MCAI Economics Vision: Prediction Markets— Legislative Regime Conversion and the Collapse of Preemption

How The Senate CEA Amendment Introduces A Statutory Category Exclusion Mechanism, Reprices Market Probabilities, And Redirects Consumer Demand Across Contract Classes

Related publications: Kalshi Is Crypto’s Test Case | Kalshi’s Prediction Market Litigation Architecture, the CFTC Amicus, and the Strategic Framework for State Enforcement | The National Kalshi Prediction Market Litigation Map | The Full Arc of Prediction Markets | Prediction Markets and the Regulatory Split | Prediction Markets— Legislative Regime Conversion and the Collapse of Preemption | Kalshi Found the One Gap in American Gaming Law Nobody Closed | The Ninth Circuit on April 16 as System Convergence — The First Measurable Test of Prediction Market Structure | Kalshi, Prediction Markets and the Conflict Architecture of Regulation

Executive Summary

On March 19, 2026, MindCast AI published Prediction Markets and the Regulatory Split, a structural analysis of the jurisdictional collision between federal derivatives oversight and state gambling enforcement. The publication assigned prediction markets to a gambling-leaning, delay-dominant equilibrium driven by three compounding forces: Arizona’s 20-count criminal complaint against Kalshi — the first criminal charges filed against any prediction market platform — a single-commissioner Commodity Futures Trading Commission (CFTC) lacking rulemaking capacity, and state attorneys general activating existing gambling statutes faster than any federal classification process could respond. The CDT Foresight Simulation in that publication assigned P45 to the base case (fragmented enforcement persists), P35 to the downside case (gambling classification locks in), and P20 to the upside case (federal derivatives framework prevails). It also produced a six-trigger forward sequence identifying the observable developments that would confirm or falsify the model. Four days later, three of those six triggers activated simultaneously — and a structural development arrived that the original analysis did not fully anticipate.

Congress is converting a regulatory conflict into a statutory regime. On March 23, 2026, Senators Adam Schiff (D-CA) and John Curtis (R-UT) introduced the Prediction Markets Are Gambling Act — the first bipartisan Senate bill targeting prediction market platforms. Senators Schiff and Curtis propose amending the Commodity Exchange Act (CEA) to prohibit any entity registered with the CFTC from listing contracts that resemble sports bets or casino-style games. Naming that move accurately matters: a statutory CEA amendment is not an enforcement escalation. Enforcement actions operate within a contested jurisdictional space. A statutory amendment eliminates the space itself.

MindCast AI’s framework identifies the mechanism as the Statutory Category Exclusion Mechanism (SCEM): a legislative instrument that converts definitional ambiguity into express prohibition, foreclosing the judicial and administrative channels that depend on ambiguity to function. State enforcement actions could face preemption from a favorable appellate ruling. CFTC jurisdiction assertions could survive administrative challenge. The SCEM bypasses both. No appellate court reinstates a preemption argument against express congressional intent. No CFTC rulemaking authorizes what Congress has expressly prohibited.

Preemption collapses along a clean causal chain. No statutory ambiguity produces no judicial pathway. No judicial pathway produces no strategic delay equilibrium. No delay equilibrium means the system resolves through legislation — on Congress’s timeline, not the courts’. The March 19 Cognitive Digital Twin (CDT) Foresight Simulation assigned P20 to the upside case, conditioned on either a Supreme Court preemption ruling or a formal CFTC rulemaking. The SCEM renders both conditions structurally inoperative for the sports contract category.

Hours after the Senate bill dropped, Kalshi announced preemptive screening features blocking politicians from trading on their own campaigns and athletes from wagering on their own sports. Kalshi is no longer defending classification. Kalshi is pre-positioning for statutory survival. MindCast AI’s Prospective Repeated Game Architecture (PRGA) predicted this behavioral shift: platforms sustain the expansion-under-loss strategy only as long as the commitment device — preserving the preemption argument by refusing state jurisdiction through compliance — remains intact. Voluntary concessions confirm the device has weakened. Platforms have already repriced the upside case.

