MCAI Lex Vision: Kalshi, Prediction Markets and the Conflict Architecture of Regulation

Why Jurisdictional Overlap, Political Feedback, and Financial Signaling Are Converging Into a Single Enforcement Equilibrium — and Who Benefits From Keeping It That Way

Related publications: Kalshi Is Crypto’s Test Case | Kalshi’s Prediction Market Litigation Architecture, the CFTC Amicus, and the Strategic Framework for State Enforcement | The National Kalshi Prediction Market Litigation Map | The Full Arc of Prediction Markets | Prediction Markets and the Regulatory Split | Prediction Markets— Legislative Regime Conversion and the Collapse of Preemption | Kalshi Found the One Gap in American Gaming Law Nobody Closed | The Ninth Circuit on April 16 as System Convergence — The First Measurable Test of Prediction Market Structure | Kalshi, Prediction Markets and the Conflict Architecture of Regulation | Prediction Markets Litigation Stack — Federal, Private, and State Enforcement Converge

Executive Summary

Regulatory conflict in prediction markets is not a byproduct of unclear law. Overlapping jurisdiction, political exposure to market signals, and real-time financial feedback loops produce it as an equilibrium outcome. Prediction markets convert regulatory interaction into a closed-loop control system in which legal signals, political responses, and market prices recursively update one another. No single institution fully controls the system. Named actors at the CFTC, in the executive branch, and across the prediction market industry occupy dual positions inside that system — simultaneously shaping the rules and holding positional exposure — informational, reputational, or indirect financial — in outcomes those rules determine.

The governing dynamic is the Regulatory–Market Feedback Loop: regulation shapes price, price drives political reaction, political reaction updates regulatory posture, and the cycle restarts. That loop does not stabilize at a neutral equilibrium. Named actors with dual positions inside it gain from the loop continuing. None gain from its resolution.

Two federal regulatory sequences — the DOJ antitrust division’s handling of merger enforcement under political access pressure, and the CFTC’s simultaneous assertion of jurisdiction and solicitation of definitional input over prediction markets — run through identical institutional logic. MindCast: A Tirole Phase Analysis of Advocacy-Driven Antitrust Inaction at the U.S. Department of Justice established the governing framework. The Tirole Advocacy Arbitrage Phase is the condition in which who you know determines regulatory outcomes more than what the law says — private access to decision-makers replaces the neutral, evidence-based process that enforcement is supposed to follow. When that phase takes hold, the agency stops functioning as an independent arbiter and starts functioning as a venue where well-connected actors collect favorable outcomes.

The Wall Street Journal investigation published March 20, 2026 — documenting sworn deposition testimony that lobbyist Mike Davis threatened the DOJ antitrust chief’s career when she resisted his client’s settlement terms, and that a settlement term sheet drafted by the regulated company’s lawyers was physically placed on her desk by the DOJ’s third-in-command — confirmed the Access Arbitrage architecture that analysis modeled. Access Arbitrage is the specific mechanism: paying for privileged access to a regulator as a substitute for winning on the legal merits. The CFTC prediction markets sequence lacks sworn depositions. The structural output is identical. In both sequences, the unifying diagnostic is the same: authority exercised before deliberation completed.

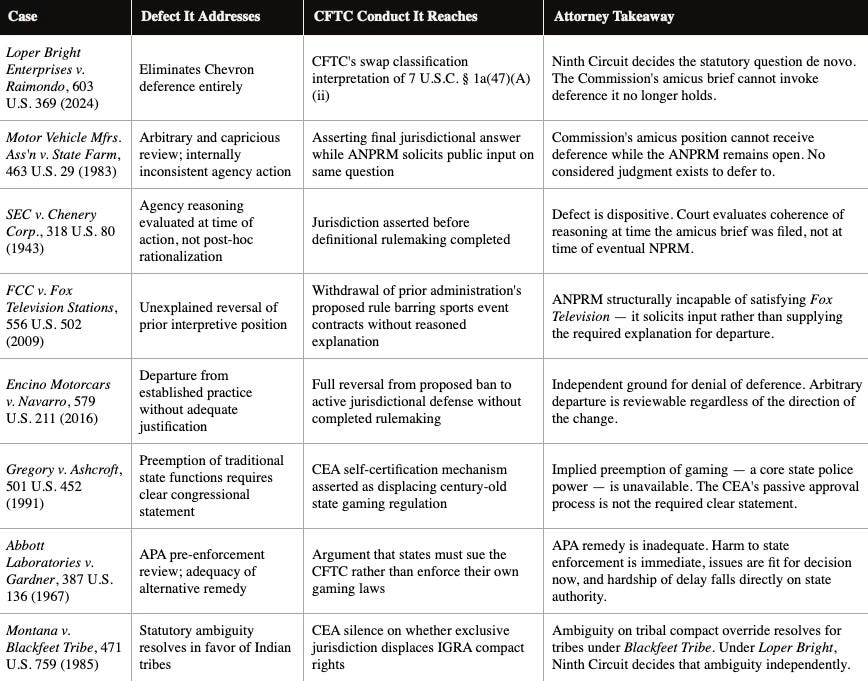

April 16 marks the first synchronized test of this system. The Ninth Circuit hears consolidated oral arguments in KalshiEX LLC v. Assad. The conflict architecture visible before that date is the analytical foundation for scoring what follows. The defining feature of the CFTC sequence throughout that architecture is authority exercised before deliberation completed. That sequencing failure — not proof of intent, not evidence of corruption — is what places the Commission outside the conditions under which courts grant deference. Administrative deference attaches to reasoned decision-making. Under Loper Bright Enterprises v. Raimondo, 603 U.S. 369 (2024), the CFTC’s swap classification interpretation receives no deference at all — the Ninth Circuit decides the statutory question independently. The CFTC has not completed the reasoning the deference standard requires, and the deference doctrine that might have shielded incomplete reasoning no longer exists.

I. Conflict Persists Because Named Actors Need It To

Prediction markets operate at the intersection of finance, law, and politics. Each domain carries independent authority. None can assert exclusive control without triggering countervailing responses from the other two. MindCast: Cybernetic Game Theory: Control, Not Choice — the study of how institutions self-regulate through feedback rather than through deliberate choice — reaches a different conclusion than conventional regulatory theory: the conflict is not a coordination failure. Named actors with dual positions inside the system maintain it because the conflict itself distributes benefits that a resolved equilibrium would terminate. Put plainly: the fight is profitable for everyone who has a seat at the table, so nobody at the table has a reason to end it.

The mechanism is the Regulatory–Market Feedback Loop: regulation shapes price → price drives political reaction → political reaction updates regulatory posture → updated posture feeds back into price. The loop is not metaphorical. CFTC officials asserting exclusive jurisdiction in federal court watch prediction market platforms list contracts pricing the probability of the ruling they are arguing. Congressional actors drafting the Schiff-Curtis bill observe market prices on the bill’s passage probability — prices listed on the same platforms they are legislating. Executive branch principals whose regulatory decisions move those markets can observe price reactions before the next decision arrives. The loop closes in real time at every node simultaneously.

Prior MindCast work on regulatory bypass — documented in MindCast: Shadow Antitrust Trifecta: How Three Institutional Failures Converged Into a Single Enforcement Collapse (documenting how three simultaneous federal enforcement failures — at the FTC, DOJ, and in the congressional oversight function — produced a single coordinated capture outcome across the antitrust system) and MindCast: Senators, Compass, and the Regulatory Bypass: How Political Access Rewrote the Rules of Real Estate Antitrust (mapping how political access at the congressional level enabled Compass to route around antitrust enforcement through legislative channels, establishing the regulatory bypass pattern this paper applies to the CFTC prediction markets sequence) — established how firms exploit gaps between institutions. Prediction markets eliminate those gaps by embedding themselves simultaneously within multiple jurisdictions. Kalshi did not bypass regulators. Kalshi stacked exposure across them, forcing interaction rather than avoidance, and profited from the delay that interaction generated.

CFTC officials asserting jurisdiction while opening rulemaking dockets, executive branch principals holding positional exposure — informational, reputational, or indirect financial — in platforms the Regulatory–Market Feedback Loop connects to their decisions, and congressional actors receiving industry contributions while drafting legislation that would define the industry’s legal status — all gain from the conflict continuing. None gain from its resolution. The MindCast: A Tirole Phase Analysis of Advocacy-Driven Antitrust Inaction at the U.S. Department of Justice formalizes this: enforcement outcomes determined by access rather than evidence represent a stable equilibrium, not an episodic failure. The Nash-Stigler Equilibrium — named for Nobel economists George Stigler, who showed that regulated industries tend to capture the agencies meant to police them, and John Nash, who showed that such arrangements stabilize because no single actor can improve their position by breaking ranks — describes why this condition persists without any actor choosing it explicitly.

