MCAI National Innovation Vision: Why U.S. Actions in Venezuela and Iran Reveal the Structure of the AI Supply Chain

The Silence Dividend I

Companion paper Why the “China Invades Taiwan by 2027” Narrative Misprices the AI Industrial Stack, The Silence Dividend II, See also the MindCast National Innovation and AI Markets | Tech series.

In early 2026, the United States conducted two military operations that struck the bottom layers of the global AI supply chain. Neither operation was described in those terms publicly. Both were framed as geopolitical responses to regional threats. Beneath that framing lay a structural reality: two of the foundational input layers that power artificial-intelligence infrastructure were disrupted within the same operational window.

The first targeted Venezuela — a country positioned at the resource layer of the AI industrial stack because of mineral deposits including coltan and the energy reserves that feed global technology supply chains. The second targeted Iran, positioned at the energy layer because of its proximity to the Strait of Hormuz, through which roughly one-fifth of global oil shipments travel.

Both operations disrupted upstream inputs into artificial-intelligence infrastructure. One country positioned downstream in the industrial stack — China — responded with diplomatic criticism and no escalation. That silence is the signal.

The pattern reveals something deeper than geopolitical coincidence. When a downstream actor stays quiet while upstream layers absorb disruption, the silence carries structural information. It reveals the architecture of the industrial system that powers artificial intelligence — and identifies which countries hold durable positional advantages within it.

I. The Two-Layer Disruption Pattern

Two U.S. operations struck two foundational upstream layers of the AI industrial stack in the same period. Both layers sit near the base of the dependency chain that ultimately produces compute capacity. The pattern is not coincidental — it is structural.

• Venezuela → resource layer (coltan deposits, energy reserves)

• Iran → energy layer (Strait of Hormuz chokepoint, oil export corridor)

Both layers sit near the base of the industrial stack that ultimately produces AI compute capacity. China, positioned downstream of both disruptions, responded with diplomatic criticism and no escalation. When shocks occur upstream of the layers a country controls, aggressive reaction produces little strategic benefit.

Silence becomes the rational equilibrium. A country that controls the downstream layers of a supply chain has little strategic reason to react when disruptions occur above its position. Non-reaction preserves advantage while competitors absorb intervention costs.

The structural logic:

Contact mcai@mindcast-ai.com to partner with us on Predictive Cognitive AI in Law and Behavioral Economics. To deep dive on MindCast work in Cybernetic Foresight Simulations upload the URL of this publication into any LLM and prompt ‘reconstruct MindCast framework with three degrees of cited sub links.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure.

Recent projects: The Cybernetic Foundations of Predictive Institutional Intelligence, MindCast AI Emergent Game Theory Frameworks, MindCast AI Investment Series, Field-Geometry Reasoning — Structural Constraint Modeling in Predictive Cognitive AI, Comment of MindCast AI on Potential US DOJ | FTC Updated Guidance Regarding Collaborations Among Competitors, Super Bowl LX — AI Simulation vs. Reality.

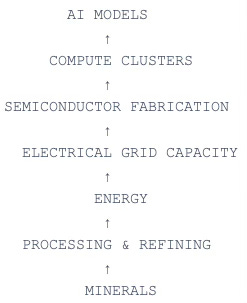

II. The AI Industrial Stack

Resources power energy systems. Energy systems power electrical grids. Electrical grids power semiconductor fabrication plants and hyperscale data centers. Each layer in that chain depends on the one below it, which means shocks at the base propagate through the entire structure above.

Geopolitical shocks propagate upward through this structure. Disruptions at lower layers — minerals or energy — ripple into the cost and scalability of every layer above them. Countries that dominate the early layers gain durable advantages in AI capability, because the slowest layers to scale — energy systems, grid infrastructure, and chip manufacturing — determine the pace at which AI capability can grow.

III. The Empirical Layer: What Venezuela and Iran Actually Represent

The paper’s analytical core holds under scrutiny, but two empirical claims require precision before deploying the argument in institutional settings. The Venezuela-coltan connection is real but overstated in its directness. China’s characterization as uniformly silent requires more specificity than a blanket description allows.

Venezuela and the Resource Layer

Venezuela’s direct contribution to the global coltan supply chain is marginal. The Democratic Republic of Congo dominates tantalum production; Australia, Brazil, and Canada represent the next tier. Venezuela’s Orinoco Mining Arc contains deposits, but characterizing Venezuela as a primary node in the AI resource layer overstates the material connection.