A state transition has occurred, not a probability revision. Reversible equilibrium has become conditional lock-in. Downside rises to P45 from P35 — now the modal outcome. Downside is no longer a tail risk. Downside is the central scenario.

I. What the March 19 MindCast Analysis Predicted — and What Just Confirmed It

The March 19 publication built a five-signal falsification architecture with explicit observable triggers. The CDT Foresight Simulation’s trigger train identified six sequential developments: Arizona criminalizes the conflict; additional states borrow the frame; platforms narrow the contract universe; institutional capital pauses; appellate courts inherit the conflict; preemption arrives or gambling lock-in compounds.

Three of those six triggers activated within five days of publication:

Trigger 1 (Arizona criminalizes): Active since March 17, confirmed in the original publication.

Trigger 2 (Additional states borrow the frame): Nevada secured a temporary ban covering Kalshi, Polymarket, Robinhood, Crypto.com, and Coinbase — multiplatform expansion of the Arizona enforcement model within one enforcement cycle, not one legislative session.

Trigger 3 (Platforms narrow the contract universe): Kalshi’s preemptive screening announcement represents the first observable instance of contract-universe restriction. The PRGA framework predicted that criminal process — unlike civil enforcement — would erode the commitment device platforms rely on. A voluntary restriction accepted without a court order is precisely that erosion.

Trigger 3 carries special analytical weight. In a repeated-game framework, a platform accepting behavioral constraints voluntarily signals that the cost of maintaining full strategic commitment has risen above the strategic threshold. Kalshi’s behavioral shift is the most direct observable evidence available that the platform’s internal probability assessment of the upside case has contracted. Platforms know their own legal position better than external observers. The concession is the signal.

Activating the SCEM through the legislative channel simultaneously with appellate review — rather than sequentially after it — introduces a mechanism the March 19 analysis flagged but did not fully develop. Section V of the original publication identified Competitive Federalism as the active enforcement mechanism and the Posner Asymmetry — legal correction is slow, enforcement is fast — as the central structural condition favoring states. A CEA amendment resolves the Posner Asymmetry by moving the correction itself to the legislative channel, which operates faster than appellate review and with binding effect across all jurisdictions at once.

II. The Statutory Category Exclusion Mechanism — Why the Senate Bill Is Structurally Different

Modeling the enforcement conflict as a jurisdictional contest — CFTC preemption claims competing against state gambling statutes, with appellate courts as the eventual resolution venue — remains accurate for the state enforcement layer. Layered above it, the SCEM operates through a structurally distinct mechanism that does not compete with state authority but supersedes the entire jurisdictional contest by eliminating the statutory ambiguity both sides are fighting over.

Preemption Collapse

Kalshi’s federal preemption defense rests on the argument that the CEA grants the CFTC exclusive jurisdiction over event contracts and that state gambling statutes cannot override that federal grant. Courts have engaged with that argument seriously because the CEA is genuinely ambiguous on whether sports-linked event contracts fall within the derivatives category the statute governs. CFTC Chairman Selig’s amicus brief in the Nevada litigation reflects the same theory.

Eliminating that ambiguity by design is precisely what the SCEM accomplishes. Legislative record for the Prediction Markets Are Gambling Act explicitly states the intent to reinforce Congress’s original intent that the CEA does not permit sports gambling. Express statutory prohibition is not a regulatory interpretation subject to CFTC override or appellate revision. Preemption collapses directly:

No statutory ambiguity produces no judicial pathway to reinstate it.

No judicial pathway means the strategic delay equilibrium loses its structural foundation.

No delay equilibrium means classification resolves through legislation — irreversibly, across all fifty states simultaneously, on Congress’s timeline.

