MCAI Lex Vision: Compass's Skillman Moment Reaches the C-Suite, Cris Nelson Moment Holds at the Regional Tier

Diagnostic Specimens From Compass's Nationwide MLS Rule-Capture Campaign — Reffkin's Q1 Earnings Call, the Spokesperson Template, and the Post-SSB 6091 Communications Architecture

Related: Compass Law and Behavioral Economics Series | The MindCast MLS Equilibrium Series

Executive Summary

Compass has executed a nationwide MLS rule-capture campaign across at least four major regional multiple listing services in the seven months between October 2025 and May 2026, with at least one additional MLS under active demand-letter pressure. Midwest Real Estate Data (MRED) in Chicago, Realtracs in Nashville, The MLS/CLAW in Los Angeles, and Bright MLS across the Mid-Atlantic each adopted identity-protective IDX rules and opened nationwide membership under partnership terms with Compass International Holdings. Hive MLS in North Carolina received a Compass demand letter on May 11, 2026, with a May 20 enforcement deadline. CEO Robert Reffkin committed to the strategy directly on the May 5, 2026 Q1 earnings call: “I want to create a national MLS to compete against local MLSs.” On May 12, 2026, Zillow filed a federal antitrust complaint in the Northern District of Illinois alleging the partnerships operate as a coordinated Sherman Act conspiracy designed to coerce portal compliance with Compass’s private-listing distribution architecture. The active analytical surface as of the publication horizon is not a Washington-specific regulatory event. The active surface is a nationwide platform transition operating across multiple state jurisdictions under simultaneous regulatory pressure.

The Washington State SSB 6091 cycle — the state licensing statute that takes effect June 11, 2026 and prohibits the off-market closed-loop network model the nationwide campaign is designed to expand — operates as one front in the broader strategy. The Washington record carries specific diagnostic value: it captures the Compass communications architecture operating without enterprise-level message management during a regional legislative fight where the campaign’s national vocabulary encountered state-level adversarial conditions. The Washington specimens this publication develops are the diagnostic instantiations of how the national campaign operates when state-level regulatory compression makes the architecture’s load-bearing assumptions visible. Section I documents the active nationwide campaign in full. The remaining sections trace the diagnostic structure tier by tier.

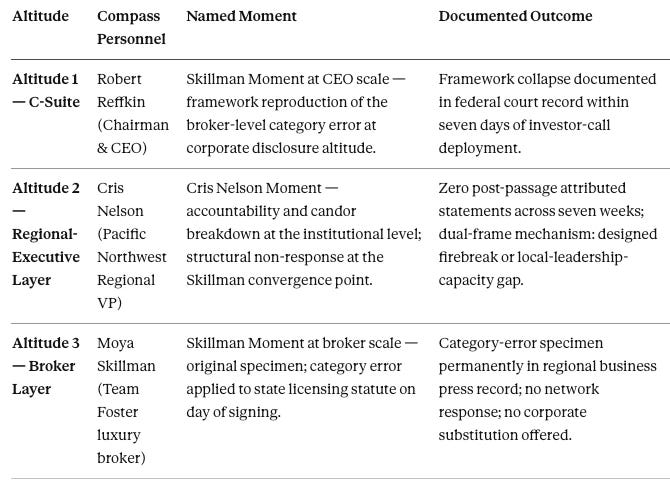

The Skillman Moment, established as a recurring analytical label across MindCast’s Compass Law and Behavioral Economics Series, names the specific failure mode in which Compass’s internal “seller choice” narrative architecture coheres inside the Compass commercial environment but fails to export when it contacts a regulatory, statutory, or evidentiary record outside that environment. The original specimen — Moya Skillman applying Reffkin’s MLS-targeted seller-choice framing to SSB 6091, a state licensing statute, on the day Governor Ferguson signed the bill into law — demonstrated the pattern at the broker level inside a regional business publication. The Cybernetics of Compass Holdings’ Narrative Control Architecture — Inventory Restriction, Commission Capture, and the Collapse of Audience Separationformalized the mechanism. How the Zillow Complaint Reframes Compass v. NWMLS as a National Coordination Casedocumented the federal-scale recurrence in the May 12, 2026 Zillow v. MRED-Compass antitrust filing.

The publication documents the parallel post-SSB 6091 specimen at the regional-executive tier — the Cris Nelson Moment, named in The Cybernetics of Compass Holdings’ Narrative Control Architecture as accountability and candor breakdown at the institutional level. Cris Nelson, Compass’s Pacific Northwest Regional Vice President, was the senior Compass executive present at both Washington SSB 6091 hearings and chose not to testify. Nelson has issued zero post-passage press statements, zero attributed quotes in Compass corporate releases since SSB 6091’s signing, and remains structurally absent from the entire Compass post-passage communications stack. The Cris Nelson Moment specimen is the structural non-response at the regional-executive tier when an agent in the Regional VP’s own jurisdiction — Moya Skillman, on Team Foster — produced the category-error public-record specimen on the day Ferguson signed the bill, the convergence point where regional-executive engagement would have interrupted the category error before it propagated upward through the spokesperson layer to the CEO layer. The interruption did not happen. The propagation chain — broker error to CEO framework reproduction seven weeks later — passed through the regional tier without regional engagement.

The Cris Nelson Moment is harder analytical work than the Huff Moment because Huff is the recorded named witness and standard testimony analysis suffices. Analysis focused solely on the named witness misses the more consequential institutional layer. Nelson did not testify; the Cris Nelson Moment specimen must be constructed from structural absence rather than documentary presence. The accountability breakdown surfaces in the negative space at convergence points where the regional tier carried operational responsibility and did not exercise it.

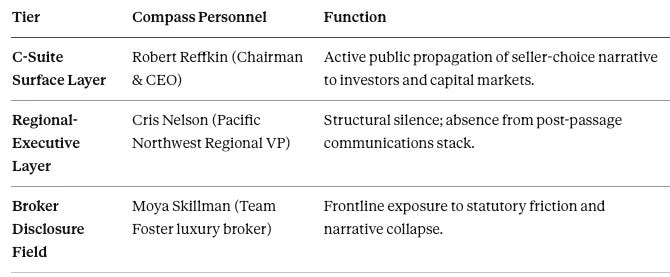

The Reffkin Q1 2026 earnings call on May 5, 2026 — the first investor communication after the SSB 6091 signing and the Anywhere merger close — supplies the third documented instantiation of the Skillman Moment and the highest-altitude one to date. Compass Chairman and CEO Robert Reffkin stated on the record that “MLS rules are just rules of a business; they’re private entities” and that “the seller should be the only person who decides how they market their home in the context of the law, and fiduciary duty and statutory duty.” The framing reproduces, verbatim at the framework level, the same category error Skillman committed at the broker level. The framing functions inside Compass’s commercial narrative environment. The framing fails to export to the federal antitrust record where, seven days later, the Zillow complaint documents Compass demanding identity-protective rule changes at four MLSs nationwide — using the same MLS rules Reffkin characterized as merely “private entities” as the operative enforcement weapon against Zillow’s display policies.

The publication identifies the post-SSB 6091 Compass communications stack as a three-tier architecture: the CEO tier (Reffkin) carries the framework; the corporate-spokesperson tier carries the templated reproduction; the regional-executive tier (Nelson) carries the structural silence. The architecture admits two competing explanatory mechanisms — designed firebreak, under which Compass strategically maintains regional silence to preserve enterprise deniability; and local-leadership-capacity gap, under which Compass corporate has centralized at national altitude because the regional tier in Washington could not credibly carry the position under post-passage adversarial conditions. Both readings produce the same observed architecture; they diverge on falsifiable forecasts for jurisdictions advancing SSB 6091 analogues. The local-flailing reading strengthens the platform-transition thesis: forced national centralization is more visible to antitrust enforcement than deliberate multi-tier fragmentation because it removes the local-distribution cover that complicates Section 1 conspiracy theories. The Skillman-active / Nelson-silent contrast within Compass’s Pacific Northwest regional structure documents the architectural divide under either reading: front-facing brokers absorb public-messaging-failure exposure while regional executives withdraw from the public communication layer entirely.

The pattern is now documented across three altitudes — broker (Skillman, January 2026), CEO (Reffkin, May 2026), and the absent-regional-executive buffer (Nelson, March 2026 through present) — across three forums (state regulatory hearing, federal investor communication, federal antitrust litigation) and three audiences (legislators, investors, federal court). The convergent failure-to-export across all three altitudes confirms the Skillman Moment as a structural feature of Compass’s narrative architecture rather than a contingent communication choice attributable to any single Compass spokesperson or any single forum. The three-tier architecture is now the operational analytical object the MindCast prediction record targets.

