MCAI Innovation Vision: The AI Infrastructure Energy Opportunity Landscape

AI Infrastructure Energy Series, Installment I Capital Is Flowing to the Wrong AI Infrastructure Layer

The MindCast series, The Power Stack, How Energy Infrastructure Became the New AI Battleground.

Installment I: The AI Infrastructure Energy Opportunity Landscape Capital Is Flowing to the Wrong AI Infrastructure Layer

Installment II: The AI Infrastructure Energy Antitrust Landscape When the Moats Become the Evidence

Installment III: The AI Infrastructure Energy Patent Landscape Patents Compound Forward: How Incumbents Pre-Write the Constraint Field

The AI infrastructure energy buildout is generating the largest constraint-removal investment opportunity in a generation — but most capital is flowing to the wrong layer. Speculative capital has concentrated in hyperscale datacenter construction, the demand layer, while the physical infrastructure that determines whether those datacenters can actually operate remains structurally undercapitalized. That gap between where capital flows and where constraint removal is most valuable is the investment thesis this installment maps.

Durable returns follow constraint removal, not bottleneck capture. Firms that expand transformer manufacturing capacity, build transmission into stranded generation corridors, or deploy next-generation geothermal supply compound alongside AI growth. Firms that secure positions within existing attractor regions without expanding system capacity generate short-term rents while accumulating the regulatory exposure that Installment II maps. The distinction between those two categories is the organizing principle of this paper.

Why This Installment Matters

Constraint removal generates the largest returns during technological expansion cycles — not at the demand layer, but at the bottleneck layer below it. The AI infrastructure buildout has created a structural misallocation: capital is flooding hyperscale datacenter construction while transformer manufacturing, advanced transmission, next-generation geothermal, and grid orchestration software remain undercapitalized relative to the demand signal they serve. The window for positioning at the constraint-removal layer before it becomes consensus is open now. This installment maps which sectors and corridors offer the most defensible expansion opportunities — and which apparent opportunities are speculative positions within existing attractors that carry antitrust and patent exposure addressed in Installments II and III.

I. Background: AI as an Energy System

Artificial intelligence is, at its foundation, an energy business. Training runs, inference clusters, and GPU racks convert electrical power into computation at scale — and compute demand is expanding faster than the grid infrastructure needed to support it. Generation construction cycles exceed five years. Transformer manufacturing lead times exceed two years. Interconnection queues contain thousands of competing projects. That structural lag between demand acceleration and infrastructure response is not temporary friction — it is the condition that makes infrastructure control strategically valuable and that makes the opportunity landscape this installment maps both real and time-sensitive. The full analytical architecture governing the series — cybernetic foundations, Field Geometry Reasoning (FGR) Vision, National Innovation Behavioral Economics (NIBE) Vision, strategic interaction, and the opportunity-antitrust loop — is developed in the series introduction at www.mindcast-ai.com/p/ai-data-center-energy-series.

II. The Constraint Landscape

AI infrastructure geography has already entered an attractor phase. Northern Virginia, Phoenix, and parts of Texas are concentrating deployment because transmission infrastructure, substation density, cooling water access, and permitting tolerance make those the only locations where large-scale deployment is feasible at acceptable cost and speed. The Geodesic Availability Ratio — the number of viable alternative deployment paths — is low and falling in major U.S. hubs. The Structural Persistence Threshold has been exceeded in major hyperscale corridors, meaning concentration is now self-reinforcing and will not correct without deliberate intervention.

Whichever layer of the stack becomes most constrained becomes the source of market power. That layer is currently energy and grid access — and the window between formation of those control positions and regulatory recognition is open now. Understanding which positions expand system capacity and which merely capture existing scarcity is the analytical task this installment performs. FGR Vision’s application to Federal Energy Regulatory Commission (FERC) proceedings and datacenter siting is developed in FERC + AI Data Centers at www.mindcast-ai.com/p/ferc-ai-dcs.

III. Market Participants and Emerging Control Positions

Three categories of firm are shaping the compute–power stack. Their positions today determine the antitrust and patent exposure that Installments II and III examine.

