MCAI Lex Vision: Death by a Thousand Depositions, A Pre-Foresight Simulation of Compass's Multi-Vector Regulatory Collapse

What Compass's 42-Day Exposure Window Reveals About How Institutional Capture Fails

Companion to Nineteen Senators, Seventeen Questions, How Compass Bought Its Antitrust Clearance and The Compass Commission Consolidation Strategy and Real Estate Marketing Transparency, The Compass-Anywhere Address Suppression Calculus.

I. Framing: What a Foresight Simulation Actually Does

Most regulatory analysis is retrospective. A firm loses a case, a bill passes, a stock drops — and analysts explain what happened. MindCast AI builds in the other direction: predicting the structural sequence before the outcomes are known.

The eight-vector framework below was adapted from Section VI of Senators to DOJ: Did Compass Buy Its Merger Clearance?, which analyzed the February 19, 2026 Warren letter and its consequences across the full Compass-Anywhere merger record. The Seattle ultra-luxury transaction dataset — 130 transactions, four commission-flow categories, the Mercer Island Exhibit Transaction, and the full Layer 3 private exclusive scaling arithmetic — is documented in The Compass Commission Consolidation Strategy and Real Estate Marketing Transparency, published the same day SSB 6091 was before the Washington House.

What makes the foresight simulation approach distinctive is that MindCast treats enforcement and markets as a single computable control system rather than separate analytical domains.

Every problem enters through Chicago School Law and Behavioral Economics as the base layer — the discipline of price theory, institutional incentives, and rational actor behavior under constraint. Chicago School Accelerated — The Integrated, Modernized Framework of Chicago Law and Behavioral Economics. From there, each problem routes through a predictive control stack that determines whether plain Chicago logic suffices or whether higher-order frameworks must govern.

The Nash–Stigler equilibrium supplies the termination logic: identifying when multi-jurisdictional conflict settles at the point where no state AG, no federal court, and no legislature offers the firm a better unilateral outcome than capitulation, and when the evidentiary record is sufficient to drive that settlement without additional proof. The Dual Nash-Stigler Equilibrium Architecture.

Tirole-style advocacy arbitrage governs pre-game constraint — modeling how a firm structures its forum-specific arguments before institutional audiences have coordinated. Phase and geometry analysis handles structural lock-in: mapping when a regulatory configuration becomes self-reinforcing rather than reversible. A Tirole Phase Analysis of Advocacy-Driven Antitrust Inaction at the U.S. Department of Justice and The Geometry of Regulatory Capture at the U.S. Department of Justice Antitrust Division.

Each framework is tied to explicit, falsifiable signals and run through cognitive digital-twin simulations — not after-the-fact narrative, but forward-state predictions against which observable outcomes are tested in real time.

What follows is not a post-hoc explanation of Compass’s difficulties. The vector framework was constructed before the depositions began, before any goodwill impairment review, before the July 2026 Zillow trial opened. The analytical value is not that we can describe what happened. It is that the compounding logic of these eight vectors — and their cross-contaminating relationships — was predictable from the moment the merger closed.

That predictability rests on one core insight: the danger to Compass was never any single proceeding. A firm the size of the combined Compass-Anywhere entity can survive a federal antitrust case. It can survive a 49-0 legislative defeat. It can survive congressional scrutiny of a merger clearance decision. What it cannot survive — at least not without structural recalibration — is all of those things activating simultaneously, feeding each other’s evidentiary records, with none requiring the others to succeed in order to cause damage.

That is what a multi-vector collapse looks like. And that is what was set in motion within 42 days of merger close.

To create a runtime simulator of issues in this publication, simply upload the URL into any LLM, and prompt ‘create framework with three degrees of cited sub links.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure for more info.

II. The Setup: 42 Days That Changed Everything

On January 9, 2026, the profit thesis for the Anywhere acquisition was straightforward: 340,000 agents at national scale, $225 million in projected cost synergies, $1 billion in high-margin franchise revenue, and a private exclusive window routing premium inventory through Compass’s internal network before open market exposure — capturing both commission sides on transactions that would otherwise split with a cooperating broker.

The Zillow antitrust trial, scheduled for July 2026, was the primary legal risk. Even that carried a plausible defense.

Six weeks later, the landscape had changed on every dimension simultaneously.

SSB 6091 passed the Washington State Senate 49-0, closing the private exclusive window in the state that generated $4.2 million in captured commission from a single metro’s monthly record. Wisconsin and Illinois advanced concurrent marketing requirements. The Southern District of New York denied Compass’s preliminary injunction against Zillow — rejecting the entire antitrust theory on its merits. Judicial Deconstruction of Compass’s Narrative Arbitrage v. Zillow. Nineteen senators formally accused the DOJ of corruption in clearing the merger. COMP dropped 3.2% in a single day on the letter’s publication. Nineteen Senators, Seventeen Questions, How Compass Bought Its Antitrust Clearance.

The regulatory assumption that justified $400-800 million of the acquisition premium — that private exclusives could be deployed at national scale without interference — was challenged in federal court, rejected in state court, legislated against in multiple states, and made the subject of a congressional corruption inquiry. All within 42 days of the merger closing.

What follows is the damage assessment. Not a list of problems. A structural analysis of why the combination is categorically different from any of the individual components — and why that distinction was predictable from the architecture before any of the outcomes materialized.

