MCAI Economics Vision: Compass Double-Sided Commissions — Consumer Policy Center Measures the Output, MindCast Models the System

Benchmark Analysis: Consumer Policy Center on Compass and Where MindCast Extends the Model

Recent works: The Compass-Reffkin Consumer Policy Center Quote-Card Specimen — A Self-Disclosure Trap Market Analysis | Compass Double-Sided Commissions — Consumer Policy Center Measures the Output, MindCast Models the System | Two NWMLS Records, One Foster-Skillman Team — Primary-Source Evidence of the Compass Two-Gate Capture Model Inside the Washington Statutory Transition Window | Rocket-Redfin Asks NWMLS to Rewrite Rules to Help Make Rocket-Redfin-Compass Partnership More Profitable — and Strategically Chose a Corporate News Platform Over an Amicus Brief

Foundational works: The Compass Narrative Inversion Playbook | Compass’s Cross-Forum Contradictions | The Compass Commission Consolidation Strategy and Real Estate Marketing Transparency | The Antitrust Litigation Trap Compass Built for Itself | The Counterclaim That Closed Compass’s Antitrust Thesis | Zillow, eXp, and Redfin–Compass. Three Deals. Twenty Days. One Outlier.

I. Framing

Compass’s private exclusive strategy creates a routing-control system that internalizes transactions; the Consumer Policy Center report is the first to measure its outputs. Most commentary about private exclusives gets trapped in rhetoric — seller choice, fiduciary duty, innovation, modernization, privacy. Stephen Brobeck instead isolates a narrower and more testable question: what happens to market share and in-house deal capture when Compass expands in targeted high-value local markets? Structure comes first. Facts follow. A branding fight becomes a market-structure inquiry.

The report demonstrates more discipline than many industry critiques. Rather than relying on broad national allegations, Brobeck samples five specific local markets — Boston, Washington D.C., Chicago, San Diego, and Austin — and measures two variables central to consumer protection analysis: concentration and double-ending. That move gives the report a concrete angle that most trade press coverage lacks. Brobeck asks not only whether Compass is getting bigger, but also whether Compass keeps more transactions inside its own network.

II. What the Consumer Policy Center Report Does Well

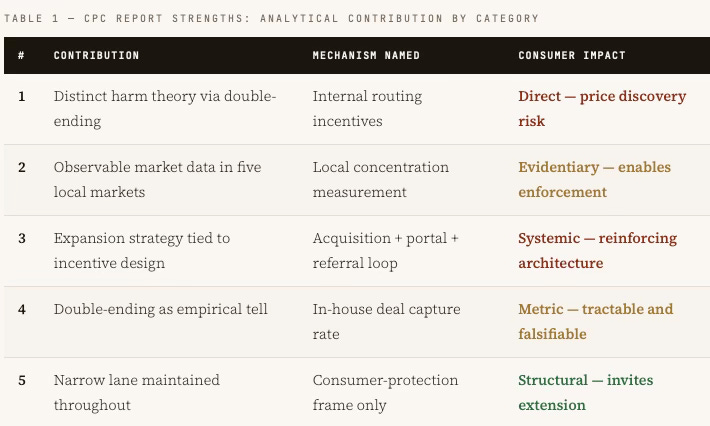

A Distinct Consumer-Protection Harm Theory

The report’s strongest move is conceptual. Treating double-ending not as a side issue but as a possible mechanism of consumer harm reframes the analysis. The concern shifts from Compass merely being large to Compass potentially using private exclusives, referral incentives, and internal routing to increase the odds of capturing both sides of the transaction. That framing links market structure to household-level effects — weakened price discovery for sellers, reduced access for buyers, and brokerage incentives that diverge from the consumer’s stated objective.

Anchoring the Argument in Observable Market Data

The report’s stated purpose — presenting new data on Compass’s potential dominance in five profitable local markets, focusing on market share and double-ended sales — constitutes the core evidentiary contribution. Residential brokerage competition resolves city by city, neighborhood by neighborhood, listing by listing. The local-market framing puts the analysis where competitive effects actually materialize.

