⚽ MCAI Market Vision: Susquehanna Is Building the Institutional Market the CFTC Does Not Require — but Still Needs

The $500 Million World Cup Offer Cannot Create Jurisdiction or Prove Demand, but It Can Supply the Commercial Record Behind the CFTC's Public-Interest Defense

Related works: The World Cup Is the First Mass-Market Stress Test for Prediction Markets | How the CFTC’s Missing “Gaming” Definition Is Losing the Kalshi Prediction-Market Preemption War | Prediction Markets and the Dual Nash-Stigler Trap — Kalshi, the CFTC, and the Prediction-Market Harm Clearinghouse | Defining “Gaming” Under the Commodity Exchange Act, The Rule 40.11 Gap Driving the Nationwide Kalshi Litigation Web | MindCast Files Second Comment in the CFTC Prediction Markets Rulemaking — Same Day the Proposal Drops

I. Executive Summary

Thesis: Susquehanna’s World Cup hedging offer builds a record the Commodity Futures Trading Commission (CFTC)does not legally require but politically needs.

Before 2000, the CFTC applied an economic-purpose test when determining whether futures contracts satisfied the statutory public-interest requirement. The 2000 Commodity Futures Modernization Act removed that test, and Dodd-Frank never restored it. A sports event contract can now clear the Commission’s public-interest inquiry without demonstrating any hedging function.

Susquehanna is not repairing the doctrine behind CFTC jurisdiction, because the Commission already claims exclusive jurisdiction on statutory grounds and does not base that claim on economic purpose. Susquehanna is supplying the concrete institutional example that makes the Commission’s permissive treatment easier to defend before courts, Congress, and a skeptical public.

One distinction runs through every section. An offer of capacity is not proof of demand. Susquehanna has built the offer side of a possible institutional market, and until a named counterparty executes a disclosed hedge, the demand side stays invisible and the facility works as legitimacy support rather than as evidence of a real market.

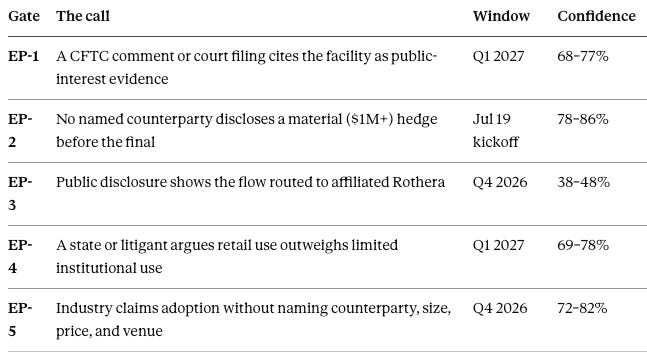

The forecast in brief, five falsifiable calls scored in a pre-resolution robustness audit:

Section II states the calls in full. The analysis that follows explains each one.

II. The Five Calls

MindCast lists forecasts the way an exchange lists contracts, each with a dated window and a falsifier. Three tools generate and score them: Dynamic Predictive Game Theory for the sequencing and best-response structure of the regulatory game, Behavioral Economics for the retail-versus-institutional composition of the market, and the MindCast AI Proprietary Cognitive Digital Twin Foresight Simulation (MP CDT FS) engine for the pre-resolution robustness audit that set the bands. The five gates below are tightly observable.

Two pairs share causal ground and should not be read as independent confirmations. EP-1 and EP-4 draw on the same comment-and-litigation record. EP-2 and EP-3 both turn on corporate disclosure behavior, and can move in opposite directions as that behavior shifts.

EP-1, the commercial-use record. At least one CFTC comment on Regulation Identifier Number (RIN)3038-AF65, or one court filing in a prediction-market federal-preemption or Rule 40.11 docket (the Fourth Circuit, Massachusetts Supreme Judicial Court, or Kaiserman v. Kalshi among them), cites Susquehanna’s hedging capacity as favorable public-interest evidence under § 40.11(a)(5). Falsifier: no qualifying citation by the end of Q1 2027. Window: through Q1 2027. Band: 68–77%.

EP-2, capacity versus demand. No named counterparty publicly discloses a material World Cup hedge, at least $1 million notional, through the facility before kickoff of the July 19 final. Nondisclosure proves only the absence of public validation, not the absence of private demand. Falsifier: a named sponsor, broadcaster, or brand discloses a $1 million-plus hedge through the facility before kickoff. Window: through kickoff of the July 19 final. Band: 78–86%.