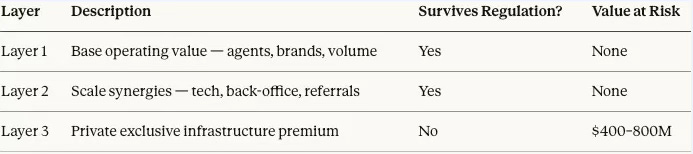

III. What the Acquisition Actually Bought: The Three-Layer Hierarchy

To understand why the eight vectors below carry the weight they do, the $1.6 billion acquisition price must be decomposed — and the transaction record that proves it must be understood as more than illustration. Not all of the acquisition value depends on the same operating conditions. Not all of the evidence against it requires a subpoena to access.

The Three-Layer Acquisition Hierarchy separates what survives transparency legislation from what does not. The transaction record that quantifies Layer 3 is publicly available, permanently discoverable, and simultaneously accessible to every enforcement sovereign examining Compass right now. The fight over private exclusives is entirely about the third layer. The evidentiary record documenting that fight was already recorded by the MLS before this publication was written.

III-A: Why the Transaction Record Is Evidentiary, Not Illustrative

The Seattle ultra-luxury transaction data presented in Section III-B is not anecdote. Before the numbers are read, three structural features of the record establish why it functions as enforcement-grade evidence across every forum currently examining Compass — without coordination between those forums, and without a single subpoena.

Provenance: Corporate Conduct, Not Agent Discretion. Team Foster operates under Compass’s brand infrastructure, Compass’s managing broker licensing, and Compass’s corporate platform. The address suppression documented on MLS #2392995 — the $79,000,000 Lake Washington estate listed on February 19, 2026 with full photographs, price, and specifications but no address — runs simultaneously across Compass’s website, Team Foster’s Compass-branded platform, print marketing, and the NWMLS entry. No individual agent made an isolated decision. The suppression is coordinated across every distribution channel Compass controls. That coordination is the threshold distinction for UDAP enforcement and institutional liability: it is corporate conduct, not individual agent behavior, and the multi-channel documentation proves it without inference.

Compass’s own Disclosure Form acknowledges that private exclusive marketing “may reduce the number of potential buyers,” “may reduce the number of offers,” and may reduce “the final sale price.” On his Q1 2025 earnings call, CEO Robert Reffkin stated the opposite: “There is no downside.” Neither document is internal. Both are in the public record. The gap between the CEO’s public statement and the company’s own client disclosure — on the same factual question — is the deceptive trade practices exposure under state UDAP statutes. Washington’s AG Civil Rights Division confirmed enforcement authority exists for exactly that conduct in the January 2025 Senate hearing transcript, a permanently discoverable legislative record now available to every state AG investigating the same business model.

Self-Authentication: No Subpoena Required. NWMLS role designations are recorded at transaction close and accessible through standard MLS search. Seattle Agent Magazine publishes the top-10 monthly luxury sales sourced directly from that data, with listing and buyer agent names and brokerage affiliations, every month without exception. Neither source requires litigation discovery, FOIA requests, or investigative access to obtain. Any state AG, legislative staff member, federal court clerk, or opposing counsel can reproduce the full 130-transaction dataset from public sources in an afternoon. The Mercer Island Exhibit Transaction — 1628 72nd Ave. SE, MLS #2362507, sold August 2025 — records four role designations: Tere Foster as listing broker and buyer broker, Moya Skillman as co-listing broker and co-buyer broker. Those designations are in the MLS. They were recorded at close. No expert witness is required to interpret them. The record is self-authenticating.

Cross-Forum Simultaneity: Every Sovereign, Same Dataset. The same transaction record is simultaneously available — without coordination — to the SDNY Zillow antitrust trial scheduled for July 2026; the NWMLS antitrust case in the Western District of Washington; the Warren letter congressional inquiry with AG Bondi’s response due March 5; Washington’s AG Civil Rights Division, which has already confirmed UDAP enforcement authority on the record; every state legislature advancing a concurrent marketing bill; and every auditor testing the goodwill assumptions recorded at the Anywhere acquisition close. No forum needs to introduce the dataset as evidence for another forum to draw from it. The MLS recorded it. Seattle Agent Magazine published it. Every enforcement sovereign has had access since the month each transaction closed. What the Warren letter and SSB 6091 accomplished in February 2026 was not to create the evidentiary record. It was to ensure that every forum is now looking at it at the same time.

III-B. The Evidentiary Dataset

To understand why the eight vectors below carry the weight they do, the $1.6 billion acquisition price must be decomposed. Not all of it depends on the same operating conditions — and the fight over private exclusives only makes sense once you understand which layer of the acquisition they defend, and why that layer is not optional.

Layer 1 — Base Operating Value. Anywhere Real Estate was worth something as a standalone brokerage before Compass arrived: 340,000 agents, established brands including Coldwell Banker and Century 21, and a functioning transaction volume. Layer 1 is reflected in Anywhere’s pre-acquisition stock price, which had been declining as a legacy portfolio with compressed margins. Layer 1 survives any regulatory change. Concurrent marketing mandates, antitrust verdicts, and congressional investigations do not touch it. It is the floor.

