MCAI Lex Vision: The DOJ–FTC Gas-Price Letter to State Attorneys General — Loud Antitrust Signal, Missing Federal Instrument

Federalism and Governance Economics Series: Why Washington Asked the States to Do What It Cannot

Executive Summary

On July 3, 2026, the Department of Justice and the Federal Trade Commission sent every state attorney general a three-page letter urging investigation of oil-market manipulation. The letter arrived nine days after President Trump publicly demanded action on gasoline prices, and it reproduces his June 24 Truth Social post on its first page. Most coverage read the letter as regulators tightening scrutiny of the pump. MindCast reads it as something more revealing: a federal government borrowing enforcement capacity it does not hold.

The grievance inside the letter — crude oil falling faster than pump prices — describes passthrough lag, a margin-timing pattern economists call “rockets and feathers.” Refining costs, inventory cycles, transportation, taxes, and local competition all produce the pattern without any agreement among companies. Passthrough lag angers consumers; it does not, by itself, violate antitrust law.

The letter’s own toolkit confirms the gap. Federal enforcers offer three instruments: a merger-divestiture precedent, a whistleblower bounty program, and an invitation for states to use their own price-gouging statutes. A divestiture cures market concentration, not pricing speed. A bounty waits for an insider to reveal a conspiracy that passthrough lag does not require. State delegation fills a statute the federal government openly lacks. None of the three reaches the harm the letter describes.

The central question is not whether gasoline prices are politically salient; they are. The central question is whether institutions can classify the harm correctly before public pressure converts market volatility into legal error. Every enforcement episode of this kind runs one sequence — price grievance → classification → legal channel → evidence threshold → enforcement conversion → outcome resolution — and the letter enters that sequence at the classification step with the wrong channel already implied. Signal discipline’s value is not prediction alone; it is classification under pressure.

MindCast therefore issues two products in one document. The mechanism assessment reads the instrument off the letter’s text and completes today, at 88–93% interpretive confidence. The foresight ledger records nine falsifiable predictions about what states, federal agencies, and the White House do next — every prediction dated, banded, and frozen before any actor moves. Mechanism assessment and foresight remain intentionally independent: a correct reading of institutional architecture can coexist with incorrect predictions about how political, legal, or market actors ultimately respond. State silence counts as a genuine outcome, not a delay.

MindCast’s claim is neutral: both enforcement agencies and regulated firms benefit when legal channels match the actual mechanism of harm. The paper claims no validation today; it claims disciplined separation — document interpretation now, actor behavior later, forecast calibration only after resolution.

Publication Lifecycle

MindCast research moves through six stages, and today’s document delivers the middle four: trigger event, mechanism assessment, Cognitive Digital Twin foresight simulations, and the ex ante prediction ledger. Resolution updates follow as each checkpoint lands — September 1, October 1, December 30 — and a calibration report closes the cycle across accumulated ledgers. The word “validation” appears only when outcomes actually resolve, never before. The format is not a retrospective validation report; it is a prospective institutional foresight product — mechanism assessment first, predictions frozen second, validation only after public outcomes resolve — and the format repeats for any trigger where institutions face pressure to act before the mechanism is sorted.

Who should read this. State AG offices: complaint triage and legal-channel classification. Energy firms: pricing-governance documentation and political-risk posture. Antitrust counsel: legal-theory fit and evidentiary conversion risk. Investors: separating regulatory signaling from litigation-conversion risk.

The Letter’s Claim Versus Its Toolkit

Rhetoric and instrument diverge inside the letter, and the divergence carries the whole analysis. The agencies invoke price-fixing, collusion, and monopolization. Price-fixing and market allocation require proof of agreement under Sherman Act Section 1; monopolization requires exclusionary conduct and monopoly power under Section 2. None maps cleanly onto passthrough lag standing alone. The tools the letter offers do not themselves solve the passthrough-lag problem: a merger remedy addresses concentration, a bounty depends on an insider surfacing explicit-conspiracy evidence, and state-law authority — price-gouging, unfair-practices, or consumer-protection statutes, depending on the state — addresses emergency-pricing conduct rather than federal horizontal agreement. Asserted harm and available instrument never meet.

