MCAI Lex Vision: The National Kalshi Prediction Market Litigation Map

State Actions, Federal Court Rulings, and the Trump Administration's Posture

Related publications: Kalshi Is Crypto’s Test Case | Kalshi’s Prediction Market Litigation Architecture, the CFTC Amicus, and the Strategic Framework for State Enforcement | The National Kalshi Prediction Market Litigation Map | The Full Arc of Prediction Markets | Prediction Markets and the Regulatory Split | Prediction Markets— Legislative Regime Conversion and the Collapse of Preemption | Kalshi Found the One Gap in American Gaming Law Nobody Closed | The Ninth Circuit on April 16 as System Convergence — The First Measurable Test of Prediction Market Structure | Kalshi, Prediction Markets and the Conflict Architecture of Regulation | Prediction Markets Litigation Stack — Federal, Private, and State Enforcement Converge

I. Overview: The Scale of the Standoff

Kalshi launched sports betting in January 2025. Within fourteen months, the company faces criminal charges in Arizona, civil enforcement actions across more than a dozen states, over twenty federal lawsuits, and a bipartisan Senate bill that would strip its federal regulatory shield entirely. The Commodity Futures Trading Commission (CFTC) — the federal agency whose designation Kalshi claims as its preemption shield — has filed friend-of-the-court briefs defending Kalshi’s federal status even as state attorneys general across both parties close in. Kalshi processes billions of dollars in weekly bets, with sports-related contracts accounting for roughly ninety percent of trading volume according to Sacra’s market analysis and Sportico’s reporting, and the company’s long-term viability hinges on how courts define a single word: gaming.

MindCast’s Prediction Markets and the Regulatory Split, published March 19, 2026, established the structural mechanism driving state enforcement as attractor dominance — when constraint density is high and a shorter legal path already exists in statutory form, enforcement agencies map novel instruments onto that path rather than constructing new regulatory categories. Arizona Attorney General Kristin Mayes did not invent a new theory. She activated a preexisting wagering statute broad enough to cover any business accepting bets on the result of any unknown or contingent future event. The statute fit. The charges followed.

MindCast assigned probability weights to three scenarios: P45 to fragmented enforcement persisting as the base case, P35 to gambling classification locking in as the downside case, and P20 to the federal derivatives framework prevailing as the upside case. Each subsequent state action — including Washington’s filing today — compounds pressure on the downside scenario.

Active litigation now spans at least a dozen jurisdictions, and officials in eleven additional states have issued cease-and-desist orders without yet filing suit. The coalition of states pushing back is not partisan. “There are only a few things right now that unite attorneys general from both parties, and prediction markets are definitely one of them,” former New Jersey Attorney General Matthew Platkin told CNN. Washington’s civil complaint filed today in King County Superior Court is the latest entry in a litigation map that is expanding faster than any single appellate court can resolve it.

Control Diagnosis

The core conflict is not merely definitional ambiguity — it is a fragmented control regime moving toward forced centralization. Four dominant mechanisms govern resolution timing more than doctrinal clarity alone: state statutory geometry creates the shortest enforcement path; strategic delay preserves Kalshi’s operating room across fragmented forums; feedback inversion converts corrective enforcement signals into preemption ammunition; and federal institutional throughput failure prevents rapid classification coherence. No single actor currently controls the outcome. State attorneys general hold the strongest near-term operating position because state wagering statutes offer the shortest enforcement path. Kalshi retains a live upside path because federal ambiguity, favorable district court rulings, and concentrated capital support preserve its ability to keep the system in motion. The regulatory architecture cannot self-correct internally — courts or Congress must impose a higher-order classification decision. Migration of resolution pressure from fragmented state enforcement to centralized federal authority is the structural finding this publication maps, predicts, and falsifies.

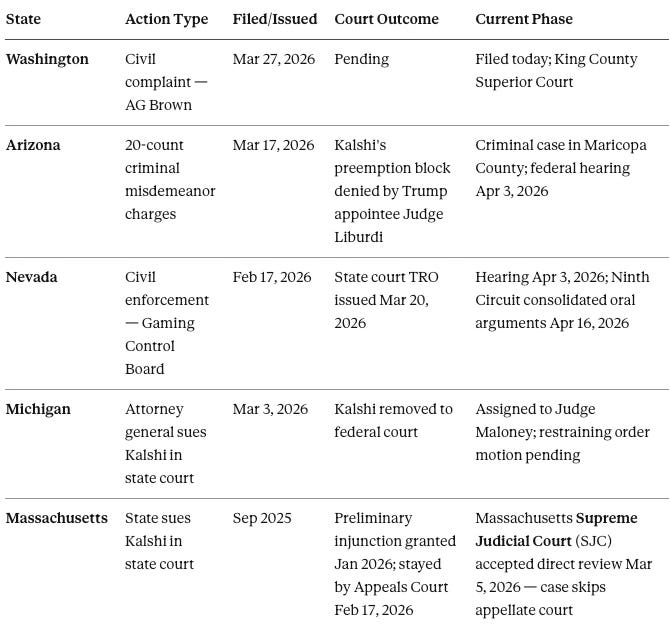

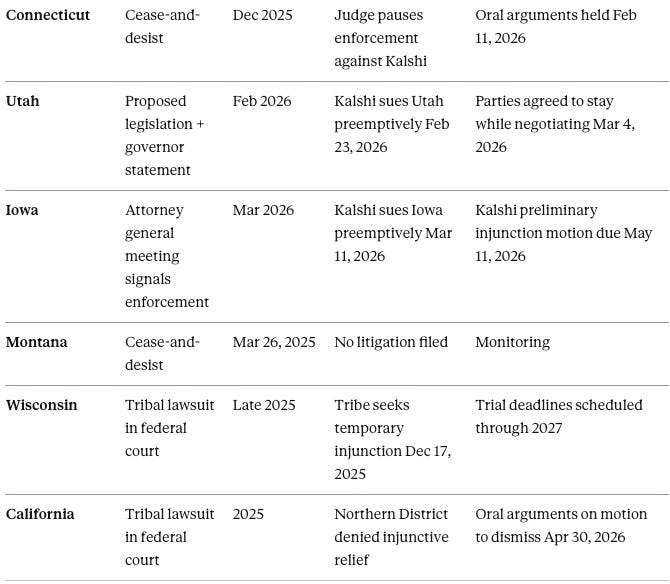

II. State-by-State Action Table

Every state that has taken formal legal or regulatory action against Kalshi as of March 27, 2026 appears below, with filing dates, court outcomes, and current procedural phase. States with cease-and-desist orders but no active litigation appear separately below the table. Three structurally distinct categories of action are covered: state-initiated enforcement suits, Kalshi’s preemptive federal lawsuits filed against state regulators before those regulators could act, and tribal government suits advancing claims under a separate federal statutory framework. All three categories share the same underlying preemption question — whether the Commodity Exchange Act (CEA), the federal statute governing derivatives trading, displaces state gambling authority over federally registered exchanges — but advance it through different procedural vehicles and different plaintiff theories. Outcomes marked “pending” reflect cases where no court has yet issued a substantive ruling. Where a temporary restraining order (TRO) — a court order blocking enforcement while a case is heard — has issued, the table notes the next hearing date.

States with cease-and-desist orders or operator license threats but no lawsuit filed: Louisiana, Pennsylvania (letters to Congress and the CFTC), Illinois (Gaming Board notice to licensees), Michigan Gaming Control Board (notice separate from attorney general suit), Nevada (notices to licensees), Massachusetts Gaming Commission, Maryland Lottery and Gaming Control Commission, Arkansas (attorney general opinion that Kalshi is illegal), Kansas and North Carolina (publicly monitoring litigation).

Contact mcai@mindcast-ai.com to partner with us on Predictive Law and Behavioral Economics + Game Theory Foresight Simulations. To deep dive on MindCast work in Cybernetic Foresight Simulations upload the URL of this publication into any LLM and prompt ‘reconstruct MindCast framework with three degrees of cited sub links.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure.

