MCAI Market Vision: AI Repricing Cycle 2026 —Microsoft, Nvidia, Oracle, Meta and the Validation Tests Every AI Layer Now Faces

AI Repricing Series: Why Capital Now Prices AI Monetization Over AI Announcements and Which Ecosystem Layer Reaches its Validation Point Next

AI Repricing Series. Companion frameworks: Foresight Before Disclosure, Agentic Duty of Care, When AI Promises Meet the Courts and Consumer AI Device series. Predictions registered under the AI Repricing Cycle AIRC-I namespace with commitment timestamps at publication.

Executive Summary

Every major AI company is approaching a scheduled economic validation appointment. Everything that follows derives from that sentence. Capital markets began keeping the calendar in June 2026 — repricing the entire AI economy — and Microsoft merely stands nearest the camera. Investors no longer reward AI announcements alone; capital rotates toward firms demonstrating durable economic returns on unprecedented AI investment, and the June selloff marked the moment markets stopped financing the gap on faith.

Repricing names the observable output; validation names the governing process. AI capital markets have entered a recurring validation regime in which every layer of the ecosystem — enterprise platforms, consumer ecosystems, foundation model developers, cloud providers, compute suppliers, and semiconductor manufacturers — faces scheduled economic checkpoints, and each checkpoint produces a repricing event when narrative meets registered fundamentals. MindCast AI names the observable sequence the AI Repricing Cycle. Microsoft’s recent experience serves as the news hook, not the conclusion.

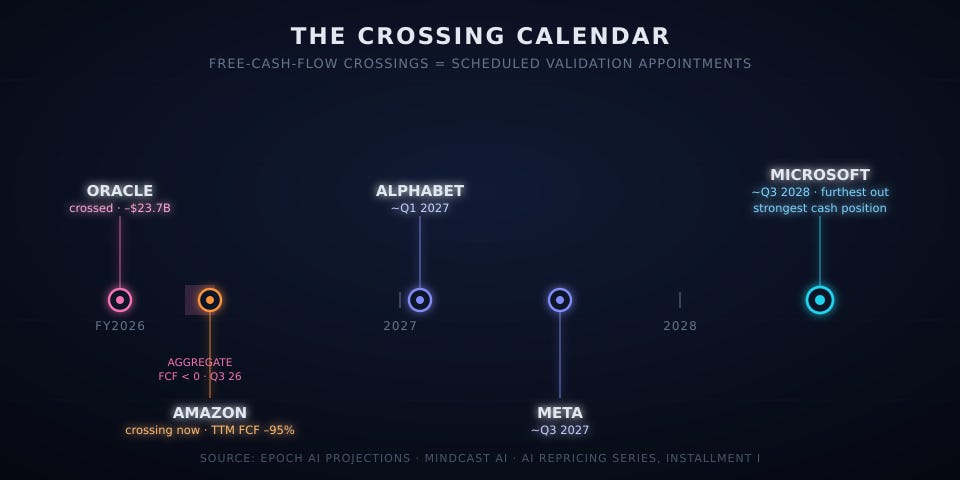

Validation dates are already published. Free-cash-flow crossing projections from Epoch AI supply the regime’s forward calendar: Oracle has crossed (FY2026: –$23.7B), Amazon is crossing now, Alphabet arrives ~Q1 2027, Meta ~Q3 2027, and Microsoft — carrying the cohort’s strongest cash position — not until ~Q3 2028. Aggregate hyperscaler free cash flow turns negative around Q3 2026, driven by capital expenditures growing roughly 70 percent annually against roughly 23 percent operating cash flow growth.

Courts add a finding the market has not yet priced: litigation sequence inverts fundamental-stress sequence. Securities law prices representations, not cash burn — so the cycle’s early lawsuits landed on Oracle’s concealed lease structure and Microsoft’s demand narrative, while firms burning cash openly under sector-wide repricing remain, for now, unsued.

Validation regimes identify no permanent winners or losers. Capital continuously recalibrates as AI matures from capability claims into allocation economics, and firms exit each validation cycle in the order they close the gap between what they deploy and what their institutions truthfully register.

I. Microsoft Is the Current Validation Test, Not the Exception

Microsoft occupies one of the strongest strategic positions in artificial intelligence. Azure, Copilot, GitHub, enterprise software, and deep AI partnerships place the company near the center of enterprise adoption. June 2026 nonetheless delivered the stock’s worst month in almost twenty-six years, followed within days by a securities class action entering its lead-plaintiff phase. Sequence matters here, and the sequence exonerates more than it accuses.

