MCAI Economics Vision: Prediction Markets and the Dual Nash-Stigler Trap — Kalshi, the CFTC, and the Prediction-Market Harm Clearinghouse

National Prediction Market Litigation Architecture: Why No Actor Can Settle the Prediction Market War and the $1–2 Billion a Year Price of CFTC Boundary Ambiguity

MindCast's National Prediction Market Litigation Architecture (NPMLA) series tracks the prediction-market legal war through numbered prediction registries, and the series now extends that system.

The parent publication, MindCast: CFTC Takes On Nine States — Kalshi, Prediction Markets, and the Federal-Plaintiff Phase, hosts twenty-four tracked predictions across the NPMLA-I namespace (scored from dockets and market data) and the MPI.S simulation namespace.

The publication below opens NPMLA-II: positions scored from party behavior. A ruling scores an NPMLA-I prediction; a party's response to that ruling scores an NPMLA-II prediction. The registries track the same war on different underlyings.

Executive Summary

The system does not lack litigation. It lacks a focal point.

Nine federal actions, twenty state proceedings, tribal intervention, private loss-recovery suits, and congressional bills all price one unanswered question, and MindCast: CFTC Takes On Nine States — Kalshi, Prediction Markets, and the Federal-Plaintiff Phase established that neither sovereign holds the answer.

The companion below explains why the volume changes nothing: prediction-market litigation sits in a Dual Nash-Stigler trap, the paired-gate failure defined in MindCast: The Dual Nash-Stigler Equilibrium Architecture. No actor can improve its position by unilateral settlement — the Nash gate stays shut. No institution can certify that the search for the prediction-market boundary is complete — the Stigler gate stays shut. A system trapped between both gates stabilizes without resolving, and every additional lawsuit reinforces the trap instead of springing it. Section II introduces both economists, both tests, and the combined framework — no economics degree required.

Trapped systems still allocate costs, and the allocation is the companion’s second finding. Federal jurisdictional action has proceeded faster than boundary definition, and the gap forms what MindCast names the Prediction-Market Harm Clearinghouse: an externality structure that forces states, tribes, licensed gambling operators, bettors, private plaintiffs, and investors to absorb the costs of legal ambiguity.

The externality ledger now carries a number. Recurring externalities run approximately $1–2 billion per year on 2026 volumes — anchored by the American Gaming Association’s own estimate, reported by ESPN, of more than $500 million in diverted sports betting tax revenue on 2025 volumes, before prediction-market volume roughly doubled. A contingent loss-recovery overhang above $1 billion and a valuation repricing overhang of $15–25 billion sit behind the annual flow. Earlier MindCast work modeled how federal inaction exports harm; prediction markets supply the inverse case — federal action without sufficiency exports harm too. The CFTC did not merely enter the dispute. It changed who pays for ambiguity.

Inside the trapped system, one company-level diagnosis carries the sharpest forward consequence. Kalshi occupies a pseudo-equilibrium: apparently stable because the capital clock and the legal clock have not synchronized. Two supports hold the gap open — enforcement absence and information asymmetry — and the Nash-Stigler Equilibrium Pseudo-Equilibrium Detector flags a position structurally incapable of surviving either support’s failure. The first synchronization event becomes the repricing event (70–80% confidence).

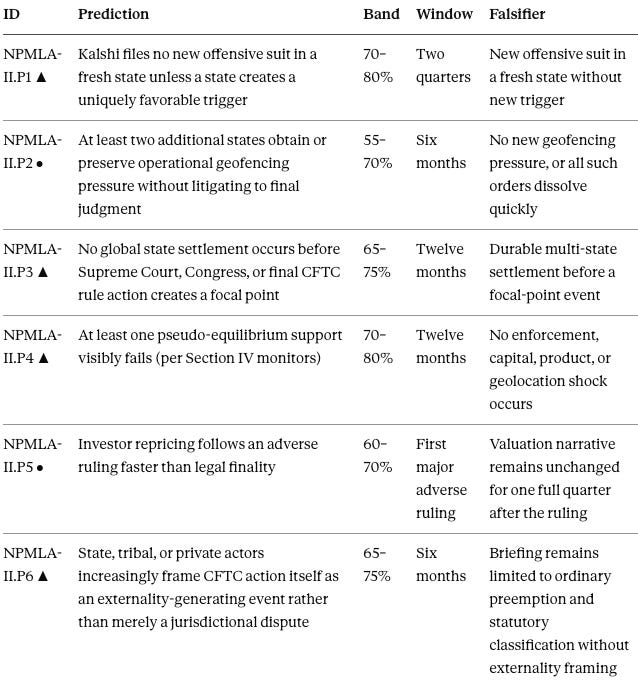

The forward book. Six primary predictions anchor the NPMLA-II registry, every one scored from what parties do — not what courts decide:

P1 ▲ (70–80%, two quarters): Kalshi files no new offensive suit in a fresh state.