Layer 2 — Scale Synergies. Above the floor sits the value created by combination: technology integration, back-office consolidation, cross-brand referrals, and recruiting leverage. A seller choosing between the combined Compass-Anywhere entity and a six-person independent brokerage still sees a resource gap regardless of whether concurrent marketing is required. Layer 2 describes a viable brokerage competing on service quality, agent talent, and operational efficiency. In Seattle, Windermere competes at 35% luxury market share without private exclusives — entirely on Layer 2 value. Layer 2 survives transparency legislation. It is the honest version of the acquisition thesis.

Layer 3 — Private Exclusive Infrastructure Premium. The third layer is where the acquisition math breaks down under regulatory pressure. Layer 3 is the value that exists only if the combined entity can hold listings off the open market long enough for an internal buyer to arrive first — capturing both commission sides on transactions that would otherwise split with a cooperating broker.

Two mechanisms compound Layer 3. The first is direct dual-agency: Compass holds the listing, routes a Compass buyer before any outside buyer sees it, and collects both the listing-side and buyer-side commission inside one firm. The second is merger internalization: transactions that previously crossed corporate lines — a Compass listing sold by a Coldwell Banker Bain buyer agent — now stay inside the combined entity without any change in agent behavior. The merger itself was the routing mechanism. Private exclusives increase the conversion rate within it.

In Seattle’s ultra-luxury market — the top-10 monthly sales by price across 13 months and 130 transactions — 16 produced commission flows that stayed or now stay entirely inside the combined Compass-Anywhere entity. Eight were confirmed dual-ends where Compass represented both buyer and seller. Eight more were cross-brand transactions that became internal revenue the moment the merger closed, without a single agent changing behavior. Together they represent $167.5 million in transaction value and $4.2 million in captured buyer-side commission from one metropolitan market’s monthly top-10 record alone. Scaled to Compass’s 35 major markets at 10-15 times the top-10 transaction volume, the same internalization rate implies $600 million to $1.5 billion of the acquisition price resting on a single operating condition: that listings can be withheld from the open market long enough for an internal buyer to arrive first.

At the Mercer Island Exhibit Transaction — 1628 72nd Ave. SE, sold August 2025 at $15,000,000 — the NWMLS records four role designations: Tere Foster as listing broker and buyer broker; Moya Skillman as co-listing broker and co-buyer broker. The same two agents who owed fiduciary duty to the seller also represented the buyer. Every dollar of the $750,000 total commission — listing side and buyer side — was captured by the same two people. No scaling or projection is required to understand the mechanism. The MLS recorded it.

Layer 3 is estimated at $400-800 million of the $1.6 billion acquisition price at the conservative end. Priced assuming states would not mandate concurrent marketing, federal courts would not reject the antitrust inversion theory, and transparency pressure would not reach critical mass — Washington and the Southern District of New York called that position within a single calendar week.

Critically, Layer 3 is not a business enhancement layered on top of a profitable core. Anywhere Real Estate carried $2.5 billion in net corporate debt at September 30, 2024; Compass assumed approximately $2.6 billion of that debt in the transaction. The firm has never posted a full-year GAAP profit. Under that debt load, with quarterly debt-service obligations compressing the profit horizon, private exclusives are not a strategic preference. They are a balance-sheet necessity. Every state that closes the private exclusive window tightens the financial constraint the merger itself created. The mechanism being defended is not discretion. It is solvency.

Layer 1 and Layer 2 describe a company. Layer 3 describes the acquisition premium that requires regulatory permission to exist. The eight vectors below map what happens when that permission is withdrawn simultaneously across multiple institutional forums.

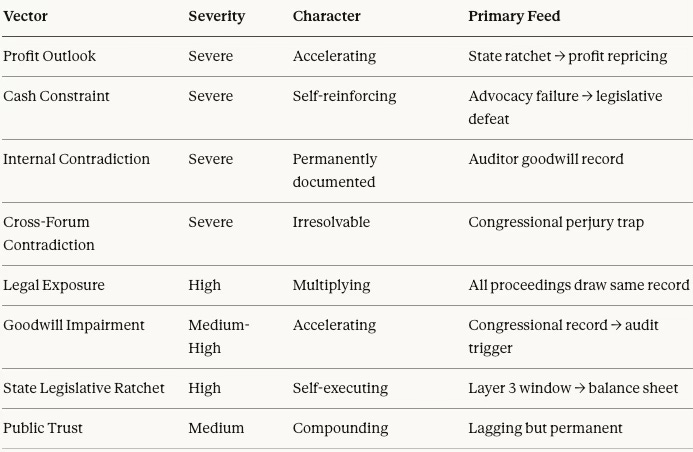

IV. The Eight-Vector Framework

The February 19, 2026 Warren letter does not operate on a single dimension. Compass's consequences run across eight distinct vectors — each with its own timeline, severity, and compounding relationship to the others. No single vector is fatal in isolation. The merger closed 42 days ago. Every enforcement vector activated within that window. What makes the current moment structurally different from anything Compass has faced since its founding is not the presence of any one threat but the simultaneity of all of them — and the way each feeds the evidentiary record the others draw from.

IV-A. A Methodological Note on Simultaneity

Before running the vectors, the simultaneity point deserves explicit treatment — because the conventional way of evaluating regulatory risk misses it entirely.