The Skillman Moment is the inevitable structural byproduct of an organization attempting to run a hyper-centralized capital-markets narrative on top of a highly fragmented, locally regulated physical infrastructure. When the broker layer, the regional-executive layer, and the CEO layer can no longer align their public statements with the statutory and evidentiary realities of state legislatures and federal courts, the corporate narrative structure collapses. The post-NAR-settlement litigation environment — operating across federal antitrust enforcement, state consumer protection authority, securities-law disclosure standards, and state licensing statutes including SSB 6091 — converts audience separation from a strategic choice into a structural impossibility. The convergence demonstrates that Compass’s communications architecture is no longer built to manage public transparency. It is built to survive it.

The deeper thesis this publication develops is that Compass is not running a defective communications operation. Compass is executing a platform transition. The communications architecture, the litigation portfolio, the MLS partnership campaign, the Anywhere merger, and the Redfin alliance are coordinated components of a single operational migration toward a partially vertically integrated visibility infrastructure operating alongside — rather than fully inside — the inherited universal-MLS cooperative model. The Skillman Moment specimens are not communication failures; they are the transition costs the migration produces in a regulatory environment that has not yet adapted to the visibility-redistribution model. Section X develops this thesis in full.

I. The Nationwide MLS Rule-Capture Campaign — Where the Platform Transition Operates Right Now

The active analytical surface as of the May 16, 2026 publication horizon is not a Washington-specific regulatory event. The active surface is a nationwide MLS rule-capture campaign that Compass has executed across at least four major regional multiple listing services in the seven months between October 2025 and May 2026, with at least one additional MLS under active demand-letter pressure. The campaign is documented in the May 12, 2026 Zillow v. MRED-Compass federal antitrust complaint, in the rolling MLS partnership announcements at MRED, Realtracs, The MLS/CLAW, and Bright MLS, and in Compass CEO Robert Reffkin’s May 5, 2026 Q1 earnings call commitment to “create a national MLS to compete against local MLSs.”

The campaign’s analytical relevance for this publication is structural. The Skillman Moment and the Cris Nelson Moment — the named specimens this publication develops in Sections IV and V — are not isolated Washington-state communication failures. The two specimens are the diagnostic instantiations of how the nationwide MLS rule-capture campaign operates when it encounters state-level regulatory compression. SSB 6091 in Washington is one front in the campaign; the campaign’s broader operational pattern propagates across Illinois, Tennessee, California, the Mid-Atlantic, and North Carolina simultaneously. The Washington specimens reveal what the architecture is and how it fails under adversarial conditions. The nationwide campaign reveals where the architecture is being deployed and what it is designed to produce.

The Rolling Partnership Record — April–May 2026

The nationwide MLS rule-capture campaign carries a documented timeline that the May 12 Zillow complaint and contemporaneous trade press coverage establish.

In October 2025, Reffkin contacted at least eight regional MLSs urging them to “rigorously enforce existing policies that prevent the rise of off-MLS databases” and to “discipline” Zillow by blocking the portal from IDX and VOW feeds unless Zillow reversed its Listing Access Standards. The Zillow complaint identifies the October 2025 outreach as the campaign’s origination point.

In April 2026, Midwest Real Estate Data (MRED) — the Chicago-area MLS with approximately 98% market share of Chicago-area listings and approximately 28% of national listing volume by Compass-affiliated calculation — announced a nationwide expansion of its Private Listing Network in partnership with Compass International Holdings (CIH). The expansion allowed Compass agents across the country to input listings into MRED’s system. Compass holds Preferred Unit Owner status at MRED. Three Compass-affiliated representatives sit on MRED’s Board of Managers, including Fran Broude, Compass regional vice president for Illinois, Minnesota, Indiana, and Wisconsin, who has served fourteen of the last sixteen years on the board. MRED CEO Rebecca Jensen concurrently serves as Board Chair of MLS Grid, the technology provider that distributes MRED feeds and provides infrastructure to other MLSs including Realtracs.

On April 30, 2026, Realtracs — Tennessee’s largest MLS, supporting 19,000-plus professionals across six states — announced its own nationwide expansion. Compass International Holdings and United Real Estate were named launch partners. Realtracs adopted IDX rules barring “excluding listings based on the identity of a Participant, brokerage firm, subscriber, licensee, or representative” — the same rule template MRED had adopted weeks earlier. Compass committed to subsidize Realtracs membership for CIH agents who joined. The Realtracs announcement framed the move under the “broker, agent, and client choice” vocabulary documented across the Compass corpus.

On May 6, 2026, The MLS/CLAW — the Los Angeles-area MLS covering Beverly Hills, Brentwood, and surrounding luxury markets — announced an equivalent partnership. CLAW updated its IDX policies and gained access to Compass’s full active listing inventory. Compass agreed to reimburse switching costs for “the first 100,000 agents who join from Compass International Holdings, as well as the first 10,000 agents who join from outside Compass International Holdings.” CLAW membership opened to any real estate professional nationwide holding an active California Department of Real Estate license.

On May 11, 2026, Compass sent a demand letter to Hive MLS in North Carolina, urging Hive to “rigorously enforce existing policies that prevent the rise of off-MLS databases” by May 20. In exchange for compliance, Compass offered to keep its listings exclusively within Hive MLS’s territory. The Hive demand letter is documented in the Zillow complaint as the most recent extension of the rule-capture campaign at the May 12 publication horizon.

On May 13, 2026 — one day after the Zillow antitrust complaint was filed — Bright MLS announced the most significant partnership to date. Bright MLS is one of the nation’s largest MLSs by subscriber count, serving New Jersey, Pennsylvania, Virginia, Maryland, Delaware, and the District of Columbia. Bright CEO Brian Donnellan published a Real Estate News op-ed stating that “Compass has committed to making its nationwide data available to our subscribers through our system” and that Compass would subsidize new Bright subscriptions for CIH agents. Bright also updated its ruleset on Sunday, May 10, 2026 — three days before the public announcement — with the same template language pattern. Bright did not respond to Inman’s questions about how the rule changes apply to Zillow and other portals.

The Same Playbook at National Scale

Zillow Chief Industry Development Officer Errol Samuelson described the pattern as “the same playbook” operating across MRED, Realtracs, and CLAW, with Bright following one day after his May 13 Inman interview. Each MLS adopted the same rule template barring portals from excluding listings based on the identity of the participating broker. Each MLS then opened nationwide membership and named Compass as a launch partner. Each rule change positioned the MLS to cut Zillow’s data feed if Zillow continued to enforce its Listing Access Standards. The template propagates across MLSs without material variation.

The May 12 Zillow complaint characterizes the pattern as a Sherman Act conspiracy. The complaint’s central allegation is that Compass and MRED “conspired to threaten to cut off Zillow’s and any other competitors’ access to all listings — a critical input for competition in the industry — in a naked effort to coerce their competitors to abandon pro-transparency policies.” The complaint extends the allegation to the Realtracs, CLAW, and Hive transactions as parts of a coordinated multi-MLS campaign rather than a series of independent commercial agreements.

The structural feature that the May 12 complaint surfaces is not the rule changes themselves. Private MLSs have historical authority to set their own rules. The structural feature is the documented pattern of coordinated rule changes across multiple MLSs simultaneously, driven by a single brokerage’s outreach campaign (Reffkin’s October 2025 demand letters to at least eight MLSs), executed under rule template language that operates uniformly across jurisdictions, and accompanied by financial subsidies (Compass subsidizing membership costs for CIH agents joining each partner MLS). The Sherman Act conspiracy theory rests on the coordination pattern, not on any individual rule.

The CEO Public Commitment to the National MLS Strategy

Reffkin stated the strategy directly on the May 5, 2026 Q1 earnings call. The relevant CEO statements:

“I want to create a national MLS to compete against local MLSs.”

“We are bringing MRED national, as well as it will be just a select number of MLSs that are pro-seller choice, where we’re going to give them all of our listings, where we’re going to subsidize our agents joining. It’s not that I want to create a national MLS to replace local MLSs. I want to create a national MLS to compete against local MLSs.”

The Reffkin statements operate as direct CEO-tier public commitment to the campaign documented in the May 12 Zillow complaint. The commitment is in the securities-disclosure record — earnings call transcripts trigger securities-law disclosure standards under Regulation FD and operate as binding admissions under Federal Rule of Evidence 801(d)(2)(D) for the CEO’s authorized statements on behalf of the corporation. The CEO has therefore publicly committed to the nationwide MLS partnership strategy that the Zillow complaint characterizes as a Sherman Act conspiracy.

