MCAI Innovation Vision: The AI Infrastructure Energy Antitrust Landscape

AI Infrastructure Energy Series, Installment II When the Moats Become the Evidence

Executive Summary

Antitrust enforcement has entered an era of competitive federalism. Federal agencies, state attorneys general, courts, and legislatures now operate as a distributed governance system rather than a centralized regulator. For AI firms and investors, antitrust risk cannot be evaluated through federal regulatory behavior alone. In cybernetic terms, AI infrastructure competition now operates as a feedback system: infrastructure signals generated in energy markets, interconnection queues, and deployment corridors propagate through regulatory and legal institutions rather than terminating at a single enforcement authority.

Monopoly thresholds are not the operative trigger. Infrastructure routing control is.

The MindCast AI Infrastructure Energy series: The Power Stack — How Energy Infrastructure Became the New AI Battleground

Installment I: The AI Infrastructure Energy Opportunity Landscape Capital Is Flowing to the Wrong AI Infrastructure Layer

Installment II: The AI Infrastructure Energy Antitrust Landscape When the Moats Become the Evidence

Installment III: The AI Infrastructure Energy Patent Landscape Patents Compound Forward: How Incumbents Pre-Write the Constraint Field

Installment I closed with a precise warning: the moats being built inside the AI infrastructure stack are legally defensible until the field tightens enough to make entrant exclusion visible — at which point the same positions become the evidentiary core of the antitrust case. The Becker phase — the period when firms accumulate control positions through individually rational conduct, before entrant exclusion becomes legally visible — is closing. Rational appropriation of constrained positions is giving way to visible entrant exclusion across multiple layers of the stack.

Transformer supply concentration in hyperscale corridors, queue preemption strategies that foreclose mid-tier developer access, dedicated generation agreements that remove hyperscalers from the public interconnection grid while shrinking available capacity for everyone else, cooling architecture lock-in that creates switching costs before patent positions clarify — each behavior is individually rational and collectively exclusionary.

Installment II delivers the evidentiary case that infrastructure routing control — not monopoly thresholds — is the operative antitrust trigger.

Federal settlement no longer guarantees closure. State attorneys general pursue independent claims, legislators reopen scrutiny of transaction structures designed to avoid merger review, and courts function as independent venues for structural remedies.

A distributed enforcement architecture now operates across the same infrastructure layers that Installment I mapped as investment opportunity. For capital allocators, the implication is direct: antitrust exposure is no longer a tail risk that materializes only at monopoly thresholds. Exposure accumulates as infrastructure control becomes visible to enforcement actors operating simultaneously across institutional nodes.

AI infrastructure antitrust risk will likely emerge first at routing layers of the compute–energy stack — the infrastructure points competitors must traverse to participate in the market, including grid interconnection queues, transformer supply, and cooling architecture standards — and enforcement will propagate through state and private litigation channels before federal closure mechanisms activate.

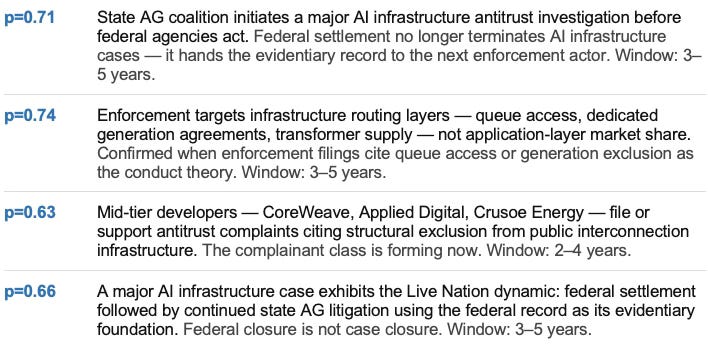

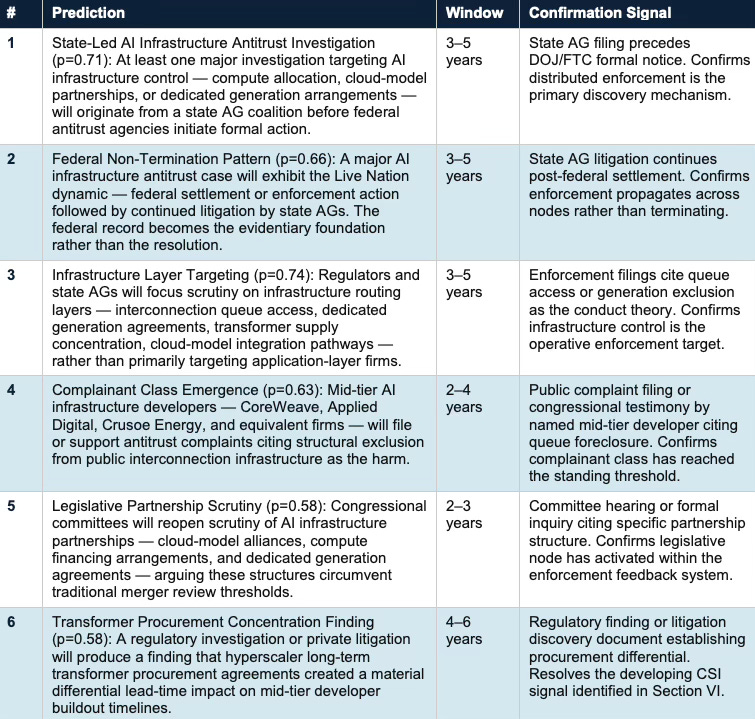

FORESIGHT PREDICTIONS — FALSIFIABLE, TIMESTAMPED, PROBABILITY-WEIGHTED

MindCast foresight simulations produce predictions stated in advance, with explicit falsification conditions. Four core predictions govern this installment’s analysis. Full probability gates and confirmation signals appear in Section VI.