Recent projects: The Power Stack Series— How Energy Infrastructure Became the New AI Battleground | MindCast AI Emergent Game Theory Frameworks | MindCast AI Field-Geometry Reasoning | MindCast AI Installed Cognitive Grammar | Runtime Geometry, A Framework for Predictive Institutional Economics | Super Bowl LX — AI Simulation vs. Reality | The Runtime Causation Arbitration Directive | Google’s Deep-Thinking Ratio Measures Effort, Not Structure | MindCast AI Constraint Geometry and Institutional Field Dynamics | Double-Sided Rational Ignorance, How Platform Intermediaries Monetize the Measurement Gap | Executive Summary of MindCast AI Investment Series

III. Federal Court Rulings: What Is Blocking State Action and What Is Not

The federal court record on Kalshi’s preemption defense is deliberately and consequentially split. No single ruling controls because no appellate court has yet issued a definitive decision on whether the Commodity Exchange Act (CEA) — which governs Kalshi’s designation as a Designated Contract Market (DCM), meaning a federally registered exchange permitted to list financial contracts — preempts state gambling laws. Courts at the district level are reaching opposite conclusions on the same statutory text, producing a landscape in which Kalshi can operate freely in Tennessee while facing a criminal prosecution in Arizona and a civil complaint in Washington simultaneously.

MindCast’s The Full Arc of Prediction Markets identified the precise mechanism behind the split: prediction markets genuinely occupy the gap between two legal frameworks — gambling law and commodity futures law — that were each constructed around a world where the distinction between them was obvious. Neither framework was designed for an activity that is simultaneously a financial instrument, an information aggregation mechanism, and a mass-participation wagering product. Courts are not confused; they are applying coherent frameworks built to answer different questions, and those frameworks reach opposite conclusions from the same facts.

Federal orders currently blocking state enforcement — Kalshi prevailing:

New Jersey — federal preliminary injunction granted Apr 2025; Third Circuit reviewing on appeal; oral arguments held Sep 10, 2025

Tennessee — federal preliminary injunction granted Feb 19, 2026; Tennessee appeals to Sixth Circuit Mar 20, 2026

Connecticut — enforcement paused by judge pending ruling; oral arguments held Feb 11, 2026

Federal orders dissolved or denied — states prevailing:

Maryland — federal court denied Kalshi’s injunction Aug 2025; Fourth Circuit oral arguments May 7, 2026 with Neal Katyal representing Kalshi

Nevada — federal injunction dissolved Nov 2025; state court TRO issued Mar 20, 2026; Ninth Circuit consolidated oral arguments Apr 16, 2026

Ohio — Kalshi preliminary injunction denied Mar 9, 2026; Kalshi appeals to Sixth Circuit; briefing runs through Jun 2026

Massachusetts — state court preliminary injunction granted Jan 2026, stayed by Appeals Court Feb 17, 2026; Massachusetts SJC accepted direct review Mar 5, 2026

Arizona — Trump-appointed federal Judge Liburdi denied Kalshi’s preemptive block Mar 17, 2026; federal hearing Apr 3, 2026

No appellate court has resolved the preemption question. Three circuit courts — the Third, Fourth, and Ninth — are reviewing it simultaneously. The Sixth Circuit enters as a fourth when the Ohio and Tennessee appeals are briefed, and the intra-Sixth-Circuit dynamic is particularly significant: Ohio ruled for the state and Tennessee ruled for Kalshi on the same statutory question, creating a split within a single circuit that accelerates certiorari pressure independently of the inter-circuit split developing across the Third, Fourth, and Ninth. A circuit split is not a risk — it is already materializing. The Supreme Court is the only institution that can issue a binding resolution, and an economics professor who studies prediction markets told NPR directly: “It’s going to be something the Supreme Court, and maybe even Congress, will have to weigh in on.”

IV. The Trump Administration’s Posture

The Trump administration’s position functions as the most structurally significant variable in the entire litigation map — and the most conflicted. The administration has deployed the CFTC as its primary institutional instrument, filing friend-of-the-court briefs defending Kalshi’s federal designation, signaling an active rulemaking agenda, and publicly warning state regulators that the agency will fight to protect its exclusive jurisdiction. At the same time, the financial interests of the first family are directly entangled with the outcome of that institutional posture — a conflict that bipartisan state attorneys general, casino industry lobbyists, and members of Congress from both parties have placed publicly on the record.

MindCast’s Legislative Regime Conversion and the Collapse of Preemption, published March 25, 2026, identified the precise mechanism by which the administration’s posture becomes structurally insufficient regardless of its intensity: the Statutory Category Exclusion Mechanism (SCEM) — a legislative instrument that converts definitional ambiguity into express statutory prohibition, foreclosing the judicial and administrative channels that depend on that ambiguity to function. No CFTC rulemaking authorizes what Congress has expressly prohibited. The administration’s ability to shield Kalshi through regulatory posture terminates the moment Congress eliminates the statutory ambiguity the posture depends on. Within the party, governors and senators have already broken from the CFTC’s position, and the casino industry — long aligned with Trump — now actively lobbies against prediction markets through a former Trump budget director.

CFTC Chair Michael Selig has been the administration’s primary instrument. In a Wall Street Journal opinion piece, Selig wrote that the CFTC would “no longer sit idly by while overzealous state governments undermine the agency’s exclusive jurisdiction over these markets.” On February 17, 2026, the CFTC filed a friend-of-the-court brief in the Nevada appellate proceeding, as reported by PBS NewsHour and the New Republic. On January 29, 2026, at a joint summit with the Securities and Exchange Commission (SEC), Selig announced a four-part regulatory agenda and formally withdrew a prior proposed rule that would have prohibited sports and political event contracts, per Sidley Austin’s analysis of the summit.

The family conflict of interest sits at the center of the administration’s posture. Trump’s eldest son, Donald Trump Jr., is a paid strategic adviser to both Kalshi and Polymarket simultaneously, according to reporting by NPR, CNN, and the Washington Times. Truth Social — the president’s own media platform — is launching a cryptocurrency-based prediction market called Truth Predict, per CNN’s reporting on the Trump family’s prediction market business interests. Any favorable CFTC decision directly benefits businesses in which the president’s family holds advisory and financial stakes. The CFTC’s own spokesperson told CNN that Selig has never spoken with Trump Jr. about prediction markets — but the structural alignment between first-family financial interests and agency posture is a matter of public record, not speculation.

Selig’s position shifted materially from his confirmation hearing posture, at which he told senators it would be best for the CFTC to defer to the courts, per PLANADVISER’s reporting on the November 2025 Senate Agriculture Committee hearing. He has since moved to actively intervene on Kalshi’s behalf in ongoing appellate litigation while simultaneously advancing rulemaking that would embed the administration’s preferred classification into agency regulation before any appellate court resolves the question.

Republican pushback has emerged and is growing. Utah Governor Spencer Cox publicly challenged Selig: “Mike, I appreciate you attempting this with a straight face, but I don’t remember the CFTC having authority over the ‘derivative market’ of LeBron James rebounds. These prediction markets you are breathlessly defending are gambling — pure and simple,” per PBS NewsHour. The bipartisan Prediction Markets Are Gambling Act (PMAGA) — co-sponsored by Democratic Sen. Adam Schiff and Republican Sen. John Curtis — would amend the CEA to bar the CFTC from permitting sports event contracts. The casino industry has hired former Trump budget director Mick Mulvaney to lobby against prediction markets, per Front Office Sports, while established casino operators have moved slowly — their prior alignment with Trump explaining the hesitation, according to Rep. Dina Titus as reported by CNN.

V. Consolidation: Formal and Functional

Whether the sprawling Kalshi litigation will consolidate into a single proceeding is among the most consequential structural questions in the entire map — and the answer requires separating two distinct mechanisms: formal Multi-District Litigation (MDL) consolidation, which concentrates cases before a single federal district judge, and functional appellate convergence, which is already occurring across four circuit courts without any formal order.

MDL consolidation is structurally unlikely in the near term. The Kalshi litigation does not map cleanly onto MDL because the cases involve fundamentally different plaintiffs — state attorneys general, tribal governments, and private class plaintiffs — advancing different legal theories across different forums. State gambling law preemption, consumer protection claims, the Indian Gaming Regulatory Act (IGRA) — the federal statute governing gambling on tribal lands — and common law recovery each require distinct analysis. No party has moved for MDL consolidation and no judicial panel has signaled interest in one.

