MCAI Lex Vision: The Motion Compass Filed and the Architecture It Could Not Address

Three Structural Absences in the April 23 Motion to Dismiss Reveal What Compass Cannot Defend at Summary Judgment

Compass’s Motion to Dismiss is optimized only for procedural dismissal, not defense. The omissions identify the parts of the record Compass cannot carry into summary judgment.

Three counterclaim elements anchored in Compass’s own self-generated record go entirely unaddressed across 29 pages and 8,356 words: the phrase “negative insights” (Compass’s own internal terminology for days-on-market and price-drop information stripped from Northwest Multiple Listing Service (NWMLS) listings); counterclaim paragraph 43(establishing Compass’s knowledge that the Private Phases of its Three-Phased Marketing Strategy (3PM) will violate Washington state law on June 11, 2026, when Substitute Senate Bill 6091 (SSB 6091) takes effect); and the Q1 2025 Reffkin earnings call statement that private exclusives carry “no downside” for sellers, contradicting Compass’s own client Disclosure Form acknowledging the practice may reduce buyers, offers, and final sale price. The motion attacks pleading sufficiency and standing geometry — questions a federal court resolves at the four-corners-of-the-pleading stage — while leaving the self-generated evidentiary record entirely outside the brief.

Under the MindCast AI Litigation v. Leverage diagnostic framework, the motion classifies as tactical litigation deploying chutzpah, narrative coercion, and asymmetric stakes. The plaintiff brokerage characterizes its enforcement-defendant cooperative as the “monopolist” suing “its own customer” for “daring to stand up for competition and homeowner choice” — moral reversal in textbook form, where the actor whose conduct triggered the enforcement reframes the enforcer as the aggressor. The motion is the front-parlor document. The architecture it cannot defend is the back yard. The audiences with access to both — federal courts at summary judgment, state attorneys general at investigation, broker-members evaluating affiliation, and prospective partners conducting pre-deal due diligence — read both.

The publication addresses the two Skillman moments at the center of the structure, the system shift the litigation is a lagging mechanism trying to control, what the motion argued, what it could not address and why, the doctrinal trap that closes whether the motion wins or loses, the genuine pressure points, the strategy set Compass now faces, and the forward conditions under which the structural model holds or fails.

I. The Skillman Moment

The structure becomes legible at the point where internal language, external conduct, and market outcome align. Two instances in the Compass v. NWMLS record meet that threshold.

A Skillman moment is the point at which the system’s hidden mechanism becomes publicly legible through a single, concrete instance of behavior. Not theory. Not narrative. A specimen. The diagnostic does three things simultaneously: it collapses abstraction into observable conduct, it bridges narrative to evidence, and it forces interpretation from every observer with access to the public record. A Skillman moment is not the same as a strong argument or a damaging fact. The two specimens documented below are not arguments NWMLS makes against Compass. They are the architecture Compass built revealing itself in Compass’s own language and Compass’s own transactions, available to any reader of the public record without further investigation. The diagnostic separates evidence the litigation produces from evidence the system produces about itself.

A note on terminology. The original Skillman Moment in the MindCast corpus refers to Moya Skillman’s February 27, 2026 Puget Sound Business Journal commentary applying Reffkin’s “seller choice” framing to SSB 6091 — the specific cross-forum contradiction specimen catalogued in The Compass Narrative Inversion Playbook. The lowercase “Skillman moments” used throughout the present analysis names the diagnostic category the original specimen instantiates: any instance where internal language, external conduct, and market outcome align to make the system’s hidden mechanism publicly legible.

The linguistic Skillman moment: “negative insights.” Compass’s own internal label for information systematically withheld from buyers — days-on-market accumulation and price-drop history — converts an abstract allegation into a disclosed design choice. The phrase is not a court’s characterization of Compass’s conduct. The phrase is Compass’s own corporate vocabulary for the information it engineered NWMLS listings to suppress. Days-on-market is the standard market signal of how long a property has sat unsold. Price-drop history is the standard market signal of how the seller’s reservation price has adjusted to demand. Compass identified both as “negative insights” and built the 3PM architecture to remove them. The internal terminology establishes that the suppression is design rather than accident.

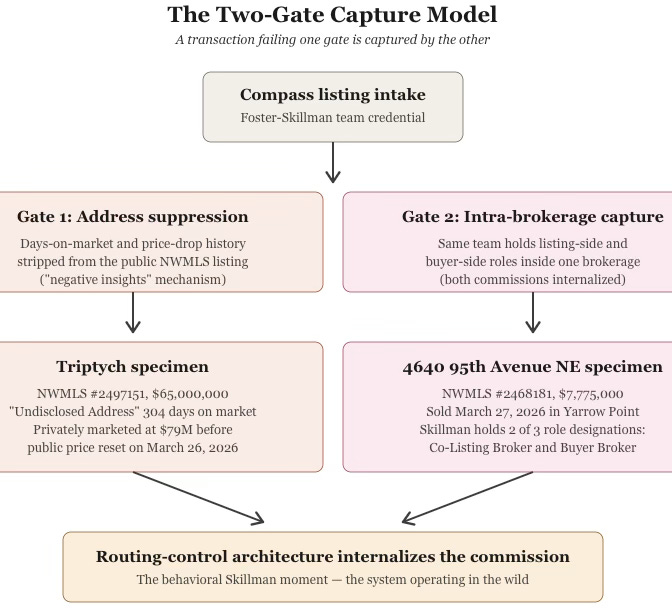

The behavioral Skillman moment: the Two-Gate specimens. NWMLS Listing #2497151 (Triptych, $65 million, “Undisclosed Address,” 304 days on market, privately marketed at $79 million before the public price reset) and NWMLS Listing #2468181 (4640 95th Avenue NE, sold March 27, 2026 at $7,775,000, with Moya Skillman holding two of three role designations on the same single sale inside the same brokerage) show the architecture operating in real transactions, under a single Foster-Skillman team credential, in the same Washington county, at the same moment. Gate 1 is address suppression at the listing layer. Gate 2 is intra-brokerage dual representation at the closing layer. The same team operates both gates simultaneously. The architecture is no longer abstract. The transaction-pattern foundation for the two-gate framework was developed in the Address Suppression Calculus game-theoretic analysis of 130 Seattle ultra-luxury transactions.

The two specimens are not allegations. They are the system revealing itself.

The two specimens do three things simultaneously. They collapse abstraction into observable conduct — the routing-control architecture becomes a phrase Compass coined and a transaction Compass closed. They bridge narrative to evidence — what the motion characterizes as “innovation” and what the legislative record characterizes as “fair housing intervention” both refer to the same documented mechanism, with the same documented outputs, in the same public record. They force interpretation from every observer — the federal court evaluating the rule-of-reason record at summary judgment, the state attorney general building an Unfair or Deceptive Acts or Practices (UDAP) enforcement predicate, the broker-member evaluating the cooperative’s enforcement against one member’s conduct, the prospective partner conducting pre-deal due diligence against the same evidentiary anchors.

Everything that follows explains what these two moments already establish. The motion is the procedural instrument. The Skillman moments are the structural condition the motion cannot displace.

II. The System State: Private Enforcement to Statutory Enforcement

The Compass v. NWMLS litigation is not a fraud-versus-no-fraud dispute. It is not an MLS-versus-innovation dispute. The framing fails because the framing misidentifies the system the litigation operates in.

The actual system shift is precise and measurable.

