MCAI Lex Vision: Kalshi Is Crypto's Test Case

Why Prediction Market Litigation Is Rewiring the Regulatory Future of Digital Assets

Related publications: Kalshi Is Crypto’s Test Case | Kalshi’s Prediction Market Litigation Architecture, the CFTC Amicus, and the Strategic Framework for State Enforcement | The National Kalshi Prediction Market Litigation Map | The Full Arc of Prediction Markets | Prediction Markets and the Regulatory Split | Prediction Markets— Legislative Regime Conversion and the Collapse of Preemption | Kalshi Found the One Gap in American Gaming Law Nobody Closed | The Ninth Circuit on April 16 as System Convergence — The First Measurable Test of Prediction Market Structure | Kalshi, Prediction Markets and the Conflict Architecture of Regulation

Executive Summary

Jurisdiction determines who controls the feedback loop of financial innovation. Prediction markets and crypto are not converging as adjacent industries chasing the same regulatory shelter — they are converging into a single control layer: prediction markets supply the information pricing infrastructure, crypto supplies the settlement infrastructure, and the Commodity Futures Trading Commission (CFTC) is the only regulatory architecture capable of governing both under a unified statutory framework. Kalshi’s litigation is not a prediction market story. Kalshi’s litigation is the first live-fire test of whether the CFTC governs the control layer that comes next — and every firm building on information pricing, tokenized settlement, or synthetic financial instruments is watching because the ruling applies to all of them simultaneously.

Crypto media covers the Kalshi litigation intensively not because prediction markets and crypto are adjacent, but because they are executing the same jurisdictional migration strategy toward the same regulatory destination. The CFTC, not the Securities and Exchange Commission (SEC), is both Kalshi’s federal regulator and crypto’s preferred regulatory home. A Kalshi win at the appellate or Supreme Court level locks the CFTC in as the governing control system for the next generation of financial instruments. A Kalshi loss forecloses that pathway for everyone operating underneath the same statutory architecture.

The field forces this convergence. Firms operating under state-by-state regulatory fragmentation face an identical structural problem: high constraint density at the state level and a single low-friction attractor at the federal level — the CFTC’s exclusive jurisdiction over derivatives. Kalshi is not the only firm pursuing that attractor. Coinbase, Robinhood, and Polymarket face the same state enforcement wave for the same structural reason: they are all running the same playbook, because the incentive geometry of the legal field produces the same output regardless of which firm is executing it. Coinbase’s prediction market product earned a Nevada preliminary injunction on March 26, 2026 — one day before Washington AG Nick Brown filed against Kalshi. The litigation is not parallel by accident. The field geometry makes it inevitable.

Four MindCast framework layers govern the analysis. MindCast Predictive Cybernetics Suite — Cybernetic Game Theory — establishes that Kalshi’s litigation is not defensive case management. Kalshi is executing a delay-dominant, equilibrium-forcing strategy designed to generate an inter-circuit collision that forces Supreme Court resolution on federal derivatives terms. How Cybernetic Feedback Latency, Loop Architecture, and Ashby’s Viability Condition Resolve Consumer AI Device Competition — Cybernetic Control Vision (CCV) — explains why crypto and prediction markets both migrate toward the CFTC: lower feedback latency, broader instrument classification tolerance, and a statutory mandate built for exactly the kind of novel instrument both industries produce. Chicago School Accelerated — The Integrated, Modernized Framework of Chicago Law and Behavioral Economics — running the Coase-Becker-Posner loop — explains why firms are not choosing crypto over prediction markets or prediction markets over sports betting; they are choosing jurisdictional efficiency, and the CFTC offers more of it than any alternative regulatory home. Field-Geometry Reasoning — Structural Constraint Modeling in Predictive Cognitive AI (FGR) closes the architecture by establishing that convergence is structurally inevitable: the constraint geometry of state-level fragmentation leaves only one viable geodesic, and every firm in the space is traveling it simultaneously.

Three forward predictions follow from the framework stack. Within six to twelve months, Coinbase explicitly reframes at least one product under CFTC derivatives logic — a Becker-predicted output of regime selection maximizing expected regulatory payoff. Within twelve to eighteen months, at least one federal appellate opinion adopts preemption language broad enough to apply beyond event contracts to digital asset instruments — the Posnerian legal system adaptation the circuit split is now producing. Within eighteen to twenty-four months, crypto derivatives gain a materially clearer CFTC pathway relative to securities classification — the FGR attractor dominance outcome once the Kalshi litigation forces a definitive classification ruling. The single falsification condition: courts reject preemption across the board and affirm state classification authority, leaving fragmentation as the durable equilibrium and blocking the CFTC migration for all instrument classes simultaneously.

Kalshi is not litigating for its own survival. Kalshi is forcing the question of who governs the next generation of financial instruments — and crypto is watching because the answer applies to everything the CFTC might claim next.

