MCAI Market Vision: Luxury Concentration as Litigation Context — Why Compass’s Post-Merger Market Position Reframes the NWMLS Dispute

April 2026 Seattle Luxury Ranking Reveals 90% Post-Merger Origination Concentration — Stage 1 of the Funnel Behind Compass’s Litigation Posture, Layer 3 Acquisition Premium, and State Enforcement Risk

Recent works: MindCast publication The Motion Compass Filed and the Architecture It Could Not Address | MindCast publication Two NWMLS Records, One Foster-Skillman Team | MindCast publication The Compass-Reffkin Consumer Policy Center Quote-Card Specimen

Executive Summary

Seattle’s luxury real-estate market increasingly reveals the economic structure underlying the conflict between Compass and the Northwest Multiple Listing Service (NWMLS). Independent trade publications now show Compass repeatedly occupying a disproportionate share of elite inventory across the Seattle metropolitan market. Compass simultaneously continues advancing private exclusives — listings marketed off the multiple listing service through internal brokerage channels before public exposure — together with internal routing architectures and anti-MLS litigation positions through Compass v. NWMLS in the Western District of Washington. A multiple listing service (MLS) is the cooperative database licensed brokerages use to share listings; the cooperative model produces the price discovery and broad distribution that competitive residential markets depend on.

The overlap matters because litigation posture and inventory economics no longer operate independently. Luxury concentration changes incentive geometry. High-end inventory increases the value of controlling buyer access, pre-market visibility, and intra-brokerage transaction routing. Once inventory concentration reaches sufficient scale, restricted distribution models become economically rational rather than ideologically motivated.

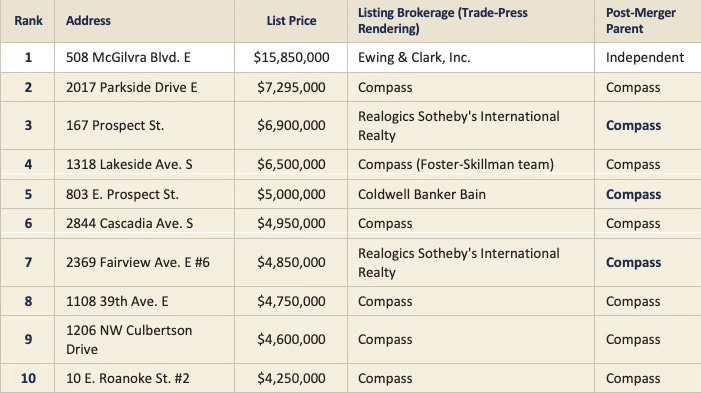

Seattle Agent Magazine’s recent ranking of the ten most expensive new Seattle listings during April 2026 functions as a neutral validation artifact for the broader structural argument the MindCast Artificial Intelligence (MindCast AI) corpus advances. The ranking renders nine of ten listings under the post-merger Compass corporate parent, distributed across three brand presentations — Compass, Sotheby’s International Realty, and Coldwell Banker — that trade press continues to render as separate brokerages four months after the January 9, 2026 close of the Compass-Anywhere merger.

The ranking unintentionally documents the market preconditions necessary for the architecture MindCast publication Two NWMLS Records, One Foster-Skillman Team previously described:

1. Concentrate elite inventory.

2. Control access pathways to elite inventory.

The dispute therefore extends beyond ordinary policy disagreement over listing syndication rules. The conflict increasingly resembles a structural contest over who governs market visibility architecture inside the Seattle housing ecosystem — and inside every regional ecosystem where the post-merger entity’s brand portfolio operates.

