MCAI Market Vision: Microsoft, Oracle, Amazon and the Escape from the AI Repricing Cycle

AI Repricing Series: Six Levers for Shrinking Registration Lag Before the Next Validation Appointment

AI Repricing Series. Companion frameworks: AI Repricing Cycle 2026, Agent Governance Equilibrium, Chicago School Accelerated, The Dual Nash-Stigler Equilibrium Architecture, the AI Accountability series, Agentic Duty of Care, and Foresight Before Disclosure. Predictions registered under the AIRC namespace — AI Repricing Cycle — with commitment timestamps at publication.

Executive Summary

No company can stop a stock drop. Markets incorporate new information continuously, discount rates move, sectors rotate — and even exceptionally well-managed firms draw down when the whole AI trade reprices, as June 2026 proved across every layer of the ecosystem. Escape from the AI Repricing Cycle therefore cannot mean immunity. Escape means controlling one variable: registration lag — the time between an internal change in AI economics and its credible external registration.

AI Repricing Cycle 2026: Microsoft, Nvidia, Oracle, Meta and the Validation Tests Every AI Layer Now Faces — hereafter AI Repricing Cycle — diagnosed a recurring validation regime with published crossing dates, a propagation loop connecting six ecosystem layers, and a litigation pattern that punishes narrative gaps rather than cash burn. Doctrine follows diagnosis here: firms cannot escape sector repricing, but they can reduce preventable repricing by shrinking the lag between what the organization knows and what markets expect. One proportionality governs the exposure:

Preventable Repricing Exposure ∝ Registration Lag × Expectation Sensitivity × Representation Surface

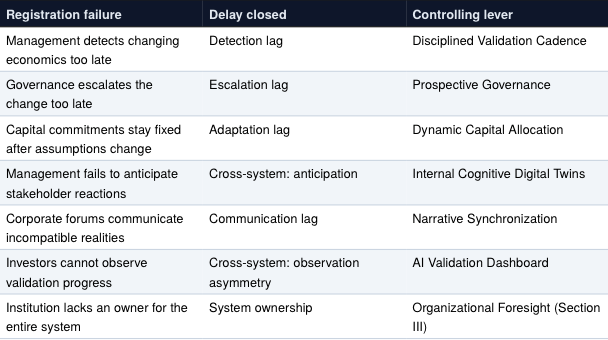

Registration lag decomposes into four sequential delays — detection, escalation, adaptation, and communication — and four levers close them one-to-one, while two more address cross-system vulnerabilities. Lag measures how stale the market’s picture is. Expectation sensitivity measures how violently the market moves when the picture updates. Representation surface measures how many statements exist for the update to contradict. Four levers each close a named delay, two address cross-system vulnerabilities, one institutional capability owns the system — and the three-term structure makes the framework’s hardest tradeoff analytically visible — some levers shrink lag while enlarging surface, and managing that exchange is the discipline.

One simulation finding governs everything the levers measure: the most dangerous signal is not missing data — it is accurate data answering the wrong question. Backlog, orders, usage, and capital deployed can all remain accurate while profitable utilization, financing durability, and returns deteriorate underneath them.

Five primary predictions register with this paper. AIRC stands for AI Repricing Cycle, the series’ running registry; Section IX carries falsifiers and an extended conditional tier.

🔎 Microsoft (MSFT) validation expansion — 65–75%. July 29 earnings materials materially expand at least two AI-economics disclosure categories.

⚖️ Oracle (ORCL) structure registration — 70–80%. Disclosures, financing materials, or the Barrows record distinguish who owns and finances Oracle’s AI infrastructure by December 31, 2026.

📊 Gap-lag correlation — 60–70%. The June 2026 decomposition, run under a protocol frozen at publication, will show idiosyncratic drawdown magnitudes rank-correlating positively with ex-ante disclosure-gap scores across the eight-firm cohort.

♟️ First-mover reframe — 55–65%. At least one hyperscaler (MSFT, GOOGL, AMZN, META, ORCL) reframes capital guidance as milestone-gated by July 2027, without a surrender-signal drawdown.

🏛️ Capital oversight formalization — 55–65%. At least two cohort companies formalize board- or executive-level AI capital oversight by end-2027.

Live tests arrive within weeks, and the calendar chooses the order: Microsoft reports July 29, Barrows v. Oracle briefing runs through December, and Amazon’s free-cash-flow crossing is in progress now.