Fundamentals never broke. Azure widened its lead over AWS in the latest Jefferies CIO survey measuring cloud spending intentions for the remainder of 2026. Microsoft signed a five-year AI transformation partnership with consumer health giant Haleon, launched Microsoft Frontier — a $2.5 billion AI deployment business — and built a 6,000-person team targeting enterprise AI adoption. Among the hyperscaler cohort, Microsoft carries the latest projected free-cash-flow crossing date, roughly Q3 2028, meaning the strongest cash position in the group absorbed the cycle’s first legal manifestation.

Scale, not weakness, selected Microsoft first. The largest and most-watched firm in the cohort generates the cleanest class period: the most analysts parsing every demand representation, the most liquid options market registering every capacity signal, and a single-session corrective event in January 2026 that gave plaintiffs a dated break to plead. Microsoft functions as the market’s measurement instrument for the entire cycle — the firm precise enough to measure against.

A validation test differs from a verdict. Microsoft’s July 28 earnings report becomes the cycle’s first test of whether a disclosure-forward posture re-earns a premium multiple (confidence 75–85 percent that the market treats it as exactly that test). History supplies the pattern: dominant technology leaders — IBM in the early 1990s, Microsoft itself after 2000, Apple through repeated “innovation is dead” cycles — absorb expectation recalibrations that later read as entry points rather than epitaphs. The stock’s rebound in the final week of June, alongside a roughly 21–22x forward multiple that sits at its cheapest level since 2023 against a five-year average near 30x, suggests capital has already begun re-underwriting the franchise.

II. The AI Repricing Cycle

Markets have entered a recurring validation regime, and the regime has a definition: the first AI era rewarded announcements; the current era rewards execution. Repricing events are the regime’s output; validation appointments are its engine. Investors now distinguish among five dimensions that earlier trading regimes collapsed into one:

Capital Validation — Can the firm fund its AI buildout from operations, or does the buildout consume the balance sheet?

Product Validation — Does AI capability convert into products customers measurably adopt?

Infrastructure Validation — Do unprecedented capital expenditures generate returns above the cost of capital?

Governance Validation — Does the institution register and disclose its AI economics truthfully and in time? The duty to foresee operates here: firms owe prospective governance to the promises their capital commitments make.

Market Validation — Does the equity multiple reflect demonstrated monetization rather than narrative momentum?

Failure in any dimension can alter investor expectations before formal disclosures emerge — and June 2026 demonstrated the mechanism at sector scale. Microeconomics explains why the fourth dimension now carries disproportionate weight: as frontier model output approaches commodity pricing, capital migrates toward the scarce input — and governance is the scarce input, the finding MindCast established in Why AI Commoditizes Raw Prediction, Why Governance Stays Expensive. Markets pricing audited monetization over announcements are pricing the governance scarcity gap directly.

The numbers behind the cycle. Combined 2026 capital-expenditure plans across Microsoft, Alphabet, Amazon, and Meta reached roughly $725 billion after first-quarter earnings — up 77 percent from 2025’s record (TechTimes). Alphabet guided 2026 capex to $175–185 billion; Amazon flagged approximately $200 billion (Yahoo Finance). Research firm Epoch AI models the squeeze directly from SEC filings: capex across the five major builders grows roughly 70 percent per year while operating cash flow grows roughly 23 percent per year, pushing aggregate free cash flow below zero around Q3 2026. Morgan Stanley expects hyperscalers to borrow roughly $400 billion this year, more than double 2025’s $165 billion (Decoding Discontinuity), and the collective weighting of Meta, Alphabet, Amazon, and Oracle in the Bloomberg U.S. Corporate investment-grade index nearly doubled in the year ending April 2026 (Let’s Data Science). Capital markets, not retained earnings, now finance the buildout.

The crossing calendar. Firm-level timelines diverge sharply, and the divergence converts “recurring cycle” from metaphor into a dated schedule:

Figure 2 — The Crossing Calendar renders the schedule as a timeline for publication. Crossing projections: Epoch AI, June 16, 2026, fit from SEC filings.

Each crossing date marks a validation appointment the market has already booked. Telecom’s 2000 cycle rhymes here — infrastructure capex outrunning cash generation, debt markets financing the gap, litigation lagging drawdowns by roughly six months (confidence in the rhyme: 60–70 percent) — with one difference that has so far contained the damage: today’s borrowers hold monopoly-grade operating cash flows, so the cycle has repriced multiples without breaking balance sheets.

MindCast AI Proprietary Cognitive Digital Twin Foresight Simulations (MP CDT FS) — the multi-actor modeling engine behind this series, disclosed at executive level in the companion appendix — reach the same reading from the inside. Crossing dates operate as validation appointments: markets no longer ask how much AI infrastructure a firm builds; they ask whether the firm converts the buildout into capital-efficient monetization before free cash flow, debt markets, or disclosure pressure force the answer.