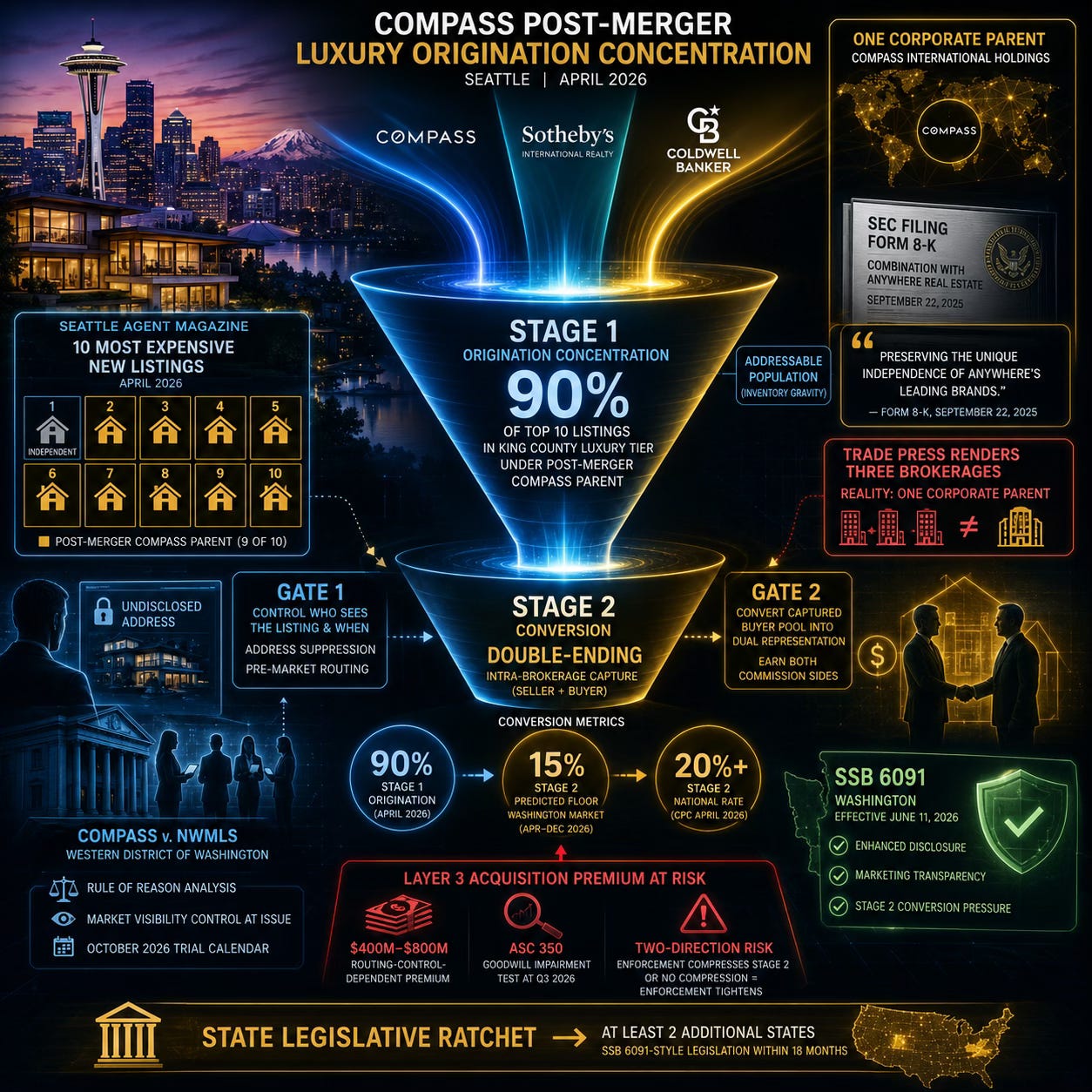

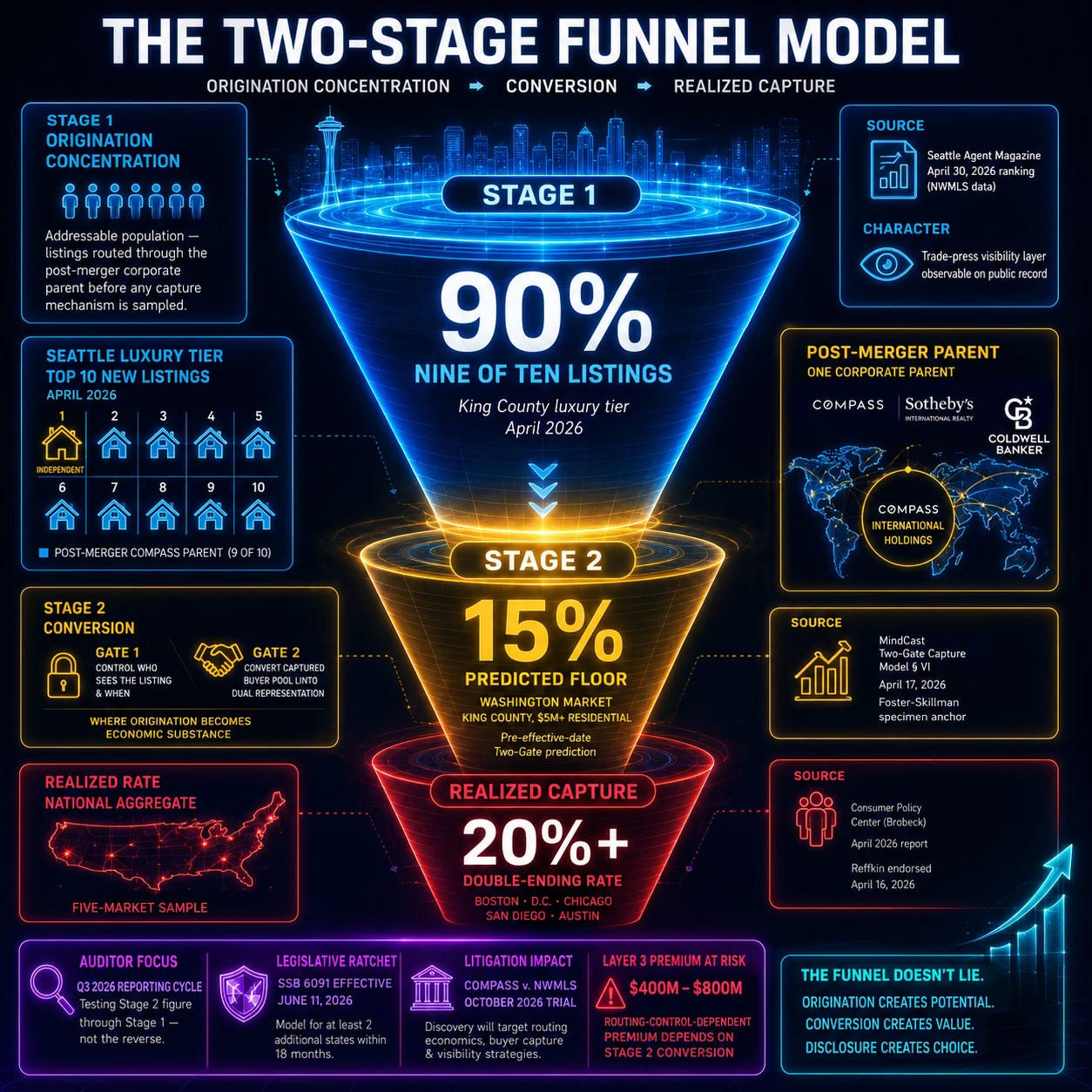

The publication formalizes a Two-Stage Funnel Model the prior MindCast corpus has been assembling without naming. Stage 1 is origination concentration — the fraction of elite inventory routed through the post-merger corporate parent. Stage 2 is conversion— the fraction of Stage 1 inventory that closes with the parent on both sides of the transaction through intra-brokerage capture (double-ending, the practice of representing both seller and buyer in a single transaction and earning both commission sides). The April ranking measures Stage 1 at 90% in the King County luxury tier. The Two-Gate Capture Model’s Section VI prediction — discussed in Section IV below — sets the Stage 2 Washington-market floor at 15%. The Consumer Policy Center (CPC) national measurement places Stage 2 realized capture at 20%+ across five sampled markets.

Origination concentration without conversion is unmonetized. The Layer 3 acquisition premium (the routing-control-dependent portion of the post-merger valuation, defined fully in Section VII), the rule-of-reason litigation defense (the antitrust analysis under which restraints are evaluated by weighing procompetitive justifications against anticompetitive effects, in contrast to per se illegality), the Accounting Standards Codification (ASC) 350 goodwill impairment analysis, and the state-level Unfair or Deceptive Acts or Practices (UDAP) enforcement predicates all sit at Stage 2. Stage 1 is a leading indicator. Stage 2 is the economic substance.

The April ranking is informative because it documents the addressable population at the top of the funnel under conditions where the post-merger parent has just become operational. Stage 2 measurement at scale arrives during the post-June 11, 2026 Substitute Senate Bill (SSB) 6091 enforcement window — Washington’s real estate marketing transparency statute, signed March 17, 2026 and effective June 11, 2026 — and the Q3 2026 Compass reporting cycle. The funnel structure organizes the next twelve months of measurement.

I. Governing Insight

Compass’s litigation posture cannot be evaluated separately from its inventory concentration strategy.

Traditional brokerage disputes center on commission rates, recruiting, marketing, or platform access. The Compass–NWMLS conflict operates at a deeper layer: control over market exposure timing, buyer routing, and visibility sequencing. Luxury inventory concentration changes the economics of distribution itself.

A brokerage operating heavily in the $5 million to $15 million segment gains disproportionately from delayed public exposure, controlled pre-market access, internal buyer matching, double-ending opportunities, and selective inventory visibility. Each incentive strengthens as concentration increases.

The Seattle Agent Magazine rankings therefore matter because they provide independent confirmation that the post-merger Compass entity has achieved meaningful penetration into Seattle’s elite inventory layer. Neutral trade-publication validation increases evidentiary significance because the concentration evidence no longer depends on litigation allegations, critics, or adversarial framing. The ranking effectively supplies a missing empirical bridge between Compass’s public rhetoric and the economic architecture underlying the litigation.

Contact mcai@mindcast-ai.com to partner with us on Predictive Game Theory in Law and Behavioral Economics. To deep dive on MindCast work in Cognitive AI upload the URL of this publication into any LLM and prompt ‘parse MindCast framework with three degrees of cited sub links.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure.