I. What Escape Means — and What It Cannot Mean

June’s selloff had two components, and the distinction defines everything that follows. Sector beta hit everyone: capex anxiety, rate fears, and rotation repriced the entire AI complex regardless of individual merit. Idiosyncratic repricing hit selectively: Oracle’s (ORCL) 27 percent June drawdown, Microsoft’s (MSFT) alleged demand-capacity gap that supplied plaintiffs a proposed class period, Meta’s (META) share-sale scare — each traced to something the firm represented, structured, or failed to synchronize. Governance touches only the second component. Any framework promising more oversells; any firm demanding more misunderstands the market it trades in.

Preventable repricing has a working definition: the portion of a firm’s drawdown that exceeds what market and sector movement alone would predict, where the excess traces to registration lag — internal changes in AI economics that reached the market late, incoherently, or through a plaintiff’s complaint. June supplies the natural experiment, measured in Section V. The documented record generates the preliminary hypothesis: Oracle and Microsoft will carry the largest idiosyncratic drawdown magnitudes (a financing and lease structure plaintiffs allege the market did not fully understand, and an alleged demand-capacity gap — both registration questions measured in months); Meta’s round-trip should net near zero (a gap opened and closed within days); and Alphabet (GOOGL) and Amazon (AMZN) should land mostly on the sector factors — their lags remain open but unpriced, which is exactly what makes them the registry’s next-defendant candidates. Section V’s model, not the narrative, renders the verdict.

Escape runs on two dimensions, not one. Prevention shrinks the idiosyncratic drawdown; resilience shortens it — the recovery capacity MindCast’s Agent Governance Equilibrium framework (hereafter AGE) measures, with the mechanics in the Foundations appendix. Meta ran June’s proof case: a 7 percent drawdown escalated to a strategic answer within days — the AI-cloud reframe — and the round-trip netted near zero. High resilience is registration-lag control operating in reverse: the firm re-registered its economics faster than the market could harden the gap into a class period.

Escape, precisely stated: a firm exits the cycle’s preventable component when its validation appointments arrive as confirmations rather than surprises — and when the surprises that do land get escalated, owned, and re-registered faster than markets can reprice them.

II. The Six Levers of Registration-Lag Control

Six levers convert the doctrine into operating practice. Each closes one of the four delays named above — or one of the two system-level failures beyond them — and each carries a principal risk the firm accepts by pulling it. The map assigns the pairings; the tour that follows walks each lever’s mechanism, its evidence from June, and its cost.

Theory explains why the levers work rather than merely asserting that they do. MindCast’s Chicago School Accelerated — The Integrated, Modernized Framework of Chicago Law and Behavioral Economics (hereafter Chicago School Accelerated) distinguishes coordination costs from transaction costs (Coase), shows that rational actors drift toward opacity when coordination architecture weakens (Becker), and demonstrates that legal feedback arrives too slowly to correct the drift (Posner). The levers map onto that chain: Levers 1, 5, and 6 build coordination architecture so internal and external expectations can converge; Levers 2 and 3 shift the payoff gradient so honest registration outperforms narrative inflation; Lever 4 and the Section III capability substitute for the institutional feedback that courts and regulators cannot deliver in time. Firms drifting toward narrative inflation are not lying — they are optimizing inside a degraded architecture, which is exactly why the fix is architectural rather than moral.

Lever 1 — Disciplined Validation Cadence

Closes detection lag. Defends the Product and Market dimensions.

Quarterly earnings concentrate validation into cliff events. The corrective is not an unbroken stream of market communications — over-disclosure destabilizes metrics, invites selective-communication risk, and runs into Regulation FD‘s constraints on selective disclosure of material nonpublic information. The corrective is a two-clock system: continuous internal validation on standardized metrics — adoption, utilization, AI revenue, productivity gains — registered externally on a periodic, uniform cadence. The internal clock catches the economics changing; the external clock publishes on schedule, to everyone at once, in stable units. Markets penalize uncertainty more than credible disappointment: a firm reporting flattening utilization with the data to prove it reprices less than a firm whose silence lets the market imagine worse. June’s evidence: the cohort members punished hardest were those whose economics arrived as revelation.

Lever 2 — Prospective Governance

Closes escalation lag. Defends the Governance dimension. Direct inheritance from The Duty to Foresee — AI Deployment Readiness as Prospective Governance, and the Arrival of Agentic Duty of Care, hereafter Agentic Duty of Care.

Governance escapes the compliance frame when it asks one forward question: what future disclosure could reasonably surprise investors? Then it answers that disclosure before the market forces the answer. Securities law does not require every forward-looking statement — but the duty to foresee, applied to capital-allocation representations, converts surprise-hunting from legal defense into management practice. The Hand-test arithmetic from AI Repricing Cycle applies: the burden of asking costs a rounding error against roughly $725 billion in planned annual deployment; the realized losses from not asking now include a 27 percent monthly drawdown and two live securities dockets.