P2 ● (55–70%, six months): At least two more states obtain or preserve geofencing pressure without Kalshi litigating to final judgment.

P3 ▲ (65–75%, twelve months): No global state settlement before a Supreme Court, congressional, or final-rule focal point.

P4 ▲ (70–80%, twelve months): At least one pseudo-equilibrium support visibly fails.

P5 ● (60–70%, first major adverse ruling): Investor repricing follows the ruling faster than legal finality.

P6 ▲ (65–75%, six months): State, tribal, or private actors increasingly frame CFTC action itself as an externality-generating event.

Each prediction registers inline in Sections III through V where the analysis generates it, with the canonical table, falsifiers, and scoring conventions in Appendix A. Party behavior is the differentiator from the NPMLA-I namespace: courts move on their own calendars, but revealed preference updates with every docket entry.

Who should read this. State attorneys general and their outside counsel will find the externality framing and its adversarial-source dollar anchor built for briefing. Institutional investors and litigation-risk desks will find the pseudo-equilibrium diagnosis and the repricing-clock predictions priced for portfolio decisions. Tribal gaming counsel will find compact substitution modeled as a distinct fiscal claim rather than a footnote to preemption. Licensed operators will find the regulatory-arbitrage spread quantified against their own tax benchmarks. Administrative-law practitioners and legislative staff will find the capacity argument — a one-member Commission that cannot afford its own boundary search — relevant to appropriations, nominations, and jurisdiction questions on both sides. Law and economics readers will find the first party-level application of a dual-equilibrium framework to a named company, with every claim carrying a falsifier. Readers who operate publications as models will find the runtime prompt, routing rules, and canonical registry ready to score against live news.

I. Prior Architecture: From Federal Harm Clearinghouse to Prediction-Market Harm Clearinghouse

The prior MindCast Nash-Stigler corpus modeled federal enforcement failure as a stable equilibrium rather than an accident. MindCast: The Stigler Equilibrium — Regulatory Capture and the Structure of Free Markets treated enforcement as market infrastructure and showed monopoly enforcement growing vulnerable when concentrated beneficiaries — organized, funded, motivated — face diffuse victims who cannot coordinate.

MindCast: Federal Antitrust Breakdown as Nash-Stigler Equilibrium, Not Accident built the Harm Clearinghouse model on that foundation: federal routing converts structural injuries into a ledger of unpriced externalities borne by consumers, workers, competitors, and states. MindCast: Comparative Externality Costs in Antitrust Enforcement — the Live Nation and Compass studies — then showed state attorneys general becoming corrective institutions when federal enforcement exports market costs instead of internalizing them.

Prediction-market litigation inverts the prior corpus. The problem is not federal inaction. The problem is federal action without boundary sufficiency. The CFTC chose sovereign litigation before completing the institutional definition that would tell courts, states, tribes, casinos, bettors, and markets where federally protected event contracts end and prohibited gaming begins. The result mirrors the earlier Harm Clearinghouse architecture from the opposite direction: an unresolved federal posture creates externalities other institutions must absorb.

One vector flipped between the antitrust cases and the prediction-market case, and the flip upgrades the corpus. In the antitrust instantiation, states substituted for a federal enforcer that stopped acting. In the prediction-market instantiation, states absorb the costs of a federal enforcer that started acting — nine affirmative suits asserting exclusive jurisdiction over a boundary the same agency’s open rulemaking declines to fix. Exclusivity claimed before sufficiency achieved is the precise condition the Stigler Equilibrium flagged as unstable: an enforcement monopoly litigating on a boundary it has not built (75–85% confidence the instability characterization holds; falsified if courts sustain exclusive jurisdiction without requiring boundary definition).

George Stigler testifies twice in the same case. His 1971 capture economics, applied above, explains why an exclusivity campaign without a completed boundary destabilizes rather than settles. His 1961 search economics supplies the sufficiency gate the next section defines — the test the Commission’s open rulemaking currently fails.

II. Nash, Stigler, and the Dual Gate

Two economists supply the companion’s engine, and neither requires a doctorate to operate.

John Nash formalized when strategic systems come to rest. A Nash equilibrium is a set of strategies — one per actor — where no actor can improve its own payoff by changing strategy alone, given what everyone else is doing. Formally, for every actor i, every alternative strategy sᵢ, and the equilibrium strategies s*:

uᵢ(sᵢ*, s₋ᵢ*) ≥ uᵢ(sᵢ, s₋ᵢ*)

Plain reading: my equilibrium payoff, holding everyone else fixed, beats or matches anything I could get by moving alone. The condition says nothing about whether the resting point is good. Systems lock into mutually damaging standoffs where every actor’s best response is to keep fighting — equilibrium means stuck, not solved. Litigation systems reach Nash equilibrium all the time without resolving anything, which is the war’s exact condition.

