MCAI Lex Vision: Nineteen Senators, Seventeen Questions, How Compass Bought Its Antitrust Clearance

How the Warren Letter Activates the MindCast Antitrust Enforcement Prediction Architecture

See also Death by a Thousand Depositions, A Pre-Foresight Simulation of Compass’s Multi-Vector Regulatory Collapse and The Compass Commission Consolidation Strategy and Real Estate Marketing Transparency, The Compass-Anywhere Address Suppression Calculus.

On February 19, 2026, nineteen members of Congress — including Senators Warren, Schumer, Sanders, Klobuchar, and Wyden — sent a formal demand letter to Attorney General Pamela Bondi accusing the Department of Justice of corruption.

The subject was a merger. In September 2025, Compass, Inc. — the largest residential real estate brokerage in the country — announced a $1.6 billion acquisition of Anywhere Real Estate, the parent company of Coldwell Banker, Century 21, and Sotheby’s International Realty. The deal would create a single company controlling 340,000 agents and more than 20% of the national residential market. Federal antitrust law requires the DOJ to review transactions of this size before they close. The career staff who conducted that review concluded the merger warranted deeper investigation. That investigation never happened.

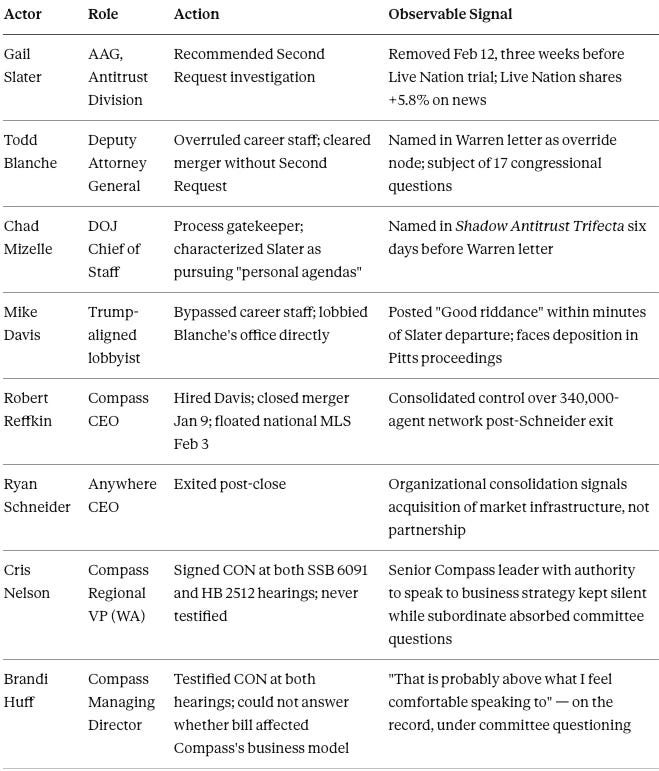

Instead, according to reporting by the Wall Street Journal, a Trump-aligned lobbyist named Mike Davis went over the heads of the career reviewers, directly to Deputy Attorney General Todd Blanche’s office. Blanche overruled the career staff. The merger closed January 9, 2026 — months ahead of schedule. The career official who had been pushing for the extended review, Antitrust Division chief Gail Slater, was removed from her position on February 12 — three weeks before she was scheduled to take the landmark Live Nation monopoly case to trial. Davis posted “Good riddance” on social media within minutes of her departure.

The senators want to know how that happened. Their letter demands written answers by March 5. It asks who communicated with Davis, what role Blanche played, why Slater was removed, and whether the DOJ’s merger review process has been corrupted.

This publication treats the letter not as political rhetoric but as an instrument panel. Each of its seventeen questions is a measurable test of whether federal antitrust enforcement can still function — or whether the institutions designed to protect American consumers from monopoly power have been captured by the interests they were built to regulate. Comparative Externality Costs in Antitrust Enforcement, A Nash–Stigler Foresight Study of Federal Enforcement Equilibria, Live Nation as Anchor, Compass–Anywhere as Validation (January 21, 2026). MindCast AI has been modeling and publishing on exactly this question since January 2026, building a prediction architecture that named the actors, mapped the mechanism, and forecast the outcomes before they became the subject of a Senate investigation.

Three prior MindCast AI publications supply the analytical foundation this instrument panel runs on. A Tirole Phase Analysis of Advocacy-Driven Antitrust Inaction at the U.S. Department of Justice (January 23, 2026) identified the terminal transition in which political access displaces evidentiary analysis as the determinant of enforcement outcomes — naming the mechanism, the actors, and the access channels before they became the subject of Senate investigation. The Geometry of Regulatory Capture at the U.S. Department of Justice Antitrust Division (January 24, 2026) established why the DOJ cannot self-correct from within a captured equilibrium — structural impossibility, not personnel failure. The Shadow Antitrust Trifecta (February 13, 2026) named Deputy AG Todd Blanche, DOJ Chief of Staff Chad Mizelle, and lobbyist Mike Davis by role six days before the Warren letter named them in a congressional demand to the Attorney General of the United States.

I. The Merger, the Bypass, and the Removal

The Warren letter cannot be read without understanding what it is responding to.

In September 2025, Compass, Inc. — the Wall Street-backed residential brokerage — announced a $1.6 billion all-stock acquisition of Anywhere Real Estate, the parent company of Coldwell Banker, Century 21, and Sotheby’s International Realty. The combined entity would control the largest agent network in the country: approximately 340,000 agents operating under a single corporate umbrella with 20%+ national residential market share and above 30% in multiple major metropolitan areas. Compass–Anywhere: When Scale Becomes Liability (January 9, 2026) modeled the full enforcement probability map on the day the merger closed — assigning 65-80% probability to formal federal inquiry within 24 months and 55-70% probability to coordinated multi-state AG action within 36 months. Compass’s Technology Trap (January 10, 2026) documented how Compass’s IPO narrative raised potential antitrust admissions.