The Nationwide Campaign as Forced Layer 3 Reconstruction

The nationwide MLS rule-capture campaign reads with greater analytical precision once anchored to the Three-Layer Acquisition Hierarchy developed across The Compass Commission Consolidation Strategy and Real Estate Marketing Transparency and applied to the Compass v. NWMLS litigation record in Compass v. NWMLS — The Counterclaim That Closed Compass’s Antitrust Thesis. The Hierarchy separates the Compass-Anywhere merger’s $1.6 billion acquisition price into three components: Layer 1 (base operating value — 340,000 agents, established brokerage brands, transaction volume across 35 markets, surviving any regulatory change); Layer 2 (scale synergies — technology platform consolidation, cross-brand referrals, agent-network advantages, surviving SSB 6091 intact); and Layer 3 (the $400-800 million private-exclusive infrastructure premium that exists only if listings can be withheld from the open market long enough for an internal Compass buyer to arrive first, capturing both the listing-side and buyer-side commission on the same transaction).

Paragraph 43 of the NWMLS counterclaim — Compass’s own counterclaim-response filing acknowledging that the Private Phases of the Three-Phased Marketing Strategy will violate Washington state law when SSB 6091 takes effect on June 11, 2026 — documents Layer 3 as legally expiring in Washington under professional certification. The internal Layer 3 architecture Compass operated through NWMLS Rule 2 between April 2025 and the SSB 6091 signing cannot continue operating after June 11. The $400-800 million of the Anywhere acquisition premium that depends on Layer 3 operation is therefore subject to Washington-specific legal extinguishment — and to state-level legislative ratchet replication as Illinois, Connecticut, Hawaii, and other jurisdictions advance SSB 6091-analogue legislation.

The nationwide MLS rule-capture campaign is the operational response to that extinguishment. Compass cannot allow Layer 3 to expire without external replacement architecture. The $2.6 billion in post-merger debt assumed at the January 9, 2026 Anywhere acquisition close, against a firm that has never posted a full-year GAAP profit, converts Layer 3 from a strategic preference into a solvency argument. The Debt-Narrative Correlation documented in The Cybernetics of Compass Holdings’ Narrative Control Architecture — Compass’s rhetorical intensity tracks balance-sheet constraints rather than market conditions — applies directly: the April–May 2026 partnership velocity (four MLSs in fourteen days, one demand letter pending, Reffkin’s May 5 framework commitment) is debt-service pressure expressed as operational urgency, not strategic confidence.

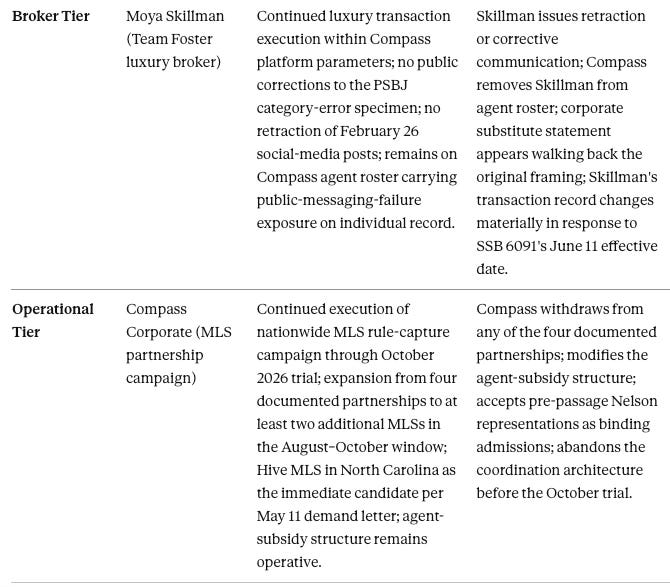

The MRED, Realtracs, CLAW, and Bright MLS partnerships are therefore not opportunistic platform consolidation. They are forced Layer 3 reconstruction. Compass is rebuilding the private-exclusive infrastructure externally — through MLS rule capture at jurisdictions that have not yet enacted SSB 6091 analogues — because internal Layer 3 (Private Exclusives operating under NWMLS Rule 2 in Washington) is statutorily eliminated June 11. The shared rule template each partner MLS adopts operates as the architectural substitute for the off-market closed-loop network the Washington statute prohibits. The agent-subsidy structure (Compass covering “switching costs for the first 100,000 agents who join from Compass International Holdings, as well as the first 10,000 agents who join from outside”) is the economic mechanism that converts the partner MLSs from neutral regional cooperatives into Compass-controlled distribution channels. Reffkin’s “create a national MLS to compete against local MLSs” on the May 5 earnings call is not aspirational framing. It is the operational commitment to Layer 3 reconstruction under debt-service compression.

The Layer 3 reconstruction framing reframes the publication’s central analytical objects. The Skillman Moment specimens are not isolated communication failures. They are the diagnostic surfaces where Layer 3 reconstruction encounters state-level regulatory compression. The Cris Nelson Moment is not generic regional silence. It is the structural absence at the layer where Layer 3’s local-jurisdictional incompatibility (Washington) cannot be articulated without exposing the campaign’s jurisdiction-dependent legal architecture. The three-tier communications architecture documented across Sections IV, V, and VI is the public-communication infrastructure that Layer 3 reconstruction requires to operate at national scale while individual state jurisdictions impose Layer 3-incompatible statutory regimes. The endgame thesis Section X develops becomes precise under this framing: the platform transition is the cooperative-to-proprietary platform-function transformation, and the nationwide MLS rule-capture campaign is its operational vehicle, and the Skillman/Cris Nelson Moments are its diagnostic specimens — all three operate as components of forced Layer 3 reconstruction under post-NAR-settlement litigation environment compression.

Where Washington Sits in the National Campaign

Washington State SSB 6091 occupies a specific position in the nationwide campaign. The statute is the first state-level transparency legislation to pass that directly prohibits the off-market closed-loop network model the campaign is designed to expand. SSB 6091 takes effect June 11, 2026 — twenty-six days after the publication horizon. The Washington operational pattern after June 11 will be governed by SSB 6091’s concurrent-marketing requirement; the campaign’s nationwide pattern operates without that constraint in the other jurisdictions where the MLS partnerships have been executed (Illinois, Tennessee, California, the Mid-Atlantic).

The Washington specimens this publication develops — the Skillman Moment at the broker level, the Cris Nelson Moment at the regional-executive level, the Skillman Moment at CEO scale — are the diagnostic instantiations of how the national campaign operates when it encounters state-level regulatory compression that the rest of the campaign’s jurisdictions do not yet impose. The Washington record reveals what the campaign architecture is structurally; the nationwide partnership rollout reveals where the architecture is being deployed and what it is designed to produce. The two analytical surfaces operate as complementary diagnostics of the same operational object — forced Layer 3 reconstruction under debt-service pressure.

The platform-transition thesis Section X develops in full applies the diagnostic structure to the strategic question: Compass is attempting to transform listing visibility from a cooperative governance function into a proprietary platform function, and the nationwide MLS rule-capture campaign is the operational vehicle of that transformation. The Washington specimens — including the four documented Cris Nelson Moment convergence points and the May 5 Reffkin CEO-scale Skillman Moment — are the points where the transformation is visible under adversarial conditions. The remaining sections trace the transformation’s diagnostic structure tier by tier.

II. The Original Specimen and the Established Pattern

The Skillman Moment was established in the MindCast Compass Law and Behavioral Economics Series across The Compass / NWMLS Antitrust Landscape, The Compass Commission Consolidation Strategy and Real Estate Marketing Transparency, and the umbrella publication The Compass Collapse — A Post Washington SSB 6091 Passage Reckoning. The original specimen carried four specific structural features.

The first feature was the audience separation. Skillman’s Puget Sound Business Journal commentary occurred inside a regional business publication on March 16, 2026, the same day Governor Ferguson signed SSB 6091 into law. The statement — that “sellers should have the right to choose when, where and how they market their homes” — reproduced Reffkin’s MLS-targeted seller-choice framing without modification. The framing had been developed in the context of Compass’s federal antitrust litigation against NWMLS Rule 2, where it operated as an argument against private cooperative governance. Skillman applied the framing to a state licensing statute — SSB 6091 amends Chapter 18.86 RCW, governing broker professional conduct, not MLS cooperative governance — without recognizing the legal-regime mismatch.

The second feature was the on-the-same-day timing. The statement appeared in the regional business press in the same news cycle as the signing of the statute the framing was being deployed against. The temporal proximity ruled out any defense that Skillman was speaking outside the immediate enforcement context.

The third feature was the absence of supporting external validation. No independent consumer group, housing advocacy organization, or unaffiliated industry body supported the seller-choice position at the SSB 6091 hearings. The bill passed 141–1 across both chambers of the Washington Legislature.

The fourth feature was the network silence after the framing was named. Once MindCast identified the Skillman Moment as a category-error specimen in the public record, no response came from Skillman, from Compass’s communications operation, or from any element of the affiliated network. The silence confirmed that the framing was not defensible outside the Compass commercial environment in which it was generated.