II. The Specimen — Nine of Ten

Seattle Agent Magazine published its ranking of the ten most expensive new Seattle listings during April 2026, sourced from NWMLS data. The ranking is publicly accessible at seattleagentmagazine.com.

Ten listings appear in the ranking, attributed by trade press as follows:

Nine of ten. One independent at the top of the distribution, with the remaining nine listings tied to the post-merger Compass corporate-parent layer through direct brokerage identity, brand ownership, or franchise affiliation.

The price distribution adds an additional analytical observation. The single independent listing — Ewing & Clark at $15.85 million — sits more than $8.5 million above the second-place listing. Ranks 2 through 10 cluster between $7.295 million and $4.25 million, and every listing in the cluster ties back to the post-merger Compass corporate-parent layer. The luxury tier between $4 million and $8 million in April 2026 King County originated entirely inside the post-merger entity at the trade-press visibility layer. The Stage 1 origination concentration figure therefore operates not against the full ultra-luxury distribution but against a tighter sub-tier the post-merger entity dominates with no observed independent presence in the same window.

The corporate-structure facts underlying the table are public. Compass announced the Anywhere acquisition in September 2025. Stockholders of both companies voted overwhelmingly to approve the merger on January 7, 2026. The merger closed January 9, 2026 with Robert Reffkin as Chairman and Chief Executive Officer of the combined entity under Compass International Holdings. Anywhere’s brand portfolio — including Sotheby’s International Realty and Coldwell Banker — operates as preserved brand identities under combined corporate control.

The trade-press rendering does not fully reflect the post-merger corporate-parent structure. Seattle Agent Magazine presents Sotheby’s, Coldwell Banker, and Compass as three brokerages on a top-10 ranking four months after the entities became one company.

A scope clarification belongs at the top of the analysis. The publication does not assert coordinated conduct among separately branded operating entities. Realogics Sotheby’s International Realty operates as a Pacific Northwest franchisee of the Sotheby’s International Realty brand under Anywhere’s franchise system. Coldwell Banker Bain operates as a regional brokerage affiliated with the Coldwell Banker brand under Anywhere. Each operating entity carries its own ownership structure, its own operational management, and its own profit-and-loss responsibility. Common ownership at the brand-licensing layer does not establish operational integration at the local-brokerage layer.

The analytical point is incentive geometry, not coordination. Common ownership at the parent level changes the economic incentives governing routing architecture, data aggregation, and strategic visibility management — regardless of whether operating entities coordinate at the transaction layer. The 90% figure measures origination concentration at the corporate-parent layer where the Layer 3 acquisition premium, the goodwill impairment analysis, and the regulatory enforcement predicates operate. The figure does not measure, and the publication does not assert, coordinated market conduct at the operating-entity layer where independent franchisee and affiliate decisions continue to govern transaction-level activity.

The Foster-Skillman team — the named economic unit on both primary-source records in MindCast publication Two NWMLS Records, One Foster-Skillman Team — appears at #4 in the April ranking. The same team operates simultaneously on the original Two-Gate evidentiary record (Triptych at $65,000,000 with Gate 1 address suppression, and 4640 95th Avenue NE at $7,775,000 with Gate 2 intra-brokerage capture) and on the April aggregate concentration record. The named economic unit bridges the team-credential layer and the aggregate-layer specimen at the same Washington county in the same statutory transition window.

III. The Two-Gate Capture Model and Luxury Inventory Economics

MindCast publication Two NWMLS Records, One Foster-Skillman Team named the Two-Gate Capture Model as a corpus analytical construct: a two-mechanism architecture in which Gate 1 controls who sees a listing and when (through pre-market routing and address suppression on listings inside the cooperative database), and Gate 2 converts the captured buyer pool into a transaction where the brokerage earns both seller-side and buyer-side commissions through intra-brokerage dual representation. The publication argued that private-exclusive strategies require two reinforcing forms of control: inventory concentration and buyer-access control. Luxury concentration now provides observable evidence for Gate 1 at the aggregate-tier layer the original publication’s Section VI measurement framework anticipated.

Without meaningful inventory gravity, private networks fail because buyers cannot justify remaining inside restricted ecosystems. Once a brokerage accumulates sufficient elite inventory, however, the economic logic changes dramatically.

Self-reinforcing dynamics begin operating: elite inventory attracts elite buyers, elite buyers attract elite agents, elite agents attract additional inventory, internal routing becomes more valuable, and public-market exposure becomes less strategically attractive. Private exclusives therefore become more than a marketing preference. Private exclusives become a distribution optimization strategy.

The Seattle luxury rankings reveal why the Compass conflict escalated nationally. Market structure changes once inventory concentration crosses a threshold where controlling access pathways becomes more profitable than maximizing open-market exposure. Behavioral economics intensifies the dynamic. Seller psychology in elite markets differs from commodity-market psychology. Privacy signaling, exclusivity signaling, insider access, and perceived buyer quality all influence decision-making. Compass’s luxury concentration increases its ability to operationalize behavioral dynamics through brokerage-controlled visibility architecture.

The Two-Gate model therefore no longer reads as abstract theory. Seattle luxury concentration increasingly validates the underlying economic mechanism at the aggregate-tier layer the team-credential specimens documented at the transaction layer.

IV. The Two-Stage Funnel Model — Origination, Conversion, and the 90% / 15% / 20% Stack

The prior MindCast corpus has been assembling a two-stage funnel architecture without naming it as a unified model. The April ranking forces the formalization. Origination and conversion operate as sequential stages. Origination concentration without conversion is unmonetized inventory. Conversion without origination concentration is bounded by the inventory the brokerage controls. The Layer 3 acquisition premium, the rule-of-reason litigation defense, the ASC 350 goodwill impairment analysis, and the state-level Unfair or Deceptive Acts or Practices enforcement predicates all sit at Stage 2. Stage 1 is the leading indicator. Stage 2 is the economic substance.

Stage 1 — Origination Concentration

Stage 1 measures the fraction of elite inventory routed through the post-merger corporate parent. Stage 1 captures the addressable population for downstream conversion. The mechanism operates through agent recruitment, brand-portfolio aggregation, and pre-market routing infrastructure.

90% — Aggregate post-merger brand-portfolio origination concentration. Nine of ten April Seattle ultra-luxury listings tie back to the combined Compass-Anywhere corporate-parent layer. The figure is observable at the trade-press visibility layer in a single regional market in a single month. The figure measures the population of listings whose buyer-side representation is available for intra-brokerage capture before any capture mechanism is sampled. Stage 1 produces a marketing flywheel, a pre-market exposure window, and a visibility-control posture in litigation. Stage 1 alone produces no per-transaction commission uplift.

Stage 2 — Conversion Through Intra-Brokerage Capture

Stage 2 measures the fraction of Stage 1 inventory that closes with the parent on both sides of the transaction through intra-brokerage capture (double-ending). Stage 2 is the revenue-extraction mechanism that converts origination concentration into the per-transaction economic uplift the post-merger valuation depends on. The Two-Gate model already named the dependency. Gate 1 controls who sees the listing and when. Gate 2 converts the captured buyer pool into a transaction where the parent earns both sides.