Hyperscale Demand Anchors

Microsoft, Google, Amazon, and Meta are the primary demand drivers. Their capital scale allows them to move faster than the institutional systems governing interconnection, permitting, and transmission — which is precisely the condition Feedback Latency Index (FLI) measures. Each has moved beyond treating energy as a procurement function. Microsoft’s twenty-year nuclear restart agreement with Constellation Energy, Google’s direct equity investment in geothermal developer Fervo Energy, and Amazon’s portfolio of dedicated generation agreements across nuclear, solar, and wind represent queue preemption strategies, not energy bets. The firms securing dedicated generation early are removing themselves from the public interconnection queue — shrinking available capacity for everyone who follows.

FLI and FGR Vision are the primary instruments here. FLI is elevated precisely because hyperscalers move at private capital speed while the institutional systems governing interconnection and permitting do not. FGR Vision identifies their dedicated generation and queue preemption moves as attractor formation behavior — the field geometry is being shaped by firms with the balance sheet to act before scarcity is publicly priced. Insight: the same moves that rationally reduce hyperscaler infrastructure exposure are the ones that will attract competition scrutiny once the field tightens — the Becker-to-Posner transition is already embedded in their current strategy.

Energy and Grid Infrastructure

Constellation Energy, Vistra, and NextEra occupy the generation layer. Their leverage is growing as hyperscalers pursue long-term dedicated supply rather than spot grid access. On the transmission and grid hardware side, ABB and Hitachi Energy dominate transformer manufacturing — the segment with the most acute supply constraint, currently running two-plus year lead times on large power transformers. Quanta Services and MYR Group control significant transmission construction capacity. These firms sit at the narrowest point in the buildout timeline: a datacenter can be designed and financed in months; the transformer it depends on may not arrive for two years.

FGR Vision and Capital Vision are the relevant instruments. FGR Vision shows that transformer and transmission capacity are the binding constraints limiting geodesic availability — the primary reason attractor regions cannot be relieved by simply building more datacenters elsewhere. Capital Vision finds this segment structurally underpriced: firms controlling transformer manufacturing capacity and transmission construction are positioned at the narrowest point in the entire buildout, yet attract less speculative capital than the demand layer they serve. Insight: ABB and Hitachi Energy’s two-year lead times are not a supply chain inconvenience — they are the clock that governs when infrastructure concentration becomes irreversible.

Cooling and Power Electronics

Vertiv and Schneider Electric supply the power management and thermal infrastructure that high-density GPU clusters require. Liquid cooling — specifically direct liquid cooling and immersion cooling — is the technology transition most relevant to Installment III: it is where the most active patent accumulation is occurring, where switching costs are highest once a facility commits to an architecture, and where a patent hold-up scenario is most structurally plausible. Eaton and Bloom Energy occupy adjacent positions in power conditioning and on-site generation.

Chicago Law and Behavioral Economics (LBE) Vision and Capital Vision are the relevant instruments. Chicago LBE Vision places the cooling technology transition squarely in the Becker layer: switching costs are high, architectural commitment is irreversible once a facility is built, and rational patent holders will extract rents from that lock-in before Posner correction arrives. Capital Vision identifies this segment as the most structurally underpriced relative to its constraint-removal value — cooling is a binding physical limit on GPU density, yet patent positions in the enabling technologies remain underappreciated by generalist investors. Insight: cooling architecture is where patent hold-up risk is most acute and most imminent — the subject Installment III examines in full.

Emerging Infrastructure Developers

A tier of infrastructure-focused developers is positioning between hyperscalers and utilities: Crusoe Energy, Applied Digital, and CoreWeave on the compute side; Pattern Energy and LS Power on transmission development. These firms matter for Installments II and III because they are accumulating infrastructure positions without the balance sheet protection of hyperscalers — making them both potential acquisition targets and potential complainants in future antitrust proceedings.

