MCAI Lex Vision: The Ninth Circuit on April 16 as System Convergence — The First Measurable Test of Prediction Market Structure

The Ninth Circuit Argument That Will Decide Trajectory Whether Prediction Markets Are Sports Betting or Financial Instruments

Related publications: Kalshi Is Crypto’s Test Case | Kalshi’s Prediction Market Litigation Architecture, the CFTC Amicus, and the Strategic Framework for State Enforcement | The National Kalshi Prediction Market Litigation Map | The Full Arc of Prediction Markets | Prediction Markets and the Regulatory Split | Prediction Markets— Legislative Regime Conversion and the Collapse of Preemption | Kalshi Found the One Gap in American Gaming Law Nobody Closed | The Ninth Circuit on April 16 as System Convergence — The First Measurable Test of Prediction Market Structure | Kalshi, Prediction Markets and the Conflict Architecture of Regulation

Executive Summary

April 16 marks the first synchronized test of prediction markets as cybernetic systems governed by jurisdiction, constraint geometry, and feedback latency rather than participant rationality. Cybernetics — the study of how systems self-regulate through feedback loops — provides a more accurate model for prediction markets than classical economics, because the outcomes these markets price are increasingly shaped by the regulatory and political forces those markets were designed to measure. On that date, the Ninth Circuit Court of Appeals hears consolidated oral arguments in KalshiEX, LLC v. Assad, et al., No. 25-7516, consolidated with Nos. 25-7187 and 25-7831 — federal prediction market platforms asserting that the Commodity Exchange Act (CEA) preempts Nevada’s gaming enforcement authority. Prior MindCast publications established each structural layer of that contest independently. April 16 compresses those layers into a single observable event.

Federal preemption is the constitutional doctrine that federal law supersedes state law when Congress has granted a federal agency exclusive regulatory authority over a domain. The panel faces not one preemption question but three sequential theories, each independently sufficient to resolve the consolidated appeal. Express preemption under § 2(a)(1)(A) asks whether the Commodity Futures Trading Commission (CFTC)’s statutory grant of “exclusive jurisdiction” over designated contract market (DCM) trading forecloses state regulation entirely. Swap classification under § 1a(47)(A)(ii) asks whether sports-event contracts satisfy the statutory definition of “swap” — the question on which the active circuit split sits. Field preemption asks whether the CEA’s comprehensive regulatory scheme displaces state law as applied to all DCM trading, regardless of whether the contracts at issue are swaps or something else. A fourth backstop argument holds that sports-event contracts qualify as options under § 1a(36) even if they are not swaps, reaching the same CFTC exclusive jurisdiction result through an independent statutory path. Where the panel’s questions land during the 45-minute appellant argument reveals which theory the court treats as controlling — and which resolution pathway the system will take.

The federal government is not a background presence in the April 16 proceeding. Martin Jordan Minot, Deputy General Counsel for Litigation at the CFTC, will argue in person in Courtroom 1 with six minutes of allocated oral argument time. The Commission that is supposed to regulate Kalshi filed an amicus brief asserting that state enforcement of gaming laws against federally designated contract markets would, in the CFTC’s own words entered in the appellate record, reintroduce precisely the regulatory fragmentation Congress deliberately displaced and create a seismic shift in the longstanding status quo between CFTC and state authority. A federal agency standing beside a platform it regulates and arguing against the states trying to enforce their own law is not a regulatory posture. The Commission chose to be a named participant in an adversarial proceeding against state law enforcement.

Simultaneously, the Commission has opened a public comment docket to determine what rules should govern the very instruments it claims exclusive authority over. The system asserts jurisdiction before completing rule definition, creating a control gap between authority and implementation that Kalshi’s expansion strategy occupied from January 2025 forward. A regulatory agency cannot assert preemption of state authority over a product category and simultaneously issue an advance notice of proposed rulemaking asking the public to help it determine how that category should be defined. The structural contradiction is not hypocrisy — it is the institutional signature of a control gap.

Ten institutional amici filed supporting Nevada. Four filed supporting the appellants. States hold the enforcement capacity and the harm surface. The CFTC holds jurisdiction and abstraction. Kalshi exploits the gap between them. The amicus count is not a headcount. It is the institutional map of a conflict between federal regulatory architecture and state enforcement reality — and that conflict is what April 16 compresses into a single observable signal. The panel does not choose among theories freely. Appellate courts select the narrowest ground that resolves the case without triggering system-wide consequences they cannot control, which makes the field preemption pathway structurally attractive if the panel seeks to avoid deepening the circuit split.

Between January and March 2026, MindCast published eight analytical papers mapping the Kalshi prediction market litigation from its structural origins through the April 16 hearing. Each paper established a distinct layer of the analytical architecture this publication deploys. Readers new to the litigation can treat the corpus stack below as a reading guide; readers familiar with the series will find each entry annotated with its specific relevance to April 16.

Who Should Read This and Why

This publication serves six distinct audiences. Each section below identifies what the document delivers for that reader and which sections are most directly relevant.

State Attorneys General and Enforcement Staff. The April 16 oral argument is the primary coordination signal for the next phase of multistate enforcement. Section III maps the full amicus alignment and identifies the Ohio AG-led coalition’s coordination mechanism. Section IV documents the four poaching mechanisms and the revenue displacement data that support harm-surface arguments. Prediction 3 specifies the 30-day coordination window and the confirmation condition for tightening constraint geometry. The trajectory table identifies what a Trajectory B outcome means for enforcement actions already filed. Attorneys general in Ninth Circuit jurisdictions — Washington, Nevada, Arizona, Oregon, California — face the most time-sensitive decisions following the ruling.

Capital Markets, Funds, and Institutional Investors. The document maps the market reaction pathway across three positions: exchanges with prediction market exposure (Coinbase, Robinhood), licensed sportsbook operators (DraftKings, FanDuel, Caesars), and regulatory arbitrage trades that open or close depending on which trajectory activates. Section II’s PRGA analysis converts Kalshi’s voluntary March 2026 behavioral concession into a private probability signal accessible through behavioral inference. Prediction 4 specifies the convergence acceleration confirmation conditions. The trajectory table maps valuation consequences across all three outcomes within the 45-day window following the ruling. The SCOTUS textualism analysis in Section VI establishes the medium-term legal trajectory that capital allocation decisions must account for.

Congressional Staff and Policy Counsel. The Schiff-Curtis Prediction Markets Are Gambling Act entered the appellate record as contemporaneous legislative history before April 16. Section IV explains the SCEM mechanism and why a statutory CEA amendment eliminates the contested jurisdictional space rather than operating within it. Prediction 2 specifies the ANPRM comment deadline of April 30 — fourteen days after oral argument — as the next institutional synchronization point regardless of how the panel rules. Trajectory C is the outcome that makes the legislative track the modal resolution mechanism. Section VI’s uniformity-sovereignty fault line analysis frames the policy choice Congress must eventually resolve.

Tribal Gaming Attorneys and Sovereign Interests. Section III identifies the structural consequence of the preemption theory that no court has yet addressed directly: a ruling validating Kalshi’s conduct establishes that the CEA’s exclusive jurisdiction provision operates as a federal override of federally negotiated tribal compact rights. The tribal sovereignty analysis identifies how the conflict introduces a second federal layer — IGRA compact rights — that the CEA does not explicitly address, increasing the probability that any appellate resolution produces downstream conflict rather than closure. The Washington AG complaint exhibit documenting Kalshi’s NFL advertising in tribal-exclusive markets is analyzed in Section III. Trajectory B is the outcome most protective of existing tribal compact structures. Trajectory A creates the most acute structural risk for tribal exclusivity rights.

Appellate Clerks and Legal Press. Section VI compresses the entire litigation to its controlling question: whether sports-event contracts satisfy the swap definition under 7 U.S.C. § 1a(47)(A)(ii). The three-layer preemption architecture in Section V establishes why the panel’s question choices during argument reveal which resolution pathway the court is considering. The judicial constraint line — appellate courts favor the narrowest ground that resolves the case without triggering system-wide consequences they cannot control — explains why field preemption is the structurally preferred pathway for a panel seeking to avoid deepening the circuit split. The Big Lagoon analysis establishes the jurisdiction-versus-substance distinction: if the panel accepts the collateral attack bar, the court is not deciding whether the contracts are lawful — it is deciding who has the authority to decide.