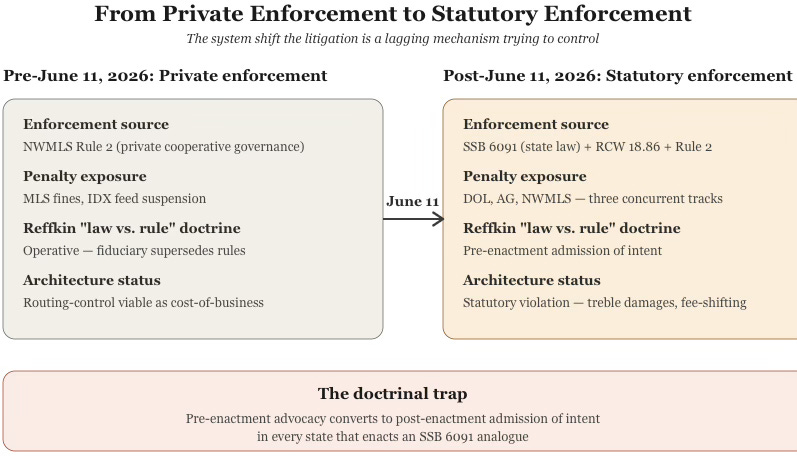

Pre-2026 environment: NWMLS rules enforced market-transparency behavior. The rules operated as private cooperative governance — binding on member brokerages by contract, enforceable through fines and Internet Data Exchange (IDX)feed suspension, but not statutorily mandated. A sophisticated firm operating at scale could rationally evaluate compliance against fine exposure as a cost-of-business calculation. The Reffkin Inman op-ed of March 25, 2026 formalized that calculation as doctrine: MLS mandates are “private contractual rules, not law,” and state fiduciary duty statutes “supersede them.” The doctrine works wherever the gap between MLS rules and state law remains open. In 46 states as of April 2026, that gap is fully open.

Post-June 11, 2026 environment in Washington: state law enforces market-transparency behavior. SSB 6091 codifies concurrent-marketing requirements that align with NWMLS Rule 2 and contradict the Private Phases of 3PM. The 141-1 legislative vote — 49-0 in the Senate, 92-1 in the House — establishes the procompetitive justification at the state-law level rather than the cooperative-rule level. The doctrine that worked under private enforcement fails under statutory enforcement. The same conduct that produced a Multiple Listing Service (MLS) fine pre-June 11 produces personal license discipline under Revised Code of Washington (RCW) 18.85, vicarious liability under RCW 18.86.090, and Consumer Protection Act (CPA) exposure under RCW 19.86.090 with mandatory treble damages and fee-shifting after June 11.

The litigation is a lagging mechanism trying to control the transition. Compass filed the federal antitrust complaint in April 2025, eleven months before SSB 6091 passed. The complaint advances the restricted-visibility-harms-consumers theory against NWMLS Rule 2. The April 23 motion to dismiss the counterclaims continues to operate within the pre-2026 framing, characterizing NWMLS as a private cartel imposing rules on its members. The framing does not engage the post-June 11 environment in which NWMLS Rule 2 is no longer a contestable private cooperative governance mechanism but anticipatory compliance with state law that the federal court evaluates under Parker v. Brown state-action immunity rather than Sherman Act rule-of-reason.

The state-level legislative ratchet operates jurisdiction by jurisdiction. Each state that enacts an SSB 6091 analogue converts the same conduct from a fine-versus-revenue calculation into a license-versus-revenue calculation. The doctrine compounds liability rather than reducing it. The litigation slows the transition in any individual jurisdiction. The litigation does not reverse the transition at the system level.

Each forum output becomes the next forum’s input, creating a feedback loop that reinforces the underlying structure regardless of individual outcomes.

Every other section of the analysis operates against this system state.

III. What the Motion Argues

The motion organizes around five attack lanes. Article III standing — both whether NWMLS suffered concrete injury and whether NWMLS can sue on behalf of “consumers” or “the public.” Declaratory judgment dismissal — on grounds of redundancy, mootness, and insufficient specificity. Fraudulent misrepresentation — attacked on Rule 9(b) particularity grounds. Consumer Protection Act — attacked on the fresh Montes v. SPARC doctrine that “objective economic loss” is required, not value-degradation theories. Tortious interference — attacked on the circular-logic argument that NWMLS rules under antitrust attack cannot simultaneously serve as the duty source whose violation establishes “improper means.”

The standing argument leads because standing is the only argument with full disposition potential. The motion’s most analytically interesting passage sits at page 11: Compass argues that at most seven properties out of 11,640 NWMLS active listings could have been affected, yielding 0.00060137457% degradation — “a quantum that could not even qualify as de minimis.” The arithmetic gives the Court a numerical hook for dismissal without reaching the merits. It does not survive discovery, but at the pleading stage it has bite.

The Rule 9(b) attack is genuine. NWMLS’s pleading names no deceived buyer, no specific listing, no transaction. Vicarious liability under RCW 18.86.090 keeps the fraud count alive but does not cure the particularity gap.

The causation-inversion argument at page 18 is the sharpest tactical paragraph in the motion. NWMLS admits at counterclaim paragraph 35 that NWMLS demanded the at-issue properties be listed. Compass weaponizes the admission: you forced the listings, then called them misleading.

The circular-logic frame on tortious interference exploits the analytical conflation between two duty sources. Compass cites Greensun v. City of Bellevue for the proposition that “improper means” requires an independent duty source — and argues the NWMLS rules under antitrust attack cannot serve as that source. RCW 18.86.030 supplies a statutory duty source independent of the rules, but the motion treats the two as a single vulnerable hook.

The Montes v. SPARC citation is the genuine doctrinal threat. The Washington Supreme Court held on April 2, 2026 — the same day NWMLS filed — that “objective economic loss” is required for CPA injury. NWMLS’s value-degradation theory does not satisfy that standard on the current pleading.

Taken on their own terms, the five arguments are competent litigation craft. Some will succeed. The declaratory judgment count will likely be dismissed under Englewood Lending v. G&G Coachella and the Ninth Circuit’s reluctance to entertain reactive declaratory actions. The CPA count will likely be dismissed with leave to amend. The fraud count requires amendment for particularity but survives in concept. The tortious interference count survives if NWMLS articulates the statutory duty source distinctly from the cooperative-rule duty source. The standing argument with prejudice is the lowest-probability outcome and the only outcome that would meaningfully disrupt NWMLS’s bilateral damages architecture.

A motion that wins three of five counts and loses on standing-with-prejudice achieves nothing structurally. The bilateral damages architecture survives. The treble-damages exposure under RCW 19.86.090 survives. Discovery opens. The Reffkin deposition proceeds. The June 11 SSB 6091 effective date arrives during the discovery window. The October 2026 trial calendar holds.

The motion operates within a delay-dominant enforcement game, where the objective is cost and timing control rather than doctrinal resolution.

The structural geometry is why the absences in the motion matter more than the arguments in it.

Contact mcai@mindcast-ai.com to partner with us on Predictive Cognitive AI in Law and Behavioral Economics. To deep dive on MindCast work in Cognitive AI upload the URL of this publication into any LLM and prompt ‘reconstruct MindCast framework with three degrees of cited sub links.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure.

Related MindCast AI Research: Run-Time Causation — Causal-signal arbitration framework; institutional evaluation of competing causal narratives. Nash–Stigler Equilibria — Equilibrium concept explaining how institutional incentives stabilize inefficient outcomes. Predictive Institutional Cybernetics — Markets as feedback systems governed by signal processing, delay, and equilibrium stabilization. Cybernetics Foundations — Theoretical lineage from Wiener through Ashby, Beer, Bateson, and Hayek into MindCast’s CDT/Vision architecture. Double-Sided Rational Ignorance (DSRI) — How market participants fail to perceive aggregate harm when information remains fragmented.