Mergers of this scale trigger mandatory review under the Hart-Scott-Rodino Act. The DOJ’s Antitrust Division — career economists and attorneys whose function is to assess whether a transaction would substantially lessen competition — began its review. According to subsequent reporting by the Wall Street Journal, Antitrust Division chief Gail Slater concluded that the transaction warranted an extended investigation: a “Second Request” that would have required the parties to produce documents and data for rigorous competitive analysis before the merger could close.

That investigation never happened.

Compass had hired Mike Davis — a Trump-aligned lawyer and lobbyist with direct access to senior administration officials — to help secure merger approval. Davis did not engage with the career staff conducting the review. He went above them. According to the Wall Street Journal, Davis “helped Compass make its case to Blanche’s office” — the office of Deputy Attorney General Todd Blanche, the second-highest official in the Justice Department. Blanche’s office overruled Slater. The merger closed on January 9, 2026 — months ahead of the originally expected late 2026 timeline. MindCast AI’s Tirole Advocacy Arbitrage framework had identified this exact routing mechanism — private intermediary lobbying above career staff directly to front-office political appointees — as the defining feature of the current enforcement regime, published eleven days before the merger closed.

Anywhere CEO Ryan Schneider exited following the close, with Reffkin consolidating direct control over the combined 340,000-agent network — the organizational consequence of a merger that was framed publicly as a partnership but structured as an acquisition of market infrastructure. Real Estate News, January 16, 2026

Slater was removed from her position on February 12, 2026. This came three weeks before she was scheduled to take the landmark Live Nation antitrust case to trial — a case joined by 40 state attorneys general seeking to force the divestiture of Ticketmaster. Live Nation shares jumped 5.8% on news of her removal. Davis posted “Good riddance” on social media within minutes of her departure becoming public. DOJ Chief of Staff Chad Mizelle characterized her enforcement posture as reflecting “personal agendas and vendettas.” MindCast AI’s How MindCast AI Predicted the Slater Ouster Before the DOJ Executed It (February 12, 2026) documented nine of ten falsifiable predictions confirmed by the events of that day — including the specific prediction that boundary-asserting staff would be removed before structural reform could occur, published nineteen days earlier. The Warren letter confirms the tenth: congressional oversight materialized within the predicted escalation window.

Contact mcai@mindcast-ai.com to partner with us on Law and Behavioral Economics foresight simulations. To create a runtime simulator of issues in this publication, simply upload the URL into any LLM, and prompt ‘create framework with three degrees of cited sub links to MindCast works.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure for more info.

II. The Letter as a Congressional Discovery Proxy

Congress does not need subpoena power to alter enforcement equilibrium. A structured demand letter with a hard deadline creates a disclosure fork: answer substantively, answer partially, delay, or refuse. Each fork signals institutional update velocity and inquiry tolerance. Each fork is itself information.

The operative variable is not accusation. It is documentary production.

A formal demand letter to the Attorney General, signed by the Senate Minority Leader, the Ranking Member of the Senate Judiciary Committee, and fifteen additional members of Congress, generates a discoverable record independent of any pending litigation. Whatever DOJ produces — or declines to produce — by March 5 becomes part of the permanent institutional record available to every state attorney general, every federal court considering related matters, and every future oversight proceeding. MindCast AI’s State Power vs. Compass Private Exclusives (February 6, 2026) established the evidentiary-record-as-mechanism principle in the legislative context: a hearing is not merely words on a record but a new information surface that destabilizes the structural asymmetry permitting cross-forum contradictions to persist. The same principle applies here at the congressional level.

If documentary clarity emerges, enforcement credibility stabilizes. If opacity persists, the constraint migrates outward — to courts, to state legislatures, to multistate AG coalitions — where different sovereigns with different authorities begin extracting the same information under oath. Federal Inaction Has Elevated State Authority (January 17, 2026) documented this redistribution dynamic across antitrust, consumer protection, and real estate market integrity: when federal enforcement gaps are structural rather than episodic, state authority does not merely supplement federal action — it substitutes for it.

By February 20 — the day after the letter was sent — mainstream real estate industry press was running the story under the word “corruption.” Inman, February 20, 2026 The letter had broken out of the policy lane into the market lane within 24 hours. Every agent, broker, and real estate investor in the country now has a reason to understand what the merger actually did.

The letter does not need to produce a prosecution. It needs to produce a record.

III. The Seventeen Questions as a Falsification Board

The letter’s seventeen questions are not random. They are structured to eliminate the possibility of a coherent institutional defense regardless of how they are answered. MindCast AI’s Cognitive Digital Twin methodology treats each question as a falsification hook — an observable condition that either confirms or disconfirms a predicted institutional behavior. The questions cluster into four structural buckets.

1. Process Integrity and Override Chain

What the questions ask: When did the parties file? What did the Division find? Did the Division intend to issue a Second Request? Who made the decision not to? Why?

Why it matters: The Hart-Scott-Rodino process is designed to insulate merger review from political interference. The Antitrust Division’s career staff — economists and attorneys with no political appointment — conduct the substantive analysis. A Second Request is the Division’s primary instrument for obtaining the evidence needed to evaluate competitive harm. If the Division recommended one and was overridden, the override is the story.