Standard risk assessment asks: what is the probability of an adverse outcome in each proceeding? That framing treats each vector as independent. It produces a portfolio of manageable risks, each survivable, each discountable against the probability of a favorable outcome.

The MindCast framing asks a different question: what happens when multiple proceedings draw from the same evidentiary record, and each proceeding’s outputs feed every other proceeding’s inputs?

That is not a portfolio of independent risks. It is a compounding network. The congressional record becomes the goodwill impairment trigger. The state legislative ratchet becomes the profit deterioration mechanism. The internal contradiction becomes the cross-forum perjury trap. The cash constraint explains why the advocacy operation failed. Every vector connects to every other. None resolves without implicating the rest.

The vector interaction map in Section V describes the primary feed relationships. The simulation runs each vector in sequence — but the sequence is artificial. In practice, all eight are running simultaneously.

IV-B. Vector 1: Profit Outlook Deterioration — Severe, Accelerating

The acquisition premium rested on a specific operating condition: that restricted listing visibility would remain legally permissible at national scale across 35 major markets. Priced as a near-certainty at close, within 42 days that condition had been challenged or closed in multiple simultaneous forums.

SSB 6091 eliminated it in Washington. Wisconsin enacted its own restriction in December 2025. Illinois reintroduced a concurrent marketing bill in February 2026. The SDNY preliminary injunction denial confirmed the antitrust theory Compass deployed to protect the mechanism nationally is not legally sound. The Warren letter activated a congressional record drawing from the same merger clearance process.

Each state that passes a no-opt-out concurrent marketing requirement closes a piece of the private exclusive window independently of any other proceeding. The private exclusive window is not a single target to defend. It is a distributed operating condition that degrades state by state, court by court, proceeding by proceeding. The profit thesis does not survive the distributed ratchet. It reprices at each legislative event.

IV-C. Vector 2: Cash Constraint — Severe, Self-Reinforcing

Compass entered the Washington State legislative fight carrying nearly $3 billion in post-merger debt, $127 million in cash on hand after burning $105 million on the Christie’s acquisition alone, and over $1.5 billion in cumulative operating losses across four years. The firm has never posted a full-year GAAP profit.

The Mike Davis federal bypass cost at least $1 million. Zillow/NWMLS litigations, and NAR lobbying run concurrently, each carrying ongoing legal spend. Against that balance sheet, the SSB 6091 opposition operation reads less like a funded professional advocacy campaign and more like a company sending employees it already pays — Brandi Huff to testify, Cris Nelson and Michael Orbino to sign in CON and stay silent — because retaining outside counsel and a professional lobbying shop was not an available line item. Nelson was present in Olympia.

LPT International CEO Michael Valdes observed after the merger close that a lack of agility follows from the debt load and the absence of a clear path to retiring it within a concise period. The SSB 6091 result confirms the diagnosis. A firm with sufficient cash and lobbying infrastructure finds a single sympathetic senator in eleven days. Compass found none across the entire Washington State Senate.

The 49-0 margin is not just a legislative outcome. It is a cash constraint diagnostic. Vector 2 feeds Vector 1 by limiting the advocacy resources available to prevent each subsequent legislative defeat.

IV-D. Vector 3: Internal Contradiction — Severe, Permanently Documented

The strategic contradiction at the core of the acquisition predates the merger close and cannot be retroactively resolved.

Anywhere CEO Ryan Schneider called the private listings approach “short-sighted” and “not our recommendation” on Anywhere’s February 2025 earnings call — while simultaneously telling investors Anywhere was prepared to deploy private listings at scale if competitors forced the market in that direction. Coldwell Banker CEO Kamini Lane wrote that private listings ignore the law of supply and demand. ERA Real Estate President Alex Vidal told Inman in July 2025 that private listing network talk simply did not exist “in the field.”

Compass acquired that skepticism along with the agents and brands. Every statement is timestamped, published, and available to every auditor, plaintiff, and state AG evaluating the goodwill assumptions recorded at close.

The internal contradiction matters for a specific reason: it places auditors in an uncomfortable position. The goodwill assumptions underlying the acquisition rested on Layer 3 — the ability to route premium inventory through internal networks before open market exposure. The Anywhere leadership ecosystem expressed consistent public skepticism about that mechanism’s strategic validity, on the record, in investor calls, in published op-eds, and in trade press. When the annual impairment review arrives, those statements become part of the factual record auditors must weigh against the goodwill carrying value.

IV-E. Vector 4: Cross-Forum Contradiction — Severe, Irresolvable

Narrative-driven strategies cannot overcome cross-forum pattern recognition of contradictions, where forum-specific rhetorical framings collapse against each other. Vector 4 is the one Compass cannot fix.

Compass is on record in federal court arguing that restricted listing visibility harms consumers and forecloses competition — the foundation of its antitrust suits against Zillow in the SDNY and against NWMLS in the Western District of Washington. Before state legislatures, Compass argues the opposite: restricted visibility protects consumers through privacy and seller choice. On its homeowner-facing website, Compass frames the same restriction as protection from “organized real estate.” Three positions, three forums, zero compatibility.