NIBE Vision and FGR Vision are the relevant instruments. NIBE Vision identifies these firms as the most exposed to institutional drag — their deployment timelines depend on the same slow permitting and interconnection systems that hyperscalers are bypassing through dedicated generation agreements. FGR Vision shows that without the capital to secure attractor-region positions early, mid-tier developers face a narrowing set of viable deployment paths as the field geometry tightens around the dominant players. Insight: firms in this tier will define the complainant class in Installment II’s antitrust analysis — they are accumulating the standing that enforcement actions require.

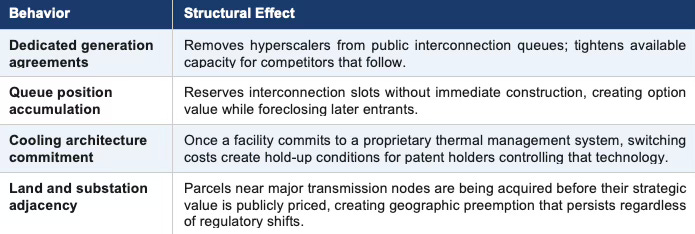

The Moats Being Built

Four observable behaviors are creating durable control positions that Installments II and III will examine as legal exposure.

None of these behaviors is characterized here as unlawful. Installment II examines where and how they cross that line. Installment III examines the patent landscape that cooling and power electronics positions create.

Chicago LBE Vision maps all four behaviors onto the same phase of the Coase–Becker–Posner sequence: rational appropriation of constrained positions in a system where coordination has already failed and legal correction has not yet arrived. FLI quantifies how long that window stays open. FGR Vision explains why the positions, once established, are self-reinforcing and difficult to unwind without active intervention. Insight: the moats being built today are legally defensible until the field tightens enough to make entrant exclusion visible — at which point the same infrastructure positions become the evidentiary core of the antitrust case Installment II maps.

Contact mcai@mindcast-ai.com to partner with us on Predictive Cognitive AI in Law and Behavioral Economics. To deep dive on MindCast work in Cybernetic Foresight Simulations upload the URL of this publication into any LLM and prompt ‘reconstruct MindCast framework with three degrees of cited sub links.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure.

Recent projects: The Cybernetic Foundations of Predictive Institutional Intelligence, MindCast AI Emergent Game Theory Frameworks, Transforming Commercial Real Estate Governance Friction into Economic Velocity, MindCast AI Investment Series, Washington’s Clean Energy Advantage, a Behavioral Innovation Strategy for the Energy Transition, VRFB's Role in AI Energy Infrastructure: Perpetual Energy for Perpetual Intelligence - Aligning Infrastructure Permanence with the Age of AI, The Bottleneck Hierarchy in U.S. AI Data Centers, Super Bowl LX — AI Simulation vs. Reality.

IV. Bottleneck Removal and Infrastructure Opportunity

The largest investment opportunity in AI infrastructure is not where most capital is currently flowing. Speculative capital has concentrated heavily in hyperscale datacenter construction — the demand layer. The constrained layers below it, the ones that determine whether those datacenters can actually operate at scale, are receiving far less capital relative to their structural importance. Transformer manufacturing, next-generation transmission technology, advanced geothermal generation, and grid orchestration software are all undersupplied relative to the demand signal they serve. That gap between where capital flows and where constraint removal is most valuable is the investment thesis.

Periods of technological expansion consistently produce the largest returns at bottleneck removal points rather than at the demand layer those bottlenecks serve. Capital that identifies and funds constraint removal before the bottleneck becomes widely recognized captures the structural value — the same logic that made fiber-optic buildout, semiconductor fab investment, and cloud storage infrastructure compelling in their respective expansion cycles.

Infrastructure investors therefore face a constraint-driven opportunity landscape. Firms capable of expanding transmission capacity, energy generation, and grid hardware production will capture value created by the rapid expansion of AI compute demand.

Durable returns follow constraint removal, not bottleneck capture. The distinction carries both investment and legal consequences — a line Parts II and III develop at length.