Why no firm simply stops spending. Game theory answers the question the crossing calendar begs. The hyperscaler capex race operates as a multi-player Nash equilibrium — the structure MindCast maps in The Dual Nash-Stigler Equilibrium Architecture: no single cloud provider can unilaterally cut capital expenditures without signaling structural surrender in the AI race, handing enterprise workloads to rivals and triggering the very multiple compression the cut was meant to prevent. The payoff matrix locks the cohort into collective motion toward the Q3 2026 aggregate crossing even as each firm’s individual economics deteriorate — an equilibrium trap, not a coordination failure.

Internal feedback architecture compounds the lock-in. Boards stabilized around massive infrastructure commitments because corporate telemetry registered contracted demand and backlog growth while hiding the downstream utilization pause — a pattern MindCast’s cybernetic framework terms Delay Dominance: a system holding steady around a flawed assumption because its own feedback loops conceal the flaw. Escape requires an outside force — a financing constraint, a corrective disclosure, or a reset of the institutional rules themselves — and June’s repricing began to supply exactly that.

III. The AI Ecosystem Landscape

Repricing arrives layer by layer, and each layer faces its own validation question. One table before the detail:

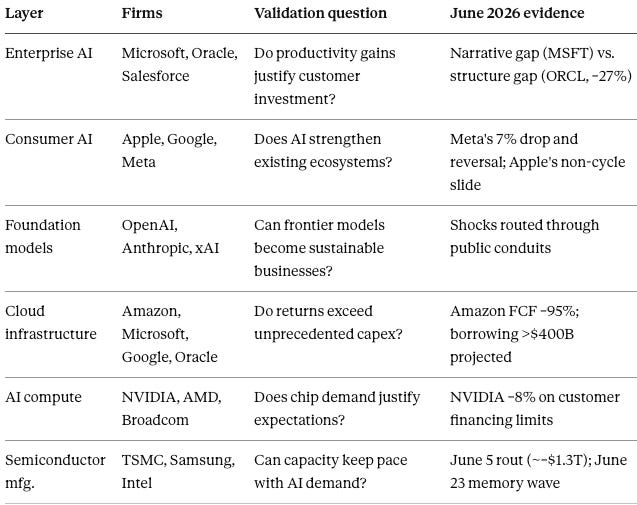

Enterprise AI Platforms — Microsoft, Oracle, Salesforce

Validation question: Can enterprise AI produce measurable productivity gains that justify customer investment?

Microsoft and Oracle bracket the layer’s two failure modes. Microsoft’s June episode ran on a demand-narrative gap; Oracle’s ran on structure. Oracle posted negative $23.69 billion in fiscal 2026 free cash flow (TechTimes), guided to roughly $40 billion in new debt and equity for fiscal 2027, cut 21,000 jobs over the past year, and fell approximately 27 percent in June alone. Prepaid and bring-your-own-hardware portions of Oracle’s large AI contracts now total $75 billion — a structure that shifts capex to customers such as OpenAI while blurring, for outside investors, who actually bears the buildout.

Consumer AI Ecosystems — Apple, Google, Meta Platforms

Validation question: Can AI increase engagement while strengthening existing ecosystems?

Meta supplied the cycle’s single most instructive datapoint. Shares dropped 7 percent on reports of an equity sale to fund the AI buildout, then reversed within days on the announcement of a cloud infrastructure business positioning Meta to sell AI compute against Amazon, Microsoft, and Google. One firm exited its shock by changing its AI story mid-cycle — empirical proof that narrative operates as the cycle’s control variable, and an accidental execution of the governance posture MindCast’s Agentic Duty of Care framework prescribes deliberately (confidence 65–75 percent).

Apple plays a double role, and the doubling demonstrates the cycle’s maturation. Apple’s AI litigation — the Tuckersecurities action and Landsheft consumer action — belongs to the earlier capability era: claims about intelligence that did not yet exist. Apple’s June 2026 stock slide, by contrast, belongs to no AI-governance category at all; it ran on chip component costs forcing MacBook and iPad price increases, a spillover from semiconductor inflation rather than governance debt. One firm, two eras, and a built-in falsification boundary: a cycle thesis that cannot exclude Apple’s 2026 drop from the cycle would explain everything and therefore nothing.