The Cybernetics of Compass Holdings’ Narrative Control Architecture formalized the mechanism as the audience-separation collapse: Compass’s narrative architecture depends on maintaining separate audiences with separate optimization functions, where framings developed for one audience are not subjected to scrutiny by another. The Skillman Moment names the specific event in which audience separation fails and a Compass framing developed inside one environment encounters another environment that rejects it.

Contact mcai@mindcast-ai.com to partner with us on Predictive Game Theory AI in Law and Behavioral Economics. To deep dive on MindCast work in Cognitive AI upload the URL of this publication into any LLM (preferably Google AI mode) and prompt ‘reconstruct MindCast framework with three degrees of cited sub links.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure.

III. The Federal-Scale Confirmation

How the Zillow Complaint Reframes Compass v. NWMLS as a National Coordination Case documented the federal-scale recurrence in the May 12, 2026 Zillow v. MRED-Compass complaint filed in the Northern District of Illinois. The complaint introduced documentary evidence of a national rule-change coordination campaign across at least four MLSs over a seven-month period: Reffkin demand letters to at least eight MLSs in October 2025, MRED Revised Rules effective October 29, 2025, Realtracs rule changes April 30, 2026, CLAW rule changes May 6, 2026, and a Hive MLS demand letter dated May 11, 2026 with a May 20 enforcement deadline.

The federal-scale Skillman Moment carries three dimensions absent from the original specimen. The first is institutional altitude — federal antitrust litigation rather than state regulatory commentary. The second is evidentiary specificity — the complaint provides documentary evidence rather than relying on structural inference. The third is institutional reach — the federal complaint operates across federal antitrust law, state consumer protection law, state licensing law in jurisdictions enacting SSB 6091 analogues, and federal securities law through Compass’s public-company disclosure obligations.

The federal-scale Skillman Moment confirmed that the analytical category operates structurally rather than incidentally. The pattern was not specific to particular Compass spokespeople, particular regulatory contexts, or particular litigation forums. The pattern was the mechanical failure mode operating whenever commercial narrative architecture exports into regulatory environments under different optimization functions.

The May 5, 2026 earnings call, which preceded the May 12 complaint by seven days, supplied the framework-level statement of the framing that the May 12 complaint would surface as a Sherman Act violation. The two documents read together constitute the cleanest paired-evidentiary anchor in the corpus. Three dimensions of the federal-scale confirmation extend the analytical record beyond the original specimen.

The Evidentiary Mismatch

Reffkin’s May 5 framework characterizes MLS rules as merely “rules of a business; they’re private entities” whose authority is subordinate to seller choice, fiduciary duty, and statutory duty. The Zillow complaint introduces documentary evidence that Compass does not, in fact, treat MLS rules as private business choices subordinate to seller authority. Compass treats MLS rules as the operative regulatory mechanism through which third-party portal display policies can be overridden under threat of feed termination.

The evidentiary mismatch is direct rather than inferential. The complaint documents that the rule changes at MRED, Realtracs, and CLAW each adopted identity-protective language prohibiting feed recipients from “excluding listings based on the identity of a Participant, brokerage firm, subscriber, licensee, or representative.” That rule language is operationally binding — Zillow’s choice is to display the protected listings or lose access to the entire feed. The same rules Reffkin characterizes as “just rules of a business” function in the Zillow complaint as private regulatory weapons compelling third-party compliance with Compass’s private-listing distribution strategy. The framework cannot accommodate this evidentiary record without conceding either that MLS rules carry binding authority (in which case NWMLS Rule 2 carries equivalent binding authority Compass cannot challenge in federal court) or that the rule changes Compass secured at four MLSs are equally non-binding (in which case Zillow retains the authority to disregard them that Compass claims sellers retain to disregard NWMLS rules). The framework’s load-bearing premise — that MLS rule authority is a function of seller-choice fidelity rather than rule-setter identity — is dismantled by the documentary record at the evidentiary layer.

The Weaponization of Data Feeds

The May 12 complaint documents the operational mechanism by which the framework was translated into market-restraint conduct. The mechanism is data feed coercion, not seller-choice advocacy.

The complaint alleges that Compass CEO Robert Reffkin contacted at least eight regional MLSs in October 2025 demanding rule changes that would terminate Zillow’s data access if the portal continued to enforce its Listing Access Standards. MRED adopted the demanded rules within weeks. Realtracs adopted parallel rule changes April 30, 2026. CLAW adopted mirroring rule changes May 6, 2026. Hive MLS received a demand letter from Compass May 11, 2026 with a May 20 enforcement deadline. The complaint also documents that on May 8, 2026, Compass terminated all direct listing feed agreements with Zillow nationwide on behalf of every Compass brokerage entity or subsidiary, and that on May 5 and 6, MRED and its data distributor MLS Grid sent Zillow emails flagging Compass listings in Florida, Georgia, and California that Zillow had blocked under its standards — demanding an explanation despite those listings being outside MRED’s traditional Chicagoland service area.

The pattern documented in the May 12 complaint is coordinated market restraint, not consumer-facing seller-choice advocacy. The investor-facing framework characterizes Compass as expanding seller options against legacy mandates. The federal court record characterizes the same operational pattern as coordinated rule-capture across four MLSs designed to compel third-party portal compliance under threat of feed termination. The investor-facing framework and the federal-court-record operational pattern address the same underlying conduct from incompatible directions. The Skillman Moment at federal scale names the moment at which audience separation between those two characterizations collapses.

Selective Transparency Rather Than Non-Transparency

The governing economic mechanism the previous three dimensions document is not transparency reduction. It is transparency redistribution. Compass is not removing listing information from public visibility. Compass is redistributing the timing, audience, and access architecture of listing visibility from a uniform-public-disclosure model to a tiered-selective-disclosure model the brokerage controls. Naming the mechanism resolves what otherwise appears as a collection of inconsistent positions across the Compass corpus.

Under the selective-transparency frame, the previously disparate components cohere into a single operational architecture. The Redfin partnership routes Coming Soon listings to 60 million Redfin monthly visitors before MLS submission. The MRED, Realtracs, CLAW, and Bright MLS partnerships compel listing display inside selected MLS environments while excluding portals that decline the identity-protective feed rules. Private Exclusives restrict pre-marketing to Compass agents and clients. Coming Soon listings expand the audience selectively across syndicated partners. The Three-Phased Marketing Strategy operates as a graduated audience-expansion architecture in which Compass — not the MLS, not the seller, not the portal — controls each phase transition.

The framework’s “seller choice” vocabulary is therefore not pretextual in the simple sense — and the analysis is sharper when this nuance is preserved. Sellers may genuinely desire selective marketing options: privacy during pre-marketing, control over price-discovery timing, ability to test demand without public days-on-market accumulation. The vocabulary names a real consumer preference the cooperative-MLS model does not fully accommodate. What the vocabulary obscures is not the existence of seller demand but the architecture governing implementation of that demand. Inside Compass’s operational pattern, the selection mechanism is not the seller; the selection mechanism is the platform-layer routing architecture Compass controls through MLS rule capture, agent network routing, and portal partnership selection. Visibility timing, visibility audience, and visibility access become strategic assets Compass administers on the seller’s nominal behalf. Transparency is no longer universal infrastructure produced by cooperative governance. Transparency becomes a negotiated commercial product distributed through Compass’s tiered partnership architecture, with the platform — not the seller — operating the negotiation.

The post-NAR-settlement regulatory environment treats this redistribution as antitrust-relevant conduct rather than consumer choice. SSB 6091’s concurrent-marketing requirement, the Zillow complaint’s Sherman Act group-boycott theory, and NWMLS Rule 2’s pre-marketing prohibition each operate under the structural assumption that visibility universality is the default and selective restriction requires affirmative justification. Compass’s operational pattern inverts that assumption: selective distribution is the default and universal visibility is one option among several in the tiered architecture. The legal-regime conflict is not between transparency and non-transparency. The conflict is between universal-default transparency (the inherited cooperative-MLS model) and selective-default transparency (the Compass tiered-distribution model). Naming the conflict at this altitude clarifies what every individual Skillman Moment specimen is illustrating: Compass’s framework is internally consistent with the selective-transparency architecture; the framework fails to export because external evidentiary records operate under the universal-default assumption the architecture is designed to displace.

The Financial Paradox

The May 5 earnings call also introduced a third dimension that intensifies rather than mitigates the framework collapse. Reffkin reported Q1 2026 revenue of $2.7 billion, a 99% year-over-year increase, with brokerage gross transaction value of $97.3 billion (85.7% year-over-year) and 99,504 brokerage transactions (102.6% year-over-year). The increases are attributed to the Anywhere Real Estate merger that closed January 9, 2026, adding the Coldwell Banker, Century 21, Sotheby’s International Realty, Corcoran, ERA, and Better Homes and Gardens brands to the Compass holding-company architecture. The combined entity reported approximately 340,000 agents across 35 markets and approximately 35% market share in Chicago — the precise market that is the operative locus of the MRED rule-capture campaign.