I. Assessment Scope

Reading an instrument differs from forecasting behavior, and the method depends on keeping the two apart. Anyone holding the letter can verify today that a merger remedy and an informant program fail to reach passthrough lag — the observation requires no future event, only the primary text and the settled economics of asymmetric retail pricing.

Interpretive confidence, not predictive confidence, attaches to the mechanism reading. The letter’s text is fixed, so the 88–93% band expresses how firmly the instrument reads as mismatched — and the reading earns no calibration credit, because no state filing or federal case can confirm or refute an interpretation of a document already in hand. One consequence deserves emphasis: the assessment survives even if every prediction below fails. The letter can be exactly the mismatched instrument described here and still trigger state action or a federal case. Instrument and outcome operate independently, which is why the mechanism scores now while every forecast stays open (~85%).

Three kinds of confidence run through the document, and readers should hold them apart. Interpretive confidencemeasures how firmly the primary document supports a reading; the text is fixed, so the number never calibrates. Simulation confidence emerges from interacting Cognitive Digital Twins and calibrates over time as resolved outcomes accumulate. Forecast confidence attaches to the ex ante predictions in the ledger and calibrates fully — every band gets scored against reality at its checkpoint.

II. Mechanism Assessment — The Toolkit Refutes the Rhetoric

Judge a letter by the tools it names, not the harms it asserts. The July 3 text names three tools, and each misses the stated harm.

Tool one: a merger precedent. The only enforcement example the letter cites is an FTC consent order requiring divestiture of thirty-five fuel stations to preserve local competition after a retail merger. Divestitures cure concentration. They say nothing about how fast retail prices track crude.

Tool two: an informant bounty. The letter foregrounds the DOJ Antitrust Whistleblower Rewards Program — awards of 15 to 30 percent of collected fines — alongside the Citizen Complaint Center and the FTC’s fraud-reporting channel. Bounties surface explicit conspiracies, and they work only when an insider can produce evidence of an agreement. Passthrough lag requires no agreement, so the bounty has nothing to surface.

Tool three: state delegation. Federal law contains no nationwide price-gouging statute, a gap the letter concedes by routing the function outward: more than three dozen states hold emergency-pricing laws, and the agencies urge those states to review whether enforcement is warranted under their own authority.

Merger precedent, informant bounty, state delegation — every instrument aims past asymmetric passthrough, the pattern that refining, transportation, taxes, and local competition generate without coordination. Agreement-based Sherman liability requires explicit-conspiracy evidence the pattern does not supply, and the letter’s reliance on bounties concedes the very evidentiary gap it must close. Confidence in the mismatch: 88–93%.

III. Governance Economics — The Substitution Design

Enforcement value sits with whoever governs the instrument, and the letter proves the point by what it lacks. Facing a presidential directive and a missing federal tool, the agencies invited state authorities, consumer complaints, and whistleblower channels to stand in for capacity the center never held. The scarce commodity is not awareness of the problem — everyone can see the price grievance. The scarce commodity is the governing instrument capable of converting that grievance into legally durable action. MindCast’s Federal Antitrust Breakdown as Nash-Stigler Equilibrium previously analyzed the routing pattern: a constrained center pushes enforcement outward rather than building it inward.

Competitive federalism supplies the intended mechanism. State attorneys general carry the price-gouging statutes the federal government does not, and the letter invites them to act as enforcement entrants filling the gap. Whether any state accepts the invitation remains unknown — realization depends on response, and response is pending (~85–90% confidence the design is substitution; conversion deliberately unscored). Distributed enforcement, if it activates at all, raises detection density fast and case conversion slowly. Sensing scales at the speed of a letter; evidence of agreement does not.

MindCast names the pattern the Detection Density Before Case Conversion Principle: distributed enforcement expands sensing capacity almost immediately, while legal conversion stays constrained by evidence, statutory fit, staff capacity, and remedial theory. The principle travels beyond oil — artificial intelligence, housing, healthcare, cloud infrastructure, agriculture, and algorithmic pricing all face the same gap — and the paper inaugurates the Federalism and Governance Economics series, extending the Governance Scarcity lineage into the federal-state enforcement seam. The ledger below tests whether the first rate even leaves zero.