I. The Field Forces Convergence: Why Crypto and Prediction Markets Arrive at the Same Destination

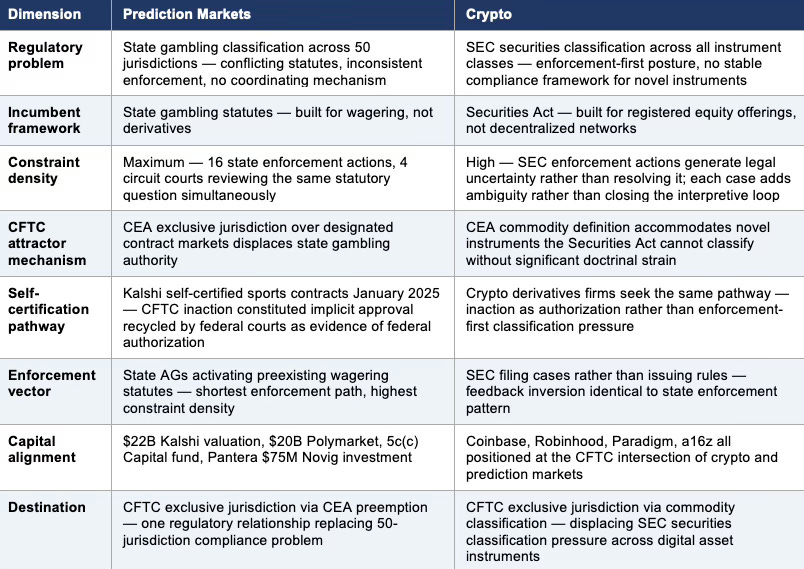

No firm operating across fifty state regulatory regimes simultaneously chooses fragmentation voluntarily. State-level gambling enforcement creates the highest constraint density in the regulatory field — conflicting statutes, inconsistent enforcement, no coordinating mechanism, and annual compliance costs that scale linearly with each new jurisdiction that activates. Against that constraint density, one low-friction attractor exists: federal preemption under the Commodity Exchange Act (CEA), the federal statute governing derivatives markets, which would convert a fifty-jurisdiction compliance problem into a single regulatory relationship with one agency.

Field-Geometry Reasoning — Structural Constraint Modeling in Predictive Cognitive AI maps exactly this dynamic through three diagnostic metrics. Constraint Density measures the friction imposed by competing regulatory frameworks on the same instrument — currently maximal at the state level, where sixteen states have filed enforcement actions against Kalshi and four federal circuits are reviewing the same statutory question simultaneously. Geodesic Availability identifies the shortest viable path through the constraint field — here, the only available geodesic runs through federal preemption under the CEA, because no other pathway reduces state-level constraint density to a manageable operating condition. Attractor Dominance measures the degree to which one regulatory endpoint pulls all actors in the field toward it regardless of individual firm strategy — and the CFTC regime currently dominates, because every firm that obtains a favorable federal preemption ruling immediately converts that ruling into supplemental authority in every other active proceeding, strengthening the attractor for all subsequent actors simultaneously.

Crypto reached the same field geometry through a different instrument pathway. The SEC’s assertion of securities classification over digital assets created the same fifty-jurisdiction compliance problem — not through state enforcement, but through federal over-classification that applied a regulatory framework built for equity securities to instruments that do not fit the Howey test, the Supreme Court standard for determining whether something qualifies as a security, without significant doctrinal strain. Crypto firms have spent a decade pushing toward CFTC jurisdiction precisely because the CEA’s definition of commodity accommodates novel instruments more naturally than the Securities Act’s definition of security accommodates decentralized networks. The field geometry is identical: high constraint density under the incumbent regulatory framework, one low-friction attractor available at the CFTC, and firms migrating toward it regardless of individual strategic preference because the field makes any other path more costly.

Kalshi’s litigation accelerates that migration for every firm in the field simultaneously. Each federal court ruling that affirms CEA preemption over state gambling law expands the jurisdictional footprint of the CFTC’s exclusive domain. Each circuit opinion that adopts broad preemption language creates persuasive authority for crypto firms arguing that their instruments also fall within CFTC exclusive jurisdiction rather than SEC securities classification. The attractor strengthens with every Kalshi win — not just for prediction markets, but for every instrument class that benefits from a more expansive reading of what the CFTC governs.

The National Kalshi Prediction Market Litigation Map documented the full constraint geometry of the current enforcement landscape: sixteen state actions, four circuit courts reviewing the same preemption question simultaneously, and a CFTC filing amicus briefs — friend-of-the-court arguments asserting the agency’s position — in Nevada, Tennessee, and every other active appellate proceeding. The Viable System Model (VSM) diagnosis, a cybernetics framework that identifies the structural conditions a system must satisfy to remain capable of self-regulation, established that the current fragmented control regime cannot persist as a stable equilibrium past Q3 2027. What that publication left implicit — and what the field geometry framework makes explicit — is that resolution through CFTC preemption does not just resolve the Kalshi case. Resolution through CFTC preemption expands the CFTC’s effective jurisdictional footprint across every novel instrument currently navigating the same attractor.

Table 1 — The Convergence Map: Prediction Markets and Crypto in the Same Field

II. The CFTC Is a Lower-Latency Control System: Why Every Firm Wants to Land There

Crypto’s decade-long push toward CFTC jurisdiction reflects a structural reality that How Cybernetic Feedback Latency, Loop Architecture, and Ashby’s Viability Condition Resolve Consumer AI Device Competition — Cybernetic Control Vision (CCV) — makes precise. The CFTC is not merely a more permissive regulator — it is a lower-latency control system. Feedback Latency measures the time required for a regulatory agency to process a novel instrument, issue interpretive guidance, and generate a stable compliance framework. Loop Closure Integrity measures the degree to which an agency’s regulatory output actually governs the instrument class it claims to oversee — whether the feedback loop between agency action and firm behavior closes completely or leaks through ambiguity, resource constraints, and jurisdictional gaps.

The SEC operates with high feedback latency and degraded loop closure on novel instruments. Disclosure architecture built for registered securities requires an issuer, a defined offering, and a registration process that decentralized networks and event contracts do not fit without significant doctrinal retrofitting. The SEC’s enforcement-first approach to crypto — filing cases rather than issuing rules — produces exactly the kind of feedback inversion that Cybernetic Foundations of Predictive Institutional Intelligence identifies as the signature of a control system operating below its requisite variety threshold, meaning the agency lacks the institutional capacity to match the complexity of the system it is trying to regulate: enforcement actions that generate legal uncertainty rather than resolving it, each case adding to the ambiguity rather than closing the interpretive loop.