IV. What the Motion Does Not Address

Three structural absences run through the brief. Each absence corresponds to a self-generated evidentiary anchor Compass cannot remove from the record at the pleading stage and cannot defend on the merits at summary judgment.

The “Negative Insights” Phrase

Section I named the linguistic Skillman moment. Section IV tracks the motion’s response to it.

The phrase does not appear in the motion. Not in the fraud section, where Compass argues that “private exclusives” and “coming soon” are not deceptive labels. Not in the CPA section, where Compass argues the labels did not deceive substantial portions of the public. Not in the tortious interference section, where Compass argues no statutory duty was violated. Not in the standing section, where Compass argues NWMLS suffered no concrete harm. The phrase is the deceptive-practice anchor of the entire CPA count, and the motion responds to a counterclaim built on labels rather than to the counterclaim NWMLS actually filed.

The reason the motion does not engage the phrase is that the phrase cannot be defended on the merits. A litigation defense that engages “negative insights” has to either (a) deny the suppression, which contradicts Compass’s own marketing materials, (b) defend the suppression as legitimate, which exposes the architecture’s purpose, or (c) characterize the suppression as immaterial to buyers, which contradicts the term Compass applied to it.

The motion chooses option (d): do not engage. The choice is the strongest possible signal that the phrase is the most damaging element of the counterclaim record. The motion’s silence preserves the Skillman moment rather than displacing it.

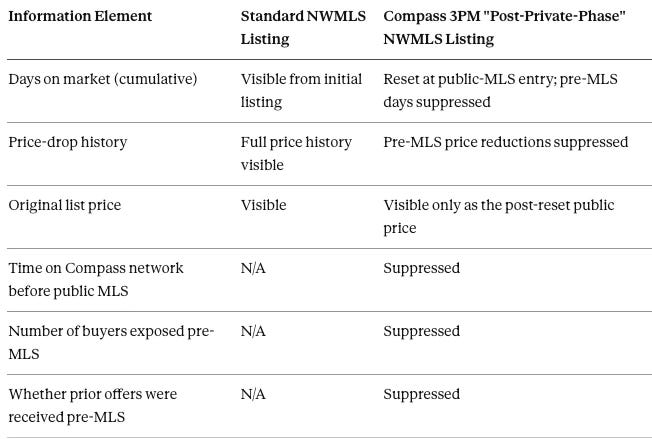

The information asymmetry the phrase names is concrete and measurable. A buyer encountering a standard NWMLS listing receives one set of information. A buyer encountering a listing that passed through Compass’s Private Phases of 3PM receives a different set:

The Triptych specimen makes the table operational. The estate was privately marketed at $79 million within the Compass network before being publicly presented at $65 million on March 26, 2026. A buyer encountering Triptych on the MLS at $65 million sees the current ask. The buyer does not see the prior $79 million asking price, the duration of pre-MLS marketing, or the pre-MLS demand response that drove the 18% price reduction. Each of those data points is what the standard market signal of days-on-market and price-drop history would normally convey. Compass’s internal terminology — “negative insights” — names the suppressed information from the seller’s perspective. From the buyer’s perspective, the suppressed information is the signal of the seller’s reservation price, the elasticity of demand at higher price points, and the negotiating leverage the buyer would otherwise possess. The asymmetry is the architecture, not a byproduct of it.

Counterclaim Paragraph 43 and the Statutory Trap Door

Counterclaim paragraph 43 reads: “Compass knows that when the Public Marketing Law takes effect on June 11, 2026, the Private Phases and related practices will violate state law.”

The motion’s engagement with that paragraph consists of two sentences in footnote 14: “3PM fully complies with this new law which, contrary to NWMLS’s suggestion, neither entitles NWMLS to listings nor codifies its rules. At any rate, the statute is not yet in effect and is irrelevant to their claims. CC ¶39.” That is the entire treatment of SSB 6091 in the brief. Two sentences. Both conclusory. No analysis of why 3PM “fully complies” with a statute that prohibits “marketing the sale or lease of residential real estate to a limited or exclusive group of prospective buyers or brokers... unless the real estate is concurrently marketed to the general public and all other brokers.” No engagement with the legislative history establishing that the statute was enacted to address the very practice Compass calls innovation. No engagement with paragraph 43’s claim that Compass knows the practice will be unlawful in 56 days.

The “not yet in effect” point is technically accurate and analytically empty. The relevant question is what the post-June 11 conduct landscape looks like and what a federal court’s evaluation of NWMLS Rule 2 looks like once the rule the rule of reason analysis evaluates is also a rule that Washington state law independently requires. The Parker v. Brown state-action immunity doctrine — 317 U.S. 341 (1943) — holds that private actors enforcing standards mandated by state law cannot be held liable under federal antitrust law for conduct the state itself requires. NWMLS’s rule, post-June 11, becomes anticipatory statutory compliance with a law Washington legislators voted 141-1 to enact. The procompetitive justification federal antitrust courts apply at rule-of-reason analysis becomes structurally unavailable to Compass.

The motion’s silence on paragraph 43 reflects a strategic constraint Compass cannot escape. Any developed engagement with SSB 6091 at the pleading stage commits Compass to a position it cannot walk back at summary judgment. If Compass argues 3PM complies with the statute, the argument requires a statutory construction that contradicts the legislative history and the plain text of the concurrent-marketing requirement. If Compass argues the statute is preempted by federal antitrust law, the argument requires a constitutional theory Compass has not articulated and that no court has accepted in the MLS-rule context. If Compass argues the statute does not apply to 3PM, the argument requires a definition of 3PM that excludes the conduct the statute was enacted to address. Each available position locks Compass into a litigation theory worse than the silence.

The silence is also a tactical surrender on the issue NWMLS most needs preserved for trial. The June 11 effective date arrives during the discovery window. The first SSB 6091 enforcement cycle begins before the October 2026 trial. Every Compass listing in Washington above $5 million during that window becomes evidence of either compliance (in which case the routing-control architecture has been operationally abandoned in the state) or non-compliance (in which case the federal court evaluating NWMLS’s procompetitive justification at summary judgment has direct evidence of the conduct the procompetitive justification addresses). The motion does not engage paragraph 43 because there is no version of engagement that improves Compass’s position at the next stage.

The Reffkin Earnings Call and the Disclosure Form Contradiction

The motion does not address the Q1 2025 earnings call statement by Reffkin that private exclusives carry “no downside” for sellers. The motion does not address Compass’s own client-facing Disclosure Form acknowledging that private exclusive marketing “may reduce the number of potential buyers,” “may reduce the number of offers,” and may reduce “the final sale price.” Both documents are public, simultaneous, and about the same product.

The contradiction is the structural foundation of the Self-Disclosure Trap pattern documented across the analytical literature: Compass’s most damaging evidence is self-generated, the exposure requires no investigation, only compilation. The earnings call is a statement to capital markets under SEC reporting obligations. The Disclosure Form is a statement to clients under Washington broker fiduciary duty obligations under RCW 18.86.030. The two documents make opposite factual claims about the same business practice, simultaneously, in writing, on the public record.

A motion that addresses the contradiction has to either (a) reconcile the two statements, which requires arguing that “no downside” and “may reduce the number of offers” are compatible characterizations, (b) characterize one statement as the operative one and the other as somehow incidental, which requires choosing whether to throw the SEC filing or the client disclosure under the bus, or (c) argue that neither statement bears on the deceptive-practice analysis because both predate the conduct alleged, which requires explaining why a Chief Executive Officer (CEO) representation to capital markets that a practice has no downside is irrelevant to whether the practice harms the consumers the practice operates on.

The motion chooses option (d) again: do not engage. The pattern is consistent across all three structural absences. These omissions persist because they are evidentiary anchors, not pleading defects. The motion’s silence on these three elements is the strongest signal in the brief about which paragraphs Compass cannot defend at the next stage. The signal is available to every reader of both documents.

