MCAI Innovation Vision: How the Chevron–Microsoft Project Kilby Agreement Validated MindCast's Firm-Power Forecast and Signals a Capacity Race Decided by Institutional Throughput, Not Model Capability

From Compute Race to Capacity Race

A companion study to AI Infrastructure, Priority Under Scarcity, How Hyperscaler Nuclear PPAs Function as Capacity-Preemption Protocols in the AI Era (December 2025), which mapped capacity preemption inside FERC's jurisdiction; this paper follows the same strategy after it crossed into ERCOT.

Executive Summary

Chevron and Microsoft announced a 20-year power agreement on June 22, 2026 to build Project Kilby, a co-located natural-gas facility in West Texas delivering roughly 2.67 gigawatts of dedicated power to a Microsoft data center, with first power targeted for 2028. Most coverage will file the agreement under energy procurement. The filing is wrong. Kilby is the moment a specific forecast MindCast published on January 2, 2026 became fact, and a marker of AI competition shifting from a contest over model capability toward a contest over capacity acquisition.

MindCast named the move before it existed. The Federal-State AI Infrastructure Collision scored Microsoft as the first hyperscaler likely to announce a firm-power co-location partnership prioritizing behind-the-meter generation, and scored Texas and its ERCOT grid as the corridor most likely to win that recruitment on speed, firm power, and regulatory clarity. Kilby satisfies both, plus the same forecast’s prediction that natural gas would remain the dominant bridge technology longer than public narratives admit. A dated, scored prediction cleared on schedule.

The deeper claim follows. Capability is no longer the scarce input; the ability to build and govern physical capacity is. A nation or a firm can hold frontier models and still lose position if it cannot pour concrete, secure firm power, and clear permitting at the speed competition demands.

Overview:

The event — Microsoft contracted dedicated, co-located gas generation in ERCOT on a 20-year term, bypassing the public interconnection queue rather than waiting in it.

The validation — the deal confirms a January 2026 MindCast forecast at the actor level (Microsoft), the geographic level (ERCOT), and the technology level (gas as bridge fuel), each scored before the fact.

The shift — the binding constraint on AI has moved from chips and models to firm power, turbines, permitting, and the institutional throughput that converts those inputs into operating capacity.

The stakes — value is migrating to whoever controls the layer where electricity becomes compute, and the public grid is sliding from primary supplier to balancing layer.

I. The Deal, Stated Correctly

Project Kilby pairs new gas generation directly with a Microsoft data center campus in West Texas’s Reeves County, structured through Chevron’s subsidiary Energy Forge One LLC and developed alongside Engine No. 1 — the activist investment firm best known for winning Exxon board seats in 2021 on an energy-transition platform. An oil major building a gas plant with that firm, to power AI, measures how completely the energy-and-compute logic has reordered old alignments. The facility scales in modular phases toward approximately 2.67 gigawatts, drawing most of its generation from GE Vernova turbines with additional capacity from Caterpillar’s Solar Turbines unit. Chevron expects a final investment decision by the end of 2026 and first power in late 2028, targeting mid-teen returns on cash flow the company describes as independent of oil-and-gas price cycles.

Read as procurement, the deal is a large customer buying electricity. Read structurally, the deal is something else: a hyperscaler co-locating dedicated generation to route around the public interconnection queue entirely. Microsoft is not buying cloud capacity, GPUs, or grid power on the open market. Microsoft is securing a private, 20-year, behind-the-meter energy supply chain from an oil major. The distinction is the whole story, because the second reading is the one MindCast has been modeling for eight months.

II. The Forecast That Named It

Foresight earns its keep only when it prints predictions that can fail, then watches them clear or break. MindCast published exactly such a forecast in January. The Federal-State AI Infrastructure Collision ran an actor-level prediction table scored on Causal Signal Integrity, and three of its entries map onto Kilby with notable precision.