Tying Expansion Strategy to Incentive Design

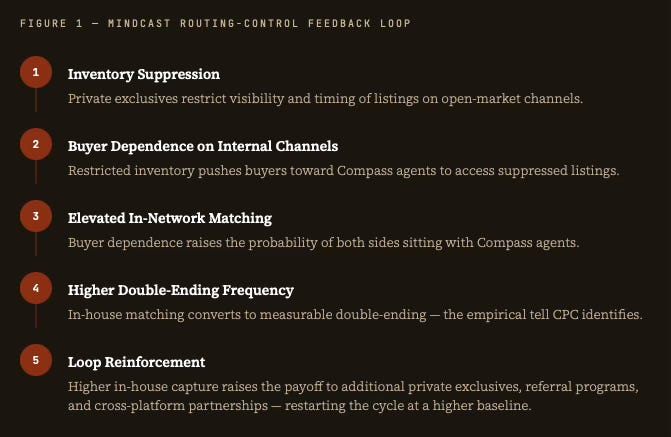

The report does more than document growth. Brobeck argues that Compass has built a reinforcing system: acquire firms in targeted high-value markets, expand consumer attention through Redfin and Rocket, steer buyers and sellers toward Compass agents, use private listing structures to control access, and create internal referral incentives rewarding in-network routing. Placing acquisitions, private exclusives, referrals, and portal strategy inside one coherent expansion logic is what makes the report analytically useful rather than merely descriptive.

Isolating Double-Ending as a Strategic Output

Where many critics claim private exclusives feel exclusionary, the report identifies the measurable output that would follow if that criticism holds. If internal routing is the real objective, in-house deal capture should rise. Double-ending rates become the empirical tell — a tractable metric rather than a vague intuition, and one that can be monitored and contested across time.

Staying Inside a Narrow Lane

The report does not attempt a full antitrust case, a full legislative history, or a full institutional theory of brokerage governance. That restraint keeps the work legible and focused. Within its lane, the report contributes a distinct consumer-protection benchmark for how concentrated brokerage growth and in-house transaction capture may interact — a bounded contribution that invites extension rather than replacement.

III. The Report’s Unique Contribution

Critics of Compass are not rare. Market participants, portals, and trade commentators have offered pointed assessments for years. The CPC report’s distinctive contribution lies in translating that controversy into a structured consumer-protection metric stack — a diagnostic frame that gives regulators and litigants something closer to operational inputs rather than generalized complaints about secrecy or disruption.

The report also treats the luxury and high-price segment not as a peripheral detail but as central to Compass’s growth logic. Expensive inventory magnifies the economic payoff from routing control. A strategy that might look marginal in lower-value segments becomes far more consequential when concentrated around high-commission inventory — a point that regulators focused on aggregate national data may systematically underweight.

The diagnostic stack identifies outputs but does not determine whether those outputs arise from isolated practices or from a coordinated system. That distinction matters operationally. If double-ending, referral incentives, and private exclusives operate independently, standard disclosure and competition remedies may suffice. If they operate as a coupled system, interventions targeting individual practices will leave the underlying mechanism intact. MindCast answers that question.

Contact mcai@mindcast-ai.com to partner with us on Predictive Law and Behavioral Economics + Game Theory Foresight Simulations. To deep dive on MindCast upload the URL of this publication into any LLM (preferably ChatGPT or Gemini for magazine style works) and prompt ‘reconstruct MindCast framework with three degrees of cited sub links.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure.

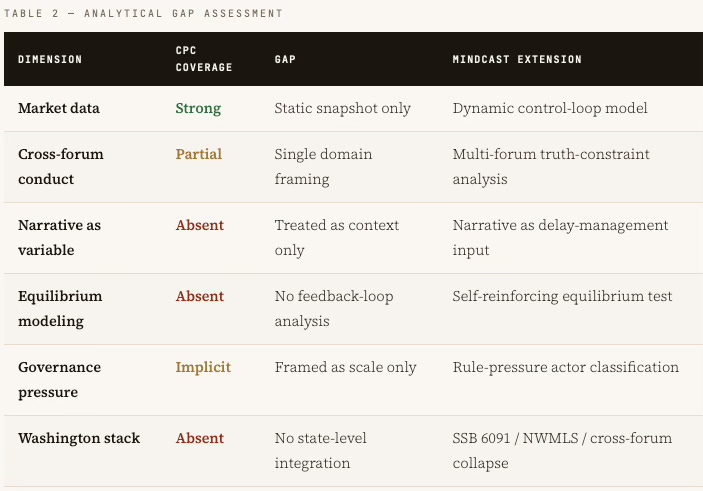

IV. What the Report Does Not Yet Fully Capture

The report excels as a consumer-protection and market-measurement paper. As a dynamic institutional model, the analysis remains less developed. Brobeck identifies important outputs but does not fully model how those outputs interact across litigation, legislation, portal policy, brokerage messaging, and competitive response. Table 2 shows that CPC identifies outputs but does not model the system generating them — that gap is precisely where MindCast extends the analysis.