EP-3, disclosed affiliated routing. Public disclosure shows the facility’s flow executing on Rothera or another Susquehanna-affiliated venue. The gate turns on disclosure, not underlying routing: affiliated routing may well occur yet never surface in a filing, which pulls the band down. Falsifier: disclosed routing to an unaffiliated venue, or no routing disclosed. Window: through Q4 2026. Band: 38–48%.

EP-4, the litigation argument. At least one state or private litigant argues that limited institutional use cannot outweigh predominantly recreational retail participation. The gate registers the argument’s appearance, not a court’s holding. Falsifier: no such argument appears in comments or filings by the end of Q1 2027. Window: through Q1 2027. Band: 69–78%.

EP-5, aggregate adoption without disclosure. Susquehanna, Rothera, Robinhood, or an industry participant characterizes the facility as evidence of institutional adoption without naming a counterparty, size, price, and venue together. Falsifier: every adoption claim supplies all four elements, or none appears. Window: through Q4 2026. Band: 72–82%.

Mechanism and pricing gates register in the separate quarterfinal Validation Report; the volume-cliff and dual-citation gates (P2, P4) stay live in the foundation register; the integrity and surveillance gates stay in the internal register.

III. The Test the CFTC Rejected

Read on its own terms, the June 10 proposal opens by dismantling an assumption most commentary still makes. Before 2000, the CFTC applied an economic-purpose test when deciding whether futures contracts met the statutory public-interest requirement. The 2000 Act removed that test, Dodd-Frank declined to revive it, and nothing in the proposed Rule 40.11 brings it back.

A sports contract can now clear the public-interest inquiry without any business ever hedging with it.

What the Commission kept is a weighing test, not a gate. The favorable side lists meaningful risk transfer, price discovery, commercially useful information, and responsible innovation. The unfavorable side lists manipulation risk, weak settlement integrity, and insider exposure.

The Commission then qualifies its own favorable factors in ways that decide this case. No single factor controls. Direct hedging use carries, in the proposal’s phrase, limited importance. A sports-contract price can serve an economic purpose even when no commercial party trades it. And properly designed professional and collegiate sports contracts already look unlikely to fail the public interest wherever an exchange keeps adequate integrity controls.

The proposal separates four ways a contract can carry economic value, and only one of them requires a hedger. Direct hedging use puts a real position on to offset a real exposure. Price discovery lets the market’s odds inform a decision. Information aggregation pools scattered knowledge into a single number. Commercial use of that number lets a business act on it without ever trading.

A hotel near a host stadium shows the difference. The hotel need not buy a single World Cup contract to use its price. A rising probability that the home team advances tells the hotel to raise room rates, add staff, and stock inventory for another week of demand. The contract’s price does economic work while the hotel stays out of the market entirely.

The distinction is why Susquehanna’s facility helps the Commission without being necessary to it. Institutional hedging strengthens the direct-use factor, the narrowest of the four, while the other three support the contracts on their own.

Permissive treatment of aggregate-outcome sports contracts therefore sits close to a baseline, not a prize an applicant must win with a hedging record.

The gap between what the rule requires and what the rule rewards is the entire opening. The Commission needs no commercial hedging to permit these contracts, yet it reaches for hedging, price discovery, and commercial usefulness again and again to justify permitting them.

A regulator still has to defend a permissive rule, before a Fourth Circuit panel, a state supreme court, a hostile congressional committee, and a wary public. Abstractions defend it less well than a concrete institutional example does. The favorable factors are legally non-controlling and politically load-bearing at the same time, and the difference between those two is the whole game.

The reading comes straight from the proposal’s text rather than from any inference: confidence 95–99%.

IV. Susquehanna Builds the Offer Side

Susquehanna’s announcement borrows the proposal’s commercial-risk vocabulary almost word for word, and the borrowing is the point.

The firm offered up to $500 million in capacity to help institutions hedge World Cup outcomes, naming exactly the clients the rule would smile on: sponsors, broadcasters, hospitality operators, and consumer brands whose promotions and rebates ride on which team advances. Line the announcement up against the favorable factors and the language matches, risk transfer, commercial utility, a legitimate hedging use.

An offer of capacity is not a market, though, and the distinction governs everything that follows. Susquehanna has built the offer side and nothing more. No public evidence names a deployed dollar, an executed hedge, a counterparty, a size, a price, or a venue.