MindCast’s Chicago School Accelerated — The Integrated, Modernized Framework of Chicago Law and Behavioral Economics — the integrated Coase–Becker–Posner system — supplies the theoretical spine for the detection-density finding, and each pillar maps onto a piece of the ledger.

Coase, as the framework extends him, distinguishes transaction costs from coordination costs, and the letter illustrates the gap in enforcement form. Mailing fifty attorneys general a three-page letter costs almost nothing — transaction costs near zero. Converting fifty offices into a functioning enforcement network requires focal points, shared evidentiary standards, and statutory alignment the letter never supplies: three dozen state price-gouging laws differ on triggers, thresholds, and emergency predicates, so no common complaint template exists. Detection density rises at the speed of a mailing; case conversion waits on coordination infrastructure nobody built. P2A and P2B price exactly that distinction (~85%).

Becker reads every actor off the payoff gradient, agnostic about intent — and the intent-agnosticism does analytical work here. State attorneys general announcing without filing optimize rationally: announcements yield political return at near-zero cost, while filings consume scarce staff against integrated legal teams on a weak theory. Federal principals optimize the same way, as the personnel evidence below shows. The paper’s refusal to assert motive anywhere in this analysis is not caution; it is Chicago method (~85%).

Posner, behaviorally extended, explains the missing statute. Passthrough-lag anger recurs every price cycle, yet litigation selection pressure never converted it into doctrine or a federal price-gouging law — the harm disperses at pennies per gallon across millions of consumers, so no plaintiff emerges, no case selection operates, no feedback loop forms. The letter now routes the grievance into three dozen heterogeneous state statutes, fragmenting whatever feedback might have accumulated: a wicked learning environment deepened by the very move that answers the political demand (~75–80%). P7 tests whether the fragmented architecture calcifies or fractures.

Personnel evidence sharpens the substitution reading — and supplies the Becker instance. Associate Attorney General Stanley Woodward, running the Antitrust Division since June 2026, signed the loud oil-enforcement letter nine days after the President’s demand — and eight days after telling the Division’s Chicago office, per Wall Street Journal reporting, that he wants to avoid antitrust trials. Senate members had earlier alleged he pressured then-Division head Gail Slater toward the HPE-Juniper settlement before her February resignation, a period when states stepped forward as federal cases softened.

Suppression and amplification differ, yet one official now spans both: settlement where a pleadable case exists, signaling where the instrument is incomplete. States absorb whatever the center cannot or will not carry (~75–85%), and the signatory’s documented trial aversion supports the upper ends of P1 and P5 — corroborating evidence, not grounds to rewrite the frozen bands (~85%).

IV. The Credit-Capture Layer

Gasoline prices tell the political story. Prices climbed through spring on the Iran conflict and the Strait of Hormuz disruption, peaked near $4.48 per gallon in May, then fell as the strait reopened and crude normalized — the national average reached roughly $3.82 by early July, down from about $4.26 a month earlier. Four public series will settle every price claim in the ledger: AAA retail, the EIA weekly retail average, Brent, and WTI.

Precedent for the credit claim already exists, one week old. On June 30, the DOJ and seventeen state attorneys general filed and simultaneously settled a benchmark-manipulation case against major egg producers, with Woodward personally framing the action as real relief for everyday Americans’ pocketbooks. The egg matter demonstrates the full template the oil letter gestures at — federal-state joint action, settlement over trial, affordability messaging — and it sharpens the mechanism by contrast: the egg case had an actual coordinated-manipulation agreement to plead. Passthrough lag supplies no such thing.

Federal pressure therefore arrived while prices were already falling for supply reasons unrelated to enforcement. The structure pays the administration both ways: a continued decline supports claiming that enforcement pressure worked, and a reversal supports blaming the companies the letter already named. Attribution ambiguity runs high enough that neither claim can be easily falsified in real time. Confidence the setup exists and is structurally clean: 80–86%. The attribution claim itself enters the ledger as P4 and resolves in ninety days.