V. How MindCast Extends the Analysis

MindCast does not displace the CPC report. MindCast builds on the foundation Brobeck lays and asks what kind of system generates those measured outputs — repeatedly, across forums, and over time.

Cross-Forum Analysis. Compass’s conduct does not operate in one venue. The same company speaks simultaneously to courts, regulators, agents, portals, legislators, and consumers. A firm can call private listings consumer choice in one setting, privacy protection in another, fiduciary duty in a third, and competitive necessity in a fourth. The key analytical question is not which slogan appears in isolation. The key question is whether the underlying conduct and incentive structure remain stable beneath the shifting language. MindCast tests that stability directly.

Narrative as a Causal Variable. The CPC report treats public statements as context. MindCast treats them as part of the operating system. Narrative can regulate how quickly regulators respond, how much broker opposition forms, how buyers interpret access restrictions, and how competitors decide whether to comply, imitate, or defect. Framing routing control as innovation, seller autonomy, or privacy functions as delay management — a strategic input that changes institutional response speed, not merely a communications choice made after strategy is set.

Feedback-Loop and Equilibrium Analysis. CPC identifies a plausible mechanism. MindCast asks whether the mechanism stabilizes into an equilibrium. Some practices are opportunistic and temporary. Others become self-reinforcing and difficult to unwind. MindCast therefore tests whether the system has reached a condition where outside brokers face worse access, sellers accept less open marketing, buyers grow more dependent on internal agent networks, competitors feel pressure to imitate or reconfigure, and regulators respond too slowly to interrupt the loop. When those conditions converge, the issue is no longer primarily consumer deception or imperfect disclosure. The issue becomes market-governance drift.

The Washington Stack. Washington compresses Compass’s strategy into a single evidentiary field. Three constraints converge simultaneously: Washington State Senate Bill 6091 (SSB 6091) — signed into law with a June 2026 effective date — imposes legislative constraint by restructuring seller disclosure obligations in direct tension with private exclusive strategy; Compass v. NWMLS federal litigation imposes legal constraint by forcing the same firm to litigate mandatory-exposure obligations in federal court while asserting seller-choice autonomy in legislative testimony; and brokerage conduct in Washington markets imposes market constraint by generating observable double-ending data within the same jurisdiction. All three constraints point at the same underlying system — leaving no narrative escape. The Skillman Moment — Compass’s own language applied inside the incentive structure SSB 6091 creates — demonstrates how narrative tools that function inside a closed system fail to export once the regulatory landscape shifts across all three constraint planes simultaneously. MindCast models that cross-forum position collapse as a falsifiable prediction, not a rhetorical observation.

Lawful Scale Versus Governance-Distorting Scale. Large market share alone does not explain the strategic significance of Compass. A distinction exists between firms that grow large while remaining bounded by existing market rules, and firms that grow large enough to force portals, MLSs, competitors, and lawmakers to respond on the firm’s terms. The second condition — governance-distorting scale — describes a different kind of actor. At that threshold, Compass stops functioning primarily as a brokerage and begins functioning as a rule-pressure actor: one whose strategic choices set the agenda for regulatory and legislative response rather than reacting to it. At governance-distorting scale, rule formation becomes endogenous to the firm’s strategy. Regulatory response no longer disciplines conduct; regulation reacts to it. Competing firms respond not to static rules, but to the trajectory of rule formation itself. The CPC report correctly identifies concentration. MindCast asks whether that concentration has crossed the threshold where standard consumer-protection remedies address only the visible symptom while the generative mechanism continues operating beneath them.