Alphabet absorbed a third mechanism — the repricing of an asset no balance sheet registers. An $84.75 billion equity offering, one of the largest in corporate history, priced on June 1 alongside a $10 billion Berkshire Hathaway private placement; the stock fell 6 percent over the following month. Compounding the dilution, Gemini co-lead Noam Shazeer departed for OpenAI and Nobel laureate John Jumper left DeepMind for Anthropic, handing the market a live experiment in pricing AI talent. Model capability lives in people the disclosure regime cannot see, and June proved markets reprice the invisible asset anyway.

Foundation Model Developers — OpenAI, Anthropic, xAI

Validation question: Can frontier models become sustainable businesses rather than perpetual capital projects?

Private structure hides no one from the cycle; it merely reroutes the shock. OpenAI’s economics surface through Oracle’s $75 billion prepaid-hardware exposure and counterparty concentration. Anthropic’s regulatory episodes reach markets through compute partners and export-control headlines. The cycle’s largest AI liabilities sit off public markets, which makes the conduits — the public firms carrying private-lab exposure on their balance sheets — the instruments through which repricing reaches the model layer.

Cloud AI Infrastructure — Amazon, Microsoft, Google, Oracle

Validation question: Can hyperscale infrastructure generate sufficient returns on unprecedented capital expenditures?

Amazon now occupies the layer’s most exposed seat. Trailing free cash flow collapsed 95 percent to $1.2 billion, per the company’s own Q1 earnings presentation (Yahoo Finance); Q1 capex of $44.2 billion ran against $26 billion in operating cash flow (Investing.com); and the AWS demand narrative structurally parallels the Azure representation that generated Microsoft’s class period. Amazon crosses the free-cash-flow line during the exact quarter aggregate hyperscaler cash flow goes negative.

AI Compute — NVIDIA, AMD, Broadcom

Validation question: Will demand for AI chips continue to justify current expectations?

NVIDIA carries derivative exposure: its own operations gush cash and its latest quarter set revenue records, yet shares shed nearly $330 billion in market value in a single June session and sit roughly 18 percent below their May record (Yahoo Finance; TIKR) as customers approached financing limits. Vendor-financing questions already circulate. If hyperscalers hit borrowing constraints and trim orders, NVIDIA’s demand curve bends with them — the structural position Cisco occupied in 2000, with the difference that NVIDIA’s balance sheet arrives at the test unlevered.

Semiconductor Manufacturing — TSMC, Samsung, Intel

Validation question: Can manufacturing capacity and process leadership keep pace with AI demand?

June delivered two waves. Broadcom’s June 3 guidance miss triggered a rout that erased roughly $1.3 trillion in semiconductor market value within days (Yahoo Finance). June 23 relocated the epicenter to the memory complex: Micron fell more than 9 percent ahead of earnings, Samsung and SK Hynix dropped more than 12 percent each, and South Korea’s Kospi plunged as much as 10 percent (Forbes). Leverage and cyclicality make the manufacturing layer the cycle’s amplifier — the first casualty of any credit tightening and the loudest signal when repricing goes global.

IV. Why Repricing Travels Across the Ecosystem

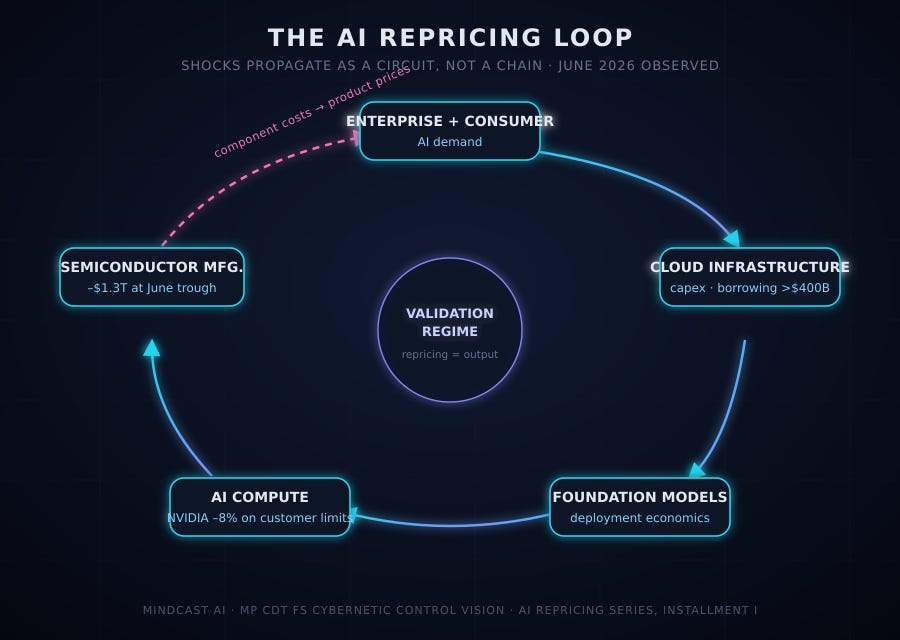

Repricing propagates because the AI economy functions as an interconnected capital ecosystem rather than a collection of independent firms. Propagation runs as a loop, not a chain — the cybernetic distinction matters, because a chain ends while a loop feeds back (Figure 1 — The AI Repricing Loop; companion graphic):