V. The Eddie Haskell Architecture

Compass presents one narrative per audience. The narratives are individually coherent and collectively incompatible.

To investors: “There is no downside” (Reffkin, Q1 2025 earnings call)

To clients: “May reduce the number of offers” and “may reduce the final sale price” (Compass Disclosure Form)

To the federal court: Innovation, consumer choice, procompetitive disruption suppressed by a monopolist cooperative (April 23 Motion to Dismiss)

To state legislators: Seller choice, privacy protection, fiduciary duty (Compass testimony, SSB 6091 hearings)

To agents: “We have your back” — corporate defense against MLS fines for executing seller-directed marketing plans (Compass-Rocket-Redfin open letter, March 19, 2026)

The contradiction is not accidental. It is required to sustain the model across audiences. The divergence is not error. It is a system requirement.

Each face is internally coherent within the audience it addresses. The faces are mutually incompatible across audiences. The Eddie Haskell architecture works on parents who only see the front parlor. Federal courts at summary judgment, state attorneys general at investigation, broker-members evaluating institutional affiliation, and prospective partners conducting pre-deal due diligence see the back yard.

In the back yard, Compass agents are operating Gate 1 address suppression on NWMLS Listing #2497151 — the Triptych estate, $65 million, “Undisclosed Address, Bellevue, WA 98004,” 304 days on market — a property that was privately marketed at $79 million before being publicly presented at $65 million on March 26, 2026. In the back yard, Compass agents are operating Gate 2 intra-brokerage dual representation on NWMLS Listing #2468181 — 4640 95th Avenue NE in Yarrow Point, sold March 27, 2026 at $7,775,000, with Moya Skillman holding two of three role designations on the same single sale inside the same brokerage. In the back yard, Reffkin is publishing Inman op-eds formalizing the doctrine that fiduciary duty supersedes MLS rules, and publishing Facebook quote cards selectively appropriating Consumer Policy Center reports as defensive evidence seven days before the federal court motion was filed.

Federal Rules of Evidence (FRE) 801(d)(2) admits party admissions across all audiences as substantive evidence. The Reffkin earnings call, the Disclosure Form, the Inman op-ed, the Facebook quote card, the open letter, the Consumer Policy Center report endorsement, the Skillman February 27 social media commentary applying Reffkin’s “seller choice” framing to SSB 6091, the Compass marketing materials internally describing “negative insights” — all are admissible at summary judgment. The motion’s silence on these elements does not remove them from the record. The silence preserves them.

For each audience reading both the motion and the underlying record:

The federal court at summary judgment evaluates the rule-of-reason record that includes Reffkin’s sworn Southern District of New York (SDNY) testimony (94% MLS terminal rate, Black Box design rationale, Coming Soon data suppression concession), the Disclosure Form versus earnings call contradiction, and the post-June 11 statutory landscape that aligns with NWMLS Rule 2.

State attorneys general evaluate the UDAP enforcement predicate that includes the “negative insights” terminology, the 20%+ double-ending rate Reffkin personally endorsed on April 16, the Two-Gate specimens documenting the architecture in operation, and the post-merger common-ownership disclosure problem affecting transactions where buyer and listing agents carry different brand names from the combined Compass-Anywhere portfolio.

NWMLS broker-members evaluate a defendant member arguing about pleading geometry rather than denying the conduct, while the cooperative they operate within faces ongoing erosion from one member’s documented routing-control architecture.

Prospective Compass partners — technology vendors, lenders, title companies, institutional capital allocators — conduct pre-deal due diligence against the same record the federal court will see at summary judgment, including the goodwill impairment question SSB 6091 raises against the Layer 3 acquisition premium.

Brokers evaluating Compass affiliation read the open letter’s “we have your back” pledge against three concurrent enforcement tracks that operate against individual licensees in Washington after June 11 — the Department of Licensing (DOL), the Attorney General (AG), and NWMLS governance — and notice that personal license discipline is not covered by the corporate fine-defense pledge.

The Eddie Haskell architecture does not work on audiences with access to the back yard. The motion is the front-parlor document. The back yard is the public record.

VI. The Doctrinal Trap That Closes Whether the Motion Wins or Loses

Fiduciary duty governs transactions. MLS rules and statutes govern markets. The two systems do not occupy the same decision layer.

An agent who withholds a listing from the MLS to protect a seller’s stated privacy preference has made a transaction-level decision. An agent who systematically routes listings through off-MLS channels to maximize dual-sided commission capture has made a market-level decision. Fiduciary duty governs the first. It has never authorized the second.

The Reffkin Inman op-ed of March 25, 2026 collapses the two layers into a single hierarchy: fiduciary duty supersedes MLS rules, MLS membership is coerced rather than voluntary, MLS fines manufacture conflicts of interest agents must disclose. The April 23 motion is the polite version of that doctrine, translated into Rule 12(b)(6) language for federal court — characterizing NWMLS Rule 2 as an unjustifiable private restriction and predicating the tortious interference defense on the argument that rules under antitrust attack cannot serve as a duty source. The collapse is the mechanism by which a legal obligation to the client becomes legal cover for conduct that harms the market the client depends on for price discovery.

The collapse fails wherever a state legislature has acted. In Washington, RCW 18.86.030 imposes the broker fiduciary duty Compass invokes — and SSB 6091 imposes the concurrent-marketing requirement that codifies the conduct standard NWMLS Rule 2 applies. After June 11, 2026, the two systems occupy the same layer of Washington law, and they are aligned. An agent following Reffkin’s “law supersedes rule” logic in Washington after June 11 is following law that contradicts other law of the same state, with personal licensing discipline, vicarious liability under RCW 18.86.090, and CPA exposure under RCW 19.86.090 with mandatory treble damages and fee-shifting.

The doctrinal trap operates in two directions simultaneously. Forward: every additional state that enacts an SSB 6091 analogue converts Compass’s pre-enactment advocacy record into post-enactment admission of intent to defy state licensing law. The Inman op-ed, the open letter, the agent training materials, and the federal court motion all sit in the public record as evidence that Compass understood the law/rule distinction and chose to treat statutory obligations as mere rules. The doctrine does not collapse in any individual state. The doctrine creates a record that compounds across states. Backward: the doctrine fails at federal antitrust rule-of-reason analysis in Compass v. NWMLS itself. NWMLS’s procompetitive justification — that mandatory listing participation maintains market-wide price discovery, reduces search costs, and prevents the information asymmetries that flow from fragmented private channels — is the same justification that supports SSB 6091. Compass’s own 94 percent MLS sell-through rate, conceded in the Inman op-ed and admissible at summary judgment as a party admission, functions as evidence of market benefit. The motion that contests Rule 2 also contests the statute that enacts the same rule.

For the tortious interference counterclaim specifically, the layer distinction supplies NWMLS’s response to Compass’s circular-logic argument. The duty source is statutory — RCW 18.86.030’s broker disclosure duties, RCW 18.85.361(3)’s licensing standards, RCW 18.86.090’s vicarious liability provisions — and the MLS rules govern cooperative market infrastructure operating at a different decision layer. The two systems are not in circular tension. They occupy different layers of the same regulatory architecture, aligned against the conduct the counterclaim alleges.

The doctrinal trap closes whether the motion wins or loses. Dismissal with leave to amend produces an amended pleading invoking the statutory duty source the original underspecified. Denial of the motion sends the counterclaims to discovery with the statutory duty source already in the trial brief. Dismissal with prejudice — the lowest-probability outcome — closes the trap in the affirmative case, where Compass’s restricted-visibility-harms-consumers theory faces summary judgment evaluation against the same statutory and procompetitive record. The architecture survives every procedural outcome.