VI. Forward Predictions and Falsification Conditions

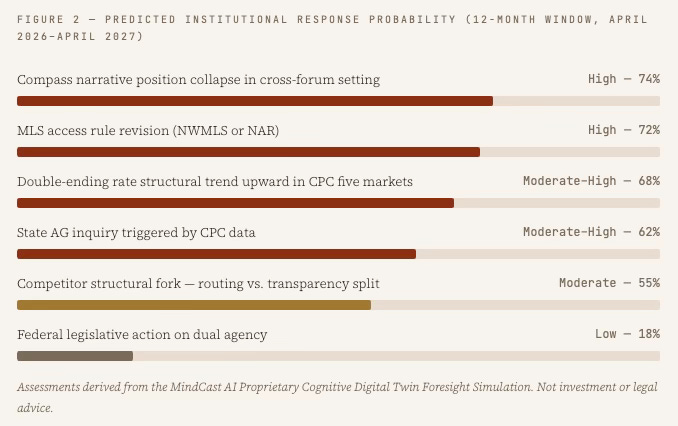

MindCast generates four discrete forward predictions across three analytical layers: institutional response, competitor alignment, and narrative collapse. Each carries an explicit falsification condition. The predictions derive from the routing-control feedback loop model and the payoff inequality at the system’s core: alignment occurs when the expected marginal revenue from in-house capture exceeds the marginal value of open-market price discovery. The Consumer Policy Center report supplies the baseline measurement. The predictions below test whether the system generating that measurement persists under competitive and regulatory pressure.

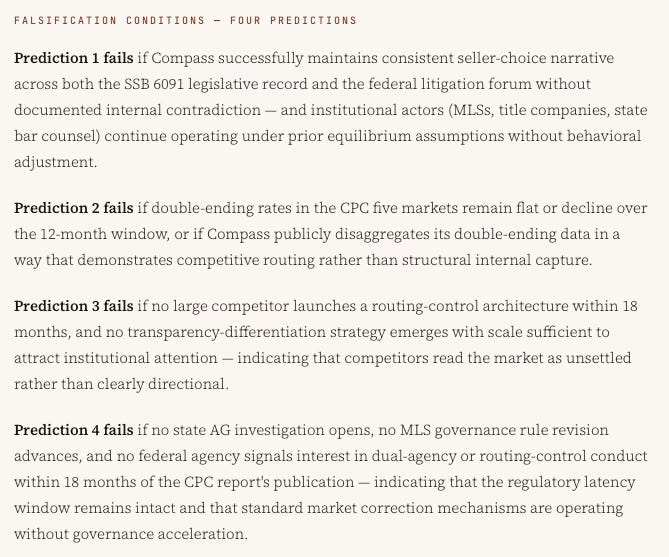

Prediction 1 — Narrative Collapse Under Shared Institutional Scrutiny. As SSB 6091 takes effect in June 2026 and the Compass v. NWMLS litigation advances, Compass’s simultaneous narrative positions — seller choice in legislative forums, mandatory access challenges in federal court — will fail under shared institutional scrutiny. Sophisticated institutional actors (title companies, MLS governance boards, state bar counsel advising brokerage clients) will register the contradiction and adjust their own conduct accordingly, reducing the narrative’s delay-management effectiveness. Competing firms respond not to market signals alone, but to the rule-setting behavior of the dominant actor — and position collapse by the dominant actor removes the narrative cover that made non-response rational.

Prediction 2 — Double-Ending Rate Acceleration. Double-ending rates in the five markets CPC sampled will increase over the 12-month window as the Rocket-Redfin partnership deepens buyer-funnel integration. The Rocket mortgage origination layer, combined with Redfin’s buyer-facing portal, creates a demand-side capture mechanism that operates independently of listing-side private exclusives. Where both mechanisms operate in the same transaction, double-ending probability compounds. The CPC report measures the current baseline; the Rocket-Redfin architecture raises the structural floor.

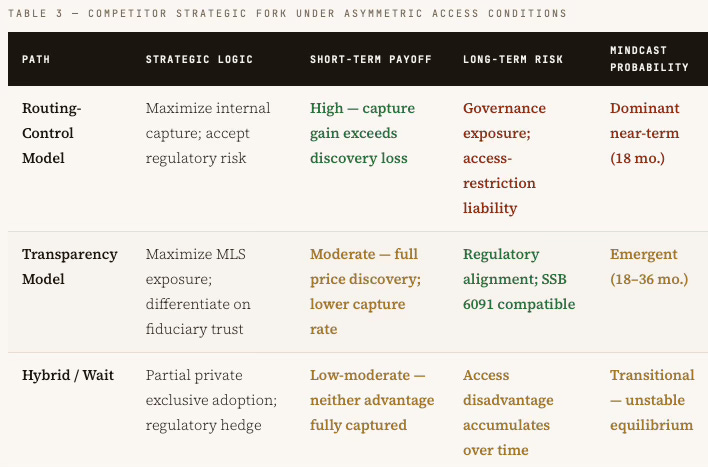

Prediction 3 — Competitor Structural Fork. Competing large brokerages face a structural fork under asymmetric access conditions, not a simple imitation choice. Firms operating in markets where Compass holds significant private-exclusive inventory face a binary decision: adopt routing-control architecture to maintain inventory access, or defect toward a transparency strategy and differentiate on open-market trust signals. Herding toward the routing-control model accelerates under regulatory uncertainty — when firms cannot assess enforcement probability, the highest visible payoff strategy dominates. Expect 12–18 months of herding behavior before a transparency-strategy competitor emerges with sufficient scale to make the fork legible to institutional observers.

