MCAI Lex Vision: The Compass-Reffkin Consumer Policy Center Quote-Card Specimen — A Self-Disclosure Trap Market Analysis

How a Single Facebook Post Compounded Party-Admission Exposure Inside an Active NWMLS Discovery Window

Recent works: The Compass-Reffkin Consumer Policy Center Quote-Card Specimen — A Self-Disclosure Trap Market Analysis | Compass Double-Sided Commissions — Consumer Policy Center Measures the Output, MindCast Models the System | Two NWMLS Records, One Foster-Skillman Team — Primary-Source Evidence of the Compass Two-Gate Capture Model Inside the Washington Statutory Transition Window | Rocket-Redfin Asks NWMLS to Rewrite Rules to Help Make Rocket-Redfin-Compass Partnership More Profitable — and Strategically Chose a Corporate News Platform Over an Amicus Brief

Foundational works: The Compass Narrative Inversion Playbook | Compass’s Cross-Forum Contradictions | The Compass Commission Consolidation Strategy and Real Estate Marketing Transparency | The Antitrust Litigation Trap Compass Built for Itself | The Counterclaim That Closed Compass’s Antitrust Thesis | Zillow, eXp, and Redfin–Compass. Three Deals. Twenty Days. One Outlier.

Context: The Compass Behavioral Economics Trilogy Architecture

The present market analysis operates as preparatory material for the third installment of MindCast AI’s Compass publication trilogy. Establishing the trilogy’s structure, the evolution of the third installment’s planned scope, and the specimen’s placement within that evolution is required before the substantive analysis begins.

Part I — The Compass Narrative Inversion Playbook (February 4, 2026) — documented the three-tier cross-forum contradiction pattern and prepared legislators and state attorneys general with falsifiable predictions and impeachment scripts for the SSB 6091 legislative window. Pre-passage instrument designed to anchor the Washington hearing record and the multi-state legislative cascade that followed.

Part II — Compass’s Cross-Forum Contradictions (February 28, 2026) — extended the analysis across six forums (federal court, state legislature, investor communications, consumer marketing, agent social media, CEO social media) and constructed the enforcement charge-code map. Post-passage consolidation instrument designed for multi-state AG coordination and plaintiffs’-counsel deployment in consolidated real estate antitrust litigation.

Part III — originally planned as Compass strategy across state-federal jurisdictions and partnerships, the concluding installment’s scope has evolved in response to three intervening institutional events. NWMLS filed its four-count counterclaim on April 2, 2026, converting Compass v. NWMLS from a defensive proceeding into a bilateral damages case with a CPA count carrying mandatory treble damages and fee-shifting under RCW 19.86.090. Compass voluntarily dismissed Compass v. Zillow on March 18, 2026, altering the forward-lock geometry Part I established. And the Consumer Policy Center (CPC) released its April 2026 Compass expansion report on April 14, 2026, introducing an independent measurement layer MindCast AI benchmarked in Compass Double-Sided Commissions — Consumer Policy Center Measures the Output, MindCast Models the System on April 15, 2026.

Three MindCast AI publications documented the new operating environment after those events converged. The Counterclaim That Closed Compass’s Antitrust Thesis (April 3, 2026) operationalized the Self-Disclosure Trap pattern — originally formalized in The Cybernetics of Compass Holdings’ Narrative Control Architecture — inside active federal litigation, demonstrating that Compass’s most damaging evidence is self-generated and that the exposure requires no investigation, only compilation. The Antitrust Litigation Trap Compass Built for Itself (April 6, 2026) consolidated the visual synthesis across the NWMLS counterclaim architecture, the Three-Layer Acquisition Hierarchy, and the MindCast Simulation probability bands that moved decisively toward P70 NWMLS prevail-or-favorable-settlement after the April 2 filing.

The Part III scope evolution follows from those publications. The original strategy across state-federal jurisdictions and partnerships framing positioned Part III as a strategic-synthesis instrument — useful when Compass’s litigation posture and legislative posture operated as separate theaters requiring coordinated analytical treatment. The post-April-2 environment collapsed that separation. Compass’s litigation posture is its legislative posture is its investor-communications posture is its CEO social-media posture, and each statement across any of those theaters now enters the Compass v. NWMLS evidentiary record under FRE 801(d)(2) as a party admission. Part III’s operative question shifted from how does Compass coordinate across jurisdictions and partnerships to how does Compass’s narrative apparatus, inside the active federal discovery window, become its own evidentiary archive. The updated Part III scope — a Self-Disclosure Trap consolidation across the post-SSB 6091, post-Zillow-dismissal, post-NWMLS-counterclaim environment — preserves the original jurisdictional and partnership dimensions as structural context while reorganizing the analytical priority around the party-admission mechanics the counterclaim activated.