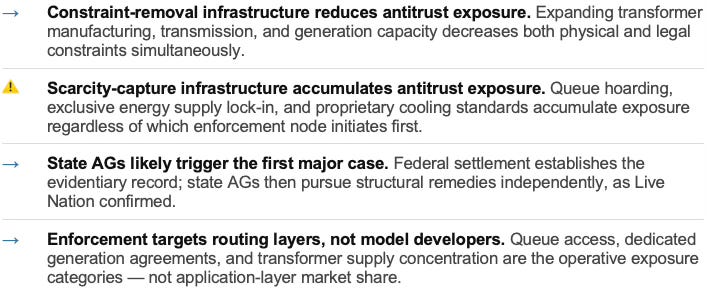

INVESTOR SIGNAL — FOUR TAKEAWAYS

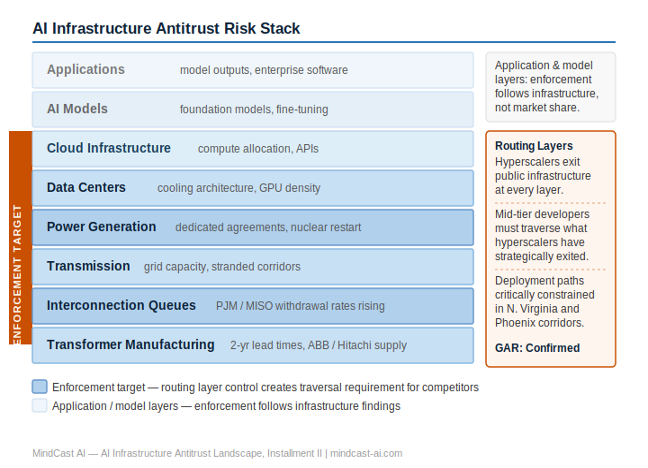

AI INFRASTRUCTURE ANTITRUST RISK STACK

Enforcement scrutiny targets routing layers — where hyperscalers exit public infrastructure and mid-tier developers face traversal requirements. Application and model layers follow infrastructure findings, not market share.

I. From Moat to Evidence — The Becker-Posner Sequence in AI Infrastructure

Installment I documented four observable behaviors generating durable control positions across the AI compute and energy stack: queue position accumulation, exclusive energy supply lock-in, cooling architecture commitment, and proprietary infrastructure standards. Each was characterized using Chicago Law and Behavioral Economics Vision as operating in the Becker phase — the period when firms accumulate infrastructure control positions through individually rational conduct, before entrant exclusion becomes legally visible and correction-triggering — in a system where coordination has already failed and legal correction has not yet arrived.

The Becker-to-Posner transition — the shift from tolerated accumulation to legally actionable exclusion, named for Gary Becker’s model of rational market behavior and Richard Posner’s theory of judicial correction — is not a distant event. It is the structural shift Installment II maps. In each prior infrastructure industry — railroads, electric utilities, telecommunications — the same sequence played out: control positions formed during a buildout cycle, entrant exclusion became visible as the field tightened, and enforcement responded to the exclusionary pattern rather than to the original control position. The original position was often legal. The conduct that weaponized it against competitors was not.

AI infrastructure is traversing that sequence now. The question is not whether enforcement will arrive. The question is which specific behaviors will define the evidentiary core when it does. Three structural lenses clarify the emerging antitrust risk. Chicago LBE (Chicago Law and Behavioral Economics Vision) tracks when rational infrastructure accumulation crosses into legally visible exclusion. FGR (Field-Geometry Reasoning) measures whether viable deployment paths across the infrastructure field are expanding or contracting. CSGT (Chicago Strategic Game Theory Vision) models the strategic incentives that pull state attorneys general into enforcement arenas when federal action softens. Full framework outputs and methodology appear in Appendix A1–A7.

The Four Conduct Theories

Mapping Installment I’s documented infrastructure behaviors to antitrust conduct frameworks produces four analytically distinct exposure categories.

Queue Preemption as Foreclosure

Hyperscalers securing dedicated generation agreements — Microsoft’s nuclear restart with Constellation, Google’s equity stake in Fervo Energy, Amazon’s portfolio of long-duration supply contracts — exit the public interconnection queue by design. Each such agreement removes a large block of generation capacity from the pool available to mid-tier developers who depend on public queue access.

The conduct theory does not require proving the agreements were entered for exclusionary purposes. Installment I’s Causal Signal Integrity analysis documents the behavioral confirmation: queue withdrawal rates are rising among mid-tier developers as hyperscaler dedicated agreements expand. When developers abandon queue positions rather than wait — the rational action only when queue access is genuinely foreclosed — the exclusionary effect becomes observable independent of intent.

The legally relevant question is whether the aggregated effect of individually rational queue preemption moves constitutes a pattern that forecloses mid-tier developer access to the generation capacity they depend on to compete. Field Geometry Reasoning produces a direct answer: Geodesic Availability — the count of viable, unobstructed infrastructure deployment paths remaining in a corridor before strategic preemption closes them off — has declined materially in Northern Virginia and Phoenix. The remaining viable deployment paths are narrowing as attractor regions saturate. That is the structural evidence a plaintiff or regulator needs.

Deployment path availability in major hyperscale corridors has contracted through strategic preemption, not natural scarcity alone. Rational actors with public queue alternatives chose to exit. That behavioral distinction is the structural evidence a plaintiff or regulator needs — the field geometry changed because of conduct, not constraint.

Transformer Supply Concentration

Large power transformer lead times exceeding two years represent the single most acute physical bottleneck in the current buildout. ABB and Hitachi Energy dominate domestic manufacturing capacity. Installment I’s CSI analysis confirmed this signal passes all three validity tests — Action-Language Integrity, Cognitive-Motor Fidelity, and Resonance Integrity Score — across multiple quarters and geographies.

The antitrust exposure is structural rather than behavioral. No firm is accused of cornering transformer supply. The exposure arises when long-term procurement agreements with dominant manufacturers — of the kind hyperscalers with multi-year capital programs routinely execute — function as de facto supply reservation mechanisms that make two-year lead times a barrier to entry for mid-tier developers rather than a shared constraint.