Prediction 4 — Regulatory Latency Window Closes Faster Than Compass's Expansion Timeline. MindCast's structural prediction on timing: the regulatory latency window — the period between strategic adoption and enforcement response — will close more quickly than Compass's expansion timeline requires. SSB 6091 compresses the window in Washington. CPC's double-ending data hands state AGs a ready-made investigative predicate. The Inman and HousingWire coverage of the Rocket-Redfin alliance has already distributed the mechanism story to the professional audience that feeds regulatory referrals. Compass needs the latency window to remain open for 24–36 months to complete its upscale-market concentration strategy. The window will not hold that long.

VIII. Stakeholders and Intended Audience

Five distinct stakeholder tiers hold direct analytical interest in the combined CPC-MindCast record.

The publication also reaches institutional subscribers — government bodies, regulatory agencies, and market research organizations — for whom the predictive architecture carries operational value beyond the Compass-specific analysis. A framework that models how dominant brokerages behave under regulatory pressure applies to any market where listing-side concentration and dual-commission incentives converge.

IX. Olympia Validated: What the Washington Record Now Means

Compass deployed significant institutional resources to defeat SSB 6091 in Washington State. The firm coordinated 162 affiliated opposition witnesses (nine disclosing affiliation, a 17:1 undisclosed ratio), placed its Pacific Northwest Regional Vice President in every major trade outlet defending private exclusives, submitted a twelve-word opt-out amendment designed to reconstitute the private exclusive window through contract defaults, and filed parallel federal antitrust litigation asserting that open-exposure requirements are anticompetitive. SSB 6091 passed the Washington Senate 49–0. The Southern District of New York denied the preliminary injunction the same week. The cross-forum contradiction — Compass arguing in federal court that restricted listing visibility harms consumers while arguing in Olympia that restricted visibility protects them — entered a permanent, discoverable legislative transcript.

The CPC report now lands in that record and materially changes what the Washington record means retroactively across three audiences.

Before regulators: Compass’s Olympia testimony — that private exclusives have no downside for sellers — now sits alongside CPC’s April 2026 national market-share and double-ending data showing the mechanism produces exactly the consumer harm Compass denied under oath. Compass’s own Disclosure Form acknowledged the risk. CEO Robert Reffkin’s Q1 2025 earnings call denied it publicly. An independent national consumer protection organization has now measured it. Three independent analytical bodies — MindCast (February 2026), CPC (April 2026), and the SDNY (February 2026) — reached converging structural conclusions without coordination. State AGs in CPC’s five sampled markets now hold a ready-made investigative predicate: the mechanism is named, the outputs are measured, the legislative contradiction is transcribed, and the UDAP enforcement authority is confirmed on the Washington record.

Before capital markets: Each state that advances a transparency bill reprices the Layer 3 acquisition premium — the $400 to $800 million of the Anywhere acquisition price that exists only if listings can be withheld from the open market. MindCast identified that premium as a regulatory short position in February 2026. The CPC report’s market-share data makes that repricing argument legible to analysts who lack the transaction-level detail the Seattle dataset supplies. The goodwill impairment question — when does cumulative regulatory divergence from the acquisition’s underwriting assumptions become material enough to require disclosure — advances from theoretical to timely with each state that acts. Washington was one. The CPC report documents five more markets simultaneously.

Before competing brokerages and other state legislatures: Washington’s record functions as a portable template. Legislative staff now know the delegation downshift (send a managing director who cannot answer business-model questions while the regional VP sits silent in the gallery), the twelve-word amendment anatomy, the Astroturf coefficient methodology, and the specific cross-forum questions that forced deflection under oath. Compass cannot deploy the same playbook in Illinois, California, New York, or Texas without those states inheriting Washington’s institutional memory. The barrier to the next transparency bill is structurally lower than the barrier Washington faced — and the CPC report supplies the national market data those states lacked when Washington went first.