Capital Vision — MindCast AI’s capital allocation framework — separates two categories of investment that market narratives frequently blur. Constraint-removal capital expands transmission, transformer production, geothermal supply, substation capacity, or cooling efficiency — increasing the number of viable deployment paths and lowering the Attractor Dominance Score. Choke-point capital secures exclusive positions in scarce queues, local power access, or irreplaceable siting corridors without enlarging field capacity. Applied to current capital flows, Capital Vision identifies a material misallocation gap: venture and infrastructure capital clusters in hyperscale datacenter construction, AI chip design, and model development, while the upstream infrastructure layer — transformer manufacturing, transmission technology, advanced geothermal generation, grid orchestration software — remains undercapitalized relative to the demand signal. The sectors scoring highest on the constraint-removal criterion are precisely those attracting the least speculative capital today. That gap is the investment thesis. Scarcity monetization produces short-term rents but accumulates regulatory attention; expansionary capital compounds alongside broader system throughput.

V. The Opportunity Landscape

The AI infrastructure energy buildout is generating investment opportunity at every constrained layer of the stack — but not all of it is equal. Constraint-removal capital, deployed into the layers that actually limit system throughput, compounds alongside AI growth. Choke-point capital, deployed to capture existing scarcity rather than expand it, generates short-term rents while accumulating regulatory exposure. The distinction between those two categories is the organizing principle of this section.

Tier 1 — Highest Defensibility: Constraint Removal at the Physical Layer

The most defensible opportunities sit at the physical infrastructure layer — the segments where the constraint is real, the lead times are long, and the capital required is large enough to deter fast-moving competitors. These are not glamorous positions. They are structural ones.

Transformer manufacturing is the single most acute bottleneck in the current buildout. Large power transformers — the units that step voltage down from transmission lines to datacenter-usable levels — now carry lead times exceeding two years from domestic producers. ABB and Hitachi Energy dominate the segment. Domestic manufacturing capacity has not expanded commensurately with AI-driven demand. Capital flowing into transformer manufacturing capacity expansion — whether through new entrants, facility expansion, or supply chain investment — is targeting the narrowest physical chokepoint in the entire AI infrastructure stack. FGR Vision confirms: geodesic availability cannot improve without transformer supply relief. Every major attractor region is constrained by it.

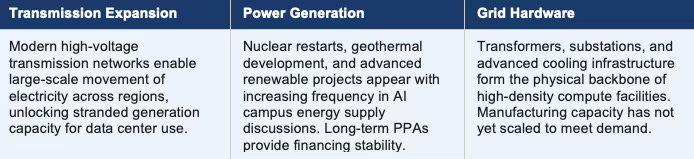

Advanced transmission technology is the second tier of physical constraint removal. High-voltage direct current (HVDC) transmission enables large-scale electricity movement across regions, unlocking stranded generation capacity for datacenter use and expanding the number of viable deployment corridors. Grid-enhancing technologies — advanced conductors, dynamic line ratings, power flow controllers — increase throughput on existing transmission without requiring new right-of-way. Quanta Services and MYR Group sit at the construction capacity layer of this opportunity. Capital targeting transmission expansion increases geodesic availability directly — the metric FGR Vision uses to assess whether attractor dominance can be relieved.

Next-generation power generation — specifically geothermal, nuclear restarts, and advanced small modular reactors — addresses the generation layer of the constraint. Geothermal is particularly well-positioned: it provides firm, dispatchable power with a small land footprint, making it viable in urban-adjacent locations where AI campuses concentrate. Fervo Energy’s agreement with Google illustrates the thesis — a developer willing to commit capital to geothermal development can secure long-term dedicated supply with a hyperscaler seeking to exit the public interconnection queue. Nuclear restarts, as illustrated by the Constellation-Microsoft agreement, follow similar logic: firm power, long-duration supply, and queue preemption in a single transaction.

Tier 2 — Strong Opportunity: Enabling Technologies with Patent Exposure

The second tier of opportunity sits in enabling technologies — the systems that make high-density compute physically possible. These carry strong returns but also carry the patent hold-up risk that Installment III maps in full.