Controlling insight: Enforcement equilibrium breaks when decision authority diverges from the analytic record. The MindCast Antitrust Regulatory Capture Geometry framework established that no survivable path from career-staff investigation to structural remedy exists once political override becomes standard operating procedure — because career staff learn that rigorous findings produce removal rather than enforcement. The escalation pattern documented across three cases makes the point: Slater’s senior deputies were removed over the HPE-Juniper settlement in July 2025; the AAG was bypassed in the Compass-Anywhere clearance in January 2026; the AAG herself was removed in February 2026. Each iteration went higher because the previous removal did not fully clear the resistance node. Shadow Antitrust Trifecta.

Forward implication: Full disclosure of the override chain stabilizes federal credibility by demonstrating that the exception was anomalous. Evasion or privilege claims signal that the override was systematic, which increases the probability of state-level intervention and judicial skepticism across all active antitrust matters including Live Nation, Google, Apple, and Netflix-Warner Bros. Discovery.

2. Access and Influence Channels

What the questions ask: Who communicated with Mike Davis? Did Davis or his representatives communicate with Blanche or anyone in his office? What were those communications? What safeguards exist to prevent outside advocates from bypassing career staff?

Why it matters: Mike Davis is not a government official. He holds no statutory authority over merger review. His influence over the Compass-Anywhere clearance — if the Wall Street Journal reporting is accurate — was purchased, not earned through legal process. The American Prospect reported Davis earned at least $1 million facilitating the clearance. The pattern is not unique to this transaction: Davis also advised HPE on the Juniper Networks merger, which settled over career staff objections eleven days before trial, and advised Live Nation on settlement negotiations conducted through Blanche’s office rather than the Antitrust Division. Judicial Process as Competitive Federalism (February 10, 2026) first documented the full scope of Davis’s multi-case involvement and its implications for the simultaneous constraint timelines now operative.

Controlling insight: When advocacy arbitrage dominates analytic scrutiny, competition shifts from markets to access. This is the terminal transition MindCast AI’s Tirole Advocacy Arbitrage framework identified: the marginal payoff of off-docket lobbying access relative to docketed adversarial advocacy now determines regulatory outcomes. The three actors named in the letter — Deputy AG Todd Blanche (front-office decision node), DOJ Chief of Staff Chad Mizelle (process gatekeeper), and Davis (access intermediary) — each occupy a distinct structural role in this routing architecture. Davis’s public claim that he recommended both Slater’s hiring and her firing, posted within minutes of her departure, is timestamped discoverable evidence the letter places directly into the congressional record.

Forward implication: Transparent disclosure of Davis-Blanche communications compresses arbitrage incentives by making the access channel visible and institutionally costly. Ambiguity or refusal expands those incentives — signaling that the channel remains open and that the cost of using it is lower than the cost of conventional antitrust process.

3. Substantive Competition Analysis

What the questions ask: Did the Division identify competition concerns? What were they? Did the Division intend to investigate further?

Why it matters: This is the core of the housing affordability argument. The Compass-Anywhere merger combined the two largest residential brokerages in the country at a moment when homeownership is already at crisis levels: first-time buyer share has fallen to a historic low of 21%, median buyer age has risen to 40, foreclosures are up 26%, and mortgage delinquencies are at a four-year high. The merged entity controls listing visibility, agent routing, and market timing across a network of 340,000 agents — the infrastructure through which most Americans encounter available homes for sale.

The housing harm the senators are describing starts with why Compass needed this merger — and what it was actually buying.

Compass operates a program called Private Exclusives: a 3-phase marketing system that withholds a home listing from the open Multiple Listing Service and from competing platforms during an initial period available only to Compass agents and buyers. The mechanism is straightforward. When a home is listed publicly on the MLS, any agent at any brokerage can bring a buyer. When a home is held as a Private Exclusive inside the Compass network, only Compass agents and their buyers see it — and when the deal closes, both the listing-side and buyer-side commission flow entirely to Compass. A transaction that would have produced one commission in an open market produces two commissions inside a closed one. At 5-6% of sale price on luxury inventory, the difference is material. See Compass’s Coasean Coordination Problem Part I, How Private Exclusives Reshape Competition and Threaten MLS Stability (December 10, 2026).

The private exclusive model works at scale. A single Compass office can run private exclusives, but the buyer pool is thin and the seller has limited negotiating leverage. What makes the model genuinely powerful — and genuinely threatening to market transparency — is national agent density. The more agents Compass controls, the larger the internal buyer pool it can route listings through before they ever reach the open market. The Anywhere acquisition was not primarily about brand consolidation or technology integration, despite how it was marketed to investors. It was about reaching the agent density threshold at which private exclusives stop being a niche offering and become a default intake channel for premium residential inventory across 35 major markets simultaneously.

The $400-800 million acquisition premium bought one thing: the regulatory permission to deploy private exclusives at national scale. Concurrent marketing requirements — laws like Washington State’s SSB 6091, which requires all listings to hit the public market simultaneously — eliminate that condition entirely. Each state that passes such a law closes a piece of the window the acquisition premium depends on. The Broker Incentives and Firm-Level Capture analysis (February 8, 2026) established the micro-mechanism: Compass converts individual broker indifference into firm-level commission capture through principal-agent divergence, requiring no coercion — only the structural unavailability of the counterfactual outcome that open-market competition would have produced.