The CFTC operates with lower feedback latency on derivatives instruments because the CEA’s commodity definition was built for exactly the kind of instrument novelty that prediction markets and crypto produce. The agency’s self-certification process — which Kalshi used to list sports contracts in January 2025, triggering no immediate CFTC action — exemplifies low-latency loop closure: a firm submits an instrument for self-certification, the agency reviews it within a defined window, and either acts or declines to act. Inaction constitutes implicit authorization. Multiple federal courts have already recycled that implicit authorization as evidence of CFTC approval — the Tennessee court specifically cited the CFTC’s decision not to block Kalshi’s self-certified sports contracts as grounds for finding Kalshi likely to succeed on preemption.

That feedback architecture is exactly what crypto needs. A regulatory home where novel instruments can be self-certified, where inaction functions as implicit approval, and where the statutory definition of the instrument class is broad enough to accommodate decentralized networks, tokenized assets, and event contracts without requiring a new legislative mandate — the CFTC offers all three. The SEC offers none of them. Every crypto firm that has watched the Kalshi self-certification process unfold has observed a lower-latency regulatory pathway produce a multi-billion-dollar market before any enforcement action could stabilize against it. The demonstration effect is not lost.

CFTC Chair Michael Selig’s posture under the Trump administration has accelerated the feedback latency advantage. Withdrawing the prior proposed rule that would have prohibited sports and political event contracts removed the regulatory ceiling that had constrained Kalshi under the Biden administration. Filing amicus briefs in Nevada, Tennessee, and every other active appellate proceeding converted the agency from a passive regulator into an active participant defending its own jurisdictional footprint. The Nash-Stigler Equilibrium Architecture — the MindCast framework explaining how regulatory agencies systematically migrate toward accommodation with the industries they oversee — established the structural mechanism producing this posture: a single-commissioner agency operating far below Ashby’s Law of Requisite Variety threshold — approximately 540 staff against a $22.88 billion annual market — finds accommodation the dominant strategy because the agency’s institutional geometry produces it automatically, independent of individual intent.

For crypto, that accommodation posture is an asset, not a liability. A CFTC whose institutional geometry produces accommodation toward novel instrument classes is a more hospitable regulatory home than an SEC whose institutional geometry produces enforcement-first classification pressure. Firms select regulatory regimes with the highest expected payoff — and the CFTC’s feedback architecture, statutory breadth, and current posture make it the dominant attractor for every firm whose instrument does not fit cleanly inside the Securities Act’s existing categories.

Contact mcai@mindcast-ai.com to partner with us on Predictive Law and Behavioral Economics + Game Theory Foresight Simulations. To deep dive on MindCast work in Cybernetic Foresight Simulations upload the URL of this publication into any LLM and prompt ‘reconstruct MindCast framework with three degrees of cited sub links.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure.

Recent projects: The Power Stack Series— How Energy Infrastructure Became the New AI Battleground | MindCast AI Emergent Game Theory Frameworks | MindCast AI Field-Geometry Reasoning | MindCast AI Installed Cognitive Grammar | Runtime Geometry, A Framework for Predictive Institutional Economics | Super Bowl LX — AI Simulation vs. Reality | The Runtime Causation Arbitration Directive | Google’s Deep-Thinking Ratio Measures Effort, Not Structure | MindCast AI Constraint Geometry and Institutional Field Dynamics | Double-Sided Rational Ignorance, How Platform Intermediaries Monetize the Measurement Gap | Executive Summary of MindCast AI Investment Series

III. Jurisdictional Efficiency: The Coase-Becker-Posner Loop Explains Every Actor

Firms are not choosing prediction markets over crypto, or crypto over prediction markets. Firms are choosing jurisdictional efficiency — and every actor in the current landscape is behaving exactly as the Chicago School Accelerated — The Integrated, Modernized Framework of Chicago Law and Behavioral Economics framework predicts.

Ronald Coase, the University of Chicago economist who identified transaction costs as the root driver of institutional behavior, explained that fragmented regulatory coordination is itself a cost firms seek to minimize. State-by-state enforcement against Kalshi, Coinbase, Robinhood, and Polymarket simultaneously is a Coasean coordination breakdown: no single actor holds the authority to resolve the classification question, so the system incurs maximum transaction costs — sixteen state enforcement actions, four appellate proceedings, congressional hearings, lobbying expenditures, and interim injunction litigation — without producing the definitive classification that would eliminate those costs. Firms seeking to minimize transaction costs pursue the pathway that produces single-authority resolution fastest. Federal preemption through the CFTC is that pathway.

Gary Becker’s rational incentive model explains the regime selection behavior observable across every firm currently in the prediction market or crypto space. Firms select the regulatory regime with the highest expected payoff net of compliance costs. The CFTC offers a broader instrument definition, lower compliance friction, and a current posture of active institutional support. The SEC offers narrower instrument definitions, higher compliance friction through registration requirements, and an enforcement-first posture that imposes significant legal cost before producing any stable compliance framework. Becker’s model predicts firms will migrate toward the CFTC regardless of which instruments they happen to be offering — because the payoff gradient runs consistently in that direction.