15% — Predicted Washington-market Stage 2 conversion floor. The Section VI prediction in MindCast publication Two NWMLS Records, One Foster-Skillman Team sets the falsification floor at 15% for Compass-listed residential transactions above $5,000,000 in King County during April 2026 through December 2026. The threshold is calibrated below the CPC 20%+ national aggregate rate to reflect the Washington-market pre-effective-date period where SSB 6091 compliance pressure is not yet operational.

20%+ — National Stage 2 conversion rate measured by the CPC. The Stephen Brobeck April 2026 CPC report measured Compass double-ending rates across five sampled markets at 20%+ aggregate. Reffkin personally endorsed the figure on April 16, 2026 through the quote-card specimen catalogued in MindCast publication The Compass-Reffkin Consumer Policy Center Quote-Card Specimen.

Funnel Conversion Math

The three figures convert as a pipeline rather than stacking as parallel observations. Of the nine listings in the top 10 inside the parent, the Two-Gate model’s Washington floor predicts 15% close with the parent on both sides — meaning roughly 1.4 listings per top-10 cohort on average in the pre-effective-date window. The CPC national figure suggests the realized number nationally is closer to 20%+, or roughly 1.8 listings per cohort. The Layer 3 acquisition premium math depends on the Stage 2 figure, not the Stage 1 figure. The April ranking establishes the addressable population for the Stage 2 measurement. The Stage 2 measurement at scale arrives during the post-June 11 SSB 6091 enforcement window and the Q3 2026 Compass reporting cycle.

The funnel structure organizes the next twelve months of measurement and resolves a vulnerability the prior stack framing carried. Readers encountering the 90% figure in isolation might mistake origination for realized capture and dismiss the publication when realized capture comes in lower. Readers encountering the funnel framing understand that 90% is the top of the funnel and that the publication’s analytical claims operate against the bottom of the funnel. The framing is more honest, more institutionally legible, and more durable across the measurement windows the publication’s forward predictions traverse.

Why Stage 1 Still Matters

Stage 1 measurement remains analytically productive for three reasons even though Stage 2 carries the economic substance.

Stage 1 supplies the leading indicator for Stage 2 measurement. Origination concentration in April 2026 supplies the inventory pool the Q3 2026 Stage 2 measurement will sample from. The April ranking gives institutional subscribers and AG enforcement teams a forward look at the Stage 2 measurement universe before Stage 2 measurement becomes available.

Stage 1 supplies the antitrust dependency structure The Motion Compass Filed and the Architecture It Could Not Address Section VIII identified. The rule-of-reason defense and the Layer 3 valuation cannot both be true simultaneously. Either origination concentration is purely procompetitive recruitment (in which case the Layer 3 premium has no economic foundation) or origination concentration is paired with a Stage 2 conversion mechanism (in which case the rule-of-reason defense weakens). Stage 1 measurement at 90% raises the Layer 3 valuation question regardless of where Stage 2 measurement lands.

Stage 1 supplies the deployment exhibit for state legislative committee testimony and AG enforcement memoranda. A single screenshot demonstrating 90% origination concentration in a regional luxury tier four months after merger close inside a statutory transition window is more institutionally legible than a Stage 2 conversion-rate measurement that requires NWMLS subscription access and statistical disclosure analysis. Stage 1 carries the publicly accessible artifact. Stage 2 carries the substance the artifact points toward.

The stack supplies a single-screen analytical exhibit the corpus did not previously have. The exhibit is deployable in committee testimony, state attorney general enforcement memoranda, and institutional subscriber briefings without further data collection — provided readers receive the funnel framing simultaneously, so origination concentration is not mistaken for realized capture.

V. Litigation Posture as Economic Expression

Compass publicly frames the dispute around innovation, consumer choice, and fiduciary flexibility. The concentration evidence complicates the framing.

A brokerage with disproportionate luxury inventory possesses stronger economic incentives to weaken mandatory public exposure rules, expand delayed marketing windows, internalize buyer flow, and preserve routing discretion. Such incentives do not automatically establish wrongdoing. Such incentives do, however, change how regulators, courts, competitors, and market participants interpret litigation behavior.

Economic structure shapes narrative credibility. The stronger Compass becomes inside elite inventory segments, the more difficult it becomes to characterize the litigation as purely philosophical disagreement detached from economic self-interest.

MindCast publication The Motion Compass Filed and the Architecture It Could Not Address addressed the broader dynamic by arguing that the litigation increasingly reflects market-structure conflict rather than ordinary procedural disagreement. The Seattle concentration evidence materially strengthens the interpretation.

The causal chain now appears increasingly coherent:

1. Compass accumulates elite inventory.

2. Elite inventory increases value of buyer-routing control.

3. Buyer-routing control increases value of restricted visibility systems.

4. MLS rules constrain restricted visibility systems.

5. Litigation pressure against MLS architecture becomes economically rational.

The sequence does not require conspiracy assumptions or speculative intent attribution. Standard incentive analysis explains the escalation.

The litigation therefore functions not merely as legal defense, but as strategic signaling to agents, sellers, investors, and competitors. Once a brokerage commits strategically to inventory concentration and private-network economics, retreat becomes costly because recruiting narratives depend on exclusivity claims, investor narratives depend on differentiation claims, and competitive positioning depends on maintaining the perception of privileged access.

VI. The Trade Press Skillman Moment

MindCast publication The Motion Compass Filed and the Architecture It Could Not Address Section V enumerated the Eddie Haskell Architecture across five audiences: investors, clients, the federal court, state legislators, and agents. The Eddie Haskell Architecture is a corpus term — borrowed from the 1950s television character whose face-to-face politeness with adults concealed conduct toward peers — that names the pattern of delivering an internally coherent message to each audience while the messages collectively contradict each other across audiences. Each audience receives an internally coherent narrative that is collectively incompatible with the narratives delivered to the other audiences. The Federal Rules of Evidence 801(d)(2) admissibility analysis — the rule treating a party’s own statements as non-hearsay admissions usable against the party at trial — converts the cross-audience divergence into summary-judgment evidence.

Trade press operates as a sixth audience the prior enumeration did not name. Seattle Agent Magazine renders Sotheby’s, Coldwell Banker, and Compass as three brokerages on a top-10 list four months after the Compass-Anywhere merger closed. The rendering presents brand portfolio as competitive structure — a visibility-layer artifact obscuring the corporate-parent reality available in the same month’s Securities and Exchange Commission (SEC) filings.

The trade-press rendering is a Self-Disclosure Trap variant of the kind catalogued in MindCast publication The Cybernetics of Compass Holdings’ Narrative Control Architecture. The Self-Disclosure Trap is a corpus term naming the pattern in which Compass’s own published statements — across litigation filings, legislative testimony, investor communications, consumer marketing, agent social media, and CEO social media — supply the contradictions that adversaries deploy against Compass without requiring discovery or subpoena. The brand portfolio’s persistence as a trade-press visibility asset is itself a published representation. The representation obscures the corporate-parent reality available to any reader of the merger filings. The divergence between rendering and corporate structure is observable on the public record without further investigation.

