MCAI Economics Vision: Zillow vs. Redfin–Compass, Premarket Control Under Expanding Transparency Laws

How Compass Turned Its Own Lawsuits Into the Legislation That Destroyed Its Business Model — and What Zillow Built While Compass Was Losing in Court

See also Zillow, eXp, and Redfin–Compass. Three Deals. Twenty Days. One Outlier. , The Compass–Redfin Alliance, Market Self-Correction Is Dead.

Regulatory momentum is not confined to Washington. A class of laws modeled on Washington SSB 6091 is emerging that forces listings into broad exposure the moment they are publicly marketed. That shift is collapsing the economic value of private listing control and redirecting competition toward buyer capture and interaction control. Zillow’s premarket rollout and the Redfin–Compass alliance are direct responses to that shift — not isolated product decisions.

Executive Summary

A new regulatory baseline is forming across U.S. real estate markets: once a listing is publicly marketed, it must be broadly accessible. Washington SSB 6091 is the clearest legislative expression of that principle, but the underlying logic is spreading. Wisconsin enacted listing transparency restrictions in December 2025. Illinois reintroduced its bill in February 2026. Each state that holds hearings generates a permanently discoverable evidentiary record that every other legislature, regulator, and opposing counsel can use.

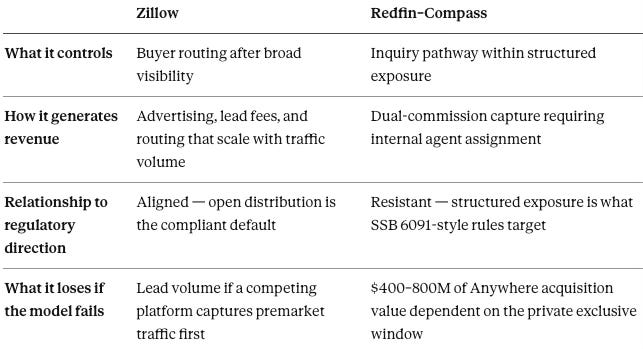

The two dominant platform responses to that baseline are now visible and structurally opposed. Zillow aligns with it by expanding public premarket visibility. Compass, through its Redfin alliance, attempts to preserve timing, presentation, and lead control within the same constraint.

MindCast identified the mechanism driving this transition before the legislative outcomes were known. The Compass Commission Consolidation Strategy established — through 130 Seattle ultra-luxury transactions — that private exclusives and address suppression are not seller-service features. They are mechanisms for routing buyers to internal agents and capturing both sides of the commission. Current legislation is targeting that exact architecture.

I. The Regulatory Direction: From Address Suppression to Broad Access

Washington SSB 6091 codifies a simple rule: once a listing is publicly marketed, it must be broadly accessible. The bill passed the state Senate 49–0 and the House 92–1 — a legislative margin that signals this is not a partisan or close question. See the bill summary.

MindCast documented the underlying market failure before the bill reached a vote. Across thirteen months of Seattle’s top-ten monthly luxury sales — 130 transactions totaling $1.08 billion — the Compass Commission Consolidation analysis found that 16 transactions produced commission flows that stayed entirely inside the combined Compass-Anywhere entity, representing $4.2 million in captured buyer-side commission from a single metropolitan market’s monthly top-ten record alone. Address suppression and private exclusives are not marketing choices. They are mechanisms for controlling who sees inventory and when — and the legislative record now confirms that both regulators and legislators read them the same way.

The ratchet effect matters here. Each state that enacts a concurrent marketing requirement reinforces the legal standard under Parker v. Brown, making federal preemption challenges progressively weaker as the state count rises. The legislative cascade is not a trend. It is a structural ratchet, and Zillow and Compass are both building platforms around where it terminates.

II. Zillow’s Response: Replace Private Control with Public Premarket

Zillow’s answer to the new regulatory environment is to build above it rather than around it. The company introduced Zillow Preview, a premarket product that exposes listings broadly before active MLS status — not to a selected network, but to the full Zillow audience. Companion listing access standards reinforce that listings should not be restricted by brokerage relationships or hidden behind access barriers.

