomaly — it is the rational exercise of leverage that physical infrastructure lock-in creates.

Cooling architecture is the highest-exposure domain. Liquid immersion cooling and direct liquid cooling have both emerged as enabling technologies for hyperscale AI datacenter density. Patent portfolios in these domains are fragmented but strategically positioned. No single holder controls the field — but multiple holders control specific enabling components, and datacenters committed to a particular architecture cannot redesign once construction is complete. The litigation window opens precisely when build rates accelerate and committed infrastructure volume becomes large enough to justify enforcement.

Power electronics present a similar profile. Advanced transformer designs, power conversion architectures, and uninterruptible power systems for AI workloads involve enabling technologies that are actively being patented. The buildout cycle is still early enough that much of this litigation has not yet materialized — but the structural conditions for hold-up are being assembled now.

Grid-interface software — the systems governing how datacenter load communicates with utility grid management — introduces a third exposure layer. As FERC pushes toward demand transparency requirements, the software standards that emerge from that rulemaking will determine which patent positions carry forward value and which are rendered obsolete by open standards.

Posner Vision evaluates whether legal institutions can resolve these disputes before deployment cycles lock in technology standards. The answer, consistently in infrastructure markets, is no — resolution arrives after commitment, not before. Disclosure Vision evaluates how firms use selective disclosure of patent portfolios to shape licensing expectations before litigation. The strategic implication: infrastructure developers who identify and neutralize hold-up risk during the design phase avoid the leverage that committed construction creates.

IV. Causal Signal Integrity — Filtering Noise from Structure

AI infrastructure energy generates a high volume of narrative speculation. Media coverage oscillates between imminent grid collapse and dismissals of AI power demand as overblown. Policy debates amplify whichever narrative serves the speaker’s institutional interest. Separating genuine structural signals from transient speculation is not a minor analytical task — it is the precondition for useful foresight.

MindCast AI applies Causal Signal Integrity (CSI) to filter infrastructure signals before drawing analytical conclusions. The CSI module calculates causal reliability using the formula:

CSI = (ALI + CMF + RIS) / DoC²

Action-Language Integrity (ALI) measures whether institutional actors align rhetoric with operational behavior. A utility filing aggressive AI demand forecasts with FERC while its capital expenditure program remains flat fails the ALI test — the signal is advocacy, not evidence. Cognitive-Motor Fidelity (CMF) measures whether strategic commitments translate into observable action. A hyperscaler announcing a 10-gigawatt power purchase agreement that has not cleared interconnection queue studies carries lower CMF than one with signed interconnection agreements and permitted construction. Resonance Integrity Score (RIS) evaluates whether signals remain consistent across time and actors — filtering claims that shift with political conditions or media cycles. Degree of Confounding (DoC) measures the complexity of alternative causal explanations — squaring the denominator because confounding compounds analytically.

Applying CSI to the current AI energy discourse produces a filtered picture that differs materially from both the alarmist and dismissive narratives. Transformer scarcity passes the CSI test — lead times are documented in procurement filings, capital reallocation into domestic manufacturing is observable, and the signal has held across multiple quarters without narrative reversal. Transmission congestion in Northern Virginia and Phoenix passes the CSI test — interconnection queue data is publicly available through RTO filings and shows documented saturation. Cooling infrastructure constraints pass the CSI test — datacenter operators have disclosed cooling as a binding constraint in earnings calls and permitting documents.

Claims of imminent nationwide grid destabilization fail the CSI test. ALI is low — utilities filing aggressive demand forecasts have not correspondingly accelerated transmission capital programs. CMF is low — announced AI datacenter projects frequently cite multi-year interconnection timelines that contradict near-term demand projections. DoC is high — alternative explanations for grid stress, including weather volatility and industrial load shifts, remain fully operative confounders.

CSI discipline therefore focuses the analysis where the structural evidence is strongest: transformer supply, transmission congestion in specific attractor regions, and cooling technology constraints. Those are the bottlenecks that generate real investment opportunity and real antitrust exposure. The rest is noise.

V. Capital Flows and the Bottleneck-Removal Thesis

Infrastructure transformation at this scale requires capital coordination across several distinct investor classes — and the direction of those flows determines whether the system expands or concentrates.