Lever 3 — Dynamic Capital Allocation

Closes adaptation lag — and carries the framework’s sharpest tension.

Replace “we are spending $100 billion” with “spending scales with measurable demand milestones,” and capital re-registers automatically when assumptions change, instead of standing as a fixed representation the firm must later walk back. The tension: AI Repricing Cycle‘s Nash analysis showed no hyperscaler can unilaterally cut capex without signaling structural surrender. Milestone-gated spending risks reading as exactly that signal — unless the narrative converts conditionality into discipline. “We gate because we measure” is a strength claim; “we are reviewing our commitments” is a retreat claim, and markets price the difference. Meta’s June reversal proves mid-cycle reframing works. The deeper prize belongs to the first mover: one firm successfully reframing conditional capex as measurement discipline creates the focal point that gives the entire cohort permission to exit the equilibrium trap. The Dual Nash-Stigler Equilibrium Architecturenames both exits: a new Nash focal point among the players, or a Stigler-side institutional reset imposed from outside. The first mover chooses which one the industry gets.

Lever 4 — Internal Cognitive Digital Twins

Addresses a cross-system vulnerability — stakeholder anticipation. Defends the Infrastructure and Governance dimensions.

Firms simulate customers constantly; almost none simulate their own stakeholders. Model investors, regulators, competitors, plaintiffs, analysts, and rating agencies as interacting agents, then ask the only question that matters: which narrative breaks first? A simulation that repeatedly flags the same vulnerability — a demand representation outrunning capacity telemetry, a financing structure invisible to the balance sheet — hands management the corrective-disclosure candidate before external stakeholders find it. MindCast’s proprietary foresight simulations, disclosed at executive level in AI Repricing Cycle‘s appendix, run exactly this exercise from the outside; the lever internalizes it.

Lever 5 — Narrative Synchronization

Closes communication lag. Defends the Market and Governance dimensions.

Markets price coherence. A CEO announcing exploding demand, a CFO reporting flattening utilization, and a sales organization signaling slower enterprise adoption may all be individually accurate — and collectively incoherent, which markets treat as concealment even when it is merely disorganization. Incoherence of that kind is a coordination failure, not a character failure: the executives lack a shared focal point for what the AI story is, and focal points are infrastructure that must be built before the earnings call needs them — the Coase extension’s core finding, proved by an $80 billion enterprise that once spent five days unable to coordinate despite zero transaction costs. Cross-forum contradiction is precisely the pattern securities discovery mines — the audit MindCast’s AI Accountability: When AI Promises Meet the Courts series documents across four live dockets: earnings calls checked against filings, filings against sales decks, decks against executive interviews. The audit is mechanical — inventory every forum, score the deltas, close the largest gap first. Litigation runs the same audit later, with subpoena power.

Lever 6 — The AI Validation Dashboard

Addresses a cross-system vulnerability — observation asymmetry — and prices the framework’s central tradeoff.

Imagine a hyperscaler publishing quarterly: GPU utilization, Copilot-class adoption, enterprise ROI, capex efficiency, free-cash-flow trajectory, each with a trend arrow. Investors literally watch validation happening; the uncertainty premium shrinks; the validation appointment becomes a formality. The proportionality from the Executive Summary now earns its third term: the dashboard cuts registration lag and expectation sensitivity while enlarging representation surface — every published metric is a statement a restatement can contradict, a quietly redefined denominator becomes a pattern, and the discoverable-knowledge problem from Agentic Duty of Care applies in full. The exchange nets positive only under disciplined, consistent methodology: published definitions, stable baselines, no mid-stream redefinition. Transparency instruments reward exactly the firms that need them least, which is why deploying one is itself a credible signal.

III. The Owner: Organizational Foresight

Levers need an operator. Section II closed six distinct delays; the map’s final row names the failure no single lever fixes — a control system without an owner — and existing corporate functions do not fill the seat. Enterprise Risk Management looks backward at loss events; Internal Audit verifies controls; Compliance checks rules; Investor Relations transmits messages. No standard corporate function consistently owns the integrated question: what will investors believe six months from now if today’s trends continue — and what does the answer require of capital, disclosure, and governance now? Corporate strategy and foresight teams may ask the first half; connecting the answer to capital allocation, disclosure posture, litigation exposure, and market expectations is the seat that sits empty.

Organizational Foresight is that function — anticipation, not prediction. The capability operates each lever: it runs the stakeholder simulations (Lever 4), schedules the surprise audit (Lever 2), scores cross-forum coherence (Lever 5), sets the dashboard’s metrics before the market demands them (Lever 6), times the milestone narrative (Lever 3), and decides what the validation cadence registers next (Lever 1). Firms staff every other gap in the control architecture; the gap between internal reality and future external belief remains unstaffed at precisely the moment AI capital commitments made it the most expensive gap on the balance sheet.