Zillow is not recreating private listings in a new wrapper. The platform is replacing the private listing window with a different control layer entirely. Listings become visible earlier — to everyone. The advantage Zillow captures is not from restricting who sees the listing. It comes from being the place where buyers show up first, and from controlling how those buyers are routed after they arrive.

That shift follows directly from the constraint SSB 6091 imposes. If listings cannot be hidden, advantage must migrate to the interaction layer above visibility. Zillow is positioning to own that layer at scale.

Contact mcai@mindcast-ai.com to partner with us on Law and Behavioral Economics foresight simulations. To create your own game theory simulation of data on Compass address suppression and private exclusives, upload the URL of this publication to any LLM (ChatGPT, Claude, Gemini, Grok, Perplexity) and prompt ‘develop MindCast framework with 3 degrees of cited sub links.’ Thereafter, all new information you upload is training data for your AI system. See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure for more info.

MindCast AI’s analytical work on SSB 6091 — transaction methodology, opposition modeling, testimony framework, and game theory prediction record — is available for deployment in any state considering real estate transparency legislation. Washington’s record does not need to be rebuilt. It needs to be applied.

Recent projects: The Compass Collapse– A Post Washington SSB 6091 Passage Reckoning, How SSB 6091 Closed the Window, What Compass Did Next, and Why the Depositions Have Not Yet Begun ; The Compass Self-Destruction Sequence, How Aggressive Federal Litigation Birthed the Legislation That Destroyed the Business Model ; SSB 6091 Has Passed. Here Is What It Now Reaches — and the Compass Enforcement Record It Inherits ; Compass Plan B, Structural Circumvention After Washington SSB 6091.

III. Redfin–Compass: Preserve Advantage Within Visibility

Compass is attempting to solve the same problem from the other direction — not by building above the regulatory constraint but by restructuring exposure to preserve conversion advantage within it.

Redfin’s partnership distributes Compass “Coming Soon” listings and contemplates expansion into private inventory. The broader Compass-Rocket alliance expands distribution across its network. Industry reporting documents lead prioritization and phased exposure mechanics built into the partnership structure.

The predecessor behavior is already documented in the public record. MLS #2392995 — a $79 million Lake Washington estate listed as “Call for Address” on fosterrealty.com during the February 2026 legislative window — required any interested buyer to contact the Compass listing agent directly to learn the property’s location. The Address Suppression Calculus modeled the revenue and detection consequences of that strategy at scale and reached a finding directly relevant to what Compass is now attempting through Redfin: revenue adequacy and detection avoidance are structurally incompatible objectives. Full-portfolio address suppression generates enough revenue to matter but immediately exceeds detection tolerances. Concentrating suppression at the high end compresses revenue to approximately $500,000 per market annually — insufficient against the combined entity’s debt service.

The litigation context makes the Redfin alliance legible as strategy rather than partnership. MindCast’s Compass Antitrust Self-Destruction Sequence documented how Compass filed federal antitrust complaints against both NWMLS and Zillow in 2025 — structured to impose asymmetric litigation cost on institutions that couldn’t sustain decade-long federal defense. Both failed. Judge Vargas denied the Zillow preliminary injunction in February 2026. The NWMLS complaint produced the opposite of its intended effect: by broadcasting the mechanics of its shadow market through public federal filings, Compass handed Washington’s legislators the operative definitional framework that SSB 6091 codified. Compass’s own counsel wrote, with billable precision, the statutory definitions subsequently used to prohibit its primary business model. The Redfin alliance followed the injunction denial. Compass shifted from litigation — trying to stop platform-level transparency enforcement through federal courts — to partnership, attempting to preserve routing advantage through a platform it previously sued. The forum shifted. The underlying objective did not.