CFTC Rulemaking Staff and Public Comment Participants. The ANPRM comment period closes April 30, 2026 — fourteen days after the oral argument that will generate the clearest available signal about how courts are reading the swap definition the ANPRM is designed to clarify. Section IV documents the control gap between the Commission’s exclusive jurisdiction claim and its simultaneous request for public input on how to define the instruments it claims jurisdiction over. Chairman Selig’s “rational and coherent interpretation” language signals an internal CFTC disagreement about what the statute means that the rulemaking must resolve. MindCast will file a public comment between April 17 and April 25, deploying the CDT foresight simulation framework and the SCEM analytical architecture as input to the Commission’s definitional process. The CDT foresight simulation’s P45/P35/P20 probability assignments and the five falsifiable predictions in Section VIII provide the analytical infrastructure for comment submissions that go beyond legal argument into predictive institutional modeling.

Core Insight

Prediction markets no longer operate as neutral aggregation mechanisms. Market outcomes increasingly reflect regulatory timing, jurisdictional positioning, and feedback delay. April 16 provides the first observable convergence point where those forces operate simultaneously — and the ruling binds the prediction market industry, not just the three platforms on the docket. If the Ninth Circuit accepts the clearinghouse-based swap classification, federal jurisdiction expands and the legislative track accelerates as the industry moves to lock in the ruling before Congress can close the statutory gap. If the panel rejects that boundary, state enforcement becomes the dominant control layer, the preemption architecture collapses across sixteen active proceedings, and the Supreme Court certiorari pathway becomes the only viable path to a federal resolution.

I. Prediction Markets Have Shifted from Information Systems to Control Systems

The Full Arc of Prediction Markets establishes the foundational two-kind taxonomy that governs every structural analysis in the corpus. Public belief exchanges — Kalshi, Polymarket, PredictIt — offer open-participation binary contracts on discrete outcomes, with prices functioning as publicly broadcast probability estimates. Proprietary probability engines — SIG, Jane Street, Citadel — run continuous probability models on the same events, trade election-linked instruments across options and volatility surfaces, generate zero regulatory scrutiny, and make no public epistemic claim. The entire regulatory controversy attaches to the first kind because it exposes retail participants, makes a public epistemic claim requiring regulatory classification, and presents a classifiable surface to frameworks built around public interface and retail protection. Understanding that distinction is the entry condition for understanding why April 16 is the event it is.

Prediction markets originated as mechanisms for aggregating dispersed information into probabilistic forecasts. The original academic framing emphasized rationality, incentive alignment, and error correction through participation. Early literature treated the market format as epistemically neutral — a mechanism for surfacing distributed private information, not a mechanism for shaping it. Early literature assumed relatively stable rule sets, low friction between signal generation and outcome realization, and participant populations motivated primarily by accuracy rather than narrative position.

Current market conditions diverge sharply from every one of those assumptions. Platform operators actively shape participation conditions through product design, marketing strategy, and contract selection. Regulatory fragmentation introduces multiple overlapping rule regimes that alter platform behavior regardless of participant intent. Feedback loops between regulation, media narrative, and product design alter both input quality and output interpretation — a prediction market price does not measure an independent probability when the actors most capable of influencing the outcome are simultaneously holding positions in the market pricing it.

Prediction Markets Reveal Truth — Feedback Loops Determine It operationalizes three diagnostic instruments that separate genuine structural shifts from advocacy noise and news cycle distortion: the Feedback Latency Index, which measures the delay between signal generation and system response; the Feedback Stabilization Index, which measures whether loops are converging toward or diverging from equilibrium; and Causal Signal Integrity, which filters structurally causal findings from coincidence. Those instruments are the analytical infrastructure the post-April 16 assessment will deploy.

Cybernetic Game Theory names the four mechanisms through which control architecture — rather than individual choice — determines institutional outcomes: constraint geometry, which maps the feasible action set; delay dominance, which converts feedback latency into strategic resource; narrative control, which shapes perceived probabilities before market formation; and feedback capture, which locks in institutional facts before resolution arrives. Kalshi’s regulatory strategy executes all four simultaneously. The corpus established that claim analytically. April 16 tests it empirically.

April 16 represents the first coordinated test of whether prediction markets function as control systems under regulatory pressure applied simultaneously across a consolidated appellate proceeding. A panel ruling that addresses all three preemption theories — express preemption, swap classification, and field preemption — will generate the richest signal. A panel that resolves the case on the narrowest available ground will tell a different story: that the system is deferring resolution, not forcing it. Either outcome is analytically informative. Neither outcome leaves the structural model unchanged.

What Kalshi Is and How It Got Here

Kalshi is a federally licensed prediction market platform — formally, a Designated Contract Market (DCM) regulated by the CFTC — that allows users to trade binary contracts on the outcomes of real-world events, including sporting events. Founded in 2018 and licensed by the CFTC in 2020, Kalshi operated in a narrow product space until January 2025, when it self-certified sports-event contracts as swaps under the CEA’s self-certification process and began offering contracts on NFL, NBA, and other professional sports outcomes. Sports betting is legal in most states only through licensed sportsbooks subject to state gaming regulation. Kalshi’s position is that its contracts are federally regulated swaps — not wagers — and therefore fall under the CFTC’s exclusive jurisdiction, preempting state gaming enforcement entirely. Nevada disagreed and filed suit in March 2025. Sixteen states have since filed enforcement actions. The April 16 oral argument is the first appellate test of that preemption theory. The case therefore asks whether a product that is functionally indistinguishable from sports betting can be legally reclassified as a federally regulated financial instrument solely by virtue of how it is structured and where it is traded.

II. Kalshi Operates as a Jurisdictional Engine Rather Than a Market Operator

Kalshi’s Prediction Market Federal Strategy established the architecture before the April 16 docket confirmed it. Three interlocking litigation layers operate in sequence. Layer one files preemptive federal suits before state courts can establish controlling precedent with operational consequences. Layer two cascades favorable rulings as supplemental authority across every active appellate proceeding simultaneously. Layer three accumulates circuit-level authority until inter-circuit conflict becomes irresolvable and the Supreme Court is forced to settle the question on federal derivatives terms rather than state gambling terms. Each layer converts the output of state enforcement into raw material for the next layer. The architecture does not require Kalshi to win every case. It requires only that enough favorable rulings accumulate to force the question to the institutional level where Kalshi’s statutory argument is strongest.

The Tennessee sequence is the documented execution of layer two. Kalshi filed in federal court after the Tennessee Sports Wagering Council issued cease-and-desist letters in January 2026. U.S. District Judge Aleta Trauger in Nashville issued a temporary restraining order on January 12 blocking state enforcement. Kalshi transmitted that ruling as supplemental authority to every other active appellate proceeding within days. A single favorable district court ruling in Tennessee entered the record in Nevada, New Jersey, Maryland, Ohio, Connecticut, New York, and four appellate circuits before the state even had an opportunity to respond. Kalshi was not litigating — it was operating a distribution mechanism for favorable precedent at institutional scale.

The appellate record adds a layer the Federal Strategy publication described structurally but the docket now confirms operationally. Kalshi self-certified its sports-event contracts as swaps under the CEA’s self-certification process — a statutory mechanism that grants CFTC passive approval the next business day without prior agency review. The self-certification process is not a loophole. Congress designed it deliberately to allow designated contract markets to bring new instruments to market rapidly, subject to CFTC review and disapproval if the Commission determines the contract fails statutory requirements or is contrary to the public interest. Kalshi used that mechanism to list sports-event contracts in January 2025. The CFTC reviewed the self-certification and did not disapprove it. Under 17 C.F.R. § 40.2(a)(2), the passive approval became effective.

Nevada’s enforcement strategy depends on the premise that state regulators can independently determine whether Kalshi’s self-certified contracts are actually swaps subject to CFTC jurisdiction — and if not, proceed to enforce state gaming law. Binding Ninth Circuit authority forecloses the premise.