The diagnostic threshold applies. The April ranking marks a point at which the post-merger concentration mechanism becomes publicly legible through a single, concrete instance of trade-press rendering. Not theory. Not narrative. A specimen. The architecture Compass built — the brand portfolio operating as competitive presentation while the corporate parent operates as a single economic unit at the parent layer — reveals itself in trade press’s own published ranking, available to any reader of the public record without further investigation. The classification holds subject to the falsification conditions specified in Section IX.

The specimen does three things simultaneously. The specimen collapses abstraction into observable conduct — the post-merger concentration architecture becomes a single ranking on a single publication date. The specimen bridges narrative to evidence — what trade press characterizes as multi-brokerage competitive distribution and what the SEC merger filings characterize as a single combined entity both refer to the same documented corporate structure, in the same public record. The specimen forces interpretation from every observer with access to both records — the federal court evaluating the rule-of-reason record at summary judgment, the state AG building a UDAP enforcement predicate, the broker-member evaluating the cooperative’s enforcement against one member’s conduct, the prospective partner conducting pre-deal due diligence, the institutional subscriber evaluating the Layer 3 acquisition premium against post-merger empirical output.

The naming convention preserves the original Skillman Moment terminology established in MindCast publication The Compass Narrative Inversion Playbook. The Skillman Moment is a corpus term naming the pattern — first identified in Moya Skillman’s February 27, 2026 Puget Sound Business Journal commentary applying Robert Reffkin’s MLS-targeted “seller choice” framing to a state licensing statute — in which a Compass agent transmits a Compass-internal narrative into a forum where the framing’s category presuppositions do not survive scrutiny. The Trade Press Skillman Moment is the third specimen at the third layer. The linguistic specimen (”negative insights”) names the suppression mechanism in Compass’s own corporate vocabulary. The behavioral specimens (the Two-Gate listings, where one team credential operates address suppression on one listing and intra-brokerage dual representation on another) document the suppression mechanism in operation under a single team credential. The trade-press specimen documents the post-merger aggregate concentration the suppression mechanism produces at the regional luxury-tier layer.

VII. Layer 3 Acquisition Premium and the Closed-Loop Architecture

MindCast publication The Compass Commission Consolidation Strategy and Real Estate Marketing Transparency named the Three-Layer Acquisition Hierarchy to describe the post-merger valuation structure. Layer 1 represents standard brokerage operations — listing services, agent infrastructure, and customer relationships that any traditional brokerage produces. Layer 2 represents technology platform value — the integrated software, customer relationship management infrastructure, and data systems Compass has built. Layer 3 represents the routing-control architecture itself — the pre-market window during which listings can be withheld from the open market long enough for an internal buyer to arrive first, capturing both commission sides on the same transaction. The publication identified $400-800 million of the Anywhere acquisition price as Layer 3 premium dependent on continued operation of that routing-control architecture. MindCast publication The Motion Compass Filed and the Architecture It Could Not AddressSection VIII identified the auditor-dispositive goodwill impairment question at the next reporting cycle if the routing-control architecture is operationally compromised by SSB 6091 enforcement.

The Layer 3 premium does not survive on Stage 1 origination concentration alone. The premium survives only if the Stage 2 conversion mechanism continues operating at scale through the SSB 6091 enforcement window. The dependency structure is the analytical center of the auditor-dispositive question. Origination concentration produces a marketing flywheel and a recruiting asset. Conversion produces the per-transaction commission uplift that supports the goodwill carrying value. The auditor at the Q3 2026 reporting cycle is testing the Stage 2 figure looking through the Stage 1 figure — not the reverse.

The April ranking supplies the empirical specimen the Stage 1 input to the auditor-dispositive analysis requires. Three observations follow:

The post-merger brand portfolio is producing the Stage 1 origination output the routing-control architecture’s Layer 3 valuation requires as a precondition. Nine of ten luxury Seattle April listings under the combined corporate parent is consistent with the routing-control architecture operating at Stage 1 capacity in the regional luxury tier four months after merger close. The figure does not by itself establish Stage 2 capture at scale. The figure establishes that the addressable population for Stage 2 capture is concentrated as the routing-control architecture requires.

Goodwill impairment testing under ASC 350 requires identification of the cash-generating unit and assessment of whether the recoverable amount of the unit exceeds carrying value. Recoverable amount depends on Stage 2 conversion at scale — origination concentration is the input population, but commission revenue per transaction depends on the conversion rate. The post-merger Stage 1 concentration is measurable at the regional level today. The Stage 2 measurement at scale arrives during the post-June 11, 2026 enforcement window. The auditor analysis at Q3 2026 will look through the Stage 1 figure to the Stage 2 figure for the recoverable-amount calculation.

The two-direction risk profile holds at the Stage 2 layer. If post-June 11 enforcement reduces the Stage 2 conversion rate materially while Stage 1 origination concentration holds, the auditor analysis triggers an impairment review against the Layer 3 premium because recoverable amount declines while the listing-share metric remains elevated. If post-June 11 enforcement does not reduce the Stage 2 conversion rate materially, the regulatory enforcement predicate against continued operation tightens because UDAP enforcement leverages the Stage 2 figure rather than the Stage 1 figure. Each direction supplies a different but converging input to the next reporting cycle’s auditor analysis.

The litigation defense and the post-merger valuation cannot both be true simultaneously. Either Stage 1 concentration is purely procompetitive recruitment unattached to a Stage 2 conversion mechanism (in which case the Layer 3 premium has no economic foundation and the auditor analysis triggers impairment review on the original carrying value) or Stage 1 concentration is paired with Stage 2 conversion at scale (in which case the rule-of-reason defense weakens because concentration paired with intra-brokerage capture under conditions of inadequate disclosure produces the UDAP enforcement predicate the CPC analysis identified). The structural dilemma operates regardless of where Stage 2 measurement lands during the enforcement window.

Institutional cybernetics provides the additional analytical layer. Feedback loops now reinforce the system: Stage 1 concentration increases routing value, routing value increases Stage 2 exclusivity incentives, exclusivity incentives increase litigation pressure, litigation visibility increases brand differentiation, and differentiation attracts additional Stage 1 inventory. Closed-loop reinforcement architectures often persist until external constraints interrupt the cycle. MindCast publication The Cybernetics of Compass Holdings’ Narrative Control Architecture formalized the underlying control-theoretic framework. The April ranking documents the Stage 1 inventory-concentration variable at a single time-stamp inside the loop.

External constraints exist on a defined timeline. SSB 6091 takes effect June 11, 2026 and operates against Stage 2 conversion through enhanced disclosure requirements. The October 2026 Compass v. NWMLS trial calendar holds and operates against Stage 1 routing infrastructure through the rule-of-reason analysis. The Q3 2026 Compass reporting cycle arrives during the post-effective-date enforcement window and operates against the Layer 3 premium through the recoverable-amount calculation. Each constraint operates as a potential interruption to a different layer of the closed-loop architecture the April ranking documents.