Liquid cooling architecture — direct liquid cooling and immersion cooling — is the technology transition that unlocks GPU density beyond what air cooling can sustain. Vertiv and Schneider Electric are the incumbent suppliers, but the field is fragmented and actively accumulating patent positions. The opportunity is real: AI cluster density is increasing faster than air cooling can absorb, and datacenters that commit to liquid cooling architectures early can run denser, more efficient facilities. The risk, developed in Installment III, is that architectural commitment before patent positions clarify creates hold-up exposure. Capital Vision rates this segment as structurally underpriced relative to constraint-removal value — but investors need visibility into the IP landscape before sizing positions.

Grid orchestration software — the systems governing how datacenter load communicates with utility grid management — is the highest-growth segment in the enabling technology layer. As FERC moves toward mandatory load transparency requirements, the software standards that emerge from that rulemaking will determine which positions carry durable value and which are rendered obsolete by open standards. Firms that establish technical standards in grid-interface software before FERC rulemaking crystallizes those standards into compliance requirements will occupy a structurally advantaged position.

Power electronics — advanced transformer designs, power conversion architectures, and uninterruptible power systems optimized for AI workloads — sit at the intersection of the physical constraint layer and the enabling technology layer. Eaton and Bloom Energy occupy adjacent positions. The patent accumulation dynamic is less advanced here than in cooling, but the structural conditions for hold-up are forming as buildout volume increases.

Tier 3 — Speculative: Positions Within Existing Attractors

The least defensible apparent opportunities are positions within existing attractor regions that do not expand system capacity. These are choke-point positions, not constraint-removal positions.

Hyperscale datacenter construction in Northern Virginia, Phoenix, and established Texas corridors is the clearest example. Capital flowing into datacenter construction within those attractors is not removing constraints — it is competing for the same constrained interconnection queue, the same limited transformer supply, and the same saturated land market that existing operators already occupy. Returns depend on queue position, not on expanding the system. FGR Vision characterizes these positions as high Attractor Dominance Score investments: high near-term returns for early movers, rapidly declining returns for followers as the attractor saturates.

Queue position accumulation — reserving interconnection slots without immediate construction — generates option value in the short term but converts into regulatory exposure as enforcement attention migrates toward queue foreclosure practices. Chicago LBE Vision places this behavior firmly in the Becker layer: rational today, legally exposed when the Posner correction arrives.

The clearest signal distinguishing Tier 1 from Tier 3 is whether the investment increases or decreases the Geodesic Availability Ratio. Transmission buildout increases it. Another datacenter in Northern Virginia decreases it. That test is the practical application of FGR Vision to capital allocation decisions.

Geographic Corridors — Where Opportunity Is Forming Outside Existing Attractors

The most underappreciated opportunity in the AI infrastructure energy landscape is geographic: the corridors that are not yet attractors but have the physical and institutional preconditions to become them.

Gulf states — Saudi Arabia, UAE, Qatar — combine capital concentration with centralized permitting authority, enabling datacenter deployment at scale on timelines that U.S. permitting structures cannot match. NIBE Vision identifies them as the most likely near-term capacity relief valve for U.S. hyperscalers locked out of domestic interconnection queues. Prediction 3 in the falsifiable ledger follows directly. Capital positioned in Gulf datacenter infrastructure before U.S. hyperscalers publicly announce offshore deployment strategies will capture the geographic arbitrage.

U.S. jurisdictions with accelerating permitting reform represent the domestic version of the same opportunity. States that combine available transmission capacity, utility coordination willingness, and shortened environmental review cycles will attract disproportionate datacenter investment relative to their current infrastructure footprint. NIBE Vision predicts widening divergence among U.S. states on this dimension over the next eighteen to thirty-six months. The states that shorten permitting cycles by even twelve months will capture capital that would otherwise route to competing jurisdictions.

Stranded generation corridors — regions with abundant renewable generation capacity but insufficient transmission to deliver it to demand centers — represent a third category of underpriced geographic opportunity. HVDC transmission investment that connects stranded generation to AI demand centers simultaneously removes a physical constraint and creates a new deployment corridor outside the existing attractors. The transmission investment is the enabling move; the corridor value follows.