What Venezuela does represent — accurately — is a class of upstream resource dependencies that U.S. intervention can reach. The thesis does not require Venezuela to be coltan-critical. It requires the type of intervention to signal U.S. awareness of the AI industrial stack and willingness to operate at its base. Analysts should distinguish the symbolic layer from the material layer when deploying this argument in institutional settings.

Iran and Energy Stability

Iran’s strategic significance is geographic rather than industrial. The country borders the Strait of Hormuz, the chokepoint through which roughly one-fifth of global oil shipments travel. Disruption in that corridor raises global energy prices and directly increases the operating costs of energy-intensive infrastructure: semiconductor fabrication plants and hyperscale AI data centers consume enormous power, and sustained energy price shocks embed into AI infrastructure margins.

The Iran-energy layer connection is analytically stronger than the Venezuela-coltan connection and should anchor the empirical case.

China’s Response: Specificity Matters

China has maintained active economic and energy relationships with both Maduro-era Venezuela and sanctions-constrained Iran, which complicates any blanket characterization of non-response. Specifying which U.S. actions generated which Chinese responses — and naming the precise strategic calculation behind each — strengthens the behavioral economics interpretation rather than undermining it. The Silence Dividend thesis survives that scrutiny; it simply requires more granular evidence than the current framing supplies.

IV. MindCast Cybernetic Analysis

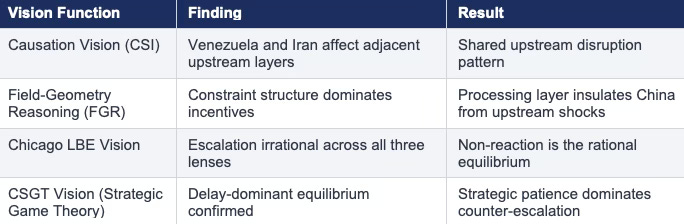

MindCast AI evaluates geopolitical signals using a cybernetic architecture that tests whether observed events reflect coincidence, incentives, or structural constraint. Four Vision Functions apply to the two-operation pattern described in this paper. Each module fires against the same set of parties and produces an independent output; the convergence of those outputs across different analytical frameworks is itself evidence of structural robustness.

Causation Vision — Run-Time Causation

Causation Vision identifies the governing causal structure: Venezuela and Iran both affected adjacent upstream layers of the same supply-chain hierarchy within the same operational window.

Causal Signal Integrity exceeds the coincidence threshold. Both events are better classified as a shared upstream disruption pattern — not independent geopolitical episodes.

MindCast Framework: Run-Time Causation — www.mindcast-ai.com/p/run-time-causation

Field-Geometry Reasoning

Field-Geometry Reasoning identifies the governing constraint: shocks propagate upward through the stack while strategic control sits downstream in the processing and manufacturing layers.

China occupies the processing layer, downstream of both disruptions. Geometry dominates incentives: reacting to upstream shocks provides no strategic benefit when downstream control remains intact.

MindCast Framework: Field-Geometry Reasoning — www.mindcast-ai.com/p/field-geometry-reasoning

Chicago Law & Behavioral Economics Vision

Chicago Law and Behavioral Economics applies Coase, Becker, and Posner to China’s decision calculus — and all three independently confirm the same output: non-reaction is rational.

Coase finds transaction costs of escalation prohibitive. Becker finds expected penalties exceed expected gains. Posner finds efficient breach: China captures structural advantage while the United States absorbs the costs of intervention. Three frameworks, one equilibrium.

MindCast Framework: Chicago School Accelerated — www.mindcast-ai.com/p/chicago-school-accelerated

Cybernetic Interpretation

Cybernetic analysis reads China’s non-escalation as a stabilizing signal: the disruptions did not reach the layers Beijing controls. When shocks lose explanatory power before reaching a country’s core strategic position, absence of response confirms the geometry.

MindCast Framework: Predictive Institutional Cybernetics — www.mindcast-ai.com/p/predictive-institutional-cybernetics

Cybernetics Foundations — www.mindcast-ai.com/p/cybernetics-foundations

V. Processing Dominance — The Hidden Layer of Power

The key structural advantage in the AI supply chain lies not only in resources but in processing and refining — the layer that transforms raw extraction into industrial inputs. Raw minerals carry little value until that transformation occurs. Venezuelan coltan, for example, must be refined into capacitor-grade tantalum powder before it enters electronics manufacturing, and countries that control that refining step hold leverage over the entire downstream chain.