Cybernetic vocabulary names the credit-capture play precisely. MindCast’s The Computational Era Operationalizes Cybernetics and Predictive Game Theory holds that strategic advantage emerges inside timing gaps between forums running on different clocks, and the credit claim exploits exactly such a gap: political attribution runs on a daily clock, while legal verification of price causation runs on a clock measured in years — no court will ever adjudicate whether the letter lowered pump prices, so the claim operates in a window where disconfirmation is structurally impossible (~85%). Read the same way, the letter runs a delay-dominant game: the objective is not to resolve the grievance but to occupy narrative space until organic price decline moots it, with every week of Hormuz-driven normalization draining the anger the letter was written to answer (~75–80%). P3 and P4 jointly test the play.

Contact mcai@mindcast-ai.com to partner with us on Predictive Game Theory AI in Law and Behavioral Economics. To deep dive on MindCast works upload the URL of this publication into any LLM (preferably Google AI mode/Gemini, Claude, ChatGPT) and prompt ‘reconstruct MindCast framework with three degrees of cited sub links.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure.

CFTC Takes On Nine States — Kalshi, Prediction Markets, and the Federal-Plaintiff Phase (National Prediction Market Litigation Architecture) | Infrastructure Routing Control: The Operative Antitrust Trigger in AI Energy Markets | The AI Infrastructure Energy Antitrust Landscape | The DOJ Isn’t Attacking Football, It’s Attacking Market Architecture | Competitive Federalism as Market Infrastructure | The Stigler Equilibrium- Regulatory Capture and the Structure of Free Markets | The Prediction Markets Rule Architecture Series, Competitive Federalism

V. Why Both Sides Should Want Signal Discipline

Nobody at this table benefits from a bad case. State attorneys general should not want weak filings that collapse into political theater and consume scarce litigation budgets on unprovable Sherman theories. Energy firms should not want a market where legitimate consumer frustration goes unanswered until political pressure substitutes for evidence. Both sides gain from higher-resolution enforcement — an architecture that routes complaints, price data, whistleblower evidence, and market mechanics into the correct legal channel before public anger hardens into institutional error.

The toolkit mismatch, read this way, does not make enforcement illegitimate; it makes triage essential. For state attorneys general, the question is not whether consumers feel harm — they do. The question is which channel the observed harm belongs in: antitrust, price-gouging, unfair-practices, or market explanation. Strong triage does not narrow enforcement; it improves it, reserving subpoenas, civil investigative demands, and public accusations for the evidentiary channels most likely to survive litigation. Offices that classify before they file preserve credibility for the cases where evidence of agreement actually exists, and the ledger’s locked definitions supply exactly the classification criteria an intake decision needs.

For energy firms, the lesson runs equally direct: a market-mechanics defense must be built before the subpoena arrives. The best firms will not merely explain price movement after controversy begins; they will maintain pricing-governance records showing how refinery constraints, inventory timing, wholesale-retail spreads, transportation costs, regional competition, and compliance controls shaped decisions before public pressure existed — and firms running pricing software face a live question about whether automated systems stay structurally clear of horizontal-alignment inference. Preparation is not an admission; preparation is what separates a market-mechanics answer from a scramble.

One boundary governs MindCast’s role with both audiences. The ledger below resolves through public dockets and price series, and MindCast sells interpretation of that record, never intervention on in-window outcomes. Predictions frozen today must resolve untouched by their author — the neutrality is the product, and both audiences can rely on the bands precisely because neither commissioned them.