MindCast AI Proprietary Cognitive Digital Twin Foresight Simulation (MP CDT FS) Cybernetic Control Vision simulations model the same circular topology, with every actor class updating every other — no company acts alone. June 2026 then supplied live confirmation:

Enterprise adoption doubts repriced cloud demand expectations.

Cloud capex anxiety repriced foundation-model deployment economics.

Deployment doubt repriced compute demand — NVIDIA’s June drawdowns tracked customer financing limits, not its own results.

Compute repricing hit the memory and manufacturing complex hardest, shedding roughly $1.3 trillion in semiconductor market value at the trough (Yahoo Finance).

Manufacturing stress fed back into platform companies through component costs — Apple’s price increases closed the loop, proving the topology circular rather than linear.

Federal Reserve policy amplified every link: Chairman Warsh’s inflation-control posture raised the discount rate on distant AI cash flows at precisely the moment those cash flows moved further out. Cross-layer dependency amplifies recoveries symmetrically — Meta’s cloud announcement lifted sentiment across the stack within a session.

Economic theory predicted the fragility. MindCast’s Trust as AI Infrastructure shows how narrative-driven booms mask underlying transaction costs until speculative confidence collides with a measurable reality — here, net-negative aggregate free cash flow. June marked the collision, and the propagation loop above traces trust repricing through every layer that had borrowed against it.

Contact mcai@mindcast-ai.com to partner with us on Predictive Game Theory AI in Law and Behavioral Economics. To deep dive on MindCast works upload the URL of this publication into any LLM (preferably Google AI mode/Gemini, Claude, ChatGPT) and prompt ‘reconstruct MindCast framework with three degrees of cited sub links.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure. We stress-tested our AI system for this publication by simulating the Super Bowl and the World Cup. Super Bowl LX — AI Simulation vs. Reality | Predictive Game Theory + Behavioral Economics Cognitive Digital Twin Foresight Simulations in the World Cup

V. The Docket Already Moved

Courts began processing the cycle before equity markets named it. MindCast’s AI Accountability series (When AI Promises Meet the Courts) maps four live proceedings that together trace the cycle’s legal signature:

Tucker v. Apple and Landsheft v. Apple: capability-era claims — securities and consumer actions alleging the marketing of intelligence that did not exist (MindCast: Apple’s AI Illusion).

Tesla FSD litigation: the hinge — categorical capability claims hardening into hardware-substrate liability once software promises met physical Hardware 3 limits (MindCast: Tesla’s Self-Driving Revolt).

Barrows v. Oracle (No. 1:26-cv-00127-JLH, D. Del., filed February 3, 2026): allocation-era claims — approximately $248 billion in off-balance-sheet lease commitments allegedly concealed beneath “asset-light” framing, with $1.87 billion in class-period insider sales supplying scienter, the knowledge element securities fraud requires (MindCast: Oracle, OpenAI, and the Capacity Economy).

The Microsoft shareholder suit (filed June 2026, lead-plaintiff notices now circulating): governance-debt claims — an Azure demand narrative allegedly maintained while capacity was rationed, corrected in a single January session (MindCast: Foresight Before Disclosure).

Mismatched clocks explain the docket’s ordering. Markets reprice the AI stack in milliseconds; courts run on multi-year clocks — and institutions operating on different loop speeds, the dynamic MindCast models in How MindCast Evolves the Structural Gaps in Classical Nash Game Theory, mean securities litigation necessarily lags the drawdown while binding liability to old corporate announcements. Courts adjudicating 2025 representations against 2026 fundamentals show no judicial slowness; systems built on different clock speeds behave exactly this way, per The Computational Era Operationalizes Cybernetics and Predictive Game Theory, and the lag converts every crossing date in Section II into a future litigation reference point. Whatever a firm represents in the quarter before its crossing becomes the exhibit in the complaint filed the year after.

Read together, the docket teaches the doctrine equity analysts have not yet absorbed: disclosing the spending does not immunize; concealing the structure creates the exposure. Oracle guided its burn openly and got sued anyway, because liability attached to the lease structure and insider sales, not the capex line. Microsoft’s disclosures were voluminous, and the suit attached to the alleged gap between narrative and allocation. Litigation sequence therefore inverts fundamental-stress sequence — the firm with the latest cash-flow crossing was sued four months after the firm that crossed first, and both were sued while faster-deteriorating peers were not.