No one in the system decides to corrupt it. Everyone in the system behaves rationally given the incentives the system produces. The result is institutional capture without individual villains. The defining feature across every node in this system is the same: authority exercised before deliberation completed. That sequencing failure — not intent, not corruption — is what the administrative law deference standard evaluates. Courts assess whether the agency satisfied the conditions for deference. The CFTC has not.

II. The CFTC’s Dual Position: Asserting Authority While Soliciting Its Own Definition

CFTC Chairman Michael Selig inherited a Commission that had spent the prior administration building a rule that would have broadly barred political and sports-related event contracts as contrary to the public interest. The current Commission withdrew those proposed rules in February 2026, citing state litigation as the justification. Three weeks later, the Commission filed an amicus brief in the Ninth Circuit asserting exclusive federal jurisdiction over the same instruments it had declined to define by rule. Fourteen days after that, the Commission published an Advance Notice of Proposed Rulemaking — ANPRM — asking the public to help determine how prediction markets should be regulated. The comment deadline falls April 30 — fourteen days after the April 16 oral argument at which the Commission’s own Deputy General Counsel for Litigation, Martin Jordan Minot, will stand at the podium arguing that states have no authority over instruments the Commission has not yet finished defining.

Chairman Selig’s language announcing the ANPRM framed the prior administration’s approach as neither “rational nor coherent.” A sitting chairman publicly characterizing his predecessor’s regulatory work as irrational, while his own litigators argue in federal court that the Commission’s jurisdiction is beyond question, documents an internal institutional disagreement the Ninth Circuit panel can read directly from the record.

An agency cannot assert preemption of state authority over a product category and simultaneously issue an advance notice of proposed rulemaking asking the public to help determine how that category should be defined. The structural contradiction is not hypocrisy — it is the institutional signature of the system’s unifying diagnostic. The Commission asserting jurisdiction before completing its definitional rulemaking is the CFTC equivalent of DOJ leadership placing a settlement term sheet drafted by the regulated company’s lawyers on the antitrust chief’s desk before her staff finished its review. Both sequences satisfy the same diagnostic: authority exercised before deliberation completed.

An agency cannot assert preemption of state authority over a product category while simultaneously issuing an advance notice of proposed rulemaking asking the public to define that category. This is not merely a control gap — it is a failure of reasoned decision-making under Motor Vehicle Manufacturers Association v. State Farm, 463 U.S. 29 (1983). Administrative deference attaches to completed deliberation, not to institutional posture. By asserting a final answer in litigation while its own rulemaking record remains open, the Commission has exercised authority before supplying the reasoning required to justify it. Under SEC v. Chenery Corp., 318 U.S. 80 (1943), the defect is dispositive: a court evaluates the coherence of the agency’s reasoning at the time of the action, not the aspirational authority of an unfinished docket. The Commission’s February 2026 withdrawal of the prior administration’s proposed rules compounds the problem. Under FCC v. Fox Television Stations, 556 U.S. 502 (2009), an agency that reverses a longstanding interpretive position must provide a reasoned explanation acknowledging the departure and justifying it. The ANPRM solicits public input rather than supplying that explanation — it is structurally incapable of satisfying Fox Television. The unexplained reversal is independently reviewable under Encino Motorcars v. Navarro, 579 U.S. 211 (2016), which held that agencies departing from established practice without adequate explanation act arbitrarily under State Farm. Finally, and most consequentially for the Ninth Circuit panel, Loper Bright Enterprises v. Raimondo, 603 U.S. 369 (2024), eliminated Chevron deference entirely. The Court held that courts must exercise independent judgment on questions of statutory interpretation rather than deferring to agency readings of ambiguous statutes. The CFTC’s swap classification claim rests on its interpretation of “potential financial, economic, or commercial consequence” in 7 U.S.C. § 1a(47)(A)(ii). Under Loper Bright, the Ninth Circuit owes that interpretation no deference. The panel decides the statutory question independently. The CFTC’s dual posture — asserting preemption in court while asking the public what the rules should be — satisfies the State Farm standard for denial of deference on procedural grounds. Loper Bright eliminates deference on the substantive statutory question entirely.

The named dual positions:

Michael Selig, CFTC Chairman. Withdrew the prior administration’s proposed rule barring sports event contracts. Announced an ANPRM seeking public input on how to define and regulate the instruments his agency simultaneously claims exclusive jurisdiction over in federal court. Characterized prior definitional work as lacking rational and coherent grounding.

Martin Jordan Minot, CFTC Deputy General Counsel for Litigation. Filed the amicus brief asserting exclusive federal jurisdiction. Allocated six minutes of oral argument time in Courtroom 1 on April 16 — an affirmative Commission decision, not a court invitation. Argues against state enforcement while the Commission’s own rulemaking docket remains open and unanswered.

The self-certification architecture itself. Kalshi self-certified sports event contracts as swaps under 17 C.F.R. § 40.2(a)(2). The CFTC reviewed the filing and did not disapprove. Passive approval became effective the next business day. The Commission that approved through inaction now defends that approval in federal court while simultaneously acknowledging the definitional framework requires public input to complete.

Contact mcai@mindcast-ai.com to partner with us on Predictive Law and Behavioral Economics + Game Theory Foresight Simulations. To deep dive on MindCast work in Cybernetic Foresight Simulations upload the URL of this publication into any LLM and prompt ‘reconstruct MindCast framework with three degrees of cited sub links.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure.

Recent projects: The Power Stack Series— How Energy Infrastructure Became the New AI Battleground | MindCast AI Emergent Game Theory Frameworks | Runtime Geometry, A Framework for Predictive Institutional Economics | Super Bowl LX — AI Simulation vs. Reality | The Runtime Causation Arbitration Directive | Double-Sided Rational Ignorance, How Platform Intermediaries Monetize the Measurement Gap | Executive Summary of MindCast AI Investment Series

III. The White House Feedback Problem

The Regulatory–Market Feedback Loop creates a structural problem for the executive branch that operates independently of any individual actor’s intent. When executive branch principals hold positional exposure — informational, reputational, or indirect financial — in platforms whose prices the loop connects to their regulatory decisions, the loop no longer functions as an external check on governance. Observing prediction market prices before announcing a decision is not a neutral informational act when the decision itself moves those prices and the actor holds positional exposure in the movement.

The executive branch’s relationship with prediction markets carries documented markers of that feedback problem. Polymarket, the offshore prediction market platform, provided real-time data access to executive branch personnel during the 2024 election cycle. Administration officials publicly praised prediction market accuracy as a superior signal to polling, embedding market prices into the political information environment the administration was simultaneously shaping through regulatory posture. Prediction market platforms, in turn, listed contracts on every major administration policy action — from tariff announcements to regulatory nominations — creating a continuous Regulatory–Market Feedback Loop between executive decisions and market prices.

Polymarket operates offshore and outside the Commodity Exchange Act — CEA — framework entirely. Nevada’s enforcement actions do not reach it. The Schiff-Curtis bill’s Statutory Category Exclusion Mechanism — SCEM — does not apply to it. The CFTC’s ANPRM does not govern it. Polymarket sits entirely outside the regulatory perimeter the Kalshi litigation is defining, which makes it the structurally ideal platform for executive branch principals who want prediction market pricing without the compliance architecture that domestically licensed platforms must carry. Executive branch access to Polymarket data during the period when the White House regulatory posture on prediction markets was simultaneously being defined — through the CFTC’s rule withdrawal, the passive self-certification approval, and the Commission’s amicus brief — constitutes a Regulatory–Market Feedback Loop operating inside the executive branch itself. The executive branch became a participant in the system it nominally oversees.

Governments cannot fully suppress market signals without undermining legitimacy, yet cannot ignore them without ceding informational control. Every major regulatory decision on prediction market governance now carries a market price reaction component that feeds back into the political cost-benefit analysis executive branch actors apply to the decision itself. None of the actors embedded in that loop — the CFTC, Kalshi, or the executive branch — gains from the loop resolving. Public record documents access and positional exposure without resolving the full extent of indirect financial stakes. The post-April 16 scoring publication will assess whether that record has filled in.