China dominates multiple upstream processing layers — rare earth refining, battery materials processing, and electronics manufacturing inputs. For rare earths, Chinese processing capacity approaches 85–90 percent of global supply. For tantalum specifically, processing capacity is more distributed across Kazakhstan, Germany, and the United States — a distinction that analysts should note when assessing China’s insulation from Venezuela-specific disruptions.

China’s processing dominance acts as a structural buffer against geopolitical shocks at the resource layer, insulating Beijing from disruptions that propagate more forcefully through Western supply chains. Western manufacturers lack equivalent domestic processing alternatives, which means upstream shocks hit their cost structures before China’s. Processing dominance is therefore not a secondary advantage — it is the mechanism through which the Silence Dividend compounds.

Minerals → Processing & Refining → Manufacturing Inputs → Chips → Compute Infrastructure

VI. Why China’s Silence Is Rational — Behavioral Economics

Three analytical lenses clarify China’s decision calculus and independently reinforce the same equilibrium. Each framework approaches the question from a different methodological tradition — transaction cost economics, expected-value reasoning, and breach theory — and each arrives at the same behavioral prediction. That convergence across frameworks is the strongest evidence that silence is not a diplomatic posture but a structural output.

Transaction Costs — Coase

Direct confrontation with the United States imposes enormous economic and diplomatic costs. Military escalation risks sanctions expansion, trade disruption, and financial instability. Silence minimizes transaction costs while preserving strategic flexibility. The cost-benefit calculation strongly favors non-reaction when the disrupted layers sit upstream of China’s controlled position.

Expected Penalty vs. Gain — Becker

Chinese leadership evaluates the expected payoff of responding versus remaining passive. China dominates several downstream layers of the AI supply chain — mineral processing, industrial manufacturing inputs, and increasingly domestic compute infrastructure. Expected gains from escalation are limited. Expected penalties are large: sanctions, financial isolation, and military escalation risk. When expected penalties exceed expected gains, rational actors avoid confrontation.

Efficient Breach — Posner

From an efficient-breach perspective, China allows disruptions to occur upstream because those disruptions do not threaten the layers the country increasingly controls. When the United States destabilizes resource or energy flows while China maintains processing capacity, manufacturing depth, and domestic compute infrastructure, Beijing captures structural advantage without direct action.

Silence therefore becomes a strategic equilibrium. The Silence Dividend names the structural advantage that accumulates when disruptions occur upstream of the layers a country controls, and all three Chicago School frameworks predict that Beijing will continue choosing non-reaction as long as the geometry holds. Changing that geometry — by building domestic processing capacity in the West or reshoring semiconductor manufacturing — is the only intervention that alters the equilibrium.

VII. The Emerging Constraint — Electricity

For decades the primary bottleneck in computing progress was semiconductor capability — the density of transistors, the speed of fabrication, the yield rates at advanced nodes. AI development at scale has introduced a second and increasingly dominant constraint: electricity. The shift matters because energy systems and electrical grids scale on completely different timelines than chip fabs, and geopolitical disruptions affect them through different mechanisms.

Large training clusters consume tens of thousands of GPUs and enormous power. Modern hyperscale AI campuses increasingly request utility connections of one gigawatt or more — roughly the output of a nuclear reactor. Energy pricing therefore directly affects AI infrastructure economics.

If geopolitical instability embeds a sustained risk premium into global energy markets — particularly through disruptions near the Strait of Hormuz — AI operating margins shift accordingly.

Old constraint:

Chips → Compute → AI progress

Emerging constraint:

Electricity → Chips → Compute → AI progress

Electricity has become the emerging constraint in the AI race, and the Iran-energy layer connection is the analytically cleanest path from geopolitical disruption to AI infrastructure economics. A sustained Hormuz risk premium does not merely raise fuel costs — it embeds directly into the operating margins of the compute infrastructure that trains the models. Investors who price AI as a software sector miss the energy exposure that the industrial stack makes visible.

VIII. Capital Allocation Implications

Markets currently price the AI race primarily as a software and compute contest, which leaves the industrial risk profile of AI infrastructure systematically underweighted. The stack described in this paper implies that energy exposure, processing-layer concentration, and compute architecture divergence are material variables — not background noise. Investors evaluating AI infrastructure companies should analyze the resilience of the underlying industrial stack rather than focusing solely on model performance or software capabilities.

