MCAI Economics Vision: The Platform Geometry of Washington’s Economy

How SSB 6091 and the Millionaires Tax Reshape Housing Markets, Venture Exits, and AI Capital

Washington’s housing transparency law and proposed millionaires tax appear unrelated. In structural economic terms they regulate the same system: platform-mediated economic geography.

SSB 6091, the Real Estate Marketing Transparency law, regulates how residential listings appear across digital housing platforms. Washington’s proposed millionaires tax would impose a 9.9% rate on income above $1 million, including pass-through business income earned by founders and small business owners.

In structural economic terms, both policies regulate information and income flows within platform ecosystems. Both therefore alter the constraint geometry that determines where economic activity occurs. Washington is becoming a laboratory for platform-regulated economic geography, and the same underlying mechanism governs both debates.

The Economic Geography of the AI Era

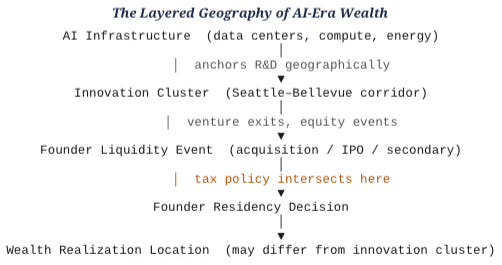

Artificial intelligence is reorganizing economic geography in ways that differ from previous technology cycles. Earlier waves of innovation dispersed productivity through relatively lightweight software and internet services. AI development instead concentrates economic activity around three physical and institutional anchors: compute infrastructure, talent networks, and capital formation hubs. These anchors create geographic clusters where training infrastructure, engineering labor, and venture finance reinforce one another. Regions such as the Seattle–Bellevue corridor, Silicon Valley, and a small number of global research centers therefore function less like traditional metropolitan economies and more like AI production nodes within a global compute network.

Concentration produces a structural asymmetry between where innovation occurs and where wealth is realized. AI systems require enormous investments in data centers, energy capacity, and specialized engineering talent, which anchors research and development activity geographically. At the same time, venture capital and founder liquidity events remain highly mobile. Entrepreneurs can relocate residency, restructure ownership, or route exits through different jurisdictions without moving the underlying innovation cluster. The resulting system resembles a layered geography: AI infrastructure and talent remain fixed, while entrepreneurial wealth and financial gains flow across jurisdictions.

Policy decisions increasingly shape how this layered geography evolves. Regulations governing digital platforms, housing markets, tax structures, and venture finance do not simply affect individual industries; they alter the constraint geometry that determines where economic actors operate and where economic outcomes materialize. When a policy closes one behavioral pathway—such as private listing networks in housing markets or certain tax advantages in venture finance—economic actors adapt by finding the next lowest-friction route through the system. The geography of AI therefore emerges not only from technological capability but also from the institutional architecture surrounding platforms, capital markets, and taxation.

Over the coming decade, regions that host AI clusters will face a strategic challenge. Retaining innovation capacity requires maintaining the dense networks of engineers, research institutions, and compute infrastructure that enable AI development. Capturing the economic returns from that innovation requires policy structures that align taxation, capital formation, and entrepreneurial incentives with those clusters. Regions that manage both will become durable centers of AI-era economic power. Regions that maintain the innovation but lose the financial realization will remain productive while watching increasing portions of entrepreneurial wealth migrate elsewhere.

I. Platform-Mediated Housing Markets

SSB 6091 targets a specific structural behavior in residential real estate: address suppression and private listing networks. When brokers withhold listings from public platforms, price discovery deteriorates and market access concentrates within private networks.

MindCast analyzed these dynamics in “SSB 6091 Has Passed. Here Is What It Now Reaches — and the Enforcement Record It Inherits” and “Compass Commission Consolidation Strategy and Real Estate Marketing Transparency.” Both publications document how broker networks controlled listing visibility within digital platforms to consolidate commissions and influence price discovery.

SSB 6091 responds by requiring residential listings to enter the open marketplace rather than private networks. Brokers and platforms now face a new constraint: the lowest-cost path can no longer run through private suppression.

II. Venture Capital and Income Flow Regulation

Washington’s proposed millionaires tax governs a different platform ecosystem: venture capital and startup finance. A 9.9% rate would apply to income above $1 million, including pass-through business income. State estimates project roughly 30,000 taxpayers would pay the tax, with proponents arguing fewer than 1% of businesses would face any liability.