The Reffkin April 16 Facebook post is Specimen 1 of the updated Part III consolidation. Five to seven additional specimens across two or more categories reach sufficient volume for Part III publication. The present market analysis preserves Specimen 1 in the record, maps the specimen onto the Self-Disclosure Trap framework, identifies the deposition-layer consequences for the forthcoming Reffkin deposition notice, and specifies the additional behavioral categories required before Part III reaches publication readiness.

This analysis is a working litigation artifact. The document operates at the specimen-level evidentiary register appropriate for NWMLS trial counsel, deposition-preparation teams, goodwill auditors, and institutional subscribers tracking the Compass v. NWMLS discovery window. Part III — when published — will operate at the broader pattern-level register that Part I and Part II established. The two registers are complementary and should not be conflated.

The Reffkin April 16 Facebook post is Specimen 1 of the updated Part III consolidation. Five to seven additional specimens across two or more categories reach sufficient volume for Part III publication. The present market analysis preserves Specimen 1 in the record, maps the specimen onto the Self-Disclosure Trap framework, identifies the deposition-layer consequences for the forthcoming Reffkin deposition notice, and specifies the additional behavioral categories required before Part III reaches publication readiness.

The essay is a working litigation artifact. The document operates at the specimen-level evidentiary register appropriate for NWMLS trial counsel, deposition-preparation teams, goodwill auditors, and institutional subscribers tracking the Compass v. NWMLS discovery window. Part III — when published — will operate at the broader pattern-level register that Part I and Part II established. The two registers are complementary and should not be conflated.