Microsoft drew a 0.72 score as the hyperscaler most likely to announce the first post-rule nuclear-or-firm-power co-location partnership, prioritizing behind-the-meter generation to cut interconnection risk — and Kilby lands squarely on the firm-power branch of that prediction. Texas, operating the ERCOT grid, drew a 0.85 — the highest corporate or state score in the table — as the jurisdiction that would accelerate hyperscaler recruitment using speed, firm power, and regulatory clarity as competitive advantages. A forward branch predicted new hyperscale commitments clustering in firm-power corridors and listed ERCOT first; a second branch held that natural gas would remain the dominant bridge technology well past the point public commentary expected. Kilby is Microsoft, behind-the-meter, firm power, gas, in ERCOT. Four scored predictions, one transaction.

The forecast did not arrive from nowhere. AI Computing Is Now Federal Infrastructure had established the parent thesis in November 2025: once the Department of Energy’s October 23 large-loads directive reframed hyperscale AI demand as a federally governed economic force, federal acceleration and corporate firm-power co-location became structurally inevitable system responses rather than discretionary choices. AI, that paper argued, is now governed by energy policy, not technology policy. Kilby is what that governance shift produces on the ground.

One checkpoint deserves its own line. The January forecast set a binary test — at least one major hyperscaler firm-power partnership announced by the fourth quarter of 2026. The announcement clears that checkpoint two quarters early, with the end-of-2026 final investment decision standing as the confirmation event still to come.

III. Why West Texas Is the Strategy, Not the Setting

Location looks like a footnote and functions as the core maneuver. ERCOT is the one major U.S. power market that sits largely outside Federal Energy Regulatory Commission jurisdiction. Every behind-the-meter co-location fight that has stalled the nuclear deals — most visibly Talen Energy’s arrangement to serve an Amazon data center from the Susquehanna plant, rejected by FERC and upheld on rehearing in early 2026 — unfolded inside FERC’s reach. Chevron and Microsoft built where that chokepoint does not bind.

Selecting the jurisdiction before pouring the foundation is routing control raised one level above the physical. MindCast’s CPI Antitrust Chronicle analysis named four routing layers where AI-infrastructure foreclosure forms — queue position, transformer supply, dedicated generation, and cooling architecture. Kilby adds a fifth, regulatory rather than physical: the venue itself. A firm that picks the jurisdiction where governance moves slowest gains the same kind of traversal advantage as a firm that picks a queue position rivals cannot reach — an edge competitors operating elsewhere cannot easily replicate.

MindCast has a name for the maneuver and a law that predicts its outcome. Innovation Becomes Governance defines latency arbitrage as the exploitation of the gap between how fast a private routing system moves and how slowly a public governance system responds — and states plainly that capture requires only outrunning the regulator, never defeating one. The same paper sets out a recurring law: the first occupant of a contested architecture loses legally yet wins structurally, because enforcement against the pioneer certifies the model for a better-capitalized successor. Talen lost the Susquehanna co-location fight at FERC. Under the law, that defeat did not kill behind-the-meter co-location; it certified the architecture and cleared the field. Kilby is the successor capturing the stabilized equilibrium, in the jurisdiction where the architecture faces no comparable challenge.

The preemption strategy migrated along three axes at once. AI Infrastructure, Priority Under Scarcity modeled the first form — nuclear, front-of-the-meter, settled through PJM — and forecast that FERC would harden front-of-the-meter into the survivable template while restricting behind-the-meter co-location. Read inside FERC, the forecast held. Kilby shows what it missed at the edges: the strategy kept its preemption function and changed everything contestable around it, shifting fuel from nuclear to gas, structure from front-of-the-meter to behind-the-meter, and venue from PJM to ERCOT. Kilby suggests that when regulators constrain one structure, firms often migrate the underlying strategy to an adjacent fuel, structure, or jurisdiction rather than abandoning it.