Appellate convergence is the functional substitute. The preemption question is ascending to multiple circuit courts on parallel tracks:

Third Circuit — New Jersey (Kalshi win at district level); oral arguments held Sep 10, 2025; ruling pending

Fourth Circuit — Maryland (state win at district level); oral arguments May 7, 2026; Neal Katyal representing Kalshi

Sixth Circuit — Ohio and Tennessee on separate tracks, creating an intra-circuit split (Ohio ruled for state, Tennessee ruled for Kalshi); Ohio briefing runs through Jun 2026

Ninth Circuit — Nevada; consolidated oral arguments for Kalshi, Robinhood, and Crypto.com scheduled Apr 16, 2026

A circuit split across all four produces Supreme Court certiorari pressure that becomes nearly irresistible. The Massachusetts SJC’s direct review adds a fifth track — a state supreme court ruling on the preemption question that will itself be certworthy if it contradicts the federal circuit decisions.

Class action litigation has already consolidated in the Southern District of New York (SDNY). The nationwide class action against Kalshi has consolidated the Yee, Pelayo, and Hallman cases, with the Alabama class action moved to SDNY and consolidated March 20, 2026, per Mick Bransfield’s litigation tracker. Plaintiff motions are due May 5, 2026. The SDNY consolidation creates a single large consumer-side litigation vehicle that will produce discovery pressure independent of the regulatory proceedings — and whose plaintiff theory, that Kalshi violated state gambling laws and misled consumers about its platform, directly parallels the Washington complaint’s Consumer Protection Act theory filed today.

Formal consolidation remains structurally unlikely before an appellate ruling resolves the preemption question. The Regulatory Split probability model now places the downside scenario — gambling classification locking in — at P45, elevated from the original P35, making it the modal outcome rather than a tail risk. The more consequential question is whether the Fourth or Ninth Circuit rules first — and whether those rulings conflict sharply enough to accelerate Supreme Court certiorari. Each day that Kalshi’s voluntary behavioral concessions — blocking politicians and athletes from trading — persist without a court order functions, under the Prospective Repeated Game Architecture (PRGA) framework established in MindCast AI Emergent Game Theory Frameworks, as a quasi-admission that the classification question is unresolved in Kalshi’s own operational judgment. Platforms know their own legal position better than external observers. The concession is the signal.

VI. The Legislative Coalition: Who Is Backing Federal Action and What They Actually Said

The legislative push against prediction markets has attracted a coalition spanning state legislatures, tribal governments, the established gaming industry, and college athletics — a breadth of opposition that gives the Prediction Markets Are Gambling Act (PMAGA) and its House companion unusual institutional weight even at early stages of the legislative process. MindCast’s Legislative Regime Conversion and the Collapse of Preemption identified the SCEM as the mechanism that forecloses appellate resolution by eliminating statutory ambiguity at its source. Understanding who is backing federal action, what they have actually said on the record, and where the claims about coalition breadth are verified versus overstated is essential to modeling whether the legislative track produces that mechanism. What follows distinguishes confirmed institutional positions from unverified assertions.

The National Conference of State Legislatures (NCSL) — the bipartisan organization representing the legislatures of all fifty states — formally wrote to Congress urging action on unregulated sports betting via prediction markets. The letter, addressed to Senate Banking Committee Chair Tim Scott and dated February 6, 2026, is a matter of public record. The NCSL also published a dedicated policy brief titled Prediction Markets: A New Frontier in State Regulatory Authority to inform state legislators and staff on the legal landscape and available policy levers. The tax revenue dimension is real and documented: state regulators across eleven states have argued that prediction markets function as unlicensed sports betting platforms that cost states over $600 million in sports betting tax revenue, according to analysis by MultiState.

The Indian Gaming Association (IGA) — representing tribal gaming operators who hold exclusive gambling rights in many states — has been among the most vocal institutional supporters of both pieces of legislation. IGA Chairman David Bean issued a formal statement when the PMAGA was introduced, stating the bill would “quiet the chaos and federal overreach that the CFTC is fostering” while reaffirming existing tribal and state government authority to regulate sports betting and limit online gambling, per the IGA’s official press release at indiangaming.com. Bean has also said: “It is no coincidence that prediction market corporations selected the smallest and weakest financial regulatory agency to push out their self-certified, self-regulated online gambling platforms,” per CDC Gaming. The IGA has taken tribal leaders to Capitol Hill for direct Senate briefings on the issue, per CDC Gaming’s reporting, and tribal organizations joined the legal brief supporting the Ho-Chunk Nation of Wisconsin’s federal lawsuit against Kalshi and Robinhood.

The American Gaming Association (AGA) — the primary trade group for the legal casino industry — issued a joint statement with the IGA welcoming the introduction of the PMAGA, calling on Congress to stop sports betting and casino gambling operating under the guise of event contracts, per iGaming trade press coverage of the bill’s introduction. The AGA’s position is complicated by the fact that its member sportsbooks — DraftKings, FanDuel, Fanatics — have themselves launched prediction market products, creating an industry posture that is internally divided even as the association formally opposes Kalshi’s unregulated expansion.

The House companion legislation, the Event Contract Enforcement Act (ECEA), was introduced by Reps. Blake Moore (R-UT) and Salud Carbajal (D-CA) on March 6, 2026, per Moore’s official House press release. The ECEA is structurally distinct from the Senate bill in one significant respect: rather than a flat ban on sports event contracts, the ECEA includes a state opt-out provision allowing individual states to exempt themselves from the gaming contract prohibition and choose whether to allow sports-related contracts within their borders. The California Nations Indian Gaming Association (CNIGA) commended Moore and Carbajal upon introduction, calling the ECEA “critical federal legislation to address illegal sports betting conducted through so-called ‘prediction markets,’” per Gambling Insider’s coverage.

NCAA President Charlie Baker has taken the strongest named institutional position in sports governance. Baker issued a statement saying the NCAA is “vehemently opposed” to prediction markets for college sports, per ESPN and CBS Sports, characterizing the pressure on student-athletes as unacceptable. In March 2026, Baker sent a four-page letter to CFTC Chair Selig demanding a full suspension of college sports prediction markets until safeguards are in place, including geolocation tracking, mandatory integrity monitoring comparable to licensed sportsbooks, and suspicious activity reporting requirements, per Sportico’s reporting. Selig has not publicly responded to either the January or March Baker letters.

What is not confirmed: Claims that Arnold Ventures has formally backed either bill, that Public Citizen or Americans for Financial Reform have publicly joined the coalition, and that Senator Catherine Cortez Masto has formally co-sponsored or publicly endorsed the PMAGA do not appear in verifiable sources as of March 27, 2026. MindCast excludes these from the confirmed coalition record. Similarly, the “39 state attorneys general coalition” framing overstates what is documented: more than thirty-six states filed amicus briefs supporting state authority in the Fourth Circuit proceeding — a procedural filing, not a formal coalition endorsement of federal legislation.

The lobbying counterpressure is substantial. Kalshi spent at least $1 million on lobbying in 2025 — a record for the company — and has since helped launch the Coalition for Prediction Markets alongside Robinhood, Coinbase, Crypto.com, and Underdog. The venture capital network backing prediction markets includes Peter Thiel and Marc Andreessen. Former Trump budget director Mick Mulvaney has made public statements in favor of some legislative action, but casino operators themselves have moved slowly — their prior alignment with Trump complicating their willingness to actively oppose his administration’s regulatory posture.