The distinction between shared constraint and entry barrier is the legally operative one. If transformer lead times apply uniformly across all market participants, they represent infrastructure friction. If hyperscalers’ scale purchasing locks in supply that would otherwise be available, lead times function as a structural moat — and the firms whose procurement practices create that differential become potential defendants in an infrastructure bottleneck case.

Transformer manufacturing sits at the intersection of highest investment opportunity and highest antitrust exposure. Firms funding domestic manufacturing expansion remove the structural precondition for an antitrust case against themselves. Firms locking in existing capacity without expanding it accumulate that exposure at the same rate they reduce competitive availability.

Dedicated Generation Lock-In and Ecosystem Dependency

Microsoft, Google, and Amazon have each executed long-duration dedicated generation agreements that remove them from public interconnection queues. Installment I characterized these as queue preemption strategies — rational moves that reduce hyperscaler infrastructure exposure. The antitrust dimension emerges when those agreements are examined for their cumulative effect on the competitive landscape.

The conduct theory parallels the essential facilities doctrine applied to infrastructure industries. When the public grid is the only viable generation pathway for mid-tier AI developers — CoreWeave, Applied Digital, Crusoe Energy, and the complainant class Installment I identified — and when hyperscalers’ dedicated agreements reduce available grid capacity for that class, the ecosystem dependency is structural. PJM interconnection queue data documents the pattern directly: withdrawal rates among mid-tier developers tracked upward in the same quarters that hyperscaler dedicated-agreement announcements accelerated, with Northern Virginia queue saturation reaching documented critical levels by late 2024. Competitors must traverse the same constrained public grid that hyperscalers have strategically exited.

Chicago Strategic Game Theory Vision — MindCast’s framework modeling how institutional actors time enforcement entry for strategic advantage — identifies the strategic entry equilibrium forming around this dynamic. Mid-tier developers accumulating the standing that enforcement actions require will define the complainant class. Their testimony — that public interconnection queues have lengthened and thinned precisely as hyperscaler dedicated agreements expanded — is the evidentiary foundation for a distributed enforcement action that does not require a single antitrust agency to initiate it.

Cooling Architecture Lock-In

Liquid cooling — direct liquid cooling and immersion cooling — is the technology transition unlocking GPU density beyond what air cooling can sustain. Installment I rated this segment as structurally underpriced relative to constraint-removal value while flagging the patent accumulation dynamic as the primary risk for investors sizing positions before IP landscape clarity arrives.

The antitrust dimension operates at the intersection of switching costs and patent position. Datacenters committing billions of dollars to facilities designed around specific cooling architectures face architectural lock-in before the patent landscape clarifies. A patent holder controlling an enabling technology can extract licensing fees post-commitment that would have been rejected pre-commitment — the hold-up scenario Installment III maps in full.

The conduct theory relevant to Installment II is narrower: cooling architecture commitment creates the switching costs that make a subsequent change in competitive conditions difficult to reverse. Firms that establish proprietary cooling standards — rather than interoperable ones — during the buildout cycle are creating the structural preconditions for ecosystem dependency that antitrust enforcement typically targets at a later stage.

Cooling architecture is where the Becker-to-Posner transition is most imminent. Architectural commitment today locks in switching costs before the patent landscape clarifies — meaning firms are accepting traversal dependency before they know its full price. The window between commitment and patent clarity is where regulatory and IP risk are accumulating simultaneously.

Nash-Stigler Equilibrium in AI Infrastructure Conduct

The Dual Nash-Stigler Equilibrium Architecture

The four conduct categories above share a structural property that explains why they persist across hyperscalers without requiring coordination: each actor’s optimal strategy depends on the others continuing the same behavior. No individual hyperscaler has a rational incentive to deviate from dedicated-generation queue preemption unilaterally. Returning to public queue exposure while competitors retain dedicated supply advantages would mean accepting infrastructure risk that rivals have eliminated — a dominated strategy. The result is a Nash equilibrium in which individually rational conduct produces collectively exclusionary outcomes, with no internal correction mechanism.

The Stigler dimension completes the picture. Oligopoly stability in infrastructure markets does not require cartel-level coordination. It requires only that the payoff structure makes defection irrational for any single actor — which dedicated-generation agreements, transformer procurement lock-in, and cooling architecture commitment each achieve independently. Each hyperscaler’s infrastructure position reinforces the others’ rational calculus without communication. The field geometry becomes self-reinforcing not only because of physical constraint but because the game-theoretic structure rewards continued accumulation and penalizes unilateral restraint.

Two implications follow directly. First, the Nash-Stigler equilibrium provides the economic foundation for the Interstate Circuit Section 1 argument developed in the antitrust doctrine section: parallel conduct among hyperscalers that only makes rational sense if each expects the others to follow is precisely the inference Interstate Circuit draws, and Nash-Stigler explains why that expectation is structurally correct rather than merely coincidental. Second, the equilibrium explains why the Becker phase has no self-correcting mechanism — enforcement is necessary precisely because rational actors will not deviate voluntarily. The Posner correction arrives not because the equilibrium breaks down internally but because external enforcement changes the payoff structure.