The seller-choice framework was developed in a market environment where Compass operated as a regional disruptor advocating for marketing flexibility against legacy MLS cooperative governance. The disruptor environment no longer exists. Compass operates as the dominant national brokerage incumbent, with the largest agent count in U.S. residential real estate, executing horizontal consolidation across legacy brokerage brands and securing rule-capture partnerships across MLSs covering several geographic regions. The choice-vocabulary framework, originally deployed against legacy incumbents on behalf of a smaller disruptor, is now deployed by the dominant incumbent against the remaining competitive infrastructure that constrains its private-listing distribution strategy.

The financial scale documented in the May 5 earnings call is the structural condition that makes the May 12 federal antitrust complaint legally tractable. The complaint’s Sherman Act group-boycott theory depends on documented market-power concentration sufficient to coerce third-party MLS rule changes against the rule-adopting institutions’ own commercial interests. Compass at $2.7 billion quarterly revenue, 340,000 agents, and 35% Chicago market share carries the documented market power. The framework cannot characterize this position as disruptor-against-incumbent advocacy without contradicting the operational record. The financial paradox is the dimension under which the framework’s legacy disruptor framing fails most decisively — the framework is being deployed by the entity it was originally framed against.

Institutional Exposure and the Collapse of Audience Separation

The three dimensions converge on a fourth, which operates at the securities-disclosure layer. When Reffkin stated on the May 5 earnings call that “MLS rules are just rules of a business; they’re private entities,” he was deploying an internal commercial defensive framing — designed to minimize the statutory authority of localized real estate infrastructure for investors who price Compass’s valuation against private-listing distribution capacity. The framing treats the MLS as a voluntary utility whose rules can be contested under the banner of seller choice. The framing is operationally severable from the underlying conduct only inside an investor-facing communication environment where audience separation holds.

The structural failure-to-export occurred exactly seven days later. The May 12 federal complaint documented that Compass does not treat MLS guidelines as private business rules. Compass weaponizes those same rules across four jurisdictions — MRED, Realtracs, CLAW, and Hive MLS — to enforce identity-protective restrictions designed to shield Compass’s Private Exclusives shadow inventory from public consumer portals. The seven-day window between the investor-facing framework statement and the federal-court documentation of operational contradiction is the documented audience-separation collapse interval.

The transition from investor-facing abstraction to court-documented anticompetitive enforcement transforms Reffkin’s earnings-call commentary into an evidentiary liability. By asserting that seller autonomy operates outside MLS cooperative governance, the C-suite narrative directly contradicts the operational mechanics surfaced in the federal complaint. In a federal antitrust framework, “seller choice” cannot operate as a shield justifying coordinated multi-MLS withholding of listing data from public-access portals.

The contradiction is not analytically reconcilable inside the regulatory environment of 2026. The post-NAR-settlement environment — following the March 2024 NAR settlement and the subsequent April 2024 Compass v. NAR / DOJ antitrust litigation cascade documented across The Compass / NWMLS Antitrust Landscape — operates under heightened evidentiary standards across multiple parallel forums. Federal antitrust enforcement, state consumer protection authority, securities-law disclosure standards, and state licensing statutes including SSB 6091 each surface conduct from the others’ records into their own adversarial-discovery environments. Audience separation under those conditions is a structural impossibility, not a communication preference. The May 5 / May 12 sequence documents the impossibility’s first federal-record specimen at the CEO altitude. The Skillman Moment at CEO scale is therefore not an isolated regional public-relations misstep. It is a systemic, corporate-wide operational dependency on separate audiences remaining permanently siloed — a structural impossibility that the post-NAR-settlement litigation environment converts into a documentary record at every federal-court appearance.

The Audience-Separation Collapse Interval as Named Diagnostic Category

The May 5 / May 12 sequence supplies the publication’s fourth original analytical concept — the audience-separation collapse interval — and operationalizes it as a measurable diagnostic category that institutional readers can apply to forecast Compass framework-export events. The interval is the elapsed time between two observable events: the framework-deployment event (T₀), at which Compass corporate communications deploy an investor-facing framework that depends on audience separation to maintain coherence; and the federal-court-documentation event (T₁), at which an adversarial federal-court filing documents operational conduct contradicting the deployed framework. The collapse interval is the measurable quantity T₁ − T₀, with the May 5 / May 12 sequence establishing the first documented specimen at CEO altitude with a seven-day measurement.

The category’s diagnostic value operates independently of the specific seven-day quantity. The interval’s value as a forecasting instrument is structural: any audience-separation collapse interval is measurable, comparable across specimens, and convergent toward zero as the post-NAR-settlement litigation environment accelerates cross-forum surfacing of operational records. Each successive Compass framework-export event will produce a measurable collapse interval. The cumulative record of those measurements supplies the empirical test of whether the audience-separation premise is sustainable under post-NAR-settlement conditions.

The audience-separation collapse interval connects directly to the Skillman Ceiling concept developed in The Skillman Moment as Analytical Rosetta Stone of the MindCast MLS Equilibrium Series, Part III of the MindCast MLS Equilibrium Series. The Skillman Ceiling identifies the boundary condition at which individual narrative-failure events transition into systemic narrative exhaustion — the point at which negative-expected-payoff conditions on framework export hold simultaneously across substantially all relevant regulatory environments, and additional commercial framings cannot restore positive expected payoff. The audience-separation collapse interval is the empirical measurement instrument that detects Skillman Ceiling proximity. As collapse intervals shorten across successive framework-export events, the cumulative record approaches the Ceiling boundary at the rate at which the cross-forum surfacing infrastructure accelerates.

Forecasting application: the Q2 2026 Compass earnings call (anticipated August 2026) and the Q3 2026 earnings call (November 2026) will produce additional framework-deployment events at CEO altitude. Each event carries a forecast collapse interval that the MindCast Simulation predicts will shorten relative to the May 5 / May 12 seven-day baseline as discovery in Compass v. NWMLS and Zillow v. MRED-Compass accelerates cross-forum documentation. If the August 2026 earnings-call framework-deployment event produces a collapse interval shorter than seven days, the prediction holds and Skillman Ceiling proximity tightens. If the collapse interval lengthens — i.e., no federal-court documentation surfaces operational contradiction within the corresponding window — the prediction is falsified and the audience-separation premise has acquired additional operational durability.

The Redfin / Rocket Realignment

The framework Reffkin deployed on the May 5 earnings call also operates against a partially restructured platform environment that the prior MindCast analysis of Compass-versus-portals conflict — see Compass v. NWMLS — The Counterclaim That Closed Compass’s Antitrust Thesis — no longer fully describes. On February 26, 2026, Rocket Companies, Compass International Holdings, and Redfin announced a three-year strategic alliance. Compass Coming Soon listings appeared on Redfin immediately. On March 18, 2026, Compass voluntarily dismissed its antitrust lawsuit against Zillow. Between February 26 and May 13, 2026, Compass secured MLS partnership rule changes at MRED, Realtracs, CLAW, and Bright MLS, while terminating direct listing feeds with Zillow nationwide effective May 8.

The pattern is not pure portal conflict. The pattern is selective platform realignment. Compass has migrated from a binary anti-portal litigation posture toward a negotiated selective-syndication architecture in which compatible platforms (Redfin via the Rocket alliance, the four MLSs that adopted identity-protective feed rules) carry Compass inventory under terms favorable to the selective-transparency model, while incompatible platforms (Zillow, NWMLS) are pushed outside the syndication architecture through litigation, MLS rule capture, and direct-feed termination. The framework is therefore not the contradiction it appears under a binary Compass-versus-portals reading. The framework is the public articulation of a platform-transition strategy in which Compass selects which platforms participate in the selective-transparency distribution layer and which do not. Under the selective-platform-realignment frame, the Zillow lawsuit dismissal and the simultaneous MRED-Realtracs-CLAW-Bright partnership expansion are not contradictory moves. They are coordinated components of the same migration architecture.