VIII. State-Level Legislative Ratchet — Deployment Exhibit

Section IX Condition 5 in MindCast publication The Motion Compass Filed and the Architecture It Could Not Address predicts that at least two additional states introduce SSB 6091-style legislation citing the Washington model within eighteen months. The condition is observable on a defined timeline. The April ranking supplies a ready-to-deploy committee-testimony exhibit for jurisdictions evaluating the legislative model.

The exhibit’s structural properties:

A single regional market. King County, Washington, with a single major metropolitan center, available to legislators in any state evaluating the model.

A single monthly window. April 2026, four months after merger close, inside the SSB 6091 statutory transition window, observable at the trade-press visibility layer without subscription access to NWMLS data.

A single corporate parent. The post-merger Compass-Anywhere combined entity, with the merger close date and the brand-portfolio preservation publicly documented through SEC filings and the merger close announcement.

A single concentration figure. Ninety percent of the regional luxury-tier top-10 ties back to the corporate parent. The figure is observable on a publicly accessible trade publication without independent data collection.

The exhibit is deployable in state legislative committee testimony for jurisdictions evaluating SSB 6091 analogues. The exhibit is also deployable in state attorney general (AG) enforcement memoranda — the New Mexico Department of Justice, the Washington AG, AG offices in the five CPC-sampled markets — building UDAP enforcement predicates against the post-merger entity.

The exhibit precedes any jurisdiction-specific data collection requirement. A state legislator in Massachusetts, Illinois, California, or Texas evaluating concurrent-marketing legislation now has a single-screen visual artifact demonstrating that the post-merger entity produces 90% concentration in a regional luxury tier four months after merger close, in a state where the legislative model under evaluation has already passed and is approaching its effective date. The artifact does not require any data collection in the legislator’s home state to support committee testimony evaluating whether the legislative model addresses concentration concerns the legislator is hearing locally.

The exhibit’s analytical efficiency is the asset. The Two-Gate model required two NWMLS primary-source records and a developed game-theoretic framework. The April ranking is one screenshot.

IX. Forward Predictions and Falsification Conditions

Five forward predictions follow from the publication’s analytical position. The predictions are stated to be tested against the SSB 6091 effective-date window, the Q3 2026 reporting cycle, and the Q1 2027 enforcement-citation window.

Prediction 1 — Trade-press rendering convergence. Within six months of the SSB 6091 effective date (June 11, 2026 to December 11, 2026), at least one major trade publication will modify its rendering of post-merger Compass-Anywhere brand presentations to reflect common ownership. The modification is institutionally rational given the auditor analysis and the AG enforcement predicate the unmodified rendering creates. Falsification: if no major trade publication modifies the rendering during the prediction window, the trade-press visibility layer continues to operate as a Compass narrative-control asset and the Trade Press Skillman Moment classification holds with strengthened force.

Prediction 2 — Stage 2 conversion compresses materially in Washington after June 11 even if Stage 1 origination concentration holds. Within twelve months of the SSB 6091 effective date, the intra-brokerage buyer-side capture rate on Compass-listed King County residential transactions above $5,000,000 falls below the 15% Two-Gate model floor — even if the April 90% Stage 1 origination concentration figure persists or grows. The compression reflects enhanced disclosure operating directly against the Stage 2 conversion mechanism while leaving Stage 1 origination infrastructure intact. Falsification: if Stage 2 conversion does not compress materially despite SSB 6091 enforcement, the routing-control architecture is operationally robust to disclosure-based enforcement at both stages, and the Layer 3 premium analysis adjusts against the original $400-800 million estimate while the regulatory enforcement predicate against continued operation tightens correspondingly.

Prediction 3 — At least one state attorney general cites the post-merger concentration figure in an enforcement memorandum or filed pleading by Q1 2027. The figure’s analytical efficiency makes it cite-ready for any state AG building a UDAP enforcement predicate or evaluating an antitrust referral. Falsification: if no state AG cites the figure during the prediction window, the post-merger concentration’s enforcement-predicate utility is lower than the publication’s analysis projects, and the institutional-reader implications adjust accordingly.

Prediction 4 — Compass continues increasing emphasis on private-network positioning despite ongoing litigation and regulatory scrutiny. The closed-loop architecture’s self-reinforcing dynamics make retreat from inventory-concentration strategy structurally costly. Falsification: if Compass meaningfully reduces emphasis on private exclusives during the measurement window, the closed-loop framework requires recalibration and the falsification thresholds in MindCast publication Two NWMLS Records, One Foster-Skillman Team Section VI tighten correspondingly.

*Prediction 5 — Future discovery battles in Compass v. NWMLS will increasingly involve internal routing economics, buyer-capture incentives, recruiting language, and visibility-management strategies.* The April ranking supplies trial counsel with aggregate-tier evidentiary anchors that complement the team-credential and transaction-level specimens already preserved in the public record. Falsification: if discovery proceeds without engagement with routing economics or visibility-management materials, the litigation operates at a procedural layer disconnected from the underlying market-structure conflict — a disconnection that would itself supply diagnostic information about the litigation’s strategic function.

X. Conclusion

Seattle luxury concentration increasingly supplies the empirical context necessary to understand the Compass v. NWMLS dispute as a market-structure conflict rather than a narrow disagreement over listing policy. The central issue is not whether private exclusives exist. The central issue is whether concentrated inventory combined with controlled visibility pathways transforms brokerage competition into a system of selective market access.

Luxury inventory concentration changes the incentive geometry underlying the litigation. Neutral trade-publication evidence now increasingly supports the interpretation. The conflict therefore sits at the intersection of law, behavioral economics, institutional cybernetics, and market-visibility governance.

Nine of ten luxury Seattle listings during April 2026 tie back to a single corporate-parent layer rendered as three brokerages by trade press. The corporate-parent reality is publicly available through SEC filings. The brand-portfolio rendering is publicly available through trade publications. The divergence between rendering and corporate structure is observable on the public record without further investigation. The rendering meets the structural threshold the corpus established for Skillman moment classification, subject to the falsification conditions specified in Section IX.

The 90% Stage 1 origination concentration figure feeds the Two-Gate Capture Model’s 15% predicted Stage 2 conversion floor and the CPC’s 20%+ national Stage 2 conversion rate. The three figures operate as a sequential funnel — addressable population at the top, predicted Washington-market conversion floor in the middle, national realized conversion rate at the base — and produce a single-screen analytical exhibit available for committee testimony, AG enforcement memoranda, and institutional subscriber briefings.

The Layer 3 acquisition premium auditor analysis at the next reporting cycle has an empirical input it did not previously have. The state-level legislative ratchet committee-testimony exhibit it requires is publicly available. The trade-press visibility layer joins the five Eddie Haskell audiences MindCast publication The Motion Compass Filed and the Architecture It Could Not Addressenumerated.

The mechanism persists across conditions. The visibility layer changes — from team credential to aggregate concentration to trade-press rendering — but the economic outcome does not. MindCast publication Two NWMLS Records, One Foster-Skillman Teamdocumented the conduct. MindCast publication The Motion Compass Filed and the Architecture It Could Not Address documented the defense architecture’s structural absences. The April ranking documents what the corporate parent produces when the conduct continues at scale and the defense architecture holds the litigation in place.