The February 3 Reffkin national MLS proposal compounded the exposure permanently. The Chicago School Accelerated Part I, Coase and Why Transaction Costs ≠ Coordination Costs. The firm that spent years in federal court arguing that MLS coordination rules harm competition proposed building a national MLS it would control, with flexible marketing rules it would write. The firm that sued to dismantle coordination infrastructure proposed to own it. That sequencing entered the congressional record, the Inman archive, and the federal court docket simultaneously. No forum separation remains.

The congressional inquiry under construction is now the first institutional venue requiring Compass to produce a single factual narrative across all three positions simultaneously. A false answer is perjury. A true one is an admission. The cross-forum contradiction, which functioned as a sustainable strategy when forums remained separated, becomes a structural liability the moment a single record forces simultaneous accountability.

IV-F. Vector 5: Legal Exposure — High, Multiplying

The congressional record under construction is the most operationally dangerous instrument in the current environment — not because of what it might produce directly, but because every answer AG Bondi provides by March 5, or declines to provide, becomes part of the permanent institutional record accessible to private plaintiffs, state attorneys general, and every federal court handling Compass-related antitrust matters.

The Pitts deposition of Mike Davis, William Levi, and Arthur Schwartz under oath in the HPE-Juniper Tunney Act proceedings runs concurrently, covering the same routing architecture the Warren letter investigates. If Davis’s sworn deposition testimony contradicts anything in DOJ’s congressional response, the gap is a perjury exposure that neither Compass nor Davis controls and neither can retract.

The Zillow federal antitrust trial is scheduled for July 2026 in the SDNY. The NWMLS case runs in the Western District of Washington. The NAR settlement created ongoing compliance obligations. Each proceeding draws from the same factual record the congressional inquiry is now expanding under oath.

Five simultaneous legal proceedings, each building the evidentiary record the others draw from. The structure is additive in a specific direction: each new sworn statement, each new congressional response, each new deposition excerpt narrows the space available for factual maneuvering in every other proceeding.

IV-G. Vector 6: Goodwill Impairment — Medium-High, Accelerating

The $400-800 million acquisition premium rested on a specific regulatory assumption: that private exclusives could be deployed at national scale across 35 major markets without legislative or judicial interference. Auditors testing that assumption for the next annual impairment review now face a materially different regulatory environment than existed at close.

Wisconsin enacted listing transparency restrictions in December 2025. Illinois reintroduced its bill in February 2026. Washington passed SSB 6091 49-0. The SDNY rejected Compass’s preliminary injunction against Zillow on the merits. Nineteen senators signed a formal corruption inquiry naming the merger mechanism. COMP dropped 3.2% the day the Warren letter became public — the market assigning probability within 24 hours to a scenario in which the regulatory assumptions underlying the acquisition premium do not hold.

One state enactment does not trigger impairment review. A coordinated multi-state legislative ratchet combined with a congressional investigation of the merger’s regulatory clearance is a different category of risk entirely. The question is not whether goodwill impairment becomes relevant — it is when the cumulative divergence between the acquisition assumption and regulatory reality becomes too large for the annual test to absorb.

Vector 6 connects directly to Vector 3: Anywhere leadership’s documented skepticism of the private exclusive mechanism, now part of the publicly available record, provides auditors a basis for treating the regulatory divergence as consistent with pre-existing internal doubts rather than an unpredictable external shock.

IV-H. Vector 7: State Legislative Ratchet — High, Self-Executing

SSB 6091 passed the Washington State Senate 49-0 on February 10 — bipartisan, zero amendments, zero opt-outs, zero absences. Compass’s lobbying operation had eleven days between committee passage and the floor vote to find a single sympathetic senator willing to insert the twelve-word exception that would have preserved the private exclusive model in Washington. None emerged.

The “seller choice” and “privacy protection” narrative achieved zero persuasive traction across the entire chamber — not among Democrats, not among Republicans, not among rural members, not among urban ones.

The ratchet is self-executing: it does not require DOJ cooperation, congressional authorization, or judicial approval. Each state that enacts a concurrent marketing requirement closes a piece of the private exclusive window independently. Under $2.5 billion in merger debt with quarterly debt-service obligations compressing the profit horizon, private exclusives are not a strategic preference — they are a balance-sheet necessity. Each state that closes the window tightens the financial constraint the merger itself created.

The Parker v. Brown doctrine amplifies the ratchet’s durability. Each adopting state reinforces the “clearly articulated state policy” standard, making federal preemption challenges progressively weaker as the state count rises. California, New York, and Texas — the other major concentration markets post-merger — represent the next ratchet positions. Five states with no-opt-out concurrent marketing requirements is not a regulatory headwind. It is a material assumption failure in the Anywhere acquisition underwriting.

IV-I. Vector 8: Public Trust and Reputation — Medium, Compounding

The word “corruption” appeared in mainstream real estate industry press within 24 hours of the Warren letter’s publication. 340,000 agents now operate under a company whose merger clearance is under active congressional investigation.

Seller confidence, buyer confidence, and agent retention are lagging indicators — they do not move immediately on a single news cycle. But the reputational vector compounds with each proceeding. Every deposition excerpt, every congressional non-response, every state legislative defeat adds another data point to the public record that agents, sellers, and institutional partners must evaluate.