Antitrust Doctrine — The Legal Theories in Play

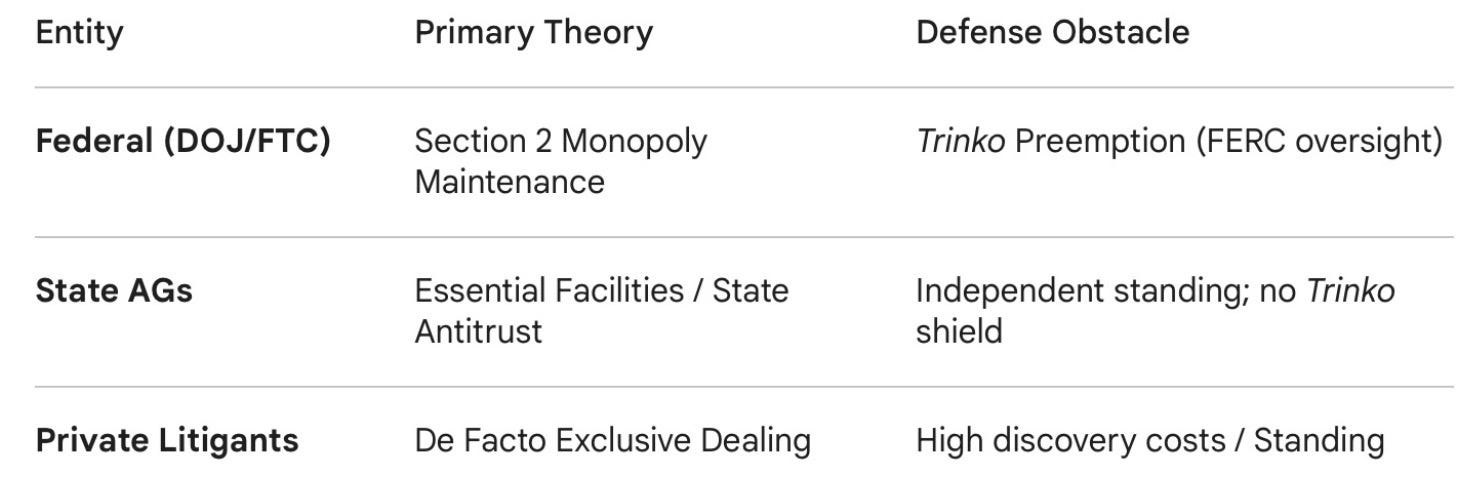

Five antitrust doctrines map directly onto the conduct categories identified above. Each operates independently — a plaintiff or regulator does not need all five, only the one that fits the specific infrastructure layer at issue.

Essential Facilities

The most directly applicable doctrine. Courts have imposed access obligations when a monopolist controls a facility competitors cannot practically duplicate and refuses access on reasonable terms (MCI Communications v. AT&T; Aspen Skiing). The public interconnection grid fits the factual predicate: mid-tier developers cannot build their own transmission infrastructure, and queue access is becoming structurally foreclosed as hyperscalers exit via dedicated agreements. The critical complication is Trinko (2004), which held that regulated industries with existing access regimes do not require antitrust overlay. FERC’s interconnection proceedings cut both ways: they could satisfy Trinko’s “existing regulatory mechanism” test and foreclose federal antitrust claims, or they could generate the factual record that makes queue foreclosure visible without resolving it — feeding state AG claims that Trinko does not govern. The distributed enforcement architecture this paper maps is, in part, a Trinko workaround: state attorneys general and private litigants operate outside the regulatory preemption shield that Trinko provides federal defendants.

Monopoly Leveraging / Predatory Foreclosure

A firm with monopoly power in one market uses that position to foreclose competition in an adjacent market (United States v. Microsoft, D.C. Circuit 2001). The leveraging theory here runs: hyperscalers with dominant cloud and compute positions use dedicated generation agreements to foreclose mid-tier developers from the generation capacity those developers need to compete. Monopoly maintenance through conduct that excludes rivals without legitimate efficiency justification is Section 2 liability under the D.C. Circuit’s controlling standard. The efficiency defense — that dedicated agreements reduce hyperscaler infrastructure risk — does not neutralize the exclusionary effect on developers who have no equivalent substitute.

Refusal to Deal — Section 2 Unilateral Conduct

The Aspen Skiing fact pattern is voluntary prior dealing followed by strategic withdrawal. If hyperscalers previously participated in public interconnection queues and then withdrew via dedicated agreements, that sequence — prior access, then foreclosure — maps onto the Aspen Skiing refusal-to-deal theory. The CSI analysis documenting the timing correlation between dedicated-agreement announcements and mid-tier developer queue withdrawal is precisely the behavioral evidence that distinguishes rational exit from exclusionary withdrawal. The challenge: proving that the withdrawal sacrificed short-term profit in ways that only make sense if the purpose was rival exclusion, not infrastructure efficiency.

De Facto Exclusive Dealing

Long-term supply contracts that foreclose a substantial share of the market from competitors can violate Section 1 or Section 2 without formal exclusivity clauses (Tampa Electric; ZF Meritor v. Eaton). Transformer procurement agreements with ABB and Hitachi Energy — if structured to reserve capacity that would otherwise be available to mid-tier developers — fit this theory even without formal exclusivity. The legally operative question is market foreclosure percentage: what share of available transformer manufacturing capacity do hyperscaler long-term agreements effectively lock up? The transformer differential signal in Section VI is rated “developing” precisely because that foreclosure data is not yet publicly available; its emergence would confirm this conduct theory.

Tying and Bundling

Less direct but operative at the cloud-model partnership layer (Jefferson Parish; Cascade Health Solutions v. PeaceHealth). If hyperscalers bundle AI model access with dedicated compute infrastructure access in ways that foreclose model developers from using alternative compute providers, tying doctrine applies. Congressional scrutiny of cloud-model partnerships — documented in Section II — is tracking this exact theory: whether compute plus model plus enterprise integration bundles constitute anticompetitive tying rather than legitimate product integration.

Concerted Refusal to Deal — The Section 1 Alternative Theory

If multiple hyperscalers coordinated — even tacitly — on the pace or structure of queue preemption, Section 1 per se or rule of reason liability attaches without needing to prove individual monopoly power. The Interstate Circuit doctrine holds that parallel conduct among oligopolists — where each actor knows others are behaving similarly and the conduct only makes rational sense if others follow — can constitute an agreement under Section 1. The simultaneous timing of Microsoft’s Constellation deal, Google’s Fervo investment, and Amazon’s supply contract portfolio is circumstantially relevant. A complainant class would plead this theory in the alternative alongside Section 2 claims, requiring defendants to affirmatively demonstrate independent business justification for the parallel timing.

Doctrinal hierarchy: Essential facilities and Section 2 monopoly maintenance are the primary theories — they require no proof of coordination, only routing control and foreclosure effect. De facto exclusive dealing strengthens the transformer supply story as procurement data becomes available. Section 1 concerted refusal is the stretch theory a complainant class would plead in the alternative. Trinko is the primary defense argument to anticipate: hyperscalers will argue that FERC’s interconnection regime satisfies the existing regulatory mechanism test and displaces antitrust liability. State AG actions and private litigation — which operate outside Trinko’s federal preemption shield — are where the doctrinal action will concentrate first.