VII. What Is Going in Kalshi’s Favor: Supporters, Court Wins, and Capital

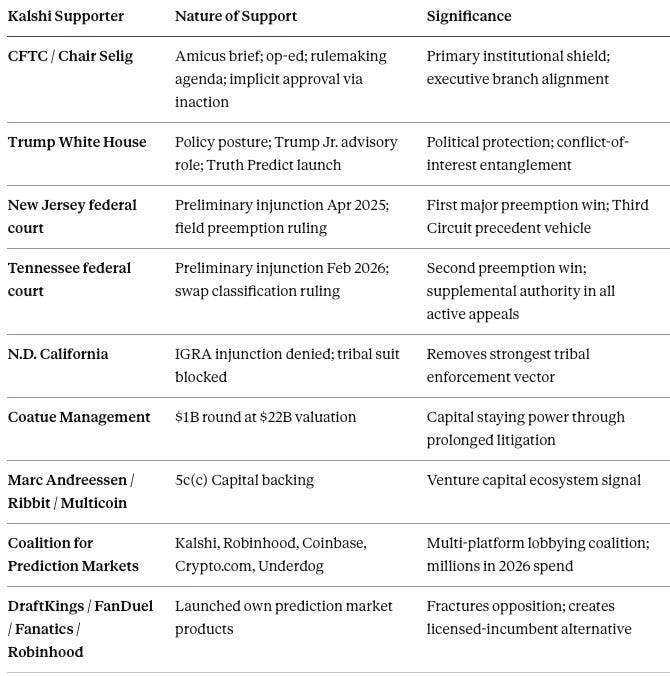

The litigation map and legislative coalition documented in prior sections create a misleading impression if read without the countervailing picture. Kalshi is simultaneously facing the most aggressive multi-state enforcement wave in prediction market history and has raised $1 billion at a $22 billion valuation per Bloomberg and the Wall Street Journal. The company has won preliminary injunctions in two federal district courts, secured the full backing of the executive branch’s regulatory apparatus, and attracted a capital coalition that includes some of the most influential figures in venture capital and fintech. MindCast’s Prediction Markets and the Regulatory Split assigned the upside case — federal derivatives framework prevailing — P20 at publication. Understanding what sustains that probability requires mapping Kalshi’s actual support structure with the same precision applied to its opposition.

The CFTC is Kalshi’s most consequential institutional backer. The agency’s posture under Chair Michael Selig has moved from neutrality to active intervention. In February 2026, the CFTC filed a friend-of-the-court brief in the Nevada appellate proceeding asserting exclusive federal jurisdiction over prediction market event contracts. Selig published a Wall Street Journal op-ed warning state regulators the agency would no longer tolerate what he characterized as overreach into federal jurisdiction. The CFTC also formally withdrew the prior proposed rule that would have prohibited sports and political event contracts — removing the regulatory ceiling that had constrained Kalshi under the Biden administration.

Critically, the agency’s January 2025 decision not to prohibit Kalshi’s sports contracts after self-certification — taking no action while retaining the authority to act — has been used by multiple federal courts as evidence of implicit federal approval. The Tennessee federal court specifically cited the CFTC’s inaction as grounds for finding Kalshi likely to succeed on preemption, per Legal Sports Report’s analysis of the February 2026 ruling: the agency had reviewed the contracts and chose not to block them, which is itself an exercise of the exclusive jurisdiction Kalshi claims.

Two federal district courts have granted Kalshi preliminary injunctions on the preemption theory. The New Jersey federal court held in April 2025 that Kalshi’s event contracts fall within the CFTC’s exclusive jurisdiction and that the CEA preempts New Jersey’s attempt to classify them as unauthorized sports wagers, per Holland & Knight’s analysis of the ruling. The court found Kalshi demonstrated a strong likelihood of success on the merits and would suffer irreparable harm from state enforcement.

The Tennessee federal court reached the same conclusion in February 2026, finding that Kalshi’s sports contracts likely qualify as swaps — financial instruments whose value derives from an underlying variable, here a sporting event outcome — under federal law, per Legal Sports Report’s analysis of Judge Trauger’s ruling. A swap classification would place Kalshi’s contracts squarely within CFTC exclusive jurisdiction and outside state gambling authority entirely. The Tennessee ruling specifically rejected the Maryland court’s conflict preemption analysis and held that requiring Kalshi to comply with both federal and state frameworks would undermine the uniform congressional framework the CEA was designed to establish. Kalshi has filed the Tennessee ruling as supplemental authority in the Third Circuit, the Fourth Circuit, and every other active appellate proceeding — each favorable ruling becoming ammunition in the next jurisdiction.

The Northern District of California delivered a separate Kalshi win on tribal grounds. The tribal lawsuit in California, brought under the IGRA, was rejected at the injunctive relief stage: the court held that IGRA does not apply to third-party platforms like Kalshi and that federal law expressly exempts CFTC-regulated transactions from the illegal internet gambling prohibition, per Epstein Becker Green’s litigation analysis. The California tribal suit continues on other grounds, but the IGRA injunction denial removed the most immediately threatening tribal enforcement vector.

The capital behind Kalshi is structurally significant and growing. Kalshi raised more than $1 billion at a $22 billion valuation — more than double its $11 billion valuation from four months prior — in a round led by Coatue Management, according to Bloomberg and the Wall Street Journal. Polymarket is simultaneously eyeing a $20 billion valuation. The joint venture capital fund 5c(c) Capital, launched March 23, 2026, is backed by Kalshi CEO Tarek Mansour, Polymarket CEO Shayne Coplan, Marc Andreessen through Moneta Luna, Ribbit Capital founder Micky Malka, and Kyle Samani of Multicoin Capital, per Fortune and Bloomberg reporting on the fund’s launch — a cross-industry signal that institutional capital views prediction markets as a durable asset class regardless of the current litigation environment.

The Coalition for Prediction Markets — a lobbying organization whose members include Kalshi, Robinhood, Coinbase, Crypto.com, and Underdog — is led by Sean Patrick Maloney, a former ten-year Member of Congress (NY-18) and former U.S. Ambassador to the OECD in Paris, who has served as the Coalition’s Chief Executive Officer since January 2026 per his LinkedIn profile. Three months after launch, the Coalition’s LinkedIn page shows 101 followers and its Facebook page shows 11 — a footprint that reveals where the money is actually going: into lobbying and litigation infrastructure, not public persuasion. Kalshi spent a record $1 million on lobbying in 2025 alone, according to Sportico, engaging firms with direct Trump administration ties: Miller Strategies LLC (whose homepage features a testimonial from Donald Trump Jr.) and Lincoln Policy Group, whose leader former Sen. Blanche Lincoln — who once told the CFTC sports event contracts served no commercial purpose — reversed course and wrote the CFTC a public letter supporting Kalshi’s sports betting expansion, also per Sportico. Pantera Capital led a $75 million Series B round in sports prediction market startup Novig at a $500 million valuation in February 2026, according to Sportico and Fortune — further evidence that institutional capital is treating prediction markets as a durable asset class rather than a regulatory casualty in waiting.

DraftKings, FanDuel, Fanatics, and Robinhood have entered the prediction market space. Each of the regulated sportsbook incumbents — simultaneously lobbying against Kalshi through the AGA — has launched its own prediction market products, creating a contradiction at the heart of the opposition coalition. The institutional willingness of these companies to enter the space while opposing Kalshi signals that the regulatory outcome they seek is not prohibition of prediction markets but redirection of market share toward licensed incumbents — a strategic posture that could fracture the opposition coalition if Congress produces a framework that licenses event contracts rather than banning them.

The statutory interpretation argument has genuine legal force. The CEA’s definition of “swap” is notably expansive, and the Tennessee court’s February 2026 ruling turned on a careful reading of whether sports event outcomes constitute “occurrences” under the statutory definition — finding they do, in direct contradiction of the Nevada court’s earlier reading. Two federal judges have read the same statute and reached opposite conclusions about the same contracts. The legal ambiguity is structural, not manufactured by Kalshi’s lawyers. The economics professor who studies prediction markets and told NPR the case will likely require Supreme Court or congressional resolution was Koleman Strumpf of Wake Forest University. MindCast maintains P20 on the upside scenario not because the litigation landscape favors Kalshi but because the legal argument has real merit and the capital, regulatory, and political support behind it is among the most concentrated in any current regulatory dispute in the United States.

VIII. Nash-Stigler Equilibrium and Chicago School Accelerated: Why Each Actor Behaves as It Does

The litigation map documented in Sections II through VII is accurate but incomplete without a governing analytical framework that explains not just what is happening but why each actor’s behavior is structurally predictable — and what that predictability implies for how the conflict resolves. Two MindCast frameworks apply directly: The Dual Nash-Stigler Equilibrium Architecture, which explains why the CFTC’s accommodating posture is the rational institutional endpoint rather than an aberration, and the Chicago School Accelerated — The Integrated, Modernized Framework of Chicago Law and Behavioral Economics framework, which explains why the incumbent sportsbook industry’s opposition to Kalshi is a barrier-to-entry strategy disguised as consumer protection advocacy.