The grid is not becoming optional, and overstating the point invites a fair rebuttal. Chevron’s own language commits Kilby to mitigating impacts on the regional grid that consumers rely on, and reporting on the project describes an on-site plant that supplies the data center directly, connects to the grid later, and sells excess generation into the Texas market — supplier first, grid second. The accurate claim is therefore sharper than “the grid is dead”: hyperscalers are reclassifying the public grid from primary supplier to insurance policy, and a reader can test the reclassification by tracking the contracted firm-service fraction against nameplate capacity. (Confidence the “demotion, not deletion” framing survives an energy-literate critique: ~80%.)

Contact mcai@mindcast-ai.com to partner with us on Predictive Game Theory AI in Law and Behavioral Economics. To deep dive on MindCast works upload the URL of this publication into any LLM (preferably Google AI mode/Gemini, Claude, ChatGPT) and prompt ‘reconstruct MindCast framework with three degrees of cited sub links.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure.

MindCast AI is a cybernetic, predictive game-theory AI firm specializing in law and behavioral economics, applied to complex litigation, innovation systems, and geopolitical risk intelligence. Rather than extrapolating historical patterns, the firm models the mechanisms that generate institutional behavior, running Cognitive Digital Twin simulations grounded in Nash equilibrium, Stigler information economics, and the Chicago School of law and behavioral economics.

IV. The Capital Signature

Capital reveals belief, and a 20-year lock-in reveals a specific one. Microsoft is trading pricing flexibility for supply certainty, a trade a buyer makes only when it fears scarcity more than overpayment. Five years ago Microsoft dictated terms to suppliers; the duration of this commitment suggests the company now assigns substantial value to long-duration capacity certainty. (Confidence the 20-year term reflects scarcity anxiety rather than ordinary hedging: ~75%.)

Kilby’s structure also sorts cleanly into a framework MindCast published in March. The AI Infrastructure Energy Opportunity Landscape separates constraint-removal capital, which expands system capacity and reduces exposure, from scarcity-capture capital, which locks up existing capacity and accumulates risk. Building 2.67 gigawatts of new, additive generation reads as constraint-removal — and that same installment had already cataloged Microsoft’s Constellation nuclear restart, Google’s Fervo geothermal stake, and Amazon’s dedicated-generation portfolio as queue-preemption strategies rather than energy bets. AI Infrastructure, Priority Under Scarcity anatomized those nuclear contracts as capacity-preemption protocols — long-term deals that decide who holds priority under shortage before regulators notice the allocation has happened. Kilby is the next entry in that list, and the move from nuclear to gas widens the pattern across fuel types rather than breaking it.

A complication runs underneath the clean read. Infrastructure Routing Control, MindCast’s argument in the CPI Antitrust Chronicle, holds that dedicated generation agreements are one of four routing layers where competitive foreclosure forms before any application-market dominance becomes measurable. New generation expands capacity and forecloses a routing layer at the same time, which is why the antitrust exposure of these deals depends less on megawatts than on whether the mid-tier developers the article names as the complainant class — CoreWeave, Applied Digital, Crusoe — can still traverse the infrastructure hyperscalers now own.

Kilby lands inside two arguments the Chronicle already made. It joins Microsoft’s Constellation, Google’s Fervo, and Amazon’s supply deals as another instance of the parallel conduct the article treats as circumstantially relevant under Interstate Circuit, and it secures the energy layer the article calls the foundational chokepoint of a full-stack foreclosure theory running from power up through compute, models, and distribution. The binding upstream constraint, meanwhile, is not the gas — it is the turbines. A late-2028 first-power date with GE Vernova as the majority supplier names the real chokepoint, and whoever holds turbine allocation holds a control point one rung above the data center itself.

V. Institutional Throughput Beats Model Capability

The headline number is gigawatts; the operative variable is throughput. MindCast’s National Innovation Behavioral Economics framework measures institutional throughput — the capacity of a system to convert resources into operating outcomes at the tempo competition requires — and pairs it with strategic behavioral coordination to determine actual output. Capacity that exists but cannot be activated produces less than its asset base predicts. National AI competition, read through that lens, resolves into a governance variable rather than a technological one: permitting velocity, interconnection discipline, and execution speed decide the race once models commoditize.