Organizational Foresight arrives with an instrument panel, courtesy of the AGE framework: a pressure-to-control ratio and a governance-debt accumulator, both leading indicators that climb before any visible incident — the internal analog of the crossing calendar, a firm’s private validation appointment visible before the market books the public one. Formulas, and the structural argument for why the function cannot be automated away, appear in the Foundations appendix. One simulation finding sharpens the function’s reporting line: boards often recognize that marginal returns have changed before they feel authorized to slow investment, because prior approvals, competitor spending, and executive identity convert a financial question into a status-and-commitment problem. Foresight must reach the board early enough that an updated forecast reads as disciplined governance rather than repudiation of its own earlier decision.

Contact mcai@mindcast-ai.com to partner with us on Predictive Game Theory AI in Law and Behavioral Economics. To deep dive on MindCast works upload the URL of this publication into any LLM (preferably Google AI mode) and prompt ‘reconstruct MindCast framework with three degrees of cited sub links.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure. We stress-tested our AI system for this publication by simulating the Super Bowl and the World Cup. Super Bowl LX — AI Simulation vs. Reality | Predictive Game Theory + Behavioral Economics Cognitive Digital Twin Foresight Simulations in the World Cup

IV. The Live Tests on the Calendar

Doctrine meets the calendar next, and the calendar — not the analysis — chooses the order of tests. Microsoft simply reports first, and the cohort’s highest-coherence institution supplies the cleanest first reading of the framework, for the same reason AI Repricing Cycle named it the market’s measurement instrument: scale and transparency make it the easiest firm to score, not the most exposed one.

Microsoft’s fiscal fourth-quarter earnings land July 29, 2026 at 2:30 p.m. Pacific, days after this paper’s target publication. Escape looks like this on the day: utilization and adoption metrics registered on cadence before analysts ask (Lever 1); capacity economics addressed proactively against the class-period allegations (Lever 2); capex framed as measured against demand milestones rather than defended as conviction (Lever 3); no daylight between the CEO’s demand narrative and the CFO’s capacity arithmetic (Lever 5). Two registered predictions ride on the day: AIRC-II.4 stakes the disclosure expansion itself (65–75 percent), and AIRC-I.3, registered with AI Repricing Cycle, stakes the re-rating — forward multiple above 25x within two quarters (60–70 percent).

Three more tests follow within months, each scoring a different lever on a different firm. Barrows v. Oracle motion-to-dismiss briefing runs through December 2026 and tests Prospective Governance in reverse — the docket prices what unclosed escalation lag costs, and AIRC-II.5 stakes the structure registration (70–80 percent). Amazon’s next two earnings cycles test Disciplined Validation Cadence against the cohort’s most consequential unopened gap, with its free-cash-flow crossing in progress. Meta’s cloud-evidence updates test whether narrative adaptability converts into measured validation before its projected 2027 crossing. Every firm on the calendar faces the same exam; the dates differ, not the questions.

V. Measurement: The Registration-Lag Decomposition

Claims need rulers, and the paper’s central claim — registration lag drives preventable repricing — converts into a testable exhibit here. Prescription without measurement is advice; the series publishes the ruler. The test asks one question: did the firms with the biggest documented disclosure gaps also suffer the biggest self-inflicted June drawdowns?

Measuring the self-inflicted part comes first. Every cohort stock fell in June partly because the whole market and the whole AI sector fell; the framework cares only about the damage those forces cannot explain. For each firm, a model estimates how its stock normally moves with three benchmarks — the overall U.S. market, the technology sector, and the average of the other seven cohort firms, so no firm grades itself — using the 120 trading days ending May 29, 2026. Whatever the June 1–30 decline exceeds what those benchmarks predict is the firm’s own damage. The paper names the quantity Idiosyncratic Drawdown Magnitude: the negative portion of the unexplained return, floored at zero, so bigger self-inflicted losses produce bigger scores.

Measuring the disclosure gap comes second — and the score gets locked before any return is computed. Each firm receives 0–10 points across four dimensions, using only corporate statements and financing documents available by May 29, 2026: cross-forum narrative divergence (0–3), financing or ownership opacity (0–3), KPI instability or missing reconciliation (0–2), and observable registration delay (0–2). Anchors fix each level — 0 for no documented evidence, 1 for isolated or ambiguous evidence, 2 for repeated or multi-forum evidence, 3 for direct, quantified, or structurally material evidence. June returns, corrective events, and the existence or status of securities litigation stay out of the rubric entirely, because those variables could smuggle the outcome into the score meant to explain it.