Named for mathematician John Nash — whose 1950 non-cooperative game theory established that actors in competition reach predictable equilibria from which no single player benefits by deviating — and economist George Stigler — who demonstrated in the 1970s that regulatory agencies systematically migrate toward accommodation with the industries they oversee — the Nash-Stigler Equilibrium describes capture not as corruption but as the rational endpoint of incentive geometry. Runtime Geometry, A Framework for Predictive Institutional Economics defines the equilibrium precisely: when oversight is concentrated at a small agency with thin resources and concentrated industry relationships, visible accommodation generates positive signals while genuine correction consumes resources, creates enemies, and produces uncertain outcomes. The referee and the player reach a strategic stalemate that benefits both at the expense of everyone else.

A. The Nash-Stigler Equilibrium: Why the CFTC Cannot Be a Neutral Arbiter

The CFTC under Chair Michael Selig has moved from neutrality to active intervention on Kalshi’s behalf — filing amicus briefs, publishing op-eds, withdrawing proposed prohibitions, and signaling imminent rulemaking to entrench federal jurisdiction. The standard interpretation treats this as ideological preference for deregulation or political alignment with the Trump administration.

The Nash-Stigler analysis identifies the deeper structural mechanism: Kalshi and its peers deliberately chose the CFTC as their regulatory home precisely because its structural profile — smallest federal financial regulator, most expansive statutory language, least enforcement capacity — produces accommodation as the dominant strategy. As Runtime Geometry establishes, the prediction markets industry selected the agency with the structural geometry most likely to produce favorable stalemate.

The Nash-Stigler diagnosis generates a specific falsifiable prediction: the CFTC will not produce a formal rulemaking that creates enforceable substantive restrictions on prediction market sports contracts before the Fourth Circuit issues a preemption ruling. The rulemaking Selig has signaled will either stall in the single-commissioner institutional vacuum — all four remaining commissioner seats are vacant — or produce guidance so permissive it functions as a shield rather than a constraint. If the Fourth Circuit rules against Kalshi, the Nash-Stigler equilibrium breaks — external appellate force is precisely the mechanism Runtime Geometry identifies as the condition under which captured stability becomes unstable. If the Fourth Circuit rules for Kalshi, the equilibrium locks in further and Supreme Court certiorari becomes the only remaining external force capable of disrupting it.

The Segmentation Condition — established in MindCast AI Emergent Game Theory Frameworks — compounds the Nash-Stigler diagnosis. Named for the structural feature it measures, the Segmentation Condition holds when the cost for any audience to observe cross-forum contradictions exceeds the enforcement benefit of doing so, producing an environment in which the CFTC can assert exclusive jurisdiction in federal court filings while simultaneously declining to produce the rulemaking that would give that jurisdiction substantive content. No single court, state regulator, or congressional committee currently possesses the cross-forum aggregation capability to hold the CFTC accountable for that gap. MindCast’s cross-forum architecture is specifically designed to detect and publish exactly this gap — which is why this publication exists.

B. Chicago School Accelerated: The Incumbent Sportsbook Strategy as Barrier to Entry

Named for the University of Chicago tradition of applying economic logic to law and social behavior — running from Ronald Coase on transaction costs through Gary Becker on rational incentive response to Richard Posner on institutional efficiency — the Chicago School Accelerated framework, developed in Chicago School Accelerated — The Integrated, Modernized Framework of Chicago Law and Behavioral Economics, establishes that behavior follows payoff gradients regardless of moral valence or stated rationale. The Becker pillar is the relevant instrument here: given the incentive structure actors face, what behavior maximizes expected returns? The answer reveals the incumbent sportsbook industry’s opposition to Kalshi as a classic barrier-to-entry strategy, not a principled consumer protection campaign.

DraftKings, FanDuel, Fanatics, and Robinhood have each launched prediction market products while simultaneously opposing Kalshi through the AGA. The AGA’s joint statement with the IGA calls for Congress to stop sports betting conducted through event contracts — a position each AGA member is simultaneously pursuing in its own product roadmap.

The Becker lens resolves the apparent contradiction immediately: the incumbents are not opposed to prediction markets. They are opposed to prediction markets operated by Kalshi under a regulatory framework that does not require the state-by-state licensing, tax payments, and regulatory compliance costs the incumbents have already absorbed. The strategy converts sunk regulatory compliance costs into a competitive moat — using the legislative process to impose on Kalshi the same cost structure the incumbents have already paid.

The Posner pillar adds the institutional learning dimension. Chicago School Accelerated, Part III: Posner and the Economics of Efficient Liability Allocation establishes that legal frameworks evolve toward efficiency — but with a lag that is itself a strategic resource. The incumbent sportsbooks have spent more than a decade building state-by-state licensing relationships, tribal compact arrangements, and tax remittance infrastructure. Kalshi entered in January 2025 and achieved $22 billion in valuation within fourteen months by bypassing that entire cost structure.

The Posnerian reading is that the regulatory framework is inefficient — it prices the same product differently depending on how it is labeled — and the legal system is now generating the pressure required to move toward a more efficient classification. The incumbents’ Beckerian strategy is to capture that correction process and direct it toward a licensed-incumbent outcome rather than a prohibition outcome. That is why DraftKings, FanDuel, and Fanatics are simultaneously inside the prediction market space and lobbying against Kalshi’s version of it.

C. Integrated Forward Predictions With Probability Bands and Measurement Windows

Six Cognitive Digital Twin (CDT) foresight simulations — MindCast’s proprietary analytical methodology, which models each institutional actor as a behavioral replica encoding objective functions, constraint stacks, and feedback sensitivities, then runs those replicas against one another to generate ranked causal findings and probability-banded predictions — converge on four ranked causal findings. Structural geometry ranks first: existing state gambling statutes create the shortest enforcement path, and states do not need new legal categories to act. Strategic delay ranks second: Kalshi benefits from parallel litigation, appellate fragmentation, and interim relief asymmetry. Feedback inversion ranks third: enforcement actions often create appellate signals Kalshi recycles as preemption ammunition in the next forum. Institutional throughput failure ranks fourth: the federal system cannot update classification fast enough to match platform expansion.

Prediction 1 — Nash-Stigler stalemate holds through Fourth Circuit: The CFTC produces no formal rulemaking with substantive sports contract restrictions before the Fourth Circuit issues its Maryland ruling. P10: 62% | P50: 79% | P90: 89% Measurement window: May 7, 2026 oral arguments through ruling date. Falsification condition: CFTC issues proposed rule with enforceable sports contract restrictions before ruling.

Prediction 2 — Incumbent sportsbook strategy shifts toward licensed participation post-legislation: If the PMAGA or ECEA advances to a floor vote, DraftKings, FanDuel, or Fanatics withdraws from AGA categorical opposition or publicly endorses a licensed prediction market framework. Incumbents are likely to redirect from opposition to controlled participation once a licensing path emerges, but the timing of that shift is a forecast rather than a proven fact. P10: 49% | P50: 66% | P90: 80% Measurement window: within 6 months of credible federal or state licensing framework development. Falsification condition: incumbents maintain categorical opposition to prediction markets after a viable licensed pathway emerges.

Prediction 3 — Kalshi preserves operational continuity through selective concessions rather than categorical retreat: Kalshi’s voluntary behavioral concessions expand to additional contract categories within 60 days of the Washington complaint filing, functioning as pre-positioning for a licensed compliance framework rather than acknowledgment of gambling classification risk. P10: 58% | P50: 76% | P90: 87% Measurement window: June 1, 2026.Falsification condition: Kalshi reverses or abandons voluntary concessions, or publicly concedes gambling classification risk.

Prediction 4 — Circuit split produces cert petition by Q4 2026: If the Fourth Circuit and the Ninth Circuit issue rulings on opposite sides of the preemption question — which MindCast assigns high structural likelihood given the current district court split — Kalshi files a certiorari petition before December 31, 2026. P10: 56% | P50: 73% | P90: 85% Measurement window: through Q4 2026. Falsification condition: both circuits rule in the same direction, removing the split that drives cert pressure.

IX. Cybernetics Applied: Feedback Loop Degradation and the Viable System Threshold

Nash-Stigler explains why the CFTC accommodates Kalshi. Chicago School Accelerated explains why incumbents oppose Kalshi strategically rather than categorically. What neither framework addresses directly is the system-level question: has the federal regulatory architecture governing prediction markets already degraded past the point of self-correction — and if so, what external force is required to restore viable feedback?