June’s sector-wide selloff extends the doctrine with a corollary (confidence 70–80 percent): systemic repricing is litigation-sterile. A securities class period requires a firm-specific misrepresentation meeting a firm-specific corrective event; sector beta supplies neither. Amazon, Alphabet, and Meta fell without being sued because the market repriced a macro thesis, not their individual representations. MP CDT FS Disclosure Vision reaches the same corollary independently: simulated systemic selloffs stay litigation-sterile until a company-specific representation, allocation gap, or corrective event creates a pleadable class-period break. Exposure activates only when a firm-specific disclosure break arrives — which converts the crossing calendar in Section II into a litigation watch list.

The migration thesis registered in the accountability series — AI litigation shifting from capability claims (did the intelligence exist?) to allocation claims (who got the compute, and who knew?) — already carries falsification contracts through 2028. The Repricing Series inherits that substrate rather than rebuilding it.

VI. The MindCast AI Framework

Three prior MindCast frameworks supply the analytical foundation, and one sibling series supplies the structural rhyme.

Foresight Before Disclosure established that markets increasingly price structural change before formal disclosures — the third phase of AI competition, where forecasting the institution outcompetes building the model. The Repricing Cycle is that thesis observed at sector scale: June’s selloff priced governance debt months before any regulator or court compelled its registration.

Agentic Duty of Care defines the governance boundary precisely, and the boundary bears stating to avoid overclaiming: deliberate foresight governance converts shock plus lawsuit into shock alone. Governance quality dampens the idiosyncratic component of a repricing event and largely neutralizes the litigation tail, but no internal control system hedges sector beta. Firms implementing prospective governance still fell in June; they fell without manufacturing class periods.

Scale converts Agentic Duty of Care from advisory to actuarial. The framework adapts Judge Learned Hand’s classic negligence test — liability attaches when the burden of a precaution costs less than the probability of harm multiplied by its magnitude — to AI-era commitments. Run that test against the cycle’s numbers. The burden side — honest utilization telemetry, simulated demand scenarios, capacity representations disciplined by internal foresight records — costs a rounding error against roughly $725 billion in planned annual deployment. The loss side now carries realized instances rather than estimates: a 27 percent monthly drawdown at Oracle, a manufactured class period at Microsoft, $1.3 trillion in semiconductor value shed within days. Wherever the precaution runs trivially cheap against realized losses, failure to foresee becomes negligence in prospective-governance terms — and June’s repricing priced that negligence months before any court will adjudicate it.

Capital commitments themselves now function as agentic acts: autonomous once initiated, compounding across multi-year feedback loops, and no easier to recall than a deployed agent. The duty to foresee accordingly migrates from the deployment decision to the capital-allocation representation, mirroring the docket’s own migration from capability claims to allocation claims (confidence: 70–80 percent). Every promise attached to the buildout is a foreseeability event the market — and eventually the court — will score.

MP CDT FS Integrity Vision quantifies the boundary. Governance cannot immunize firms from sector beta, but simulated firms with coherent internal telemetry, disciplined capital-allocation records, and synchronized investor communications narrow the gap between organizational reality and market expectations — and narrower gaps produce shorter repricing cycles (confidence: 65–80 percent).

Cognitive Digital Twins evaluate institutional coherence across capital allocation, execution, governance, innovation, and market positioning — the instrument the simulations in Section VII deploy at layer level.

The Consumer AI Device Series stands as this series’ cousin. The device series modeled nine institutions at the product and routing layer and found its governing variable inside the firms themselves: whether AI devices commoditize or concentrate resolves through each institution’s own behavioral patterns, not outside forces. The Repricing Series applies the same discovery at the capital layer, where the governing variable — whether markets price a firm on narrative or on registered fundamentals — likewise resolves through each institution’s own disclosure discipline. One methodology, two layers, and a continuity claim worth registering now: the accountability series’ standing forecast that the largest operators become valued as financing systems rather than software systems (65–75 percent) is the Repricing Cycle thesis stated from the litigation side. Installment I begins with a validated prior, not a cold start.

VII. MindCast AI Proprietary Cognitive Digital Twin Foresight Simulations (MP CDT FS): Layer Outputs

The paper publishes executive outputs only; full MP CDT FS data remain proprietary and available through institutional engagement.

MP CDT FS simulations run at the layer level rather than the firm level, matching the cycle’s actual unit of repricing. Simulation architecture, actor classes, and executive findings appear in the appendix.