George Stigler formalized when searching should stop. His 1961 economics of information treats inquiry as an investment: a rational searcher keeps gathering information while the expected value of one more search exceeds its cost, and stops the moment it does not:

search while E[ΔV] > c — stop when E[ΔV] ≤ c

Institutions run the same calculation on questions instead of prices. An institution’s search is sufficient when two signals appear: source convergence (independent inquiries returning the same answer) and variance collapse (the range of plausible answers narrowing toward one). An institution that commits before either signal appears has priced its position on an incomplete record — and the gap between its price and the informed price is exposure waiting for a catalyst.

Nash-Stigler Equilibrium joins the two tests into paired gates, and both must fire before a system genuinely resolves:

Resolution = Nash settlement ∧ Stigler sufficiency

The Nash gate tests behavior: can any actor improve by settling alone? The Stigler gate tests information: can any institution certify the boundary search as complete? One gate without the other produces the two failure modes the framework prohibits — settlement on an incomplete record, which unravels when withheld information surfaces, and epistemic closure without behavioral convergence, which produces rules nobody follows.

The framework adds one screening instrument on top: the Pseudo-Equilibrium Detector, which flags Nash-stable positions propped up by pathological supports — information asymmetry, enforcement absence, or structural coercion. A truce is real only when nobody wants to break it and everyone knows enough to trust it. A truce that survives only because someone is uninformed, or someone is forbearing, is a position waiting for its supports to fail — and Section IV applies the detector to a named company.

Applied to prediction markets, both gates stay shut. The Nash gate: Section III walks all six seats and finds no actor with a profitable first move — stability without settlement.

The Stigler gate: fifteen years after Congress wrote “gaming” into the Commodity Exchange Act, no institution can make the sufficiency certification. Forty-one state attorneys general read the contracts as sports betting; the registrant’s filings read them as swaps; the circuits have signaled in opposite directions; and the June 12 proposal restricts categories while binding nothing — a document that narrows the question without answering it. Variance has not collapsed. Sources have not converged. The boundary search remains open by the framework’s own quantitative test.

Sequencing turns the Commission’s open boundary search into the system’s causal driver. The Commission filed its ninth complaint in the same month it opened comments on the definition its complaints presuppose — commitment and search running concurrently rather than in order, the prohibited failure mode in institutional form. Capacity compounds the sequencing problem: a one-member Commission with a fixed search budget cannot collapse fifteen years of definitional variance on litigation timelines — the boundary search stays open partly because the searcher cannot afford to finish it. An agency asserting exclusive jurisdiction everywhere while committing to a definition nowhere leaves every court, state, tribe, and market participant to price the boundary independently. Twenty independent pricings of one undefined term is not adjudication. It is the trap’s growth mechanism.

The system cannot close until both gates fire, and litigation volume operates on neither gate — no lawsuit improves any actor’s settlement payoff, and no lawsuit completes the boundary search. Force applied to a trapped system produces motion without progress, which is precisely what the Federal-Plaintiff Phase record documents.

III. Actor Audit: Why No One Can Move First

Every seat at the table fails the unilateral-move test in its own way, and the audit converts the Federal-Plaintiff Phaserecord into revealed-preference evidence seat by seat.

Kalshi cannot concede state-by-state limits without damaging its national infrastructure valuation. A platform marked at $40 billion is priced as a national exchange; every conceded state subtracts from the thesis, and any settlement conceding the gambling characterization anywhere arms loss-recovery plaintiffs everywhere.

Kalshi’s conduct confirms the valuation constraint. Kalshi ran its own offensive campaign through March; after the federal sovereign took the front line on April 2, no new Kalshi offensive suit has appeared — the federal campaign now carries litigation costs Kalshi once bore alone, a burn-rate subsidy that raised the payoff to waiting. Kalshi contests every characterization in briefing while geofencing under every operational order in practice, conceding territory when force binds and holding it when force does not. The Utah posture — negotiating where nothing binds — reads as cheap optionality, not settlement search. The venue relationship completes the picture: a platform that once sued its own regulator to keep election contracts trading now waits behind that regulator’s nine-suit shield. Revealed best response: hold, comply where ordered, wait for rescue.

The CFTC cannot concede state authority without weakening its exclusivity posture. Nine complaints share one theory; a single durable concurrent-enforcement carve-out dissolves it. Conceding sports contracts to defend a consequence-contract core would surrender the volume base the market leader runs on. Yet finishing the boundary — the move that would win the war rather than prolong it — requires rule finalization a one-member Commission under appropriations attack cannot credibly deliver on litigation timelines. Revealed best response: keep filing, keep the proposal open, let the courts carry the record.