Cybernetics — the science of control and communication in complex systems, originating with mathematician Norbert Wiener’s 1948 work and developed through Ross Ashby, Stafford Beer, and Gregory Bateson — answers that question by modeling regulatory systems as feedback loops and diagnosing whether those loops are functioning, degraded, or inverted. MindCast developed its cybernetics application across three publications: the MindCast Predictive Cybernetics Suite, Predictive Institutional Cybernetics, and The Cybernetic Foundations of Predictive Institutional Intelligence. Applied to the Kalshi litigation, the cybernetics architecture reveals a system that has not merely drifted — it has undergone a structural regime transition in which the feedback loops designed to regulate the system are now encoding and amplifying the very distortions they were built to correct.

A. Ashby’s Law of Requisite Variety and the CFTC’s Capacity Failure

Ross Ashby’s Law of Requisite Variety — published in An Introduction to Cybernetics (1956) — holds that a control system must match the complexity of the system it regulates. Regulatory variety, meaning the range of responses an agency can deploy, must be at least equal to the variety of behaviors the regulated system can produce. When regulatory variety falls below the threshold required to govern the system, the control architecture fails not because regulators are incompetent but because the instrument is structurally insufficient for the system it is trying to govern.

Predictive Institutional Cybernetics operationalizes Ashby’s Law through MindCast’s CDT methodology. Applied to the CFTC, the CDT profile reveals a catastrophic requisite variety failure. The agency has one sitting commissioner — all four remaining seats are vacant, with no new nominations announced, as WilmerHale and Cointelegraph both confirmed following Selig’s December 2025 swearing-in. It operates with approximately 540 full-time staff — roughly one-eighth the workforce of the Securities and Exchange Commission — against the regulatory complexity of a market that processed $22.88 billion in trading volume in 2025 alone, a 1,108% year-over-year increase according to Sacra, operating in all fifty states simultaneously, with sports contracts accounting for 89% of Kalshi’s 2025 fee revenue. The behavioral variety Kalshi can produce — new contract categories, new market structures, new jurisdictional arguments, new lobbying configurations — massively exceeds the regulatory variety the CFTC can deploy in response. Ashby’s Law predicts that a control system in this condition will not regulate the system — it will be absorbed by it. The CFTC’s posture under Selig is not ideological capture alone. It is the predictable output of a control system operating far below the requisite variety threshold.

B. Wiener’s Feedback Loop Architecture and the Inversion Condition

Norbert Wiener demonstrated that intelligent behavior in any system — biological, mechanical, or institutional — depends on feedback mechanisms that detect deviation from a desired state and generate corrective signals. When feedback loops function, systems self-regulate. When feedback loops are inverted, systems drift without correction and eventually reach a state where deviation from the desired condition becomes the stable equilibrium.

The Kalshi litigation has produced precisely that inversion condition: the feedback mechanisms designed to correct regulatory drift are now operating in reverse. Consider the circuit. State regulators file enforcement actions — the feedback signal that Kalshi’s activity violates gambling law. Kalshi responds by filing preemptive federal lawsuits, which shift the correction mechanism from state enforcement to federal court, where the CFTC’s friend-of-the-court brief reinforces Kalshi’s position. The federal court in Tennessee issues a preliminary injunction blocking state enforcement — which Kalshi immediately files as supplemental authority in every other active proceeding, using the corrective signal (a court ruling) to suppress the original error signal (state enforcement). Each state enforcement action that reaches a favorable federal court strengthens Kalshi’s preemption argument in the next jurisdiction. The correction mechanism is feeding the distortion.

The system class produced by this diagnosis is a semi-closed loop control system with inversion pressure: not fully closed because Congress, state courts, appellate courts, and tribal suits continue to inject external shocks, but closed enough for Kalshi and the CFTC to convert partial victories into broader strategic leverage. The single causal chain linking all three cybernetic thinkers runs precisely here: low regulatory variety weakens loop closure; weak loop closure permits inversion; inversion raises the probability of external structural intervention as the only remaining path to restored feedback integrity.

The Cybernetic Foundations of Predictive Institutional Intelligence identifies Gregory Bateson’s recursive learning levels as the diagnostic tool for this condition — distinguishing three types of institutional response. Learning I is surface behavioral adjustment: Kalshi’s voluntary blocking of politicians and athletes from trading. Learning II is changing the rules governing responses: what the PMAGA attempts by amending the CEA to eliminate the statutory ambiguity that allows the inversion to persist. Learning III is restructuring the system itself: what a Supreme Court ruling on federal preemption or a congressional overhaul of the CFTC’s enabling statute would accomplish. Learning I responses cannot resolve a Learning III structural condition. Kalshi’s behavioral concessions are Learning I outputs deployed against a Learning III problem — they will not stabilize the feedback loop but will signal to sophisticated institutional observers that Kalshi has correctly classified the depth of the systemic problem and is pre-positioning for statutory survival rather than claiming the existing system works.

C. Beer’s Viable System Model and the Five-Layer Causation Stack

Stafford Beer’s Viable System Model (VSM) — developed in Brain of the Firm (1972) — identifies the structural conditions a system must satisfy to remain viable, meaning capable of self-regulation and adaptation under environmental pressure. The VSM specifies five systems that must all function: operations (System 1), coordination (System 2), control (System 3), intelligence (System 4), and policy (System 5). When multiple systems fail simultaneously, the system cannot recover through internal means alone.

Predictive Institutional Cybernetics operationalizes the VSM through MindCast’s five-layer causation stack — Event, Incentive, Feedback Loop, Structural Geometry, Identity Grammar — which maps directly onto the VSM’s functional layers. Applied to the federal prediction market regulatory architecture, the VSM diagnosis is precise:

System 1 (Operations) — functioning but fragmented. Kalshi operates across all fifty states while sixteen states take enforcement action. Operations continue despite enforcement pressure because federal preemption injunctions in New Jersey and Tennessee create safe harbors that operations exploit.

System 2 (Coordination) — severely degraded. No coordination mechanism exists between state gambling regulators, the CFTC, federal courts in four circuits, tribal governments, and Congress. Each actor sends independent signals that other actors cannot aggregate into coherent regulatory direction. The Segmentation Condition from MindCast AI Emergent Game Theory Frameworks is the mechanism producing System 2 failure: cross-forum observation costs exceed enforcement benefits, so no actor maintains the full picture.

System 3 (Control) — captured. The CFTC is formally the System 3 control layer for prediction markets. Its actual behavior — filing amicus briefs defending Kalshi, signaling rulemaking favorable to expansion, declining to prohibit self-certified sports contracts — is not control behavior. The Nash-Stigler Equilibrium has converted the System 3 control layer into an amplifier of the distortion it is designed to regulate.

System 4 (Intelligence) — absent at the system level. No institution currently performs cross-forum intelligence aggregation across all active proceedings, legislative tracks, lobbying records, and appellate timelines simultaneously. Congress legislates without full visibility into what courts are doing. Courts rule without full visibility into what Congress is considering. The CFTC asserts jurisdiction without full visibility into what state courts are ordering.

System 5 (Policy) — contested. The policy layer — what prediction markets are and whether they are permitted — is the precise question four circuit courts, Congress, and the CFTC are all attempting to answer simultaneously through incompatible mechanisms. A viable system has one System 5. The prediction market regulatory system currently has at least six competing System 5 actors issuing incompatible policy determinations from incompatible authority bases.

The VSM diagnosis is unambiguous: the federal prediction market regulatory architecture is not viable in its current form. External force — either a definitive appellate ruling or a congressional amendment — is the minimum intervention required to restore viability. MindCast Predictive Cybernetics Suite establishes that systems operating below the viable system threshold do not stabilize through accumulated incremental actions. They require a structural intervention at the Identity Grammar layer — the deepest layer of the five-layer causation stack — which in institutional terms means a change in the legal classification regime itself, not a change in how actors behave within it.

D. Cybernetic Forward Predictions: Structural Intervention Required by Q3 2027

The cybernetics framework produces system-level forward predictions that the game theory and Chicago School analyses do not. The system cannot self-correct through internal feedback alone. The federal architecture is not merely contested — it is throughput-constrained. Federal institutional lag is actively helping preserve the very fragmentation Congress claims to dislike. Every month the classification question remains unresolved, Kalshi normalizes further, capital accumulates further, and the political cost of categorical reversal rises further. The conflict is a contest over institutional control architecture, and the throughput failure of federal institutions is helping the defendant more than any court ruling.