IV. The Cris Nelson Moment — Regional-Executive Specimen and Structural Silence

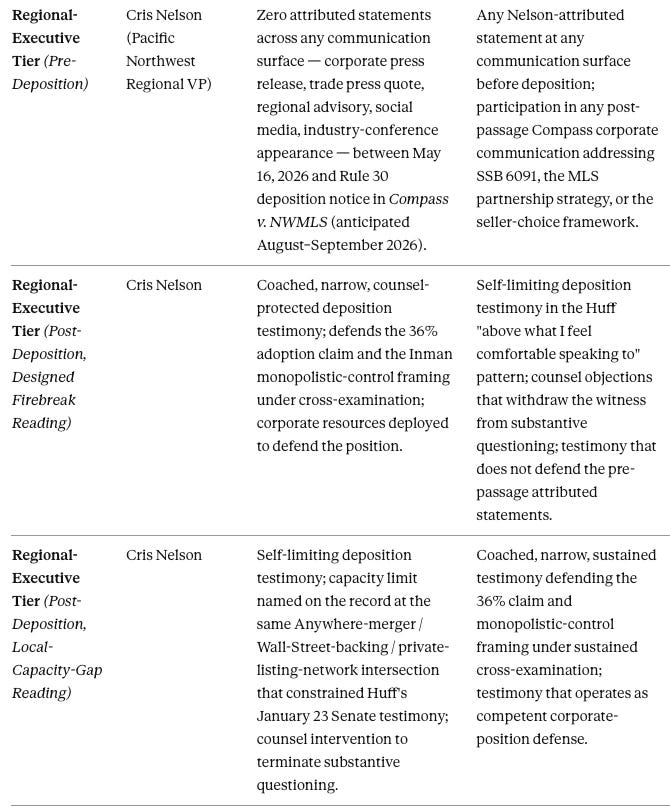

The Cris Nelson Moment is defined in the prior MindCast corpus — see The Cybernetics of Compass Holdings’ Narrative Control Architecture — as accountability and candor breakdown at the institutional level, the regional-executive specimen of the Compass detection taxonomy that operates parallel to the Skillman Moment at the broker level and the Huff Moment at the named-witness level. The current section documents the specimen as it appears in the post-SSB 6091 record at the May 16, 2026 horizon.

The Cris Nelson Moment must be constructed from structural absence at the intermediate altitude rather than from documentary presence — the Executive Summary explains why analysis focused solely on the named witness misses the more consequential institutional layer. The analytical work is therefore negative-space analysis: identifying the events where Nelson’s institutional position required engagement, and documenting the non-response. The accountability breakdown surfaces in the absence — not the presence — of regional-executive statements at convergence points where the regional tier carried operational responsibility.

Cris Nelson is Compass’s Pacific Northwest Regional Vice President, with documented operational exposure to the Pacific Northwest transaction record analyzed in The Compass-Anywhere Address Suppression Calculus and the Compass Washington legislative campaign analyzed in The Cybernetics of Compass Holdings’ Narrative Control Architecture. The accountability surface at this tier is direct: Pacific Northwest agent conduct, regional MLS-rule interpretation, and regional response to state-level transparency legislation each fall within the Regional VP’s documented institutional responsibility. Nelson’s post-SSB 6091 communication record across these surfaces is empty.

The Nelson Public Record — Trade Press Deployment vs. Legislative Silence

The Cris Nelson Moment specimen rests on a documented pre-passage public record that is substantially larger than the post-passage silence record. Nelson served as Compass’s corporate-designated regional spokesperson on Private Exclusives across every major real estate trade outlet during the April 2025 NWMLS-Compass conflict and the subsequent SSB 6091 legislative trajectory. The record establishes the baseline against which the post-passage silence is measured and against which the Olympia testimonial absence reads as deliberate cross-forum allocation rather than scheduling coincidence.

The trade press deployment record carries four documented Nelson statements across four outlets, each operating under different evidentiary standards than legislative testimony.

On NWMLS rule authority — the “monopolistic control” framing (Inman, April 25, 2025):

“This is a stark example of monopolistic control, with NWMLS having 100% market share of real estate agents, that limits homeowner choice, stifles competition and sets a dangerous precedent for broker accountability and market fairness.”

Source: Inman, April 25, 2025.

The Inman quote is the strongest single Nelson statement on the federal antitrust framing. The framing characterizes NWMLS rules as monopolistic control that limits homeowner choice. The May 12, 2026 Zillow complaint documented Compass deploying the inverse operational pattern — using MRED, Realtracs, CLAW, and Hive MLS rules to compel third-party portal display under threat of feed termination. The same regional executive who characterized cooperative MLS rules as monopolistic when they constrained Compass deployed no comparable framing when Compass corporate executed the rule-capture campaign that the May 12 complaint characterizes as a Sherman Act group boycott. The Inman quote operates as Nelson’s framework-level statement at the regional altitude — and the framework collapses under the same cross-forum-contradiction analysis Section III applies to Reffkin’s framework-level statement at the CEO altitude.

On consumer demand — the 36% adoption claim (Compass corporate press release, April 25, 2025):

“We’ve seen strong demand from Seattle homeowners for pre-marketing options. When given the choice, 36% of homeowners working with a Compass agent in Seattle chose to pre-market their home as a Compass Private Exclusive, which was done by NWMLS rules at the time.”

Source: Compass newsroom, April 25, 2025.

The Compass corporate press release attached Nelson’s name and Regional VP title to the litigation-announcing communication explicitly. The naming is itself a corporate-disclosure-level commitment: Compass corporate identified Nelson as the named regional spokesperson on the federal antitrust complaint at the moment Compass filed it. The April 25, 2025 named-attribution position established Nelson’s institutional role in the trade press cycle and made the subsequent legislative-testimony substitution structurally visible.

On homeowner choice — the “forced into one-size-fits-all” framing (RISMedia, April 17, 2025):

“Homeowners in Washington State are asking why they are the only ones in America without a choice in how they sell their homes... Compass agents in the area have seen firsthand how these restrictions hurt sellers. Unlike in other states, Washington homeowners are forced into a one-size-fits-all approach that can weaken their negotiating power and reduce their home’s value.”

Source: RISMedia, April 17, 2025.

On private exclusives as consumer innovation (parallel deployments at Real Estate News and HousingWire across April 2025): Nelson reproduced the seller-choice and homeowner-protection framing in companion statements to Real Estate News and HousingWire during the same April 2025 NWMLS-Compass conflict cycle. The trade press deployment was systematic across the four major real estate industry publications — Inman, RISMedia, Real Estate News, HousingWire — and operated as a coordinated regional-executive communication campaign.

The four-outlet deployment record is analytically dispositive of one question: Nelson’s silence post-passage cannot be explained by absence of communication capacity. The regional-executive tier demonstrated extensive communication capacity across the April 2025 cycle, deploying framework-level statements on monopolistic control, consumer demand, homeowner choice, and private-exclusives innovation across the entire real estate industry trade press. The same tier produced zero attributed statements in the four months following the SSB 6091 signing. The capacity is documented; the silence is documented; the gap between them is the operative analytical surface.

The cross-forum deployment pattern carries one additional documented feature. Nelson’s statements to Inman, RISMedia, Real Estate News, and HousingWire were made in forums where statements cannot be used as party admissions at the October 2026 NWMLS trial under standard Federal Rules of Evidence applications. Trade press quotations carry hearsay status and require independent admissibility analysis. Legislative testimony, by contrast, enters the official record of a state legislative proceeding and operates as direct evidence under FRE 803(8) for public-records purposes. The same factual representations Nelson made to four trade outlets in April 2025 — monopolistic control, consumer demand, homeowner choice — were never made under legislative-hearing conditions in January 2026. The cross-forum allocation is precise: maximum statement volume in non-discoverable forums; zero statement volume in the discoverable forum that operated during the same legislative cycle.

The Skillman social-media post from January 28, 2026 supplies the documentary anchor that places Nelson physically in the room at the House Consumer Protection Committee hearing. Skillman posted a photo captioned in part “EXTRAORDINARY leadership team pushing against extremely strong headwinds,” tagging Nelson and Huff. The post operates as a third-party-attested documentary record of Nelson’s hearing-room presence on January 28 — independent of any Compass corporate disclosure or legislative sign-in record. The Olympia footprint is therefore established at three documentary altitudes: the legislative sign-in record (Nelson signed in CON); the Skillman social-media post (Nelson in the room with the Huff testimonial team); and the absence from the official testimonial record (Nelson did not testify). Three documentary anchors, one structural pattern: presence without testimony.

The Specimen — Structural Silence at the Skillman Convergence Point

The operative Cris Nelson Moment specimen is the structural non-response at the regional level when Moya Skillman — a Compass broker on Team Foster, operating in the Pacific Northwest geography Nelson supervises as Regional VP — produced a category-error public-record specimen on March 16, 2026, the day Governor Ferguson signed SSB 6091 into law.

The convergence point is precise. The Skillman PSBJ quote — applying Reffkin’s MLS-targeted seller-choice framing to a state licensing statute — produced a documented public-record error attached to an agent in Nelson’s regional jurisdiction. The standard institutional response under any reasonable theory of the Compass operating model would be regional-executive engagement: a corrective statement to walk back the category error before it propagated; a regional advisory clarifying the correct framing for Pacific Northwest agents operating under the new statute; a public position from the Regional VP either supporting the agent’s framing under cross-examination conditions or correcting it under the same conditions. Three response surfaces, each operationally available to the Regional VP, each carrying institutional precedent at Compass and at peer brokerages.