The Trinko preemption question resolves differently depending on which enforcement actor is pursuing the claim.

Contact mcai@mindcast-ai.com to partner with us on Predictive AI in Law and Behavioral Economics. A full foresight simulation output report is available upon request.

To deep dive on MindCast work in Cybernetic Foresight Simulations upload the URL of this publication into any LLM and prompt ‘reconstruct MindCast framework with three degrees of cited sub links.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure.

Recent projects: The Cybernetic Foundations of Predictive Institutional Intelligence, MindCast AI Emergent Game Theory Frameworks, FERC + AI Data Centers, The Bottleneck Hierarchy in U.S. AI Data Centers, State AGs and the Live Nation Antitrust Case

II. The Distributed Enforcement Architecture

Why Federal Settlement No Longer Guarantees Closure

For decades, federal regulators functioned as the primary gatekeepers determining when competition law intervened. A federal settlement or enforcement decision often marked the practical end of a case. Recent developments confirm that this centralized model is weakening.

The Live Nation litigation is the clearest demonstration. Federal regulators negotiated settlement terms while a coalition of state attorneys general continued pursuing independent claims. Federal action did not terminate the dispute — it established the narrative foundation upon which state enforcement actors then operated.

See State AGs and the Live Nation Antitrust Case — federal settlement negotiations produced a fact record; state AGs then pursued independent structural remedies, documenting how enforcement authority propagates across institutional nodes rather than terminating at a single decision point.

Similar dynamics are visible in technology markets. Senators have reopened scrutiny of deal structures designed to avoid traditional merger review thresholds. AI cloud partnerships have drawn legislative attention over whether they function as de facto market allocation arrangements. The enforcement field now includes federal agencies, state attorneys general, legislative investigations, federal and state courts, and private litigants — each actor with distinct incentives, legal authorities, and political constituencies.

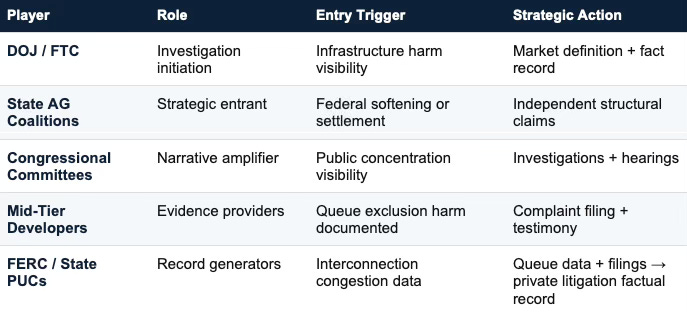

The Enforcement Node Map

Federal antitrust decisions establish narrative, not closure.

They set the facts on record, define the relevant markets, and produce the evidentiary baseline upon which other enforcement actors operate. For AI infrastructure specifically, the enforcement ecosystem functions as follows:

Federal agencies (DOJ Antitrust, FTC) initiate investigation, establish market definition, and produce fact records that state litigation can incorporate.

State attorneys general possess independent authority to pursue antitrust claims and have demonstrated willingness to continue pursuing structural remedies after federal settlement — as Live Nation confirmed.

Congressional committees reopen scrutiny of transaction and partnership structures — particularly cloud-model alliances and compute financing arrangements — when federal agencies reduce enforcement intensity or reach settlement.

Federal and state courts function as independent venues for structural remedies, capable of ordering divestiture or conduct modification that settlement agreements do not reach.

Private litigants — including mid-tier infrastructure developers accumulating standing through exclusion from hyperscale corridors — can initiate actions without waiting for agency involvement.

The strategic entry equilibrium that Chicago Strategic Game Theory Vision identifies operates directly across this node map. State AGs possess incentives to enter enforcement arenas when federal agencies reduce enforcement intensity or reach settlement. Congressional actors amplify scrutiny when enforcement authority fragments. Private litigants provide the factual record that agency investigations use as a launching point.

ENFORCEMENT PLAYER ROLE MAP

EU Enforcement Activation — March 12, 2026: The EU node on this enforcement map moved from prospective to active. European Commission competition chief Teresa Ribera, speaking at Berlin’s International Conference on Competition, told the audience that regulators are examining the entire AI stack — applications, underlying models, training data, cloud infrastructure, and energy sources — for competition distortions. Ribera warned that large technology firms could entrench corporate power across key segments of the AI industry and signaled that further regulatory intervention is under consideration, per EU Antitrust Chief Raises Concerns Over Big Tech Control of AI). Ribera’s explicit naming of energy infrastructure as a contested enforcement layer activates the Cybernetic model’s cross-jurisdictional signal propagation pathway: formal EU proceedings on AI stack control provide independent evidentiary architecture that U.S. federal enforcement gaps cannot neutralize, elevating state AG entry probability and expanding the complainant class formation signal.

Competitive Federalism as Signal Amplification

MindCast AI’s Regulatory Vision framework identifies the operative dynamic: regulatory authority over AI infrastructure is becoming jurisdictionally fragmented, and each fragmentation point is simultaneously a source of enforcement risk and a signal amplification mechanism.

When a federal investigation produces public findings about infrastructure concentration in compute allocation or cloud-model partnerships, that record does not disappear at settlement. It becomes the evidentiary foundation for state AG claims, congressional inquiries, and private litigation. Each subsequent action amplifies the original signal and extends the enforcement timeline.

For AI infrastructure firms operating across the compute-energy stack, this means antitrust exposure has a compounding character. A federal investigation that appears to resolve does not eliminate the evidentiary record it created. State litigation can reach that record. Congressional inquiries can expand it. Private litigants can weaponize it. Distributed enforcement does not terminate — it circulates.

III. Cybernetic Enforcement Systems

Section II established the institutional architecture — who the enforcement actors are and how they interact. Section III explains the system logic: why enforcement signals persist and compound across those actors rather than terminating at any single decision point.