The contrast that sharpens the point is regional, and MindCast already wrote it down. Washington’s Clean Energy Advantage observed in November 2025 that Washington State holds the cheapest clean industrial power in North America and the densest AI compute cluster, yet watches capital migrate to Texas and Virginia — because Washington has the energy and lacks the institutional throughput to deploy it. Kilby is the Texas side of that exact migration. The corridor MindCast named as the destination just captured the deal, while the home state with superior physical endowment did not.

Hardware analysts have been circling the same conclusion from the other direction. Nvidia’s Moat vs. AI Datacenter Infrastructure-Customized Competitors argued in August 2025 that Nvidia’s real risk is not AMD or Intel but the grid — that the bottleneck had already shifted from algorithms to power, cooling, and bandwidth. Kilby provides evidence that scarcity is migrating from silicon toward power, permitting, transmission, and physical infrastructure, ten months after the thesis was published. The next frontier of AI competition is not algorithmic superiority; it is infrastructure acquisition, and the firms standing up dedicated power-procurement teams are revealing where they believe the contest is now decided.

VI. The Sovereignty Layer

Capacity acquisition at this scale buys more than power. A private, jurisdiction-selected, 20-year power-compute enclave acquires a measure of governance autonomy — a position the public regulatory process does not fully reach.

The shift in architecture is what makes the autonomy concrete. Firms once bought electricity from shared infrastructure and took a number in a public allocation queue. Kilby substitutes a different design — private generation, private capacity reservation, and private coordination of a supply chain feeding a single customer. The result is not sovereignty in the political sense but partial autonomy from shared bottlenecks, a condition in which capacity gets governed first by contract and only second by public allocation.

MindCast’s meta-paper, published the same day as the Kilby announcement, supplies both the unit and the metaphor. Why AI Commoditizes Raw Prediction, Why Governance Stays Scarce, and How MindCast Prices the Gap Between Themargues that raw prediction collapses toward free while governance holds a cost floor, and that durable value flows to whoever prices the widening gap — a quantity the paper names governance scarcity. The paper’s closing figure casts MindCast as the grid operator that knows where power flows, who holds the switches, and where the system fails when demand outruns governance capacity. Kilby turns that metaphor literal: an actual grid, actual switches, and an enclave assembling capacity faster than public governance can price the autonomy it confers.

The governance-scarcity frame scales to the national level without modification. Why the “China Invades Taiwan by 2027” Narrative Misprices the AI Industrial Stack treats compute, energy, and fabrication as a single industrial stack on which national competitiveness now rests. A 20-year domestic firm-power agreement is infrastructure sovereignty acquired at the corporate level — the same logic that drives export controls and sovereign-compute positioning, expressed as a private contract rather than a state policy. The unpriced cost on the other side of that sovereignty is governance scarcity, which is the quantity the meta-paper was built to measure.