I. Framing

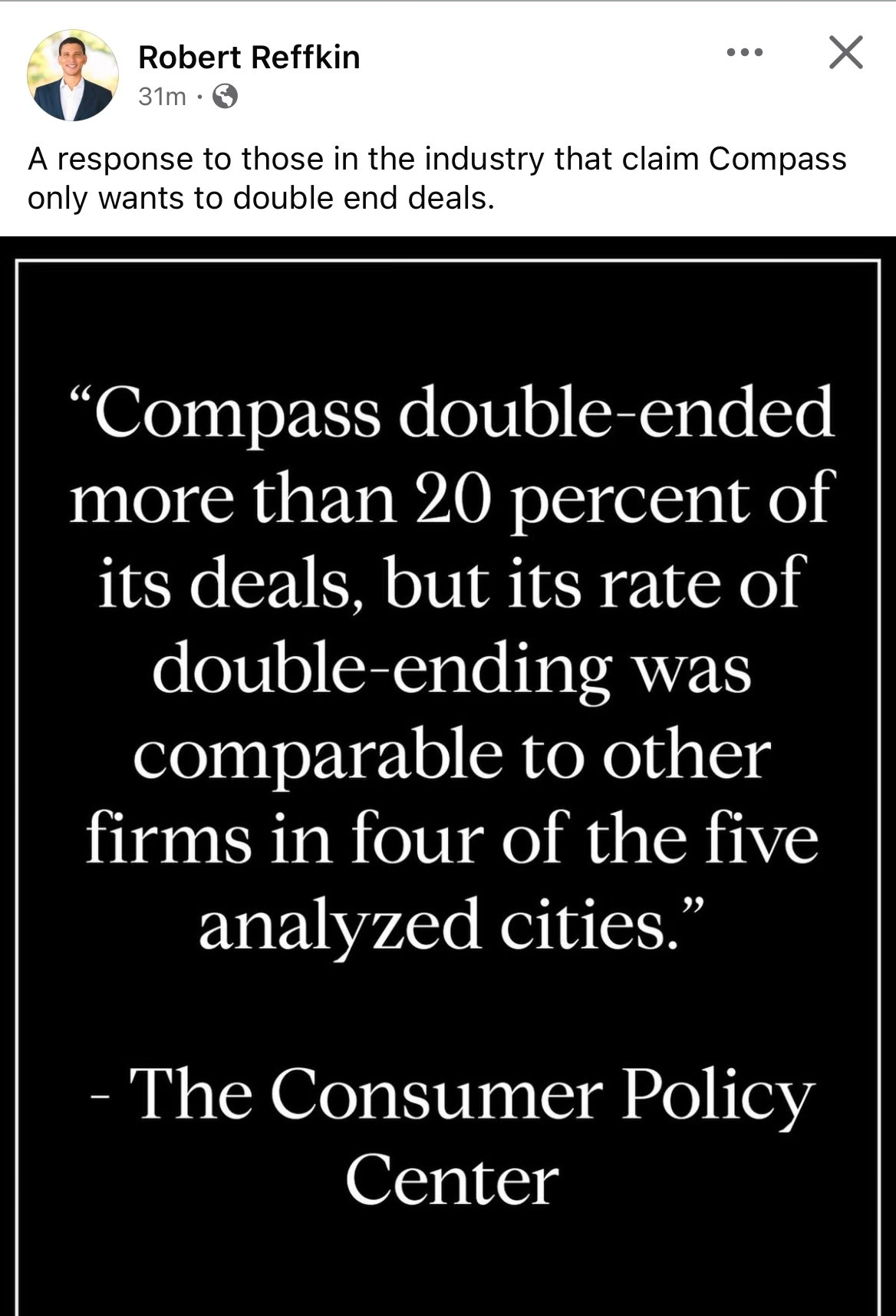

Robert Reffkin posted a quote card on his personal Facebook account on April 16, 2026, captioned: “A response to those in the industry that claim Compass only wants to double end deals.” The quote card extracted one sentence from the Consumer Policy Center’s April 2026 Compass expansion report: “Compass double-ended more than 20 percent of its deals, but its rate of double-ending was comparable to other firms in four of the five analyzed cities.” Attribution on the card: “The Consumer Policy Center.”

Reffkin offered no additional commentary. The implicit argument is complete in the caption and the quote: an independent consumer-protection organization’s report purportedly exonerates Compass on the double-ending question. Industry critics are wrong. The CPC supports Compass.

Read the post in isolation and the specimen looks like a Narrative Inversion Playbook deployment — selective quotation, scale neutralization, cross-forum contradiction. Read the post against the active Compass v. NWMLS counterclaim record and the specimen reclassifies. Reffkin’s April 16 post is a Self-Disclosure Trap specimen produced inside an active federal discovery window, with direct party-admission consequences under Federal Rules of Evidence (FRE) 801(d)(2), landing 56 days before Substitute Senate Bill (SSB) 6091’s June 11, 2026 statutory effective date and 14 days after NWMLS filed its four-count counterclaim on April 2, 2026.

The specimen’s evidentiary weight is structurally different from any cross-forum specimen MindCast AI catalogued before April 2, 2026. Before the counterclaim filing, Compass’s public statements entered a cross-forum record observable across venues but not aggregated into a single bilateral damages proceeding. After April 2, every Compass public statement feeds directly into Document 88’s evidentiary architecture. The CPA count’s mandatory treble damages and fee-shifting under RCW 19.86.090 multiply the financial consequence of each additional admission. The October 2026 trial calendar compresses the window in which such admissions can be produced without appearing in the summary judgment record.

Reffkin produced one anyway. Section II through Section VIII document the structural consequences.

II. What Reffkin Actually Did — Three Simultaneous Moves

Three structural moves operate simultaneously in a single Facebook post, and each carries independent evidentiary consequence under Document 88’s counterclaim architecture.

Move 1: Selective quotation as narrative inversion. Reffkin extracted the single sentence in the CPC report most favorable to Compass and presented it as the report’s conclusion. Read in context, the sentence describes a baseline measurement, not an exoneration. CPC’s thesis — documented across the report’s full architecture — argues that Compass has built a reinforcing system of acquisitions, private exclusives, referral incentives, and portal integration engineered to produce double-ending outputs, and that the strategic significance lies not in the aggregate rate but in the routing-control architecture producing it. Rate parity with other firms is the condition under which the architecture’s strategic consequence becomes more alarming, not less — because the architecture is designed to extract value from the same baseline rate through concentration in high-value inventory segments.

Reffkin performed the precise maneuver The Compass Narrative Inversion Playbook catalogued as the defining move across all five predicted arguments: reclassifying market infrastructure as personal preference. Applied to the CPC context, the move reclassifies a system-level indictment as a rate-parity defense.

Move 2: National-market endorsement that activates a new judicial-estoppel predicate. The CPC report’s five-city sample (Boston, Washington D.C., Chicago, San Diego, Austin) operates as a national analytical frame. Reffkin publicly endorsed that frame as favorable to Compass. The Counterclaim That Closed Compass’s Antitrust Thesis Section II identified the cross-forum market-definition lock as one of three structural vulnerabilities converging at NWMLS summary judgment: Compass argued a national market in the Southern District of New York (SDNY) Zillow proceeding through Dr. Aron’s expert testimony; Compass argues a Seattle and King County market in Compass v. NWMLS. Dr. Aron’s testimony sits in the federal record available to NWMLS trial counsel by subpoena.