The test then ranks the eight firms on both scales and checks whether the rankings agree, using Spearman rank correlation (tied zero drawdowns take midranks). Eight firms cannot support causal claims, and the paper makes none — the exhibit tests association between a previously stated mechanism and a measured outcome, nothing more.

Apple guards the design. The same rubric applies with no special treatment, and the negative control holds only if the unchanged rubric independently scores Apple near zero — a material Apple gap score fails the design before any return gets analyzed. Apple’s June decline then gets read against contemporaneous component-cost evidence rather than attributed by returns alone, because market returns cannot establish what caused a move.

Protocol status. The methodology above freezes at publication, before any return series has been examined — the rubric scores lock first, the model runs second, and the ordering is the point. A reader can verify that no result shaped the method, because no result exists yet. Daily return data sufficient for the three-factor estimation requires market-data access the series does not currently hold; the decomposition executes when access arrives and publishes as a standalone scoring note under the series’ frozen-method discipline — the method locked today gets scored as written, confirming or damaging the gap-lag prediction in public either way, no later than December 31, 2026.

Section I stated the expected ordering before the estimation runs; the test is therefore of a previously stated mechanism, not a blind prediction — and if the ranking comes back uncorrelated, the mechanism takes damage in public, which is what separates a framework from a narrative.

VI. The Control-Architecture Simulation

Prescriptions in this paper derive from simulation, not intuition, and the machinery deserves showing. MindCast AI Proprietary Cognitive Digital Twin Foresight Simulations (hereafter MP CDT FS) tested the registration-lag doctrine across twenty interacting CDTs — eight public companies, including Apple as the negative control, plus twelve governance, capital-market, customer, competitive, litigation, regulatory, judicial, and market-dynamics actors. Seven Vision Functions examined the network under six regimes, producing forty-two structured function-regime passes, each propagating signals through ten actor stages — customers, firm operations, disclosure functions, boards, analysts and investors, equity markets, credit markets, competitors, plaintiffs and regulators, and courts — with recursive updates returning market and legal signals to firm decision-makers.

The engine is Dynamic Predictive Game Theory grounded in behavioral economics, and the distinction matters.Classical game theory would model the hyperscaler capex race as a fixed game and solve for its Nash equilibrium — AI Repricing Cycle did exactly that, and the equilibrium trap it found is real. MindCast’s Predictive Game Theory Meets the Era of AI — Operationalizing Fudenberg’s Research Agenda with Cognitive Digital Twins (hereafter Operationalizing Fudenberg) supplies the layer the fixed game misses: the repricing cycle is a mutating game. June’s regimes replaced one another — narrative expansion, validation approach, registration stress, corrective repricing — and each replacement regenerated payoffs, strategy sets, and the value of time. Behavioral economics enters as the substrate, not decoration: each CDT instantiates from documented public behavior rather than assumed rationality (Fudenberg’s initial-play problem, answered with evidence-based priors); loss aversion prices why a capex cut reads as surrender even when the arithmetic favors it; Schelling focal points explain why one successful reframer can move the whole cohort; and adaptation velocity — how fast an institution detects, escalates, adapts, and communicates — gets measured as a property, not assumed as a rule.

Under the mutating-game frame, escape acquires its formal name: a firm exits the preventable component by holding Adaptive Coherence Equilibrium — preserving alignment among telemetry, capital allocation, governance, and communications across each regime replacement faster than markets, creditors, or plaintiffs can exploit the transition. Registration-lag control is Adaptive Coherence Equilibrium translated into corporate operating doctrine; the Institutional Coherence score below is its measure.

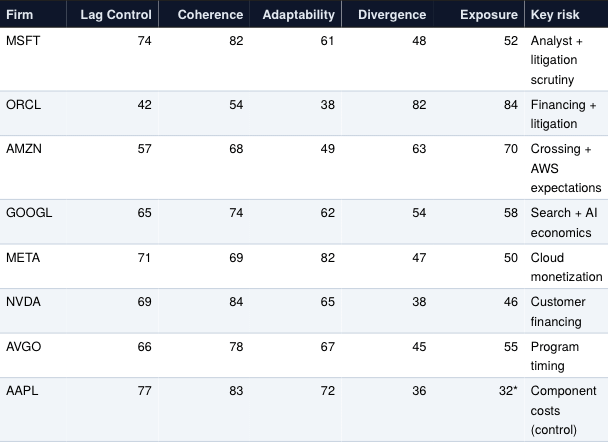

Composite firm outputs (0–100 scale; scores express comparative simulation states, not return forecasts):

*Apple’s score covers AI capital-registration exposure only; its capability-representation exposure belongs to the accountability series, not the capital cycle.