What the facility can do is turn a regulatory abstraction into a citable commitment, a commercial fact pattern ready for the record the moment the permissive rule is challenged.

Timing carries the same double meaning. Capital announced inside the comment window, dressed in the language of the public-interest factors, reads as a fact pattern staged for the record, even as the approaching final gives Susquehanna an ordinary commercial reason to move now. The two motives coexist rather than compete: confidence the offer materially serves record-construction alongside commercial origination, 62–72%.

Contact mcai@mindcast-ai.com to partner with us on Predictive Game Theory AI in Law and Behavioral Economics. Our verticals include simulating complex litigation, innovation economics and geopolitical risks.

To deep dive on MindCast works upload the URL of this publication into any LLM (preferably Google AI mode) and prompt ‘reconstruct MindCast framework with three degrees of cited sub links.’ See Appendix A and Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure.

We stress-tested our AI system for this publication by simulating the Super Bowl and the World Cup.

V. How the Hedge Would Actually Work

A concrete example turns the abstraction into mechanics. Picture a consumer brand that promises customers a rebate if the national team it sponsors wins the World Cup. Each round the team survives raises the expected rebate the brand will owe.

The brand buys contracts that pay if the team reaches the triggering stage. A favorable run then moves two cash flows at once: the rebate liability climbs, and the contract payout climbs with it, so one offsets part of the other.

The offset is partial by design. The contract hedges the triggering event, not the full economic loss, and the size of the position sets how much of the liability it covers. A brand that buys too little stays exposed, and a brand that buys too much overshoots into a speculative position.

Basis risk lives in the gap between the contract’s settlement terms and the actual liability. A contract that pays on a semifinal berth does not match a rebate that triggers on the title, and closing that mismatch is the hedger’s job to size.

The choice between venues is a real tradeoff, not a foregone conclusion. An exchange offers standardized pricing and divisible exposure, so a treasurer can buy a precise notional in a liquid market. Insurance offers tailored coverage written closer to the actual loss, at the cost of liquidity and speed.

Susquehanna sits on the supply side of the exchange route. The firm supplies liquidity against the institutional order while the exchange lists and clears the position, which is why the announcement reads as capacity rather than as a placed trade.

The phrase itself measures room to transact, not money at work. “Up to $500 million” describes available transaction capacity, not executed volume and not reserved cash, so the figure sets a ceiling on what the facility could absorb rather than a floor under what it has done.

VI. Capacity Is Not Demand

Dynamic Predictive Game Theory treats the offer as a move in a repeated regulatory game, and a strategic claim in that game settles only when two conditions hold at once. The players’ behavior has to converge, the game-theoretic condition, and enough information has to exist to confirm the claim, the informational condition. MindCast’s framework names the joint requirement the Dual-Equilibrium Termination Architecture (DETA), taking the first from Nash and the second from Stigler.

Susquehanna’s offer meets neither cleanly, and the shortfall is the forecast.

Take the behavioral condition first. A public offer of execution capacity is a real, observable, reputationally costly signal, and a firm of Susquehanna’s size needs no segregated vault to make it credible. The announcement appears to represent fungible execution capacity rather than segregated capital, though the public record does not disclose the internal allocation.

The signal’s defensive value holds even if no hedge executes, because a citable commitment lends narrative support to the venues Susquehanna co-owns regardless of use. One firm moving, though, is not convergence. The Commission set the game by proposing the rule; Susquehanna merely moved first among market participants.

The informational condition stays open, and it does the real work. Enough evidence to confirm genuine demand does not yet exist: no disclosed counterparty, executed hedge, size, price, or venue. Capacity creates the test; only execution produces the evidence that passes it.

The offer moves through four states, and each one settles a different question. First, the offer is announced, which is where the record sits today. Second, a counterparty shows interest, which validates curiosity and nothing more. Third, a transaction executes, which validates private demand. Fourth, the transaction becomes publicly observable, which is the only state that validates the public legitimacy narrative.

The distance between the third state and the fourth is the whole forecast. A hedge can execute privately and never surface, so demand can be real while the public record stays empty.

The open layer is demand, not defensive value. The offer already works as legitimacy support, and only its weight as proof of genuine commercial use waits on execution.

Counterparty confidentiality, authorization lead times, and the short tournament window make public validation less likely than private execution. A pre-resolution MP CDT FS audit therefore raises the confidence that no named counterparty discloses a material hedge before kickoff of the July 19 final to 78–86%, with silence proving only the absence of public validation, not the absence of private demand.