The numbers from the ground make the national scaling logic concrete. MindCast AI’s Compass Private Exclusives Monopoly (February 19, 2026) analyzed 130 top-tier Seattle transactions over thirteen months: $167.5 million in transaction value, $4.2 million in captured buyer-side commission from a single metropolitan market’s monthly top-10 record alone. The $4.2 million is not the argument — it is the calibration. Scaled to 35 major markets, the same mechanism implies that $400-800 million of the acquisition premium exists only if one operating condition holds: that listings can be withheld from the open market long enough for an internal Compass buyer to arrive first. On February 19, 2026 — the same day the Warren letter was sent — a $79 million Lake Washington estate appeared on the Compass Team Foster website with full photographs, price, and specifications, and no address. Any buyer who wanted to know where it was had to call Compass first. Not a historical data point — the mechanism, operating in real time.

https://fosterrealty.com/properties/triptych

As examined in The Compass Commission Consolidation Strategy and Real Estate Marketing Transparency, What Seattle Region Ultra-Luxury Records Reveal About Price Discovery and Market (February 19, 2026), the Team Foster transaction record is the most direct evidence available to antitrust regulators assessing Compass's anticompetitive conduct — not because the team violated any rule, but because their NWMLS role designations document, in publicly verifiable form, the precise mechanism the private exclusive model is engineered to produce: dual representation, address suppression, and full commission internalization operating simultaneously in the same market, during the same legislative window in which Compass was defending the program before a state committee.

The transaction record does not require inference, projection, or scaling. It is the mechanism recorded by the MLS's own field designations, in a publicly accessible database, on closed transactions that cannot be revised or withdrawn. For antitrust regulators assessing whether the Anywhere acquisition created the conditions for anticompetitive commission capture at national scale, Team Foster's NWMLS record is the ground-level proof of concept the merger's critics predicted and the merger's architects depended upon.

Combined market share exceeding DOJ Merger Guidelines concentration thresholds in multiple high-volume metros — above 80% in Manhattan and Washington, D.C. according to industry concentration analyses — is the quantitative anchor the letter uses to convert the housing affordability argument from qualitative concern into a measurable enforcement gap. MindCast AI’s Nash-Stigler Externalities framework (January 21, 2026) quantified the five-year consumer and market externality load at $12.5-15 billion when federal enforcement terminates at procedural sufficiency rather than structural correction — the dollar figure underlying Warren’s housing cost claims.

What makes the housing harm argument legally potent — and what the Warren letter implicitly invokes without fully naming — is that Compass has already created a self-defeating evidentiary record across forums. In federal court, Compass argues that restricted listing visibility harms consumers and forecloses competition — the foundation of its antitrust lawsuits against Zillow in the Southern District of New York and against NWMLS in the Western District of Washington. Before state legislatures, Compass argues the opposite: that restricted visibility protects consumers through privacy and seller choice, and that bills like SSB 6091 threaten those protections. On its homeowner-facing website, Compass frames restricted visibility as protection from “organized real estate.” These three positions cannot coexist. A firm cannot simultaneously argue that withholding listings from the market injures consumers in one forum and benefits them in another without one set of claims being false.

The Compass Narrative Inversion Playbook (February 4, 2026) documented this cross-forum contradiction as a structural feature of Compass’s advocacy strategy — not an oversight but a necessity, because the business model requires different claims in different forums to survive scrutiny in any one of them. The legislative testimony record makes the design visible. At both the Senate and House hearings on SSB 6091, Compass sent Managing Director Brandi Huff and Compass Team Foster Managing Broker Michael Orbino to testify against the bill. When the Senate committee asked whether SSB 6091 would affect Compass’s business model, Huff answered: “That is probably above what I feel comfortable speaking to.” Cris Nelson — Compass’s Regional VP for Washington, the senior leader with actual authority to speak to business strategy — signed in CON at both hearings and never said a word.

Compass sent an employee without clearance to answer the one question that mattered, and kept the people with clearance off the record. The committee transcript documents this. The congressional record now compounds it: Huff’s non-answer and Nelson’s silence, are now part of the same evidentiary surface as the Davis-Blanche bypass and the Slater removal. See How Compass’s State Legislative Testimony Undermined its Federal Antitrust Claims (January 30, 2026).

The Playbook identified the one question that collapses the entire structure: “Do you stand by your federal complaint’s claim that restricted visibility harms consumers?” Asked in a state legislative hearing, it forces Compass to either abandon its federal antitrust theory or abandon its state legislative testimony. Asked in a congressional record, the same question carries an additional consequence — a false answer is perjury and a true one is an admission. The Warren letter is more than oversight theater: it closes the forum separation that has allowed Compass to maintain contradictory positions without consequence.

Then, on February 3, 2026 — three weeks after the merger closed — Compass CEO Robert Reffkin publicly floated the idea of replacing the country’s 500+ local MLS systems with a single national MLS, agent-owned and utility-like, with rules allowing “flexible marketing” including private exclusives. Inman, February 3, 2026 Industry executives noted the proposal with a mix of intrigue and alarm, citing antitrust risks and feasibility concerns. Inman, February 19, 2026 The analytical significance is not the feasibility of the proposal. It is the sequencing. Compass spent years arguing in federal court that existing MLS coordination rules restrict competition and harm consumers. Having acquired the scale to potentially dominate a national MLS, it is now proposing to build one — with rules it would write. The cross-forum contradiction documented in the Compass Narrative Inversion Playbook has advanced to its logical endpoint: the firm that sued to dismantle coordination infrastructure is now proposing to own it.

Forward implication: Detailed analytic memos showing the Division identified and evaluated concentration concerns validate procedural integrity — even if clearance was ultimately granted. Absent, thin, or withheld analysis raises the probability of state statutory correction and private class-action litigation, both of which MindCast AI assigned 45-65% probability within 18 months in its January 2026 merger liability forecast.

4. Institutional Safeguards Going Forward

What the questions ask: How does DOJ ensure similarly situated companies receive equal scrutiny? What steps is DOJ taking to protect smaller parties? What reforms are being implemented?