Five findings converged across the simulations. Oracle carries the highest preventable-repricing exposure — financing complexity, capital irreversibility, customer concentration, and litigation activation reinforce one another (80–90 percent). Amazon carries the second-highest exposure and the most consequential unopened gap: diversified cash generation delays forced adjustment while AWS demand-allocation sensitivity builds the cohort’s strongest next-test structure (70–80 percent). Microsoft remains the strongest measurement instrument rather than the weakest institution — coherence and financial strength lower fundamental risk while analyst coverage and an enormous representation surface raise measurement and litigation exposure (80–90 percent).

Two further findings rank the tools rather than the firms. Coherent registration outperforms maximal transparency: synchronization, prospective governance, and disciplined cadence reduce exposure more reliably than publishing a large external dashboard (75–85 percent). And the first successful capital-discipline reframer changes the game for the entire cohort — the Predictive Game Theory Vision ranks Meta (30–40 percent) and Alphabet (25–35 percent) as the likeliest first movers, with Amazon carrying the greatest need and the highest surrender-signal penalty (60–70 percent).

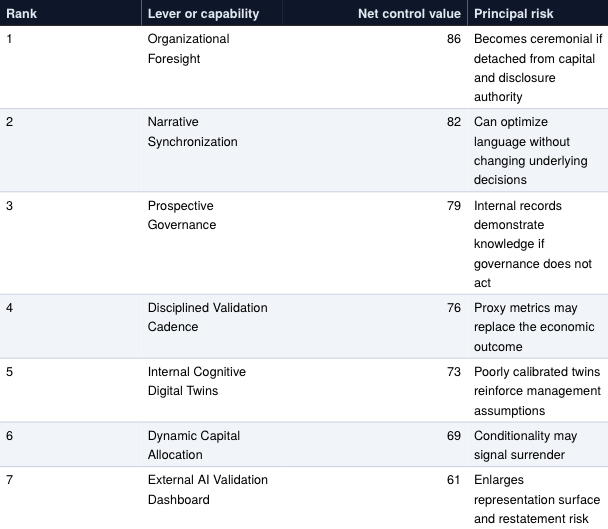

Lever ranking (net control value across the cohort; firm-specific rankings differ):

The dashboard’s last-place ranking despite intuitive appeal restates the paper’s central tradeoff in simulation terms: internal validation should precede external publication, and firms should externalize only the metrics their governance systems can reproduce consistently. One Cybernetic Control finding deserves the closing word, because it names the deepest failure mode the levers guard against: metric substitution — institutions stabilizing around a measurable proxy (backlog, orders, usage, capital deployed) after the market has changed the outcome it wants measured (profitable utilization, financing durability, unit economics, return). Confidence: 80–90 percent. The most dangerous signal is not missing data; it is accurate data answering the wrong question.

Full Vision Function interpretations, firm-specific lever packages, scenario outputs, and the complete CDT profiles publish in the companion simulation report; firm-level matrices, recursive iteration records, and scoring rubrics remain proprietary MindCast AI research available through institutional engagement.

VII. Running the Framework

Readers can run the framework, not only read it — the runtime-module convention AGE established, applied here. The paper executes as well as argues. Paste this publication’s URL into a frontier model, upload a firm’s most recent earnings call transcript, investor deck, and 10-K risk factors, and ask the model to apply the six levers: where representations outrun telemetry, which forums contradict which, where the dashboard would expose versus protect, and what the surprise audit surfaces first. Structure comes from MindCast; the values come from the reader’s documents; the computation happens in the tool the reader already runs. The first pass yields diagnosis and direction rather than audited numbers — calibration against internal telemetry is the institutional engagement.

VIII. Who Uses the Framework

Registration-lag control changes a different decision for each seat at the table, and the framework earns its keep only where a decision actually changes. Five stakeholders, five decisions:

Boards and audit committees decide when slowing AI investment reads as discipline rather than retreat — the decision AIRC-II.3 predicts at least two cohort boards will formalize by end-2027. The framework supplies the forward question no existing committee charter asks (what will investors believe in six months if today’s trends continue?) and the permission structure the simulations flagged: foresight must reach the board early enough that an updated forecast registers as governance, not repudiation of its own prior approvals.

Chief financial officers, investor relations, and disclosure committees own four of the six levers day to day. The two-clock cadence decides what publishes and when; the representation-surface term decides what stays internal — the dashboard tradeoff in one sentence: externalize only the metrics the governance system can reproduce consistently, because a stable metric builds credibility and a revised one manufactures an exhibit.