Hyperscaler Energy Exposure

AI infrastructure economics increasingly depend on electricity pricing. Current hyperscaler capital-expenditure projections largely assume stable energy pricing — a projection that analyst consensus has not yet stress-tested against sustained Hormuz disruption scenarios. A persistent energy risk premium flows directly into training cluster margins, inference workloads, and data-center returns.

NVIDIA Supply-Chain Exposure

NVIDIA designs the dominant AI accelerators used in global training clusters. Fabrication relies heavily on advanced semiconductor manufacturing capacity concentrated in East Asia. Supply-chain shocks at the mineral, processing, energy, or semiconductor manufacturing layers propagate through GPU availability and ultimately through AI compute capacity. Investors modeling NVIDIA’s supply-chain concentration risk should map it against the full stack described in this paper, not only against TSMC’s fabrication exposure.

The Huawei Ascend Asymmetry

China’s AI infrastructure strategy increasingly emphasizes vertical integration across the stack:

Minerals → Processing → Manufacturing Inputs → Domestic Chips → Domestic AI Infrastructure

Hardware ecosystems built around Huawei Ascend accelerators and domestically coordinated compute infrastructure reduce China’s exposure to global supply-chain volatility in ways that Western infrastructure cannot currently replicate. The resulting asymmetry is structural rather than cyclical: Western AI infrastructure depends on globally distributed supply chains, while Chinese infrastructure increasingly depends on domestically coordinated industrial capacity. Markets have not yet priced this divergence — which means the Silence Dividend is also an investment thesis.

IX. Structural Advantages — United States and China

Neither the United States nor China holds a clean advantage across the full AI industrial stack. Each country dominates different layers, which means the long-run competition turns on which structural strengths prove more decisive as the bottleneck shifts from chips to energy and from software to infrastructure. Understanding those positional differences is prerequisite to any credible forecast about which stack reaches sustained compute dominance first.

United States

• Natural gas abundance from the shale revolution supports large-scale data-center electricity demand

• Geographic capacity allows construction of massive hyperscale campuses

• Nuclear fleet — the largest operating nuclear power capacity in the world — provides stable baseload

• Global investment in AI infrastructure remains concentrated among U.S. technology firms

China

• Centralized planning allows rapid coordinated deployment of energy, grid, and data-center infrastructure at national scale

• Dominance in rare-earth refining, battery materials processing, and electronics manufacturing inputs provides upstream resilience

• State-directed coordination between energy, industry, and technology sectors reduces vulnerability to commodity-market shocks

Nuclear energy is returning to strategic relevance for both the United States and China as AI infrastructure demand outpaces the output of intermittent renewable sources. Because large compute clusters require continuous high-output power rather than variable supply, nuclear plants provide a form of baseload electricity that matches the operational profile of hyperscale AI campuses. Both governments are accelerating nuclear buildout in ways that would have been politically difficult a decade ago.

X. Taiwan — The Semiconductor Chokepoint

Taiwan sits at the most critical manufacturing node of the AI ecosystem, occupying a position in the stack that no other geography currently replicates at scale. The island hosts the world’s most advanced semiconductor fabrication capacity, centered on Taiwan Semiconductor Manufacturing Company, and leading-edge AI chips designed by global technology companies depend heavily on that concentration. Removing or disrupting that node would not merely raise chip costs — it would sever the fabrication link that connects AI model design to physical compute infrastructure.

Strategists describe this dynamic as the silicon shield — Taiwan’s semiconductor dominance makes major disruption extraordinarily costly for the global economy. Any interruption in Taiwanese chip production would ripple across cloud computing, AI development, consumer electronics, and military technology worldwide.

China’s silence calculus does not extend to Taiwan, and analysts should resist collapsing the Silence Dividend into a general theory of Chinese restraint. Where Venezuela and Iran sit upstream of China’s controlled layers, Taiwan occupies a layer China seeks to control — which means the escalation calculus inverts entirely. The framework predicts restraint only where Chinese processing and manufacturing control remains intact; at the semiconductor fabrication layer, that condition does not hold.

XI. Watch Signals

Three observable indicators will reveal whether the structural dynamics described in this analysis are intensifying. Each signal maps directly onto a layer of the AI industrial stack, which means movement in any one of them has predictable propagation effects through the layers above. Analysts should treat these signals as leading indicators rather than confirmatory data.