Reffkin’s April 16 post supplies NWMLS an additional estoppel predicate without a subpoena. The CEO personally relied on a national five-city study to rebut the same consumer-harm theory Compass’s Seattle/King County NWMLS complaint depends on narrowing. A plaintiff whose market definition shifts between forums based on tactical advantage has defined markets for litigation purposes, not economic purposes — and the CEO just publicly endorsed the forum that contradicts the live Washington pleading.

Move 3: Timing inside the statutory-effective-date window. Paragraph 43 of Document 88 establishes that Compass knows its Private Phases will violate Washington state law when SSB 6091 takes effect on June 11, 2026. The April 16 post lands 56 days before that effective date, on the public Facebook account of the CEO of the counterclaim defendant, defending the double-ending mechanism the same statute is designed to eliminate. The post is party-admission evidence that Compass intends to continue operating — and publicly defending — the mechanism through the statutory transition. The evidentiary predicate for NWMLS’s declaratory judgment count at Document 88 strengthens without a deposition.

Contact mcai@mindcast-ai.com to partner with us on Predictive Law and Behavioral Economics + Game Theory Foresight Simulations. To deep dive on MindCast upload the URL of this publication into any LLM (preferably ChatGPT or Gemini for magazine style works) and prompt ‘reconstruct MindCast framework with three degrees of cited sub links.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure.

III. Why the Specimen Is a Self-Disclosure Trap Event, Not Just a Cross-Forum Event

MindCast AI’s The Cybernetics of Compass Holdings’ Narrative Control Architecture formalized the Self-Disclosure Trap as the eighth emergent pattern across the Compass corpus: “Compass’s most damaging evidence is self-generated. The exposure requires no investigation — only compilation.” The Counterclaim That Closed Compass’s Antitrust Thesisoperationalized the pattern inside federal litigation — documenting how NWMLS’s April 2 counterclaim filed the “negative insights” phrase, the Three-Phased Marketing Strategy (3PM) definitions, and the Disclosure-Form-versus-earnings-call contradiction into Document 88 as pre-discovery evidentiary anchors.

Reffkin’s April 16 post is a Self-Disclosure Trap specimen in the purest form the pattern produces. Three mechanics operate simultaneously.

Self-generated CPA deceptive-practice reinforcement. Document 88’s CPA count at Paragraph 23 quotes Compass’s own internal marketing materials describing the “negative insights” mechanism — the systematic stripping of days-on-market and price-drop history from NWMLS listings after the Private Phase. CPC’s report documents the 20%+ double-ending rate as the measurable output of the same routing-control architecture that produces the “negative insights” suppression. Reffkin publicly endorsed the 20%+ figure — on his personal Facebook account, in his own voice, as CEO of the counterclaim defendant — three days after CPC published. The endorsement supplies NWMLS’s trial counsel a self-authenticating admission that the routing-control architecture produces the output the CPA count identifies as deceptive. No subpoena required. No deposition required. A URL and a timestamp.

National-market estoppel activation. Reffkin personally relied on CPC’s national five-city frame as favorable evidence. The reliance is timestamped, public, and attributable. The Counterclaim publication’s market-definition lock analysis identifies judicial estoppel as the available motion when a plaintiff’s market definition shifts between forums. The April 16 post moves the shift from Dr. Aron’s SDNY expert testimony (defensible as a witness’s framework) into the CEO’s personal public communication (indefensible as anything other than the plaintiff’s own position). The estoppel predicate strengthens at the individual-actor level the defense cannot disclaim.

Paragraph 43 public-defiance signal. Document 88’s Paragraph 43 establishes Compass’s knowledge that the Private Phases will violate Washington law after June 11. Reffkin defending the double-ending mechanism on April 16 is the CEO publicly continuing to advocate for conduct Compass’s own federal pleading acknowledges will be unlawful in 56 days. The post functions as evidence of continued-operation intent — material to the scope of any injunction NWMLS seeks, material to the willfulness element of CPA treble damages, and material to the goodwill-impairment analysis auditors apply to the Anywhere acquisition premium.