Nelson’s response was silence across all three surfaces. No corrective statement. No regional advisory in the public record. No Regional VP position taken on the Skillman framing in the seven weeks between the March 16 signing and the May 5 Q1 earnings call. The category error propagated upward through the Compass communications stack without regional-executive interruption — first to the corporate-spokesperson layer in the post-passage press releases, then to the CEO layer at the May 5 earnings call, where Reffkin reproduced the same category error in the framework formulation Section V documents in detail.

The accountability breakdown is documented in the propagation pathway. Compass’s operating model assigns the regional-executive tier responsibility for correcting broker-level public-record errors within the regional jurisdiction. Nelson did not exercise that responsibility. The framework-collapse specimen the May 12 Zillow complaint converted into federal evidentiary record was the same category error the regional-executive tier had failed to interrupt at the broker layer seven weeks earlier. The Cris Nelson Moment is the structural absence at the intermediate altitude that allowed the category error to propagate from broker to CEO without regional-executive interruption.

The Convergence Documentation

The Cris Nelson Moment specimen is supported by four convergence points in the pre- and post-passage record where Nelson’s attributed statements met the post-passage operational and evidentiary record. Each pairs a documented Nelson trade-press quote with the post-passage record element that contradicts or inverts the quote. At each pairing, the regional-executive tier produced no engagement.

The 36% adoption claim decay. Nelson’s April 25, 2025 corporate-press-release quote positioned Private Exclusives as a consumer-demand product producing 36% adoption among Compass-represented Seattle homeowners. The Paragraph 43 concession in Compass v. NWMLS — Compass’s own counterclaim filing admitting that the Private Phases of its Three-Phased Marketing Strategy will violate Washington state law when SSB 6091 takes effect on June 11, 2026 — directly contradicts the consumer-demand framing. If the architecture were producing consumer-driven adoption at 36%, the post-June 11 transition would surface that demand redirecting through the SSB 6091-compliant pathway; the operational pattern instead is documented circumvention through MLS rule-capture and selective-syndication restructuring.

The “one-size-fits-all” inversion. Nelson’s RISMedia quote framed Washington homeowners as “forced into a one-size-fits-all approach that can weaken their negotiating power” — positioning SSB 6091 as regulatory restriction against homeowner choice. The April–May 2026 federal-court record documented Compass restricting third-party portal display through coordinated MLS rule changes across MRED, Realtracs, CLAW, and Hive MLS — the operational pattern the May 12 Zillow complaint characterizes as an attempt to compel uniform identity-protective display behavior across the national MLS landscape. The “one-size-fits-all” complaint Nelson directed at SSB 6091 applies operationally to Compass’s own conduct documented seven days later.

The monopolistic-control framing collision. Nelson’s Inman quote characterized NWMLS rules as “a stark example of monopolistic control” that “limits homeowner choice, stifles competition and sets a dangerous precedent for broker accountability and market fairness.” The May 12 Zillow complaint documented Compass executing the operationally equivalent pattern at federal scale — coordinated rule-capture across four MLSs, identity-protective feed rules designed to compel third-party portal compliance, the same MLS-rule-as-enforcement-weapon mechanism Nelson named as monopolistic control when deployed against Compass. The convergence is therefore not a contradiction between the Nelson framework and Compass conduct; it is identical conduct framed as illegitimate when others execute it and legitimate when Compass executes it.

The Olympia testimonial absence. Nelson accompanied Brandi Huff to both the January 23 and January 28, 2026 Washington legislative hearings. Nelson signed in CON at both hearings. Nelson did not testify at either. The Olympia footprint predates the Skillman convergence by approximately seven weeks and establishes the pattern repeated across every subsequent convergence point.

Across all four convergence points, the regional-executive tier did not engage. The accountability-and-candor breakdown is not a single-event specimen; it is a recurring structural feature of the regional-executive tier’s response architecture across the entire SSB 6091 cycle from January 2026 through the May 16 publication horizon.

The Explanatory Mechanism — Local-Leadership Capacity Versus Designed Firebreak

The Cris Nelson Moment specimen documented above admits two competing explanatory mechanisms. The publication presents both because the falsifiable test distinguishing them carries direct forecasting weight for jurisdictions advancing SSB 6091 analogues.

The first mechanism is the designed firebreak reading. Under this reading, Compass corporate strategically maintains the regional-executive tier in structural silence to insulate enterprise-level deniability about regional jurisdictional reality. The Nelson silence is deliberate architecture — chosen at the corporate level to prevent Washington-specific statutory constraints from contaminating Reffkin’s national investor narrative. The architecture is portable: Compass will replicate the designed-firebreak structure in every SSB 6091-analogue jurisdiction by silencing the relevant regional-VP tier and routing all public communication through the CEO layer.

The second mechanism is the local-leadership-capacity-gap reading. Under this reading, Compass corporate has been forced to centralize at national altitude because the local regional-executive tier in Washington lacks the institutional capacity to defend the position under post-passage adversarial conditions. The Olympia testimonial substitution — Huff testifying, Nelson silent — was not designed buffer architecture; it was emergency operational workaround that revealed the regional-VP layer could not credibly carry the testimonial exposure. The post-passage silence is not strategic deniability; it is the documented limit of regional-leadership capacity to engage post-passage convergence points. The national-leadership centering at the May 5 earnings call, the spokesperson template, and the LinkedIn responses is forced consolidation — Compass has worked around the regional-leadership-capacity gap by centralizing communication authority at the only tier that can carry the position. The architecture is local-leadership-specific: Compass will need to assess regional-leadership capacity in each new jurisdiction and centralize earlier where the local tier cannot carry the post-passage adversarial environment.

The two readings produce divergent forecasting outputs for Illinois, Connecticut, Hawaii, and other states advancing SSB 6091-analogue legislation. The designed-firebreak reading predicts portable replication: every new jurisdiction will exhibit the same regional-executive silence pattern Compass executed in Washington. The local-leadership-capacity-gap reading predicts variable centralization: jurisdictions with stronger Compass regional leadership will produce some regional-executive engagement; jurisdictions with weaker regional leadership will replicate the Washington pattern of immediate centralization at the CEO tier. The divergence is testable across the 2026–2028 legislative cycle as analogue statutes advance through additional state legislatures. The state-by-state regional-leadership-capacity forecasting will be developed in a separate MindCast publication in the Prediction Markets Rule Architecture Series.

The operational implication for the current publication is that the two readings are not analytically equivalent on the post-NAR-settlement litigation environment thesis developed in Sections III and X. The designed-firebreak reading characterizes Compass as executing a sophisticated multi-tier communications architecture under deliberate corporate strategy. The local-leadership-capacity-gap reading characterizes Compass as executing a forced national centralization in response to documented regional-leadership inability to carry the post-passage adversarial environment. Forced national centralization is typically more visible to antitrust enforcement than deliberate multi-tier fragmentation, because forced centralization removes the local-distribution cover that complicates Section 1 conspiracy theories. The local-leadership-capacity-gap reading therefore strengthens the platform-transition thesis: the centralization that Compass is executing at national altitude is not optional positioning; it is the only available execution layer once the regional tier has demonstrated incapacity. The endgame architecture documented in Section X operates with greater antitrust visibility under the local-flailing reading than under the firebreak reading, and the regulatory-compression risk identified in Section X accelerates accordingly.

Supporting Evidentiary Record — The Olympia Footprint and the Post-Passage Communication Vacuum

The Olympia legislative trajectory establishes the Cris Nelson Moment specimen’s pre-passage baseline. Nelson accompanied Brandi Huff, Compass’s Managing Director for WA / ID / WY, to both the January 23, 2026 Senate Housing Committee hearing and the January 28, 2026 House Consumer Protection Committee hearing. The personnel substitution at Olympia carries specific analytical weight: Huff is not a line broker but the Managing Director with three-state operational oversight — the highest documented Compass tier below the Pacific Northwest Regional VP. The substitution Compass executed at Olympia was therefore Managing Director for Regional VP, not broker for Regional VP. The two-layer structure indicates that Compass distinguishes between operational-executive accountability (Managing Director, exposed to testimonial record) and strategic-executive accountability (Regional VP, preserved as the unexposed regional layer). The Skillman-Huff-Nelson stratification is a three-tier division across the Compass Pacific Northwest organization, with each tier carrying a calibrated exposure profile.