Startup founders typically accumulate wealth through equity appreciation and realize taxable income only during acquisition or IPO events. When taxation concentrates at the liquidity event, founders can adjust behavior by relocating before the event occurs. Pass-through taxation therefore intersects directly with venture liquidity timing—and behavioral economics predicts three adaptive responses: pre-exit relocation, delayed liquidity events, and ownership restructuring prior to exits.

MindCast’s Chicago School Accelerated framework explains these responses through Coase on coordination costs, Becker on incentive responses, Posner on legal learning, and Stigler on information equilibrium. Tax policy shifts the expected payoff matrix. When the payoff geometry changes, behavior follows.

Washington’s real question is therefore not whether startups leave. Founders who move before liquidity events occur drive the actual structural outcome—and that distinction rarely appears in the public debate.

III. Constraint Geometry Across Both Platforms

SSB 6091 and the millionaires tax both change the constraint geometry governing economic actors. MindCast models this mechanism through “Field-Geometry Reasoning — Structural Constraint Modeling in Predictive Cognitive AI,” which examines how structural constraints determine behavior through constraint density, curvature steepness, and geodesic availability—the number of viable low-friction paths through the constraint field.

The structural mechanism underlying both policies aligns closely with the Chicago School tradition of institutional economics. Ronald Coase demonstrated that economic outcomes depend heavily on the institutional rules governing transactions rather than on abstract notions of market equilibrium alone—when those rules change, actors reorganize behavior to minimize transaction costs. Gary Becker extended this logic by showing that individuals adjust behavior whenever incentive structures shift, even in non-market contexts. George Stigler established that markets function better when information is widely available, which underpins the housing transparency argument directly. In Washington’s case, SSB 6091 alters the information structure of housing markets while the millionaires tax alters the payoff structure governing venture liquidity events. The resulting behavioral adaptations are therefore not ideological reactions but predictable responses to changes in institutional design.

In the housing market, SSB 6091 closes the suppression path and forces listings into public marketplaces. Brokers who built commission strategies around address suppression now face a constraint field with fewer geodesics.

In the venture ecosystem, the millionaires tax alters the timing of founder relocation relative to liquidity events. Founders who can establish residency in a no-income-tax state before an exit find that relocation becomes the geodesic path rather than tax absorption. The adaptation is mechanical rather than ideological.

Both policies produce the same structural effect: previously available low-cost paths close, and actors find the next lowest-cost alternative.

Contact mcai@mindcast-ai.com to partner with us on Predictive Cognitive AI in Law and Behavioral Economics. To deep dive on MindCast work in Cognitive AI upload the URL of this publication into any LLM and prompt ‘reconstruct MindCast framework with three degrees of cited sub links.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure. Recent projects: The Cybernetic Foundations of Predictive Institutional Intelligence, MindCast AI Emergent Game Theory Frameworks, Transforming Commercial Real Estate Governance Friction into Economic Velocity, MindCast AI Investment Series, Washington’s Clean Energy Advantage, a Behavioral Innovation Strategy for the Energy Transition, Super Bowl LX — AI Simulation vs. Reality.

IV. AI Capital Formation

Washington sits at the center of the global AI capital formation cycle, which makes the intersection of these policies consequential beyond the immediate policy debates. Microsoft, Amazon, and the Allen Institute for Artificial Intelligence anchor the state’s AI infrastructure, and the concentration of engineering talent in the Seattle-Bellevue corridor makes Washington a primary node in global compute investment.

AI development requires massive capital concentration in compute infrastructure, which amplifies the importance of venture exits and founder liquidity. Founders who relocate before liquidity events while their startups remain in Washington produce an equilibrium already observed in other high-cost technology hubs: innovation activity stays geographically concentrated while entrepreneurial wealth distributes geographically.

Washington retains the productive capacity. Other states capture the taxable event.

V. Predictive Implications

If current policies persist across both domains, Washington’s economic structure will likely evolve toward three simultaneous equilibria.

SSB 6091 will increase transparency in residential markets and weaken private listing networks. The Compass-Redfin-Rocket partnership announced in February 2026 eliminated Compass’s primary antitrust defense and makes the bill’s concurrent-marketing requirement directly enforceable. Open platform dynamics will accelerate.

AI infrastructure and startup ecosystems will remain anchored in Washington due to talent concentration, proximity to Microsoft and Amazon, and the depth of the regional engineering labor market. Tax policy alone cannot relocate an innovation cluster.

Founder wealth realization will become more geographically distributed. Pre-exit relocation will emerge incrementally rather than as a dramatic exodus—structurally significant but politically invisible until well after the fact.