Why it matters: These questions are prospective, not retrospective. They test whether the Department can articulate a credible commitment to process integrity going forward — a commitment that will be monitored by the same nineteen signatories who signed this letter.

Controlling insight: Durable enforcement requires structural guardrails, not ad hoc discretion. The Geometry of Regulatory Capture framework established that institutions cannot self-correct from within a captured equilibrium — correction requires external constraint. These questions create that constraint: the Department must now either articulate reform commitments it will be held to, or acknowledge that no such commitments exist. The Assefi Test (February 13, 2026) framed the diagnostic precisely: does new acting leadership change the topology, or only the tone? The answer depends not on who occupies the AAG role but on whether routing authority — who controls the settlement channel — has actually changed.

Forward implication: Concrete reform commitments signal Phase Exit acceleration — the institution is acknowledging the capture and beginning to address it structurally. Procedural platitudes signal inertia and invite escalating oversight.

IV. The Constraint Collision: March 2 and March 5

Three deadlines now operate simultaneously, and each creates information the others can use.

March 2 — The Live Nation antitrust trial is scheduled to begin. This is the landmark case in which DOJ, joined by 40 state attorneys general, sought to force Live Nation to divest Ticketmaster, breaking up what the government alleged is an illegal monopoly over ticketing and live entertainment. Gail Slater was removed three weeks before this trial was set to begin. Acting AAG Omeed Assefi — installed by Bondi and Blanche after Slater’s departure — must decide whether to proceed with the structural case Slater was building or settle on terms that the Antitrust Division’s career staff had previously rejected. Live Nation’s 5.8% share price jump on news of Slater’s removal prices the market’s expectation. MindCast AI’s Assefi Test (February 13, 2026) established the diagnostic framework: the Live Nation trial window is the first observable test of whether the capture geometry has been altered or merely rebranded.

March 5 — Warren’s deadline for written responses from AG Bondi. Whatever DOJ produces enters the permanent congressional record. Whatever it declines to produce becomes its own signal.

Concurrent — U.S. District Judge Casey Pitts (N.D. Cal.) has authorized state attorneys general to depose Mike Davis, William Levi, and Arthur Schwartz under oath as part of the Tunney Act review of the DOJ’s HPE-Juniper settlement. The Tunney Act requires a federal court to find that a DOJ consent decree is in the public interest before it becomes final. In the HPE-Juniper case, state AGs argued that the settlement — reached over career staff objections, eleven days before trial, after Davis’s involvement — was not in the public interest. Judge Pitts agreed that sworn testimony from the access intermediaries was appropriate. Davis now faces deposition obligations in a parallel antitrust proceeding covering the same routing architecture the Warren letter is investigating. Judicial Process as Competitive Federalism (February 10, 2026) modeled this constraint collision nine days before it materialized: “Discovery has become contemporaneous with advocacy. Advisors shaping antitrust outcomes now face sworn testimony obligations in parallel proceedings.”

Courts demand evidence under oath. Congress demands explanation under record. States monitor both. Simultaneity changes incentives: silence becomes information, delay becomes signal, partial compliance becomes data.

If federal disclosure aligns with judicial transparency, enforcement equilibrium stabilizes. If congressional inquiry meets opacity while courts extract aggressively, competitive federalism intensifies and state attorneys general inherit the enforcement constraint role that the federal government has vacated.

V. Phase Exit Completion vs. Phase-Lock Continuation

The MindCast AI Tirole framework — which models enforcement regimes as stable equilibrium states that resist change until external pressure exceeds a structural threshold — identifies two possible paths from the current moment.

Phase Exit is the transition out of Advocacy Arbitrage Phase-Lock: the captured equilibrium in which enforcement outcomes are determined by political access rather than evidentiary analysis, structural remedies are unreachable, and the system cannot self-correct from within. Phase Exit does not require criminal prosecution or political accountability. It requires institutional visibility — the conditions under which the capture architecture becomes too costly to maintain.

Phase-Lock Continuation is the alternative: the capture geometry becomes self-reinforcing, career staff learn to self-censor or exit, and settlements take compliance-monitor form that ratifies monopoly market structure as official enforcement output. How MindCast AI Predicted the Slater Ouster documented this dynamic: “Each element reinforces the others. No traversable path from investigation to structural remedy remains.”

Phase Exit Completion Markers

Production of internal review memoranda and documented decision chains in response to Warren’s March 5 deadline.

Explicit acknowledgment of the analytic thresholds — market share, concentration ratios, competitive effects — used in the Compass-Anywhere clearance decision.

Continuation of the Live Nation trial on March 2 without pre-trial settlement, demonstrating that acting leadership has maintained at least the procedural independence Slater’s removal was designed to eliminate.

Coordinated state-federal signaling reinforcing transparency norms — state AG action that references and builds on the congressional record being created.

Completion does not require fault. It requires clarity.

Phase-Lock Continuation Markers

Procedural opacity or privilege shields — deliberative process privilege, executive privilege — invoked without substantive explanation across the seventeen questions.

Delayed or non-responsive communication past the March 5 deadline, forcing the senators to escalate to subpoena or contempt proceedings.

Live Nation settlement announced before March 2, removing the most visible enforcement test and signaling that the access channel remains operative.

Davis’s deposition in the Pitts proceedings quashed or indefinitely delayed, severing the judicial discovery thread before sworn testimony can be extracted.

SSB 6091 stalled in the House — the House Rules Committee declines to schedule the bill for a floor vote, achieving through calendar management what Compass’s lobbying operation failed to achieve through amendment. SSB 6091 Cross-Forum Analysis (February 10, 2026).

Continuation preserves short-term institutional stability at the cost of long-term enforcement credibility.