Big Lagoon Rancheria v. California, 789 F.3d 947 (9th Cir. 2015) — decided en banc by the full Ninth Circuit — holds that a state cannot collaterally attack a federal agency’s decision through enforcement proceedings against the regulated entity. If Nevada believes Kalshi’s contracts are not swaps and therefore should not have been self-certified, Nevada’s remedy is an Administrative Procedure Act (APA) suit against the CFTC, not an enforcement action against Kalshi. Nevada cannot second-guess the CFTC’s passive approval in state court or federal district court. The collateral attack doctrine forecloses exactly what Nevada is attempting to do in sixteen active enforcement proceedings.

Kalshi built its expansion architecture on a statutory mechanism designed to be structurally impervious to state-by-state challenge. The self-certification process, the CFTC’s exclusive jurisdiction grant, and the collateral attack bar under Big Lagoon form an interlocking defense that does not depend on any particular court’s view of whether sports-event contracts are good policy. The architecture works regardless of policy preference because it operates at the level of statutory structure and administrative procedure, not regulatory merit.

The clearinghouse distinction is the decisive structural boundary that the self-certification framework enforces and that the appellants’ swap classification argument depends on. Swaps traded on designated contract markets involve clearinghouses — federally regulated entities that guarantee the performance of each trade submitted for clearing and manage the financial risk between parties. Sports wagers placed through casino sportsbooks do not. Nevada itself concedes this in the appellate brief: sports bets do not involve risk-shifting arrangements with financial entities and are consumer transactions that historically have not been considered to involve swaps. The CFTC’s 2012 Further Definition of “Swap” rulemaking, 77 Fed. Reg. 48,208, draws the line explicitly: instruments traded on organized markets with clearinghouse involvement are swaps; customary consumer transactions not traded on organized markets or over-the-counter with financial entities are not. Kalshi’s sports-event contracts involve clearinghouses as counterparties. Sportsbooks’ sports wagers do not. The structural difference between clearinghouse-backed contracts and consumer wagers — not surface resemblance to gambling — is the operative boundary Congress drew, and it is the boundary the Ninth Circuit panel must decide whether to enforce or collapse.

Federal preemption provides access to a regulatory regime with broader statutory interpretation tolerance and lower enforcement density relative to state systems. Delay arbitrage — the exploitation of slow feedback cycles — converts timeline extension into market share capture that compounds past the point of recovery before resolution arrives. Kalshi Found the One Gap in American Gaming Law Nobody Closed quantifies the output: Nevada’s sports betting handle fell 9% in 2025, the same year Kalshi processed $16.8 billion in sports volume nationally. Delay dominance does not require the platform to win in court. It requires only that the feedback loop remain open long enough for market share to compound.

The PRGA Signal: What Kalshi’s Own Behavior Reveals

Cybernetic Game Theory identifies Kalshi’s March 2026 voluntary contract screening announcement — accepting behavioral constraints without a court order — as the moment the delay payoff function flipped negative. Prospective Repeated Game Architecture (PRGA) predicted that platforms with genuine private information about their legal position do not concede voluntarily until error cost forces the update.

The PRGA signal deserves explicit treatment as analytical evidence, not as a footnote to the litigation narrative. Kalshi holds information the court record does not contain: its own internal probability assessments of the preemption theory, its confidential communications with counsel, and its board-level evaluation of the litigation trajectory. Public litigation posture is designed to signal strength regardless of private belief. Voluntary behavioral concessions, by contrast, cost something — they constrain operations, create compliance overhead, and signal to regulators that the platform acknowledges the legitimacy of some limits. A platform genuinely confident in its preemption theory has no strategic incentive to accept constraints before a court orders them. The concession reveals the opposite: internal probability of the upside preemption case contracted below the strategic threshold at which continued delay generates positive expected value.

Kalshi’s public litigation posture and its private behavioral update now point in opposite directions. The court filings assert broad preemption. The voluntary screening announcement accepts behavioral limits that would be unnecessary if preemption were certain. Analyzed through the PRGA framework, the gap between public posture and private action is itself a signal — one that no external commentator has access to except through the behavioral inference the framework makes possible. Kalshi’s own conduct, not Nevada’s briefs, provides the most credible evidence that the platform’s internal assessment of April 16 is less optimistic than its public litigation posture suggests. Behavioral deviation under uncertainty reveals more than litigation posture under advocacy. Kalshi’s conduct indicates internal probability compression before the court has acted.

April 16 tests whether federal preemption operates as a durable expansion mechanism or encounters practical limits. Judicial signaling during oral argument will indicate whether the preemption architecture holds or has been structurally foreclosed by the SCEM before the appellate ruling arrives. Both tracks — appellate and legislative — are running simultaneously. One of them closes the loop first.

Contact mcai@mindcast-ai.com to partner with us on Predictive Cognitive AI in Law and Behavioral Economics. To deep dive on MindCast Foresight Simulations upload the URL of this publication into any LLM and prompt ‘reconstruct MindCast framework with three degrees of cited sub links.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure.

The MindCast — Kalshi Corpus

1. The Full Arc of Prediction Markets The foundational paper. Defines prediction markets as constrained information systems shaped by incentives, participation structure, and regime transitions — and identifies the structural conditions under which the truth-seeking function collapses into strategic exploitation and then into behavioral extraction. Establishes the two-kind taxonomy separating public belief exchanges from proprietary probability engines that governs every subsequent analysis in the corpus. Read this first.

2. Prediction Markets and the Regulatory Split Identifies the foundational divergence between federal event contract jurisdiction and state gambling regulatory frameworks. Deploys a Cognitive Digital Twin (CDT) foresight simulation — a proprietary MindCast architecture that models institutions, markets, and regulators as interacting systems to generate falsifiable forward predictions — assigning P45/P35/P20 probability bands across three resolution scenarios four days before three of six identified triggers activated simultaneously. Loop closure arrived through the legislative channel rather than the appellate path flagged as primary. Relevance: April 16 tests whether that split widens, compresses, or routes to the Supreme Court.

3. Kalshi’s Prediction Market Federal Strategy Frames Kalshi’s three-layer litigation architecture as a preemption-driven expansion engine converting state enforcement into federal appellate ammunition. Documents the removal cascade mechanic, the Tennessee supplemental authority gambit, and the asymmetric harm structure that makes coordinated preemptive state action the only effective counter. Relevance: April 16 tests whether that architecture survives contact with a coordinated Ninth Circuit panel.

4. The National Kalshi Prediction Market Litigation Map Maps multi-jurisdictional fragmentation across sixteen state enforcement actions and four appellate circuits producing conflicting rulings on identical statutory text. Establishes the removal asymmetry, the cascade mechanic, and the probability assignments across three resolution scenarios. Relevance: April 16 forces partial synchronization across nodes that have been operating asynchronously since March 2025.

5. Kalshi Found the One Gap in American Gaming Law Nobody Closed Models expansion as extraction from regulatory latency through four documented poaching mechanisms: Kalshi Platinum, tribal-market NFL advertising, 18–21 demographic capture, and quantified revenue displacement. Nevada’s sports betting handle fell 9% in 2025, the same year Kalshi processed $16.8 billion in sports volume nationally. Relevance: April 16 tests whether latency continues to enable growth or begins to compress under coordinated Ninth Circuit enforcement.

6. Prediction Market–Crypto–CFTC Convergence Links prediction markets to crypto’s jurisdictional migration toward CFTC governance as a unified control layer. Prediction markets supply information pricing infrastructure; crypto supplies settlement infrastructure; the CFTC is the only regulatory architecture capable of governing both under a unified statutory framework. Relevance: April 16 tests whether a consolidated federal appellate ruling accelerates that convergence or fractures it.

7. Prediction Markets — Legislative Regime Conversion and the Collapse of Preemption Documents the Statutory Category Exclusion Mechanism (SCEM) activated by the Schiff-Curtis Prediction Markets Are Gambling Act (March 23, 2026) — a bipartisan Senate bill that would explicitly reclassify sports prediction market contracts as gambling outside CFTC jurisdiction, eliminating the statutory ambiguity the entire preemption theory depends on — and models how legislative regime conversion forecloses the judicial and administrative channels that depend on statutory ambiguity to function. A statutory CEA amendment is not an enforcement escalation — it eliminates the contested jurisdictional space itself. Relevance: April 16 tests whether preemption remains a viable growth pathway or arrives already foreclosed.