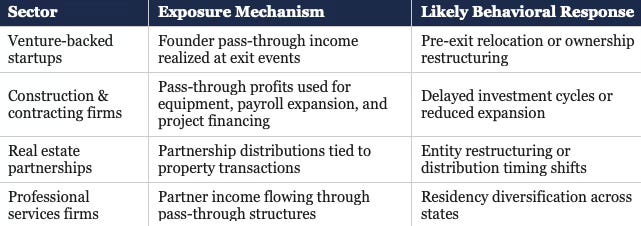

VI. Economic Exposure Map

Washington’s proposed millionaires tax concentrates on individual income above $1 million, but the policy’s practical effects propagate through several sectors that rely heavily on pass-through income structures. Understanding exposure requires examining how different industries convert income into reinvestment, employment, and growth.

These sectors do not simply absorb tax changes. Actors adjust timing, ownership structure, and geographic exposure in response to altered payoff structures. Mapping sector exposure clarifies which parts of Washington’s economy face the strongest behavioral incentives to adapt.

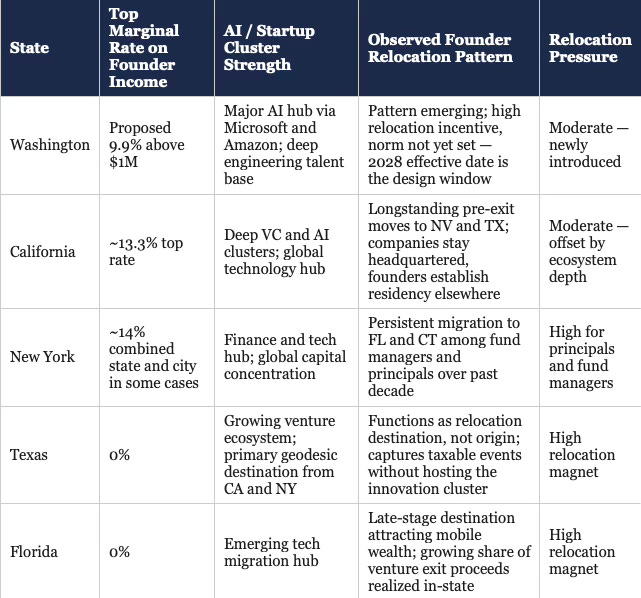

VII. Washington’s Competitive Position Among Innovation States

Washington competes with a small group of states that host major technology and startup ecosystems. Tax structure interacts with ecosystem strength to determine whether founders relocate or remain anchored to a region.

Historically, innovation clusters resist relocation because talent networks, venture capital relationships, and technical infrastructure accumulate locally. Founder residency decisions, however, remain mobile. A hybrid equilibrium results: innovation activity stays concentrated while wealth realization disperses geographically.

VIII. Founder Liquidity Pathway

Startup wealth typically accumulates through equity appreciation rather than salary income. Founding precedes early funding, which precedes growth, which precedes acquisition or IPO—and taxation intersects with this lifecycle at the moment liquidity occurs.

When taxation concentrates at that liquidity point, founders possess one critical strategic option: relocating residency before the exit event occurs. The company remains anchored to its talent and infrastructure base while the taxable event occurs under a different jurisdiction.

Policy debates focused solely on business relocation therefore misinterpret the actual behavioral response. Structural adaptation occurs at the level of founder residency rather than corporate location—which is why the signal rarely appears in conventional economic statistics until well after the fact.

IX. Policy Design Alternatives

Tax policy design determines whether behavioral adaptations occur at scale. Several design adjustments could mitigate relocation incentives while preserving revenue goals.

A liquidity deferral mechanism would allow taxation of founder equity gains only when proceeds convert to cash distributions rather than unrealized or reinvested equity. A founder reinvestment credit would provide tax deferrals when liquidity proceeds are reinvested in Washington-based startups, venture funds, or research institutions. A startup safe harbor would exclude pass-through income from early-stage companies below a defined revenue or valuation threshold, protecting emerging ventures from the tax’s reach.

Policy design choices do not eliminate incentives but alter the constraint geometry governing founder decisions.

X. Business Migration Early-Warning Indicators

Because founder relocation often occurs gradually and quietly, early signals are necessary to detect structural shifts before they appear in economic statistics. Key indicators include changes in founder residency prior to major acquisitions or IPOs, growth in dual-state residency declarations among venture founders, increasing share of startup incorporations occurring outside Washington, geographic distribution of venture exit proceeds, and venture capital investment flows tied to founder relocation decisions.