The geometry now favors elimination over competition. Kalshi can litigate state enforcement actions one jurisdiction at a time. Kalshi cannot litigate a direct congressional amendment to its enabling statute.

Selective Constraint and Flow Redistribution

Deliberately bounded, the bill’s scope bans sports contracts and casino-style games while leaving macro-event and policy-forecast categories intact. Contracts on Federal Reserve decisions, economic data releases, geopolitical developments, and electoral outcomes at the federal level sit in a different statutory exposure zone — one where the gambling framing has weaker purchase because participants hold genuine informational exposure and the hedging function is more legally defensible.

MindCast Field-Geometry Reasoning (FGR) predicts the behavioral response: the SCEM blocks one geodesic, and flow redistributes rather than disappears. Capital and participation will migrate toward macro-information contracts if the sports category closes. Platforms will redesign contract architectures to avoid categorical triggers — probabilistic framing, indirect event exposure, synthetic structures that preserve the informational function without replicating sportsbook payoff architecture.

Capital segmentation following sports restriction is Prediction 3 from the March 19 simulation, now operating on a compressed timeline. Institutional users face a risk management decision, not a speculative one: segment exposure ahead of Senate bill advancement or absorb statutory closure risk in the sports contract portfolio.

III. Updated Foresight Simulation — Phase Transition and Probability Revision

Probability assignments in the March 19 simulation rested on structural conditions active as of March 17. Five compounding developments — Arizona criminal charges, Nevada temporary ban, Ohio injunction denial, Kalshi’s preemptive concessions, and the Senate CEA bill — shift the structural conditions underlying each assignment. What follows does not represent subjective probability revision. Each updated figure reflects a state-transition output: reversible equilibrium has become conditional lock-in.

Base Case — Revised to P40 (from P45)

State-level enforcement expands across additional jurisdictions. Platforms restrict high-risk contract categories. Institutional adoption slows but remains exploratory. Fragmentation persists without decisive appellate resolution. Revision downward reflects the SCEM introducing a second resolution pathway — legislative rather than appellate — capable of collapsing the fragmented equilibrium faster than the original base case assumed. Holding the base case requires the Senate bill to stall in committee, which bipartisan sponsorship makes structurally less probable than a partisan measure.

Downside Case — Revised to P45 (from P35)

Coordinated enforcement across multiple states, amplified by criminal conviction risk in Arizona and SCEM passage, classifies prediction markets broadly as illegal wagering in the sports and entertainment categories. CFTC jurisdiction assertion fails for those categories. Institutional capital exits sports and entertainment contracts while macro-event contracts survive in a restricted derivatives framework. Downside is now the modal outcome. Absent from the March 19 analysis as a live legislative instrument, the SCEM threat now functions as the primary structural force in the system. Bipartisan Senate sponsorship is the critical new signal: sports restriction commands cross-aisle support that macro-event restriction does not.

Upside Case — Revised to P15 (from P20)

Federal regulators establishing a formal derivatives category through emergency rulemaking, or a favorable Supreme Court ruling preempting state gambling statutes, would open the upside path — but only for non-sports contract categories. A Supreme Court ruling cannot restore sports contracts if Congress has already amended the CEA to exclude them. Surviving only in truncated form, the upside case offers a derivatives framework for macro-event and policy-forecast contracts alongside a statutory ban on sports contracts. Full-spectrum institutional adoption of prediction markets as financial infrastructure is structurally precluded for the sports category regardless of appellate outcomes.

Revised probability distribution: Downside P45 / Base P40 / Upside P15. Downside is now the modal scenario. A unified federal classification framework resolving all contract categories simultaneously — the only development that would invalidate the fragmented equilibrium assumption — would require legislative coordination that the current bipartisan sports-only frame makes structurally improbable.

Contact mcai@mindcast-ai.com to partner with us on Predictive AI in Law and Behavioral Economics. A full foresight simulation output report is available upon request.