The behavioral evidence confirms the Becker prediction. Coinbase launched prediction market products while simultaneously carrying billions in crypto trading volume — not because prediction markets are its core business, but because prediction markets occupy the same CFTC regulatory home its crypto derivatives business needs. Robinhood expanded into prediction markets through its existing brokerage infrastructure for the same jurisdictional reason. Polymarket — a blockchain-native platform that settles contracts in cryptocurrency — sits squarely at the intersection of the two instrument classes and faces the same state enforcement pressure as Kalshi for the same statutory reason. Every actor’s behavior follows the payoff gradient the Becker model identifies.

Richard Posner’s legal efficiency framework explains why courts become the resolution mechanism and why the resolution they produce will have implications far beyond prediction markets. Legal systems evolve toward efficiency — toward classifications that minimize total social cost — but with a lag that is itself a strategic resource for firms that can absorb the cost of extended litigation. Kalshi has spent fourteen months generating that lag deliberately. Kalshi’s Prediction Market Litigation Architecture, the CFTC Amicus, and the Strategic Framework for State Enforcement identified the three-layer fragmentation strategy Kalshi deploys: preemptive federal filings to freeze state enforcement, conversion of every district ruling into multi-jurisdiction ammunition, and categorical reframing of sports event contracts as derivatives rather than wagers. Each layer of the strategy consumes time — and time is what Kalshi needs for the inter-circuit split to ripen into Supreme Court jurisdiction.

The Posnerian insight is that the doctrinal clarification Kalshi’s litigation is forcing does not apply only to sports event contracts. Every appellate opinion that addresses whether the CEA preempts state gambling law must, in the process, define what kind of instrument falls within the CFTC’s exclusive jurisdiction. A broad preemption ruling — one that reads the CEA’s swap definition expansively, as the Tennessee court did in February 2026 — generates persuasive authority for every subsequent instrument classification argument that invokes the same statutory text. Crypto derivatives, tokenized event contracts, and digital asset instruments whose securities classification remains contested all benefit from an expansive reading of what the CFTC governs. The legal system’s lag is Kalshi’s runway, and the doctrinal output of that runway extends to every instrument class currently navigating the same classification contest.

IV. Equilibrium-Forcing Strategy: Why Kalshi’s Litigation Is Not Defensive

Kalshi is not playing a single-play game against individual state attorneys general. Kalshi is executing a delay-dominant, equilibrium-forcing strategy designed to generate the inter-circuit collision that produces Supreme Court jurisdiction — on federal derivatives terms, not gambling-policy terms.

MindCast AI Emergent Game Theory Frameworks — Chicago Strategic Game Theory Vision (CSGT) — classifies this behavior through the Equilibrium Persistence Under Loss (EPUL) signal: a firm absorbing significant current costs — legal fees, interim injunctions, criminal charges in Arizona, civil complaints in sixteen states — to build the precedent record, institutional relationships, and credibility that make future iterations cheaper to win. Every state enforcement action Kalshi defeats reduces the cost of the next defense. Every voluntary concession — blocking politicians and athletes from trading — reduces the political cost of the next congressional hearing without conceding the legal argument. Every favorable district ruling gets filed as supplemental authority in every other active proceeding, strengthening Kalshi’s preemption argument in the next jurisdiction before that jurisdiction’s enforcement apparatus has even activated.

Three specific mechanisms drive the strategy. Delay Dominance keeps the case in motion across fragmented forums long enough for the inter-circuit split to become irresolvable without Supreme Court intervention. The intra-Sixth Circuit split — Ohio ruling for the states, Tennessee ruling for Kalshi on the same statutory question — already generates certiorari pressure within a single circuit. When the Fourth and Ninth Circuits rule on Maryland and Nevada respectively, the inter-circuit split becomes structurally probable, and a four-circuit split produces certiorari pressure that becomes nearly irresistible.

Narrative Control — the mechanism formalized in MindCast Runtime Narrative Control Cybernetics as the process by which institutional actors convert the classification contest from gambling-law terrain to derivatives-law terrain — converts the core question at every available forum. Kalshi’s legal argument is not “prediction markets are not gambling” — it is “the CEA’s exclusive jurisdiction over designated contract markets displaces state gambling authority regardless of whether the underlying instrument resembles a wager.” Reframing moves the case from terrain where states hold the strongest arguments — gambling law, consumer protection, police power — to terrain where the federal agency’s statutory mandate controls. Courts resolve jurisdiction questions faster than moral classification questions. Every successful reframing shortens Kalshi’s runway to a favorable resolution forum.

Feedback Capture converts corrective enforcement signals into preemption ammunition. State regulators file enforcement actions — the feedback signal that Kalshi’s activity violates gambling law. Kalshi responds by filing preemptive federal lawsuits, which shift the correction mechanism from state enforcement to federal court, where the CFTC’s amicus brief reinforces Kalshi’s position. The federal court issues a preliminary injunction blocking state enforcement — which Kalshi immediately files as supplemental authority in every other active proceeding, using the corrective signal to suppress the original error signal. The National Kalshi Prediction Market Litigation Map identified this as the feedback inversion condition: the correction mechanism feeds the distortion rather than resolving it.

Crypto’s litigation posture mirrors Kalshi’s strategy precisely because the same game theory governs both. Coinbase files amicus briefs in Kalshi proceedings. Robinhood joins the Coalition for Prediction Markets. The 5c(c) Capital fund — launched March 23, 2026, backed by Kalshi CEO Tarek Mansour, Polymarket CEO Shayne Coplan, Marc Andreessen through Moneta Luna, Ribbit Capital, and Multicoin Capital — is institutional capital treating the litigation outcome as a shared asset. The capital coalition is not speculating on whether prediction markets will survive. The capital coalition is funding the strategy that forces the legal system to produce the classification ruling that benefits every instrument class in the portfolio simultaneously.

