MCAI Lex Vision: Compass v. NWMLS — The Counterclaim That Closed Compass's Antitrust Thesis

How Four Causes of Action, One Statutory Paragraph, and the Phrase "Negative Insights" Collapsed Compass's Litigation Thesis, Investor Narrative, and Public Credibility Simultaneously

Related publication: The Law and Behavioral Economics of Compass vs. NWMLS | Visual Synthesis: The Antitrust Litigation Trap Compass Built for Itself

Executive Summary

NWMLS’s counterclaim did not answer Compass’s lawsuit — it removed the structure that made the lawsuit viable.

Compass entered the Northwest Multiple Listing Service (NWMLS)federal antitrust proceeding carrying one strategic asset above all others: the ability to frame the dispute as a private governance conflict between a member brokerage and a regional cooperative. Keep the conflict bilateral, keep the legal theory contained to Sherman Act doctrine, and manage the public narrative through the seller-choice vocabulary Compass’s communications infrastructure had been deploying since April 2025. The MindCast AI Proprietary Cognitive Digital Twin (CDT) Foresight Simulation (MindCast Simulation) — developed across the The Law and Behavioral Economics of Compass vs. NWMLS — Procedural Survival Is Not Substantive Victory analysis — assigned P50–P70 probability to NWMLS prevailing or settling on terms preserving mandatory-sharing architecture. The April 2 counterclaim moved that distribution decisively toward the high end.

NWMLS’s Answer, Affirmative Defenses, and Counterclaim — Document 88, Case No. 2:25-cv-00766-JNW — filed four causes of action: Declaratory Judgment, Washington Consumer Protection Act (CPA), Fraudulent Misrepresentation, and Tortious Interference with Contract. Each claim rests on a different structural foundation. None requires Compass to win on antitrust grounds to proceed. All four compound simultaneously against a balance sheet carrying $2.6 billion in post-merger debt and a firm that has never posted a full-year GAAP profit.

The counterclaim’s deeper function is a frame inversion. Compass framed the case as a question of competition — whether MLS rules suppress innovation. NWMLS reframes it as a question of truth — whether Compass’s model suppresses information. Relocating the dispute from competitive restriction to information suppression changes the burden of proof, changes how courts resolve the dispute, and realigns how every other audience — regulators, platforms, investors, brokers, and consumers — interprets the same set of facts. Once framed as information suppression, Compass is no longer defending innovation. Compass is defending selective visibility.

The phrase “negative insights” — Compass’s own internal label for the days-on-market and pricing history data it stripped from NWMLS listings before public submission — is the evidentiary proof of that reframe. No deposition produced it. No discovery motion compelled its disclosure. Compass’s own marketing materials supplied the terminology, and the counterclaim filed it in federal court on April 2, 2026.

Paragraph 43 — the most consequential sentence in the filing — establishes that Compass knows the Private Phases of its Three-Phased Marketing Strategy (3PM) will violate Washington state law when Substitute Senate Bill (SSB) 6091 takes effect on June 11, 2026. Converting Compass’s attack on NWMLS Rule 2 from an antitrust challenge against private cooperative governance into an effective challenge against a statute the Washington legislature endorsed 141–1 produces three structural consequences. Injunctive relief becomes structurally unavailable — federal courts do not issue orders compelling parties to violate state law without a constitutional preemption basis Compass has not articulated. The damages predicate narrows — absent a countervailing judicial finding, Compass cannot recover antitrust damages for enforcement of a standard state law simultaneously requires after June 11. And the jury pool question becomes structural: the trial occurs in the Western District of Washington, drawn from the same state whose elected representatives voted 141–1 to mandate exactly what Compass is suing NWMLS for enforcing.

Four audiences — investors, potential partners, broker recruits, and the general public — now possess a closed evidentiary record operating independent of any single publication or proceeding. The counterclaim did not create new exposure. Filed April 2, 2026, it filed the receipt for exposure Compass generated across two federal courts, a state legislature, and its own marketing materials since April 2025.