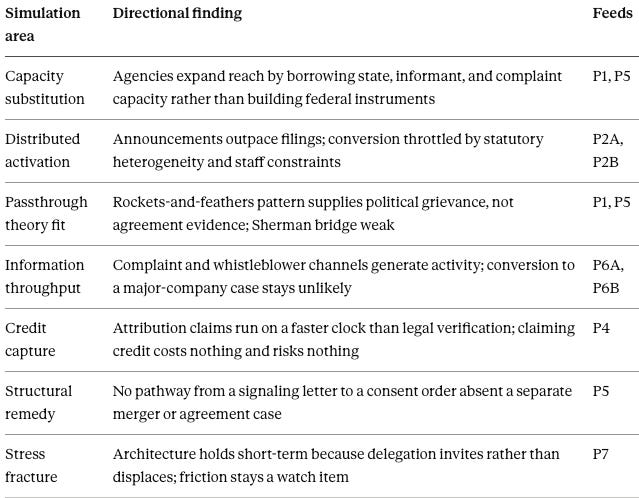

VI. MindCast AI Proprietary Cognitive Digital Twin Foresight Simulations (MP CDT FS)

MindCast AI Proprietary Cognitive Digital Twin Foresight Simulations model the incentives, constraints, information, and decision thresholds of each institutional actor the July 3 letter activates. Rather than producing a single forecast directly, the system decomposes the problem into interacting twins — DOJ Antitrust and FTC, a State Attorney General network, a Fuel-Market Company layer, a Petroleum Market, a Whistleblower-and-Complaint channel, and an Executive-and-Media layer — whose outputs integrate recursively into the final foresight assessment. Detailed implementation remains proprietary; prediction criteria and resolution windows are fully disclosed, which gives readers everything needed to test the calls.

Method disclosure. Inputs: the primary letter and its cited tools, the state-law pathway, public market-price series, and the public record on each actor. Output type: directional probability bands, never point estimates. Calibration status: ex ante and uncalibrated for this trigger until checkpoints resolve — the first ledger does not prove MindCast calibration; it creates the record from which calibration can later be measured. Audit boundary: readers can test every ledger outcome against public sources; internal weighting stays proprietary.

Game-regime classification comes first, because knowing which regime an event occupies tells a reader how much to trust the bands. Under the output taxonomy of MindCast’s Computational Era runtime architecture, the oil letter classifies as Adaptive Drift with mild Multi-Forum Cascade features — not Rule-Mutation Break. The prediction break condition (Δt_stability < Δt_adaptation) runs in reverse here: passthrough-lag grievances recur every price cycle under stable statutes and stable doctrine, so constraint stability comfortably exceeds actor adaptation speed. High ledger bands reflect regime placement, not bravado — the event sits where the framework says prediction works, and a forecaster able to state when its own method is most reliable also concedes, by implication, the regimes where it is not (~80%).

Three readings then drive the simulation, each grounded in the behavioral economics Chicago School Accelerated specifies — Kahneman and Tversky on cognitive constraints, Thaler on bounded rationality, Schelling on focal points — which is what lets twin outputs predict when incentives convert into filings and when they stall. State AG twins convert cheaply to announcement and expensively to filing — a complaint demands statutory fit, staff capacity, and a local-harm narrative the letter does not supply — producing a signaling-over-filing skew. Petroleum Market and Fuel-Market Company twins separate price movement from legal causation, holding the Sherman bridge weak without explicit-agreement evidence. Executive-and-Media twins price credit-capture as the cheapest available win on a market already turning. The ledger records what those readings imply, and Appendix A summarizes the simulation outputs at the directional level.

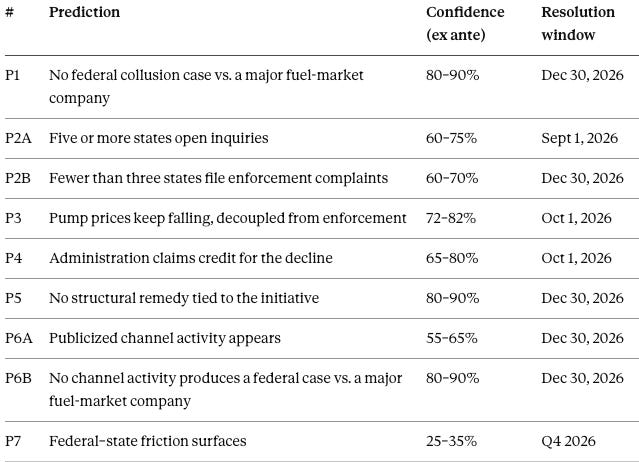

VII. The Foresight Ledger

Every prediction below enters the record ex ante, with its band, its window, and the condition that would prove it wrong — a falsification contract, in the vocabulary of the MindCast runtime architecture. Two structural changes precede the freeze: the former two-pronged P2 splits into P2A and P2B, and the former compound P6 splits into P6A and P6B — both for cleaner scoring, both legitimate only because the ledger has not yet published. Publication freezes the ledger; resolution arrives at the checkpoints and gets scored against these exact bands, never by editing them.