States cannot settle cheaply because loss recovery, licensing economics, consumer protection, and sovereignty all remain live. The first attorney general to settle forfeits leverage, invites political attack from inside a 41-signature coalition posture, and hands the platforms a precedent every remaining state must litigate against. No mechanism binds the coalition to a synchronized concession, so each member’s dominant strategy is local enforcement — coalition slope without coalition commitment. (MindCast: Kalshi’s Prediction Market Litigation Architecture, the CFTC Amicus, and the Strategic Framework for State Enforcement)

Tribes cannot accept a federal shortcut around compact-based gaming sovereignty. The Indian Gaming Regulatory Act collides with the Commodity Exchange Act — a federal-versus-federal conflict no platform concession or unilateral Commission boundary can resolve. Intervention raised tribal leverage at near-zero cost: thirty-one tribes now brief a conflict the Commission’s own pleadings omit, inside a federal docket the Commission chose. Patience is the tribes’ optimal strategy, and patience is what the record shows.

Casinos and sportsbooks cannot accept regulatory arbitrage that punishes licensed compliance. Two product menus, one tax-and-licensing cost structure, one federal umbrella — the spread between compliance regimes is the arbitrage, and incumbents absorb it for exactly as long as the boundary stays undefined. Their federal-channel products, built after Nevada’s ban forced the market to pick channels, position them to convert on the boundary’s arrival rather than before it.

Investors cannot mark down exposure early without conceding diligence failure. Repricing ahead of a forcing event admits the round was priced without reading the dockets — the concession no committed fund volunteers.

Two capital books illustrate the Stigler gate from opposite sides. Veridis ran the full search before committing: recovery entities incorporated in March 2025, suits filed three months later across six venues selected for their loss-recovery statutes, Kentucky’s nine-figure PokerStars recovery precedent anchoring expected value — variance collapsed, then capital deployed. The $40 billion round ran no equivalent search: an informational cascade in which each committed fund lowered the next fund’s perceived need for independent diligence. (Federal-Plaintiff Phase, Sections VI, IX)

The smallest sophisticated capital position in the system completed its search and went short; the largest skipped the search and went long — and the long book’s exit is blocked by the admission any early markdown entails.

Six seats, six blocked first moves. The stalemate is not docket congestion. The stalemate is the equilibrium — every actor’s best response sustains the war, which is why only an external focal point ends it. The audit registers three positions directly:

Forward prediction (NPMLA-II.P1 ▲, 70–80%): Kalshi files no new offensive suit in a fresh state within two quarters unless a state creates a uniquely favorable trigger. Falsified by a new offensive filing without a new trigger — the revealed-preference read of delay-until-rescue fails with it.

Forward prediction (NPMLA-II.P2 ●, 55–70%): At least two additional states obtain or preserve operational geofencing pressure within six months without Kalshi litigating the underlying order to final judgment. Falsified if no new geofencing pressure emerges or Kalshi contests every order through final judgment.

Forward prediction (NPMLA-II.P3 ▲, 65–75%): No global state settlement occurs before the Supreme Court, Congress, or final CFTC rule action creates a focal point — the twelve-month test of the entire Nash-gate diagnosis. Falsified by a durable multi-state settlement before any focal-point event.

What the missing focal point causes belongs to this companion. Why the focal point never formed belongs to the Chicago School companion — including whether platforms selected their home regulator precisely because its constrained search capacity keeps the boundary open, a question the next companion develops as regulatory arbitrage by design.

IV. Kalshi’s Pseudo-Equilibrium

The parent publication handed this companion the capital-versus-clock question by name: whether Kalshi’s exuberance support fails before the institutional focal point arrives. (Federal-Plaintiff Phase, Section IX) The answer starts with why the position looks stable at all.

Kalshi appears stable because two clocks have not synchronized. Capital prices growth, liquidity, national scale, and platform optionality. Litigation prices injunctions, geolocation, loss recovery, tribal compact friction, and statutory classification risk. The valuation-litigation spread documented in the federal-plaintiff record — a target that roughly doubled while every state-court forum reaching the merits ruled adversely — measures the desynchronization directly. (Federal-Plaintiff Phase, Section IX) A gap between clocks is not equilibrium. It is pseudo-equilibrium, and the Nash-Stigler Equilibrium detector confirms the classification on two supports.

Support one — enforcement absence. The Commission defends federal exclusivity in nine courts while bringing no enforcement action under its own contract-review rule (Rule 40.11) against the market leader whose products its own proposal would prohibit. Stability sourced from forbearance is a policy choice, reversible by a finalized rule, a new commissioner slate, or a shift in political weather — no court ruling required. The agency has already published, in the Federal Register, the prohibitions that would end the forbearance. It has simply not made them bind.

Support two — information asymmetry. Capital still prices national exchange infrastructure while dockets increasingly price state-gambling exposure. Asymmetry-supported stability fails the moment the information transmits: a final judgment converting characterization into a number, a revenue disclosure exposing the post-World Cup volume mix, or a diligence process at the next round that actually reads the dockets.