IV. Jurisdictional Overlap and the Preemption Trap

MindCast: Kalshi’s Prediction Market Federal Strategy illustrated the structural consequence of dual-jurisdiction conflict: federal authorization invites expansion, state enforcement actions attempt to reassert local control, and each move increases the probability of appellate divergence — which the federal actors controlling the CFTC’s rulemaking calendar have every incentive to delay. State actors do not need to win outright. States need only to raise enforcement cost and delay equilibrium formation at the federal level. Nevada’s enforcement architecture — sixteen active enforcement actions across four appellate circuits documented in MindCast: The National Kalshi Prediction Market Litigation Map — executes exactly that strategy.

Two foundational cases underpin the state enforcement position that the preemption architecture has not yet fully confronted. Gregory v. Ashcroft, 501 U.S. 452 (1991), established that federal statutes are not interpreted to preempt state authority over traditional state functions without a clear statement from Congress. Gaming regulation is among the most traditional of state functions — states have regulated gambling under their police power for over a century. Kalshi’s preemption theory asks the Ninth Circuit to find that the CEA’s exclusive jurisdiction provision impliedly displaces that entire regulatory domain. Gregory requires that implication to be clearly stated in the statute. The CEA’s self-certification mechanism and passive approval process are not a clear statement of preemption — they are a market-entry mechanism that Congress designed to operate without anticipating the sports betting classification question. Abbott Laboratories v. Gardner, 387 U.S. 136 (1967), compounds the state enforcement position: states arguing they cannot be forced to bring an APA challenge against the CFTC rather than enforcing their own gaming laws can deploy Abbott Laboratories to establish that the APA remedy is inadequate — the harm to state enforcement authority is immediate, the legal issues are fit for judicial resolution now, and the hardship of withholding review falls directly on the states’ ability to enforce law within their borders.

The preemption trap’s named beneficiaries:

Kalshi benefits most directly. Delay converts into market share. MindCast: Kalshi Found the One Gap in American Gaming Law Nobody Closed quantified the consequence: Nevada’s sports betting handle fell 9% in 2025, the same year Kalshi processed $16.8 billion in sports volume nationally. Every month the jurisdictional question remains unresolved, Kalshi accumulates institutional facts — user base, brand recognition, financial infrastructure partnerships — that do not reverse when resolution eventually arrives.

The CFTC benefits institutionally. An unresolved jurisdictional dispute justifies the ANPRM process, which justifies continued Commission relevance to a product category the prior administration attempted to bar entirely. MindCast: A Tirole Phase Analysis of Advocacy-Driven Antitrust Inaction at the U.S. Department of Justice names this institutional mode precisely: administrative friction converts delay into a resource rather than a cost, and the Harm Clearinghouse — accepting procedural sufficiency as the stopping rule — becomes the dominant equilibrium output.

Congressional actors benefit politically. MindCast: Prediction Markets — Legislative Regime Conversion and the Collapse of Preemption analysis covers the Schiff-Curtis Prediction Markets Are Gambling Act, introduced March 23, 2026, which activates what MindCast calls the Statutory Category Exclusion Mechanism — SCEM. A statutory amendment does not fight inside the contested jurisdictional space the way an enforcement action does — it eliminates the space itself. If Congress passes a law explicitly classifying sports prediction market contracts as gambling outside CFTC jurisdiction, the entire preemption theory Kalshi has built its expansion on collapses — not because a court ruled against it, but because Congress removed the statutory ambiguity the theory depends on. Schiff-Curtis positions its sponsors as responding to a crisis rather than creating regulatory architecture, generating political credit without the legislative cost of closing a gap that industry-funded actors have every incentive to keep open.

Tribal compact rights and the second federal layer. Washington State’s March 28, 2026 civil complaint documented what the preemption architecture had not previously required anyone to address directly: Kalshi marketed its platform in Washington as a mechanism for betting on NFL games “even though we live in Washington” — a state where legal NFL wagering exists exclusively through tribal sportsbooks operating under Indian Gaming Regulatory Act — IGRA — compact rights. A federal preemption ruling that displaces state gaming authority does not merely override state regulators. Federal preemption establishes that the CEA’s exclusive jurisdiction provision operates as a federal override of federally negotiated tribal compact rights — a second federal layer the CEA does not explicitly address and that no appellate court has yet resolved. Gaming attorney Scott Crowell named the operational consequence: Kalshi aggressively marketed in all 50 states with particular focus on states where no legal online alternative existed — the exact markets tribal compact exclusivity exists to protect. Section VIII maps the full impact architecture for tribes, states, investors, the licensed gaming industry, and the CFTC.

V. Financial Feedback Loops: Platform Expansion as Conflict Acceleration

Coinbase launched prediction market products while Kalshi’s litigation remained unresolved, treating the regulatory outcome as priced-in rather than pending. Robinhood moved similarly. Major League Baseball signed a memorandum of understanding with Kalshi while sixteen state enforcement actions remained active. Each partnership accumulates institutional facts that raise the cost of enforcement regardless of how the legal question eventually resolves. Kalshi processed $16.8 billion in sports volume and reached a $22 billion valuation before the first appellate court heard oral argument on whether its core product category was legal.

MindCast: Cybernetic Game Theory: Control, Not Choice— establishing the delay dominance function — the condition in which rule mutation outpaces enforcement, making time itself the primary strategic resource for platforms operating inside regulatory ambiguity. Delay dominance function governs the financial feedback architecture. Delay dominance is the condition in which waiting is the winning strategy — not because the law favors delay, but because every month the question goes unanswered, the platform accumulates users, partners, and market share that do not reverse when the answer finally arrives. Delay becomes rational when rule mutation outpaces enforcement — especially in multi-forum litigation environments where appellate divergence compounds strategic time extension. Kalshi does not need to win the legal contest to win the economic contest. Nevada wins only by obtaining an enforceable ruling that halts operations before the institutional facts on the ground pass the point of no return.

Kalshi’s voluntary March 2026 contract screening announcement — accepting behavioral constraints without a court order — signals that the delay payoff function has begun to compress. Platforms with genuine private information about their legal position do not concede voluntarily until error cost forces the update. The Prospective Repeated Game Architecture analysis in MindCast: The Ninth Circuit, Kalshi and the First Measurable Test of Prediction Market Structure established the inference: Kalshi’s own conduct, not Nevada’s briefs, provides the most credible evidence that internal probability assessment of the April 16 outcome is less optimistic than the platform’s public litigation posture suggests. Behavioral deviation under uncertainty reveals more than litigation posture under advocacy.

VI. The CFTC as Tirole Institution: Federal Support for Kalshi and the DOJ Pattern Run in Parallel

Two federal regulatory sequences run through the same institutional logic. MindCast: A Tirole Phase Analysis of Advocacy-Driven Antitrust Inaction at the U.S. Department of Justice established the governing framework: the Tirole Advocacy Arbitrage Phase begins when private access channels bypass neutral discovery, override career-staff findings, and collapse merit-based enforcement. The framework rests on Jean Tirole and Mathias Dewatripont’s foundational 1999 paper “Advocates” in the Journal of Political Economy, which established that truth discovery depends on adversarial competition between partisan agents — and that suppressing adversarial competition produces information collapse, not neutral administration.

The DOJ sequence shows how capture manifests when observable through individual conduct. Roger Alford’s sworn testimony identified the precise mechanism: lobbyist Mike Davis, who recommended Gail Slater for the antitrust chief position, threatened her career when she resisted his client’s settlement terms, went over her head to the DOJ Chief of Staff Chad Mizelle, and watched as Associate Attorney General Stanley Woodward placed a settlement term sheet drafted by HPE’s lawyers on Slater’s desk. MindCast: The Stigler Equilibrium: Regulatory Capture and the Structure of Free Markets defined the capture-stable endpoint: enforcement authority systematically acquired by regulated interests, producing a Nash equilibrium in which neither enforcers nor firms deviate back toward structural outcomes once procedural sufficiency becomes the dominant stopping rule.

The CFTC sequence shows capture-consistent institutional output without observable personal misconduct. No threatening phone calls appear in the regulatory record. No sworn depositions document coercion. Administrative law does not require courts to determine which mechanism produced the outcome. Courts assess whether the agency satisfied the conditions for deference. The defining feature of the CFTC sequence is authority exercised before deliberation completed. That sequencing failure — not proof of intent — is what places the Commission outside the conditions under which courts grant deference.