VI. Institutional Throughput and Regulatory Delay

Institutional speed determines AI geography as much as physical infrastructure does. Private capital deploys fast. Transmission planning, environmental review, and interconnection queue management do not. That gap forces developers to compete for existing constrained capacity rather than expand the system — amplifying concentration in existing attractor regions and closing off alternative corridors before they can develop. NIBE Vision’s Temporal Drag Coefficient is at historically elevated levels across the U.S. grid interconnection system. Regulatory authority fragments across FERC, regional transmission organizations, state public utility commissions, and local zoning boards — no single agency can accelerate deployment across all four layers simultaneously, which means the governance gap between infrastructure formation and legal recognition is structural, not incidental.

Regulatory Vision predicts a two-stage sequence: permitting bottlenecks shape early winners first; enforcement attention migrates toward oversight and correction only after concentration becomes visible. That sequence is the opportunity window — and it is closing. The NIBE framework is specified in NIBE + SBC at www.mindcast-ai.com/p/nibesbc. The antitrust consequences of that sequence are the subject of Installment II.

VII. Strategic Implications

The system is in the Becker phase: scarcity exists at key constraint points, rational actors are appropriating scarce positions, and legal correction has not yet arrived. Queue position hoarding, exclusive energy contracts, land acquisition near substations, and proprietary infrastructure standards are predictable responses to a delay-dominant environment — not outliers. Each move rationally reduces the actor’s infrastructure exposure while deepening bottlenecks for competitors that follow. Where and how those moves cross into exclusionary conduct is the subject of Installment II.

Investors looking only at model developers and chip manufacturers are watching the wrong layer. Durable returns in the next phase of AI competition will accrue at the infrastructure layers below compute — energy supply, transmission access, grid hardware, and institutional throughput. Capital that reaches constraint-removal positions before the bottleneck becomes consensus will capture returns that later-stage datacenter investment cannot replicate. The game theory architecture governing strategic interaction patterns is developed in MindCast AI Emergent Game Theory Frameworks at www.mindcast-ai.com/p/mindcast-game-theory.

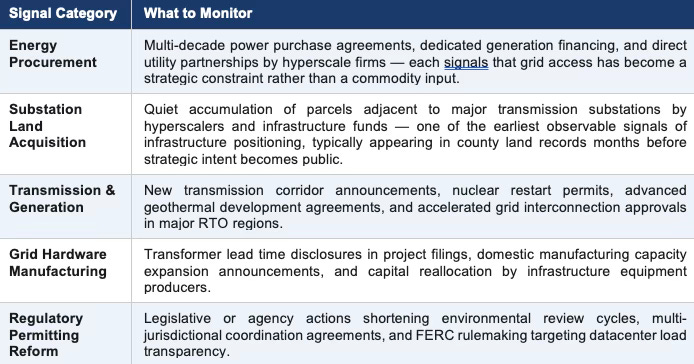

VIII. Signals to Watch

Infrastructure bottlenecks reveal themselves through observable market behavior before constraints become widely recognized. Within the MindCast AI framework, the signals below function as leading indicators of FLI elevation — early data points that the feedback gap between compute demand and infrastructure response is widening. Energy contracts, permitting acceleration, and infrastructure financing decisions often appear in public filings months before the underlying scarcity becomes consensus knowledge. Monitoring those signals allows investors and AI firms to detect structural shifts early and position capital before attractor formation is complete.

Acceleration across those indicators signals that the compute–power constraint cycle is intensifying. Organizations that respond before constraints become widely understood will capture the greatest strategic advantage.

IX. Signal Validation — What the Evidence Actually Supports

AI infrastructure energy generates more narrative than signal. Media cycles between grid collapse and AI power demand being overblown. Capital markets price both narratives at different points in the same quarter. Separating what the structural evidence actually supports from what is advocacy, speculation, or confounded data is the precondition for any investment thesis that will hold.