VII. The Insurance Counterfactual

The clearest real case of sports-outcome hedging never touched a prediction market, and it sets the bar Susquehanna has to clear.

Club Atlético Osasuna paid €1.2 million for an insurance policy that would have returned €6 million on relegation, a bespoke bilateral contract written for a party with real exposure. Insurance and tailored bilateral deals already hedge sports outcomes for the entities that carry the risk, so institutional demand for this protection is not in question.

Whether an exchange-traded event contract is the efficient way to supply it is very much in question, and both sides of the comparison carry weight.

A bespoke policy can be illiquid, costly to structure, and difficult to transfer. An exchange-traded contract can offer standardized terms, transparent pricing, divisible exposure, and centralized clearing that reduces bilateral counterparty exposure. Whether it offers superior capital efficiency depends on the contract’s collateral and margin requirements.

The countervailing fact is behavioral, and equally real. The entities with genuine exposure already hedge through insurance and bilateral deals, while retail speculation appears to supply a substantial share of sports-contract activity, the market-composition signal Behavioral Economics tracks. The open question is whether the efficiency gain mainly serves hedgers or mainly lowers the friction on speculation.

Neither the proposed rule nor existing doctrine forces that showing as a legal matter, yet the answer sets how persuasive the institutional-use story becomes. A litigant will likely press the comparison, arguing that institutional hedgers already have insurance and bespoke markets: confidence that argument appears in comments or filings by Q1 2027, 68–78%.

VIII. The Legitimacy Game

Susquehanna’s offer plays in a legitimacy game, not a jurisdiction game, and separating the two dissolves the strongest temptation in the analysis. Two paths run side by side, and the offer touches only one.

The Legal Path

Economic use does not move classification. A sponsor’s hedge does not turn a touchdown-total contract into a derivative, and it does not push a sports contract into exclusive federal jurisdiction.

Contract structure, statutory definitions, registration status, and the reach of federal preemption decide those questions, and a $500 million offer touches none of them. The legal path runs on statute and precedent, and no commercial fact pattern reroutes it.

The Legitimacy Path

What the offer touches is defensibility, the record the Commission leans on when courts, Congress, and the public ask why sports contracts should list freely.

Three players move together, and the offer resequences all of them. The Commission, defending a rule now that Loper Bright has ended mandatory Chevron deference, gains a concrete example where it once had only abstraction. A well-developed administrative record can still support the rule as reasoned agency decision-making under arbitrary-and-capricious review, and courts may credit that reasoning under Skidmore even without any institution publicly disclosing a trade, so the fact pattern strengthens the political defense rather than supplying a missing legal element.

The platforms, whose growth products draw heavy retail speculation, gain an institutional-use story that softens the gambling-site framing. Susquehanna, first to move, converts capacity into standing in the record before any rival can.

The system keeps settling into the same split, contests to the states and consequences to the CFTC. The offer is a legitimacy bid on the federal side of that line, not a lever that moves the line.

The Vertical-Integration Question

Susquehanna’s own shape raises the sharper question. Firms like Susquehanna, Jane Street, and Citadel have priced these events for years, but privately, for their own books, making no public claim, what MindCast’s field map calls proprietary probability engines.

Susquehanna now occupies several layers of a public exchange at once: market maker on Kalshi, co-owner of Rothera through its joint venture with Robinhood, and potential originator of the very institutional flow the facility promises. The same offer that dresses retail speculation in institutional-risk vocabulary also lends legitimacy support to the venues Susquehanna co-owns.

The footprint creates a real conflict-management question about affiliated routing and captive liquidity. The footprint does not establish self-dealing, and the honest reading says so: confidence the affiliated-venue question surfaces in commentary or filings by Q4 2026, 55–65%.