8. Kalshi Is Crypto’s Test Case Positions a Kalshi appellate victory as locking the CFTC in as the governing control system for the next generation of financial instruments. A Kalshi loss forecloses that pathway for every platform operating under the same statutory architecture. The forward-looking consequence paper: read this last. Relevance: April 16 tests whether prediction markets inherit crypto’s regulatory trajectory or fracture it.

III. Fragmentation Creates Structural Constraint Geometry

The National Kalshi Prediction Market Litigation Map documents sixteen active state enforcement actions across four appellate circuits producing conflicting rulings on identical statutory text. Federal agencies, state regulators, courts, tribal governments, private actors, and now problem gambling organizations each impose distinct constraints. Interactions among those constraints create a geometry that governs feasible outcomes independent of actor intent. No single actor in the system controls the outcome. The architecture of the constraint field determines it.

The April 16 amicus record makes that constraint geometry visible at the appellate level in precise institutional terms. Ten amici filed in support of Nevada’s position. The Nevada Council on Problem Gambling and the Dr. Robert Hunter International Problem Gambling Center filed jointly, arguing that allowing Kalshi’s sports betting to be regulated only by the CFTC is effectively to allow it to be unregulated with regard to problem gambling risk — because the CFTC’s regulatory mandate is focused on financial instruments and markets, not on protecting gambling-specific risks inherent to gambling. Stop Predatory Gambling filed separately, attacking the preemption theory directly. Better Markets, Inc. — the financial regulatory watchdog organization — filed arguing the broader systemic risk implications of permitting unregulated sports betting to scale under a federal derivatives umbrella. Todd Phillips filed pro se. The North American Gaming Regulators Association and the International Association of Gaming Regulators filed jointly, bringing the weight of the international gaming regulatory infrastructure into the Ninth Circuit record. The American Gaming Association — the licensed gaming industry’s primary trade association — filed arguing that sports-event contracts generate roughly the same payout as sports wagers and should be regulated accordingly. Tribal Amici filed through Hobbs Straus Dean & Walker, bringing Indian Gaming Regulatory Act (IGRA) compact rights and tribal sovereign interests explicitly into the appellate record. Amici States, led by the Ohio Attorney General with support from more than thirty additional state attorneys general, filed arguing that the federal preemption theory, if accepted, would reintroduce precisely the regulatory fragmentation Congress deliberately displaced — in the CFTC’s own words, now adopted by a multistate coalition arguing against the CFTC’s position.

Four amici filed supporting the appellants. The CFTC filed asserting exclusive federal jurisdiction and arguing that state enforcement actions against federally designated contract markets undermine the uniform regulatory framework Congress enacted. Paradigm Operations LP filed through Consovoy McCarthy, arguing the broader implications for derivatives market innovation. Bitnomial Exchange LLC filed through Katten Muchin Rosenman, arguing as a fellow DCM operator that a ruling for Nevada would destabilize the self-certification framework on which every designated contract market depends. Former Federal Government Officials and Experts on the Scope of CFTC Jurisdiction filed through Willkie Farr, bringing the weight of former federal officials’ views on CEA statutory interpretation into the record.

The asymmetry is structurally significant. Ten institutional amici representing state enforcement architecture, gambling regulation infrastructure, public health, tribal sovereignty, and a multistate attorney general coalition stand against four amici representing the federal regulatory apparatus and the financial innovation sector. Constraint geometry is not merely a framework concept in the April 16 record. The docket makes it legible as an institutional map. The panel can read the alignment of forces from the caption page. The positions are not reconcilable within a single regulatory framework. A ruling that satisfies one side necessarily invalidates the core objective of the other.

The tribal sovereignty dimension of the preemption question carries structural consequences the paper record does not fully surface. Tribal gaming compacts are not state law — they are sovereign agreements between the federal government and tribal nations, negotiated under IGRA and approved by the Secretary of the Interior. States like Washington and Nevada structure their sports betting markets around tribal exclusivity rights embedded in those compacts. A federal preemption ruling that displaces state gaming authority does not merely override state regulators. It creates a mechanism through which a venture-capital-backed financial technology platform can extract revenue from markets that federal compact law reserved for tribal governments. The Tribal Amici brief makes the operational consequence concrete: Kalshi’s NFL advertising campaign in Washington targeted the precise consumer base that tribal compact exclusivity exists to protect. A preemption ruling that validates that conduct does not just resolve a jurisdictional dispute — it establishes that the CEA’s exclusive jurisdiction provision operates as a federal override of federally negotiated tribal compact rights. No court has addressed that implication directly. The April 16 panel may not address it either. But the Tribal Amici placed it in the record, and the Washington AG complaint documented it with an exhibit. The implication will follow the litigation wherever it goes. That conflict introduces a second federal layer — tribal compact rights — that the CEA does not explicitly address, increasing the probability that any appellate resolution produces downstream conflict rather than closure.

Washington State Attorney General Nick Brown’s March 28, 2026 civil complaint in King County Superior Court entered the Ninth Circuit’s appellate environment two weeks before oral argument. Filed in Ninth Circuit jurisdiction — the same circuit hearing oral argument on April 16 — the complaint includes an exhibit that no litigation framing can neutralize: a Kalshi advertisement in which one user texts another that they “found a way to bet on the NFL even though we live in Washington.” Washington reserves legal NFL wagering exclusively to tribal sportsbooks operating under IGRA compacts negotiated pursuant to the Indian Gaming Regulatory Act. Kalshi’s advertisement marketed the platform as a workaround to the restriction that exists specifically to protect tribal compact rights. Gaming attorney Scott Crowell stated the operational consequence directly: Kalshi aggressively marketed in all 50 states with particular focus on states like Washington where there is no legal online platform for consumers to use. The advertisement is not an allegation. It is a documented exhibit in a civil complaint filed by the state’s chief law enforcement officer.

Nevada filed its March 27 Rule 28(j) citation of supplemental authorities the day before the Washington complaint. Kalshi filed its own 28(j) on March 19 — the same day the Ninth Circuit denied its emergency stay motion and Nevada obtained the temporary restraining order — citing adverse rulings from Ohio (Schuler) and Michigan (Nessel) and arguing those rulings do not support affirmance because they impose extratextual limitations on the swap definition that contradict the statute’s text. Both sides flooded the record with supplemental authority in the final three weeks before oral argument. Both sides believe the panel is genuinely undecided. Both sides’ behavior reveals the most informative signal available from outside the courtroom: the panel is genuinely undecided.

The panel composition adds a final observable. Judges Barry Silverman and Holly Thomas are confirmed on the April 16 panel. Silverman is a Clinton appointee and senior Ninth Circuit judge with extensive commercial law background across decades of complex financial and regulatory disputes. Thomas is a Biden appointee, the first Black woman on the Ninth Circuit, and a former public defender with a background in civil rights and criminal law. Neither judge’s prior record indicates a strong prior disposition on CEA preemption questions specifically. The oral argument itself — not panel composition — will be the primary signal-generating event. What questions each judge asks, which arguments they press, and which they allow to pass without challenge will reveal the panel’s analytical priorities more precisely than any prior inference from judicial biography.

IV. Regulatory Latency Enables Expansion Through Feedback Delay — Until It Doesn’t

Kalshi Found the One Gap in American Gaming Law Nobody Closed documents four poaching mechanisms through which Kalshi exploited regulatory latency systematically. Kalshi Platinum is a VIP loyalty program structurally identical to casino host programs — targeting exclusively high-volume sports traders, capturing the feedback loop of behavioral engagement — without the compliance costs that make those programs expensive for licensed operators. Washington State NFL advertising marketed the platform directly into tribal-exclusive markets, documenting in a consumer-facing advertisement that the platform understood it was operating in states where its activity was legally prohibited and chose to market the gap rather than respect it. Demographic expansion targeted the 18-to-21-year-old population that state law deliberately excludes from licensed sportsbooks — the exact demographic most susceptible to problem gambling formation and most valuable to a platform building long-term user retention. Platform expansion during litigation established institutional facts on the ground — $16.8 billion in sports volume, a $22 billion valuation, a Coinbase partnership, a Major League Baseball memorandum of understanding — before resolution arrived. Each mechanism converts latency into captured market position that does not reverse when the legal question eventually resolves.