Cybernetic Prediction 1 — Internal federal correction remains insufficient through Q1 2027: The CFTC’s behavior — amicus briefs, nonfinal rulemaking signals, and case-by-case relief — is structurally explainable without concluding bad faith: resource scarcity, concentrated industry relationships, and institutional incentive geometry all produce accommodation as the dominant output. Definitive CFTC rulemaking imposing real substantive restrictions before an appellate forcing event would falsify this prediction. P10: 62% | P50: 79% | P90: 89% | Window: through Q1 2027.Falsification condition: definitive CFTC rulemaking imposes enforceable substantive restrictions on sports contracts before the Fourth Circuit rules.

Cybernetic Prediction 2 — External intervention becomes necessary for restored loop integrity: Neither the CFTC alone, nor state enforcement alone, nor any single appellate ruling can restore coherent System 5 policy control. Coherent and durable lower-court or agency-led settlement without higher-order intervention would falsify this prediction. P10: 57% | P50: 74% | P90: 86% | Window: Q4 2026 to Q3 2027. Falsification condition: coherent and durable lower-court or agency-led settlement without higher-order intervention.

Resolution arrives through exactly three forms. First: a Supreme Court certiorari grant resolves the preemption question definitively, restoring System 5 policy coherence. Second: a congressional amendment through the PMAGA or ECEA eliminates the statutory ambiguity driving the inversion, restoring System 3 control through a mechanism external to the captured CFTC. Third: a complete circuit split produces such acute System 2 coordination failure that Congress intervenes regardless of lobbying equilibrium.

Falsification condition for Q3 2027 horizon: If the fragmented multi-forum enforcement architecture persists as a stable operational condition past Q3 2027 — with Kalshi continuing to operate under conflicting court orders in different jurisdictions without appellate resolution — the cybernetic viable system prediction is falsified and the system has achieved a non-viable stability the VSM framework did not anticipate. MindCast assigns that outcome low structural likelihood but commits to publishing a formal model revision if it materializes.

X. Control Layer: Who Actually Determines the Outcome

The prior nine sections diagnose the system. Section IX establishes it is non-viable. Section VIII establishes why each actor behaves as it does. Sections II through VII map the full operational landscape. What remains unresolved for all three primary audiences — state attorneys general, federal lawmakers, and investors — is the question that converts analysis into action: who actually controls the outcome, and how does that control shift as the litigation matures?

Control in a non-viable system does not disappear. It migrates — from one actor class to another, through identifiable transition events, on a timeline that is structurally predictable even when procedurally uncertain.

A. Current Control State: Fragmented with Inversion Active

No single actor currently controls the outcome. Control is distributed across at least six institutional actors — state attorneys general, the CFTC, four federal circuit courts, the Massachusetts SJC, Congress, and the capital markets — none of whom possesses sufficient requisite variety to impose resolution unilaterally. The feedback inversion identified in Section IX-B is operating: each state enforcement action that reaches a favorable federal court strengthens Kalshi’s preemption argument in the next jurisdiction, meaning the actors nominally in control of the correction mechanism are involuntarily amplifying the distortion they are trying to correct.

The dominant control dynamic in the current phase is state enforcement velocity versus federal preemption consolidation. States generate enforcement actions faster than Kalshi can obtain federal injunctions to block them. Washington’s filing today is the latest acceleration. But each Kalshi federal court win — New Jersey, Tennessee — simultaneously creates supplemental authority that slows the next state action’s trajectory toward enforcement. The fragmented control state is not stable. It is a race condition: states accumulating enforcement precedent versus Kalshi accumulating preemption precedent, with the circuit courts as the eventual arbiter.

B. Control Transition Paths

Three structurally distinct paths lead from the current fragmented control state to a resolved outcome. Each path transfers control to a different actor class, on a different timeline, with different implications for each audience.

Path 1 — Judicial: Supreme Court certiorari. Control transfers to the Supreme Court when the circuit split becomes acute enough to force a cert grant. The intra-Sixth Circuit split — Ohio ruling for states, Tennessee ruling for Kalshi on the same statutory question — already creates cert pressure within a single circuit. When the Fourth Circuit and Ninth Circuit rule — with Fourth Circuit oral arguments May 7, 2026 and Ninth Circuit consolidated arguments April 16, 2026 — an inter-circuit split becomes structurally probable. Under Path 1, the outcome is binary and permanent: Kalshi’s federal designation either preempts state gambling law nationwide or it does not.

Path 2 — Legislative: Congressional amendment via the Statutory Category Exclusion Mechanism. Control transfers to Congress when the PMAGA or ECEA advances to a floor vote. Under Path 2, the Nash-Stigler Equilibrium at the CFTC becomes irrelevant — express statutory prohibition overrides administrative accommodation regardless of agency posture. The SCEM does not compete with appellate preemption arguments — it eliminates the statutory ambiguity those arguments depend on, as MindCast’s Legislative Regime Conversion and the Collapse of Preemptionestablished. Control under Path 2 rests with the Senate Agriculture Committee, which has jurisdiction over the CFTC, and with the floor vote arithmetic in a Republican-controlled chamber where the administration’s pro-Kalshi posture conflicts with a bipartisan state coalition and growing intra-party pressure from governors like Spencer Cox.

Path 3 — Market: Capital and incumbent reshaping of equilibrium. Control transfers to capital markets and incumbent sportsbooks when the legislative and judicial tracks produce sufficient delay that the industry restructures around the uncertainty. Under Path 3, DraftKings, FanDuel, Fanatics, and Robinhood — all of whom have already launched prediction market products — achieve dominant market positions under state licensing frameworks while Kalshi remains in litigation limbo. The PRGA from MindCast AI Emergent Game Theory Frameworks predicts incumbents drop their opposition the moment a licensed pathway is legislatively encoded, effectively converting the legislative fight into a market entry race. Under Path 3, Kalshi does not lose in court — it loses market share while winning procedural battles.

C. Control Timing Windows

Three sequential windows define when control transitions become structurally possible.

Window 1 — Pre-Fourth Circuit ruling (now through ~Summer 2026). State enforcement velocity dominates. Each new attorney general complaint adds to the enforcement record and raises operating costs for Kalshi. Kalshi’s dominant strategy is to obtain federal injunctions faster than states can file new actions. States’ dominant strategy is to file in jurisdictions where preemption arguments have already failed — Maryland, Ohio, Massachusetts — and build the enforcement record that supports congressional action. Control holder: diffuse, with slight advantage to states as the enforcement-velocity leader.

Window 2 — Post-circuit split, pre-Supreme Court resolution (~Summer 2026 through ~Q1 2027). Once the Fourth and Ninth Circuits rule, the preemption question exists simultaneously in an irreconcilable state across federal circuits. Kalshi can operate under New Jersey and Tennessee injunctions while being blocked in Maryland, Nevada, Massachusetts, and Ohio. Congressional pressure to resolve the split intensifies. The PMAGA and ECEA move from committee posturing to floor-vote calculus. Control holder: Congress, which alone can resolve the ambiguity without waiting for the Supreme Court’s timeline.

Window 3 — Post-legislation or post-Supreme Court resolution (~Q1 2027 and beyond). Either Congress has amended the CEA — transferring control to state licensing frameworks through the ECEA opt-out or prohibiting sports contracts outright through the PMAGA — or the Supreme Court has issued a definitive preemption ruling. Control holder: the actor whose statutory or judicial instrument produces the framework — either Congress or the Supreme Court.

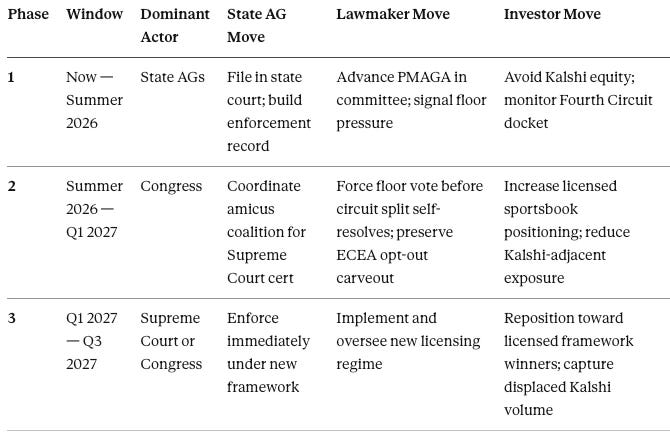

D. Dominant Actor by Phase

E. Forward Lock

If the current structural conditions persist — intra-Sixth Circuit split active, Fourth Circuit ruling imminent, PMAGA advancing in Senate Agriculture Committee, Washington complaint adding a parallel state track today — control shifts from fragmented state enforcement to centralized federal resolution by Q3 2027 regardless of Kalshi’s litigation success in any individual jurisdiction.