The Compass collapse is not externally imposed. Self-inflicted causation runs through Compass, not merely against it.

“NWMLS does not need to out-argue Compass. It needs to let Compass prove its own case — and fail doing it. Compass built the trap. The counterclaim closed it.”

— MindCast, The Law and Behavioral Economics of Compass vs. NWMLS

I. What the Counterclaim Actually Does

A counterclaim with four causes of action converts a cost-imposition proceeding into a bilateral damages structure — and the Washington CPA’s mandatory treble damages and fee-shifting provisions convert that structure into a quantifiable financial threat. The asymmetric stakes mechanism Compass deployed as offense has been seized and turned.

Reading the NWMLS counterclaim purely as a litigation document produces an accurate but incomplete assessment. The claim theories are sound. The fraud counterclaim’s evidentiary anchors — Compass’s own marketing materials, the CEO’s public statements, the documented offer to cover broker sanctions for rule violations — are all self-generated and pre-discovery. The tortious interference theory flips Compass’s own cause of action back against the entity that induced the rule violations. Those are the surface mechanics. The financial instrument underneath them is addressed below.

The deeper function is architectural. Compass structured its April 2025 complaint as a cost-imposition vehicle: deploy elite antitrust counsel to exhaust a regional cooperative without the resources for decade-long federal defense, preserve the pre-MLS marketing window during the proceeding, and manage the public narrative through seller-choice vocabulary. As documented in Death by a Thousand Depositions — A Pre-Foresight Simulation of Compass’s Multi-Vector Regulatory Collapse, the eight-vector collapse framework identified the bilateral damages conversion as the structural mechanism that inverts Compass’s cost-imposition architecture.

The counterclaim dismantles that architecture on two fronts simultaneously. NWMLS now holds affirmative damages claims with fee-shifting potential under the CPA — meaning the entity that was supposed to bleed financially now faces bilateral damages exposure six months from trial. The SSB 6091 codification paragraphs, filed before discovery has produced a single document, lock the governing legislative record into the pleadings before Compass can manage around it. The financial attrition strategy inverted. The narrative containment strategy is now inside the record it was designed to control.

The specific financial instrument driving that inversion deserves explicit treatment. Under Washington’s Consumer Protection Act, RCW 19.86.090, a prevailing plaintiff recovers actual damages — and the court shall treble those damages up to $25,000 per violation. Reasonable attorneys’ fees and costs are mandatory, not discretionary. NWMLS is not merely defending against Compass’s complaint. NWMLS is pursuing affirmative damages that the statute requires to be multiplied, in a proceeding where Compass’s own marketing materials, CEO’s public statements, and documented internal conduct supply the evidentiary foundation without a single deposition. Compass entered the litigation expecting to impose cost on a membership cooperative. The Washington CPA converted that calculus: every dollar of NWMLS’s recoverable damages is a dollar subject to statutory multiplication, and every dollar of NWMLS’s attorneys’ fees is a dollar Compass must cover if NWMLS prevails. A firm carrying $2.6 billion in post-merger debt, with no full-year GAAP profit in its history, facing treble damages and mandatory fee-shifting on a CPA claim anchored in its own internal marketing language — is not imposing cost. It is absorbing it. The cost-imposition weapon did not misfire. It was seized and turned.