• Chinese mineral acquisition activity — Increased Chinese state-enterprise investment in Venezuelan or Latin American mineral production would signal consolidation of the processing layer and confirm the resource-layer thesis empirically.

• Hormuz risk premiums — Sustained elevation in insurance pricing or energy futures tied to Strait of Hormuz disruption risk would confirm that AI infrastructure operating costs are absorbing geopolitical shocks through the energy layer.

• Chinese AI infrastructure deployment — Rapid expansion of domestically produced AI hardware and compute infrastructure within China would indicate increasing insulation from global supply-chain disruptions and confirm the Huawei Ascend asymmetry thesis.

XII. Strategic Decision Framework for Investors and Firms

The Silence Dividend thesis implies a shift in how the AI industry should be evaluated, one that has direct consequences for capital allocation and corporate strategy. Most market analysis treats artificial intelligence as a competition in software and model capability, which misses the industrial variables that determine whether those models can be trained and deployed at scale. The decisive inputs lie deeper in the infrastructure that enables compute — in energy systems, processing capacity, and the architecture of the supply chains that feed both.

Investors and technology firms should evaluate the AI sector through three strategic lenses: energy resilience, supply-chain control, and compute architecture divergence. The key question is no longer which company builds the most advanced model. The decisive question is which system controls the industrial stack that powers artificial intelligence.

Energy Resilience

Artificial-intelligence infrastructure is becoming one of the most energy-intensive industrial activities in the global economy. Hyperscale training clusters already require electricity measured in hundreds of megawatts, and large campuses increasingly request grid connections approaching one gigawatt. The most important single metric investors should track is energy cost per AI compute unit. When energy prices rise relative to compute output, AI infrastructure margins compress directly.

Sustained volatility in energy markets — particularly shocks tied to disruptions near the Strait of Hormuz — raises the operating cost of training clusters and inference workloads. Firms that secure long-term energy supply through nuclear partnerships, dedicated power agreements, or resilient grid access will hold structural advantages over competitors dependent on volatile electricity markets.

Strategic implication: treat energy supply as a core determinant of AI infrastructure profitability, not a background operating cost.

Supply-Chain Control

The industrial stack described in this paper reveals that upstream processing and manufacturing inputs play a decisive role in determining compute capacity. China’s dominance in multiple processing layers — rare-earth refining, battery materials processing, and electronics manufacturing inputs — creates structural insulation against disruptions in upstream resource regions.

Companies and countries lacking domestic processing capacity remain exposed to shocks in mineral supply chains and industrial inputs. Processing chokepoints determine supply-chain risk at least as much as chip access or software capability.

Strategic implication: evaluate AI infrastructure firms based on their exposure to processing-layer chokepoints, not only on their access to chips or models.

Compute Architecture Divergence

The global AI ecosystem is increasingly dividing into two partially independent infrastructure stacks. Western AI infrastructure relies heavily on NVIDIA GPU design, TSMC semiconductor fabrication, and hyperscale data-center networks. China’s strategy emphasizes vertical integration from domestic minerals through Chinese processing, domestic semiconductor development, and Huawei Ascend compute infrastructure.

Western stack: NVIDIA → TSMC → hyperscalers

Chinese stack: domestic minerals → Chinese processing → Huawei Ascend → state infrastructure

If these stacks diverge further, the AI industry may evolve into two parallel ecosystems rather than a single global market. Investors must determine which stack becomes economically dominant — and position accordingly before that divergence becomes consensus.

Strategic implication: monitor whether Chinese infrastructure becomes sufficiently self-sufficient to operate independently of Western semiconductor supply chains.

Monitoring Dashboard

Four observable signals will reveal whether the structural dynamics described in this paper are intensifying. Movement in any one of them has compounding effects on the others, because the AI industrial stack is a dependency system rather than a collection of independent variables. Investors who track these signals together will have earlier visibility into structural shifts than those who monitor chip availability or model benchmarks alone.

● Energy market volatility — Persistent increases in energy-market risk premiums tied to Strait of Hormuz disruptions signal rising cost pressure on global AI infrastructure. Watch sustained moves in Hormuz insurance premiums, long-term oil futures, and electricity prices in AI data-center regions.

● Chinese industrial consolidation — Expansion of Chinese state-owned enterprises into mineral processing, refining capacity, or manufacturing inputs reinforces China’s structural advantage in the processing layer. Watch SOE acquisition activity in Latin America and Africa.