IV. The Triptych Parallel — Live Transaction-Level Demonstration

The Counterclaim That Closed Compass’s Antitrust Thesis Section IV documented Tere Foster and Moya Skillman’s Triptych estate listing — Tom Kundig-designed, Lake Washington, Bellevue — privately marketed at $79 million without a publicly listed street address, then publicly presented at $65 million on March 26, 2026. An 18% price reduction. The Triptych listing is identified in the Counterclaim analysis as the live transaction-level demonstration of the “negative insights” mechanism: a buyer encountering Triptych on the MLS at $65 million would see the current ask without knowing the property had been privately marketed at $79 million, without knowing how long the property circulated within the Compass network, and without the suppressed days-on-market record that would otherwise inform negotiating position.

Reffkin’s April 16 rate-parity defense of the double-ending mechanism lands 21 days after Triptych publicly documented the exact price-drop suppression the CPA count indicts. The temporal proximity matters because NWMLS trial counsel operates a discovery calendar in which Compass agents’ public conduct feeds directly into the deposition preparation architecture The Antitrust Litigation Trap Compass Built for Itself Section IV catalogued. Nelson, Huff, and Skillman sit at the intersection of Compass’s Washington legislative campaign and its pre-MLS marketing architecture. Reffkin’s April 16 post sits at the CEO layer above that deposition architecture — and the post cites a report whose methodology the Triptych listing perfectly illustrates.

The Visual Synthesis publication’s MindCast Simulation probability bands moved decisively toward P70 NWMLS prevail-or-favorable-settlement after the April 2 counterclaim filing. The April 16 post is a data point strengthening the P70 assessment. Each additional self-generated admission inside the discovery window narrows Compass’s summary judgment maneuvering space further.

V. The PR-Blitz Signature — Debt-Narrative Correlation in Real Time

The initial analytical observation in the draft’s predecessor noted Reffkin’s April 16 post as a delegation upshift — the CEO personally stepping forward in a manner that broke the Nelson-Huff executive-buffer pattern documented in State Power vs. Compass Private Exclusives as the Delegation Downshift. The observation is correct but undersized. Connected to the Debt-Narrative Correlation framework established in The Cybernetics of Compass Holdings’ Narrative Control Architecture, the specimen’s institutional significance becomes fully visible.

The Debt-Narrative Correlation holds that Compass’s rhetorical intensity tracks balance-sheet constraints, not market conditions. The Counterclaim publication characterizes the March 19-20 sequence — Zillow dismissal, SSB 6091 signing, fiduciary-duty LinkedIn carousel, open letter naming NWMLS as a retaliatory enforcer — as “the most intense single-week escalation in the correlation’s documented history.” Reffkin’s April 16 CPC quote card is the continuation of that blitz into the post-counterclaim phase, now directed at appropriating an independent consumer-protection report as defensive evidence.

The delegation-upshift pattern clarifies when read against the correlation. Compass’s institutional reflex under scrutiny at the pre-blitz stage was the Delegation Downshift — send a subordinate, keep the executive buffer intact, insulate the Regional VP from the cross-examinable record. The blitz phase inverts the reflex because the scale of the narrative collision exceeds what subordinate-level messaging can absorb. No Managing Director can brand-manage a CPC report landing three days earlier. No Regional VP can defend a 20%+ double-ending rate by pivoting to seller-choice vocabulary. The CEO has to step forward because the buffer mechanism has become a bottleneck. The delegation upshift is not merely the opposite of the Delegation Downshift — the delegation upshift is the institutional signature of a firm whose debt-narrative correlation has crossed the threshold at which executive buffering costs more than executive exposure.

At $2.6 billion in post-merger debt, zero full-year GAAP profit history, four counterclaim counts with mandatory treble damages exposure under the CPA, and 56 days to the statutory effective date that voids the Layer 3 acquisition premium, Reffkin personally metabolizing a CPC report on Facebook is not confidence. The post is the most publicly visible form of solvency pressure the correlation produces.

VI. Compass v. Zillow Dismissal — Altered but Not Resolved Forward-Lock Geometry

Context on the Compass v. Zillow status matters for framework calibration. Compass voluntarily dismissed the Zillow antitrust suit without prejudice on March 18, 2026, following Judge Vargas’s February 6 denial of Compass’s preliminary injunction on all claims and following Zillow’s March 17 announcement of a revised Listing Access Standards policy (Zillow Preview). Reffkin announced the dismissal on social media, framing the voluntary withdrawal as a victory produced by Zillow’s policy “reversal.”