V. The Current Regime and Its Transition: Labyrinth to Arena

The current regulatory environment is a Labyrinth — the Game Regime Identification (GRI) classification, established in MindCast AI Emergent Game Theory Frameworks, for high-constraint, high-latency conditions characterized by conflicting jurisdictions, slow judicial resolution, and maximum strategic maneuvering room. In a Labyrinth regime, no single actor controls the outcome, fragmentation persists as a stable operating condition, and firms with the longest time horizons and deepest capital reserves extract the most advantage from delay.

The Full Arc of Prediction Markets established the structural taxonomy distinguishing public belief exchanges — open platforms like Kalshi where retail participants trade contracts on real-world outcomes — from proprietary probability engines — private institutional firms like Susquehanna International Group that price probabilities internally and never expose retail participants to the mechanism. The classification problem sits at the root source of regulatory controversy: prediction markets genuinely occupy the gap between gambling law and commodity futures law, and neither framework was designed for an instrument that is simultaneously a financial product, an information aggregation mechanism, and a mass-participation wagering product. Courts applying coherent frameworks reach opposite conclusions from the same facts — not because they are confused, but because the frameworks were built to answer different questions.

The Labyrinth regime persists as long as the classification question remains unresolved. The transition to an Arena regime — high-constraint but lower-latency, where a single dominant authority issues binding classification — requires exactly one of three structural interventions: a Supreme Court certiorari grant resolving the preemption question definitively; a congressional amendment through the Prediction Markets Are Gambling Act (PMAGA) or the Event Contract Enforcement Act (ECEA) eliminating the statutory ambiguity the inversion depends on; or a complete circuit split producing such acute coordination failure that Congress intervenes regardless of lobbying equilibrium.

Each transition path carries different implications for crypto. A Supreme Court ruling affirming CFTC preemption produces the broadest possible doctrinal output — a binding interpretation of CEA exclusivity that crypto derivatives litigants can cite in every subsequent instrument classification dispute. A congressional amendment through the PMAGA prohibiting sports event contracts narrows the outcome without resolving the underlying jurisdictional question — potentially leaving crypto derivatives in a more favorable CFTC position than prediction markets while restricting the specific instrument class that generated the controversy. An ECEA state opt-out framework licenses event contracts at the state level — the worst outcome for the crypto CFTC migration strategy, because it validates state authority rather than federal preemption as the governing framework.

The control timing windows established in The National Kalshi Prediction Market Litigation Map determine which transition path completes first. Pre-Fourth Circuit ruling — now through approximately summer 2026 — state enforcement velocity dominates and the legislative track retains maximum shaping power. Post-circuit split through pre-Supreme Court resolution — approximately summer 2026 through Q1 2027 — Congress holds the decisive instrument because a floor vote before the Supreme Court resolves the split preserves the state opt-out flexibility that a binding constitutional ruling would extinguish. Post-legislation or post-Supreme Court — Q1 2027 and beyond — the Arena regime locks in and the CFTC’s jurisdictional footprint is defined for the next decade of financial instrument innovation.

VI. Causal Integrity: Why the Convergence Is Structural, Not Narrative

The crypto-prediction market convergence passes the Causal Signal Integrity (CSI) filter — established in Predictive Institutional Cybernetics as the MindCast diagnostic that separates structurally causal findings from narrative coincidence. CSI measures whether the link between two phenomena holds because of a genuine underlying mechanism or merely because the phenomena appear together. Three CSI conditions govern the analysis.

Action Language Integrity (ALI) requires that the legal theory underlying the convergence applies consistently across instrument classes rather than opportunistically to a single case. The CEA’s exclusive jurisdiction argument applies with equal logical force to crypto derivatives and to prediction market event contracts: both involve instruments whose value derives from a contingent future outcome, both involve a CFTC-regulated designated contract market asserting federal preemption over state classification authority, and both involve the same statutory text — the CEA’s swap definition — that courts are currently interpreting in conflicting directions. The alignment is not manufactured by analogy. The alignment is produced by the same statutory architecture governing both instrument classes.

Cognitive Motor Fidelity (CMF) requires that the behavioral convergence — identical litigation strategy, identical capital coalition, identical regulatory destination — follows from the structural mechanism rather than from individual firm decisions that could have been otherwise. Coinbase, Robinhood, Kalshi, and Polymarket are all running the same playbook not because they coordinated, but because the payoff gradient of the regulatory field produces the same output from any firm operating within it. Remove any individual firm from the analysis and the convergence persists — because the field geometry, not the firm strategy, is the causal mechanism. CMF is satisfied when removing individual actors does not change the structural outcome. Removing Kalshi from the litigation landscape does not change the fact that Coinbase, Robinhood, and Polymarket face the same state enforcement pressure for the same structural reason and will pursue the same federal preemption pathway through whatever litigation vehicle remains available.

Relational Integration Score (RIS) requires that the capital, legal, and regulatory layers of the convergence align rather than pointing in conflicting directions. Capital points toward CFTC jurisdiction: the $22 billion Kalshi valuation, the $20 billion Polymarket valuation, the 5c(c) Capital fund, and the Pantera Capital $75 million Novig investment all treat CFTC-regulated prediction markets as a durable asset class worth funding through the litigation period. Legal strategy points toward CFTC jurisdiction: every major firm in the space has filed amicus briefs, joined the Coalition for Prediction Markets, or deployed lobbying resources toward CFTC rulemaking rather than state-by-state licensing. Regulatory posture points toward CFTC jurisdiction: Chair Selig’s amicus briefs, the withdrawal of the prior proposed prohibition, and the four-part regulatory agenda announced at the January 2026 joint summit with the SEC all signal an agency actively expanding its jurisdictional footprint. All three layers point in the same direction. RIS is satisfied.