The Nash-Stigler coalition collapse The Compass Antitrust Self-Destruction Sequence — How Aggressive Federal Litigation Birthed the Legislation That Destroyed the Business Model documented explains why the structural inversion was predictable from the moment Compass filed. The Nash-Stigler framework — developed in The Nash–Stigler Dual Equilibrium Architecture — identifies two sequential thresholds: Nash equilibrium marks the point at which no actor in a coalition can improve their position by unilateral defection, locking coordinated behavior without requiring explicit coordination; Stigler equilibrium marks the point at which the evidentiary record is sufficient to drive settlement without additional proof. Compass’s federal complaints triggered both simultaneously by collapsing a fragmented equilibrium — NWMLS, Windermere, Zillow, and Washington Realtors with partially overlapping but not perfectly aligned interests — into a unified coalition with a single dominant strategy: eliminate the conduct legislatively rather than litigate it bilaterally. Each actor independently reached the same cost-benefit conclusion: legislative preemption is cheaper, faster, and more durable than antitrust defense. A floor vote is not a federal courthouse. The standard of proof is a committee hearing. The remedy is permanent and self-executing. NWMLS did not need to outspend Compass’s antitrust budget. It needed one legislative session. Compass provided the brief — and the counterclaim now files the legislative record back into the judicial proceeding as the procompetitive justification predicate.

The “Negative Insights” Paragraph

Paragraph 23 of the counterclaim quotes Compass’s own internal marketing materials: the firm promised listing brokers participating in 3PM that they could list properties “without accumulating days on market and price drop history.” Compass internally labeled that suppressed information “negative insights” — material facts a buyer needed before making an offer, systematically stripped from NWMLS listings after the Private Phase concluded.

No deposition produced that phrase. No discovery motion compelled its disclosure. Compass’s own marketing materials documented the conduct, used that specific terminology, and positioned the suppression as a seller benefit. NWMLS’s CPA counterclaim deploys the phrase as the deceptive practice predicate: Compass submitted inaccurate data to NWMLS, those inaccuracies deceived buyers and the 30,000+ broker members who relied on NWMLS data, and the platform value NWMLS depends on was measurably degraded. As The Cybernetics of Compass Holdings’ Narrative Control Architecture — Inventory Restriction, Commission Capture, and the Collapse of Audience Separationestablished through the Self-Disclosure Trap pattern, Compass’s most damaging evidence is self-generated.

Requiring no legal translation, the “negative insights” phrase lands with immediate clarity for any buyer who has purchased a home. Litigation value and public record value are one and the same.

“Compass’s most damaging evidence is self-generated. The Disclosure Form, the CEO’s public statements, the federal antitrust complaint, and the internal marketing materials make mutually exclusive factual claims about the same business practice. The exposure under Unfair and Deceptive Acts and Practices (UDAP) statutes requires no investigation — only compilation.”

— The Cybernetics of Compass Holdings’ Narrative Control Architecture

Paragraph 43 and the Statutory Trap Door

Compass’s greatest fear upon reading the counterclaim is not its most obvious claim. Paragraph 43 reads: “Compass knows that when the Public Marketing Law takes effect on June 11, 2026, the Private Phases and related practices will violate state law.”

Compass’s entire antitrust complaint rests on a single predicate: NWMLS Rule 2 is an anticompetitive restraint that unlawfully restricts how Compass markets properties before MLS submission. Strip that predicate and every cause of action is structurally exposed. Every Sherman Act count, every CPA claim, every tortious interference theory depends on characterizing Rule 2 as an unjustifiable private governance restriction on competitive conduct.

Paragraph 43 structurally undermines that predicate. After June 11, 2026, Compass’s Private Phases do not merely violate NWMLS’s contractual rules — Washington RCW 18.86 as amended by SSB 6091 makes them unlawful.

NWMLS Rule 2 is no longer, on this record, a contestable private cooperative governance mechanism evaluated under the rule of reason — the legal standard requiring a plaintiff to demonstrate that challenged conduct harms competition across the full market, not merely harms a single competitor, before courts will intervene. Enforcing concurrent marketing requirements is anticipatory statutory compliance — compliance with a law NWMLS had no role in drafting, emerging entirely from Compass’s own litigation generating the definitional framework the Washington legislature applied.

As The Compass Antitrust Self-Destruction Sequence — How Aggressive Federal Litigation Birthed the Legislation That Destroyed the Business Modelestablished: Compass’s elite antitrust counsel drafted, with billable precision, the operative definitions of “public marketing,” “pre-marketing,” and “selective exposure” that SSB 6091 codified. Washington’s drafters did not need to invent a regulatory framework. Compass filed one in federal court, and the Legislature applied it 141–1.