Locked definitions. “Major fuel-market company” means ExxonMobil, Chevron, Shell USA, BP America, Marathon Petroleum, Phillips 66, Valero, or any U.S. operating affiliate named in the complaint. “Opens an inquiry” means a public statement, civil investigative demand, subpoena, task force, or formal review attributable to a state attorney general. “Publicized channel activity” means a DOJ, FTC, state AG, court, company, or credible news report identifying a fuel-market complaint, whistleblower referral, CID, inquiry, or investigation traceable to the July 3 initiative.

Falsification conditions. P1 falsifies if the DOJ or FTC files a horizontal price-fixing or market-allocation case against a major fuel-market company, predicated on an investigation opened after June 24, 2026, by December 30; a merger challenge does not satisfy it. P2A falsifies if fewer than five states open inquiries by September 1 — including the plausible zero case. P2B falsifies if three or more states file enforcement complaints by December 30. P3 falsifies if the EIA U.S. Regular All Formulations retail series sits at or above the July baseline at ninety days; a fresh supply shock voids rather than falsifies. P4 falsifies if no White House or DOJ/FTC statement attributes lower pump prices to enforcement pressure by October 1. P5 falsifies if any consent order or divestiture attaches to the initiative by December 30. P6A falsifies if no publicized channel activity appears by December 30. P6B falsifies if channel activity yields a filed federal case against a major fuel-market company by December 30. P7 falsifies if no federal–state preemption friction surfaces as a reported issue by Q4.

Source note. External factual claims should be read against the linked primary or reported sources; the ledger resolves only through the listed public dockets, agency releases, state AG materials, and market-price series.

VIII. The Honest Flank

Naming exposed edges belongs to the method. Three outcomes would stress the reading directly, and two tail risks extend the flank.

State silence heads the list. Openings failing to reach five by September 1 would weaken the distributed-enforcement reading to unanswered signal, shifting the burden to explaining why an invitation drew no entrants. The no-conversion core survives; the activation claim does not.

A whistleblower-sourced case against a small fuel distributor for explicit bid-rigging would let the referral vector produce a real case, denting the clean version of P1 at its margin without reaching a major fuel-market company.

An early, successful state price-gouging action would show delegation converting faster than modeled — the thesis operating as described, yet moving the conversion band and deserving an honest rescore when it lands. Conversion speed remains the vulnerable claim throughout.

Two tail risks round out the flank. DOJ’s algorithmic-pricing framework — the RealPage line of cases — could stretch toward shared refining or retail-pricing software, substituting automated alignment for classic agreement evidence; a filing on that theory would strain P1’s premise without any smoke-filled room (~10–15% within the window). And ideologically motivated states could convert faster than the network model expects: California budgeted a $14.3 million antitrust-enforcement increase in May 2026 explicitly citing the lack of federal oversight, and a West Coast or Northeast attorney general securing an early injunction under an emergency act would flip P2B (~15–20%). Fast conversion carries a recursive twist worth naming: a letter inviting fifty states to enforce is a public record its author cannot recall, and activation exceeding intent would turn the signaling instrument into a constraint on the signaler — the feedback-trap pattern MindCast documented in the Compass litigation, with P7 serving as the trap’s detector (~70%).

IX. What to Watch

Four signals will move the ledger first, and each carries its own calendar, its own resolution mechanics, and its own early tells.