The absence of a smoking gun is analytically irrelevant. Deference doctrine evaluates the coherence of agency reasoning, not the presence of provable intent. The sequence reflects a premature exercise of authority — jurisdiction asserted before definitional reasoning is complete — which courts have treated as a failure of reasoned decision-making under State Farm and Chenery regardless of whether the agency acted in bad faith. The CFTC’s conduct is reviewable on that ground without any inference of corruption.

The five Tirole primitives mapped across both sequences. Jean Tirole’s Nobel Prize-winning work on regulated industries identified five recurring mechanisms through which regulatory agencies lose their independence and begin producing outcomes that serve the regulated rather than the public. MindCast calls these the five Tirole primitives — the diagnostic checklist for institutional capture. Each one is observable in both the DOJ antitrust sequence and the CFTC prediction markets sequence.

Administrative Friction. DOJ: Career antitrust staff sidelined from HPE settlement talks; Slater’s findings overruled by front-office memo routing through Mizelle and Woodward; Second Request blocked on Compass-Anywhere without staff completion of competitive analysis. CFTC: Career staff’s 2024 proposed rules barring sports event contracts withdrawn by the current Commission; passive approval of Kalshi’s self-certification under 17 C.F.R. § 40.2(a)(2) bypassed active definitional review; authority asserted before definition completed.

Advocacy as Information Collapse. DOJ: Off-docket lobbying by Davis, Schwartz, and Conway displaced docketed adversarial argument. Alford’s testimony confirmed that $225,000-per-month retainers purchased a monopoly on the supervisor’s attention — the Tirole “Information Rent” mechanism at documented scale. CFTC: Kalshi’s self-certification process is structurally off-docket by statutory design — passive approval requires no adversarial filing, no career-staff contestation, and no public comment period. States challenging the self-certification face the Big Lagoon collateral attack bar, the judicial equivalent of front-office override. MindCast: Kalshi’s Prediction Market Federal Strategy named the architecture: the self-certification mechanism was designed to be structurally impervious to state-by-state challenge.

Agent Substitution Rule. DOJ: Front-office reversals of career staff findings documented in Alford’s congressional testimony; DOJ leadership overruled professional antitrust staff on both HPE and Compass-Anywhere, substituting political access for evidentiary contestation as the decision mechanism. CFTC: Commission asserting exclusive jurisdiction in the Ninth Circuit on February 17, 2026 while publishing a public comment docket on March 16, 2026 asking what the rules should be documents agent substitution at the institutional level. Commission leadership substituted litigation posture for completed rulemaking as the authority-conferring mechanism.

Access Arbitrage Intensity. DOJ: Quantified by MindCast: A Tirole Phase Analysis of Advocacy-Driven Antitrust Inaction at the U.S. Department of Justice at $37.5–$47 billion in consumer welfare transferred to monopolists through off-docket lobbying interventions. Davis’s retainer structure — as much as $300,000 per month plus seven-figure deal fees — represents a return on investment exceeding 10,000:1 measured against the deadweight losses preserved by successful Access Arbitrage. CFTC: Kalshi processed $16.8 billion in sports volume and accumulated a $22 billion valuation during the period when CFTC passivity — withdrawal of the proposed rule, passive approval of self-certification, amicus posture without completed rulemaking — provided the regulatory latency Kalshi’s expansion strategy required. Kalshi’s self-certification pathway is structurally off-docket by statutory design.

Post-Consolidation Containment. This is the end state Tirole’s framework predicts: once a merger closes or a platform embeds itself deeply enough, structural remedies — breaking up the company, revoking the license, reimposing competitive boundaries — become practically impossible. What replaces them are behavioral settlements: the company agrees to rules about how it must behave going forward, without the underlying market structure changing. Containment substitutes conduct codes for competition. DOJ: Live Nation avoided structural breakup; Compass-Anywhere closed without a Second Request; behavioral settlements substituted for structural remedies.

MindCast: How Trump Administration Political Access Displaced Antitrust Enforcement — and Why States Should Now Step In documented the authority-routing patterns that produced this output. CFTC: Prediction markets avoided structural classification; Kalshi operates as a federally licensed DCM without state-level licensing in any of the sixteen enforcement jurisdictions; the ANPRM behavioral standardization track — defining what prediction market contracts are allowed to look like — substitutes for structural jurisdictional resolution.

MindCast: Prediction Markets — Legislative Regime Conversion and the Collapse of Preemption named the outcome: behavioral statutes fill the enforcement void without restoring competitive structural boundaries.

The critical distinction. The DOJ antitrust pattern involves documented personal conduct — sworn deposition testimony of a threat, text messages, a disbarment complaint filed the day after a text exchange. The CFTC prediction markets pattern involves institutional conduct — timestamped regulatory filings, a dated amicus brief, a published ANPRM, a passive approval under a statutory mechanism Congress designed to operate without adversarial contestation. The distinction is between mechanism and output, not between evidence and absence of evidence. Both sequences produce the same capture-consistent output: adversarial truth discovery collapsed, career expertise bypassed, platform expansion proceeding under regulatory latency. Administrative law does not require courts to identify which mechanism produced a defective agency action. Courts assess whether the agency satisfied the conditions for deference. On that standard, the CFTC’s conduct is reviewable on its face.

MindCast: The Stigler Equilibrium: Regulatory Capture and the Structure of Free Markets does not require personal corruption to explain regulatory outcomes acquired by regulated interests. The CFTC’s passive approval of Kalshi’s self-certification, the withdrawal of the prior administration’s proposed rule, and the amicus brief asserting exclusive jurisdiction without completed definitional rulemaking all follow Stigler’s supply-and-demand model of regulation without requiring a single threatening phone call. Nash equilibrium logic explains why the CFTC institutional pattern stabilizes rather than self-corrects: once Kalshi accumulated $16.8 billion in annual sports volume and a $22 billion valuation, no regulatory actor deviates unilaterally from a position that acknowledging the error would require abandoning. Intent is not the standard. Coherence is the standard. The CFTC has not supplied it.

The Skrmetti Vector in prediction markets. The MindCast: A Tirole Phase Analysis of Advocacy-Driven Antitrust Inaction at the U.S. Department of Justice identified what MindCast calls the Skrmetti Vector — named for the pattern of state-level enforcement that operates independently of federal capture — as the mechanism through which distributed enforcers break federal capture-stable equilibria. The plain meaning: when enough state attorneys general file independent enforcement actions, they collectively apply more pressure than the federal settlement attractor can absorb, and the capture-stable equilibrium breaks. MindCast’s modeling established ten states as the threshold coalition density required for that break to occur. The prediction markets enforcement map has already crossed that threshold. Ohio AG Dave Yost’s multistate coalition — thirty-plus state AGs in the Amici States brief — exceeds the modeled breakage threshold. Washington AG Nick Brown’s March 28 King County complaint documents tribal compact harm with exhibit-level evidentiary specificity. April 16 tests whether that density is sufficient to force the equilibrium transition the Tirole framework predicts.

Access Arbitrage does not require a threatening phone call to produce capture-stable regulatory outcomes. The CFTC’s institutional sequence — passive approval, rule withdrawal, jurisdiction assertion without completed definition — runs the same Tirole Phase logic as the DOJ antitrust pattern. The mechanism differs. The equilibrium output is identical.

The Deference Defect: Coherence Over Character

The critical distinction between the DOJ and CFTC sequences — the presence or absence of a smoking gun — is legally irrelevant to the question of deference. Administrative law does not require proof of personal coercion to reject agency action. Administrative law requires that the decision reflect a reasoned judgment grounded in the record.

The DOJ pattern shows how capture manifests when observable through individual conduct. The CFTC pattern shows that the conditions for deference have failed because the agency’s litigation position and its rulemaking docket are in active, public conflict. The defect is procedural, not moral. Whether the institutional output stems from overt threats — as documented at the DOJ through Roger Alford’s sworn testimony — or structural latency — as documented at the CFTC through timestamped regulatory filings — the result is the same: the agency has bypassed the deliberative process that judicial deference presupposes. Under State Farm and Chenery, the court’s task is to assess the coherence of the output, not the character of the officials who produced it. The CFTC’s departure from the prior administration’s proposed rules without adequate explanation is separately reviewable under Encino Motorcars v. Navarro, 579 U.S. 211 (2016) — an agency that abandons established practice without reasoned justification acts arbitrarily regardless of the direction of the change. The Commission spent the prior administration building a rule that would have barred sports event contracts. It reversed that position without completing any rulemaking that explained the reversal. Encino Motorcars makes that unexplained departure an independent ground for denial of deference.