To deep dive on MindCast work in Cybernetic Foresight Simulations upload the URL of this publication into any LLM and prompt ‘reconstruct MindCast framework with three degrees of cited sub links.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure.

Recent projects: Chicago School Accelerated — AI Infrastructure Patent Coordination, MindCast Predictive Cybernetics Suite, The AI Infrastructure Energy Antitrust Landscape, Super Bowl LX — AI Simulation vs. Reality, Foresight on Trial, The Diageo Litigation Validation.

IV. Consumers — Behavioral Demand and Regulatory Targeting

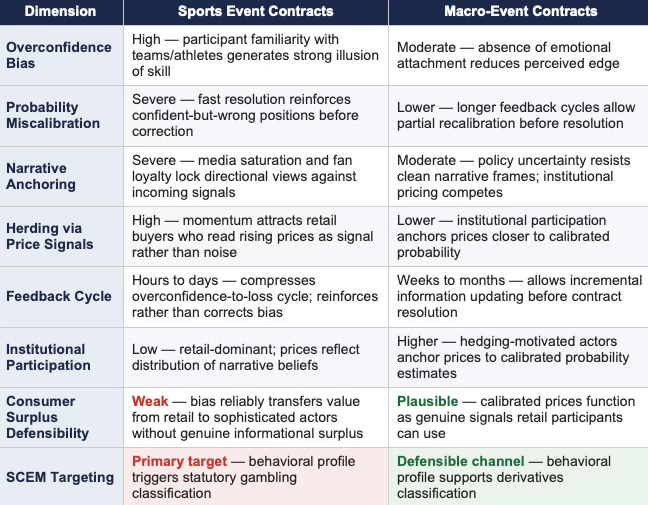

Prediction markets do not eliminate bias — they price it. Retail participants enter prediction markets carrying three behavioral drivers that the platforms’ informational framing obscures but does not neutralize: belief in personal informational edge, illusion of control over uncertain outcomes, and systematic misclassification of event contracts as investment instruments rather than wagers. Each driver is independently documented in behavioral economics literature. Prediction market contract architecture activates all three simultaneously, and sports contracts — with their short feedback loops, high emotional salience, and participant familiarity with the underlying events — amplify each one to the point where the behavioral profile is structurally indistinguishable from problem gambling.

Overconfidence bias drives entry: participants consistently overestimate the precision of their probability assessments on high-salience public events. Probability miscalibration compounds the entry error — retail participants treat a contract trading at 60 cents as confirmation that the market “knows” the outcome is 60 percent likely, rather than recognizing the price as a liquidity-weighted aggregate of similarly miscalibrated beliefs. Narrative anchoring locks positions: once a participant has formed a directional view, incoming price signals read as confirmation rather than information. Herding via price signals accelerates the loop — rising contract prices attract additional buyers who interpret momentum as signal. The result is a “market equals truth” fallacy that retail participants sustain even after repeated losses, because the market’s apparent precision supplies a plausible external explanation for each incorrect prediction.

Sports contracts concentrate all four dynamics at maximum intensity. Feedback resolves in hours or days, compressing the overconfidence-to-loss cycle into a timeframe that reinforces rather than corrects the bias. Emotional attachment to teams and athletes converts informational uncertainty into perceived skill — the participant who believes their team will win experiences contract purchase as informed prediction rather than bet placement. Macro-event contracts present a structurally different behavioral profile: feedback cycles span weeks or months, institutional participants with genuine hedging exposure anchor prices closer to calibrated probability, and the absence of emotional attachment reduces narrative anchoring. A retail participant buying a contract on the Federal Reserve’s next rate decision is operating under lower overconfidence pressure than one buying a contract on Sunday’s playoff outcome, because the former lacks the illusion of skill that sports familiarity generates.