The Huff testimonial record itself supplies the strongest single piece of evidence for the local-leadership-capacity-gap reading developed above. At the January 23 Senate Housing Committee hearing, Senator Alvarado posed the question at 44:41 connecting the Compass-Anywhere merger and Wall Street backing to the exclusive-network architecture SSB 6091 was designed to address. Huff initially deflected, claiming the model “would not be affected” with the proposed amendments. Chair Bateman pressed the follow-up: “But without the amendments?” Huff’s response acknowledged the limit of her testimonial capacity directly:

“That is probably above what I feel comfortable speaking to.”

The Huff admission carries specific analytical weight as documentary evidence for the local-leadership-capacity-gap reading. The question Senator Alvarado posed — the Anywhere merger / Wall Street backing intersection with the exclusive-network architecture — is the precise question the Regional VP tier was structurally positioned to address. Nelson was present in the room and did not testify. Huff acknowledged on the official Senate Housing Committee record that the question was above her testimonial capacity, and the Compass corporate apparatus produced no backstop coverage at the Regional VP tier to supply the answer Huff acknowledged she could not provide. The exchange is the documented exposure of the entire regional-leadership-tier limit — not just the Managing Director’s — because the capacity limit was named, on the record, in real time, by the Compass witness carrying the testimonial substitution.

Both explanatory readings accommodate the exchange. Under designed-firebreak, Nelson’s silence preserves enterprise-level deniability about the Anywhere / Wall Street intersection because the answer would create unfavorable evidentiary record. Under local-leadership-capacity-gap, Nelson’s silence reflects the Regional VP’s own institutional inability to defend the model under cross-examination; Compass corporate allowed the Huff admission to absorb the exposure rather than escalating to Nelson. The Huff admission is direct documentary evidence that the regional-leadership tier had a known capacity limit on precisely the question that mattered most to the legislative record.

The post-passage Compass communications record measures the silence at the Nelson tier directly. The three Compass corporate press releases issued from the SSB 6091 signing (March 19, 2026) through May 5, 2026 are “Compass to Dismiss Lawsuit Following Zillow Ban Reversal” (March 18, 2026), “Compass Named Top U.S. Brokerage for the Fifth Consecutive Year” (April 10, 2026), and “Compass, Inc. Reports First Quarter 2026 Results” (May 5, 2026). None names Cris Nelson. None carries a Nelson-attributed quote. None addresses SSB 6091 in operative content. The communication volume at the Pacific Northwest Regional VP tier moved from the documented April 2025 four-outlet trade press deployment record — the Inman monopolistic-control quote, the Compass corporate press release deploying the 36% adoption claim, the RISMedia “one-size-fits-all” framing, and the parallel Real Estate News and HousingWire statements — to total silence beginning the day Ferguson signed the bill into law. The May 12-13 Zillow complaint response cycle confirmed the silence: corporate-spokesperson statement issued anonymously, CEO LinkedIn response issued personally by Reffkin, no regional-executive appearance at any communication surface.

The architecture’s response template to MindCast publications naming Cris Nelson Moment specimens — across The Cybernetics of Compass Holdings’ Narrative Control Architecture, The Law and Behavioral Economics of Compass v. NWMLS, and the prior publications in the Compass Law and Behavioral Economics Series — is the same template. No response from Nelson has followed any MindCast publication naming the testimonial absence at Olympia, the 36% claim decay, the one-size-fits-all inversion, or the Skillman convergence non-response. The silence is consistent across pre-passage and post-passage horizons, across each named convergence point, and across each MindCast publication that names the category. The structural silence is itself the operative Cris Nelson Moment specimen.

V. The CEO-Scale Specimen — May 5, 2026

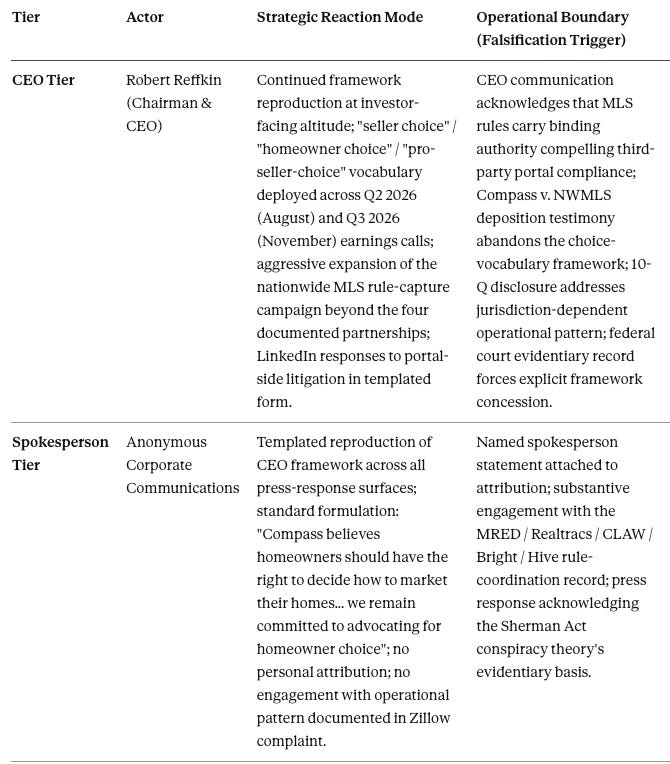

The Q1 2026 earnings call occurred on May 5, 2026 — the first investor communication after the SSB 6091 signing (March 19, 2026) and the closing of the Compass-Anywhere merger (January 9, 2026). The call carried the highest documented Compass communication altitude post-SSB 6091. Reffkin used the call to reiterate the seller-choice framing in three distinct framework-level formulations.

The first formulation: “Didn’t the seller deserve that five years ago and 10 years ago? Why didn’t they have it? Shouldn’t sellers have more choices, not less choices? We’re pushing on the system so that sellers and agents have more choices, less mandates.”

The second formulation: “The seller should be the only person who decides how they market their home in the context of the law, and fiduciary duty and statutory duty. MLS rules are just rules of a business; they’re private entities.”

The third formulation, delivered in connection with the announced national MLS partnership strategy: “I want to create a national MLS to compete against local MLSs. We are bringing MRED national, as well as it will be just a select number of MLSs that are pro-seller choice, where we’re going to give them all of our listings, where we’re going to subsidize our agents joining.”

The three formulations together reproduce the Skillman Moment at framework level rather than illustration level. The first formulation deploys seller-choice framing against unspecified “mandates” — operationally extensible to MLS rules, state licensing law, federal antitrust requirements, or any other constraint. The second formulation characterizes MLS rules as merely “private entities” whose authority is subordinate to seller choice, fiduciary duty, and statutory duty. The third formulation describes a national MLS network in which Compass selects which MLSs are “pro-seller choice” and subsidizes agent participation accordingly.

The Internal Contradiction the Framework Exposes

The Reffkin framework deploys two operationally inconsistent claims about MLS rule authority within a single communication.

The first claim: MLS rules are private business rules that should not bind sellers because they are merely the rules of private entities subordinate to seller choice. The claim operates as the load-bearing argument in Compass’s federal antitrust litigation against NWMLS Rule 2, documented in Compass v. NWMLS — The Counterclaim That Closed Compass’s Antitrust Thesis.

The second claim: Compass is building a national MLS network composed of “pro-seller choice” MLSs that will adopt rules favorable to Compass’s private-listing distribution strategy. The rules these MLSs adopt are documented in the May 12 Zillow complaint as identity-protective feed rules that override portal display policies — i.e., rules that compel third parties to display Compass listings under threat of feed termination.

The framework cannot accommodate both claims simultaneously without collapse. If MLS rules are merely private-entity rules subordinate to seller choice, then the rules adopted by MRED, Realtracs, CLAW, and Bright MLS at Compass’s direction are equally subordinate to seller choice — meaning portals like Zillow retain the same authority to disregard them that Compass claims sellers retain to disregard NWMLS rules. If, conversely, MLS rules carry binding authority that compels portal display under threat of feed termination, then NWMLS Rule 2 carries equivalent binding authority that compels Compass listing submission. The two claims cannot coexist except by treating MLS rule authority as a function of which party benefits from the rule.

The framework dispute meets the definition of the Skillman Moment at framework level. The framing functions inside the Compass commercial environment, where the audience is investors evaluating a private-listing distribution strategy and the optimization function is enterprise growth narrative. The framing fails to export to the federal antitrust environment, where the same MLS rules are documented as the load-bearing mechanism of a coordinated national campaign that the complaint characterizes as a Sherman Act group boycott.

The Spokesperson Template

The Compass corporate communications operation deployed a templated response to the May 12 Zillow complaint that reproduces the Reffkin framework at spokesperson altitude. The Compass spokesperson statement: “Compass believes homeowners should have the right to decide how to market their homes. The industry is evolving to give consumers more choice and we support that progress. We remain committed to advocating for homeowner choice and an open, competitive marketplace.”