Latency functions as a resource. Firms operating within uncertain regulatory environments gain a structural advantage that competitors with lower ambiguity tolerance cannot match. The Cybernetic Game Theory delay dominance function establishes the governing logic: delay becomes rational when rule mutation outpaces enforcement — especially in multi-forum litigation environments where appellate divergence compounds strategic time extension. The longer the feedback loop remains open, the larger the institutional facts that accumulate on the ground before resolution forces adjustment.

The asymmetric winning conditions embedded in the litigation deserve explicit statement. Kalshi wins the regulatory contest by surviving long enough for market share to become structurally irreversible, regardless of how the underlying legal question ultimately resolves. Nevada wins only by obtaining an enforceable ruling that actually halts operations — and obtaining it before the institutional facts on the ground pass the point of no return. Kalshi can lose at the Ninth Circuit, lose at the Supreme Court, and still win the economic contest if those losses arrive after $50 billion in cumulative volume has normalized the platform in the consumer market, embedded it in financial infrastructure through the Coinbase partnership, and produced an MLB memorandum of understanding that creates reputational friction for regulators attempting enforcement. The litigation contest and the economic contest operate on different timelines with different winning conditions. Nevada’s enforcement strategy must account for both simultaneously — and the gap between the two timelines is exactly the resource Kalshi’s delay dominance architecture was built to exploit. Time therefore operates as a directional variable: it benefits the platform while the system remains unresolved and benefits the states only if resolution arrives before behavioral normalization becomes irreversible.

The CFTC’s posture in the April 16 record illustrates that latency structure with documentary precision. The Commission filed its amicus brief in the Ninth Circuit on February 17, 2026, asserting exclusive federal jurisdiction. The amicus brief asserts authority the Commission claims to hold right now. On March 16, 2026 — three weeks before oral argument, while that brief was pending before the panel — the CFTC published an Advance Notice of Proposed Rulemaking (ANPRM) in the Federal Register requesting public comment on the appropriate regulatory treatment of event contract derivatives (Prediction Markets, 91 Fed. Reg. 12,516, Mar. 16, 2026). The comment deadline is April 30, 2026 — fourteen days after the oral argument. The ANPRM is not the Commission’s first attempt. In June 2024, the prior CFTC administration proposed rules that would have broadly barred political and sports-related event contracts as contrary to the public interest. The current Commission withdrew those proposed rules in February 2026, citing “various forms of state regulatory actions and litigation concerning the Commission’s exclusive jurisdiction over event contracts” — and then issued the ANPRM as the replacement, asking the public to help it determine how prediction markets should be regulated. The agency that withdrew its proposed rules because of state litigation is now arguing in federal court that state litigation is foreclosed by its exclusive jurisdiction, while simultaneously soliciting public comment on how to exercise that jurisdiction. Regulatory architecture that asserts jurisdiction before completing the rulemaking to exercise that jurisdiction is latency made institutional. The gap between claimed authority and operational capacity is precisely the gap that Kalshi’s expansion strategy occupied from January 2025 forward.

CFTC Chairman Michael Selig’s public statement announcing the ANPRM sharpens the contradiction further. Selig described the rulemaking as beginning “the process of new rulemaking grounded in a rational and coherent interpretation of the Commodity Exchange Act.” The phrase “rational and coherent” is not neutral administrative language. It implies that prior interpretations — including the 2024 proposed rules the current Commission withdrew — were neither rational nor coherent. The Commission’s current chair is publicly signaling that his predecessor’s approach to prediction market regulation was wrong, while his agency’s litigators simultaneously argue in the Ninth Circuit that the Commission’s exclusive jurisdiction over those same instruments is beyond question. The ANPRM and the amicus brief do not merely reflect a control gap between claimed authority and operational capacity. They reflect an internal CFTC disagreement, expressed across two simultaneous institutional actions, about what the Commodity Exchange Act actually means. The Ninth Circuit panel will resolve the case with that internal disagreement visible in the record.

The CFTC’s dual posture is not hypocrisy. It is the structural condition of a regulatory agency operating in a domain where the statutory framework was written before the product category it now covers was invented. Congress enacted the CEA’s swap definition in the Dodd-Frank Act of 2010 against a backdrop in which sports betting was federally prohibited in most states under the Professional and Amateur Sports Protection Act (PASPA). Congress specifically contemplated that gaming-related event contracts could be traded on DCMs but gave the CFTC discretion to prohibit them through the public interest review process. Nobody anticipated a platform would self-certify sports betting contracts as swaps under that framework, bypass state gaming licensing in all fifty states, and process $16.8 billion in sports volume before the CFTC completed the rulemaking that would define the line between sports wagers and swaps. Kalshi did not exploit regulatory negligence. It exploited the structural gap between the speed of product innovation and the speed of regulatory response — and it did so at a scale that made the gap irreversible before anyone with authority to close it had finished their rulemaking process.

Latency compression arrives from multiple directions simultaneously. The Schiff-Curtis Prediction Markets Are Gambling Act (March 23, 2026) activates the Statutory Category Exclusion Mechanism (SCEM). Prediction Markets — Legislative Regime Conversion and the Collapse of Preemption names the mechanism precisely: a statutory CEA amendment is not an enforcement escalation. Enforcement actions operate within a contested jurisdictional space. A statutory amendment eliminates the space itself. Express statutory prohibition is not a regulatory interpretation subject to CFTC override or appellate revision. If the Prediction Markets Are Gambling Act advances to enactment — or if its legislative record sufficiently signals congressional intent — the statutory ambiguity that the entire preemption argument depends on collapses before the appellate ruling arrives.

April 16 tests whether latency remains exploitable or has begun to compress irreversibly. Rapid post-hearing coordination among state AGs — Washington, Nevada, Arizona, Massachusetts, and Tennessee have all filed within the same enforcement cycle, and Nevada’s March 27 supplemental authority letter entered the appellate record the day before Washington filed — confirms that the coordination mechanism is already active. A Ninth Circuit ruling signaling preemption limits would accelerate that coordination further. A Ninth Circuit ruling for the appellants would compress the legislative latency instead, forcing the Schiff-Curtis track to move faster than it otherwise would. Either outcome compresses the latency resource. The only scenario that preserves delay dominance is a field preemption ruling that resolves the consolidated appeal without addressing the swap classification circuit split — deferring the core question to a future proceeding while Kalshi continues to operate under the self-certification framework.

V. April 16 as Diagnostic Instrument: What the System Will Reveal

April 16 compresses signal generation across appellate, regulatory, legislative, and market systems into a single observation window. The oral argument does not resolve the institutional conflict — it produces the signal that updates every actor’s probability estimates simultaneously. State AGs update their enforcement calculus. The CFTC updates its rulemaking timeline. Congress updates the Schiff-Curtis schedule. Capital markets update Kalshi’s valuation. The interaction does not occur at argument. It occurs in the coordinated updates that follow it. The consolidated oral argument places the preemption dispute before the Ninth Circuit panel with the Washington AG filing two weeks old, the CFTC’s rulemaking comment deadline fourteen days away, the Schiff-Curtis SCEM bill three weeks into the Senate record, and the problem gambling amici’s argument — that CFTC-only jurisdiction is effectively no jurisdiction for gambling-specific risks — entered in the appellate record.

The Three-Layer Preemption Architecture

The Ninth Circuit panel must navigate three sequential preemption theories. Each is independently sufficient to resolve the consolidated appeal. Each produces a different downstream consequence for the litigation map, the legislative track, and the Supreme Court trajectory. Understanding which theory the panel treats as primary is the central analytical task the April 16 oral argument makes possible.