Recognizing the behavioral asymmetry between contract categories explains why the SCEM is selective rather than categorical. Regulators targeting sports contracts are not making a judgment about prediction markets as a technology. They are making a judgment about which contract categories generate consumer harm — where “harm” means a behavioral environment in which systematic bias reliably transfers value from retail participants to sophisticated actors without supplying the informational surplus that justifies the market’s existence. Macro-event and policy-forecast contracts retain a plausible consumer surplus argument because calibrated institutional participation generates prices that retail participants can use as genuine signals. Sports contracts do not retain that argument at scale: when participation is dominated by emotionally anchored retail actors, the price reflects the distribution of narrative beliefs rather than the distribution of informational edges. Applying behavioral economics rather than just gambling law, regulators targeting the SCEM at sports contracts are making a durable choice — one whose durability derives precisely from the behavioral asymmetry the statutory structure encodes.

Consumer participation will not uniformly decline after sports restriction. Retail engagement will migrate toward macro-event contracts, where participants will carry the same overconfidence and miscalibration dynamics that drove sports contract participation — but into a contract category where those dynamics are less behaviorally catastrophic and more defensible under existing consumer protection frameworks. Lower average accuracy, despite higher perceived informational value, is the predicted consumer outcome of the migration. Platforms should treat that dynamic as the central design constraint for the post-restriction product architecture, not an afterthought.

Table 1: Contract Category Behavioral Profile

V. Field-Geometry Reasoning Update

Five field geometry scores from the March 19 simulation reflected conditions as of March 17. Updated measures as of March 24 follow. Across every metric, the geometry now favors elimination over competition.

Constraint Density (CD): 0.91 / High — Senate SCEM, Arizona criminal charges, Nevada ban, and Ohio denial compound the existing state statute layer. Each enforcement event increases constraint density nonlinearly because it generates a public evidentiary record that reduces the cost of parallel actions.

Attractor Dominance Score (ADS): 0.86 / Gambling attractor dominant — Legislative action strengthens the gambling classification path; the derivatives attractor has lost one of its two primary structural supports (CEA ambiguity). CFTC rulemaking capacity — the second support — remains constrained by the single-commissioner vacancy.

Geodesic Availability Ratio (GAR): 0.22 / Very Low — Derivatives pathway continuation now requires defeating the Senate bill, surviving the Nevada and Ohio appellate proceedings, and maintaining CFTC support — three simultaneous conditions where previously one would suffice.

Structural Persistence Threshold (SPT): 0.84 / High — Kalshi’s voluntary behavioral concessions create a public record that weakens the form-content decoupling argument in all future proceedings. Voluntary restriction accepted without court order functions as quasi-admission.

Escape Velocity Threshold (EVT): 0.91 / Near-prohibitive for sports contracts — Federal override now requires defeating legislation rather than outrunning rulemaking latency. The SCEM has moved the EVT for the sports category beyond what any administrative action can reach.

Widening materially, the gap between current CFTC institutional capacity and the Escape Velocity Threshold now separates administrative capability from what statutory reversal requires. Chairman Selig’s single-commissioner CFTC can assert jurisdiction, file amicus briefs, and issue guidance — but cannot override an express congressional amendment to its own enabling statute. For the sports category, the EVT is no longer a policy threshold. Congressional action has converted it into a constitutional one.

VI. Chicago Strategic Game Theory Vision — Equilibrium Update

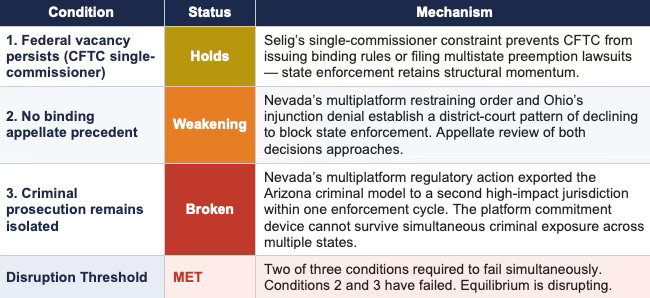

Framing the prediction markets conflict as a delay-dominant, jurisdictionally fragmented equilibrium sustained by positive delay payoffs for every actor remains accurate as a starting point. Three structural conditions sustained that equilibrium in the March 19 analysis. Two have now failed or broken. MindCast AI Emergent Game Theory Frameworks | The Dual Nash-Stigler Equilibrium Architecture.