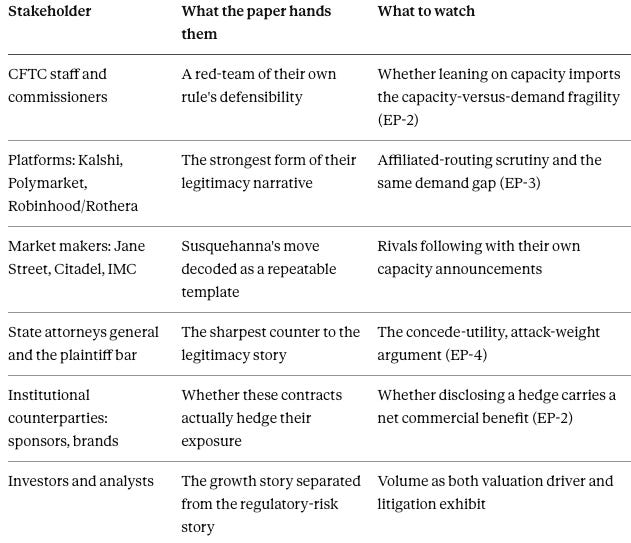

IX. What the Paper Means for Each Stakeholder

Susquehanna built one object that every actor can translate into its own language. The Commission sees commercial utility it can cite. The platforms see institutional maturation. The states see a thin institutional layer resting on a much larger base of retail speculation. The counterparties see one more risk-transfer tool to price against insurance. And Susquehanna sees liquidity, influence over the record, and optionality across the venues it touches.

Susquehanna built one object that every actor can translate into its own language. The Commission sees commercial utility it can cite. The platforms see institutional maturation. The states see a thin institutional layer resting on a much larger base of retail speculation. The counterparties see one more risk-transfer tool to price against insurance. And Susquehanna sees liquidity, influence over the record, and optionality across the venues it touches.

Each reading is internally consistent, which is what makes the offer effective. One disclosed, material, executed hedge would convert the offer from a fact pattern into shared evidence. Continued silence leaves each camp holding its own interpretation and the central claim unproven.

X. Conclusion

Susquehanna cannot manufacture jurisdiction by offering hedging capacity, and it has not tried to. The Commission already claims exclusive jurisdiction over these contracts on statutory grounds, so institutional hedging does not change the statutory classification analysis or independently resolve who governs them.

What the offer changes is the quality of the Commission’s public explanation. A regulator defending free-listed sports contracts argues from firmer ground with a concrete institutional example than with favorable-factor abstractions alone. The favorable factors are legally non-controlling and politically load-bearing at once, and Susquehanna has offered institutional support for that load.

Value here resolves on execution, not announcement. Capacity creates the test the institutional-use story must pass; executed, disclosed, material hedging would close that gap, though the Commission can still defend sports contracts on other public-interest factors.

Until execution arrives, the record holds an observable offer rather than an observable market, and the distance between the two is where the legitimacy contest plays out.

Appendix A: MindCast AI Works

The CFTC NPRM Is a Litigation Brief. The reading of the June 10 rulemaking behind Section III: the rejected economic-purpose test, the non-controlling favorable factors, and the treatment of properly designed sports contracts.

The Full Arc of Prediction Markets. The field map behind Section VIII, which classifies firms like Susquehanna as proprietary probability engines and frames the affiliated-routing conflict without overclaiming self-dealing.

The Dual Nash-Stigler Equilibrium Architecture. The closure logic behind Section VI: a claim settles only when behavioral convergence and informational sufficiency hold together.

How MindCast Evolves the Structural Gaps in Classical Nash Game Theory. The game-theoretic frame for the sequencing advantage the offer exploits.

The CFTC’s Undefined Category. The companion on the classification-jurisdiction axis, scoring the July 7 New York ruling.

The World Cup Is the First Mass-Market Stress Test for Prediction Markets. The foundation piece supplying the four-engine framework and the P2 and P4 gates this register inherits.

Defining “Gaming” Under the Commodity Exchange Act: A Rule 40.11 Framework. MindCast’s April 17 comment on RIN 3038-AF65.

MindCast AI Comment on the Prediction Markets NPRM. MindCast’s June 10 comment on the same docket.

Appendix B: Primary and External Sources

Susquehanna Announces World Cup Hedging Capacity of Up to $500 Million. BusinessWire, July 8, 2026. Establishes the offer as up to $500 million in capacity, the offer side, not deployed capital.

CFTC Notice of Proposed Rulemaking, “Prediction Markets; Public Interest Determinations,” RIN 3038-AF65. Published June 10, 2026; comments due July 27, 2026; Press Release 9249-26.

Osasuna, Clarification on the Contracting of Relegation Coverage. The €1.2M/€6M relegation insurance policy behind Section VII.

Robinhood–Susquehanna Prediction Markets Joint Venture. The ownership behind Rothera and the affiliated-routing question in Section VIII.

Bloomberg via Yahoo Finance, “Susquehanna Puts Up $500 Million for ‘Hedging’ World Cup Games” (Bernard Goyder), July 8, 2026. Ric Best’s named risk categories and the Osasuna detail.