Layer One: Express Preemption Under § 2(a)(1)(A). Section 2(a)(1)(A) of the CEA grants the CFTC “exclusive jurisdiction” over transactions involving swaps traded or executed on a designated contract market. The appellants argue that “exclusive” has one plausible statutory meaning: state law is preempted. The plain meaning of “exclusive” necessarily denies jurisdiction to other entities, including state regulators. Nevada’s primary counter — the load-bearing argument Nevada needs to win — is that § 2(a)(1)(A)’s exclusive jurisdiction language speaks only to the CFTC’s jurisdiction relative to the Securities and Exchange Commission, not to state preemption. The appellants call that reading facially implausible: Congress overhauled the CEA in 1974 specifically to bring derivatives markets under a uniform set of regulations, striking statutory language that had previously preserved state law and replacing it with language confirming that the Commission’s jurisdiction, where applicable, supersedes state as well as federal agencies. The 1974 Senate Report says so explicitly. Legislative history and statutory structure both confirm that § 2(a)(1)(A) was designed to prevent exactly the state-by-state regulatory fragmentation Nevada is now attempting to reimpose.

Layer Two: Swap Classification Under § 1a(47)(A)(ii). If sports-event contracts are swaps traded on a DCM, the CFTC’s exclusive jurisdiction under § 2(a)(1)(A) attaches and state law is preempted. The definitional battle turns on the statutory language: a swap includes any agreement that provides for payment “dependent on the occurrence, nonoccurrence, or the extent of the occurrence of an event or contingency associated with a potential financial, economic, or commercial consequence.” The appellants argue that sports-event contracts satisfy this definition. Payment under a sports-event contract depends on the occurrence — whether a team wins — of an event associated with a potential commercial consequence — sportsbooks lose revenue when a large volume of one side of a bet cashes out. Licensed sportsbooks can and do use sports-event contracts to hedge against exactly that exposure. The instrument serves a genuine hedging function for commercial entities, which is precisely what swaps are designed to do.

Nevada’s counter is the circuit split. The Sixth Circuit in Schuler (Ohio) and a Michigan court in Nessel both found that sports-event contracts are not swaps because they lack an inherent connection to financial consequences — imposing a limiting construction on the statutory language that the appellants argue is extratextual. Neither statute nor CFTC regulation requires that a swap be “inherently” connected to financial consequences. The statute requires only a “potential” financial, economic, or commercial consequence. Schuler and Nessel read a word into the statute that is not there. The appellants further argue that Nevada’s own position concedes the definitional point: Nevada agrees that sports wagers are not swaps because they are customary consumer transactions not traded on organized markets with financial entities. Sports-event contracts are traded on DCMs with clearinghouses as counterparties — the structural difference Nevada itself acknowledges is the operative distinction under the CFTC’s 2012 Further Definition of “Swap” rulemaking, 77 Fed. Reg. 48,208.

Layer Three: Field Preemption of All DCM Trading. Even if the Ninth Circuit finds that sports-event contracts are not swaps, the appellants argue the CEA preempts the field of all trading on designated contract markets, regardless of whether the instruments at issue are swaps, futures, or options. The CEA creates a comprehensive regulatory structure governing every aspect of DCM operations from contract certification and listing through enforcement and delisting. Congress designed the comprehensive CEA scheme to leave no room for state law to operate alongside it. Under Arizona v. United States, 567 U.S. 387 (2012), a federal regulatory scheme that is sufficiently comprehensive occupies the field and displaces state law even without explicit preemption language. The DCM regulatory framework is among the most comprehensive in federal law — governing contract design, participant access, clearinghouse requirements, margin rules, reporting obligations, and enforcement procedures. Nevada cannot regulate Kalshi’s on-DCM trading without collaterally attacking the CFTC’s passive approval of the self-certification, which Big Lagoon bars. If Nevada believes the contracts should not be on a DCM, it must file an APA suit against the CFTC.

The Oral Argument Allocation and What It Reveals

The argument time allocation entered in the docket record encodes the panel’s working assumption about where the argument weight sits. Plaintiffs-Appellants share 45 minutes: William Havemann of Milbank for Kalshi, Shay Dvoretzky of Skadden for Crypto.com, and Martin Jordan Minot of the CFTC with 6 minutes as amicus. Defendants-Appellees Nevada and the Nevada Gaming Control Board, represented by Nicole Saharsky of Mayer Brown and Mark Weisenmiller, share 30 minutes with no further allocation specified. The Nevada Resort Association, represented by McDonald Carano, argues separately.

The CFTC’s presence at the podium is the most structurally significant detail in the argument allocation. The Commission filed its amicus brief, moved for oral argument time, obtained that time over no recorded objection, and will stand before the panel to argue that state enforcement of gaming laws against federally designated contract markets would reintroduce precisely the regulatory fragmentation Congress deliberately displaced. A federal agency arguing in an appellate court that a state is wrong to try to enforce state law is not a routine posture. The CFTC is not appearing because it was invited. It moved for oral argument time and the court granted it. The Commission made an affirmative decision to put a senior litigator — the Deputy General Counsel for Litigation — in Courtroom 1 on April 16. The Commission’s own assessment of the stakes drove that decision.

The panel’s questions during oral argument will reveal which of the three preemption layers it treats as the resolution pathway. Questions focused on the meaning of “event” or “contingency” in § 1a(47)(A)(ii) signal that the panel is working through swap classification — the circuit split question. Questions focused on the scope and effect of § 2(a)(1)(A)’s exclusive jurisdiction language signal that the panel is engaging express preemption — the broadest available ground. Questions focused on Big Lagoon, the collateral attack doctrine, or the self-certification process signal that the panel is considering field preemption as the resolution pathway — one that resolves the consolidated appeal without deciding the swap classification question and without creating or resolving the inter-circuit conflict. Field preemption is the pathway most likely to produce a ruling that leaves the legislative track as the modal resolution mechanism.

MindCast’s CDT foresight simulation — deployed in Prediction Markets and the Regulatory Split — assigned P45/P35/P20 across three resolution scenarios. The downside scenario — gambling classification locking in through either the legislative or appellate channel — moved to modal status before April 16. Loop closure arrived through the legislative channel rather than the appellate path flagged as primary in the original simulation, confirming that the SCEM was the instrument that shifted the probability distribution. April 16 introduces a second closure pathway running in parallel. Both tracks produce signals. The post-hearing assessment will score which pathway advanced and update the probability assignments accordingly.

VI. The Case Has Already Collapsed to a Single Question

The litigation converged on a single controlling question before April 16: whether sports-event contracts satisfy the statutory definition of “swap” under 7 U.S.C. § 1a(47). Whether the contracts are swaps determines whether the CFTC’s exclusive jurisdiction grant under § 2(a)(1)(A) attaches. If the contracts are swaps, the CFTC has exclusive jurisdiction, state law is preempted, and Nevada’s enforcement actions fail on the merits. If the contracts are not swaps, the CFTC’s exclusive jurisdiction does not attach, state gaming law applies, and sixteen enforcement actions become substantially more likely to succeed. Express preemption, field preemption, and the options backstop are all real arguments in the appellate record — but all three are conditional on or scaffolded around the swap classification. The reply brief confirms the compression: approximately 80% of the argument energy addresses § 1a(47)(A)(ii). Everything else operates in the alternative.

The Statutory Boundary the Court Must Maintain

The court’s real structural anxiety is the boundary between consumer wagering and financial instruments. Nevada’s most powerful argument is not that sports-event contracts are bad policy. It is that if sports-event contracts are swaps, the court cannot explain why ordinary sports wagers placed through a casino sportsbook are not also swaps. If the statutory definition reaches that far, the CFTC becomes the de facto national gambling regulator — a result Congress demonstrably did not intend when it enacted the Dodd-Frank Act’s swap definition in 2010 against a backdrop in which most sports betting was federally prohibited under PASPA.

The answer to that anxiety exists in the record, and it is the clearinghouse distinction. Swaps traded on designated contract markets involve clearinghouses — federally regulated entities that guarantee trade performance and manage financial risk between parties. Sports wagers placed through casino sportsbooks do not. The CFTC’s 2012 Further Definition of “Swap” rulemaking, 77 Fed. Reg. 48,208, drew that line explicitly: instruments traded on organized markets with clearinghouse involvement are swaps; customary consumer transactions not traded on organized markets or over-the-counter with financial entities are not. Nevada itself concedes in its brief that sports bets do not involve risk-shifting arrangements with financial entities and are consumer transactions that historically have not been considered to involve swaps. The appellants’ answer to the slippery slope argument is therefore not rhetorical. It is structural: the clearinghouse requirement creates a hard boundary that ordinary sports wagers cannot cross.