VII. The Montes Pressure Point on Consumer Protection Act Injury

Montes v. SPARC Group LLC, 2026 WL 900481 (Wash. April 2, 2026), is the only doctrinal development in the motion that requires careful response from NWMLS. The Washington Supreme Court held — answering a certified federal question — that “objective economic loss” is required for CPA injury, and that subjective disappointment is insufficient to support a Consumer Protection Act claim.

The decision lands the same day NWMLS filed its counterclaim. The timing is coincidental but consequential. NWMLS’s CPA injury theory rests on value-degradation language: that “the value of the information [NWMLS] provides has been severely degraded.” That formulation is closer to the subjective-disappointment characterization Montes rejects than to the objective-economic-loss standard Montes requires. The dispute reduces to whether harm is measurable or merely asserted.

The pressure point is real. NWMLS’s pleading does not allege lost revenue, lost subscribers, or quantifiable economic harm to NWMLS as an entity. The pleading does allege harm to consumers, to broker-members, and to the public — but those alleged harms run to third parties, not to NWMLS itself, and they support the standing analysis Compass attacks separately. The CPA count specifically requires NWMLS to plead its own objective economic loss, and the current pleading does not particularize that loss.

The structural answer is available, but it requires careful articulation in NWMLS’s response brief and likely an amended pleading. NWMLS is not a consumer asserting subjective disappointment with a purchased product. NWMLS is a B2B platform operator asserting product-quality degradation by a member’s documented conduct. The objective economic harms run to platform integrity costs (enforcement expenditures, governance costs, brand defense costs), to subscriber confidence costs (the institutional cost of operating a platform whose data integrity is contested), and to direct enforcement costs (the resources NWMLS expended cutting Compass’s IDX feed and forcing compliance, which are documented in the counterclaim’s factual narrative). Each of these is an objective economic loss susceptible to particularization.

The Two-Gate Capture Model specimens preserved in the public record — Triptych at $65 million, 4640 95th Avenue NE at $7.775 million — supply the transaction-level anchors that allow NWMLS to move from value-degradation rhetoric to particularized economic harm. The 4640 95th Avenue NE transaction at the closed-sale level, with $194,375 in buyer-side commission captured inside the single-brokerage structure through the Foster-Skillman team’s three-role broker assignment, supplies the concrete commission-flow data the Montes standard requires. NWMLS does not need to plead its own pecuniary loss in those transaction terms — the harm the counterclaim alleges runs to platform integrity. But the transaction-level specimens establish that the platform-level degradation has observable downstream consequences in the market the platform serves, which is the foundation for arguing that the platform-level harm is objective rather than subjective.

The amendment burden is manageable. The dismissal-with-leave-to-amend outcome is likely on the CPA count and not catastrophic. The treble-damages architecture survives the amendment as long as the amended pleading clears Montes. The discovery calendar continues to run during the briefing window. The Reffkin deposition timeline does not slip materially.

Montes is the genuine pressure point in the motion. It is not the standing argument, which relies on a pleading-stage arithmetic construction that does not survive contact with the actual exposure population during the late-March to April-17, 2025 Private Phases window. It is not the particularity argument, which can be cured by amended pleading invoking the Two-Gate specimens and the documented “negative insights” mechanism. It is not the causation-inversion argument, which has bite at the pleading stage but loses force when discovery establishes that NWMLS’s enforcement action followed Compass’s documented rule violations rather than preceding them. Montes is the pressure point, and the response requires discipline rather than scale.

VIII. Where Compass Stands Going Forward

The motion’s filing closes nothing. It opens the next phase of the litigation, and the next phase opens against a structural environment that has tightened materially since Compass filed its initial complaint in April 2025.

The Anywhere acquisition closed January 9, 2026, bringing Coldwell Banker, Century 21, Sotheby’s International Realty, ERA, and the rest of the Anywhere portfolio under common Compass corporate control. The post-merger entity carries $2.6 billion in assumed debt against a firm that has never posted a full-year Generally Accepted Accounting Principles (GAAP) profit. The Layer 3 acquisition premium — $400-800 million of the deal price that exists only if the routing-control architecture continues to operate — depends on a regulatory permission structure that three simultaneous institutional forces are now actively withdrawing.

The first force is judicial. Compass v. Zillow in the Southern District of New York produced 268 days of litigation, a four-day preliminary injunction hearing, and zero judicial relief before Compass voluntarily dismissed without prejudice on March 18, 2026. The voluntary dismissal does not retract the underlying legal theory. Reffkin’s sworn PI testimony — the 94% MLS terminal rate, the Black Box design rationale, the Coming Soon data suppression concession — remains permanent federal record available to NWMLS trial counsel under FRE 801(d)(2) as party admissions. Compass v. NWMLS in the Western District of Washington advances toward October 2026 trial with the counterclaim record now including the “negative insights” phrase, paragraph 43’s statutory knowledge admission, the Disclosure Form contradiction, and the Two-Gate specimens preserved in the public record.

The second force is statutory. SSB 6091 takes effect on June 11, 2026, codifying concurrent-marketing requirements that align with NWMLS Rule 2 and contradict the Private Phases of 3PM. The 141-1 legislative vote is not a legal argument. It is the simplest possible legislative signal about what the practice the statute prohibits actually is. Other states are tracking the Washington template. The Reffkin doctrinal trap converts pre-enactment advocacy in those states into post-enactment admission of intent. The state-level legislative ratchet operates jurisdiction by jurisdiction, and each enacted analogue creates a new instance of the same compliance exposure.

The third force is the voluntary industry consensus that emerged in the twenty-day sequence following the Compass-Redfin partnership announcement. Zillow Preview offered transparent premarket visibility with full buyer data and open access. eXp announced three-portal non-exclusive syndication. Realtor.com CEO Damian Eales explicitly contrasted “equal access for all buyers” against “a subset selected by the listing agent.” Every major industry actor except Compass chose open distribution architecture within twenty days of each other. Competing brokerages now operate in a market where the industry’s own voluntary judgment endorsed the transparency model that SSB 6091 mandates and NWMLS Rule 2 has always required. Windermere operates at 35% Washington luxury market share entirely on Layer 1 and Layer 2 value — service quality, agent talent, transaction expertise — none of which SSB 6091 touches.

The three forces operate independently of the motion’s outcome. A federal court order granting Compass’s motion in part on May 21 does not change the SSB 6091 effective date. It does not retract the voluntary industry consensus. It does not remove Reffkin’s earnings call testimony from the federal record or his Inman op-ed from the public record. It does not unsuppress the days-on-market field on Triptych. It does not undo the broker-assignment record on 4640 95th Avenue NE. The motion is a procedural instrument. The architecture is a structural condition.

Compass’s Narrowing Strategy Set

Three options remain available to Compass, and the strategy set narrows further with each enacted state analogue:

Option 1 — Comply and abandon the routing-control advantage. Compass operationally retreats from the Private Phases of 3PM in Washington before June 11, 2026, and in each subsequent state that enacts an SSB 6091 analogue. The compliance posture is defensible in every forum. The cost is the elimination of the Layer 3 acquisition premium — $400-800 million of the Anywhere deal price that depended on continued operation of the routing-control architecture — beginning with the largest single market in NWMLS jurisdiction and ratcheting jurisdiction by jurisdiction as additional states legislate. The goodwill impairment question becomes auditor-dispositive at the next reporting cycle.