MindCast AI applies Causal Signal Integrity (CSI = (ALI + CMF + RIS) / DoC²) as the filter. Action-Language Integrity measures whether actors align rhetoric with operational behavior. Cognitive-Motor Fidelity measures whether strategic commitments translate into observable action. Resonance Integrity Score measures whether signals hold across time and actors without narrative reversal. Degree of Confounding squares in the denominator because confounding compounds — a high DoC collapses an otherwise strong signal.

Three signals pass the full CSI test and anchor the opportunity thesis in this installment.

Transformer scarcity passes. Lead times exceeding two years are documented in procurement filings across multiple quarters. Capital reallocation into domestic manufacturing is observable in public announcements from ABB, Hitachi Energy, and emerging domestic entrants. ALI is strong — manufacturers are expanding capacity, not just raising prices. CMF is strong — hyperscaler procurement teams are factoring transformer lead times into campus timelines in earnings calls and permitting documents. RIS is strong — the signal has not reversed across multiple quarters or across geographies. DoC is manageable — no credible alternative explanation accounts for the breadth and consistency of the constraint.

Transmission congestion in Northern Virginia and Phoenix passes. Interconnection queue saturation is publicly documented in PJM and MISO filings. Queue withdrawal rates are rising, indicating developers are abandoning positions rather than waiting — a behavioral confirmation that the constraint is binding, not merely bureaucratic. ALI is strong — grid operators are publicly acknowledging saturation. CMF is strong — hyperscalers are responding with dedicated generation strategies that bypass the queue entirely, which is the rational action only if queue access is genuinely foreclosed. RIS is strong across multiple years of queue data.

Cooling infrastructure as a binding operational constraint passes. Datacenter operators have disclosed cooling as a ceiling on GPU density in earnings calls, facility announcements, and permitting documents. The transition from air to liquid cooling is being driven by physics, not preference — GPU thermal density has exceeded what air systems can manage at current cluster sizes. ALI is strong. CMF is strong — capital is flowing into liquid cooling procurement ahead of facility completion, not after. RIS is strong and accelerating.

Two signals that dominate media coverage fail the CSI test and should not anchor investment decisions.

Nationwide grid destabilization fails. ALI is low — utilities filing aggressive AI demand forecasts with FERC have not correspondingly accelerated transmission capital programs. The gap between forecast rhetoric and capital commitment is the ALI failure. CMF is low — announced datacenter projects routinely cite multi-year interconnection timelines that directly contradict near-term demand projections. DoC is high — weather volatility, EV load growth, and industrial reshoring are all operative confounders that make AI the marginal rather than primary stress factor in most regional grids.

Uniform national transformer shortage fails the geographic precision test. The constraint is real in specific corridors serving hyperscale demand — it is not uniform across all transformer classes and all geographies. Investment theses built on nationwide scarcity will misprice both the opportunity and the risk.

The CSI output therefore focuses the opportunity thesis precisely: transformer supply in hyperscale corridors, transmission congestion in established attractor regions, and cooling architecture transitions are where structural evidence is strongest. Those are the bottlenecks generating real investment opportunity in Tier 1 and Tier 2. The rest is noise that Installments II and III will need to filter as they assess conduct and patent exposure against the same evidentiary standard.

X. Conclusion

The AI infrastructure energy buildout is not a single investment theme — it is a tiered landscape in which returns, risks, and defensibility vary sharply depending on where in the stack capital is deployed. Tier 1 positions in transformer manufacturing, advanced transmission, and next-generation generation expand system capacity and compound alongside AI growth. Tier 2 positions in liquid cooling, grid orchestration software, and power electronics carry strong returns but require IP landscape visibility before sizing. Tier 3 positions within existing attractors generate short-term rents for early movers and rapidly diminishing returns for followers.

The geographic dimension is equally tiered. Gulf states offer the clearest near-term capacity relief valve for hyperscalers locked out of domestic interconnection queues. U.S. jurisdictions accelerating permitting reform will attract disproportionate capital relative to their current infrastructure footprint. Stranded generation corridors, unlocked by transmission investment, represent the most underpriced domestic opportunity in the landscape.