VII. Falsification and Forward Foresight

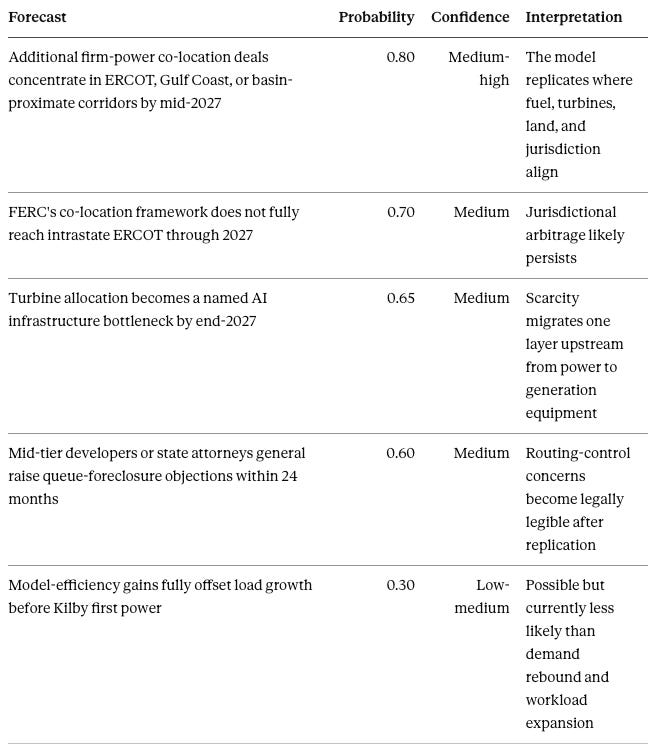

Foresight without kill criteria is commentary. The capacity-race thesis breaks under three conditions, each observable: a federal co-location framework extends to the intrastate ERCOT market and closes the jurisdictional arbitrage; grid-scale storage or small modular reactor economics undercut dedicated gas self-generation before Kilby’s 2028 first power; or model-efficiency gains cut power-per-token faster than usage rises, stranding 20-year contracts as overbuilt. Tracking those three is how the thesis stays honest.

Conditional on the thesis holding, four predictions follow, scored and dated for later grading:

p ≈ 0.80 — adoption concentrates rather than democratizes. The corridor-clustering branch of the January forecast is already materializing — Google exploring on-site gas with Crusoe in Texas, Oracle’s gas-fired Jupiter campus in New Mexico, the Exxon-NextEra Southeast site marketed to hyperscalers — so the live question shifts from whether the model replicates to how its scarce inputs concentrate. By mid-2027, multi-year turbine allocation, ERCOT-grade jurisdictions, and basin-proximate land sit disproportionately with hyperscalers and majors, foreclosing sub-500 MW developers from the same architecture.

p ≈ 0.70 — FERC’s national co-location rulemaking stops short of reaching intrastate ERCOT, preserving the jurisdictional arbitrage through 2027.

p ≈ 0.65 — turbine-supply allocation displaces “chips” as the publicly named binding constraint in mainstream AI-infrastructure commentary by the end of 2027.

p ≈ 0.60 — a mid-tier developer or a state attorney general raises the queue-foreclosure objection against an ERCOT firm-power deal within 24 months, opening the routing-control question MindCast’s CPI argument anticipates.

Conclusion

Capacity races reward execution systems over invention systems, and economic history is consistent on the point. Railroad expansion, electrification, interstate logistics, cloud computing, and semiconductor fabrication each crowned not the first inventor but the institution that could deploy physical capacity at scale. AI is entering the same phase, and Kilby is an early move in it.

Project Kilby is not an energy story, and treating it as one misses both the validation and the shift. MindCast forecast the actor, the geography, and the fuel in January, scored each before the fact, and watched the transaction clear the checkpoint two quarters early. The forecast held, which is evidence the framework is reading the right variable: AI competition increasingly turns on the capacity to build and govern physical infrastructure at speed, not on the marginal model benchmark. The compute race produced the models. The capacity race will decide who runs them — and a 20-year contract for West Texas gas, signed to outrun a regulator and lock down scarce power for two decades, is what the opening move of that race looks like.

Appendix A: MindCast AI Proprietary Cognitive Digital Twin Foresight Simulation

Purpose

MindCast ran targeted Cognitive Digital Twin (CDT) Vision Function flows against the Chevron–Microsoft Project Kilby event to test whether the transaction functions merely as an energy procurement agreement or as evidence of a broader AI infrastructure capacity race. The flows evaluated institutional throughput, routing control, governance scarcity, and forward competitive concentration.

1. NIBE Vision: Institutional Throughput Flow

Vision Function: National Innovation Behavioral Economics

Core Question: Does Project Kilby validate the thesis that institutional throughput now governs AI infrastructure advantage?

CDT Output

Project Kilby scores as a high-throughput infrastructure execution event. Microsoft did not merely procure electricity; it secured a long-duration capacity pathway through a jurisdiction, fuel source, generation partner, turbine supply chain, and deployment corridor capable of converting strategic intent into physical capacity by late 2028.