The architecture does not adjust to the model. The model adjusts to the evidence. The evidence is publicly accessible on a trade publication’s April 2026 ranking page.

Source Documents

Emily Marek, *The 10 most expensive new listings in Seattle*, Seattle Agent Magazine, April 30, 2026 (sourced from Redfin and Northwest Multiple Listing Service data).

Compass, Inc. and Anywhere Real Estate Inc., *Compass and Anywhere Stockholders Overwhelmingly Approve Merger*, PR Newswire (January 7, 2026).

Compass, Inc., Form 8-K filing announcing combination with Anywhere Real Estate, including the express commitment to “preserving the unique independence of Anywhere’s leading brands” — Better Homes and Gardens Real Estate, Century 21, Coldwell Banker, Coldwell Banker Commercial, Corcoran, ERA, and Sotheby’s International Realty (September 22, 2025).

Florida Realtors, *Compass Completes $1.6B Anywhere Acquisition*, reporting on the post-close combined entity led by Robert Reffkin under Compass International Holdings with approximately 340,000 real estate professionals and affiliate broker-owners (January 12, 2026).

The Real Deal, *Compass-Anywhere merger dodges antitrust concerns for speedy closing*, reporting on Reffkin’s confirmation that Anywhere’s brands — including Corcoran, Coldwell Banker, Sotheby’s International Realty, and Century 21 — would maintain their identities under the combined entity (January 9, 2026).

Northwest Multiple Listing Service, Listing #2497151, “Triptych,” Undisclosed Address, Bellevue, WA 98004 (active at $65,000,000 as of April 17, 2026).

Northwest Multiple Listing Service, Listing #2468181, 4640 95th Avenue NE, Yarrow Point, WA 98004 (sold March 27, 2026 at $7,775,000).

Stephen Brobeck, Compass Expansion: New Data on Market Share and Double Ending (Consumer Policy Center, April 2026).

Substitute Senate Bill 6091, Washington State Legislature (2026 Regular Session), signed March 17, 2026, effective June 11, 2026.

MindCast AI Analytical Foundation

MindCast publication Two NWMLS Records, One Foster-Skillman Team — Primary-Source Evidence of the Compass Two-Gate Capture Model (April 17, 2026).

MindCast publication The Motion Compass Filed and the Architecture It Could Not Address (April 25, 2026).

MindCast publication The Compass Commission Consolidation Strategy and Real Estate Marketing Transparency (February 19, 2026).

MindCast publication The Compass-Anywhere Address Suppression Calculus (February 22, 2026).

MindCast publication Compass Double-Sided Commissions — Consumer Policy Center Measures the Output, MindCast Models the System (April 15, 2026).

MindCast publication The Compass-Reffkin Consumer Policy Center Quote-Card Specimen — A Self-Disclosure Trap Market Analysis (April 16, 2026).

MindCast publication The Cybernetics of Compass Holdings’ Narrative Control Architecture (March 21, 2026).

MindCast publication The Compass Narrative Inversion Playbook (February 4, 2026).

Appendix: MindCast Publication Summaries and Relevance to the Present Analysis

The eight MindCast publications cited in the body operate as the prior corpus the Two-Stage Funnel Model integrates. The appendix records each publication’s substantive contribution and its specific relevance to the present analysis. The publications are ordered chronologically.

1. The Compass Narrative Inversion Playbook

The Playbook documents the three-tier cross-forum contradiction pattern across federal court, state legislative testimony, and investor communications, and prepares legislators and state attorneys general with falsifiable predictions and impeachment scripts for the SSB 6091 legislative window. The publication catalogs the original Skillman Moment specimen — Moya Skillman’s February 27, 2026 Puget Sound Business Journal commentary applying Reffkin’s MLS-targeted “seller choice” framing to a state licensing statute, illustrating how Compass’s institutional narrative exports to agents without the category correction enterprise-level messaging would supply.

Relevance to the present analysis. The Playbook supplies the Skillman Moment naming convention the present publication extends to the trade-press visibility layer. Section VI treats the Seattle Agent Magazine April 2026 ranking as the third specimen at the third layer — linguistic specimen (Playbook), behavioral specimens (Two-Gate listings), and trade-press specimen (April ranking). Without the Playbook’s original taxonomy, the present analysis would have no corpus-internal vocabulary for classifying the trade-press rendering as a recurring evidentiary pattern.

2. The Compass Commission Consolidation Strategy and Real Estate Marketing Transparency

The publication models the routing-control mechanism using thirteen months of Seattle ultra-luxury NWMLS transaction data across 130 transactions totaling $1.08 billion. The Three-Layer Acquisition Hierarchy identifies Layer 3 — $400 to $800 million of the Anywhere acquisition premium — as a regulatory short position dependent on a single operating condition: that listings can be withheld from the open market long enough for an internal buyer to arrive first. Category A through D commission-flow architecture documents direct dual-agency capture, merger internalization in both directions, and the open-market outcomes the private exclusive program is engineered to prevent.

Relevance to the present analysis. The publication supplies the Layer 3 acquisition premium framework the present Section VII ties to the ASC 350 goodwill impairment analysis. The $400-800 million figure and the structural argument that the premium depends on continued operation of the routing-control architecture both originate here. The Two-Stage Funnel Model’s Stage 2 conversion mechanism extends the publication’s Category A through D commission-flow taxonomy.

3. The Compass-Anywhere Address Suppression Calculus

The publication operates as a game theory simulation modeling the Tere Foster and Moya Skillman team structure and detection-window incompatibility across price tiers. The simulation establishes the formal proof that the Anywhere acquisition premium is structurally unrecoverable through address suppression alone: revenue scales with deployment volume while detection scales with deployment volume in the same direction. The publication models the optimization problem the combined entity faces — the price threshold at which address suppression maximizes dual-commission capture while remaining below the detection threshold that triggers NWMLS enforcement, competitor complaints, and regulatory scrutiny.

Relevance to the present analysis. The publication establishes the pre-merger game-theoretic baseline against which the April 2026 Seattle Agent Magazine ranking provides post-merger empirical confirmation. The simulation’s projected concentration outcome at the regional luxury-tier level is what the April ranking documents at the trade-press visibility layer four months after merger close. The publication’s revenue-versus-detection structural finding underwrites Forward Prediction 2 in Section IX.

4. The Cybernetics of Compass Holdings’ Narrative Control Architecture

The publication formalizes the three-layer control architecture and the cybernetic foundations of the Self-Disclosure Trap pattern. The architecture operates through three named roles: Robert Reffkin as Architect (originating the “seller choice” framing and calibrating its multi-forum deployment), Moya Skillman as Amplifier (transmitting the framing through the Puget Sound Business Journal and through transaction-level activity at the Foster-Skillman team), and Cris Nelson as Enforcer (the Pacific Northwest Regional Vice President who attended both January 2026 SSB 6091 hearings, monitored Compass-affiliated testimony, and declined to testify under oath despite his position). The Foster-Skillman architecture is documented at the transaction level through MLS #2362507 (a $15M Mercer Island property producing dual-end capture) and MLS #2392995 (the $79M Triptych estate marketed as “Call for Address”). The Debt-Narrative Correlation establishes that Compass’s rhetorical intensity tracks balance-sheet constraints, not market conditions.