The CSI analysis produces a single conclusion: the crypto-prediction market convergence is structurally causal. No firm chose to connect these two industries. The legal field, the incentive geometry, and the capital dynamics produce the connection automatically — and Kalshi’s litigation is the mechanism forcing the system to resolve it.

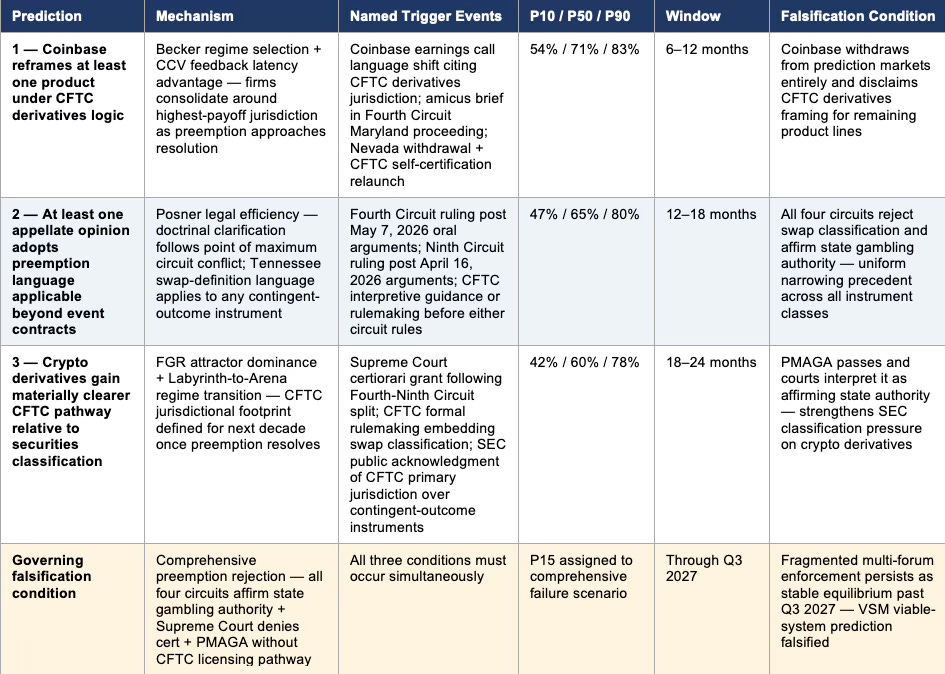

VII. Forward Predictions: Three Probability-Banded Outcomes With Falsification Conditions

Six Cognitive Digital Twin (CDT) foresight simulations — MindCast’s proprietary methodology, documented in MindCast Predictive Cybernetics Suite, which models each institutional actor as a behavioral replica encoding objective functions, constraint stacks, and feedback sensitivities — converge on three ranked forward predictions. A CDT is not a static forecast. It is a running simulation of the decision architecture that generates outcomes, updated as new signals enter the system.

Table 2 — Forward Predictions Summary: Three Probability-Banded Outcomes With Falsification Conditions

Probability bands follow a three-tier structure. P10 is the lower-confidence bound — the probability under unfavorable structural conditions. P50 is the base case. P90 is the upper-confidence bound under favorable conditions. Each prediction also carries named trigger events — specific observable developments that would confirm the prediction is on track — and a falsification condition that would defeat it.

Prediction 1 — Coinbase explicitly reframes at least one product under CFTC derivatives logic within six to twelve months.

Becker’s regime selection model and the CCV framework both predict this output: a firm operating at the CFTC intersection of crypto and prediction markets will consolidate its regulatory framing around the higher-payoff jurisdiction as the preemption question approaches appellate resolution. Coinbase’s prediction market product — already subject to the Nevada preliminary injunction issued March 26, 2026 — gives it both the litigation exposure and the strategic incentive to crystallize its CFTC positioning before the Fourth and Ninth Circuits rule. A CFTC-forward reframing reduces Coinbase’s state enforcement exposure while strengthening its amicus standing in the Kalshi proceedings.

Named trigger events: Coinbase earnings call language shift explicitly citing CFTC derivatives jurisdiction; Coinbase public filing or amicus brief in the Fourth Circuit Maryland proceeding adopting swap-definition framing; Coinbase withdrawal of prediction market products in Nevada combined with simultaneous relaunch under a CFTC self-certification filing.

P10: 54% | P50: 71% | P90: 83% | Window: six to twelve months from publication date. Falsification condition: Coinbase withdraws from prediction markets entirely and explicitly disclaims CFTC derivatives framing for its remaining product lines.

Prediction 2 — At least one federal appellate opinion adopts preemption language broad enough to apply beyond event contracts to digital asset instruments within twelve to eighteen months.

Posner’s legal efficiency framework predicts that doctrinal clarification follows the point of maximum circuit conflict — and the current four-circuit split on the same statutory question creates exactly that point. The Tennessee court’s February 2026 ruling — finding that Kalshi’s sports contracts likely qualify as swaps under the CEA’s statutory definition, where a swap is any financial instrument whose value derives from an underlying variable — deployed language that applies to any instrument whose value derives from a contingent future event. A Ninth Circuit or Fourth Circuit opinion adopting that reasoning and affirming CEA exclusivity would generate persuasive authority for crypto derivatives instrument classification arguments in every subsequent proceeding that invokes the same swap definition.