Institutional investors and analysts gain a screening variable the multiple does not carry: registration lag. The composite table in Section VI ranks the cohort on it; the metric-substitution finding supplies the diligence question — for every metric management offers, ask what outcome it stopped measuring. Decision changed: separating drawdowns that price sector beta (buyable) from drawdowns that price an opening gap (early).

Securities litigators on both sides read the lever map in reverse. For plaintiffs, the map locates exhibits: cross-forum deltas, revised metrics, and capital commitments that outlived their assumptions. For defendants, the same architecture builds a contemporaneous foresight record that can support a stronger scienter defense — a firm that ran the surprise audit and registered on cadence walks into discovery with its foresight documented. No governance architecture guarantees dismissal; documentation shifts the odds.

Credit analysts and rating agencies hold the cycle’s confirmation switch: equity registers narrative first, credit decides whether the change constrains the strategy set — the sequencing AIRC-II.7 stakes. Spread and rating signals within five trading days of a firm-specific drawdown separate durable financing stress from a valuation argument.

IX. Predictions Registry

AIRC stands for AI Repricing Cycle — the series’ running prediction registry. AI Repricing Cycle registered entries AIRC-I.1 through AIRC-I.6; entries below carry the AIRC-II prefix and register with this paper. Identifiers stay fixed once timestamped — the registry never renumbers a published claim. Five primary entries carry unconditional checkpoints; three extended entries score only if their trigger events occur.

📊 AIRC-II.1 — Gap-lag correlation. June 2026 Idiosyncratic Drawdown Magnitudes, estimated per the Section V protocol, rank-correlate positively (Spearman) with the Section V ex-ante disclosure-gap scores across the eight-firm cohort. Confidence: 60–70 percent. Falsifier: Spearman correlation at or below zero. Checkpoint: scored at protocol execution, no later than December 31, 2026; methodology frozen at publication.

♟️ AIRC-II.2 — First-mover reframe. At least one of the five hyperscalers (Microsoft, Alphabet, Amazon, Meta, Oracle) publicly reframes capital guidance as milestone- or demand-gated by July 31, 2027, presented as measurement discipline, with announcement-week cumulative abnormal return no lower than −5 percentage points. Confidence: 55–65 percent. Falsifier: no hyperscaler reframes by the checkpoint, or the first reframer’s announcement-week abnormal return falls below −5 percentage points.

🏛️ AIRC-II.3 — AI capital oversight formalization. At least two cohort companies publicly disclose a board- or executive-level process connecting AI capital commitments to utilization, demand, or return thresholds by December 31, 2027. Confidence: 55–65 percent. Falsifier: fewer than two firms disclose such a process in filings, governance materials, or earnings communications by the checkpoint.

🔎 AIRC-II.4 — Microsoft (MSFT) validation expansion. Microsoft’s July 29, 2026 earnings materials materially expand disclosure in at least two categories among capacity economics, Copilot adoption, AI revenue contribution, and capital efficiency. Material expansion means a new quantitative metric or numerical comparison not supplied in the prior-quarter materials, counted separately per category. Confidence: 65–75 percent. Falsifier: qualifying expansion in fewer than two categories. Checkpoint: July 29, 2026.

⚖️ AIRC-II.5 — Oracle (ORCL) structure registration. Public disclosures, financing materials, or the Barrows record materially distinguish the allocation of infrastructure ownership and financing between Oracle and its counterparties by December 31, 2026. A qualifying disclosure supplies a dollar, percentage, categorical, or contractual allocation that distinguishes infrastructure ownership, financing responsibility, or utilization risk beyond the July 10, 2026 public baseline. Confidence: 70–80 percent. Falsifier: no qualifying disclosure by the checkpoint.

Extended tier — entries score only if their trigger events occur:

🔁 AIRC-II.6 — Cohort language imitation. After the first successful AIRC-II.2 reframe, at least two peer hyperscalers adopt materially similar milestone, utilization, efficiency, or return-linked capital language within two reporting cycles. Confidence: 60–70 percent, conditional on AIRC-II.2 occurring. Falsifier: fewer than two peers adopt qualifying language within two reporting cycles.

🏦 AIRC-II.7 — Credit confirmation of durable stress. Persistence triggers the score: when a cohort firm suffers a firm-specific weekly equity drawdown exceeding ten percent on AI capital economics and at least 80 percent of the initial abnormal loss remains after twenty trading days, an adverse credit-spread or rating signal will have appeared within five trading days of the drawdown. Confidence: 55–65 percent. Falsifier: a qualifying persistent drawdown shows no adverse credit or rating signal within the five-day window. Checkpoint: event-triggered through December 31, 2027.