ERCOT functions as the throughput amplifier. Its value does not derive only from gas availability or land availability. Its strategic value comes from lower regulatory friction, faster project translation, and weaker exposure to federal co-location constraints compared with FERC-regulated corridors.

Washington illustrates the inverse condition. A region may hold superior clean-energy endowment and dense AI talent while losing deployment share when institutional throughput cannot convert those advantages into operating infrastructure at competitive speed.

Interpretive Finding

Kilby validates the NIBE claim that AI competition increasingly turns on activation capacity, not merely resource possession. Power that cannot be permitted, interconnected, financed, and delivered on schedule has lower strategic value than dirtier or less elegant power that can be converted into compute faster.

NIBE Classification

Output Class: High-Throughput Capacity Acquisition Event

Institutional Throughput Score: 0.84

Strategic Behavioral Coordination Score: 0.79

Confidence Band: 80–85%

Prediction

By mid-2027, AI infrastructure announcements will increasingly lead with execution variables — firm power date, turbine allocation, permitting status, interconnection status, and jurisdiction — rather than model benchmarks or GPU counts.

Probability: 0.72

Confidence: Medium-high

2. Infrastructure Routing Control CDT Flow

Vision Function: Infrastructure Routing Control

Core Question: Does Kilby extend routing control from physical infrastructure into jurisdictional venue selection?

CDT Output

Project Kilby validates dedicated generation as a routing layer and extends the prior routing-control framework. The CPI Antitrust Chronicle analysis identified four routing layers: queue position, transformer supply, dedicated generation, and cooling architecture. Kilby adds a fifth layer: regulatory venue selection.

The transaction shows that routing control does not require physical ownership alone. A firm can gain traversal advantage by selecting the jurisdiction where its preferred infrastructure architecture faces the least governance resistance. ERCOT therefore becomes more than a grid. It becomes a strategic routing environment.

Kilby’s risk profile remains analytically dual. New generation expands total system capacity, which reduces physical scarcity. Yet dedicated capacity also channels infrastructure access through private contracting, which may limit the ability of mid-tier developers to traverse the same stack.

Interpretive Finding

Kilby does not prove anticompetitive conduct. It does validate the structural claim that AI infrastructure competition is moving upstream into control points that precede application-market dominance.

Routing-Control Classification

Output Class: Regulatory Routing Layer Extension

Routing Layer Activated: Dedicated generation + jurisdictional venue

Foreclosure Risk: Emerging, not mature

Legal Exposure: Structural watch zone, not violation finding

Confidence Band: 75–80%

Prediction

Within 24 months, at least one public objection from a mid-tier developer, state attorney general, utility stakeholder, or policy analyst will frame hyperscaler firm-power agreements as a queue-access or infrastructure-foreclosure problem rather than a conventional energy procurement issue.

Probability: 0.60

Confidence: Medium

3. AGE / Governance Scarcity Flow

Vision Function: Agent Governance Equilibrium / Governance Scarcity

Core Question: Does Kilby show private infrastructure governance moving faster than public allocation governance?

CDT Output

Kilby indicates rising governance scarcity. Public grid allocation, FERC co-location review, interconnection queues, and transmission planning cannot move at the speed hyperscaler AI demand requires. Microsoft’s response is not to wait for public coordination to improve. It substitutes a private contractual governance architecture: Chevron, Engine No. 1, GE Vernova, Caterpillar Solar Turbines, ERCOT, land, gas, and a 20-year offtake arrangement.

The public grid remains relevant, but its role changes. It becomes a balancing layer, backup layer, and excess-generation outlet rather than the primary source of AI infrastructure certainty.

Interpretive Finding

Kilby shows the governance gap becoming physical. When public allocation mechanisms cannot price scarcity quickly enough, private actors create enclaves where capacity is governed first by contract and second by public systems.