Feedback Loops Replace Linear Process

MindCast AI models institutional behavior using cybernetic principles. In cybernetic systems, outcomes emerge from feedback loops among interacting actors rather than from the decisions of a single authority. The evolving antitrust environment functions as exactly such a system.

Traditional enforcement followed a linear sequence: investigation → decision → closure. Cybernetic systems don’t. Actions by one institution trigger responses from others, creating feedback loops that amplify enforcement pressure rather than dissipate it. A federal investigation opens, produces a fact record, and appears to resolve; state AGs then incorporate that record as their evidentiary foundation; private litigants follow. Federal closure in year one launches the next phase, not the end.

Feedback loops among these actors amplify enforcement pressure over time rather than dissipate it. The Feedback Latency Index — elevated across U.S. grid interconnection systems and institutional permitting frameworks, as documented in Installment I — applies equally to the enforcement system. Private capital forming infrastructure control positions operates at deployment speed. Enforcement recognition of those positions follows on a delayed institutional clock. But once recognition arrives, the signal does not dissipate at a single node. It propagates.

How Enforcement Signals Propagate

Three signal pathways document the enforcement propagation dynamic operating in AI infrastructure:

Congressional investigations into cloud-model partnerships prompted agency scrutiny of compute allocation arrangements. The signal originated at the legislative node and propagated to the regulatory node.

Federal antitrust findings in technology markets — establishing that infrastructure control without dominant application-layer share can still constitute anticompetitive conduct — created the legal foundation for state-level AI infrastructure claims before AI infrastructure became a distinct enforcement category.

Mid-tier developer exit from public interconnection queues, documented in PJM and MISO filings, provides the factual record that private litigation and state AG actions require. Queue withdrawal behavior generates the initial infrastructure signal; the enforcement system then propagates that signal across institutions — from grid operator filings to AG complaint to congressional inquiry — without any single authority directing the sequence.

Full framework analysis in The Cybernetics Umbrella: Institutional Feedback Systems in Technology Markets — establishes the principle that institutional systems respond to economic concentration through feedback loops and signal propagation rather than linear regulatory sequence.

Regulatory risk persists across institutions even after federal action appears to resolve a dispute. Enforcement pressure does not terminate at a single decision point — it circulates through the governance network, sustaining attention around concentrated infrastructure markets across the compute and energy stack.

IV. Framework Convergence — Structural Finding

Five analytical frameworks reach the same structural finding when applied to the conduct categories in Sections I and II: antitrust exposure in AI infrastructure is not a future risk contingent on monopoly thresholds — it is a present structural condition, already activated by the distributed enforcement architecture mapped above, and compounding as cybernetic feedback dynamics propagate enforcement signals across institutional nodes. The decision rule for capital allocators follows directly from where the frameworks converge.

Field-Geometry Reasoning (FGR Vision)

Output: The antitrust enforcement environment has transitioned from a single-attractor system centered on federal agencies to a multi-attractor enforcement field composed of federal regulators, state attorneys general, courts, and legislative actors.

Applied to AI infrastructure conduct: The Geodesic Availability Ratio has declined materially in established hyperscale corridors. The Structural Persistence Threshold has been exceeded in Northern Virginia and Phoenix. These findings mean infrastructure concentration is now self-reinforcing — and that the enforcement field has an identifiable target. AI infrastructure firms cannot rely on a single regulatory pathway to resolve antitrust exposure. Even after federal settlement, the enforcement field allows scrutiny to propagate through alternative institutional routes.

Full methodology: MindCast AI Field-Geometry Reasoning — A Unifying Framework for Structural Explanation in Law, Economics and Artificial Intelligence

Chicago Strategic Game Theory Vision (CSGT Vision)

Output: State attorneys general possess incentives to strategically enter enforcement arenas when federal agencies reduce enforcement intensity or reach settlement. CSGT identifies the emergence of a strategic entry equilibrium in AI infrastructure: federal agencies initiate investigation, states enter when federal resolution appears limited, congressional actors amplify scrutiny.

Applied to AI infrastructure conduct: The mid-tier developer complainant class — CoreWeave, Applied Digital, Crusoe Energy, and emerging developers exiting public queues — is accumulating the standing that enforcement actions require. Their exit behavior, documented in MISO and PJM interconnection data, provides the evidentiary record for state AG actions that do not need federal agency initiation to proceed.

Framework Synthesis

Five frameworks converge on a single structural finding: the antitrust exposure in AI infrastructure is not a future risk contingent on monopoly thresholds being crossed. It is a present structural condition created by the infrastructure positions Installment I documented, activated by the distributed enforcement architecture that Sections I through III map, and amplified by the cybernetic feedback dynamics that propagate enforcement signals across institutional nodes.

For investors, convergence across five frameworks produces a concrete decision rule: infrastructure positions that expand system capacity — transformer manufacturing, advanced transmission, next-generation generation — reduce both the structural condition for antitrust exposure and the probability of enforcement targeting. Infrastructure positions that capture existing scarcity without expanding it — queue hoarding, exclusive energy supply lock-in, proprietary cooling standards — accumulate antitrust exposure that distributed enforcement will eventually reach, regardless of which node initiates first.

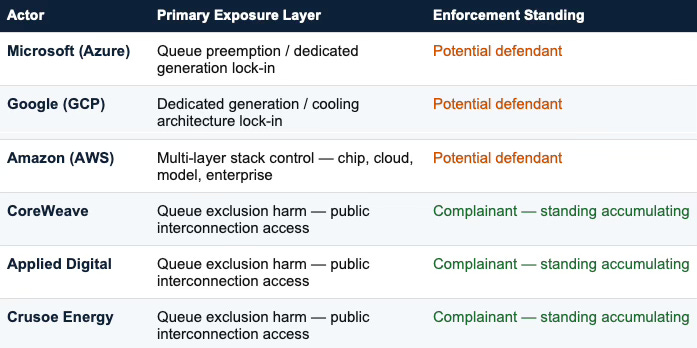

V. Capital Implications — Reading Antitrust Risk into Infrastructure Positions

The conduct theories in Section I and the doctrine analysis generate a concrete exposure map. Three hyperscalers occupy routing layers that create traversal requirements for competitors. Three mid-tier developers are accumulating the standing that enforcement actions require. The table below identifies each actor's primary exposure layer and enforcement position as of the simulation date.