The convergence condition does not depend on Kalshi winning or losing. A non-viable system resolves through structural intervention at the Identity Grammar layer — the classification of prediction market event contracts as derivatives or gambling — and that intervention arrives through one of exactly three paths. The path determines who wins. The timing of the path determines how much capital is created or destroyed in the transition.

Prediction market litigation now functions as a contest over institutional control architecture. State attorneys general control near-term enforcement velocity. Federal courts control interim doctrinal leverage. Congress and the Supreme Court alone can impose final classification coherence. Fragmented coexistence can persist for a period. Fragmented coexistence is not the durable endpoint.

State attorneys general maximize leverage in Phase 1 by filing in jurisdictions where preemption has already failed and building the enforcement record. Federal lawmakers maximize leverage in Phase 2 by forcing a floor vote before the circuit split resolves itself — because a Supreme Court ruling forecloses the legislative shaping of the outcome that the ECEA’s state opt-out preserves. Investors maximize returns by positioning toward licensed incumbent sportsbooks in Phase 1, increasing that position as the SCEM advances in Phase 2, and capturing displaced Kalshi volume in Phase 3 regardless of which resolution path prevails.

The system is converging. The control layer determines who shapes the convergence — and on whose terms.

XI. Shadow Antitrust Trifecta: Active Capture Versus Passive Capture

The Shadow Antitrust Trifecta — MindCast’s February 13, 2026 analysis of how three actors replaced evidentiary doctrine with off-docket enforcement routing across HPE-Juniper, Compass-Anywhere, and Live Nation — raises a direct structural question about the Kalshi scenario: are we looking at the same mechanism?

The geometry dominance test answers yes. The Trifecta identified one routing mechanism producing enforcement weakening across three unrelated cases in different industries. The Kalshi scenario runs the same test and passes: one routing mechanism — placing a single-commissioner agency operating far below Ashby’s requisite variety threshold between the platform and state enforcement — produces accommodation as its dominant output across every active proceeding simultaneously, in all fifty states, across four federal circuits. The same Nash-Stigler Equilibrium governs both. The same Segmentation Condition suppresses cross-forum accountability in both. Intent-Outcome Decoupling is elevated in both: stated institutional goals decouple from observable enforcement outputs in a pattern that structural routing explains and individual intent cannot.

Both involve a private access intermediary converting political proximity into enforcement outcomes. In the Trifecta, Mike Davis functions as the intermediary — earning reported million-dollar success fees on the HPE-Juniper settlement and Compass-Anywhere clearance while simultaneously architecting the public narrative that reframed Slater’s ouster. In the Kalshi scenario, Trump Jr.’s simultaneous paid advisory roles at Kalshi and Polymarket — confirmed by NPR, CNN, and the Washington Times — combined with Truth Social’s Truth Predict launch, function as the access channel. Neither intermediary holds a government title. Both convert political proximity into regulatory output while the agency maintains procedural deniability.

The mechanisms diverge at the point that matters most for correction pathway analysis.

The Trifecta operated through active capture via agent substitution — commission, not omission. Career staff were fired. Second Requests were overridden. Gail Slater was removed three weeks before the Live Nation trial. Each act generated discoverable evidence: timestamped narrative coordination, consent decrees without career attorney signatures, deposition targets with documented contradictions. The correction pathway ran through judicial discovery — sworn testimony from Davis, the Mizelle routing record, the Slater deposition. The evidentiary record the Trifecta created is itself the instrument of accountability.

The Kalshi scenario operates through passive capture via structural vacancy — omission, not commission. The CFTC never had an enforcement posture to suppress. Kalshi self-certified its sports contracts in January 2025, the agency took no action, and that inaction has been recycled by federal courts as evidence of implicit federal approval. No one was fired. No Second Request was overridden. Selig can credibly claim at any point that he is waiting for appellate resolution. The accommodation is structural — a control system below requisite variety produces it automatically — which makes it more durable, harder to attack in court, and immune to the deposition-based correction pathway that the Trifecta’s evidentiary record enables.

Three material implications follow from that distinction.

Legal exposure differs. The Trifecta created a transactional record: specific human actors making specific decisions to terminate enforcement already in motion. The Kalshi scenario creates a structural record: an agency whose institutional geometry produces accommodation as its dominant output regardless of individual intent. CFTC inaction is formally lawful. The accommodation is not a scandal — it is an equilibrium.

Correction pathways differ. The Trifecta’s correction runs through discovery and the Tunney Act proceedings before Judge Pitts. The Kalshi correction runs through Congress or the Supreme Court, not discovery, because there is no off-docket channel to expose. The Statutory Category Exclusion Mechanism (SCEM) is the corrective instrument in the Kalshi scenario — not a deposition.

Stability differs. The Trifecta equilibrium was personnel-dependent and therefore fragile. Remove Davis, replace Blanche, and the routing mechanism loses its human nodes. The Kalshi equilibrium is structurally encoded. A new CFTC chair operating with one commissioner and approximately 540 staff against a $22.88 billion annual market faces the same requisite variety failure Selig faces today. The capture persists through institutional geometry, not through any individual.

Together, the two scenarios complete a taxonomy that neither document establishes alone. The Trifecta documented how Nash-Stigler capture works through commission in an enforcement-active agency. The Kalshi scenario documents how it works through omission in an enforcement-absent agency. Both are capture equilibria. Both satisfy the geometry dominance test. Both produce Intent-Outcome Decoupling as their observable signature. The mechanism is not personality-dependent — it is a structural feature of how concentrated regulatory authority interacts with concentrated industry access, regardless of whether the agency is the DOJ Antitrust Division or the CFTC.

The Kalshi equilibrium is the more dangerous of the two precisely because it is the harder one to unwind.

Conclusion

The Kalshi litigation is not a prediction market story. It is a control architecture story. Sixteen states have filed enforcement actions. Four federal circuits are reviewing the same statutory question and reaching opposite conclusions. A single-commissioner agency operating with approximately 540 staff against a $22.88 billion annual market is filing friend-of-the-court briefs on behalf of the platform it is supposed to regulate. A lobbying coalition with 101 LinkedIn followers and 11 Facebook followers is spending millions on congressional access while its members simultaneously enter and oppose the market they are lobbying to protect. Washington’s civil complaint, filed today in King County Superior Court, is the latest data point in a structural convergence that has been building since January 2025.

The six CDT foresight simulations converge on one finding: the current fragmented control regime cannot persist as a stable equilibrium past Q3 2027. It is not viable in the cybernetic sense — the feedback loops have inverted, the control architecture lacks requisite variety, and the System 5 policy layer is being contested simultaneously by six incompatible actors issuing incompatible determinations from incompatible authority bases. Fragmented coexistence is not the durable endpoint. It is the precondition for forced centralization — and the path to centralization determines who wins.

State attorneys general hold the strongest operating position in Phase 1 because they hold the enforcement velocity advantage and the shortest legal path. Federal lawmakers hold the decisive instrument in Phase 2 because the SCEM forecloses judicial resolution by eliminating the statutory ambiguity that every preemption argument depends on — and a congressional floor vote in Phase 2 preserves the state opt-out flexibility that a Supreme Court ruling would extinguish. Investors who treat the current multi-forum fragmentation as a permanent operating environment are mispricing regime risk. The system is converging. The only open question is which actor shapes the terms.

MindCast will track every falsifiable prediction in this publication against observable evidence and publish formal model revisions when conditions require it. All predictions carry explicit measurement windows and falsification conditions. The arc began with Prediction Markets and the Regulatory Split and The Full Arc of Prediction Markets. Washington’s complaint today confirms the downside scenario is now the modal outcome. The control layer will determine what comes next.