AGE Classification

Output Class: Governance-Constrained System

AGE Band: 1.25–1.45

Governance Debt: Rising

Governance Resilience: Moderate

Confidence Band: 75–85%

Prediction

By 2028, policy debate over AI infrastructure will shift from “how much electricity do data centers consume?” to “who controls the governance layer where electricity becomes compute?”

Probability: 0.68

Confidence: Medium-high

4. Capacity Race Forecast Matrix

Integrated CDT Conclusion

The recommended Vision Function flows support the publication’s central thesis: Project Kilby is not merely an energy procurement transaction. It is a capacity-acquisition event, a routing-control event, and a governance-scarcity event.

NIBE Vision identifies the decisive variable as institutional throughput. Infrastructure Routing Control CDT identifies the new strategic layer as regulatory venue selection. AGE Vision identifies the governance condition driving the transaction: private capacity governance moving faster than public allocation governance.

The combined interpretation is clear: AI competition is entering a phase where advantage accrues to firms that can secure the physical, contractual, and jurisdictional pathways through which electricity becomes compute. Model capability still matters, but the scarce variable is increasingly the governed capacity to run those models at scale.

Appendix B: Citations and Relevance

Primary source

Chevron Signs 20-Year Power Agreement with Microsoft for West Texas Data Center (BusinessWire, June 22, 2026) — The Chevron announcement of Project Kilby and the source for all deal terms cited above.

MindCast corpus

Why AI Commoditizes Raw Prediction, Why Governance Stays Scarce, and How MindCast Prices the Gap Between Them — The meta-paper that names governance scarcity as the AI economy’s unit of account and supplies the grid-operator metaphor Kilby renders literal.

The Federal-State AI Infrastructure Collision — The January 2026 foresight simulation that scored Microsoft firm-power co-location (CSI 0.72) and ERCOT (CSI 0.85) before the deal existed, making Kilby a validation event.

AI Computing Is Now Federal Infrastructure — The November 2025 parent paper establishing that the DOE large-loads directive made hyperscaler firm-power co-location a structurally inevitable response.

The AI Infrastructure Energy Opportunity Landscape — Distinguishes constraint-removal from scarcity-capture capital and already cataloged hyperscaler dedicated-generation deals as queue-preemption strategies, the list Kilby extends.

AI Infrastructure, Priority Under Scarcity (December 2025) — The CDT simulation that named hyperscaler PPAs as capacity-preemption protocols and framed the contest as priority under shortage; Kilby extends the template from nuclear and front-of-the-meter to gas and behind-the-meter.

Infrastructure Routing Control: The Operative Antitrust Trigger in AI Energy Markets (CPI Antitrust Chronicle, April 2026) — Names the four routing layers where AI-infrastructure foreclosure forms and the full-stack foreclosure theory Kilby anchors; the draft extends it by adding jurisdiction as a fifth, regulatory routing layer.

Innovation Becomes Governance — Supplies latency arbitrage, the infrastructure-sovereignty thesis, and the “lost legally, won structurally” law that connects Talen’s FERC defeat to Kilby’s success.

National Innovation Behavioral Economics — Defines institutional throughput, the spine variable behind the claim that AI competition now turns on execution capacity rather than model capability.

Washington’s Clean Energy Advantage — Documents capital migrating from energy-rich Washington to Texas for lack of throughput, the regional contrast Kilby’s Texas siting confirms.

Nvidia’s Moat vs. AI Datacenter Infrastructure-Customized Competitors — Argued that Nvidia’s real risk is the grid, naming the chip-to-power migration of scarcity that Kilby makes concrete.

MindCast AI’s NVIDIA NVQLink Validation — Logged a forecast that energy would become the binding constraint by 2028, the year Kilby targets first power.

MindCast Dynamic Game Theory — Models rule mutability and forum selection as strategic variables, the logic underneath choosing ERCOT to route around FERC.

Why the “China Invades Taiwan by 2027” Narrative Misprices the AI Industrial Stack — Frames compute and energy as one industrial stack underpinning national competitiveness, scaling Kilby’s sovereignty implication beyond the firm.