The deeper institutional damage runs to Compass’s narrative infrastructure. The firm spent the Washington legislative window arguing a position its own Disclosure Form contradicted, its own litigation posture contradicted, and that an independent consumer protection organization has now measured against real market data and found wanting. The “no downside” claim has been refuted in four independent venues — SDNY, Olympia, the Seattle NWMLS transaction record, and CPC’s national study — within a single calendar quarter. Each refutation enters the same discoverable public record. Each subsequent state that holds hearings inherits that record without having to generate it from scratch. Compass did not merely lose a legislative fight in Olympia. Compass generated a permanent evidentiary archive that compounds with every institutional development that follows.

X. Benchmark Conclusion

Consumer Policy Center shows the pattern. MindCast explains the machine.

Consumer Policy Center’s report earns its place in the analytical record because Brobeck demonstrates discipline. Narrowing the field, naming a measurable mechanism, and supplying a consumer-protection frame more rigorous than the standard debate over private listings — centering double-ending as the key observable output of internal routing — constitutes a benchmark contribution that regulators and litigants can actually use.

MindCast builds on that foundation. The extension demonstrates that the report captures only one layer of a larger system. The observed increase in local concentration and in-house deal capture represents the visible output of a broader control architecture operating across listings, referrals, portals, litigation, messaging, and market governance. The Washington stack — SSB 6091, NWMLS, cross-forum position tension — adds the state-level dimension the national frame leaves open. The distinction between lawful scale and governance-distorting scale adds the structural dimension that standard consumer-protection analysis is not designed to reach.

The MindCast AI Proprietary Cognitive Digital Twin Foresight Simulation architecture converts Brobeck’s snapshot into a dynamic institutional model with falsifiable forward predictions — the form of analysis that distinguishes predictive institutional cybernetics from commentary.

The CPC report did not generate the framework now under institutional discussion. MindCast published it first. In February 2026 — two months before the CPC report — The Compass Commission Consolidation Strategy and Real Estate Marketing Transparency modeled the same routing-control mechanism Brobeck later measured, using thirteen months of Seattle ultra-luxury NWMLS transaction data to document the Category A through D commission-flow architecture: direct dual-agency capture, merger internalization in both directions, and the open-market outcomes the private exclusive program is engineered to prevent. The Three-Layer Acquisition Hierarchy in that publication identified Layer 3 — $400 to $800 million of the Anywhere acquisition premium — as a regulatory short position dependent on a single operating condition: that listings can be withheld from the open market long enough for an internal buyer to arrive first.

The companion publication, The Compass-Anywhere Address Suppression Calculus, ran a game theory simulation using the same dataset and reached a finding that Prediction 4 above independently replicates: the regulatory latency window closes faster than Compass’s expansion timeline requires, because revenue adequacy and detection avoidance are structurally incompatible objectives across every price threshold modeled. CPC supplied the national market-share and double-ending rate data that MindCast’s transaction-level analysis lacked. MindCast supplied the causal system, the balance sheet grounding, the cross-forum architecture, and the falsifiable forward predictions that CPC’s consumer-protection frame was not designed to produce. The two bodies of work occupy different but complementary positions in the same analytical record — and the sequencing matters: the framework preceded the measurement.

EXTERNAL SOURCES

Stephen Brobeck, Compass Expansion: New Data on Market Share and Double Ending (Consumer Policy Center, April 2026).

Taylor Anderson, Compass Is Dominating Key Markets And Keeping More Deals In-House (Inman, April 14, 2026).

Rocket Companies, Compass and Rocket Form Historic Alliance to Dramatically Increase Home Listing Inventory on Redfin (Rocket Companies Press Release, February 23, 2026).

Taylor Anderson, Docs Offer Inside Peek at Compass’s War Against ‘Organized Real Estate’ (Inman, January 9, 2026).

AJ LaTrace, Compass to Launch Client Portal Amid Private Listings Push (Real Estate News, February 1, 2025).

Brooklee Han, Compass Launches Referral Program for Listing Agents’ Buyer Leads (HousingWire, February 23, 2026).

MINDCAST AI PUBLICATIONS

The Compass Commission Consolidation Strategy and Real Estate Marketing Transparency (MindCast AI, February 19, 2026). Primary MindCast evidentiary publication: thirteen months of Seattle ultra-luxury NWMLS transaction data, Category A–D commission-flow architecture, Three-Layer Acquisition Hierarchy, and Layer 3 regulatory short position analysis.