The GAR test — does this investment increase or decrease Geodesic Availability across the infrastructure field — is the practical decision rule that separates constraint-removal capital from choke-point capital. Transmission buildout increases it. Another datacenter in Northern Virginia decreases it. Capital that passes the GAR test compounds alongside the system. Capital that fails it accumulates the regulatory exposure Installment II maps in full.

Infrastructure buildout at this scale introduces a parallel risk domain that operates independently of competition law: intellectual property hold-up. Once a datacenter commits billions of dollars to facilities designed around specific cooling architectures, power management systems, or grid-interface software, a patent holder controlling an enabling technology can extract licensing fees that would have been rejected before commitment.

The three highest-exposure domains — liquid immersion and direct liquid cooling, advanced power electronics, and grid-interface software — are actively accumulating patent positions now, while buildout is still early enough that most litigation has not yet materialized. Installment III maps the hold-up landscape in full.

Opportunity and antitrust risk are two sides of the same structural equation. Actors that build transmission, expand transformer manufacturing, deploy geothermal generation, or develop advanced cooling systems increase the number of viable deployment paths across the infrastructure field — reducing FLI, expanding geodesic availability, lowering the Attractor Dominance Score. Private incentives align with systemic stability. Actors that hoard queue positions, lock in exclusive energy supply, or control proprietary infrastructure standards generate short-term rents while accumulating exactly the regulatory exposure that Chicago Law and Behavioral Economics Vision predicts will arrive — and in infrastructure markets, when enforcement arrives, the structural damage is already embedded. The actors who shape the next phase of the global AI economy will be those who expanded the system’s capacity to function, not those who extracted rents from its constraints.

Future installments examine the opportunity landscape, the emerging antitrust risks surrounding infrastructure concentration, and the intellectual property dynamics that may arise as control points consolidate across the AI infrastructure ecosystem.

The market still describes this phase as infrastructure buildout. The Vision Functions describe it more precisely as control formation inside a constrained field. The next major competitive divide in AI will separate firms that secured infrastructure control from firms that remained exposed to public-grid scarcity. If compute demand continues to outpace grid expansion and permitting throughput, electricity access will become the primary competitive constraint in frontier AI deployment by the late 2020s — visible first through accelerating hyperscale power contracts, dedicated generation partnerships, and increasing capital flows into transmission and grid hardware manufacturing. That is the core falsification pathway for the thesis developed here.

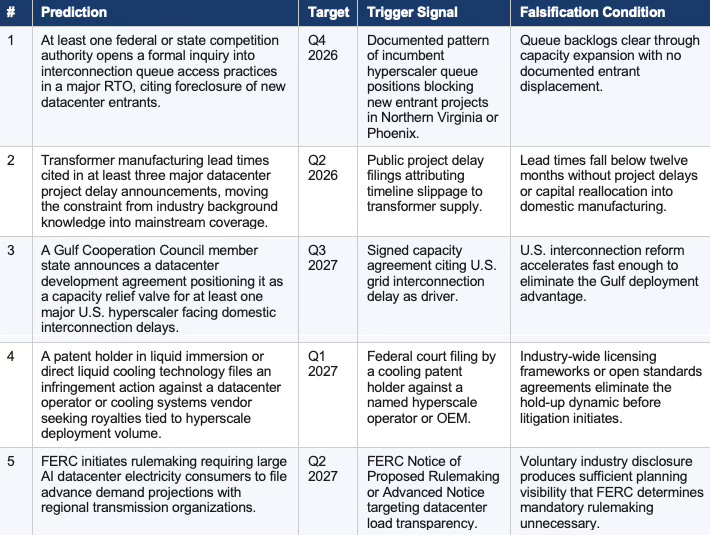

Falsifiable Predictions

MindCast AI closes every analytical series with a dated prediction ledger. Forecasts are not hedged into meaninglessness — they are falsifiable commitments against which the analytical framework can be evaluated.