Option 2 — Continue and accept regulatory and litigation convergence. Compass operationally maintains the Private Phases of 3PM in Washington after June 11, 2026, and in each subsequent state that enacts an SSB 6091 analogue. The revenue posture is preserved short-term. The cost is the activation of three concurrent enforcement tracks against individual licensees in each enacted jurisdiction (DOL, AG, MLS governance), the conversion of the Reffkin doctrinal record into post-enactment admission of noncompliance intent, and the supply of state regulators with an enforcement predicate that requires no independent investigation. The bilateral damages exposure in Compass v. NWMLS compounds. The Layer 3 premium remains at risk regardless because each enforcement action is itself a goodwill impairment trigger.

Option 3 — Reframe the model before additional states legislate. Compass restructures the Private Phases architecture into a configuration that complies with concurrent-marketing requirements while preserving some commission-capture economics — for example, eliminating the address-suppression mechanism, restoring days-on-market and price-drop history, and competing on the team architecture’s intra-brokerage routing alone. The reframe preserves Gate 2 (intra-brokerage dual representation through the team structure) while abandoning Gate 1 (address suppression and pre-MLS routing). The cost is partial loss of the routing-control advantage and an explicit acknowledgment that the original 3PM architecture was incompatible with statutory transparency requirements — an acknowledgment Compass has spent eighteen months litigating against. The window for this option closes with each additional state that enacts before the reframe is announced, because each additional state extends the pre-enactment advocacy record that contradicts the reframe.

Each option carries different costs at different timelines. None preserves the Layer 3 premium intact.

The April 24, 2026 Compass-MRED announcement, filed the day after the motion, indicates Compass selected a structural variant of Option 3. Compass committed to nationwide listing sharing through Midwest Real Estate Data’s Private Listing Network — including Private Exclusive and Coming Soon Listings — and will subsidize MRED full membership for the first 100,000 Compass agents. The move is not the abandonment-of-routing-control reframe Option 3 originally posited. It is regulatory-arbitrage migration: preserving the Private Phases architecture by relocating it to MLS infrastructure that permits the practice (MRED’s PLN), while building the agent-membership pipeline that operationalizes the Compass-Rocket-Redfin open letter into distribution capacity. The Reffkin announcement quote — committing to “support MLSs... that protect their customers, who are real estate agents, from retaliation by other MLSs and portals, and ensure that agents can fulfill their fiduciary duties” — ports the Inman op-ed’s law/rule doctrine directly into corporate transaction language and characterizes NWMLS’s enforcement of Rule 2 as “retaliation.” The quote enters the public record as a third Skillman moment specimen: a doctrinal commitment converting into operational deployment, attributable to Reffkin personally, on the same day the motion was filed. The MRED move strengthens NWMLS’s tortious interference count by supplying inducement language directly, supplies an additional judicial-estoppel predicate against Compass’s restricted-visibility-harms-consumers theory in the federal court (Compass voluntarily lists with private exclusives on MRED), and confirms that the strategic decision Compass selected is not retreat but redistribution. The Layer 3 premium remains at risk in every state where statutory enforcement arrives, regardless of the alternative MLS infrastructure available in jurisdictions where it has not. The move does not change the architecture. It changes where the architecture runs.

Audience-Specific Implications

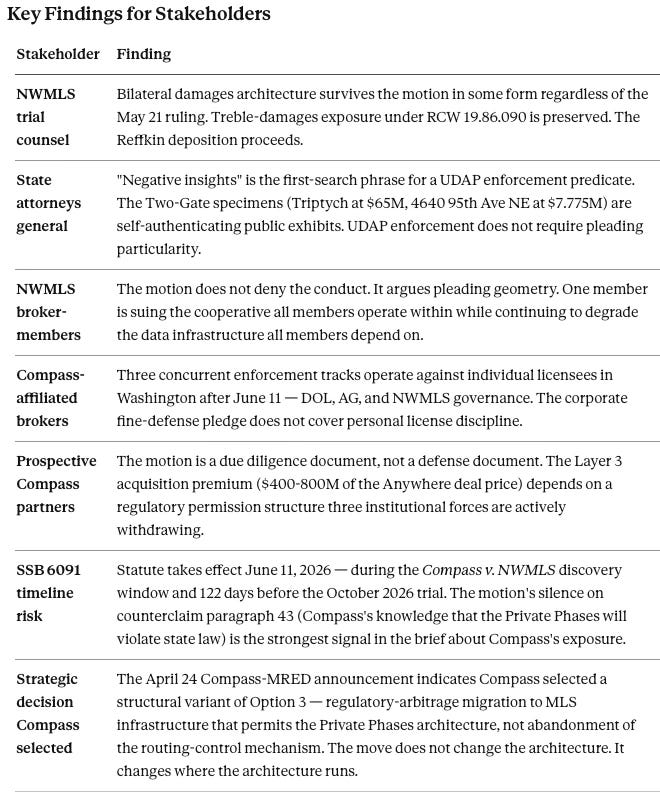

For NWMLS trial counsel, the forward-looking question is how the bilateral damages architecture interacts with the discovery calendar. The Reffkin deposition is the highest-leverage individual deposition in the proceeding. He has already testified four days in the SDNY Zillow proceeding under Judge Vargas. He understands what cross-examination produces when the cross-examiner holds his own sworn statements as impeachment material. The discovery sequence — Reffkin first, then the Foster-Skillman team principals on the Triptych and 4640 95th Avenue NE transactions, then Nelson and Huff on the Washington legislative apparatus, then Skillman on the February 27 Puget Sound Business Journal commentary applying Reffkin’s “seller choice” framing to SSB 6091 — is the specific institutional mechanism through which the Self-Disclosure Trap converts public CEO communication into summary-judgment evidence. The motion does not affect that sequence.

For state attorneys general evaluating UDAP enforcement, the motion clarifies what Compass’s defense architecture cannot reach. The motion attacks pleading sufficiency. UDAP enforcement does not require pleading particularity in the same way private CPA litigation does. The Washington AG’s consumer protection division, the New Mexico DOJ, and AG offices in the five Consumer Policy Center (CPC)-sampled markets (Boston, Washington D.C., Chicago, San Diego, Austin) operate against a public record that the motion does not displace. The “negative insights” phrase, the Disclosure Form contradiction, the Reffkin earnings call, the 20%+ double-ending rate Compass’s own CEO publicly endorsed on April 16, the Two-Gate specimens documenting the architecture in operation — all sit in the public record available to any state AG building an enforcement predicate.

For NWMLS broker-members evaluating their relationship with the cooperative, the motion clarifies the structural position Compass occupies in the proceeding. Compass is suing the cooperative the brokers operate within. The counterclaim alleges that one member — Compass — has been engaged in conduct that systematically degraded the data infrastructure all members depend on. The motion does not deny that conduct. The motion argues that NWMLS lacks standing to bring the counterclaim, that the pleading lacks particularity, that the rules cannot be the duty source, and that the value-degradation theory fails Montes. None of those arguments deny the conduct. Brokers reading the motion against the counterclaim see a defendant arguing about pleading geometry, not about whether the conduct alleged occurred.

For prospective Compass partners — technology vendors, lenders, title companies, institutional capital — the motion is a due diligence document, not a defense document. The motion’s silence on counterclaim paragraph 43 is the silence partners need to read against the June 11 SSB 6091 effective date. The motion’s silence on the Disclosure Form contradiction is the silence partners need to read against Compass’s own client disclosure obligations. The motion’s silence on the Reffkin earnings call is the silence partners need to read against the SEC reporting obligations Compass operates under as a public company. Partners conducting pre-deal due diligence are not the audience the motion is written for. They are the audience the motion’s silences create exposure for.