The dismissal altered but did not resolve the forward-lock geometry The Compass Narrative Inversion Playbook Section VIII identified. The Zillow complaint’s factual allegations remain unrepudiated in the public record. A voluntary dismissal without prejudice neither confesses error nor retracts the underlying legal theory. Reffkin’s sworn testimony during the four-day PI hearing — the 94% MLS terminal rate, the Black Box design rationale, the Coming Soon data suppression concession — remains permanent federal record available to NWMLS trial counsel under FRE 801(d)(2) as party admissions, as The Counterclaim That Closed Compass’s Antitrust Thesis Section II documented.

The NWMLS case carries the full cross-forum inversion weight the Zillow case once shared. Compass’s Western District of Washington complaint advances the restricted-visibility-harms-consumers theory. Compass’s Washington legislative record opposes the concurrent-marketing requirement on the opposite theory. The irreconcilable positions still coexist. Reffkin’s April 16 post operates against this altered but structurally stable geometry — and compounds the geometry by adding a national-market estoppel vector Compass’s NWMLS pleading cannot absorb.

VII. Forum Count Progression After the April 16 Specimen

Compass’s Cross-Forum Contradictions documented six forums. The April 16 post populates a seventh. The seventh forum’s distinction from the earlier six is the post’s operation inside an active federal discovery window with a pending counterclaim.

Federal court — SDNY, Compass v. Zillow — dismissed without prejudice March 18, 2026, factual allegations unrepudiated.

Federal court — Western District of Washington, Compass v. NWMLS — active, October 2026 trial, four-count counterclaim filed April 2, 2026.

State legislature — SSB 6091 testimony — permanent legislative record, 141-1 final passage.

Investor communications — Q1 2025 earnings call — “there is no downside” admission against Disclosure Form warnings.

Consumer marketing — compass-homeowners.com — “liberation from organized real estate.”

Agent social media — Moya Morgan Skillman, February 27, 2026 — commission-capture framing delivered to consumers as a feature.

CEO social media on Redfin launch — Reffkin, February 28, 2026 — “premium placement” and MLS-enforcement delegitimization.

CEO appropriation of independent consumer-protection report — Reffkin, April 16, 2026 — CPC’s measurable output reframed as rate-parity defense, inside active NWMLS discovery window.

Each incremental forum destroys the informational compartmentalization the earlier positions depended on. Cross-forum visibility crosses the Stigler information-sufficiency threshold and renders the compartmentalized strategy mathematically unsustainable, as The Dual Nash-Stigler Equilibrium Architecture established. The April 16 post accelerates the crossing because the post itself introduces a document — CPC’s report — into Compass’s public-facing defense corpus, and the introduced document internally contradicts every position Compass advances in every other forum.

Self-impeachment through selective quotation. Reffkin’s quote card publicly endorses the 20%+ double-ending figure in the CEO’s own voice. The figure is now attributed to Compass’s own citation practice, not just to CPC’s independent measurement. Any subsequent Compass argument that CPC’s methodology is flawed, that the sample is unrepresentative, or that the rate is inaccurate becomes structurally harder to advance — the CEO personally quoted the number as reliable. The quote card is a self-authenticating admission against interest of the measurable output CPC identified.

VIII. Attribution Signatures That Make the Specimen Part III Material

Three attributes make the April 16 post analytically distinctive and preserve the specimen’s evidentiary value for the forthcoming trilogy installment.

Attribution is unambiguous. Robert Reffkin personally, first person, public account, timestamped April 16, 2026. Not a government-affairs deputy. Not a regional vice president. Not an aligned broker. Not an astroturf affiliate. The CEO, directly. Institutional readers track delegation movement in both directions. The delegation upshift signals that Compass’s internal threat assessment of CPC exceeded the executive-buffering threshold.

The selected quote hands CPC the opening for direct public response. CPC’s report frames the 20%+ aggregate rate not as its finding but as the floor above which Compass’s routing-control architecture extracts additional value at the luxury and high-price tier. Reffkin’s decision to foreground the rate-parity sentence creates an entry point for CPC — and for MindCast AI — to reintroduce the structural argument the post was designed to suppress.

The post functionally concedes the 20% figure. The number is now in the Compass CEO’s own voice, cited approvingly, deployed as a defensive exhibit. Every subsequent institutional actor — state attorneys general, congressional investigators, plaintiffs’ counsel in consolidated litigation, goodwill auditors at Anywhere brands — now operates against a baseline the Compass CEO publicly endorsed. The concession moves a disputed empirical point into the settled-fact column.