VI. The Damage Assessment: Five Vectors

The February 19, 2026 Warren letter does not operate on a single dimension. Its consequences for Compass run across eight distinct vectors — each with its own timeline, severity, and compounding relationship to the others. No single vector is fatal in isolation. The combination is what makes the current moment structurally different from anything Compass has faced since its founding. The merger closed 42 days ago. Every enforcement vector activated within that window.

📊 Profit Outlook Deterioration — Severe, Accelerating On January 9, 2026, the profit thesis for the Anywhere acquisition was straightforward: 340,000 agents at national scale, $225 million in projected cost synergies, $1 billion in high-margin franchise revenue, and a private exclusive window that would route premium inventory through Compass’s internal network before open market exposure — capturing both commission sides on transactions that would otherwise split with a cooperating broker. The Zillow antitrust trial, scheduled for July 2026, was the primary legal risk, and even that carried a plausible defense. Six weeks later, the landscape has changed on every dimension simultaneously. SSB 6091 passed the Washington State Senate 49-0, closing the private exclusive window in the state that generated $4.2 million in captured commission from a single metro’s monthly record. Wisconsin and Illinois are advancing concurrent marketing requirements. The Southern District of New York denied Compass’s preliminary injunction against Zillow, rejecting the entire antitrust theory on its merits. Nineteen senators have formally accused the DOJ of corruption in clearing the merger. COMP dropped 3.2% in a single day on the letter’s publication. The regulatory assumption that justified $400-800 million of the acquisition premium — that private exclusives could be deployed at national scale without interference — has been challenged in federal court, rejected in state court, legislated against in multiple states, and made the subject of a congressional corruption inquiry, all within 42 days of the merger closing.

💸 Cash Constraint — Severe, Self-Reinforcing Compass entered the Washington State legislative fight carrying nearly $3 billion in post-merger debt, $127 million in cash on hand after burning $105 million on the Christie’s acquisition alone, and over $1.5 billion in cumulative operating losses across four years. The firm has never posted a full-year GAAP profit. Mike Davis cost at least $1 million for the federal bypass. Zillow, NWMLS, and NAR litigation run concurrently, each carrying ongoing legal spend. Against that balance sheet, the SSB 6091 opposition looks less like a funded professional advocacy campaign and more like a company sending employees it already pays — Brandi Huff to testify, Cris Nelson and Michael Orbino to sign in CON and stay silent (Cris was present in Olympia) — because retaining outside counsel and a professional lobbying shop was not an available line item. LPT International CEO Michael Valdes observed after the merger close: “I don’t see a clear path to a retirement of this debt within a concise period of time. With that, there comes a lack of agility.” The SSB 6091 result confirms the diagnosis. The result speaks for itself: 49-0 in the Washington State Senate.

📋 Internal Contradiction — Severe, Permanently Documented The strategic contradiction at the core of the acquisition predates the merger close and cannot be retroactively resolved. Anywhere CEO Ryan Schneider publicly called the private listings approach “short-sighted” and “not our recommendation” on Anywhere’s February 2025 earnings call — while simultaneously telling investors Anywhere was prepared to deploy private listings at scale if competitors forced the market that direction. Coldwell Banker CEO Kamini Lane wrote that “private listings ignore the law of supply and demand.” Alex Vidal, president of Anywhere’s ERA Real Estate, told Inman in July 2025 that private listing network talk simply didn’t exist “in the field.” Taken together, the Anywhere leadership ecosystem expressed consistent skepticism about the strategic foundation of the mechanism the acquisition was built around — on the record, in investor calls, in published op-eds, and in trade press interviews. Compass acquired that skepticism along with the agents and brands. Every statement is timestamped, published, and available to every auditor, plaintiff, and state AG evaluating the goodwill assumptions recorded at close. Real Estate News, February 13, 2025 | Inman, September 25, 2025

🔁 Cross-Forum Contradiction — Severe, Irresolvable The vector Compass cannot fix. Narrative driven strategies cannot overcome cross-forum pattern recognition of contradictions, where forum specific rhetorical framings collapse on each other. The firm is on record in federal court arguing that restricted listing visibility harms consumers and forecloses competition — the foundation of its antitrust suits against Zillow in the Southern District of New York and against NWMLS in the Western District of Washington. Before state legislatures, Compass argues the opposite: that restricted visibility protects consumers through privacy and seller choice. On its homeowner-facing website, Compass frames the same restriction as protection from “organized real estate.” Three positions, three forums, zero compatibility. The congressional record now forces simultaneous accounting across all three for the first time — a false answer is perjury, a true one is an admission. Reffkin’s February 3 national MLS proposal compounded the exposure permanently: the firm that spent years in federal court arguing that MLS coordination rules harm competition is now proposing to build a national MLS it would control, with “flexible marketing” rules it would write. The firm that sued to dismantle coordination infrastructure is now proposing to own it. That sequencing is in the congressional record, in the Inman archive, and in the federal court docket simultaneously. No forum separation remains.

⚖️ Legal Exposure — High, Multiplying The congressional record under construction is the most operationally dangerous instrument because it is available to every other enforcement vector simultaneously. Every answer AG Bondi provides by March 5 — or declines to provide — becomes part of the permanent institutional record accessible to private plaintiffs, state attorneys general, and every federal court handling Compass-related antitrust matters. The Pitts deposition of Mike Davis, William Levi, and Arthur Schwartz under oath in the HPE-Juniper Tunney Act proceedings runs concurrently, covering the same routing architecture the Warren letter investigates. If Davis’s sworn deposition testimony contradicts anything in DOJ’s congressional response, the gap is a perjury exposure that neither Compass nor Davis controls and neither can retract. The Zillow federal antitrust trial is scheduled for July 2026 in the Southern District of New York. The NWMLS case runs in the Western District of Washington. The NAR settlement created ongoing compliance obligations. Each proceeding draws from the same factual record the congressional inquiry is now expanding under oath.