Compass's litigation also carried a rhetorical function beyond the courtroom. By characterizing Zillow's listing access standards as the infrastructure of a de facto national MLS, Compass attempted to reframe the transparency enforcer as the monopolist. The argument inverts the actual power structure — Zillow does not own cooperative listing infrastructure, does not require exclusive membership, and does not restrict which agents can access its platform. But the framing was designed for legislative hearings and trade press, not judicial scrutiny. Compass needed a narrative in which it was defending broker freedom against platform coercion. The national MLS framing supplied that narrative. SSB 6091's 141–1 passage is the legislative record's answer to it.

The Redfin alliance is Compass’s attempt to resolve that incompatibility by distributing the exposure mechanism across a partner platform rather than concentrating it internally. Redfin–Compass does not reject visibility. It restructures visibility to preserve timing advantage, information control, and lead routing priority. Whether that restructuring survives SSB 6091-style rules in the states where Compass holds significant listing share is the operative question.

Compass cannot publicly concede SSB 6091 as a defeat without handing every state legislature that follows a validated template and a confirmed prediction. The national MLS framing serves that purpose: by casting Zillow's listing access standards as monopolistic platform infrastructure rather than transparency enforcement, Compass preserves a legislative narrative in which it is defending broker freedom and seller choice against coercive platform control. The argument inverts the actual power structure — Zillow does not own cooperative listing infrastructure, does not require exclusive membership, and does not restrict which agents can access listings on its platform. But judicial scrutiny was never the target. The framing was designed for trade press, state legislative hearings, and the states where SSB 6091-style bills have not yet moved. Washington's 141–1 passage is the legislative record's answer to it. The Redfin alliance is Compass's operational answer: if the listing control layer closes state by state, shift the narrative to voluntary market evolution and preserve the buyer interaction layer through platform distribution before the next legislature convenes.

IV. Where the Models Diverge

Zillow and Redfin–Compass both operate in the premarket window. The difference is what each platform is trying to control.

Zillow distributes listings broadly and captures demand at scale. More buyers see more listings earlier, and Zillow becomes the routing infrastructure through which buyer interest flows. Compass structures exposure to maintain conversion advantage for its own agents — listings reach more platforms, but the inquiry pathway remains directed.

MindCast framed this conflict in the Compass Commission Consolidation analysis as private network control versus open infrastructure. The current platform competition extends that conflict into the premarket layer. Private control at the listing level is being legislated away. Both platforms are now competing for the layer that replaces it: control over how buyers interact with listings after they become visible.

Zillow’s model scales with the regulatory direction. Every new state that adopts an SSB 6091-style rule expands the market where Zillow’s open-distribution premarket product is the compliant default. Compass’s model requires preserving a structured exposure advantage that the same regulatory direction is designed to eliminate.

V. Investor Impact

Regulatory direction favors platforms that do not depend on restricting listing access to generate revenue.

Zillow benefits directly. Earlier buyer engagement means larger lead funnels, and broader listing visibility increases the platform’s value to both buyers and agents. As private listing advantages are constrained, the economic value of buyer routing increases — and Zillow is building the infrastructure to capture that value at national scale.

Compass and Redfin face compression from two directions simultaneously. The timing advantages that justified Compass’s $400–800 million premium above Anywhere’s standalone value — the ability to hold listings off the open market long enough for an internal buyer to arrive first — shrink with each state that enacts a concurrent marketing requirement. The goodwill on the Anywhere acquisition is tested against that assumption at every legislative event. The Compass Commission Consolidation analysis put the acquisition premium dependent on the private exclusive window at $400–800 million of the $1.6 billion deal value. That premium does not evaporate gradually. It reprices at each legislative event.

MindCast’s Address Suppression Calculus predicted this compression explicitly: once private listing advantages are constrained, economic value shifts to the next controllable layer. That shift is now observable in the platform strategies both companies are executing. Value is migrating from listing control to buyer interaction control, and the two platforms are not equally positioned to compete for it.