Most consequentially, Loper Bright Enterprises v. Raimondo, 603 U.S. 369 (2024), transforms the deference landscape entirely. The Ninth Circuit owes the CFTC’s swap classification interpretation no deference under Loper Bright. The Court held that courts must exercise independent judgment on questions of statutory interpretation rather than deferring to agency readings of ambiguous statutes. The CFTC’s claim that sports event contracts satisfy the swap definition in 7 U.S.C. § 1a(47)(A)(ii) is a statutory interpretation question. The panel decides it de novo. The practical consequence is that the CFTC’s litigation posture — asserting that its interpretation deserves deference — is legally unavailable after Loper Bright. The Commission’s amicus brief argues for a result the doctrine of deference no longer supports. The Ninth Circuit panel need not decide whether the Commission acted in bad faith. The panel exercises independent statutory judgment. The record of authority exercised before deliberation completed answers the coherence question before oral argument begins. Loper Bright answers the deference question before it is even raised.

Doctrinal Case Map

VII. The Collision Field: No Institution Controls All Three Dimensions

Jurisdictional overlap, political exposure, and financial feedback converge into a single operational environment. Regulatory actions influence market prices. Market prices influence political narratives. Political narratives drive further regulatory action. The loop closes and repeats. Congressional actors drafting the Schiff-Curtis bill observe market prices on the bill’s passage probability — prices listed on the same platforms they are legislating. CFTC officials asserting exclusive jurisdiction in federal court watch those courts’ dockets generate market contracts pricing the ruling’s probability. State attorneys general coordinating enforcement actions communicate through public filings that prediction market platforms immediately incorporate into probability estimates. No actor in the system observes from the outside. Every actor is simultaneously a participant in the loop and a target of its output.

The three dimensions of the collision field operate concurrently, not sequentially. Understanding each dimension independently — as Sections II through V establish — is the prerequisite. Understanding them operating simultaneously is what makes April 16 the event it is.

Dimension One: Jurisdictional

The CFTC asserts exclusive federal jurisdiction over Kalshi’s sports event contracts as swaps under 7 U.S.C. § 1a(47)(A)(ii). Nevada asserts gaming enforcement authority under state police power. Sixteen state enforcement actions across four appellate circuits assert the same. No court has yet issued a definitive ruling on which jurisdictional claim controls. Both exist simultaneously. Both generate legal obligations on the same platform for the same product. The jurisdictional dimension of the collision field does not resolve when one party files — it intensifies with each additional filing because every new enforcement action adds constraint geometry that compounds rather than cancels prior actions. The Ninth Circuit oral argument on April 16 does not eliminate that geometry. A ruling for either side routes the contest toward one of three trajectories, each of which preserves some version of the jurisdictional conflict in a different institutional forum.

The preemption architecture Kalshi constructed — self-certification under 17 C.F.R. § 40.2(a)(2), passive CFTC approval, the Big Lagoon collateral attack bar foreclosing state-by-state challenge — was designed to resolve the jurisdictional dimension in Kalshi’s favor before the states could organize a coherent response. The strategy worked until the enforcement density crossed the Skrmetti threshold. At that point the jurisdictional collision field stopped functioning as a mechanism for delay and started functioning as the primary constraint on every actor’s viable action set. No actor now exits the jurisdictional dimension voluntarily. The CFTC cannot withdraw its amicus brief without conceding the preemption theory. States cannot drop enforcement actions without conceding the field. Kalshi cannot accept state licensing without conceding the core legal argument. Every actor is locked into a position the jurisdictional collision field created before any of them chose it.

Dimension Two: Political

Prediction markets externalize political uncertainty into tradable prices. Every administration policy decision generates a contract. Every regulatory announcement moves a market. Every market movement becomes political intelligence. The Regulatory–Market Feedback Loop the executive branch is embedded in — documented in Section III — operates independently of any individual actor’s intent and independently of the legal question the Ninth Circuit is deciding. A ruling for Kalshi reprices SCOTUS certiorari probability contracts, Schiff-Curtis passage probability contracts, and Kalshi operational status contracts simultaneously. The executive branch observes all three price movements before deciding whether to signal on the ruling. The signal the executive branch sends in response then generates new contracts pricing the probability of executive intervention. The loop does not pause for legal deliberation.

Congressional actors face the same feedback structure from the opposite direction. Schiff-Curtis sponsors observe prediction market prices on their own bill’s passage probability. A ruling for the appellants raises the bill’s passage probability — the SCEM becomes urgent. A ruling for Nevada lowers it — the states have accomplished through judicial interpretation what the statute was designed to accomplish through legislative action. Either outcome feeds back into the political cost-benefit analysis the sponsors apply to every subsequent committee and floor decision. The political dimension of the collision field means no congressional actor can evaluate the Schiff-Curtis bill in isolation from the market price the bill itself generates. The legislation is simultaneously a proposed statute and a tradable contract on a platform the statute would regulate. No prior regulatory domain produced that structural condition.

Dimension Three: Financial

Kalshi’s $22 billion valuation and $16.8 billion in annual sports volume represent institutional facts accumulated inside the jurisdictional and political collision field before resolution arrived. Coinbase and Robinhood launched prediction market product lines while the litigation remained unresolved. Major League Baseball executed a memorandum of understanding with Kalshi while sixteen state enforcement actions remained active. Each institutional fact raises the cost of enforcement regardless of how the legal question resolves — not because the facts are legally dispositive, but because the financial feedback loop converts them into market prices that every actor observing those prices treats as evidence about the probable outcome.

The financial dimension of the collision field operates at higher speed than either the jurisdictional or political dimensions. A Ninth Circuit ruling generates capital market repricing within hours. State AG filings take weeks. Congressional markup takes months. Rulemaking takes years. The speed asymmetry means the financial dimension shapes the information environment in which the slower institutional dimensions operate. A sharp Kalshi valuation decline following a Trajectory B ruling reaches every investor, every distribution partner, and every congressional staff member reading financial news before any state AG has filed a follow-on enforcement action or any committee has scheduled a Schiff-Curtis markup. The financial feedback loop does not just reflect institutional outcomes — it generates the information environment that shapes the next round of institutional decisions.

Why No Single Actor Controls the System

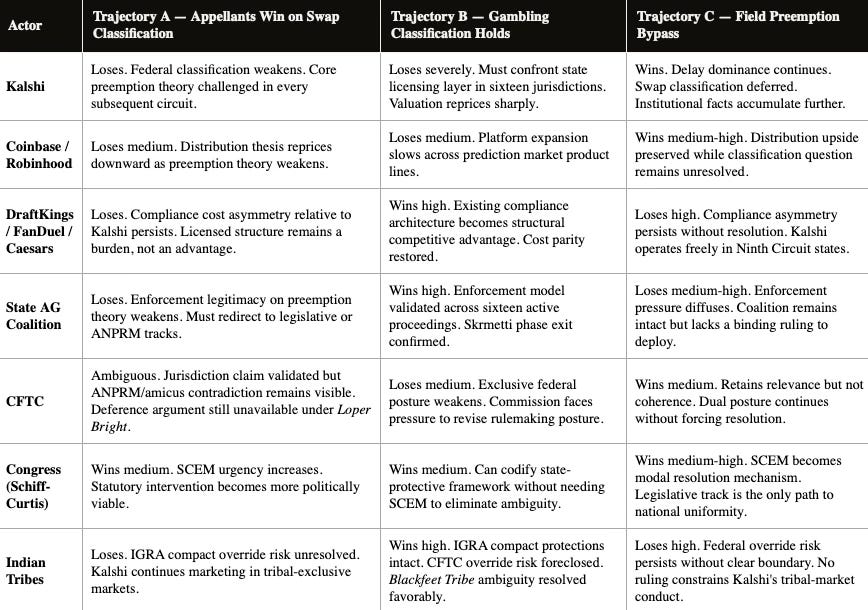

Control in a collision field requires simultaneous command of all three dimensions. No actor in the prediction markets system holds that position. The CFTC controls the jurisdictional dimension partially — its amicus brief and passive self-certification approval shaped the legal architecture — but cannot control the political dimension it is embedded in or the financial feedback loop it observes without governing. Kalshi controls the financial dimension partially — its $22 billion valuation and distribution partnerships accumulated institutional facts that raise enforcement costs — but cannot control the state AG coalition that crossed the Skrmetti threshold or the congressional actors whose Schiff-Curtis bill can eliminate the statutory ambiguity Kalshi’s entire architecture depends on. State AGs control the enforcement density dimension — thirty-plus coalition members have crossed the phase exit threshold — but cannot control the Ninth Circuit panel’s doctrinal preferences or the financial markets repricing the outcome before the opinion issues.