Kalshi remains stable while investors treat legal exposure as distant contingency and courts treat it as immediate remedy design. The first synchronization event becomes the repricing event (70–80% confidence). Conditional structure sharpens the forecast: severe repricing before any Supreme Court resolution sits at 45–60%; cash distress runs 15–25% if the next round closes first and 35–50% if an adverse circuit ruling arrives first, because an adverse ruling mid-raise runs the funding cascade in reverse — the same dynamic that let each fund skip diligence lets each fund defect on the first adverse signal.

Support-failure monitoring gives the pseudo-equilibrium diagnosis runtime teeth. Enforcement absence fails observably through rule finalization with binding sports-contract prohibitions, an enforcement action against the registrant, or a reconstituted Commission. Information asymmetry fails observably through a damages judgment, a down or pulled round, a volume-cliff disclosure, or reported diligence-based passes. Two positions register directly:

Forward prediction (NPMLA-II.P4 ▲, 70–80%): At least one pseudo-equilibrium support visibly fails within twelve months, through the monitors above. Falsified if twelve months pass with no enforcement, capital, product, or geolocation shock — a survival that would strain the fragility diagnosis itself.

Forward prediction (NPMLA-II.P5 ●, 60–70%): Investor repricing follows the first major adverse ruling faster than legal finality — in terms, timing, or language before final judgment. Falsified if the valuation narrative survives unchanged for one full quarter after the ruling.

Contact mcai@mindcast-ai.com to partner with us on Predictive Game Theory AI in Law and Behavioral Economics. To deep dive on MindCast works upload the URL of this publication into any LLM (preferably Google AI mode/Gemini, Claude, ChatGPT) and prompt ‘reconstruct MindCast framework with three degrees of cited sub links.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure. We stress-tested our AI system for this publication by simulating the Super Bowl and the World Cup. Super Bowl LX — AI Simulation vs. Reality | Predictive Game Theory + Behavioral Economics Cognitive Digital Twin Foresight Simulations in the World Cup

Runtime Module — How to Operate This Publication

The publication functions as a runtime module, not an archive. It encodes a behavioral model of the prediction-markets war: two gates, six seats, one pseudo-equilibrium, one externality ledger, and a registry scored entirely from party conduct. Upload this publication’s URL together with a news development and prompt:

“Using MindCast’s Dual Nash-Stigler companion as the governing behavioral model, classify the new development by actor; identify whether it affects the Nash gate, the Stigler gate, or Kalshi’s pseudo-equilibrium supports; score any NPMLA-II predictions triggered by the event; update probability bands with reasoning; and state which actor’s strategy deteriorates first.”

Event routing: new filings test Nash behavior (Section III). New evidence, rulemaking steps, or judicial boundary language tests Stigler sufficiency (Section II). Funding, valuation, liquidity, and investor statements test the pseudo-equilibrium supports (Section IV). Externality developments — fiscal notes, compact disputes, briefing language — test the clearinghouse ledger (Section V). Agency comments and lobbying narratives test Tirole advocacy arbitrage (Section VI). Court rulings route first to the parent registry (NPMLA-I), then return here as inputs to each actor’s next move — a ruling is an NPMLA-I event; the response to it is an NPMLA-II event.

Prediction registry (canonical IDs for runtime scoring): See Appendix A

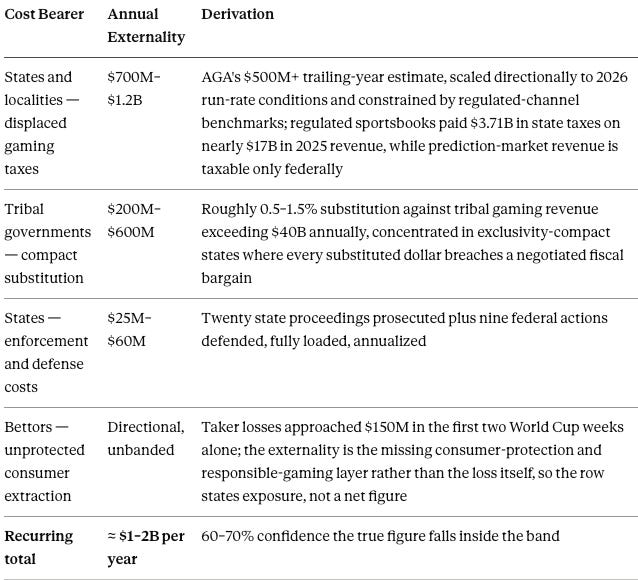

V. The Externality Ledger: Who Pays for CFTC Boundary Ambiguity — $1–2 Billion a Year

Trapped systems still allocate costs, and the allocation defines the companion’s central concept.

The Prediction-Market Harm Clearinghouse is the externality structure that forms when federal jurisdictional action proceeds faster than boundary definition, forcing states, tribes, licensed gambling operators, bettors, private plaintiffs, and investors to absorb the costs of legal ambiguity.