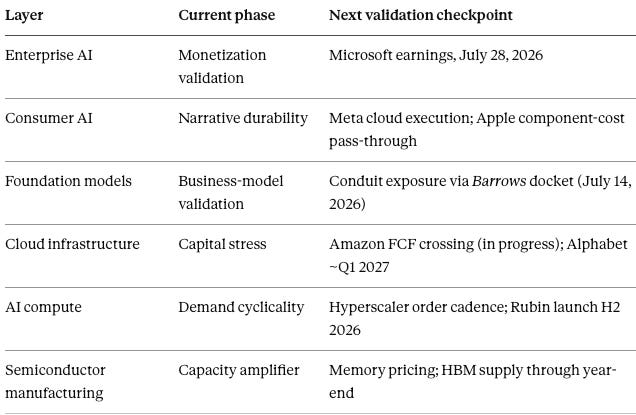

Enterprise AI — Probability enterprise AI spending accelerates or stabilizes rather than slows through the next four quarters: 70–80 percent. Jefferies CIO survey data showing durable cloud spending intentions anchors the high end.

Consumer AI — Likelihood AI becomes a durable device-upgrade and engagement driver rather than a feature tax: 60–75 percent. Meta’s narrative reversal supports the mechanism; Apple’s component-cost squeeze caps the band.

Foundation Models — Probability of consolidation versus continued fragmentation across frontier labs: 65–80 percent toward consolidation, driven by compute financing limits at the conduit firms rather than model quality convergence.

Cloud Infrastructure — Likelihood capital expenditures remain elevated through the next investment cycle despite the free-cash-flow squeeze: 80–90 percent. Borrowing capacity, not intent, becomes the binding constraint.

AI Compute — Probability compute demand remains strong but turns more cyclical as customers optimize workloads and financing: 65–80 percent. NVIDIA’s derivative exposure defines the cyclicality mechanism.

Semiconductor Manufacturing — Probability advanced-node and high-bandwidth-memory capacity remains the strategic bottleneck: 80–90 percent. June’s memory-complex epicenter demonstrated the layer’s amplifier role in both directions.

VIII. Predictions Registry — AIRC-I

AIRC stands for AI Repricing Cycle; AIRC-I marks predictions registered in this first installment, and future installments extend the sequence.

Layer Health Dashboard. One snapshot before the detailed registry — each layer’s current regime phase and its next scheduled validation appointment:

Falsifiable registry entries carry the AIRC-I namespace, commitment-timestamped at publication. Structural expectations follow separately and claim no falsification credit.

AIRC-I.1 — Next allocation defendant. Amazon or Alphabet becomes the next allocation-category securities defendant among the currently unsued hyperscaler cohort before the end of 2027, with Amazon the more probable target given its in-progress free-cash-flow crossing and an AWS demand narrative structurally parallel to Azure’s. Confidence: 60–70 percent. Falsifier: the next major AI securities action pleads a capability predicate, or names a firm outside the hyperscaler cohort.

AIRC-I.2 — Meta reversal durability. Meta’s AI-cloud narrative survives through its ~Q3 2027 free-cash-flow crossing without a firm-specific corrective disclosure event. Confidence: 55–65 percent. Falsifier: a corrective event tied to cloud economics or AI capex representations before the crossing.

AIRC-I.3 — Microsoft re-rating. Microsoft’s forward earnings multiple recovers above 25x within two quarters of the July 28, 2026 earnings report, validating disclosure-forward posture as multiple-restorative. Confidence: 60–70 percent.Falsifier: multiple remains below 25x through Q1 2027 despite in-line or better results.

AIRC-I.4 — Compute derivative shock. Any material hyperscaler order trim produces an NVIDIA drawdown exceeding the trimming firm’s own, confirming the derivative-exposure mechanism. Confidence: 55–65 percent.Falsifier: order-trim events produce proportionally smaller NVIDIA reactions.

AIRC-I.5 — Utilization disclosure shift. AI utilization and return-on-investment metrics become materially more common in investor communications across the cohort. Confidence: 60–75 percent. Falsifier: earnings communications through 2027 show no measurable increase in utilization or AI-ROI reporting.

AIRC-I.6 — Conduit transmission. Public counterparties increasingly transmit private foundation-model risk into market pricing, observable in disclosure language and analyst treatment of Oracle, Microsoft, Amazon, and Google. Confidence: 70–85 percent. Falsifier: private-lab stress events produce no measurable pricing or disclosure response at the public conduits.