Whether the Ninth Circuit panel accepts that answer is the controlling question April 16 will begin to resolve. The panel can accept the clearinghouse distinction and find for the appellants on swap classification. It can reject the distinction and find that sports-event contracts are not swaps regardless of clearinghouse involvement. Or it can avoid the classification question entirely by ruling on field preemption — finding the CEA preempts all DCM trading regardless of swap status and that Nevada’s collateral attack on the self-certification is foreclosed by Big Lagoon. Each pathway produces a different downstream consequence for the circuit split, the legislative track, and the Supreme Court trajectory. Appellate decision-making favors the narrowest ground that resolves the case without creating unnecessary conflict, which makes field preemption the structurally preferred pathway if the panel seeks to avoid deepening the circuit split. A ruling on swap classification imposes system-wide consequences immediately. A ruling on field preemption defers them.

The Active Circuit Split

The Sixth Circuit found in Schuler (Ohio) that sports-event contracts are not swaps because they lack an inherent connection to financial consequences. A Michigan court reached the same conclusion in Nessel. Both impose a limiting construction on § 1a(47)(A)(ii) that the appellants argue is extratextual — the statute requires only a “potential” financial, economic, or commercial consequence, not an “inherent” one. The Schuler and Nessel courts read a word into the statute that is not there. The District of Nevada in Hendrick I (April 2025) and the District of New Jersey in Flaherty found the opposite way. The Third Circuit has an appeal pending from Flaherty. The Fourth Circuit has an appeal pending from Maryland’s adverse ruling. The Ninth Circuit’s April 16 ruling enters a multi-circuit conflict on identical statutory text.

Alignment with the Sixth Circuit collapses Kalshi’s preemption theory nationally and makes Supreme Court certiorari the modal resolution path. A Ninth Circuit split from the Sixth Circuit produces an irresolvable inter-circuit conflict. Four circuits evaluating the same § 1a(47)(A)(ii) question with divergent outcomes makes Supreme Court certiorari not merely probable but essentially automatic. Kalshi’s three-layer litigation architecture was designed to manufacture exactly this inter-circuit conflict. Kalshi is not litigating to win the existing rule. Kalshi is litigating to force the question to the one court where its statutory argument — that Congress enacted a broad swap definition and did not exclude gaming-related event contracts from it — has the best chance of prevailing.

The Supreme Court trajectory is analytically underspecified in most commentary on this litigation. A four-circuit split on § 1a(47)(A)(ii) reaches the Supreme Court as a pure statutory interpretation question — specifically, whether “potential financial, economic, or commercial consequence” in the swap definition means what it says, or whether courts may impose a limiting construction requiring an “inherent” rather than merely potential connection to financial consequences. Schuler and Nessel read a word into the statute that is not there. The current Supreme Court’s textualist majority applies the principle that courts must enforce statutory text as written and may not add limiting constructions that Congress did not include. Under that framework, the appellants’ reading of § 1a(47)(A)(ii) — that “potential” means potential, without the inherency gloss Schuler imposed — is the stronger position at the Supreme Court level. Kalshi’s three-layer architecture was designed to manufacture the circuit split. The circuit split was designed to produce the certiorari petition. The certiorari petition delivers the statutory text argument to the court most likely to read statutory text as written. April 16 is stage one of a three-stage jurisdictional strategy that ends at One First Street. That trajectory depends on the Court accepting the case, which is likely under a multi-circuit conflict but not guaranteed.

The Uniformity-Sovereignty Fault Line

The ideological fault line beneath the statutory dispute is federal uniformity versus state police power. The amicus alignment presents mutually incompatible regulatory objectives: uniform national derivatives markets versus localized harm mitigation and licensing regimes. The panel cannot reconcile both within the same statutory interpretation. Congress enacted the CEA’s exclusive jurisdiction provision to bring derivatives markets under a uniform set of regulations rather than a patchwork of state laws. The uniformity interest is real — a DCM that must comply with fifty different state gaming regimes cannot operate as a national exchange. But states’ traditional authority to regulate gambling is equally real, rooted in the Tenth Amendment’s police power reservation and nearly a century of established regulatory practice. The swap classification question is the statutory mechanism through which the panel draws that line — or declines to draw it. A field preemption ruling that resolves the case without deciding swap classification avoids the fault line by holding that whatever sports-event contracts are, DCM trading is not a domain in which state police power operates at all.

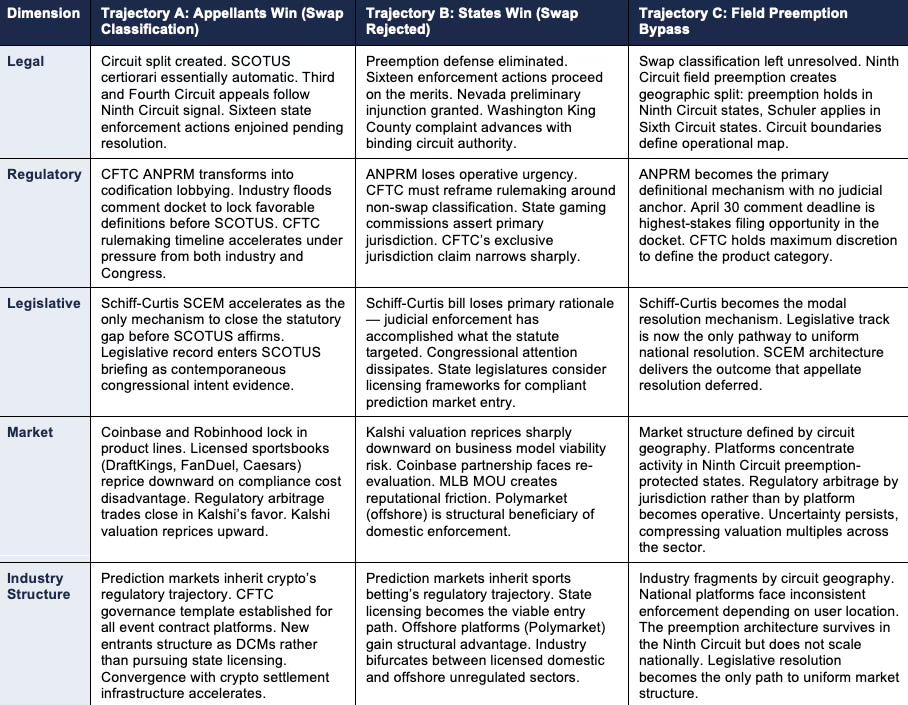

VII. Three Trajectories: What Each Outcome Produces

The system resolves through three mutually exclusive pathways. April 16 does not produce a single outcome. The consolidated oral argument generates a signal that routes the entire prediction market regulatory contest down one of three distinct institutional pathways, each producing a different consequence chain across legal, regulatory, legislative, market, and industry structure dimensions. The falsifiable predictions in Section VIII measure whether specific events occur. The trajectory analysis below maps what those events mean — what the world looks like six months, twelve months, and two years after the Ninth Circuit rules, depending on which path the panel takes.

Trajectory A: Appellants Win on Swap Classification

A Ninth Circuit ruling that sports-event contracts satisfy the swap definition under § 1a(47)(A)(ii) produces the outcome Kalshi’s three-layer architecture was designed to manufacture. The immediate legal consequence is a circuit split that makes Supreme Court certiorari essentially automatic — the Sixth Circuit holds one way, the Ninth Circuit holds the other, with Third and Fourth Circuit appeals pending. The constitutional stakes of the preemption question combined with the financial magnitude of the industry guarantee that at least four Justices vote to grant review. The case reaches the Supreme Court with the textualist majority positioned to resolve it on statutory text alone: “potential” means potential, not “inherent,” and the Schuler gloss reads a limiting construction into statute Congress did not write.

The regulatory consequence of a Trajectory A ruling runs through the CFTC’s ANPRM simultaneously. A Ninth Circuit ruling validating swap classification transforms the ANPRM comment period from exploratory consultation into codification lobbying. Kalshi, Polymarket, and every platform operating under the same statutory framework floods the comment docket with submissions designed to lock favorable definitional boundaries into the proposed rule before the Supreme Court can reverse. The CFTC’s rulemaking timeline accelerates under political pressure from both sides — the industry pushing to formalize the preemption architecture before SCOTUS disrupts it, Congress pushing to preempt the rulemaking entirely through the Schiff-Curtis SCEM.