📐 AIRC-II.8 — Metric revision penalty. The first cohort firm that materially revises, withdraws, or changes the denominator of a newly introduced AI utilization or return metric without full historical reconciliation suffers a negative abnormal return during the disclosure window — the three trading days from one day before through one day after the disclosure. Confidence: 60–70 percent, conditional on a qualifying revision. Falsifier: the first qualifying revision produces no negative abnormal return. Checkpoint: event-triggered through December 31, 2027.

Dated checkpoints: Microsoft fiscal Q4 earnings, July 29, 2026, 2:30 p.m. Pacific (scores AIRC-I.3 and tests Section IV live); Barrows v. Oracle motion-to-dismiss briefing through December 2026; decomposition publication with this paper’s final version.

X. Conclusion

AI Repricing Cycle ended on the twin law: the crossing date you never watched governs your multiple. The agency clause completes it — the lag you never measured governs your drawdown, and the lag, unlike the calendar, belongs entirely to the firm. Validation appointments cannot be cancelled; firms can arrive at them with registration current, so the market finds nothing to reprice but the sector it was always going to reprice anyway.

AI Repricing Cycle identified the validation calendar; the escape doctrine identifies the control architecture: six levers, each closing a distinct registration delay; one proportionality pricing the tradeoffs; one owner running the system. Firms exit the cycle in the order they register their own economics truthfully — and registration-lag control is how registration gets done on purpose.

Appendix — MindCast Foundations

Eight MindCast works carry load in this paper. Each entry states where and why.

AI Repricing Cycle 2026: Microsoft, Nvidia, Oracle, Meta and the Validation Tests Every AI Layer Now Faces — The diagnosis this paper converts into doctrine. Supplies the validation regime, the crossing calendar, the propagation loop, the Nash capex analysis, and the eight-firm cohort the Section V decomposition measures. Every registration failure the six levers close was first documented there as a market outcome.

Agent Governance Equilibrium — Supplies the paper’s quantitative instrument panel and the runtime-module convention Section VII follows. The Section III gauges: AGE = (A × V × C) / (G × R) — agent autonomy, operational velocity, and organizational complexity over governance capacity and human review — with governance debt accumulating as GD(t) = GD(t−1) + (A × V × C) − (G × R). Governance Resilience, GR = (E × T) / C — escalation effectiveness times organizational trust over complexity — measures the recovery dimension Section I invokes. The framework also secures Section III’s structural floor: an optimizer cannot validate its own objective from inside itself, so review capacity can shrink but cannot reach zero, and the evaluative channel must sit outside the optimizer.

Chicago School Accelerated — The Integrated, Modernized Framework of Chicago Law and Behavioral Economics — Explains why the levers work rather than merely that they do. Coase’s coordination-cost extension grounds Levers 1, 5, and 6 as coordination architecture; Becker’s incentive-exploitation analysis explains narrative drift as optimization inside degraded architecture; Posner’s wicked-learning-environment finding explains why firms cannot wait for legal feedback to correct the drift.

The Dual Nash-Stigler Equilibrium Architecture — Names the two exits from the hyperscaler capex trap that Lever 3 navigates: a new Nash focal point created by a first mover, or a Stigler-side institutional reset imposed from outside. The first-mover framing in Dynamic Capital Allocation applies its dual-equilibrium structure directly.

AI Accountability: When AI Promises Meet the Courts — Documents across four live dockets the audit Lever 5 tells firms to run on themselves first: earnings calls against filings, filings against sales decks. Also supplies the documented record from which Section V’s disclosure-gap scores are defined ex ante.

The Duty to Foresee — AI Deployment Readiness as Prospective Governance, and the Arrival of Agentic Duty of Care — The direct parent of Lever 2. The framework’s forward question — what future disclosure could reasonably surprise investors? — becomes the surprise audit; its Hand-test arithmetic prices the audit’s burden against $725 billion in planned deployment, and its discoverable-knowledge problem defines Lever 6’s representation-surface risk.

Predictive Game Theory Meets the Era of AI — Operationalizing Fudenberg’s Research Agenda with Cognitive Digital Twins — Supplies Section VI’s engine and its equilibrium object. Dynamic Predictive Game Theory treats the repricing cycle as a mutating game whose regimes replace one another, behavioral economics grounds every CDT in documented public behavior rather than assumed rationality, and Adaptive Coherence Equilibrium gives escape its formal definition: coherence held across regime replacements faster than counterparties can exploit the transition.

Foresight Before Disclosure — Established that markets price structural change before formal disclosure, which is the condition making registration lag expensive: by the time a firm registers late, the market has already priced the gap and the plaintiffs have already dated the class period. Registration-lag control operationalizes its central finding as management practice.