Named trigger events: Fourth Circuit ruling in the Maryland case following May 7, 2026 oral arguments; Ninth Circuit ruling in the consolidated Nevada proceeding following April 16, 2026 oral arguments; CFTC interpretive guidance or proposed rulemaking issued before either circuit rules, which would itself become a trigger for accelerated appellate resolution.

P10: 47% | P50: 65% | P90: 80% | Window: twelve to eighteen months from publication date. Falsification condition: all four circuits reject the swap classification for event contracts and affirm state gambling authority, generating uniform circuit precedent that narrows rather than expands the CEA’s reach.

Prediction 3 — Crypto derivatives gain a materially clearer CFTC pathway relative to securities classification within eighteen to twenty-four months.

Field-Geometry Reasoning and the CCV framework both converge on this output as the Labyrinth-to-Arena regime transition completes. Once the preemption question resolves — through Supreme Court certiorari, congressional amendment, or a decisive circuit split — the CFTC’s jurisdictional footprint becomes defined for the next decade of instrument innovation. A broad preemption ruling that affirms CEA exclusivity over event contracts simultaneously clarifies that the CFTC, not the SEC, governs instruments whose value derives from contingent future outcomes — which includes most crypto derivatives currently navigating securities classification pressure. The clarification does not require a separate crypto-specific ruling. The Kalshi ruling does the work.

Named trigger events: Supreme Court certiorari grant on the preemption question following a Fourth-Ninth Circuit split; CFTC formal rulemaking embedding the swap classification for event contracts before a circuit ruling issues; SEC public statement acknowledging CFTC primary jurisdiction over instruments tied to contingent future outcomes — a low-probability but high-signal trigger that would indicate the inter-agency boundary is shifting without requiring litigation to force it.

P10: 42% | P50: 60% | P90: 78% | Window: eighteen to twenty-four months from publication date. Falsification condition: the Kalshi litigation resolves through congressional prohibition rather than judicial preemption — specifically, the PMAGA passes and courts interpret it as affirming state authority over event contracts, generating a precedent that strengthens rather than weakens SEC classification pressure on crypto derivatives.

Single governing falsification condition across all three predictions:

Courts reject preemption comprehensively — all four circuits affirm state gambling authority, the Supreme Court denies certiorari, and Congress enacts prohibition through the PMAGA without preserving a CFTC licensing pathway. Under that scenario, the CFTC migration strategy fails for prediction markets, the field geometry shifts back toward state-level constraint density as the stable operating condition, and crypto derivatives lose the Kalshi litigation as a jurisdictional precedent vehicle. MindCast assigns that comprehensive outcome low structural probability — P15 — because the intra-circuit split within the Sixth Circuit alone generates certiorari pressure that is unlikely to resolve without Supreme Court intervention regardless of how the Fourth and Ninth Circuits rule.

VIII. Who This Analysis Is For: Stakeholder Significance by Audience

The framework stack in Sections I through VII produces different operational intelligence depending on who is reading it. Each audience faces a distinct decision set — and the analysis bears on each one differently.

State Attorneys General — Washington, Arizona, Maryland, Nevada, Ohio, Massachusetts

The feedback capture mechanism documented in Section IV is the most consequential finding for state enforcement actors. Every enforcement action that reaches a favorable federal court strengthens Kalshi’s preemption record in the next jurisdiction. AGs filing uncoordinated individual actions are structurally contributing to the precedent architecture Kalshi needs to reach the Supreme Court on federal derivatives terms. The April 16 Ninth Circuit and May 7 Fourth Circuit rulings are countdown events — not background developments. The CFTC amicus brief asserting exclusive federal jurisdiction in those proceedings means every state enforcement action filed without coordination now risks strengthening the preemption record rather than building against it. Filing in the right forum, at the right speed, before those rulings issue is the operational window. Coordination across AG offices is not a courtesy. Coordination is the structural counter to Kalshi’s multi-forum fragmentation strategy.

Federal Lawmakers — Senate Agriculture Committee, Senate Banking, House Financial Services

The Statutory Category Exclusion Mechanism (SCEM) — the legislative instrument that converts definitional ambiguity into express statutory prohibition, identified in Legislative Regime Conversion and the Collapse of Preemptionas the most powerful tool available to Congress — is why the timing of a floor vote matters so acutely. A congressional floor vote in the current window preserves the state opt-out flexibility that a Supreme Court ruling would permanently extinguish. Lawmakers who wait for judicial resolution are ratifying the court’s classification without legislative input. The PMAGA and ECEA are not gambling policy bills. They are the only instrument capable of foreclosing the CFTC migration for the entire next-generation instrument stack — including crypto derivatives, AI-generated contracts, and tokenized assets — before the field locks.

Crypto Firms and Their Counsel — Coinbase, Robinhood, Polymarket, and Legal Teams

Kalshi is running crypto’s test case at its own expense on a timeline that benefits every instrument class simultaneously. The CCV analysis in Section II maps exactly why: the CFTC’s self-certification pathway, implicit approval through inaction, and statutory breadth are the same regulatory features every crypto derivatives firm has been seeking for a decade. The three forward predictions carry named trigger events — April 16 Ninth Circuit arguments, May 7 Fourth Circuit arguments, any CFTC formal rulemaking — that give in-house counsel and regulatory strategy teams specific observable checkpoints for adjusting CFTC positioning before the field locks into the Arena regime.