Compass-dominant markets — Manhattan, Washington D.C., Seattle — are exactly the markets where sophisticated sellers and high-net-worth buyers have the most alternatives. Windermere East appeared seven times in the Seattle ultra-luxury dataset as the outside brokerage that won buyer-side commission on Compass listings through open-market competition — demonstrating that a luxury brokerage with 35% market share can operate without private exclusives and win. Windermere’s Regional Director Lucy Wood testified under oath that Windermere could deploy the private exclusive model and chose not to. That testimony now competes with Compass’s reputational position in the same market, in the same permanent legislative record.

Reputational damage is recoverable if the legal vectors resolve favorably. The legal vectors will not all resolve favorably. Too many simultaneous proceedings with too many different sovereigns are extracting the same information under oath.

V. The Vector Interaction Map

The structural argument is not that any single vector is fatal. The feed relationships between vectors create a compounding network where each adverse development simultaneously strengthens multiple other attack surfaces.

Congressional record → Goodwill impairment trigger. Each sworn statement in the congressional inquiry and the Pitts depositions expands the factual record auditors must account for when testing the Layer 3 assumption.

State legislative ratchet → Profit deterioration mechanism. Each state that passes concurrent marketing requirements eliminates another piece of the operating condition the acquisition premium required.

Internal contradiction → Cross-forum perjury trap. Anywhere leadership’s documented skepticism of the private exclusive mechanism, combined with Compass’s three-forum narrative incompatibility, makes any single sworn account of the acquisition rationale potentially self-contradictory against the published record.

Cash constraint → Advocacy failure. The balance sheet constraint explains why Compass could not sustain a professional lobbying operation across multiple concurrent state legislative fights — confirming the ratchet’s self-executing character.

Legal exposure → Cross-forum contamination. Each sworn deposition, each congressional response, each trial exhibit expands the record every other proceeding draws from.

The cascade runs in both directions. Legislative defeats feed legal exposure. Legal exposure feeds goodwill impairment. Goodwill impairment feeds profit deterioration. Profit deterioration feeds cash constraint. Cash constraint feeds advocacy failure. Advocacy failure feeds the next legislative defeat.

Compass’s worst-case scenario is not a single prosecution, a single adverse verdict, or a single legislative defeat. The structural danger is simultaneity: eight vectors activating within 42 days of merger close, each feeding the evidentiary record the others draw from, none requiring the others to succeed in order to cause damage.

VI. The Forward Prediction

The framework above was built before outcomes materialized. The forward test is already running.

Seven active Team Foster listings documented on fosterrealty.com on February 19, 2026 — $136 million in inventory, $3.4 million in buyer-side commission at stake — include MLS #2392995, a $79,000,000 Lake Washington estate listed without an address. Any buyer seeking to locate the property must contact Team Foster directly, entering the Compass internal routing network before any independent buyer’s agent can identify the property, show it to clients, or compete for the buyer-side representation. When each listing closes, the NWMLS will record who represented the buyer. If the pattern documented in the Mercer Island Exhibit Transaction repeats, the internalization model holds. If independent brokers win the buyer side at open-market rates, the regulatory pressure is already reshaping behavior before the law formally takes effect.

MLS #2392995 alone represents 58% of total buyer-side commission at stake across all seven active listings — $1,975,000 from a single transaction. The prediction is simple and falsifiable. Closing records will resolve it without interpretation.

The congressional record will resolve its own prediction by March 5 — the date AG Bondi’s response to the Warren letter is due, or declines to be provided. Each outcome feeds the next simulation cycle.

Death by a thousand depositions is not a metaphor. It is the operational description of what happens when eight compounding vectors share a single evidentiary substrate — and none of them stop running.

VII. The Acquisition That Ate Its Own Premium: Why Layer 3 Was Unacquirable at Any Price That Required It

The eight vectors documented above share a common origin. Locating that origin requires running the analytical sequence in reverse — not forward from merger close, but backward from the 42-day collapse to the decision architecture that made it structurally inevitable. The question is not why Compass lost in Olympia, or why the SDNY rejected the preliminary injunction, or why nineteen senators signed a corruption inquiry. Each of those outcomes has a proximate explanation. The deeper question is why a firm with Compass’s institutional sophistication, legal resources, and regulatory experience proceeded with an acquisition that activated all of those outcomes simultaneously within six weeks of close.

The Chicago answer is uncomfortable: the acquisition was rational under the information set Compass disclosed, and catastrophic under the information set the transaction itself generated.

VII-A. The Pricing Paradox

Layer 3 was valued at $400-800 million of the $1.6 billion acquisition price. That valuation rested on a single operating assumption: that private exclusives could be deployed at national scale across 35 major markets without legislative or judicial interference sufficient to close the window.

Pricing that assumption required treating three conditions as stable: federal antitrust clearance would hold, state legislatures would not coordinate concurrent marketing requirements, and the federal court record Compass had spent years building — arguing that restricted listing visibility forecloses competition — would remain forum-separated from the state legislative arguments the private exclusive model required.

All three conditions were destabilized by the merger announcement itself.

The DOJ clearance drew immediate congressional attention precisely because the merger’s scale made the antitrust theory visible at a level it had never been before. Individual Compass listings in individual markets did not generate nineteen-senator corruption inquiries. A national merger that internalized 340,000 agents and $1 billion in franchise revenue did. The clearance decision that was supposed to resolve federal antitrust risk instead created a congressional record examining how that resolution was reached.