📉 Goodwill Impairment — Medium-High, Accelerating The $400-800 million acquisition premium rested on a specific regulatory assumption: that private exclusives could be deployed at national scale across 35 major markets without legislative or judicial interference. Auditors testing that assumption for the next annual impairment review now face a materially different regulatory environment than existed at close. Wisconsin enacted listing transparency restrictions in December 2025. Illinois reintroduced its bill in February 2026. Washington passed SSB 6091 49-0. The Southern District of New York rejected Compass’s preliminary injunction against Zillow on the merits. Nineteen senators signed a formal corruption inquiry naming the merger mechanism. COMP dropped 3.2% the day the Warren letter became public — the market assigning probability within 24 hours to a scenario in which the regulatory assumptions underlying the acquisition premium do not hold. One state enactment does not trigger impairment review. A coordinated multi-state legislative ratchet combined with a congressional investigation of the merger’s regulatory clearance is a different category of risk entirely. The question is not whether goodwill impairment becomes relevant — it is when the cumulative divergence between the acquisition assumption and regulatory reality becomes too large for the annual test to absorb.

🏛️ State Legislative Ratchet — High, Self-Executing SSB 6091 passed the Washington State Senate 49-0 on February 10 — bipartisan, zero amendments, zero opt-outs, zero absences. Compass’s lobbying operation had eleven days between committee passage and the floor vote to find a single sympathetic senator willing to insert the twelve-word exception that would have preserved the private exclusive model in Washington. None emerged. The “seller choice” and “privacy protection” narrative achieved zero persuasive traction across the entire chamber — not among Democrats, not among Republicans, not among rural members, not among urban ones. Wisconsin enacted concurrent marketing restrictions in December 2025. Illinois reintroduced its bill in February 2026. Each state that enacts a concurrent marketing requirement closes a piece of the private exclusive window independently of any federal action. The ratchet is self-executing: it does not require DOJ cooperation, congressional authorization, or judicial approval. Under $2.5 billion in merger debt with quarterly debt-service obligations compressing the profit horizon, private exclusives are not a strategic preference — they are a balance-sheet necessity. Each state that closes the window tightens the financial constraint the merger itself created.

📢 Public Trust and Reputational — Medium, Compounding The word “corruption” appeared in mainstream real estate industry press within 24 hours of the letter’s publication. Inman, February 20, 2026 340,000 agents now operate under a company whose merger clearance is under active congressional investigation. Seller confidence, buyer confidence, and agent retention are all lagging indicators — they do not move immediately on a single news cycle. But the reputational vector compounds with each proceeding. Every deposition excerpt, every congressional non-response, every state legislative defeat adds another data point to the public record that agents, sellers, and institutional partners must evaluate. Compass-dominant markets — Manhattan, Washington D.C., Seattle — are exactly the markets where sophisticated sellers and high-net-worth buyers have the most alternatives. The reputational damage is recoverable if the legal vectors resolve favorably. The legal vectors will not all resolve favorably. There are too many simultaneous proceedings with too many different sovereigns extracting the same information under oath.

Overall: Compass’s worst-case scenario is not a single prosecution, a single adverse verdict, or a single legislative defeat. Each of those is survivable in isolation. The structural danger is simultaneity: eight vectors activating within 42 days of merger close, each feeding the evidentiary record the others draw from, none requiring the others to succeed in order to cause damage. The congressional record becomes the goodwill impairment trigger. The state ratchet becomes the profit deterioration mechanism. The internal contradiction becomes the cross-forum perjury trap. The cash constraint explains why the advocacy operation failed. Every vector is connected. None can be resolved without implicating the others. Death by a thousand depositions is not a metaphor. It is the operational description of what happens next.

VII. The Forward Lock

By mid-April 2026, one of two paths will be observable. Either documentary clarity compresses speculation and reinforces federal enforcement credibility, or opacity redistributes constraint power to states and courts — institutions with different authorities, different timelines, and no obligation to reach the same conclusions federal agencies declined to reach.

A bill that passed the Washington State Senate 49-0 — with bipartisan sponsorship, zero amendments, zero opt-outs, zero absences — does not fail on the merits. It either advances to a floor vote, or it dies on a calendar. Those are the only two paths. The analytical record documenting why this bill passed unanimously is now the same record a congressional investigation is using to question whether the merger it targets received lawful antitrust clearance. The legislative and federal enforcement timelines have converged.

While the federal system decides whether to self-correct, the state enforcement path is already active — and already dismantling the merger’s core economic assumptions without waiting for Washington to act.

Washington’s SSB 6091 passed 49-0 on February 10 — the same week the Southern District of New York denied Compass’s motion for a preliminary injunction against Zillow, rejecting every element of Compass’s antitrust theory on its merits. SSB 6091 Cross-Forum Analysis documented the convergence: two institutional forums, same week, same structural conclusion. The 49-0 vote deserves more weight than summary statistics alone convey. A unanimous bipartisan vote on legislation that directly threatens a major corporation’s existing business model is not a procedural footnote — it is an institutional verdict. Eighteen senators co-sponsored the bill spanning Democratic and Republican caucuses. No senator filed an amendment. No senator introduced a seller opt-out provision. No senator was absent.