● Chinese domestic compute infrastructure — Rapid deployment of Huawei Ascend clusters or state-directed AI data-center expansion signals growing insulation of China’s AI ecosystem from global supply-chain disruptions.

● Western energy infrastructure expansion — Large-scale nuclear, grid, or natural-gas investments linked to AI data-center development could offset China’s processing-layer advantage by strengthening Western energy resilience. Watch hyperscaler power-purchase agreements and nuclear partnership announcements.

XIII. Vision Function CDT Flows, Interpretation, and Foresight Predictions

MindCast AI evaluates the Venezuela–Iran pattern by running the identified parties through a routed set of Vision Function CDT flows. The relevant parties are: the United States as intervention actor, China as downstream industrial actor, Venezuela as resource-layer node, Iran as energy-layer node, and the Western AI infrastructure stack as the exposed compute system. Each flow generates an independent output; the convergence of those outputs across causation, geometry, behavioral economics, and game theory frameworks constitutes the evidentiary basis for the Silence Dividend thesis.

1. Causation Vision CDT Flow

Target parties: United States, Venezuela, Iran, Western AI infrastructure, China

Signal intake

● U.S. intervention in Venezuela

● U.S. strike on Iran

● China non-escalatory response

● Persistent dependency of AI infrastructure on minerals, energy, and processing

Causal inference engine

Both U.S. actions affected adjacent upstream layers of the same industrial stack. Venezuela touched the resource layer; Iran touched the energy layer. Both layers feed the cost structure of semiconductor fabrication and hyperscale compute.

Causal Signal Integrity result

High enough to reject coincidence as the dominant explanation. The events are better classified as a shared upstream disruption pattern within the AI industrial stack.

Interpretation

The paper’s core pattern holds. The Venezuela and Iran events should be analyzed together because they affect adjacent cost and input layers in the same supply system.

Foresight prediction

If a third geopolitical disruption strikes either the processing layer or the grid layer, markets will begin repricing AI infrastructure as an industrial system rather than a software sector. The likelihood of that repricing rises if energy premiums remain elevated through the next 6–12 months.

2. Field-Geometry Reasoning CDT Flow

Target parties: China, Western AI infrastructure, Venezuela, Iran

System model input

Minerals → Processing & Refining → Energy → Grid Capacity → Chips → Compute → AI Models

Geometry Dominance Test

The stack behaves as a vertical dependency system. Shocks propagate upward through the stack, while durable control sits at processing, manufacturing, and infrastructure bottlenecks.

Result

Geometry dominates intent-first or incentive-first explanations. China sits downstream of the disrupted layers and therefore absorbs less direct strategic damage than Western compute infrastructure.

Interpretation

China’s silence is structurally rational because the country occupies a better geometric position in the supply chain than the actors exposed to energy and mineral cost volatility.

Foresight prediction

Unless the United States materially reduces dependence on globally exposed processing and energy inputs, future upstream shocks will continue to strengthen China’s relative position without requiring overt Chinese escalation. Over a 12–24 month window, the most likely outcome is widening divergence between Western compute costs and Chinese industrial-stack resilience.

3. Chicago Law & Behavioral Economics Vision CDT Flow

Target party: China Industrial System CDT

Coase test

Transaction costs of escalation are high. Direct confrontation risks sanctions expansion, trade disruption, financial instability, and acceleration of balancing coalitions.

Becker test

Expected gains from escalation are limited because the disrupted layers sit upstream of China’s strongest positions. Expected penalties remain high.

Posner test

Efficient breach logic applies. China can preserve structural advantage while allowing rivals to absorb the visible costs of intervention and disruption.

Result

Non-reaction is the rational equilibrium. China benefits more from preserving downstream industrial advantage than from contesting upstream disruptions directly.

Interpretation

The Silence Dividend is not rhetorical. It is the output of a law-and-behavioral-economics equilibrium in which expected penalties exceed gains and structural advantage compounds through restraint.

Foresight prediction

China will continue favoring industrial consolidation, infrastructure scaling, and selective diplomatic criticism over direct escalation when future disruptions occur upstream of its controlled layers. That pattern is likely to persist over the next 1–3 years unless a shock directly threatens Taiwan, domestic energy security, or Chinese-controlled processing capacity.

4. Chicago Strategic Game Theory Vision CDT Flow

Target parties: United States, China, Western AI infrastructure

Interaction model

The United States imposes costly interventions at upstream nodes. China preserves advantageous downstream position in processing, industrial coordination, and increasingly domestic compute infrastructure.