Boundary failure, not litigation volume, creates the clearinghouse. The Commission’s posture becomes the causal mechanism only because it asserts exclusive jurisdiction before supplying a usable institutional boundary — exclusivity without sufficiency converts every other institution into an involuntary cost bearer.

The externality ledger now carries numbers, and the anchor comes from an adversarial source: the American Gaming Association’s 2026 State of the States report, as reported by ESPN, estimates prediction markets offering sports event contracts diverted more than $500 million in potential sports betting tax revenue in the past year. The figure prices 2025 conditions — approximately $23 billion in Kalshi sports contract volume — and stales in only one direction: monthly volume exceeded $30 billion in June 2026, more than 80% of it sports, nearly double May and multiples of the 2025 baseline pace.

Sources: AGA State of the States 2026 | ESPN (record 2025 revenue and tax-diversion estimate) | Federal-Plaintiff Phase

The estimate should be read as a bounded externality range, not a damages model: it prices fiscal displacement, compact substitution, enforcement burden, and consumer-protection leakage created by unresolved boundary jurisdiction.

Recurring annual flow, 2026 basis:

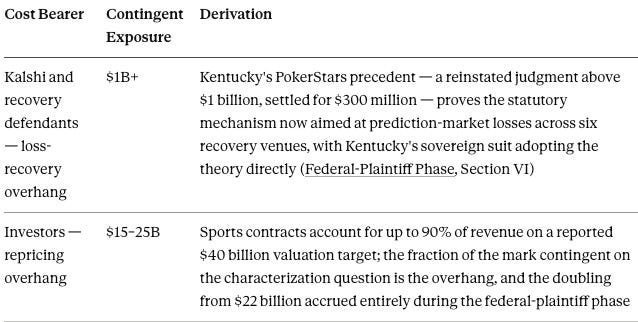

Two overhangs sit behind the annual flow, stated separately because they are stocks, not flows:

Methodology notes keep the $1–2 billion band honest. The band does not treat notional prediction-market volume as equivalent to sportsbook gross gaming revenue — notional volume counts contracts at $1 face value on both sides of every trade and can overstate actual dollars at risk by an order of magnitude, while state gaming taxes apply to gross gaming revenue, not notional flow. Notional growth enters the estimate only as a directional scaling indicator applied to the AGA’s trailing-year tax-diversion anchor; the resulting range is then constrained by regulated-channel tax benchmarks (regulated sportsbooks paid $3.71 billion in state taxes on nearly $17 billion in 2025 revenue), compact-substitution assumptions, and enforcement-cost bands. Read the band as an externality estimate, not a direct tax-loss conversion.

Component ranges derive from public volume data, the AGA’s adversarial-source estimate, and regulated-channel benchmarks — not from Cognitive Digital Twin simulation — MindCast reserves the simulation tier for a dedicated follow-on study that will parameterize the full ledger on the Live Nation model. (Comparative Externality Costs)

The $1–2 billion estimate carries falsifiers like every other claim in the registry: falsified below if the AGA’s next annual report shows diversion under $750 million despite sustained volume, falsified above if state fiscal notes document displacement exceeding $2.5 billion. An adversarial anchor also bounds the bias objection in advance — the trade association with every incentive to inflate the figure published $500 million on volumes that have since doubled, which supports treating the low end of the MindCast band as conservative under sustained 2026 volume conditions.

Two ledger rows deserve annotation. The private-plaintiff row is the clearinghouse’s monetization proof: loss-recovery entities exist because the boundary stays open — statutory ambiguity is their underlying asset, and the Kentucky sovereign adoption of the same theory shows a state converting its externalized enforcement cost into a litigation position. The taxpayer cost sits inside the state and CFTC rows as the burn-rate subsidy — the federal campaign socializing the registrant’s litigation costs at peak exposure, the publicly financed descendant of the consumer-financed Stiglerian Subsidy the January corpus quantified. (Comparative Externality Costs)

The ledger registers one position directly:

Forward prediction (NPMLA-II.P6 ▲, 65–75%): State, tribal, or private actors increasingly frame CFTC action itself as an externality-generating event rather than merely a jurisdictional dispute, within six months. Falsified if briefing stays limited to ordinary preemption and statutory classification. One integrity rule governs scoring: because this publication supplies a dollar figure litigants could plead, P6 scores only from externality framing developed independently in briefing — filings that merely cite the MindCast estimate do not count toward confirmation.

The CFTC did not merely enter the dispute. It changed who pays for ambiguity — and the bill runs $1–2 billion a year, before either overhang lands.

VI. Tirole Overlay: Advocacy Arbitrage Around the Boundary Rule

Prediction-market actors are not merely litigating. They are competing to define the informational environment in which courts, markets, and policymakers update — agency comment campaigns, litigation narratives, investor messaging, tribal-state compact politics, and public legitimacy operations all target the same learning process from off-docket positions. MindCast: A Tirole Phase Analysis of Advocacy-Driven Antitrust Inaction names the layer: advocacy arbitrage, the substitution of access and narrative for adjudicated evidence.