Increased participation does not resolve the tension. A prediction market with $16.8 billion in annual sports volume alone — before election, political, and economic contracts are counted — creates a conflict whose resolution requires Supreme Court intervention, statutory amendment, or executive branch coordination that no single actor controls. The Washington AG complaint, the Ohio AG-led multistate coalition, the Schiff-Curtis bill, the CFTC’s ANPRM, and the Ninth Circuit consolidated docket all activated within a single 90-day window. April 16 functions as a forcing event precisely because every actor recognized that delay dominance was compressing and moved to establish position before the appellate signal updated the system’s probability distribution. The collision field does not resolve at April 16. April 16 is the first moment at which the collision field becomes measurable — the first date on which the system can be scored.

VIII. Constituency Impact: What the Conflict Architecture Does to Each Actor

The conflict architecture does not distribute its consequences evenly. Five constituencies occupy structurally distinct positions inside the system. Each gains a different analytical instrument from this framework. Each faces different decisions before and after the April 16 appellate signal arrives.

States suing Kalshi. The Tirole Phase comparative framework gives state AG offices a published model characterizing the Commission’s passive approval and jurisdiction assertion as capture-stable institutional behavior rather than considered regulatory judgment — the standard deference doctrine requires. An agency in the Tirole Advocacy Arbitrage Phase has not exercised the deliberate institutional judgment that deference presupposes.

The Skrmetti Vector analysis converts the thirty-plus-state amicus coalition from a headcount into a structural claim: the distributed enforcer density required to break a federal Nash-Stigler equilibrium is present. States still need to win on the clearinghouse distinction in the Ninth Circuit — the Tirole analysis is a structural argument about the CFTC’s institutional conduct, not a statutory argument about swap classification.

What the framework supplies is the argument that the CFTC amicus brief deserves no deference at all. Under Motor Vehicle Manufacturers Association v. State Farm, the Commission’s amicus position cannot receive deference as long as the ANPRM remains open — the agency has asserted a final jurisdictional answer while its own rulemaking record affirmatively invites contradiction of that answer. Under Loper Bright Enterprises v. Raimondo, 603 U.S. 369 (2024), the Commission’s swap classification interpretation receives no deference regardless — the Ninth Circuit decides the statutory question independently. Under Gregory v. Ashcroft, 501 U.S. 452 (1991), federal preemption of traditional state police power functions requires a clear congressional statement. Gaming regulation is a traditional state function. The CEA’s self-certification mechanism is not that clear statement.

State AGs submitting comments to the ANPRM docket before April 30 can deploy all three standards simultaneously: the Commission has no considered judgment to defer to while the definitional process remains incomplete, no interpretive deference to claim under Loper Bright, and no clear preemption statement to invoke under Gregory. None of those arguments requires states to win on the merits of swap classification.

Resorts and casinos. The licensed gaming industry — DraftKings, FanDuel, Caesars, MGM, the Nevada casino infrastructure — holds a direct financial stake in Trajectory B, where sports event contracts are classified as gambling subject to state licensing requirements. Kalshi processed $16.8 billion in sports volume while carrying no state licensing overhead, no problem gambling compliance costs, and no tribal compact obligations. Nevada’s sports betting handle fell 9% in the same year. Kalshi’s structural cost advantage is not a product of superior technology — it is the direct output of regulatory latency.

MindCast: A Tirole Phase Analysis of Advocacy-Driven Antitrust Inaction at the U.S. Department of Justice calculated Access Arbitrage consumer harm at $37.5–$47 billion in the antitrust domain.

Applied to prediction markets, the compliance cost asymmetry between Kalshi and licensed operators is the measurable output of institutional capture, directly deployable in CFTC ANPRM comment submissions, state legislative testimony, and amicus briefs in circuits where the swap classification question remains open. Trajectory C — field preemption bypass without swap classification — is the worst structural outcome for licensed gaming: Kalshi continues operating in Ninth Circuit states under federal preemption with the classification question deferred, extending the period during which the cost asymmetry compounds.

Indian tribes. Tribal sovereignty analysis carries the most direct and underappreciated impact of any constituency-specific contribution here. Running the CFTC’s institutional sequence through the Tirole framework reaches a conclusion the appellate record has not yet articulated — and one that is significantly harder for the federal government to defend against a sovereign entity than against a private party. Federal agencies override tribal compact rights when Congress clearly authorizes it or when the agency exercises deliberate considered judgment that the override serves a legitimate federal interest.

The Premature Authority argument strips that second ground from the CFTC entirely: an agency that approved through inaction under a self-certification mechanism, withdrew its predecessor’s proposed definitional rules, and simultaneously opened a public docket to determine what its jurisdiction covers has not exercised the deliberate considered judgment the override standard requires. Under Chenery, the court evaluates the quality of the agency’s reasoning at the time of the action.

At the time the CFTC’s amicus brief was filed, the agency’s own rulemaking record was affirmatively soliciting the public’s help in determining what the Commission’s authority covers. No deliberate judgment was complete. No override was authorized. Montana v. Blackfeet Tribe, 471 U.S. 759 (1985), compounds the tribal position: statutes are construed in favor of Indian tribes when the statutory language is ambiguous. The CEA’s exclusive jurisdiction provision does not explicitly address whether it displaces IGRA compact rights. Ambiguity on that question resolves in the tribes’ favor under Blackfeet Tribe — and under Loper Bright, the Ninth Circuit decides that ambiguity independently rather than deferring to the CFTC’s self-serving interpretation. The combination of Blackfeet Tribe, Chenery, and Loper Bright gives tribal attorneys a three-layer sovereign-specific argument for denying CFTC deference that does not require prevailing on the swap classification question at all.

The Washington AG complaint’s Kalshi advertisement exhibit — “found a way to bet on the NFL even though we live in Washington” — converts from a consumer protection violation into systemic evidence: a federally licensed platform used one federal statutory framework to extract revenue from markets a second federal statutory framework — IGRA — had reserved for tribal sovereign economic development, under the cover of an agency authority claim that was incomplete when it was made.

Investors. Three repricing positions activate simultaneously when the April 16 signal arrives. Kalshi’s $22 billion valuation was built inside the gap between claimed CFTC authority and completed definitional rulemaking. An agency in the Tirole Advocacy Arbitrage Phase does not provide durable regulatory shelter — it provides latency. When the latency compresses through appellate ruling, SCEM activation, or completed rulemaking, the valuation built on regulatory ambiguity reprices.

Coinbase and Robinhood carry indirect exposure to the Ninth Circuit swap classification outcome without the explicit position disclosure that direct Kalshi investors hold. DraftKings, FanDuel, and Caesars hold the inverse position: Trajectory B restores cost parity and reprices licensed sportsbook operators upward relative to Kalshi. For arbitrage desks holding positions on the Ninth Circuit outcome, Prediction 0’s Tirole Phase Exit Test supplies the falsification conditions that define the trade: the thirty-plus-state coalition has crossed the Skrmetti threshold, and an adverse ruling for the appellants produces a structural transition — not a temporary market reaction — that does not reverse when the news cycle moves on.

The CFTC. Placing the Commission’s own conduct inside the same five-primitive capture framework that the DOJ antitrust pattern satisfies with sworn deposition support is the most institutionally consequential output of this analysis. No named CFTC official faces personal accountability claims. Institutional conduct following the Tirole capture pattern produces capture-stable regulatory outcomes without requiring individual bad actors — making the structural argument more durable than a personal one.

Chairman Selig’s “rational and coherent” language — publicly characterizing his predecessor’s approach as irrational — documents internal CFTC disagreement visible in the appellate record. The Ninth Circuit panel can read that language alongside the Tirole framing and conclude that the Commission’s litigation posture does not represent the institutional deliberation that deference doctrine requires — without characterizing the Commission’s conduct as corrupt or bad-faith. The structural capture pattern is sufficient. The Commission’s path out of the Tirole capture framework runs through the ANPRM, not through the Ninth Circuit.