Compass’s lobbying operation had eleven days between committee passage and floor vote to find a single sympathetic senator willing to insert the twelve-word exception that would have preserved the private exclusive model. None emerged. The “seller choice” and “privacy protection” narrative that Compass deployed in testimony achieved zero persuasive traction across the entire Washington State Senate — not among Democrats, not among Republicans, not among rural members, not among urban ones. Wisconsin enacted listing transparency restrictions in December 2025. Illinois reintroduced its bill in February 2026. Each state that enacts a concurrent marketing requirement closes a piece of the private exclusive window that justifies $400-800 million of the acquisition premium — dismantling, state by state, the regulatory assumption underlying the transaction’s valuation.

SSB 6091 now sits with the House Rules Committee — the single procedural gate between a unanimous Senate vote and a House floor decision. The committee that schedules it clean closes the legislative ratchet that the Senate set in motion without a single dissent. The committee that delays it hands Compass the calendar death that its lobbying operation failed to achieve through amendment.

The contrast with Windermere sharpens the picture of why that valuation assumption was precarious from the start. Windermere Real Estate holds approximately 25% statewide market share in Washington and 35% dominance in the luxury segment — a position from which private exclusives would be immediately profitable. Windermere’s own leadership acknowledged this at the January 23 Senate Housing Committee hearing: the firm would “clean house” if private exclusives were permitted at scale. Windermere rejected that path anyway. Windermere and Compass: Two Philosophies of Real Estate (January 25, 2026) established why: Windermere’s firm value is tied to market integrity over a long time horizon, and defection from cooperative infrastructure would destroy the trust-based coordination that sustains its transaction volume. A Nash-stable strategy — but only available to a firm with patient capital and no debt-service pressure. Compass does not have that option.

The Anywhere acquisition added $2.5 billion in corporate debt to Compass’s balance sheet. Quarterly debt-service obligations have compressed the firm’s profit horizon from the long-run venture-capital timeframe of its pre-IPO expansion to the near-term financial reporting cycle of a public company servicing leveraged acquisition debt. Under those conditions, private exclusives are not a strategic preference — they are a balance-sheet necessity. The merger created the debt. The debt requires the dual commissions. The dual commissions require the private exclusive window to stay open. Each state that closes that window tightens the financial constraint the merger itself created.

The Securities Law Dimension: Goodwill Impairment

That financial constraint has a securities-law dimension that has not yet received the attention it warrants. Acquisition goodwill — the premium above book value that Compass paid for Anywhere — must be tested annually against the assumptions used to justify it. The $400-800 million premium rested on a specific regulatory assumption: that private exclusives could be deployed at national scale across 35 major markets without legislative or judicial interference. Wisconsin, Illinois, and Washington represent the leading edge of a divergence between that assumption and emerging regulatory reality.

A formal congressional corruption inquiry naming the merger mechanism — signed by nineteen members of Congress including the Senate Minority Leader — is not background political noise. It is a material event that Compass’s auditors, investors, and legal counsel must now evaluate against the goodwill assumptions recorded at close. The market has already begun pricing this risk. Compass shares (COMP) fell 3.2% midday on February 20, 2026 — the day after the Warren letter was made public — as investors processed the possibility of post-merger investigations or remedies. Seeking Alpha, February 20, 2026 A single-day stock move is not a goodwill impairment trigger. But it is the market assigning probability to a scenario in which the regulatory assumptions underlying the acquisition premium do not hold.

One state enactment does not trigger impairment review. A coordinated multi-state legislative ratchet combined with a congressional investigation of the merger’s regulatory clearance is a different category of risk entirely. The question is not whether goodwill impairment becomes relevant — it is when the cumulative divergence between the acquisition assumption and regulatory reality becomes too large for the annual impairment test to absorb.

The congressional path creates the evidentiary infrastructure that all other enforcement vectors can use. A sworn response from the Attorney General documenting the merger review process — or a refusal to provide one — is available to every state AG, every private plaintiff, every court reviewing related antitrust matters. From Open Market to Private Governance (December 31, 2025) identified this dynamic in the pre-consummation period: “The doctrinal gap is not a failure of enforcement will but a limitation of analytical tools. Regulators cannot act on harms they lack frameworks to identify.” The congressional record being built through seventeen questions supplies those frameworks with a new evidentiary surface.

Phase Exit does not declare guilt. The measure is whether enforcement institutions can withstand simultaneous scrutiny without deflection. The letter does not complete the transition.

It activates it.

The model is now live.

VII. Simulation Trigger and Update Protocol

This publication is not the foresight simulation. It is the baseline state vector.

The Warren letter supplies the measurement instrument. March 2 and March 5 supply the calibration events.

The Phase Exit architecture now contains three live variables:

DOJ documentary production in response to the March 5 deadline — substantive disclosure, partial response, privilege invocation, or non-compliance.

Live Nation trial posture beginning March 2 — structural prosecution, pre-trial settlement, or continuance.

State legislative ratchet acceleration — Washington SSB 6091 House Rules Committee scheduling and floor vote outcome, Illinois bill trajectory, and any new state introductions during the same window.

Each variable produces an observable update. Each update modifies the Cognitive Digital Twin of federal enforcement behavior.

The formal foresight simulation will run at the first of two triggers:

Trigger A: DOJ produces substantive documentary disclosure or invokes privilege on or before March 5.

Trigger B: Live Nation proceeds to trial or settles before evidence presentation.

At that point, MindCast AI will assign conditional probabilities to:

Coordinated multi-state AG action within 12 months

Congressional subpoena escalation beyond the March 5 deadline

Goodwill impairment risk threshold activation

Private exclusives revenue contraction under state transparency statutes

Phase Exit completion versus Phase-Lock continuation

The purpose of this publication is structural stabilization. The purpose of the forthcoming simulation is forward probability assignment.

The simulation will not speculate. It will update.