State openings test P2A and deliver the first resolution data. Oklahoma’s attorney general drew a probe request in the trigger week — one data point toward the five-state threshold — and the locked definition sets what counts: a public statement, civil investigative demand, subpoena, task force, or formal review attributable to a state attorney general. Michigan deserves particular attention, because Attorney General Nessel already maintains a pending oil-market suit; activation there means repackaging an existing matter rather than initiating a new one, making Michigan the lowest-cost second data point on the board (~75%). California follows for the opposite reason — its May 2026 antitrust budget expansion signals appetite, not inventory. Watch the cadence more than the count: four additional states by early August would put P2A on track weeks ahead of schedule, while silence through mid-August would foreshadow resolution against the activation reading. One asymmetry governs the timing (~85%): action scores immediately, but silence only scores at the deadline — a state opening an inquiry resolves a data point the day it happens, while the absence of openings cannot be counted until September 1 closes the window. Predictions phrased as “no” resolve slowly by construction, which is why the ledger’s early weeks will feel quieter than the underlying probabilities.

Pump prices test P3, and the EIA U.S. Regular All Formulations weekly retail series is the sole benchmark — published Mondays, revision-stable, read against the roughly $3.82 July baseline at the October 1 checkpoint. AAA’s daily average, Brent, and WTI serve as context, never as resolution sources. One calendar fact concentrates the void risk (~70%): P3’s ninety-day window runs through August and September, the statistical peak of Atlantic hurricane season, so a Gulf refinery outage — the classic supply shock — is likeliest to arrive precisely when it would matter. A shock voids rather than falsifies, and the distinction will need stating plainly at resolution if it triggers, because a voided prediction reads like a dodge to anyone who missed the ex ante condition.

Federal dockets decide P1 and P5, with DOJ Antitrust and FTC press channels as the primary feeds. Two routing rules prevent miscounting. A filing predicated on a grand jury opened before June 24 does not count against P1 — the exclusion exists because a years-old investigation surfacing now would owe nothing to the July 3 letter. And a whistleblower-sourced case against a small fuel distributor routes to P6A and P6B, not P1; the locked entity class confines P1 to the named major fuel-market companies, so a bid-rigging case against a regional jobber complicates the flank without touching the headline call.

Presidential and agency statements test P4, scored for an explicit causal claim — enforcement pressure lowered pump prices — rather than the co-occurrence of “gasoline” and “investigation” in the same release. White House fact sheets, Truth Social posts, and DOJ or FTC press statements all qualify as sources. The egg-settlement template suggests where the claim will surface if it comes (~70%): attached to an enforcement milestone rather than freestanding, because the June 30 precedent bundled the affordability message with a settlement announcement, and a state action or referral milestone would supply the same stage. P7 rides alongside as the quiet fifth signal — any reported federal pushback against a state’s price-gouging theory, or a preemption argument raised in a state proceeding, converts the watch item into a live prediction.

Checkpoints anchor the calendar: September 1 scores P2A, October 1 scores P3 and P4, and December 30 closes P1, P2B, P5, P6A, and P6B, with P7 reviewed at year-end.

X. Placement and Lineage

Today’s assessment introduces the Detection Density Before Case Conversion Principle and applies it against the letter’s own text, instantiates Why AI Commoditizes Raw Prediction, Why Governance Stays Scarce at the moment a federal grievance meets a missing federal instrument, applies Chicago School Accelerated‘s Coase–Becker–Posner system to an enforcement network rather than a regulated market, classifies the game regime and prices the timing asymmetries under The Computational Era, reads the delegation through Judicial Process as Competitive Federalism — A Live Nation CDT Foresight Simulation, and extends the modernization argument of the Comment of MindCast AI LLC on Potential Updated Guidance (DOJ/FTC Docket ATR-2026-0001) — all under the Mechanism-Outcome Validation Doctrine.

A three-page letter became the catalyst for a broader institutional question, and the question now has a home: the paper opens the Federalism and Governance Economics series, where prior works on the state-federal enforcement seam — the Nash-Stigler breakdown analysis, the Live Nation competitive-federalism simulation — form the retroactive backbone and the resolution updates become the next installments. Distributed enforcement may prove durable governance architecture, or it may remain signaling without conversion — and the foresight ledger records the distinction before the relevant actors move, so the mechanism assessment, the simulations, and the predictions can each be evaluated independently as evidence accumulates. Resolution arrives through the state dockets over the next sixty to one hundred eighty days, including, honestly, by silence.