VI. Consumer Impact

Consumers gain something real from this transition: earlier access to listings. A home that previously circulated inside a private network for days or weeks before appearing publicly is now, under SSB 6091-style rules, visible to all buyers from the moment it enters the market. For buyers who lacked brokerage relationships with the listing firm — the majority of buyers in most markets — that is a genuine improvement in market access.

What consumers do not gain is transparency in what happens after they see the listing.

Listings are visible, but inquiry routing and agent assignment remain structured. A buyer who contacts a listing through a platform partner in the Redfin–Compass network may be routed to a Compass-affiliated agent regardless of whether that assignment serves the buyer’s interests. The interaction pathway — who handles the inquiry, which agents are presented as options, how showing requests are prioritized — remains under platform and brokerage control even when the listing itself is publicly visible.

MindCast documented this dynamic in the Address Suppression Calculus: the mechanism that generates dual-commission capture does not require the listing to be hidden. It requires the buyer inquiry to be routed to an internal agent. Address suppression was one tool for achieving that routing. Structured platform partnerships are another. Eliminating visible exclusion does not eliminate control. It relocates control one layer deeper — from who sees the listing to who handles the buyer after they do.

Consumers see more. Consumers control less of the interaction pathway than the increased visibility suggests.

VII. Strategic Consequence

The strategic divergence between Zillow and Compass is not primarily a product decision. It reflects a difference in how each company’s business model relates to the regulatory direction now unfolding.

Zillow’s revenue does not depend on controlling which agent represents the buyer. The platform profits from advertising, lead generation, and routing fees that scale with listing volume and buyer traffic — both of which increase as visibility expands. SSB 6091-style rules are structurally favorable to Zillow’s model. Each new state that forces listings into open distribution is a state where Zillow’s premarket product becomes the compliant default and its buyer funnel deepens.

Compass’s revenue depends substantially on capturing both sides of the transaction — and that capture requires controlling the buyer interaction, not just the listing presentation. The Redfin alliance is an attempt to preserve that control under greater visibility pressure, but it introduces a structural tension the Compass Commission Consolidation analysis identified in the legislative context: Compass’s cross-forum positions are structurally incompatible. The arguments Compass makes to investors about acquisition value, the arguments it makes to legislators about seller choice, and the transaction record visible in public MLS data cannot occupy the same evidentiary record without collapsing each other.

The shift is now clear and the direction is not reversible. Control has moved from listings to buyers. Zillow built for that destination. Compass is adapting to it under pressure.

VIII. Forward Implications

If legislative momentum continues on its current trajectory:

More states adopt SSB 6091-style concurrent marketing requirements, accelerating under the Parker v. Brownratchet as the state count rises

Public premarket visibility becomes the standard operating environment for residential real estate, not a platform differentiator

Private exclusives lose economic value as the window they depend on closes legislatively in market after market

Regulatory focus shifts downstream — from listing suppression to buyer steering, lead routing, and the platform mechanics that replace visible exclusion with structured interaction control

The falsification condition is specific: if SSB 6091-style legislation stalls or is reversed, if Compass demonstrates sustained timing advantage post-enactment in the markets where the bill applies, or if Zillow’s premarket product fails to generate buyer routing revenue at the scale its model requires — any of these would falsify the analysis above.

Final Synthesis

Transparency laws are standardizing listing visibility across U.S. real estate markets. That standardization does not eliminate competitive advantage. It relocates it.

Zillow captures the new advantage by controlling buyer interaction after visibility — building the routing infrastructure that replaces the private listing window. Compass attempts to preserve its existing advantage by restructuring how exposure is delivered, using platform partnerships to maintain the inquiry control that address suppression and private exclusives previously provided directly.

The $400–800 million of Anywhere acquisition value that depended on the private exclusive window is the number against which both strategies are ultimately measured. Each SSB 6091-style enactment reprices that assumption. The decisive advantage in the market that emerges will belong to the actor that controls the buyer after the listing is seen — and the regulatory environment is systematically dismantling every architecture that tried to control the listing instead.