For brokers evaluating affiliation with Compass, the motion compounds the three concurrent risk vectors that operate independently of the Washington proceeding. The compliance vector: three concurrent enforcement tracks operate against individual licensees in Washington after June 11 — DOL, AG, and NWMLS governance — and the corporate backstop’s track record in Washington is zero judicial relief across two proceedings. The visibility vector: Zillow Preview and Redfin’s platform architecture penalize listings not broadly exposed, and an agent whose listing strategy generates platform removal risk cannot serve clients as effectively as agents operating on fully open-distribution terms. The reputation vector: the “negative insights” phrase is now in a federal court counterclaim, and any Compass agent who explains their pre-market strategy to a client sophisticated enough to search the case docket faces a conversation the open letter cannot script. The motion does not reduce any of these vectors. The motion’s filing demonstrates that Compass has chosen to defend the architecture rather than retreat from it, which is the choice that converts the doctrinal commitment into a forward-running liability rather than a sunk cost.

IX. Forward Conditions and Falsification Criteria

The structural model produces specific forward conditions that are observable, time-bound, and falsifiable. The conditions hold whether the Court grants Compass’s motion in whole, in part, or denies it.

Condition 1 — Fraud and CPA dismissed or narrowed at the May 21 noting under Rule 9(b) and Montes v. SPARC.The Rule 9(b) particularity gap on the fraud count and the Montes objective-economic-loss requirement on the CPA count are doctrinally available to the Court. The likely outcome is dismissal with leave to amend on both counts. NWMLS’s amended pleading particularizes the “negative insights” mechanism through the Two-Gate specimens, articulates the statutory duty source under RCW 18.86.030 distinctly from the cooperative-rule duty source, and pleads platform integrity costs as objective economic loss. The treble-damages architecture survives the amendment.

Condition 2 — The case converges to the antitrust core, with rule-of-reason analysis becoming central by Q3 2026.Compass’s affirmative claims survived Doc. 86. The counterclaim’s bilateral-damages architecture survives the motion in some form regardless of the May 21 ruling. Discovery opens. The rule-of-reason record begins to develop, and the procompetitive justification for NWMLS Rule 2 becomes the central evidentiary question. NWMLS’s procompetitive justification is the same justification SSB 6091’s legislative history adopts.

Condition 3 — SSB 6091 becomes dispositive context after June 11, 2026. The statutory landscape shifts the analysis from private rule to public law. NWMLS Rule 2 becomes anticipatory statutory compliance rather than contested cooperative governance. The Parker v. Brown state-action immunity analysis becomes available to NWMLS in its strongest form. Compass’s continued operation of the Private Phases in Washington after June 11 becomes either operational abandonment in the state (eliminating the routing-control architecture from the largest single market in NWMLS jurisdiction) or non-compliance with state law (creating the enforcement predicate state regulators need without independent investigation).

Condition 4 — Discovery produces contradiction amplification, particularly at the CEO testimony level. The Reffkin deposition operates against four years of public statements that the cross-examiner can use as impeachment material. The Disclosure Form versus earnings call contradiction. The Inman op-ed’s law/rule doctrine. The Facebook quote card’s selective endorsement of the CPC double-ending rate. The SDNY Zillow PI testimony. Each statement is admissible at summary judgment as a party admission under FRE 801(d)(2). The deposition does not produce new evidence — it produces synchronized cross-references between the existing public record and Reffkin’s own future testimony under oath.

Condition 5 — The doctrinal trap closes in additional jurisdictions over the eighteen-month window following SSB 6091’s June 11 effective date. At least two additional states introduce SSB 6091-style legislation citing the Washington model. At least one state-level regulatory enforcement action, licensing guidance, or legislative referral addressing off-MLS marketing practices emerges in a jurisdiction that has enacted statutory listing-transparency obligations by June 2027. Each enacted analogue replicates the same cycle: pre-enactment advocacy converts to post-enactment admission of noncompliance intent in that jurisdiction.

Falsification Condition

The causal chain the model rests on runs: omission → information asymmetry → market distortion → legal and regulatory exposure. The model holds only if the suppressed information is legally material; immateriality would break the chain.

If Compass successfully defends “negative insights” as immaterial to buyers or compliant with statutory disclosure duties under RCW 18.86.030, the structural model fails. The model rests on the analytical claim that the suppression of days-on-market and price-drop history is material under both Washington broker fiduciary duty law and Washington consumer protection law, and that the internal terminology Compass applied to the suppressed information establishes that the suppression is deliberate rather than incidental. A defense theory that successfully characterizes the suppression as either (a) immaterial to buyer decision-making or (b) authorized by the seller-direction provisions of broker fiduciary law would invalidate the central analytical claim. Such a defense theory is not visible in the April 23 motion. If it emerges in the response brief on May 21 or in subsequent filings, the structural model adjusts accordingly.

Secondary falsification condition: if SSB 6091 is preempted by federal antitrust law in Compass v. NWMLS or in subsequent litigation, the state-law-as-procompetitive-justification framework collapses. The preemption theory has no federal authority Compass has cited and no Supreme Court precedent supports its application to state real estate licensing law. Preemption would require either a federal statutory framework that explicitly displaces state regulation of broker conduct (none exists) or a federal antitrust holding that state-law concurrent-marketing requirements are per se unlawful (no court has so held). The conditions for falsification are extremely narrow. But if the federal court evaluating Compass v. NWMLS accepts a preemption theory at summary judgment, the structural model adjusts.

The five conditions and two falsification criteria stated above are predictions, not arguments. They are stated to be tested. The next observable checkpoint is the May 21 noting date. The next structural checkpoint is the June 11 SSB 6091 effective date. The next litigation checkpoint is the discovery production cycle through Q3 2026. Each checkpoint produces evidence that confirms or falsifies the model. The model adjusts to the evidence. The architecture does not adjust to the model.

X. Conclusion

The April 23 Motion to Dismiss is an 8,356-word brief written with billable precision around three structural absences. The “negative insights” phrase appears nowhere. Counterclaim paragraph 43’s statutory knowledge admission gets two conclusory sentences in a footnote. The Q1 2025 Reffkin earnings call statement contradicting Compass’s own client Disclosure Form is not engaged at all. The motion attacks pleading sufficiency and standing geometry while leaving the self-generated evidentiary record entirely outside the brief.

Under the Litigation v. Leverage diagnostic framework, the motion classifies as tactical litigation deploying chutzpah, narrative coercion, and asymmetric stakes — the moral-reversal posture in which the actor whose conduct triggered the enforcement reframes the enforcer as the aggressor. The framework predicts that such litigation activates Behavioral Economics, Narrative Economics, and Information Economics most strongly, with Law and Institutional Economics serving as enablers. The April 23 motion is exactly that profile in operation.

The system shift the litigation is a lagging mechanism trying to control is the transition from private enforcement of market transparency (NWMLS rules pre-2026) to statutory enforcement of market transparency (SSB 6091 post-June 11, 2026). The doctrine the motion advances in litigation form — that NWMLS Rule 2 is an unjustifiable private restriction on competitive conduct — was formalized publicly by Reffkin’s March 25 Inman op-ed as a categorical hierarchy in which fiduciary duty supersedes MLS rules. The doctrine works in 46 states where no SSB 6091 analogue exists. The doctrine fails in 1 state where the analogue has arrived. The state-level legislative ratchet operates jurisdiction by jurisdiction. Each enacted analogue converts pre-enactment advocacy into post-enactment admission of intent to defy state licensing law. The doctrinal trap closes whether the motion wins or loses.

Montes v. SPARC Group LLC is the one genuine pressure point. The objective-economic-loss requirement for CPA injury requires NWMLS to particularize platform integrity costs, enforcement expenditures, and direct compliance costs in the response brief and likely in an amended pleading. The amendment burden is manageable. The treble-damages architecture survives the amendment. The discovery calendar continues to run during the briefing window.