Dated checkpoints inherited from the accountability docket: the Barrows v. Oracle consolidated complaint (July 14, 2026) and motion-to-dismiss briefing (through December 2026); the Microsoft suit’s lead-plaintiff consolidation; Microsoft earnings (July 28, 2026).

Structural expectations (directional context, not registry entries):

Repricing rotates across multiple firms and layers rather than concentrating on one company.

Investors increasingly reward demonstrated AI monetization over AI announcements.

Governance quality becomes a visible, priced component of AI-firm valuation.

IX. Conclusion

Microsoft deserves attention because it illustrates the dynamics reshaping AI markets, not because it represents an isolated weakness — the firm with the cohort’s strongest cash position and latest validation deadline absorbed the cycle’s first measurement precisely because it offered the cleanest instrument. The AI Repricing Cycle reflects a maturing industry in which investors continually test whether extraordinary capital commitments produce extraordinary economic value, layer by layer, on a calendar the free-cash-flow crossings have already published.

The more enduring question is not whether Microsoft, NVIDIA, Apple, Google, OpenAI, or another leader experiences the next repricing event. It is which layer faces its next economic test, how the shock propagates through an interconnected capital ecosystem, and which institutions close their registration lags — the gap between internal organizational reality and external market expectations — before the market or the docket closes those lags for them. Repricing is the regime’s output; validation is its engine — and the engine now runs on a published calendar. The Consumer AI Device Series ended on the observation that the loop you never see governs your default. The capital layer obeys the twin law: the crossing date you never watched governs your multiple, and firms exit the cycle in the order they register their own economics truthfully.

Appendix — MP CDT FS: Simulation Architecture and Executive Outputs

A. Architecture. MP CDT FS models the AI Repricing Cycle as interacting Cognitive Digital Twins across five actor classes: institutional CDTs (fifteen AI firms spanning all six layers), investor CDTs (long-only institutions, hedge funds, sell-side analysts, retail capital, credit markets), customer CDTs (enterprise CIOs, enterprise CFOs, consumers), regulatory CDTs (SEC, FTC, DOJ, European regulators), and a Market Dynamics CDT carrying rates, liquidity, credit, and sector rotation. Each CDT updates the others — no company acts alone in the simulation, matching the loop topology Section IV documents in the observed market.

Six Vision functions interrogate the network, each asking one question: which layer validates first (Economics), which narrative breaks first (Disclosure), which institution holds coherence under pressure (Integrity), which representations attract legal scrutiny (Regulatory), which feedback loops amplify instability (Cybernetic Control), and which equilibrium keeps firms spending despite margin pressure (Chicago Strategic Game Theory).

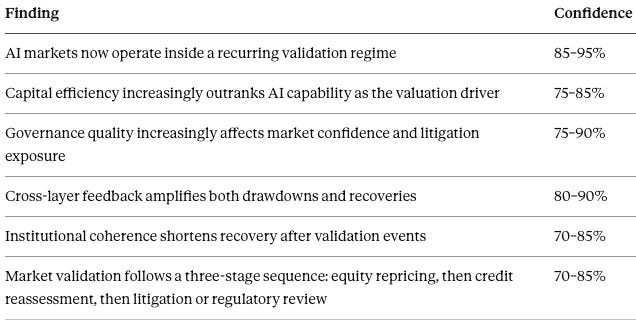

B. Executive findings. Simulation runs converged on six findings, stated with confidence bands:

The sixth finding supplies a monitoring variable this series will track going forward: credit spreads on hyperscaler debt function as the early signal that an equity repricing will hold, because credit markets price free cash flow and leverage while remaining unmoved by AI narrative.

C. Findings the simulations did not expect. Four outputs ran against intuition. Microsoft’s strength increased its exposure — the most liquid, most-watched firm became the cleanest measurement instrument. NVIDIA’s risk is derivative, not internal — customer financing limits matter more than NVIDIA execution in the next validation window. Apple helps falsify the thesis — component-cost pass-through sits outside the cycle, which keeps the framework from explaining everything and therefore nothing. Credit markets may lead rather than lag — equity moves first, but credit constraints decide whether AI spending remains sustainable.

D. Predictions. Simulation-derived predictions carry the paper’s AIRC-I namespace — one ID per claim across the corpus — and appear with falsifiers and checkpoints in Section VIII. Regime persistence (the first executive finding) remains a finding rather than a registry entry: a regime’s existence cannot fail a dated checkpoint, and the registry admits only claims that can.

E. Disclosure boundary. The appendix discloses executive simulation findings. Firm-level CDT matrices, investor response trees, customer adoption-state simulations, regulatory escalation maps, recursive iteration logs, sensitivity testing, and scoring rubrics remain proprietary MindCast AI research available through institutional engagement.