Completing the definitional rulemaking before the appellate ruling arrives — or immediately after — is the only institutional action that documents the considered regulatory judgment deference doctrine requires and restores the Commission’s credibility as an independent regulatory authority rather than a capture-stable apparatus defending a platform it approved through inaction.

IX. Cognitive Digital Twin Foresight Simulation and Predictions

A Cognitive Digital Twin (CDT) models an institution, market, or actor as a decision-making system under constraints, incentives, and feedback. Instead of describing what an institution says, a CDT simulates how it behaves—tracking how signals, pressures, and internal logic produce actions over time. A CDT treats courts, agencies, firms, and markets as adaptive systems with memory, latency, and strategic responses.

The MAP CDT (MindCast AI Proprietary Cognitive Digital Twin Foresight Simulation) is the operational engine that runs those simulations. It ingests signals, filters them through causal inference and trust validation, routes them across specialized Vision Functions (strategy, regulation, feedback, etc.), and outputs structured foresight with probabilities, triggers, and falsification conditions. Where a CDT defines the model, MAP CDT executes it—turning real-world signals into predictive simulations of how the system will move next.

A formal MindCast CDT foresight simulation of the system confirms that regulatory conflict in prediction markets operates as a closed-loop control architecture rather than a coordination failure. MAP CDT — the modeling framework that treats institutions, regulators, and markets as interacting systems — routes the dominant causal pathway not through legal doctrine but through signal interaction: regulatory assertion → market pricing → political response → regulatory update. Institutional contradictions — jurisdiction asserted before definition completed, rulemaking opened while litigation posture asserts completeness — are not system noise. They are signals of incomplete control. The CDT does not predict what actors intend. It predicts what the system’s structure makes likely regardless of intent.

System Equation. Before the simulation outputs, the conflict’s stability can be expressed as a single function:

Conflict Stability ≈ (Jurisdictional Overlap × Feedback Speed × Financial Exposure) / Resolution Capacity

Jurisdictional overlap spans sixteen active state enforcement proceedings and four appellate circuits. Feedback speed is confirmed by the 90-day window in which the Washington AG complaint, the Ohio AG coalition, the Schiff-Curtis bill, the CFTC ANPRM, and the Ninth Circuit consolidated docket all activated simultaneously. Financial exposure stands at $16.8 billion in annual sports volume and $22 billion in platform valuation. Resolution capacity remains low: the CFTC’s definitional rulemaking is incomplete, the appellate circuit split is unresolved, and the legislative track has not yet reached committee markup. Conflict stability is therefore high. April 16 is the first event that materially compresses any numerator term or expands the denominator.

System Routing (MAP CDT Flow Output). The system’s strengths are its signal density and feedback speed: multiple institutions continuously generate observable actions, markets translate legal and political signals into prices immediately, and state actors increase enforcement pressure without requiring central coordination. The system’s binding constraints are equally structural: no single actor can terminate the feedback loop, legal resolution lags behind market adaptation, and institutional credibility degrades under visible inconsistency. The CFTC’s simultaneous amicus brief and ANPRM is the clearest expression of the third constraint operating in real time — visible inconsistency the Ninth Circuit panel reads from the caption page before a question is asked.

Feedback Control (Cybernetic Control Vision). The system is transitioning from semi-closed to closed-loop control. Feedback capture rate is highest at the platform level — Kalshi and its distribution partners adapt faster than any regulatory actor in the system. Adaptation velocity is highest in markets, slower in agencies. Feedback latency is compressing due to real-time pricing. The practical consequence is that regulatory actors have become reactive rather than directive: markets now act as control surfaces rather than passive indicators. When the CFTC asserts exclusive jurisdiction, prediction market platforms immediately list contracts pricing the probability that the assertion holds. The agency is no longer shaping the information environment. The information environment is shaping the agency’s next move.

Causal Integrity (Causation Vision). The DOJ and CFTC sequences share a common structural signature across three observable dimensions: authority exercised before deliberation completed, adversarial process weakened or bypassed, and institutional output favoring regulated entity expansion. Causal Signal Integrity is high. The similarity between the two sequences is not superficial or analogical — it reflects a shared causal architecture operating under different mechanisms. Strong explanatory coherence across domains increases predictive validity: when institutional patterns repeat across agencies, the structural conditions producing them are more likely to persist than the specific actors who instantiate them. If courts reassert adversarial control through the Ninth Circuit ruling, the CDT model updates accordingly.

Strategic Interaction (Chicago Strategic Game Theory). The system is currently delay-dominant but approaching a transition threshold. Platforms benefit from time extension. Agencies maintain optionality through incomplete rulemaking. States increase pressure but lack immediate termination power. Delay dominance is weakening as enforcement density increases and appellate review compresses timelines. April 16 is the compression event: the consolidated oral argument forces simultaneous updating across every actor, reducing the latency resource that delay dominance depends on. Strategic flexibility is highest for all actors before the ruling. After it, the corridor narrows.

Regime Classification: Labyrinth Moving Toward Trap. High constraint across legal, political, and financial dimensions combined with high latency across multi-forum litigation produces a narrowing corridor of viable actions. Future outcomes will be driven less by actor preference and more by structural constraint. The actors with the most flexibility before April 16 are the state AG coalition — which has already crossed the Skrmetti threshold — and the CFTC itself, which retains the ability to complete its definitional rulemaking and exit the capture-consistent posture before the appellate ruling forces external resolution. After April 16, the corridor narrows. The Trap closes when the appellate signal, the SCEM legislative track, and financial repricing across three market positions activate within overlapping time windows.

Foresight Predictions

The simulation generates six falsifiable predictions tied to named actors and event-linked triggers already in motion. The post-April 16 scoring publication will assess each against observed outcomes.

Prediction 0 — Tirole Phase Exit Test. The Skrmetti Vector has already crossed the ten-state threshold. April 16 tests whether appellate signal from a thirty-plus-state coalition produces phase exit — a transition from capture-stable equilibrium to adversarial contestation — or whether the CFTC’s institutional preemption posture absorbs the state coalition’s signal without updating.

P10 (Trajectory A — appellants win, phase continues): preemption holds, state coalition absorbs ruling without escalation, ANPRM proceeds as industry codification exercise. P50 (Trajectory C — field preemption bypass): Kalshi continues operating, swap classification deferred, SCEM becomes modal resolution mechanism, phase exit delayed 12–18 months. P90 (Trajectory B — states win on swap classification): phase exit triggered within 45 days, multistate coordination activates, capital markets reprice across all three positions. Trigger window: 90 days from April 16 ruling. Falsification: Ninth Circuit rules for appellants, multistate coalition files no further coordinated action within 60 days, CFTC issues no revised rulemaking guidance by June 30.

Prediction 1 — CFTC Dual Position Resolution. Chairman Selig cannot simultaneously assert exclusive jurisdiction in the Ninth Circuit and maintain an open public comment docket on how to define the instruments subject to that jurisdiction past the April 30 deadline without one of the two institutional postures requiring explicit revision.

P10: Commission issues a Notice of Proposed Rulemaking — NPRM — within 60 days of April 30, formally completing the definitional step the amicus posture required. P50: Comment period closes, Commission issues no NPRM within 60 days, but modifies its litigation posture following the ruling to acknowledge the definitional gap. P90: Both tracks continue operating independently past June 30 with no institutional revision to either. Trigger window: 60 days from April 30. Falsification: ANPRM closes and Commission maintains appellate preemption claim without revision through June 30.

Prediction 2 — White House Signal Sensitivity. Executive branch signaling intensifies during the 30-day window following the April 16 ruling as prediction market prices on the ruling’s downstream consequences — Supreme Court certiorari probability, Schiff-Curtis passage probability, Kalshi operational status — feed back through the Regulatory–Market Feedback Loop into the political cost-benefit analysis executive principals apply to their next regulatory moves.

P10: Executive branch issues a public statement supporting Kalshi’s preemption position within 30 days of ruling. P50: CFTC receives informal White House guidance on rulemaking timeline following ruling. P90: No observable executive branch signaling within 45 days. Trigger window: 45 days from ruling. Falsification: No executive branch statement, regulatory action, or personnel decision affecting prediction market governance within 45 days of the ruling.