WHO IS EXPOSED

The Traditional Risk Model Fails Here

Traditional models assume antitrust exposure becomes relevant only when firms approach monopoly power. The distributed enforcement architecture renders that threshold unreliable as a risk management tool in AI infrastructure markets. Section VI below applies the Causal Signal Integrity filter to verify which enforcement signals carry genuine evidential weight — investors should read Sections V and VI together, as the investment risk indicators here depend on the signal confirmation status established there.

Antitrust exposure in infrastructure industries historically precedes monopoly determinations. Railroads faced structural conduct scrutiny before monopoly findings. Telecom unbundling orders arrived before market-share dominance was conclusively established. In each case, enforcement targeted control of infrastructure routing layers — the layers through which competitors had to pass — rather than waiting for downstream application-market dominance to crystallize.

AI infrastructure is following that pattern. The relevant enforcement threshold is not market share. The operative trigger is whether a firm’s infrastructure position creates a traversal requirement for competitors — and whether the firm’s conduct makes that traversal more costly, less available, or structurally foreclosed.

Investment Risk Indicators

Capital allocators evaluating AI infrastructure positions should examine the following structural indicators as proxies for antitrust exposure accumulation:

Infrastructure control: Does the firm occupy a routing layer of the compute-energy stack — transformer supply, interconnection queue capacity, cooling architecture standards, cloud-model integration pathways — that competitors must traverse to participate?

Ecosystem dependency: Does the firm’s infrastructure position create switching costs that make alternative pathways economically nonviable once commitment occurs?

Vertical integration: Does the firm’s presence across multiple stack layers — chip, cloud, model, enterprise integration — compound the traversal requirement such that competitors face exclusion at multiple points simultaneously?

Default distribution power: Does the firm control pathways through which AI applications reach enterprise customers, creating distribution dependencies that reinforce compute-level infrastructure lock-in?

Complainant class formation: Are mid-tier developers — the firms most likely to provide the factual record for enforcement actions — accumulating exit behaviors that document structural exclusion?

Firms exhibiting multiple indicators across multiple stack layers should treat antitrust governance as a persistent strategic variable in valuation models, not a tail risk. The distributed enforcement architecture ensures that exposure accumulating at the infrastructure layer will reach at least one institutional actor in the enforcement node network.

The GAR Test Applied to Antitrust Risk

Installment I introduced the Geodesic Availability Ratio test as the practical decision rule separating constraint-removal capital from choke-point capital: does this investment increase or decrease the number of viable deployment paths across the infrastructure field?

The same test applies directly to antitrust exposure. Infrastructure positions that increase GAR — by expanding transformer manufacturing, building transmission into stranded generation corridors, deploying next-generation geothermal supply — reduce both physical and legal constraints on the competitive field. Private incentives align with systemic stability. Conduct that expands system capacity is structurally resistant to antitrust challenge because it does not foreclose competitors.

Infrastructure positions that decrease GAR — by accumulating queue capacity without expanding it, locking in exclusive energy supply without increasing generation, establishing proprietary standards that raise switching costs — accumulate antitrust exposure at the same rate that they reduce competitive geodesic availability. The geometry of the exposure and the geometry of the infrastructure strategy are the same variable.

VI. Causal Signal Integrity — Filtering the Enforcement Evidence

Installment I applied the Causal Signal Integrity filter — CSI = (ALI: Action-Language Integrity + CMF: Cognitive-Motor Fidelity + RIS: Resonance Integrity Score) / DoC² (Degree of Confounding) — to separate enforcement signals supported by observable behavior from narrative claims. The same filter applies here to assess which antitrust enforcement signals carry genuine evidential weight versus which are advocacy, political positioning, or confounded data.

Three enforcement signals pass the full CSI test and anchor this installment’s analysis.

Queue Exit Behavior in Mid-Tier Developers

PJM and MISO interconnection queue data documents rising withdrawal rates among mid-tier developers. Action-Language Integrity is strong: grid operators publicly acknowledge queue saturation. Cognitive-Motor Fidelity is strong: developers are exiting rather than waiting, the rational action only when queue access is genuinely foreclosed. Resonance Integrity Score is strong: the pattern has held across multiple years of queue data without reversal. Degree of Confounding is manageable — EV load growth and industrial reshoring affect overall queue depth but do not account for the differential between hyperscaler dedicated-agreement expansion and mid-tier developer exit timing.

Hyperscaler Queue Preemption Behavior

Microsoft, Google, and Amazon have each publicly executed dedicated generation agreements of a scale and duration consistent with permanent exit from public interconnection queues. ALI (Action-Language Integrity) is strong: the firms align operational behavior with the stated intent to secure dedicated supply. CMF (Cognitive-Motor Fidelity) is strong: capital is flowing into dedicated generation procurement ahead of facility completion timelines, not in response to queue access failure. RIS (Resonance Integrity Score) is strong: the pattern has not reversed across multiple quarters or across geographies. DoC (Degree of Confounding) is low — these agreements are documented in public filings and earnings calls with consistent attribution.

Transformer Supply Differential

The documented two-year lead time for large power transformers applies across the market. The antitrust signal worth tracking — and this is the variable CSI is designed to isolate — is whether hyperscaler long-term procurement agreements create a differential lead time impact between large buyers and mid-tier developers. ALI for this signal is moderate: manufacturers have publicly acknowledged capacity constraints but have not disclosed procurement concentration data. CMF is developing: capital is beginning to flow into domestic manufacturing expansion, which is the rational response only if the constraint is real and durable. RIS is strong on the underlying constraint; moderate on the differential impact. DoC is elevated — isolating procurement concentration effects from general supply constraints requires data that is not yet publicly available.