Appendix A — Foresight Simulation Summary

Seven simulation areas produced the directional readings behind the ledger. Each area ran the interacting twins against a distinct question, and each output feeds specific predictions. Point scores and internal weightings stay proprietary; the table reports direction and the prose reports the reasoning a reader needs to evaluate the calls.

Three structural readings organize the areas. The State Attorney General network converts cheaply to announcement and expensively to filing, because a complaint demands statutory fit, staff capacity, and a local-harm narrative the letter does not supply. The market twins separate price movement from legal causation, holding that crude-to-retail lag reflects refining margins, inventory cycles, transportation, taxes, and local competition rather than coordination. The executive and media twins price public credit-claiming as the cheapest available win on a market already turning — a play the timing gap between political and legal clocks makes structurally safe.

Game-regime placement anchors the confidence levels. The event classifies as Adaptive Drift with mild Multi-Forum Cascade features: stable statutes, stable doctrine, and a recurring grievance pattern put constraint stability well above actor adaptation speed, which is the regime where the MindCast runtime holds prediction reliable. Bands would run materially wider in a Rule-Mutation Break environment, and stating the dependence is part of the disclosure.

Appendix B — Cited MindCast Works and Relevance

Why AI Commoditizes Raw Prediction, Why Governance Stays Scarce (Governance Scarcity flagship). Supplies the paper’s central economic claim: prediction commoditizes while the governance instrument — who holds authority, which statute exists, who bears litigation risk — stays scarce. The oil letter instantiates the thesis at the moment a federal grievance meets a missing federal instrument, and the substitution design in Section III is the scarcity rendered operational.

The Computational Era Operationalizes Cybernetics and Predictive Game Theory (Innovation Vision). Provides the system-level vocabulary: latency arbitrage across forums on different clocks (the credit-capture play in Section IV), the delay-dominant game classification, the prediction break condition that grounds the regime placement in Section VI and Appendix A, the falsification-contract framing of the ledger, and the recursive feedback-trap pattern P7 detects.

Chicago School Accelerated — The Integrated, Modernized Framework of Chicago Law and Behavioral Economics (Economics Vision). Supplies the actor-level theory: Coase’s transaction-cost/coordination-cost distinction grounds P2A and P2B, Becker’s intent-agnostic payoff-gradient analysis grounds the Woodward reading and the paper’s refusal to assert motive, and the behaviorally extended Posner explains why passthrough anger never converted into a federal statute. Applied here to an enforcement network rather than a regulated market.

Federal Antitrust Breakdown as Nash-Stigler Equilibrium (January 2026). Establishes the routing pattern Section III builds on: a constrained federal center pushes enforcement outward to state authorities rather than building capacity inward, with state consumer-protection law substituting for federal structural action.

Judicial Process as Competitive Federalism — A Live Nation CDT Foresight Simulation (February 2026). Models state attorneys general as independent structural actors who absorb enforcement whenever the federal center cannot or will not carry it — the mechanism the oil letter now invokes deliberately, from the amplification side rather than the suppression side the earlier work documented.

Comment of MindCast AI LLC on Potential Updated Guidance (DOJ/FTC Docket ATR-2026-0001) (filed April 2026). Establishes MindCast’s standing in the federal enforcement-modernization record and supplies the coordination-capacity toolkit referenced in the algorithmic tail risk. Cited for institutional lineage; the comment’s algorithmic-coordination proposals inform the honest flank rather than the core mechanism, because the letter contains no algorithmic-pricing facts.

Detection Density Before Case Conversion — The DOJ–FTC Oil-Market Letter as a Distributed-Enforcement Prototype (companion working paper, forthcoming). Extends the governance-economics argument this assessment introduces, including the full treatment of distributed enforcement as capacity substitution and the cross-domain implications beyond petroleum. The present paper is the first MindCast publication on the July 3 trigger; the companion develops the principle at length.