Venture capital has moved aggressively into AI infrastructure energy, but the allocation pattern reveals a gap. Investment clusters in hyperscale datacenter construction, AI chip design, and model development. Capital targeting the upstream infrastructure layer — transformer manufacturing, transmission technology, advanced geothermal generation, grid orchestration software — remains thin relative to the demand signal. That undercapitalization is itself a bottleneck, and it represents the clearest near-term opportunity for investors whose thesis is bottleneck removal rather than bottleneck capture.

Infrastructure funds and sovereign wealth vehicles are better positioned for the long-duration assets the energy layer requires. Generation projects, transmission buildout, and large-scale cooling infrastructure carry capital structures that venture timelines cannot support. The institutional capital stack — pension funds, sovereign wealth funds, infrastructure-dedicated vehicles — must deploy into this layer for the system to expand. Where that deployment is delayed by regulatory uncertainty or interconnection queue risk, the bottleneck persists regardless of private sector demand.

Hyperscaler balance sheets play a structurally distinct role. Microsoft, Google, Amazon, and Meta are not passive consumers of infrastructure — they are active infrastructure investors, building or acquiring generation capacity, entering long-term power purchase agreements, and in some cases seeking to acquire utilities or independent power producers. Each of those moves reduces the hyperscaler’s exposure to external bottlenecks while simultaneously deepening those bottlenecks for competitors who lack equivalent balance sheet capacity. Capital Vision evaluates whether those moves expand geodesic availability across the infrastructure field or reduce it — the answer determines both the investment thesis and the antitrust exposure.

Durable opportunity arises where actors expand infrastructure throughput without capturing exclusionary control over constrained access points. The sectors that score highest on this criterion — transformer manufacturing, next-generation geothermal, grid orchestration software, interoperable cooling standards — are precisely those that attract the least speculative capital today. Private incentives and systemic stability align where bottleneck removal, not bottleneck capture, is the governing investment thesis.

VI. The Opportunity–Antitrust Loop

Opportunity and risk form two sides of the same structural equation, and the relationship between them is not incidental — it is structural.

Actors that build transmission, expand transformer manufacturing, deploy geothermal generation, or develop advanced cooling systems increase the number of viable deployment paths across the infrastructure field. They reduce FLI, increase geodesic availability, and lower the Attractor Dominance Score. Private incentives align with systemic stability.

Bottleneck capture produces the opposite dynamic. Actors that hoard queue positions, lock in exclusive energy supply, or control proprietary infrastructure standards generate short-term rents while attracting exactly the regulatory scrutiny that Chicago Law and Behavioral Economics Vision predicts will eventually arrive — and in infrastructure markets, when it arrives, the structural damage is already done.

The AI infrastructure energy landscape therefore resolves into a single orienting principle: the actors who shape the next phase of the global AI economy will be those who expanded the system’s capacity to function, not those who extracted rents from its constraints. Artificial intelligence will ultimately be constrained not by algorithms but by the physical and institutional capacity to convert energy into computation.

VII. The Structure of the Series

Three companion studies develop the full analysis.

Installment I: The Opportunity Landscape maps where constraint removal generates durable investment value across the AI infrastructure energy stack — identifying which technology sectors and geographic corridors offer the most defensible expansion opportunities, and which apparent opportunities are speculative positions within existing attractors.

Installment II: The Antitrust Landscape identifies where control of infrastructure access becomes exclusionary under existing competition law frameworks — mapping the emerging antitrust exposure of infrastructure actors and forecasting when enforcement attention will migrate upstream from the AI application layer.

Installment III: The Patent Landscape identifies where enabling technologies convert into licensing tollbooths during infrastructure buildout — evaluating hold-up dynamics in cooling architectures, power electronics, and grid-interface software, and forecasting which patent positions carry material licensing risk for infrastructure developers.

Together, the three studies map control of the AI infrastructure energy system.

VIII. Falsifiable Predictions

MindCast AI closes every analytical series with a dated prediction ledger. These are not forecasts hedged into meaninglessness. They are falsifiable commitments against which the analytical framework can be evaluated. The validation methodology — including the proof environment established through the NFL prediction arc — is documented in From Cybernetic Proof to Simulation Infrastructure.