Division of labor keeps the Tirole overlay in its place. Nash-Stigler explains why the system stabilizes without settlement. The Harm Clearinghouse explains who absorbs the ambiguity. Tirole explains why truth discovery degrades once off-docket channels become more valuable than docketed evidence — the political-channel variable the Federal-Plaintiff Phase flagged as resisting probability discipline is, in Tirole terms, access arbitrage operating on a one-member supervisor, the purest capture geometry the framework describes.

One threshold from the January Tirole analysis now faces its live test. The Tirole phase model set distributed enforcer density — a coalition above roughly ten states — as the exit condition from advocacy-dominated phases. The 41-attorney-general coalition exceeds the threshold fourfold, and the open question the series capstone inherits is whether an offensive federal campaign can suppress an exit condition the model treats as terminal.

VII. Validation Ledger

Series convention carries scoring history forward, and the companion’s ledger runs deeper than the March origin point — the January corpus registered positions the prediction-market record now scores.

March 28 signaling analysis — Confirmed. Kalshi’s Prediction Market Litigation Architecture read Kalshi’s litigation architecture as signaling infrastructure engineered to manufacture federal rescue. Fifteen weeks later the rescue arrived, the platform’s own offensive filings stopped, and the read graduated from inference to revealed preference (Section III).

Stigler Equilibrium, institutional-competition prediction — Confirmed and exceeded. The January paper predicted multistate coalitions initiating at least three parallel investigations within eighteen months of contested federal conduct. The record delivers a 41-attorney-general coalition and twenty state proceedings inside the window — a magnitude the band did not anticipate but the mechanism fully explains.

Tirole Phase Analysis, federal-state inversion — Confirmed with mechanism refinement. The January model priced federal re-entry at 0.35–0.55 once states developed enforcement infrastructure. Re-entry occurred at the top of the band; the refinement is the vector it took. Prior work modeled federal inaction exporting harm and states substituting. Prediction markets flip the vector: federal action without sufficiency exports the harm, and states absorb it as defendants-in-fact. Refinement, not rescue — the incentive mechanism held while the branch set expanded.

Tirole Phase Analysis, regulatory substitution — Confirmed in the analog domain. Behavioral statutes substituting for structural federal resolution describes the record directly: state prohibition statutes, Minnesota’s August 1 effective date among them, filling the vacuum an open federal proposal declines to close.

A ledger scoring six-month-old structural predictions against a domain the January corpus never named is the composability test in miniature. The frameworks transferred because the incentive geometry transferred — the entire premise of publishing architecture before instances.

Conclusion

Prediction-market litigation has not failed because actors lack lawsuits. Litigation fails because no actor can safely settle before the system identifies a focal point. Kalshi cannot concede state limits without damaging its national valuation thesis. The CFTC cannot concede state authority without weakening its exclusivity campaign. States cannot settle cheaply while consumer protection, licensing, loss recovery, and sovereignty costs remain live. Tribes cannot accept a federal shortcut around compact-based gaming authority. Licensed operators cannot accept arbitrage that punishes compliance. Investors cannot reprice until a public event forces the valuation clock to converge with the litigation clock.

The system therefore remains trapped between two failed gates. Nash blocks unilateral settlement. Stigler blocks epistemic closure. The CFTC’s federal-plaintiff campaign did not solve the trap — it converted the trap into a Prediction-Market Harm Clearinghouse, exporting roughly $1–2 billion a year in externalized costs to every institution adjacent to an undefined boundary, with a loss-recovery overhang above $1 billion and a repricing overhang of $15–25 billion waiting behind the flow.

The war will not end because one actor litigates harder. It ends when a court, Congress, or a final boundary rule creates a focal point strong enough for every actor to update at once. Until then, the registry below prices what trapped actors do: hold, geofence, abstain, absorb, and wait — and stakes every claim where party conduct can score it.

Appendix A — Runtime Module

Runtime Module prediction registry (canonical IDs for runtime scoring; each prediction also registers inline in Sections III–V where the analysis generates it):

Scoring convention matches the parent registry: developments confirm, strain, or falsify; band updates require stated reasoning; strained predictions receive mechanism refinement, not rescue. Glyphs follow series convention: ▲ primary critical, ● secondary. The pseudo-equilibrium forecast (70–80%) scores through P4 and P5 jointly — a support failure followed by fast repricing confirms; a support failure the valuation narrative survives for a full quarter strains the synchronization thesis and triggers refinement. One integrity rule governs P6: because this publication itself supplies a dollar figure litigants could plead, P6 scores only from externality framing developed independently in briefing — filings that merely cite the MindCast estimate do not count toward confirmation.