Prediction 3 — Additional State Enforcement Filings. State enforcement actions emerge within a near-term window as state AGs in Ninth Circuit jurisdiction — Washington, Oregon, California, Arizona — move to establish position before the appellate ruling forecloses or validates the preemption architecture. A ruling adverse to the appellants activates the Ohio AG-led coordination mechanism within 30 days.

P10: Two or more Ninth Circuit state AGs file within 30 days of a Trajectory B ruling. P50: One Ninth Circuit state AG files or joins the Ohio coalition within 45 days of any ruling. P90: No additional filings within 45 days. Trigger window: 45 days from ruling. Falsification: No additional state enforcement action or coordinated multistate filing within 45 days of the ruling.

Prediction 4 — Schiff-Curtis SCEM Activation. A Trajectory A outcome accelerates the Schiff-Curtis timeline by eliminating the statutory ambiguity the preemption theory depends on. A Trajectory C outcome — field preemption bypass without swap classification — makes the SCEM the only remaining mechanism capable of forcing the classification question to resolution without Supreme Court intervention.

P10: Schiff-Curtis receives committee markup within 60 days of a Trajectory A ruling. P50: Schiff-Curtis receives Senate floor consideration within 90 days of a Trajectory C ruling. P90: No committee or floor action within 90 days regardless of trajectory. Trigger window: 90 days from ruling. Falsification: Schiff-Curtis receives no committee markup or floor consideration within 90 days of the ruling regardless of trajectory outcome.

Prediction 5 — Financial Market Repricing Across Three Positions. Coinbase and Robinhood reprice based on whether federal preemption holds. DraftKings, FanDuel, and Caesars reprice based on whether their compliance cost structure relative to Kalshi is validated or compressed. Regulatory arbitrage trades open or close depending on which trajectory activates.

P10: All three positions reprice materially within 45 days of a Trajectory B ruling. P50: At least two of three positions reprice within 45 days of any ruling. P90: No measurable repricing across any position within 45 days. Trigger window: 45 days from ruling. Falsification: No measurable capital market repricing across any of the three identified positions within 45 days of the ruling.

Actor Probability Bands by Prediction

State Enforcement Acceleration (State AGs: WA, OH coalition, CA, NY). P80 within 30–45 days: additional filings or coordinated actions post-ruling. P60 within 15–30 days: pre-positioning filings in Ninth Circuit states — Washington, California, Oregon, Arizona. P20: no coordinated follow-on activity. Trigger: Ninth Circuit ruling across any trajectory. Falsifier: no new filings or coalition action within 45 days of the ruling.

CFTC Internal Resolution (Chairman Selig, Litigation Division). P75 within 30–60 days: movement from ANPRM to NPRM or explicit definitional guidance. P50 within 15–30 days: partial signaling through public statements or docket updates. P25: continued dual posture — litigation plus open definition loop — beyond 60 days. Trigger: April 30 comment deadline combined with appellate outcome. Falsifier: no rulemaking or definitional clarification within 60 days.

Executive Signal Response (White House, Executive Branch). P70 within 15–30 days: public or indirect signaling tied to market reactions — policy framing, personnel messaging. P40 within 30–45 days: informal agency coordination without direct statement. P15: no observable response. Trigger: market repricing of ruling implications through policy probability contracts on prediction platforms. Falsifier: no executive-linked signal within 45 days.

Financial Repricing (Kalshi, Coinbase, Robinhood, DraftKings, FanDuel, Caesars). P85 within 0–30 days: immediate repricing across at least two categories — prediction platforms and gaming incumbents. P60 within 30–45 days: secondary repricing as regulatory clarity evolves. P10: no measurable repricing. Trigger: appellate ruling combined with liquidity response. Falsifier: no capital or pricing movement within 45 days.

Legislative Activation (Schiff-Curtis Sponsors, Committees). P65 within 45–90 days: committee action, markup, or formal advancement tied to ruling trajectory. P35 within 30–60 days: increased signaling without formal movement. P20: legislative inactivity. Trigger: ruling that clarifies or destabilizes classification ambiguity. Falsifier: no legislative movement within 90 days.

Positioning Map: Who Benefits Under Each Trajectory

Time Compression Curve: Latency Collapse Post-April 16

The system’s dominant resource before April 16 is time. Kalshi, the CFTC, and distribution partners benefit from delay while state enforcers and licensed incumbents benefit from compression. April 16 reduces the amount of time each actor has to preserve ambiguity. The compression runs in five phases.

Pre-Argument (now through April 15). The system is delay-dominant and optionality is preserved. Kalshi, the CFTC, and distribution partners — Coinbase, Robinhood — are the primary beneficiaries. States, tribes, and gaming incumbents bear the cost of continued latency.

Synchronization Event (April 16). The oral argument forces simultaneous updating across all actors. No single actor holds a durable advantage at the moment of signal generation. All actors face repricing risk simultaneously — which is what makes April 16 a synchronization event rather than a resolution event.

Immediate Compression (0–15 days after ruling). Narrative and market repricing outrun formal regulatory response. Fast-moving market actors — arbitrage desks, platform operators, institutional holders of exchange exposure — update before agencies can respond. Slow-moving agencies lose the ability to shape the post-ruling information environment.

Institutional Compression (15–45 days after ruling). AG filings, executive signaling, and platform repositioning intensify. Actors with prepared playbooks — state AG coalitions, licensed gaming operators with ANPRM submissions ready, tribal attorneys with supplemental authority letters drafted — benefit. Actors dependent on continued ambiguity lose the latency resource they were operating on.

Structural Repricing (45–90 days after ruling). Legislative, rulemaking, and valuation effects become visible. Winners and losers depend on which trajectory activated. Actors mispositioned before the ruling — investors holding Kalshi exposure at $22 billion under the assumption that preemption was durable shelter, or licensed gaming operators who did not submit ANPRM comments — face the largest adjustment costs.

April 16 does not merely produce a legal result. April 16 collapses latency. Actors who relied on regulatory ambiguity lose the ability to stretch time at the same rate after the signal arrives.

CDT Scorecard

System Control: semi-closed loop moving toward closed — feedback dominance increasing — dominant actor: platforms (Kalshi and distribution partners) — risk level: High.

Regulatory Coherence: fragmented, compressing under pressure — dominant actor: CFTC — risk level: High.

Strategic Regime: Labyrinth moving toward Trap, options narrowing — dominant actor: courts (Ninth Circuit) — risk level: High.

Feedback Capture: uneven, consolidating toward markets — dominant actor: markets — risk level: High.

Enforcement Density: rising and accelerating — dominant actor: state AG coalition — risk level: Medium-High.

X. Extended Foresight Predictions: Second and Third-Order Effects

The predictions in Section IX measure immediate reactions to the April 16 appellate signal. The extended set below measures whether the system itself is changing form. If these predictions validate, the implication is not that prediction markets are being regulated. The implication is that governance is adapting to feedback-driven financial systems across domains — and that the conflict architecture this paper maps is the template, not the exception.

Second-Order Institutional Predictions

Prediction 6 — Judicial Behavior Shift Across Circuits. Written opinions from the Ninth Circuit generate cross-circuit citation uptake as parallel cases in the Third and Fourth Circuits addressing identical statutory text reference the Ninth Circuit’s reasoning. Doctrinal divergence between circuits increases the probability of a Supreme Court certiorari grant.

P70 within 60–120 days: other circuits begin referencing Ninth Circuit reasoning in parallel proceedings. P40 within 90–150 days: divergent reasoning emerges, deepening the circuit split. P20: minimal cross-circuit uptake. Trigger: written opinion publication and citation adoption in pending Third and Fourth Circuit appeals. Falsifier: no citation or doctrinal uptake in other circuits within 120 days of opinion publication.

Prediction 7 — CFTC Internal Fragmentation. Post-ruling pressure combined with the April 30 ANPRM comment deadline forces observable divergence inside the Commission between commissioners, between the litigation division and the rulemaking division, or between career staff and political appointees. Chairman Selig’s “rational and coherent” signal — publicly characterizing the prior administration’s approach as irrational — has already documented an internal disagreement visible in the appellate record. Post-ruling pressure intensifies that fault line.

P65 within 30–90 days: public or observable divergence between commissioners or internal divisions. P45 within 60–120 days: staff-level leaks or indirect signaling of disagreement through public statements or docket filings. P25: unified institutional posture maintained. Trigger: ruling combined with ANPRM closure on April 30. Falsifier: no observable divergence in statements or institutional actions within 90 days.

Market Structure Predictions