Monitoring these signals allows policymakers and business organizations to distinguish between temporary political debate and structural migration trends.

XI. What Chambers of Commerce Should Monitor

Business associations and regional chambers can play an important role in tracking how policy changes interact with entrepreneurial behavior. Founder residency patterns before major venture exits, venture capital investment flows into Washington startups, geographic distribution of startup acquisitions involving Washington companies, high-growth company formation rates within the Seattle-Bellevue corridor, and capital reinvestment levels by founders following liquidity events all provide early insight into the state’s evolving economic geography.

These indicators reveal whether Washington maintains its position as a leading innovation hub while founder wealth realization shifts geographically.

XII. Ten-Year Structural Outlook

If current policy trajectories continue, Washington’s economic system will likely evolve toward three simultaneous equilibria over the coming decade.

SSB 6091 will reinforce open-platform dynamics in residential real estate, improving price discovery and reducing the viability of private listing networks. The Seattle-Bellevue corridor will remain anchored as a global center of AI research and cloud infrastructure, supported by Microsoft, Amazon, and the region’s engineering talent base. Founder wealth realization will become geographically dispersed as entrepreneurs adjust residency prior to liquidity events—preserving innovation capacity within Washington while redistributing taxable liquidity events across multiple jurisdictions.

Understanding this structural trajectory is essential for policymakers, investors, and chambers of commerce seeking to maintain Washington’s position within the emerging economic geography of the AI era.

XIII. The Export Lens: What Washington Reveals, What It Can Learn

Washington’s policy combination—platform transparency regulation in housing and pass-through income taxation in venture finance—is not unique in its individual components. What makes Washington distinctive is deploying both simultaneously within a single AI-concentrated innovation corridor. That combination creates a natural experiment with observable structural outputs that other states and policymakers can study.

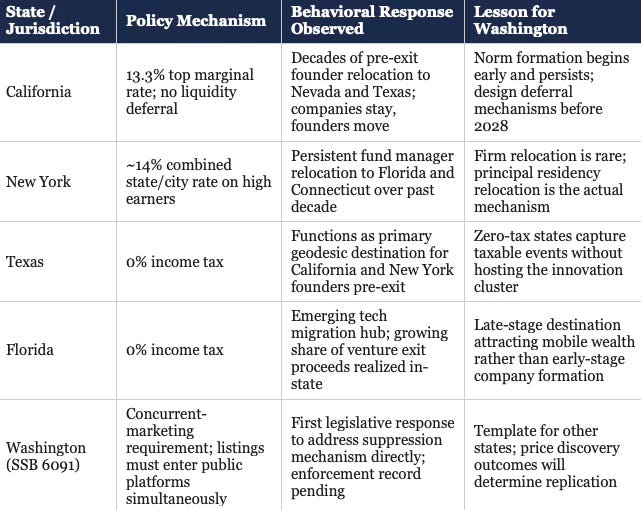

Several of Washington’s underlying pressures are not unique to the state. Any jurisdiction that hosts a high-density innovation cluster without a pre-existing income tax faces the same structural tension: the absence of income tax historically attracted entrepreneurial capital, and introducing one mid-cycle disrupts behavioral expectations that founders formed under the prior regime. Florida and Texas face an analogous challenge in reverse—both attract founders precisely because of zero income tax, and any future fiscal pressure to introduce income taxation would trigger identical founder liquidity timing responses.

Housing platform suppression is similarly not a Washington-specific phenomenon. Compass operated its Private Exclusives strategy across multiple major metropolitan markets, including New York, Los Angeles, and Chicago. Washington’s SSB 6091 is among the first legislative responses to address the structural mechanism directly, making it a template other states can adopt. States watching Washington’s enforcement record will determine whether the statute’s concurrent-marketing requirement produces measurable price discovery improvement—and whether that outcome justifies replication.

California offers the most instructive comparison on the venture taxation question. With a 13.3% top marginal rate and no separate liquidity deferral mechanism, California has generated decades of pre-exit relocation behavior by founders. Nevada and Texas function as its primary geodesic alternatives. The pattern is well-documented: companies stay headquartered in San Francisco or Los Angeles, founders establish Nevada residency before acquisition events, and California captures far less founder wealth than its innovation output would suggest. Washington is now positioned to observe whether its 9.9% rate—lower than California’s but newly introduced—produces a compressed version of the same behavioral arc, or whether the lower rate and deeper workforce anchoring produces a different equilibrium.