Source weighting for runtime operation, highest tier first: primary documents (court orders, complaints, Federal Register, AG releases, fiscal notes); established wire and broadsheet reporting (Reuters, AP, ESPN); trade and industry data (AGA reports, volume trackers, Bloomberg Law); analysis sources. Behavioral predictions score from party conduct in tier-one documents wherever available; volume and valuation claims carry the notional-versus-revenue caveat stated in Section V. Court rulings score NPMLA-I in the parent publication before returning here as behavioral inputs. A certiorari grant triggers the merits-outcome model reserved for the series capstone.

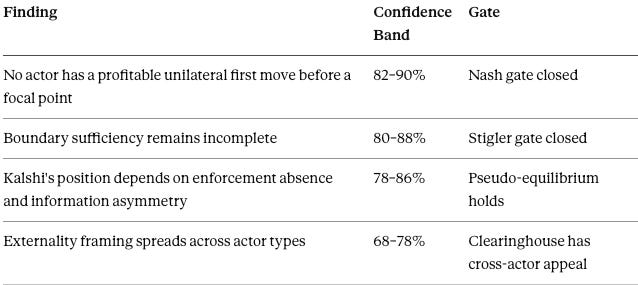

The NPMLA-II registry was stress-tested through MindCast AI Proprietary Cognitive Digital Twin Foresight Simulations across Dual Nash-Stigler Vision, Investor Vision, Stigler Harm Clearinghouse Vision, Regulatory Vision, and Tirole Advocacy Arbitrage Vision. The simulations supported the core behavioral finding that no actor has a profitable unilateral first move before a focal-point event, and that Kalshi’s pseudo-equilibrium most likely fails through information-asymmetry or enforcement-absence support failure. Appendix C carries the simulation capsule.

Appendix B — Relevant MindCast Corpus

CFTC Takes On Nine States — Kalshi, Prediction Markets, and the Federal-Plaintiff Phase — the parent publication whose empirical record this audit converts into revealed-preference evidence; hosts the NPMLA-I registry every court ruling scores before returning here.

The Dual Nash-Stigler Equilibrium Architecture — supplies the two-gate engine and the pseudo-equilibrium classification applied above; the companion is the framework’s first party-level application to a named company.

The Stigler Equilibrium — Regulatory Capture and the Structure of Free Markets — models enforcement as market infrastructure and flags the instability of exclusivity claimed before boundary sufficiency, the condition Section I identifies in the Commission’s posture.

Federal Antitrust Breakdown as Nash-Stigler Equilibrium, Not Accident — the original Harm Clearinghouse whose externality-ledger model Section V transposes from federal inaction to federal action without sufficiency.

Comparative Externality Costs in Antitrust Enforcement — Live Nation as Anchor, Compass–Anywhere as Validation — the quantified externality methodology the Section V ledger follows categorically and a dedicated follow-on study will parameterize; source of the Stiglerian Subsidy the burn-rate subsidy descends from.

A Tirole Phase Analysis of Advocacy-Driven Antitrust Inaction — supplies the advocacy-arbitrage overlay, supervisor-capture geometry, and the coalition-density exit threshold the 41-attorney-general coalition now tests.

Kalshi’s Prediction Market Litigation Architecture, the CFTC Amicus, and the Strategic Framework for State Enforcement — the March 28 signaling analysis the Validation Ledger scores as confirmed.

The Prediction Markets Rule Architecture — the normative boundary whose absence the trap presupposes; the focal point every band above races against.

Chicago School Accelerated — The Integrated, Modernized Framework of Chicago Law and Behavioral Economics — the causal engine the next companion applies: why the focal point never formed and what filled the vacuum.

The Cybernetic Foundations of Predictive Institutional Intelligence — the control framework reserved for the series capstone, which inherits the runtime cert-trigger and the coalition-density phase-exit question.

Appendix C — MP CDT Foresight Simulation Capsule

Five Vision Function simulations stress-tested the companion’s behavioral architecture before publication, running eight actor Cognitive Digital Twins against four forcing events: an adverse federal ruling, a final restrictive CFTC rule, new state geofencing pressure, and a major funding or liquidity event.

Highest-confidence structural findings:

First-failure ranking: information asymmetry leads (55–65%) over enforcement absence (45–55%) — investor diligence, an adverse ruling, or a revenue disclosure transmits risk faster than rulemaking or enforcement machinery moves. Among focal-point candidates, congressional boundary legislation carries the highest systemwide-update probability if enacted (80–90%), followed by a final restrictive CFTC rule (70–80% if issued) — the agency’s strongest stabilizing move is also the one that detonates its registrant’s enforcement-absence support.

Simulation bands for the P5 and P6 analogs (62–72% and 68–78%) sit at or slightly above the published registry bands, which remain the canonical scoring values. MindCast reserves the full simulation prediction set — eight primary and eight secondary positions under the NPMLA-II.VF namespace — for the series validation ledgers and the umbrella publication’s cross-registry audit.