Condition 1 (Federal vacancy persists): Holds. Selig’s single-commissioner constraint remains the primary structural support for state enforcement momentum.

Condition 2 (No binding appellate precedent): Weakening. Nevada’s multiplatform temporary restraining order and Ohio’s injunction denial do not constitute binding appellate precedent, but they establish a district-court pattern of declining to block state enforcement. Appellate review of those decisions approaches.

Condition 3 (Criminal prosecution remains isolated): Broken. Nevada’s multiplatform regulatory action demonstrates that the Arizona criminal model exported to a second high-impact jurisdiction within one enforcement cycle. Maintaining the preemption argument by refusing state jurisdiction through compliance — the core commitment device — cannot survive simultaneous criminal exposure across multiple states.

Table 2: Equilibrium Conditions Status

Two conditions have failed. The equilibrium is disrupting.

Confirming the PRGA prediction and extending it, Kalshi’s behavioral response reveals a platform no longer defending classification but pre-positioning for statutory survival — adapting to expected law rather than current law. Feedback loops tightened by criminal process pressure, adaptation velocity increased by the SCEM threat, platform behavior driven by the anticipated statutory regime rather than the current enforcement posture: all three are Cybernetic Control Vision in action. Anticipation has replaced reaction.

Platforms have already repriced the upside case. Voluntary concessions make that repricing observable. No platform sustaining a genuine belief in a P20-or-higher upside case accepts behavioral constraints without a court order during the critical period when preemption arguments remain live. The concession is the signal. The repricing has occurred.

VII. Forward Predictions — Updated Sequence

Prediction 1 — Contract Narrowing (T+0 to T+6 months)

Compressed from T+6 to T+12 months. Kalshi’s preemptive screening announcement activates Prediction 1 immediately. Formal contract-category restrictions — removal or geofencing of sports and entertainment contracts — will precede Senate bill advancement as platforms attempt to moot the legislation’s most immediate threat.

Prediction 2 — Follow-On State Action (T+0 to T+6 months)

Compressed from T+3 to T+9 months. Nevada’s multiplatform enforcement action confirms Prediction 2 is already active. Two to four additional states will file formal proceedings within the next quarter using Nevada’s restraining order architecture as the template.

Prediction 3 — Capital Segmentation (T+3 to T+9 months)

Unchanged timeline, elevated probability. Institutional users will segment sports and entertainment contract exposure ahead of Senate bill advancement. Capital segmentation is now a risk management decision, not a speculative one.

Prediction 4 — Appellate Centrality (T+9 to T+18 months)

Unchanged. A small number of appellate cases will define the preemption boundary for non-sports contract categories. Sports contracts face a separate and faster legislative resolution track through the SCEM.

Prediction 5 — SCEM Binary Event (T+30 to T+90 days)

New prediction. Senate Agriculture Committee action — Schiff sits on the committee — will determine whether the SCEM accelerates faster than appellate review. A committee advancement triggers simultaneous probability revision across all three scenario classes. A committee stall is the single observable most likely to temporarily stabilize the upside case.

Prediction 6 — Political Spillover (T+6 to T+18 months)

New prediction, absent from the March 19 analysis. Statutory exclusion of sports contracts will generate legislative scrutiny of political event contracts within six to twelve months. Identical coalition incentives produced the bipartisan sports bill — state sovereignty concerns, tribal gaming protection, consumer protection framing — and apply with near-equal force to election event contracts. Binary payoffs on public events that retail participants treat as bets present the same optics problem regardless of whether the event is a playoff or a primary. No legislative actor who has committed to the sports exclusion frame can credibly resist extending it to election contracts without a principled distinction that the contract architecture does not supply. Political spillover is the second-order consequence of activating the SCEM, and no current market participant’s public probability estimate appears to incorporate it.