Institutional Investors — Hedge Funds, Crypto-Native Funds, Fintech VCs

Investors treating the current multi-forum fragmentation as a permanent operating condition are mispricing regime risk at every layer of the emerging financial infrastructure stack. The Labyrinth-to-Arena transition is not a tail scenario — the VSM diagnosis establishes it as the structural default. The P10/P50/P90 bands on the three forward predictions give portfolio managers a probability-weighted timeline for when the CFTC jurisdictional footprint expands to cover crypto derivatives. The 5c(c) Capital coalition — Kalshi, Polymarket, Andreessen, Ribbit, Multicoin — is already positioning for exactly this transition. The named trigger events are the observable checkpoints for updating that positioning in real time.

Washington Tribal Gaming — WIGA, Snoqualmie, Tulalip, Puyallup

The feedback capture mechanism is the most important finding for tribal legal counsel, and it runs counter to instinct. Uncoordinated state enforcement — each AG filing independently, each case reaching a favorable federal court in isolation — feeds the very preemption record Kalshi needs. The tribes’ economic interest in the outcome is direct: Snoqualmie Casino holds the licensed sports betting monopoly closest to Seattle’s population center, and Kalshi is openly marketing to Washington residents as a workaround to that monopoly. The Washington AG complaint and the Indian Gaming Association (IGA) congressional briefing are powerful signals. Their value compounds when coordinated with the broader enforcement strategy this publication maps — and diminishes when filed in isolation into forums that produce federal preemption authority Kalshi recycles against the next state.

AI Firms and Tokenization Infrastructure Builders

The beyond-crypto argument in the conclusion names the structural implication most AI and tokenization firms have not yet publicly acknowledged: every instrument class that does not fit cleanly inside existing SEC or state regulatory frameworks faces the same field geometry Kalshi is navigating now. AI-generated contracts, tokenized real-world assets, and synthetic financial instruments all require exactly the statutory flexibility the CEA’s commodity definition provides and the Securities Act does not. A CFTC preemption ruling expands the jurisdictional footprint of the only regulatory architecture currently capable of governing instruments that AI and tokenization are producing faster than any legislative body can classify. Firms building on those instrument classes have a structural interest in the Kalshi outcome that the field geometry makes inevitable — whether they recognize it yet or not.

Policy Staff, Think Tanks, and Regulatory Reform Advocates

The VSM diagnosis delivers the most rigorous structural indictment of CFTC institutional capacity in the current public record: one sitting commissioner, approximately 540 staff, against a $22.88 billion annual market operating across all fifty states simultaneously, with the feedback loops governing classification inverted rather than functioning. Policy staff working on CFTC reform, financial innovation regulation, or AI governance legislation get a falsifiable, timestamped analytical framework with explicit measurement windows and falsification conditions — the architecture that distinguishes structural analysis from post-hoc commentary and makes the work citable, contestable, and useful.

Conclusion: Who Controls the Feedback Loop Controls the Future

Kalshi is not a prediction market company fighting state gambling regulators. Kalshi is the mechanism through which the legal system is being forced to answer a question that governs the next decade of financial instrument innovation: does the CFTC’s exclusive jurisdiction over designated contract markets displace state classification authority over novel instruments whose value derives from contingent future outcomes?

Crypto media covers the case because crypto firms already know the answer matters to them. The field geometry, the incentive architecture, and the capital alignment all point in the same direction — toward a CFTC regulatory home that offers lower feedback latency, broader instrument classification tolerance, and active institutional support that the SEC has never offered to novel financial instruments. Kalshi is not adjacent to crypto. Kalshi is running crypto’s test case through the federal court system, at its own expense, on a timeline that benefits every instrument class simultaneously.

The field geometry logic does not stop at crypto. AI-generated contracts — instruments whose terms, pricing, and settlement are produced by machine inference rather than human negotiation — require a regulatory framework capable of governing novel instrument structures that no existing classification was designed to anticipate. Tokenized real-world assets — real estate, commodities, receivables converted into on-chain instruments — require a regulatory home where the underlying asset’s contingent value can be priced and settled without triggering securities registration requirements that were built for equity offerings, not asset-backed tokens. Synthetic financial instruments — derivatives whose reference obligation is itself a derived quantity rather than a physical asset or registered security — require exactly the kind of statutory flexibility the CEA’s commodity definition provides and the Securities Act’s security definition does not. Every instrument class that does not fit cleanly inside existing SEC or state regulatory frameworks faces the same field geometry Kalshi is navigating now. A CFTC preemption ruling does not just resolve prediction markets and crypto. It expands the jurisdictional footprint of the only regulatory architecture currently capable of governing the instruments that AI and tokenization are producing faster than any legislative body can classify them.

If the field geometry persists — and the constraint density, geodesic availability, and attractor dominance metrics all indicate that it will — CFTC expansion is not a possibility. CFTC expansion is the default outcome. The only variables are timing and the degree to which congressional action shapes the specific boundaries of that expansion before the courts impose them without legislative input. State attorneys general hold the enforcement velocity advantage now. Federal lawmakers hold the decisive instrument in the legislative window before the circuit split resolves. Investors who treat the current fragmentation as a permanent operating condition are mispricing regime risk at every layer of the emerging financial infrastructure stack.

Control of the feedback loop of financial innovation is migrating toward the CFTC. Kalshi is the mechanism forcing that migration. The litigation outcome determines not just whether Kalshi survives — it determines who governs the instruments that come next, and on whose terms.

MindCast will track every falsifiable prediction in this publication against observable evidence and publish formal model revisions when conditions require it. All predictions carry explicit measurement windows, named trigger events, and falsification conditions. The arc began with The Full Arc of Prediction Markets. The litigation map followed with The National Kalshi Prediction Market Litigation Map. The enforcement strategy framework extended it with Kalshi’s Prediction Market Litigation Architecture, the CFTC Amicus, and the Strategic Framework for State Enforcement. The system-level implication closes the loop here.