State legislative coordination followed the same logic. No single state had organized concurrent marketing legislation while Compass operated as a regional luxury brokerage. The merger announcement transformed a local market practice into a national policy question — giving consumer advocates, competing brokerages, and state attorneys general a unified target that had not existed at the scale required to drive coordinated legislative action. Washington, Wisconsin, and Illinois did not advance concurrent marketing requirements simultaneously by coincidence. The merger made the mechanism legible at the scale that justifies legislative response.

The federal court record contamination was the most avoidable and the least avoided. Compass’s antitrust suits against Zillow and NWMLS were already in the record before the merger closed. Every state legislative argument available to defend private exclusives — seller choice, privacy protection, consumer benefit — ran directly into Compass’s own filed positions arguing the opposite. No merger integration team resolved that contradiction before close because resolving it would have required either abandoning the federal litigation or abandoning the Layer 3 defense. Both options repriced the acquisition downward. Neither was taken.

The pricing paradox is this: the conditions that made Layer 3 worth $400-800 million were conditions the acquisition itself destroyed. The premium was self-liquidating from the moment it was assigned.

VII-B. The Testimony Strategy as Revealed Preference

The most diagnostically precise evidence of Compass’s strategic constraint is not the 49-0 margin. It is the personnel decisions Compass made in the eleven days between committee passage and the Senate floor vote — and what those decisions reveal about the firm’s internal assessment of its own argument.

Cris Nelson is Compass’s most media-credible spokesperson on luxury market conditions. Journalists quote her because she projects market authority. Nelson signed in CON on SSB 6091 and did not testify. Brandi Huff testified in her place. Huff carries no independent media profile, no published record of market analysis, and no credibility capital that cross-examination could damage. The substitution was not a scheduling accident. Compass deployed its least credible available witness in the forum that creates a permanent legislative record, while preserving its most credible spokesperson for forums — press interviews, industry panels, earnings call narratives — where sustained cross-examination does not occur.

That is a rational evidentiary exposure management decision under Chicago. Nelson’s media value derives precisely from the absence of adversarial questioning. Every published quote she has provided on private exclusive benefits, seller choice, and luxury market dynamics is a claim made without cross-examination. Deploying her before a Senate committee — where legislators had access to the MLS transaction record, the Compass disclosure form acknowledging the mechanism may reduce sale prices, and Reffkin’s contradictory “no downside” earnings call statement — would have subjected those claims to adversarial testing for the first time, in a permanently discoverable forum, simultaneously accessible to every enforcement sovereign examining the same business model.

The problem Compass faced was not finding the right witness. Compass could not send Nelson because Nelson’s testimony would have required her to defend a narrative the transaction record directly contradicts. Compass could not send a corporate lobbyist because a retained lobbyist creates a discoverable paper trail — retainer agreements, lobbying registrations, invoice records — connecting Compass’s corporate decision-making apparatus to the opposition effort at exactly the moment when a congressional corruption inquiry was simultaneously examining whether Compass improperly influenced federal regulatory outcomes. Sending employees already on payroll minimized the institutional footprint. Huff, Nelson signing in CON, Michael Orbino silent — the entire legislative presence was constructed to absorb the exposure with the lowest evidentiary cost.

The testimony strategy reveals what Compass’s internal legal team had already concluded: the narrative was not defensible under cross-examination. A firm that believes its argument wins sends its best witness. Compass sent Huff. That decision is the clearest available signal that Compass’s own lawyers understood the self-contradiction before any senator voted.

VII-C. The Three Strategic Windows That Closed

Strategic optionality existed before the merger closed. Each window closed in sequence, and none was used.

Compass could have preemptively and publicly abandoned the Layer 3 mechanism before the merger closed — framing the decision as a proactive competition commitment, offering it as a voluntary merger condition, and building a legislative record across every state that would subsequently advance concurrent marketing requirements. The cost was real and immediate: $400-800 million of acquisition premium disappears from the transaction model. The benefit was structural: every enforcement vector documented in Sections IV and V loses its primary evidentiary substrate. No private exclusive mechanism means no antitrust inversion contradiction, no state legislative target, no goodwill impairment trigger, no cross-forum narrative incompatibility. A Chicago actor with full information about the 42-day collapse trades the certain $400-800 million loss against the probabilistic destruction of the entire acquisition thesis. Compass priced the regulatory risk as manageable. The observable outcomes suggest that pricing assigned too low a probability to coordinated multi-forum activation.

The second window was proactive state legislative authorship at merger close. The strategic alternative to opposing transparency legislation was writing it. A Compass-drafted concurrent marketing framework — introduced in January 2026 before consumer advocates and competing brokerages organized their own bills — would have shaped the operative text, preserved negotiated seller opt-out provisions, and created a public record of Compass as a transparency leader rather than a transparency obstacle. Owning the bill is categorically different from opposing it. SSB 6091’s 49-0 margin reflects the legislative outcome available to a firm that arrives as the opposition. The window required moving in the first two weeks of January 2026. Compass’s opposition posture foreclosed it before legislative sponsors had finished drafting.