The motion is the front-parlor document. Compass presents one narrative per audience — to investors, to clients, to the federal court, to state legislators, to agents — and the narratives are individually coherent and collectively incompatible. The Eddie Haskell architecture works on parents who only see the front parlor. Federal courts at summary judgment, state attorneys general at investigation, broker-members evaluating institutional affiliation, and prospective partners conducting pre-deal due diligence see the back yard.

The motion closes nothing. It opens the next phase of the proceeding, and the next phase opens against a structural environment that has tightened materially. The Anywhere acquisition closed in January 2026 with $2.6 billion in assumed debt. SSB 6091 takes effect June 11, 2026. The voluntary industry consensus on transparent distribution emerged in February 2026. The Reffkin deposition will proceed in the discovery window. The two Skillman moments at the center of the structure — the linguistic specimen (”negative insights”) and the behavioral specimen (the Two-Gate listings: Triptych at $65 million on the active listing, 4640 95th Avenue NE at $7.775 million on the closed transaction) — will be the first elements a state AG investigator searches when building a UDAP enforcement predicate, and the first specimens broker-members and prospective partners examine when evaluating whether the architecture Compass defended in court is the architecture they want to be associated with going forward.

Each forward condition specified in Section IX is observable on a defined timeline. The structural model is offered to be tested. The architecture does not depend on the model being correct. The architecture depends on what the system already revealed about itself — the Skillman moments the motion’s three structural absences confirm Compass cannot defend at the next stage.

The motion tests the pleading. The Skillman moments test the system.

XI. Cognitive Digital Twin Validation Layer

The MindCast AI Cognitive Digital Twin foresight architecture runs five Vision Functions against the Compass v. NWMLS record. Each function returns a converging output.

Chicago Strategic Game Theory (CSGT) Vision. Game type: delay-dominant enforcement game. Equilibrium: non-resolving, cost-escalation. The motion is consistent with optimization for time and cost rather than doctrinal resolution.

Cybernetic Control Vision (Feedback System). System type: semi-closed loop trending toward closed-loop control. Each forum output becomes the next forum’s input. Motion strengthens counterclaim. Counterclaim strengthens regulatory framing. Statute strengthens court interpretation. Public statements strengthen discovery exposure. Control shifts from actors to the loop itself.

Causation Vision (Causal Signal Integrity, CSI). Causal chain: omission → information asymmetry → market distortion → legal and regulatory exposure. Causal Signal Integrity is high but stress-tested. Primary risk: legal reinterpretation of materiality. The chain holds unless suppression is ruled immaterial.

Disclosure Vision (Information Release Pattern). Pattern: structured cross-forum divergence. Cross-Forum Divergence is high; Disclosure Consistency Index is low. The divergence is systematic, not random — internally rational under audience-specific optimization constraints.

Posner Vision (Economic-Legal Clarity). The motion is strongest where it converts complexity into measurable thresholds (the 0.0006% degradation arithmetic at page 11). The Montes dispute resolves to whether harm is measurable or merely asserted.

All five Vision Function outputs converge on a single conclusion: the system persists independent of any single ruling.

Source Documents

Compass, Inc. and Compass Washington, LLC. Plaintiffs’ Motion to Dismiss Defendant’s Counterclaims, Case No. 2:25-cv-00766-JNW, Document 93 (W.D. Wash., April 23, 2026).

Northwest Multiple Listing Service. Defendant Northwest Multiple Listing Service’s Answer, Affirmative Defenses, and Counterclaim, Case No. 2:25-cv-00766-JNW, Document 88 (W.D. Wash., April 2, 2026).

Substitute Senate Bill 6091, Washington State Legislature (2026 Regular Session), signed March 17, 2026, effective June 11, 2026.

Montes v. SPARC Group LLC, 2026 WL 900481 (Wash. April 2, 2026).

Northwest Multiple Listing Service, Listing #2497151, “Triptych,” Undisclosed Address, Bellevue, WA 98004, active at $65,000,000 as of April 17, 2026.

Northwest Multiple Listing Service, Listing #2468181, 4640 95th Avenue NE, Yarrow Point, WA 98004, sold March 27, 2026 at $7,775,000.

Robert Reffkin, Law vs. Rule: MLS Mandates Cannot Supersede Fiduciary Duty, Inman (March 25, 2026).

Stephen Brobeck, Compass Expansion: New Data on Market Share and Double Ending (Consumer Policy Center, April 2026).

Jacqui Mueller, MRED Expands Nationwide Access as Compass Becomes First Brokerage to Share Listings on PLN, Chicago Agent Magazine (April 24, 2026).

MindCast AI Analytical Foundation

Diagnostic Framework

MCAI Lex Vision: Litigation v. Leverage, How MindCast AI Decodes Intent Behind Legal Action (April 28, 2025) — diagnostic framework for classifying legal action by intent across Behavioral, Narrative, Information, Law, and Institutional Economics

Routing-Control Architecture: Framework and Specimens

The Compass Commission Consolidation Strategy and Real Estate Marketing Transparency (February 19, 2026) — establishes the Three-Layer Acquisition Hierarchy and the $400-800M Layer 3 acquisition premium dependent on the routing-control architecture

The Compass-Anywhere Address Suppression Calculus, A Hypothetical Scenario Using Seattle Ultra-Luxury Transaction Data January 2025 – January 2026 (February 22, 2026) — Nash-Stigler game-theoretic simulation of 130 Seattle ultra-luxury transactions producing the Foster-Skillman team-pattern foundation

Two NWMLS Records, One Foster-Skillman Team — Primary-Source Evidence of the Compass Two-Gate Capture Model Inside the Washington Statutory Transition Window (April 17, 2026) — the Triptych and 4640 95th Avenue NE specimens documenting Gate 1 address suppression and Gate 2 intra-brokerage capture

Compass Double-Sided Commissions — Consumer Policy Center Measures the Output, MindCast Models the System(April 15, 2026) — separates CPC empirical measurement from the framework analyzing the system that produces the 20%+ double-ending rate

Narrative Architecture and Self-Disclosure Trap

The Compass Narrative Inversion Playbook (February 4, 2026) — original Skillman Moment specimen catalog and the narrative inversion pattern across Compass-controlled forums

Compass’s Cross-Forum Contradictions (February 28, 2026) — cross-forum contradiction matrix establishing the Self-Disclosure Trap mechanism

The Cybernetics of Compass Holdings’ Narrative Control Architecture (March 21, 2026) — three-layer control architecture and the cybernetic foundations of the Self-Disclosure Trap pattern

The Compass-Reffkin Consumer Policy Center Quote-Card Specimen — A Self-Disclosure Trap Market Analysis (April 16, 2026) — the April 16 Reffkin quote card establishing the personal-attribution judicial-estoppel predicate

Doctrinal and Litigation Analysis

MCAI Lex Vision: The Law and Behavioral Economics of Compass vs. NWMLS (March 23, 2026) — foundational analysis classifying the litigation as a delay-dominant equilibrium in which procedural survival is not substantive victory; runs the six Vision Function CDT convergence the present publication updates against the April 23 motion

Compass Holdings, Robert Reffkin’s Doctrinal Trap (March 25, 2026) — analysis of the Reffkin Inman op-ed and the law/rule doctrinal collapse mechanism

The Counterclaim That Closed Compass’s Antitrust Thesis (April 3, 2026) — analysis of the NWMLS counterclaim architecture and the bilateral damages exposure

MCAI Market Vision Visual Synthesis: The Compass Narrative War Against MLSs (April 5, 2026) — visual synthesis integrating the Reffkin doctrinal trap with the cross-forum contradiction architecture