Equilibrium test

One player absorbs intervention costs and external volatility. The other player gains from delay, non-reaction, and structural insulation.

Result

Delay-dominant equilibrium. China’s best response is not counter-escalation but strategic patience while the United States bears the costs of intervention and Western compute systems bear the costs of volatility.

Interpretation

The relevant equilibrium is not military parity but industrial asymmetry. China wins when the game remains at the level of upstream disruption while control of downstream bottlenecks stays intact.

Foresight prediction

If Washington continues to treat AI competition primarily as a chip or software contest rather than an industrial-stack contest, China’s relative strategic position will improve even without visible geopolitical victories. The highest-probability equilibrium over the next 2–5 years is a dual-stack world in which Chinese AI infrastructure becomes more insulated while Western infrastructure remains more globally exposed.

Combined Runtime Interpretation

The routed Vision Function outputs converge on one conclusion. Venezuela and Iran are not isolated geopolitical episodes. They are adjacent upstream shocks inside the same industrial system. China’s muted response reflects downstream control, not passivity. The industrial geometry of the AI stack allows Beijing to preserve advantage through non-reaction so long as disruption remains upstream of the layers it controls.

That convergence produces the paper’s central conclusion: the Silence Dividend. Four independent analytical frameworks, operating on the same input data, arrive at the same behavioral prediction and the same structural explanation. When that degree of cross-framework convergence occurs, the result is not a hypothesis — it is a foresight output with institutional-grade evidentiary support.

Vision Function Runtime Summary

Foresight Simulation Output Classes

Base case — Dual-stack equilibrium

Western AI infrastructure remains strong but exposed to volatile energy, processing, and fabrication dependencies. Chinese AI infrastructure becomes more vertically integrated and more resilient. This is the highest-probability path over the medium term.

Bull case for the United States

U.S. natural gas abundance, nuclear expansion, grid buildout, and supply-chain reshoring reduce exposure to upstream shocks. Western compute leadership holds if energy resilience improves faster than Chinese domestic chip substitution.

Bull case for China

China deepens processing dominance, accelerates domestic compute deployment, and benefits from repeated upstream disruptions that raise Western infrastructure costs without threatening Chinese-controlled bottlenecks.

Observable Foresight Predictions

● Energy repricing will matter more to AI margins than most software analysts currently model. Sustained Hormuz-related energy premiums will begin appearing in infrastructure economics, data-center siting decisions, and power-contract strategy.

● China will respond to future upstream shocks with industrial acceleration rather than headline escalation. Watch for processing investments, state-backed manufacturing moves, and infrastructure coordination rather than public confrontation.

● Western and Chinese AI infrastructure stacks will continue diverging. The divergence will appear first in energy resilience, domestic chip substitution, and compute-cluster coordination rather than in frontier-model rhetoric.

● Taiwan remains the main falsification boundary. The silence-dividend logic applies when shocks remain upstream of China’s controlled layers. A direct threat to Taiwan would alter the equilibrium and trigger a different strategic logic.

XIV. Strategic Conclusion

Observers commonly frame the AI race as a contest between software systems or machine-learning algorithms, which correctly identifies where capability appears but misidentifies where it originates. The governing equilibrium runs deeper in the industrial stack — in the mineral deposits, processing facilities, energy corridors, and grid infrastructure that ultimately determine how much compute a country can deploy. Algorithmic advantage built on a fragile industrial foundation is a temporary lead, not a durable one.

Resources power energy systems. Energy systems power electrical grids. Electrical grids power semiconductor fabrication plants and hyperscale data centers. Each layer in that chain depends on the one below it, which means shocks at the base propagate through the entire structure above.

Countries that dominate the early layers of the stack gain durable advantages in AI capability. China’s silence in response to disruptions at the resource and energy layers reflects that structure — not diplomatic restraint, and not passivity. Beijing does not need to escalate aggressively when the layers it controls remain intact.

The Silence Dividend describes the structural advantage that accrues to countries positioned downstream of disrupted layers, and it compounds silently while markets focus on model benchmarks and chip counts. Markets have not yet priced it. The Silence Dividend is not a geopolitical metaphor. It is an industrial asymmetry embedded in the global AI supply chain. The country that controls the infrastructure layers beneath compute will determine the long-term economics of artificial intelligence.