The third window was a negotiated opt-out during the SSB 6091 committee process. Consumer advocates wanted transparency, not prohibition. A negotiated seller-directed opt-out with mandatory disclosure requirements was achievable in the first week of committee consideration. Compass’s cross-forum contradiction had already closed that window before the committee convened — because any opt-out language Compass accepted in Olympia would have entered the SDNY Zillow trial and the NWMLS case immediately, where Compass’s litigation position required arguing that any restriction on listing visibility forecloses competition. Accepting a legislative restriction it was simultaneously arguing was anticompetitive in federal court was not a coherent option. Window Three closed not because Compass chose the wrong negotiating posture, but because the federal court record foreclosed any negotiating posture that acknowledged the mechanism’s costs.

Each window closed because the prior strategic failure had already foreclosed it. The sequence was not bad luck. It was the compounding output of a single upstream decision: acquiring Layer 3 at a price that required it to survive.

VII-D. Why Compass Proceeded Anyway

The rational actor question deserves a direct answer. Compass is not an unsophisticated institution. Its legal team understood the federal court record. Its regulatory team understood state legislative dynamics. Its finance team understood the balance sheet constraint.

Why did a sophisticated actor proceed with an acquisition whose premium rested on conditions the acquisition itself destabilized?

Three mechanisms explain the decision architecture. Optimism bias in regulatory risk pricing led Compass to extrapolate from its pre-merger track record — years of operating private exclusives without material legislative interference — to a post-merger national scale that was categorically different in institutional visibility. That extrapolation was falsified within six weeks. The solvency imperative distorted the strategic calculus in a more structural way: under $2.6 billion in assumed debt with no path to GAAP profitability, private exclusives were not a strategic enhancement layered on a profitable core. They were the balance-sheet mechanism required to service quarterly debt obligations.

A firm that needs Layer 3 to remain solvent cannot price the regulatory risk of losing it accurately, because accurate pricing would require acknowledging that the acquisition is not viable at the terms being negotiated. The forum separation assumption completed the architecture: the cross-forum contradiction was only sustainable as long as federal courts, state legislatures, investors, and congressional inquiries remained separated — each seeing a different narrative slice without a single institutional venue forcing simultaneous accountability. The Warren letter was the first forum to break that separation. Compass’s decision architecture assumed the separation would hold long enough for Layer 3 to generate the returns required to justify the premium. The 42-day collapse suggests the separation was always more fragile than the acquisition model required.

VII-E. The Unacquirable Premium

Layer 3 was not acquirable at any price that required it to survive. The mechanism’s value derived entirely from its ability to route premium inventory through internal networks before open market exposure. Deploying that mechanism at national scale — across 35 major markets, with 340,000 agents, under the institutional visibility a $1.6 billion acquisition creates — generated the legislative coordination, federal judicial scrutiny, and congressional attention that closed the window the mechanism required. The acquisition premium and the acquisition risk were not separable. Acquiring the premium activated the risk. The larger the premium, the more aggressively the mechanism needed to be deployed. The more aggressively the mechanism was deployed, the faster the enforcement vectors activated.

A smaller Compass, operating the private exclusive model in a handful of luxury markets without merger-scale institutional visibility, could sustain the forum separation the model required. The acquisition destroyed the condition that made the model viable by making it visible at the scale that justified a coordinated response.

That is what an unacquirable premium looks like under Chicago School analysis. Not a bad bet that happened to lose. A structural configuration in which acquiring the asset activated the forces that destroyed it — predictably, compoundingly, and without a recovery path that didn’t require repricing the transaction before it closed.

VIII. Conclusion

The 42-day collapse is not the story of a firm that made strategic errors after a reasonable acquisition. It is the story of a premium that was already liquidating itself on the day the merger closed — because the premium required a regulatory environment, and the merger announcement was the event that ended it.

What the eight-vector framework documents is not a series of institutional misfortunes arriving in unlucky sequence. Each vector was load-bearing before the merger closed. The congressional record existed because the merger made the antitrust clearance visible at national scale. The state legislative ratchet existed because the merger made the private exclusive mechanism visible at the scale that justifies coordinated response. The cross-forum contradiction existed because the federal court record and the state legislative defense were irreconcilable before a single senator voted. The cash constraint existed because the acquisition assumed the debt load that made professional advocacy unaffordable. The testimony strategy — Nelson signing in CON, Huff absorbing the cross-examination risk, no lobbyist, no retained counsel, no discoverable paper trail — was not a communications failure. It was the revealed preference of a legal team that had already concluded the narrative could not survive adversarial questioning.

None of these vectors required the others to activate in order to cause damage. All of them were drawing from the same evidentiary substrate simultaneously. That is what makes the current moment structurally different from anything Compass has previously navigated. A firm the size of the combined Compass-Anywhere entity can survive a federal antitrust case. It can survive a state legislative defeat. It can survive congressional scrutiny of a merger clearance decision. What it cannot survive — without structural recalibration that reprices the acquisition thesis entirely — is all of those things activating at once, feeding each other’s records, with each adverse development simultaneously strengthening multiple other attack surfaces.

The premium on private exclusives is liquidating in real time. The depositions have not yet begun.

MLS closing records on the seven active Team Foster listings will resolve the Layer 3 behavioral question by transaction close. AG Bondi’s congressional response resolves the institutional question by March 5. The analytical framework does not require either outcome to validate the structural argument above — but both outcomes will test it in real time, exactly as the foresight simulation methodology requires.