New York’s experience with financial services pass-through income offers a parallel worth examining. New York’s combined state and city income tax burden on high earners approaches or exceeds 14% in some scenarios, and the state has observed persistent fund manager and principal relocation to Florida and Connecticut over the past decade. The mechanism is identical to what Washington’s venture ecosystem now faces: taxation at the point of income realization drives residency relocation rather than firm relocation. Financial firms remain in New York. Partners move to Palm Beach.

What other states can learn from Washington is more granular. SSB 6091’s concurrent-marketing requirement—which mandates that listings marketed privately must simultaneously enter public platforms—addresses the suppression mechanism more precisely than blanket disclosure requirements do. States considering housing transparency legislation can study whether Washington’s enforcement architecture produces the intended price discovery outcome before designing their own statutes. On the taxation side, Washington’s passage of a high-threshold pass-through tax within an AI-concentrated corridor provides a real-time behavioral dataset on founder mobility that no other state currently possesses at comparable ecosystem scale.

What Washington can learn from other states is primarily about sequencing and design. California’s experience suggests that once a founder relocation norm establishes itself within a venture network, it persists and expands through social contagion even when individual tax burdens are modest. Washington has a narrow window—roughly the period between passage and the tax’s 2028 effective date—to design deferral mechanisms, reinvestment credits, or safe harbors that alter the behavioral path before relocation becomes the established norm within the Seattle-Bellevue founder community. Norm formation, not the tax rate itself, determines the long-run equilibrium.

Conclusion

Washington’s housing transparency law and millionaires tax debate appear to address different policy domains. In structural economic terms, both policies regulate platform ecosystems that govern information and income flows. Both close previously available low-cost behavioral paths. Both force actors toward the next available geodesic.

Adjustments across both domains will shape not only housing markets and startup finance but also the geographic distribution of entrepreneurial wealth during the coming AI investment cycle. Whether Washington becomes a model for platform-regulated economic geography or a case study in unintended capital migration depends on whether policymakers understand the structural mechanism both laws activate—and whether the resulting constraint geometry gets designed intentionally or left to produce outcomes by default.

Runtime Module Note

MindCast publishes this piece as a runtime module allows policymakers, investors, and analysts to use the URL as a structural interpretation layer for incoming news rather than as a static article. When the publication is uploaded or referenced inside a large language model, the model can map new developments—legislation, venture exits, founder relocations, or housing platform enforcement actions—onto the framework the paper establishes.

Each new development becomes an input the model evaluates against the module’s core mechanisms: constraint geometry, founder liquidity timing, platform transparency enforcement, and AI capital formation dynamics. Rather than treating headlines as isolated events, the model classifies them within the system the publication defines and updates its interpretation of Washington’s economic trajectory accordingly.

The module maps directly onto MindCast’s named metrics stack. When analysts upload this publication, the model can track the following:

Transaction Delay Cost (TDC) — enforcement lag between SSB 6091’s passage and measurable price discovery improvement; delay between the millionaires tax’s 2026 passage and its 2028 effective date during which relocation norms form.

Synchronization Index Score (SIS) — alignment between housing platform enforcement, venture tax policy, and AI infrastructure investment cycles; measures whether regulatory bodies governing each domain are operating on compatible timelines or producing conflicting constraint signals.

Defection Probability Index (DPI) — likelihood that founders within a given cohort adopt pre-exit relocation as the dominant strategy; increases as relocation norm establishes itself within Seattle-Bellevue venture networks and as the 2028 effective date approaches.

Geodesic Availability — number of viable low-friction behavioral paths remaining after each policy change; SSB 6091 closes the private suppression geodesic in housing while the millionaires tax opens the pre-exit relocation geodesic in venture finance.

Norm Formation Velocity — rate at which pre-exit relocation becomes the expected default behavior within founder networks; California’s experience establishes that once this norm sets, it persists independent of marginal tax rate changes.

For policy staff, the module functions as a decision filter that identifies whether a development strengthens or weakens Washington’s innovation cluster. For investors, the same module interprets signals about founder mobility, venture exit geography, and AI capital concentration. For chambers of commerce and economic development organizations, the module provides a consistent structural lens for evaluating legislative proposals before they reach a vote.

The result is that the publication functions less like commentary and more like a framework the model can repeatedly apply to real-time information flows—allowing decision-makers to ingest news through a consistent structural interpretation rather than reacting to each development in isolation.