IX. Deposition-Layer Consequence for the Reffkin Notice

The Visual Synthesis publication’s Section IV identified Nelson, Huff, and Skillman as the deposition layer running beneath Reffkin’s enterprise-level deposition. As the Visual Synthesis noted, Reffkin’s deposition notice in the NWMLS case carries the greatest individual settlement pressure because he has already testified four days in the Zillow proceedings and understands what cross-examination produces when the cross-examiner holds his own sworn statements as impeachment material.

The April 16 post is now part of that impeachment material. NWMLS trial counsel taking Reffkin’s deposition in Compass v. NWMLS can place the Facebook post on the record and ask a sequence no prepared answer resolves cleanly:

“Mr. Reffkin, on April 16, 2026, you publicly cited the Consumer Policy Center’s national five-city study as evidence that Compass’s double-ending rate is comparable to other firms. Is that your position?”

“Compass’s complaint in this proceeding defines the relevant market as Seattle and King County. Is the Consumer Policy Center’s five-city national study favorable evidence for Compass’s conduct in the Seattle market specifically, or in markets generally?”

“Dr. Aron testified in the SDNY Zillow preliminary injunction hearing that the relevant market for online home search is national. You have now publicly endorsed a national-market analytical frame as favorable to Compass. Does Compass’s Seattle-and-King-County market definition in this proceeding reflect Compass’s economic understanding of the business, or does the definition reflect a litigation tactic?”

“Paragraph 43 of the counterclaim states Compass knows the Private Phases will violate Washington state law on June 11, 2026. Your April 16 Facebook post defends the double-ending mechanism 56 days before that effective date. Is it Compass’s position that the conduct defended on April 16 will continue through June 11?”

No prepared answer protects Compass’s litigation posture across the full sequence. Affirming the April 16 post’s substantive argument activates national-market estoppel. Disclaiming the post undermines the CEO’s public communications credibility in every other forum. Parsing the two positions invites the follow-up question about whether Compass’s market definition is economically grounded or tactically constructed. The deposition sequence is the specific institutional mechanism through which the Self-Disclosure Trap converts public CEO communication into summary-judgment evidence.

The post adds no new deposition topic — the NWMLS market definition was already a deposition topic, the Paragraph 43 compliance issue was already a deposition topic, the cross-forum contradiction was already a deposition topic. The post strengthens every existing topic with a public CEO statement attributable to no one else, timestamped inside the discovery window, produced without prompt or subpoena.

X. Part III Specimen Monitoring Categories

The Reffkin April 16 quote card is Specimen 1 of the Self-Disclosure Trap consolidation the opening Context section positioned. Part III publication requires additional specimens of comparable analytical weight to establish that the specimen documents a pattern rather than a single tactical deployment.

Specimens to monitor for Part III maturation:

CEO and executive social media activity appropriating institutional reports — state AG filings, additional consumer-protection organization analyses, academic publications, goodwill-impairment guidance.

Compass v. NWMLS substantive filings in the Western District of Washington — continued reliance on the restricted-visibility-harms-consumers theory through summary judgment briefing, discovery disputes that surface additional internal marketing materials, deposition transcript excerpts entering the public record.

Compass’s response to subsequent state legislative introductions (Illinois, California, New York, Texas) — replication of Washington apparatus, opt-out amendment reintroduction, delegation patterns.

Q1 and Q2 2026 earnings call treatment of the CPC report, the NWMLS counterclaim, and the SSB 6091 compliance cost — divergence or alignment between investor-facing framings and the federal court record.

Partnership infrastructure expansions beyond Redfin — Zillow Preview engagement patterns, MLS-alternative distribution channels, portal-level integration announcements.

Goodwill-impairment disclosure movement at Anywhere brand level as state regulatory environments diverge from acquisition underwriting assumptions. The April 2026 audit cycle will be the first to encounter Paragraph 43 in the federal record.

Deposition-layer specimens — Nelson, Huff, and Skillman discovery-stage conduct during the NWMLS discovery window, including additional social media activity, public statements at industry events, and responses to subpoenas or notices.

Five to seven additional specimens across two or more categories reach sufficient volume for Part III publication.

XI. Institutional Reader Implications

For state attorneys general monitoring Compass conduct in anticipation of UDAP or antitrust enforcement action, the April 16 post is evidence that Compass’s CEO will personally deploy public communications as part of the firm’s defense architecture — including public endorsement of figures that reinforce the deceptive-practice predicate. The enforcement implication matters at the deposition and interrogatory stage. The CEO is an active content producer, the content is on the record, and the content contradicts both the company’s client Disclosure Form and the company’s federal litigation allegations.