Prediction 7 — Consumer Migration with Accuracy Decline (T+6 to T+18 months)

New prediction, grounded in the consumer behavioral layer. Retail participation will decline in restricted sports categories but increase in macro-event contracts, with lower average predictive accuracy despite higher perceived informational value. Overconfidence bias, probability miscalibration, and narrative anchoring migrate with the participant — they do not dissolve upon category transfer. Macro-event contracts will attract retail participants who misclassify their informational edge in a domain where they have less sports-style familiarity, generating a behavioral environment where prices reflect the distribution of narrative beliefs rather than calibrated probability. Falsifier: retail accuracy improves materially post-migration, or participation declines uniformly across all categories rather than redistributing.

VIII. Falsification — Updated Conditions

Derivatives Pathway Validation (Upside Confirmation)

Senate Prediction Markets Are Gambling Act fails to advance out of committee within 90 days of introduction, preserving the CEA ambiguity that supports the preemption argument.

Federal appellate court affirms CFTC preemption in Nevada or a parallel circuit, establishing binding precedent that state enforcement cannot override CFTC jurisdiction over registered prediction market platforms.

Arizona criminal charges resolve to civil settlement before trial, eliminating the commitment-device erosion dynamic the PRGA framework identifies as the primary behavioral threat.

Gambling Classification Confirmation (Downside Confirmation)

Senate bill advances to floor vote within 60 days, particularly if additional Republican co-sponsors join Curtis — signaling the bipartisan frame is durable enough to survive CFTC jurisdictional objections.

Two or more additional state attorneys general file criminal charges against prediction market platforms using the Arizona template, converting isolated prosecution into a multistate criminal enforcement pattern.

Kalshi formally removes or geofences sports contract categories before the Senate bill passes — a voluntary restriction that functions as quasi-concession and weakens the preemption commitment across all parallel proceedings simultaneously.

Political event contracts draw Senate scrutiny within six months of sports contract restriction, confirming the SCEM spillover prediction.

Framework Failure Conditions

MindCast AI’s analytical architecture fails under two conditions. First: Congress enacts a unified federal classification framework covering all prediction market contract categories within 12 months. A unified framework would invalidate the fragmented equilibrium assumption — the system resolving faster and cleaner than the architecture predicts, eliminating rather than confirming the fragmentation dynamic. Second: platform participation contracts rather than migrates following sports restriction, contradicting the FGR flow-redistribution prediction. Both failure conditions require outcomes that the current bipartisan sports-only legislative frame and field-geometry scores assign low structural probability.

Conclusion

Legislative action has removed ambiguity from the system faster than courts could resolve it. Platforms, capital, and regulators are now adapting to a constraint that has not yet passed but is already shaping behavior. Converting a jurisdictional contest into a statutory regime, the SCEM raises the bar for reversal from a favorable ruling to a legislative override — a higher threshold, operating on a different timeline, producing binding effect that no administrative body can circumvent.

Prediction markets retain a viable institutional future in macro-event and policy-forecast contract categories where the gambling framing has weaker statutory purchase. Sports and entertainment categories face a different trajectory. Extending that trajectory further than current market pricing reflects, the second-order risk — political spillover from sports restriction to election contract scrutiny — now belongs in every capital allocation model operating in the sector.

Platforms, capital, and regulators are no longer deciding whether prediction markets are gambling. All three are deciding which categories survive the classification. Capital allocation decisions and platform design choices made in the next 90 days will determine which platforms capture the flow redistribution that FGR predicts, and which ones stake their survival on a preemption argument whose statutory foundation is under active legislative revision.

Category selection governs survival. The Statutory Category Exclusion Mechanism has compressed the timeline for that selection from years to months.