The Compass-Anywhere Address Suppression Calculus (MindCast AI, February 22, 2026). Game theory simulation modeling detection-window incompatibility across four price tiers; source of the revenue-adequacy vs. detection-avoidance structural finding cited in Prediction 4.

The Compass Narrative Inversion Playbook (MindCast AI). Documents Compass’s three-tier cross-forum contradiction: federal court, state legislative testimony, and investor communications arguing structurally incompatible positions on the same conduct. Prepared as a direct briefing for state legislators and attorneys general.

SSB 6091 Cross-Forum Analysis (MindCast AI). Tracks how the 49–0 Washington Senate vote and the SDNY preliminary injunction denial converged in the same week — two independent institutional forums reaching the same structural conclusion simultaneously.

Compass, Competitive State-Driven Federalism, and the Legislative Ratchet (MindCast AI). Analyzes how multi-state transparency adoption reinforces the Parker v. Brown state-action immunity standard, making federal preemption challenges progressively weaker as state count rises.

Compass Broker Incentives and the Game Theory of Agent Migration (MindCast AI). Applies game theory to show how Compass converts individual broker indifference into firm-level commission capture — behavior that follows payoffs, not intentions.

Windermere and Compass: Two Philosophies of Real Estate (MindCast AI). Documents Windermere’s stated decision to forgo private exclusives despite possessing the market position to exploit them — the direct falsification of Compass’s competitive-necessity argument.

Death by a Thousand Depositions: A Pre-Foresight Simulation of Compass’s Multi-Vector Regulatory Collapse (MindCast AI). Pre-foresight simulation modeling simultaneous collapse across litigation, legislative, and regulatory vectors.

Nineteen Senators, Seventeen Questions: How Compass Bought Its Antitrust Clearance (MindCast AI). Analyzes the legislative record of Compass’s antitrust clearance strategy.

The Shadow Antitrust Trifecta (MindCast AI). Maps Compass’s structurally incompatible positions across federal court, state legislatures, and investor communications as behavioral evidence of strategic rather than principled advocacy.

MINDCAST AI ANALYTICAL FRAMEWORKS

The following frameworks underpin the analytical architecture deployed throughout this publication. Readers unfamiliar with these models will find brief descriptions below each citation.

MindCast Nash-Stigler Equilibrium Architecture (MindCast AI). Framework explanation: Most institutional analysis asks what outcome is most likely. The MindCast Nash-Stigler Equilibrium Architecture asks two prior questions simultaneously. Nash equilibrium — drawn from game theory — identifies the stable multi-player outcome: the point at which no actor (a regulator, a competing brokerage, a court, a firm) can improve its position by changing strategy unilaterally. Stigler equilibrium — drawn from information economics — identifies the evidentiary sufficiency threshold: the point at which the public record contains enough documented evidence that institutional actors can and will act without requiring additional proof. Running both simultaneously produces a richer prediction than either alone. A strategy may be Nash-stable under current information conditions but Stigler-unstable the moment a transaction record, a legislative transcript, or an enforcement action shifts the information environment. The routing-control feedback loop in this publication reaches Nash stability at the $20M+ tier and Stigler instability below $15M — which is why the detection window closes faster than the revenue opportunity requires.

Chicago School Accelerated: The Integrated, Modernized Framework of Chicago Law and Behavioral Economics (MindCast AI). Framework explanation: The Chicago School Accelerated framework synthesizes classical price theory (Coase, Becker, Posner) with behavioral economics and institutional analysis into a forward-looking regulatory prediction tool. Where traditional Chicago School analysis explains past conduct through efficiency logic, Chicago School Accelerated asks how rational actors optimize under mutable rules, regulatory uncertainty, and multi-forum truth constraints — the conditions that govern real institutional contests rather than idealized markets.

The Shadow Antitrust Trifecta (MindCast AI). Framework explanation: The Shadow Antitrust Trifecta maps cross-venue argument inconsistency — identifying where a firm’s positions in federal court, state regulatory proceedings, and investor or public communications are structurally incompatible. Inconsistency of that kind is not merely a credibility problem; under the Trifecta framework, it functions as behavioral evidence of strategic rather than principled advocacy, and it supplies the evidentiary foundation for cross-forum enforcement actions that no single-venue analysis could generate alone.