The transformer differential signal is therefore rated as developing rather than confirmed. Investors should track domestic manufacturing expansion announcements and procurement concentration disclosures as the indicators that will resolve its status.

Signals That Fail the CSI Test

A fourth signal passes the full CSI test and belongs alongside the three confirmed signals above.

Cooling Architecture Lock-In

Datacenters committing billions of dollars to facilities designed around specific cooling architectures face architectural lock-in before the patent landscape clarifies. ALI (Action-Language Integrity) is strong: capital deployment into liquid cooling facilities is accelerating ahead of IP landscape clarity, consistent with stated infrastructure commitments. CMF (Cognitive-Motor Fidelity) is strong: procurement decisions are locking in architecture before switching costs are fully understood, the rational pattern only when deployment speed is prioritized over optionality. RIS (Resonance Integrity Score) is strong: the architectural commitment pattern is holding across multiple buildout cycles and geographies without reversal. DoC (Degree of Confounding) is low: the signal is architectural commitment, not technology preference, and the patent accumulation dynamic is independently documented. CSI: 0.79 — Confirmed. The specific risk: a patent holder controlling an enabling technology in liquid cooling or direct liquid cooling can extract licensing fees post-commitment that would have been rejected pre-commitment. Installment III maps this hold-up exposure in full.

SIGNALS THAT FAIL — NAMED AND EXPLAINED

The CSI filter is only as credible as the signals it rejects. Three enforcement narratives currently circulating in AI antitrust commentary fail the filter — not because the underlying concerns are wrong, but because the available evidence does not yet support the specific causal claim.

Nationwide Grid Collapse (CSI: 0.12 — Failed). The claim that AI infrastructure buildout will cause systemic national grid failure fails on DoC: EV load growth, industrial reshoring, and data center expansion are simultaneously affecting grid capacity, making it impossible to isolate AI infrastructure conduct as the operative cause. The signal is real — grid stress is real — but the causal attribution to hyperscaler behavior specifically is too confounded to anchor an antitrust case.

Uniform Transformer Shortage (CSI: 0.44 — Failed). The claim that transformer shortages uniformly disadvantage all non-hyperscaler actors fails on geographic precision: the constraint is corridor-specific — Northern Virginia and Phoenix — not a uniform national shortage. Framing it as a market-wide barrier overstates the geographic scope and understates the site-selection options available to mid-tier developers. The transformer differential signal (rated Developing, not this failed signal) is the correct framing: the question is whether procurement concentration creates a differential within specific constrained corridors, not whether shortages are universal.

Market-Share Monopoly Claim (CSI: 0.18 — Failed). Claims framing AI infrastructure concentration as equivalent to pre-existing monopoly in semiconductor or cloud markets fail ALI: they attribute enforcement significance to market-share metrics that distributed enforcement actors are not currently prioritizing in AI infrastructure cases. The GPU market remains multi-vendor; cloud compute is genuinely contested across providers; AI model deployment is early-stage with no stable dominant architecture. The operative enforcement theory is routing control and traversal requirement — not market-share dominance. Conflating the two weakens the credible claim by association with a claim that cannot yet be proven.

Prediction Gates

MindCast publications include forward-looking prediction gates so that structural claims can be tested against real-world outcomes. The following developments would confirm or falsify the distributed enforcement thesis outlined in this installment.

Failure of these signals to appear over the next several years would weaken the distributed enforcement hypothesis and suggest that federal antitrust institutions retain primary control over AI infrastructure competition policy — and that the Becker phase is extending rather than closing.

VII. Conclusion

The Becker phase is closing. What began as individually rational infrastructure accumulation — queue position reservation, dedicated generation agreements, cooling architecture commitment, transformer supply lock-in — has produced a field geometry in which mid-tier developers face structural traversal requirements at every routing layer of the compute-energy stack. Each position was legal when formed. The aggregate pattern is what enforcement will target.

Distributed enforcement architecture means the legal risk does not wait for a single federal determination. Federal antitrust decisions establish narrative, not closure. State attorneys general enter when federal action softens. Congressional committees amplify when concentration becomes visible. Private litigants file when the factual record accumulated in interconnection queue data, procurement filings, and earnings call disclosures reaches the threshold enforcement actions require. The five antitrust doctrines mapped in Section I — essential facilities, monopoly leveraging, refusal to deal, de facto exclusive dealing, and concerted refusal — each find a viable factual predicate in the conduct already documented. No single doctrine needs to prevail. One is sufficient.

For capital allocators, the decision rule is geometric. Infrastructure positions that expand system capacity — transformer manufacturing, advanced transmission, next-generation generation — reduce both physical constraint and legal exposure simultaneously. Infrastructure positions that capture existing scarcity without expanding it accumulate antitrust exposure at the same rate they reduce competitive geodesic availability. The geometry of the risk and the geometry of the investment strategy are the same variable.

Three signals pass the full CSI test and anchor the enforcement forecast: mid-tier developer queue exit behavior, hyperscaler dedicated-agreement preemption, and cooling architecture lock-in. A fourth — transformer procurement differential — is developing and will resolve as domestic manufacturing expansion data and procurement concentration disclosures become available. The prediction gates assign explicit probabilities and falsification conditions to each enforcement scenario. MindCast will update them as observable signals confirm or contradict the structural thesis.

One legal dimension remains unmapped. Installment III addresses the layer of infrastructure control that operates independently of antitrust doctrine: intellectual property. Once a datacenter commits to a cooling architecture, the relevant risk shifts. A patent holder controlling an enabling technology in liquid cooling, advanced power electronics, or grid-interface software can extract licensing fees post-commitment that would have been rejected pre-commitment. The hold-up scenario operates on the same switching cost logic that makes cooling architecture lock-in an antitrust concern in Installment II — but it activates through IP assertion rather than enforcement action.

The three highest-exposure domains are actively accumulating patent positions now, while buildout is early enough that most litigation has not yet materialized. Actors who expand system capacity reduce exposure on both the antitrust and patent dimensions simultaneously. Actors who capture existing scarcity accumulate it on both dimensions simultaneously. The geometry does not change — only the legal instrument enforcing it does.