For plaintiffs’ counsel in consolidated real estate antitrust litigation, the April 16 post is a self-authenticating public exhibit connecting the 20%+ double-ending rate to the CEO’s direct endorsement and to the national-market analytical frame. The exhibit requires no foundation beyond the public URL and the timestamp. The exhibit simultaneously serves as impeachment material against any Compass expert witness who attempts to characterize the CPC methodology as unreliable — the CEO personally relied on it.

For state legislators in jurisdictions considering concurrent-marketing transparency legislation, the April 16 post confirms Compass’s behavior pattern under pressure: deploy confusion artifacts rapidly, bypass substantive engagement, exploit audience segregation. The Washington evidentiary record remains portable. The Reffkin CPC post adds to that record.

For NWMLS trial counsel, the April 16 post is new impeachment material for the Reffkin deposition, a strengthened judicial-estoppel predicate for the market-definition lock motion, and evidence of continued-operation intent relevant to the scope of any injunctive relief and the willfulness element of CPA treble damages.

For institutional subscribers tracking Compass’s solvency geometry, the April 16 post is a behavioral signature of continued acceleration rather than retrenchment — the pattern Death by a Thousand Depositions identified as the core structural vulnerability. A firm facing converging regulatory, litigation, and market constraints that responds with narrative production rather than operational adjustment is a firm whose story has become the asset and whose debt service depends on the story’s continued propagation. The Debt-Narrative Correlation predicts exactly the pattern the April 16 post manifests.

XII. Conclusion

Reffkin’s April 16 Facebook post is small in format and large in structural implication. A single quote card executes three MindCast AI predicted behaviors simultaneously — narrative inversion, cross-forum contradiction, and scale neutralization — while extending the contradiction matrix into an eighth forum and, more significantly, operating inside the active Compass v. NWMLS discovery window as a Self-Disclosure Trap specimen with direct party-admission consequences under FRE 801(d)(2).

The Zillow dismissal altered the forward-lock geometry but did not resolve the underlying framework. The Compass v. NWMLS litigation remains active, the Washington legislative record remains permanent, the four-count counterclaim with mandatory treble damages under the CPA is pending, and the Compass CEO continues producing the narrative collisions the framework predicted. The specimen arrives in the correct register for the planned Compass Trilogy Part III — a Self-Disclosure Trap consolidation — but does not yet constitute sufficient volume for trilogy publication.

The market analysis preserves the specimen in the record, maps the specimen onto the Self-Disclosure Trap framework, identifies the deposition-layer consequences for the forthcoming Reffkin notice, and specifies the additional behavioral categories required before Part III reaches publication readiness.

Compass is not retrenching. Compass is accelerating. Each acceleration inside the discovery window produces a new self-authenticating admission. MindCast AI is assembling them. The counterclaim filed the receipt. The CPC quote card added a line item.

Source Publications

The Antitrust Litigation Trap Compass Built for Itself (April 6, 2026)

The Counterclaim That Closed Compass’s Antitrust Thesis (April 3, 2026)

Compass Double-Sided Commissions — Consumer Policy Center Measures the Output, MindCast Models the System (April 15, 2026)

The Compass Narrative Inversion Playbook (February 4, 2026)

Compass’s Cross-Forum Contradictions (February 28, 2026)

The Compass Commission Consolidation Strategy and Real Estate Marketing Transparency (February 19, 2026)

The Compass-Anywhere Address Suppression Calculus (February 22, 2026)

The Cybernetics of Compass Holdings’ Narrative Control Architecture

State Power vs. Compass Private Exclusives: Legislative Testimony as a One-Way Gate (February 6, 2026)

Death by a Thousand Depositions: Compass’s Multi-Vector Regulatory Collapse (February 21, 2026)

The Dual Nash-Stigler Equilibrium Architecture (January 2026)

External Sources

Stephen Brobeck, Compass Expansion: New Data on Market Share and Double Ending (Consumer Policy Center, April 2026).

NWMLS Answer, Affirmative Defenses, and Counterclaim — Document 88, Case No. 2:25-cv-00766-JNW (W.D. Wash., April 2, 2026).

Compass International Holdings, Compass to Dismiss Lawsuit Following Zillow Ban Reversal (Press Release, March 18, 2026).

Taylor Anderson, Compass Drops Antitrust Lawsuit Against Zillow (Inman, March 18, 2026).

Robert Reffkin, Facebook post, April 16, 2026 (on file).