Relevance to the present analysis. The publication supplies the Self-Disclosure Trap framework the present Section VI applies to the trade-press visibility layer. Each three-layer role generates a different Self-Disclosure Trap response under cross-forum scrutiny: the Architect role generates trap exposure through direct attribution (Reffkin’s April 16 quote-card endorsement of the Consumer Policy Center 20%+ figure), the Amplifier role generates trap exposure through narrative export into incompatible forums (the Skillman Moment in PSBJ), and the Enforcer role generates trap exposure through testimony-avoidance — declining to speak under oath in a forum where prior media positions would surface as impeachment material. Nelson’s silence at the January 2026 hearings is not a separate phenomenon from the Skillman Moment; it is the same Self-Disclosure Trap pressure producing a different observable behavior at a different layer of the architecture. The brand portfolio’s persistence as a trade-press visibility asset is itself a published representation obscuring the corporate-parent reality — a Self-Disclosure Trap variant the publication’s three-layer control architecture predicts. The closed-loop architecture in the present Section VII (concentration → routing value → exclusivity incentives → litigation pressure → brand differentiation → additional concentration) operationalizes the cybernetic framework the publication formalized.

5. Compass Double-Sided Commissions — Consumer Policy Center Measures the Output, MindCast Models the System

The publication operates as a benchmark-and-extension analysis of the Stephen Brobeck CPC report measuring Compass double-ending rates across five sampled markets at 20%+ aggregate (Boston, Washington D.C., Chicago, San Diego, Austin). The publication establishes that MindCast modeled the routing-control mechanism in February 2026 — two months before the CPC report — using thirteen months of Seattle ultra-luxury NWMLS transaction data. Prediction 2 forecasts that double-ending rates in the five sampled markets will increase as the Rocket-Redfin partnership deepens buyer-funnel integration, with double-ending probability compounding where listing-side and demand-side capture mechanisms operate in the same transaction.

Relevance to the present analysis. The publication supplies the 20%+ national Stage 2 conversion rate that anchors the bottom of the Two-Stage Funnel Model. The 90% / 15% / 20%+ stack the present Section IV formalizes traces directly to the publication’s benchmark architecture. The present analysis’s Forward Prediction 2 extends the publication’s Prediction 2 from a national five-market frame to the Washington-market post-effective-date enforcement window.

6. The Compass-Reffkin Consumer Policy Center Quote-Card Specimen — A Self-Disclosure Trap Market Analysis

The publication catalogs the Reffkin April 16, 2026 Facebook quote-card extracting one sentence from the CPC report under the caption “A response to those in the industry that claim Compass only wants to double end deals.” The specimen lands 21 days after Triptych publicly documented the price-drop suppression the NWMLS counterclaim’s Consumer Protection Act count indicts, and 14 days after NWMLS filed its four-count counterclaim. The publication treats the quote card as a Self-Disclosure Trap specimen produced inside an active federal discovery window, with party-admission consequences under Federal Rules of Evidence 801(d)(2), establishing Reffkin’s personal endorsement of the 20%+ figure as a national-market judicial-estoppel predicate (the doctrine preventing a party from advancing a position clearly inconsistent with one it has successfully asserted in another proceeding).

Relevance to the present analysis. The publication establishes the personal-attribution chain that converts the CPC 20%+ figure from a third-party measurement into a Reffkin-endorsed datum the present analysis stacks against the 90% origination concentration figure. Section IV’s funnel construction depends on the Reffkin endorsement holding the 20%+ figure as a national Stage 2 baseline against which the Washington-market Stage 2 prediction calibrates. The publication’s Self-Disclosure Trap classification supplies the diagnostic vocabulary the present Section VI Trade Press Skillman Moment formalization extends.

7. Two NWMLS Records, One Foster-Skillman Team — Primary-Source Evidence of the Compass Two-Gate Capture Model

The publication establishes the Two-Gate Capture Model as a named analytical construct through two NWMLS primary-source records under a single Foster-Skillman team credential. Gate 1 address suppression operates on Triptych at $65,000,000 with 304 days under “Undisclosed Address” designation. Gate 2 intra-brokerage dual representation operates on 4640 95th Avenue NE at $7,775,000 sold March 27, 2026 with Skillman as both Co-Listing Broker and Buyer Broker on the same transaction. Section VI sets the falsification floor at 15% for Compass-listed residential transactions above $5,000,000 in King County during April 2026 through December 2026.

Relevance to the present analysis. The publication supplies the Two-Gate model the present analysis extends to the aggregate concentration layer. The Foster-Skillman team operating both gates of the model in the original specimens appears at #4 on the April Seattle ranking, placing the named economic unit simultaneously on the team-credential record and the aggregate concentration record. The 15% prediction is the middle figure in the 90% / 15% / 20%+ funnel stack — the predicted Washington-market Stage 2 conversion floor against which post-June 11 enforcement-period measurements will be tested.

8. The Motion Compass Filed and the Architecture It Could Not Address

The publication analyzes Compass’s April 23, 2026 motion to dismiss the NWMLS counterclaim and identifies three structural absences in the brief Compass cannot defend at summary judgment. Section V enumerates the Eddie Haskell Architecture across five audiences — investors, clients, the federal court, state legislators, and agents — each receiving an internally coherent narrative collectively incompatible with the narratives delivered to the others. Section VIII identifies the auditor-dispositive goodwill impairment question at the next reporting cycle. Section IX Condition 5 predicts at least two additional states introduce SSB 6091-style legislation citing the Washington model within eighteen months.

Relevance to the present analysis. The publication supplies three direct architectural inputs. The Eddie Haskell Architecture five-audience enumeration is what the present Section VI extends by identifying trade press as a sixth audience. The auditor-dispositive analysis at the Q3 2026 reporting cycle is what the present Section VII develops through the Stage 1 / Stage 2 dependency framing. The Section IX Condition 5 state-level legislative ratchet prediction is what the present Section VIII operationalizes by treating the April Seattle ranking as a deployable committee-testimony exhibit.

Cumulative Architecture

The eight publications form a sequential corpus where each publication’s contribution feeds the next. The Playbook (February 4) named the cross-forum contradiction pattern. The Commission Consolidation Strategy (February 19) supplied the Layer 3 acquisition premium framework. The Address Suppression Calculus (February 22) modeled the team-structure detection-window dynamics. The Cybernetics publication (March 21) formalized the three-layer control architecture. The CPC Benchmark publication (April 15) supplied the 20%+ national conversion rate. The Self-Disclosure Trap publication (April 16) converted the rate into a personally endorsed party admission. The Two-Gate Capture Model publication (April 17) supplied the 15% Washington-market prediction floor. The Motion-to-Dismiss publication (April 25) named the Eddie Haskell Architecture and the auditor-dispositive structural dilemma. The present analysis integrates all eight contributions into the Two-Stage Funnel Model and identifies the Trade Press Skillman Moment as the third specimen layer the prior corpus had not yet sampled.