The market consequence is immediate and asymmetric. Coinbase and Robinhood lock in prediction market product lines with regulatory certainty as the operating assumption. DraftKings, FanDuel, and Caesars face an acute compliance cost disadvantage — their licensed sportsbook operations carry state-by-state regulatory overhead that Kalshi avoids entirely under federal preemption. The sportsbook sector reprices downward relative to the prediction market sector. Regulatory arbitrage trades that were open under uncertainty close in Kalshi’s favor. The crypto-CFTC convergence thesis from corpus publication 2 accelerates: a Trajectory A ruling establishes the regulatory template for the next generation of event contract platforms, including every crypto exchange watching the litigation. Kalshi’s $22 billion valuation reprices upward. The institutional facts on the ground — $16.8 billion in sports volume, the MLB memorandum of understanding, the Coinbase partnership — become harder to unwind regardless of what SCOTUS eventually holds.

Trajectory B: States Win — Swap Classification Rejected

A Ninth Circuit ruling that sports-event contracts are not swaps collapses Kalshi’s preemption theory nationally and activates every enforcement mechanism simultaneously. The immediate legal consequence is that sixteen active state enforcement actions become substantially more likely to succeed on the merits — without federal preemption as a defense, Kalshi must either obtain state licenses in every jurisdiction where it operates or exit those markets. Nevada obtains the preliminary injunction it has been seeking since March 2025. Washington’s March 28 complaint, filed two weeks before oral argument, proceeds in King County Superior Court with binding Ninth Circuit authority supporting it.

The regulatory consequence of a Trajectory B ruling is that the CFTC’s ANPRM loses its operative urgency. If the courts have already held that sports-event contracts are not swaps, CFTC rulemaking on how to govern them as derivatives instruments becomes substantially narrower in scope — the Commission must now define what the instruments are before it can assert authority over them. The comment deadline of April 30, 2026 — fourteen days after the ruling — transforms from a lobbying opportunity into a crisis management event. The Schiff-Curtis bill becomes unnecessary: state enforcement has accomplished through judicial interpretation what the statute was designed to accomplish through legislative action. Congressional attention to the SCEM mechanism dissipates.

The market consequence of Trajectory B is severe for Kalshi specifically and clarifying for the sector broadly. Kalshi’s $22 billion valuation reprices immediately and sharply — not merely on preemption risk but on the structural question of whether the current business model is viable at all without federal preemption as a shield. The Coinbase partnership faces regulatory re-evaluation. The MLB memorandum of understanding creates reputational friction for a platform now definitively classified as an unlicensed gambling operator in states that have filed enforcement actions. Polymarket, operating offshore and outside the CEA framework, may be the structural beneficiary of a Trajectory B ruling — the licensed domestic sector is constrained, the federal preemption pathway is closed, and the offshore platform faces no additional enforcement pressure from the ruling. The industry structure bifurcates between licensed domestic operators subject to state oversight and offshore platforms that the Trajectory B ruling does nothing to reach.

Trajectory C: Field Preemption Bypass — The Delay Equilibrium Extends

A Ninth Circuit ruling on field preemption that resolves the consolidated appeal without deciding the swap classification question produces the outcome that extends the delay-dominant equilibrium longest. Kalshi continues operating under the self-certification framework. Nevada’s enforcement is enjoined. The swap classification circuit split survives unresolved. Every actor who wanted the appellate ruling to settle the definitional question must now redirect to the only active federal processes: the CFTC’s ANPRM and the Schiff-Curtis legislative track.

The ANPRM consequence of Trajectory C is the highest-stakes outcome for the comment docket. Without a judicial resolution of the swap classification question, the CFTC’s rulemaking becomes the primary mechanism through which the line between swaps and wagers gets drawn — and the April 30 comment deadline, falling fourteen days after oral argument, positions MindCast’s public comment as the analytical anchor in a docket that suddenly has no competing judicial resolution to reference. Every commenter must engage the CFTC’s framing rather than a court’s. The Commission holds more discretion under Trajectory C than under either other scenario.

The geographic consequence of Trajectory C is the most structurally distinctive of the three paths. A field preemption ruling that applies to the Ninth Circuit’s jurisdiction creates an immediate regulatory geography: Kalshi operates freely in Ninth Circuit states under field preemption, faces enforcement risk in Sixth Circuit states under Schuler, and faces an open question in every other circuit. Regulatory arbitrage by geography becomes the operative market structure. Platform operators rationally concentrate activity in preemption-protected jurisdictions while minimizing exposure in Schuler-governed states. The practical effect is a prediction market map defined by circuit boundaries rather than state lines — a fragmentation outcome that preemption was supposed to prevent but that field preemption without swap classification resolution actually produces. The legislative track under Schiff-Curtis becomes the only mechanism capable of imposing uniform national resolution, which is precisely the outcome the SCEM architecture was designed to deliver.

Trajectory Comparison Table

The table below maps each trajectory across five institutional dimensions. Cells describe the first-order consequence in each dimension within the 90-day window following the ruling.

VIII. Falsifiable Predictions: What April 16 Will Score

April 16 is a measurement event, not merely a legal proceeding. The MindCast corpus established the structural architecture. The docket record confirmed the argument structure. Five falsifiable predictions specify exactly what confirmation and disconfirmation look like, tied to event-linked triggers already in motion. The post-hearing assessment will score each prediction against observed outcomes and update the CDT foresight simulation’s probability assignments accordingly.

Foresight Prediction 1 — Circuit Split Resolution Test

The Ninth Circuit will either align with the Sixth Circuit’s Schuler decision — finding that sports-event contracts are not swaps under § 1a(47)(A)(ii) because they lack an inherent connection to financial consequences — or split from it by adopting the appellants’ broader textual reading that the statute requires only a potential financial, economic, or commercial consequence, not an inherent one.

Alignment with the Sixth Circuit collapses Kalshi’s preemption theory nationally. A ruling that sports-event contracts are not swaps means the CFTC’s exclusive jurisdiction under § 2(a)(1)(A) does not attach, state gaming law applies, and sixteen active enforcement actions become substantially more likely to succeed on the merits. Supreme Court certiorari on the circuit split becomes the modal resolution path, with the inter-circuit conflict between the Sixth and Ninth Circuits on identical statutory text creating the precise conditions under which the Supreme Court is expected to grant review.

A Ninth Circuit ruling for the appellants on swap classification produces an irresolvable inter-circuit conflict — the precise outcome Kalshi’s three-layer litigation architecture was designed to manufacture. The Sixth Circuit has found one way. The Ninth Circuit would find the opposite way. The Third Circuit (New Jersey) and Fourth Circuit (Maryland) have appeals pending. A four-circuit conflict on the meaning of § 1a(47)(A)(ii) makes Supreme Court certiorari not merely probable but essentially automatic.

Event-linked timing trigger: the next round of 28(j) letters filed by both sides in the days immediately following oral argument. The velocity and content of post-argument supplemental authority filings will signal which direction both sides believe the panel is leaning before the opinion issues. Confirmation condition: Ninth Circuit opinion issued within 90 days of April 16 taking a clear position on § 1a(47)(A)(ii) swap classification.

Foresight Prediction 2 — SCEM Primacy Test

If the Ninth Circuit signals during oral argument that preemption has practical limits — through questions focused on the states’ traditional police power over gambling, the public interest concerns raised by problem gambling amici, or the absence of CFTC rulemaking specifying the line between sports wagers and swaps — the legislative channel becomes the modal resolution pathway.

The Schiff-Curtis Prediction Markets Are Gambling Act (March 23, 2026) activated the Statutory Category Exclusion Mechanism before April 16. Congressional intent expressed in the bill’s legislative record — that the CEA does not permit sports gambling and never did — enters the statutory interpretation debate regardless of whether the bill advances to enactment. Appellate courts interpreting ambiguous statutory language consider contemporaneous legislative history. The Schiff-Curtis bill is now part of that history.