The Parker v. Brown state action immunity doctrine is structurally available to NWMLS in its most powerful form. Parker v. Brown — 317 U.S. 341 (1943) — holds that private actors enforcing standards mandated by state law cannot be held liable under federal antitrust law for conduct the state itself requires. A court applying that doctrine — absent a federal preemption argument Compass has not yet articulated — would find that NWMLS enforcing concurrent marketing requirements after June 11, 2026 is mandatory compliance with state law, not a private anticompetitive restraint. Every complaint paragraph characterizing Rule 2 as anticompetitive becomes, conditional on that finding, a characterization of the statute Rule 2 anticipates. The statute carries a 141–1 bicameral record that a Western District of Washington jury will encounter before it weighs Compass’s antitrust theory.

Two structural consequences follow, each conditional on the statutory alignment holding at summary judgment. First, the injunctive relief theory becomes structurally unavailable — absent a constitutional preemption basis Compass has not articulated, federal courts do not issue orders compelling parties to violate state law. Second, the damages window narrows materially: Compass’s ability to recover antitrust damages for enforcement of a standard that state law simultaneously requires after June 11 is, at minimum, severely constrained and at most foreclosed.

II. Impact on Compass’s Antitrust Lawsuit

The Zillow preliminary injunction denial established what Compass’s theory looks like under adversarial evidentiary testing. The counterclaim ensures the October 2026 NWMLS trial applies that record with greater precision and broader scope.

Judge Vargas’s February 6, 2026 Southern District of New York (SDNY)opinion produced five durable structural consequences for the NWMLS proceeding before NWMLS filed a single counterclaim paragraph. As documented in The Compass–Zillow Antitrust Litigation Arc Is Closed. Here Is What the Record Shows, Reffkin’s sworn testimony — the 94% MLS terminal rate, the Black Box design rationale, the Coming Soon data suppression concession — is permanent federal record available to NWMLS trial counsel under Federal Rules of Evidence (FRE) 801(d)(2) as party admissions.

The mandatory injunction classification established that Compass was not defending a right it possessed but demanding a structural accommodation that never existed. The self-inflicted injury characterization anchored the antitrust standing analysis against Compass. The 44% adoption decline — 3PM falling from 39% to 22% of sellers following Zillow’s Listing Access Standards (LAS) announcement — documented that the model’s commercial value was always conditional on full-channel distribution. And zero judicial relief across 268 days eliminated the preliminary injunction option in NWMLS before Compass could attempt it.

The counterclaim adds four compounding mechanisms to that foundation.

The Cross-Forum Market Definition Lock

Compass argued national market in the Zillow proceeding — online home search platforms operate nationally, national pricing, national policy implementation. Compass argues Seattle and King County in NWMLS. Both cases involve the same 3PM strategy, the same conduct, and the same product. As The Law and Behavioral Economics of Compass vs. NWMLS — Procedural Survival Is Not Substantive Victory analysis established in Section VI, Dr. Aron’s national market testimony from the SDNY preliminary injunction hearing sits in the federal record available by subpoena. NWMLS trial counsel can place that testimony directly alongside Compass’s Seattle/King County allegations. Judicial estoppel is available as a motion. The credibility attack is available regardless. A plaintiff whose market definition shifts between forums based on tactical advantage has defined markets for litigation purposes, not economic purposes.

The Free-Rider Kill Condition at Summary Judgment

The free-rider argument is NWMLS’s strongest weapon at summary judgment — and Reffkin’s sworn Zillow testimony establishes its evidentiary foundation without NWMLS lifting a subpoena. Free-riding in antitrust terms means extracting value from a shared infrastructure while withholding the contribution that infrastructure depends on — here, pulling price discovery data from the MLS commons while refusing to list into it during Phase 1. Phase 1 withholds listing inventory from NWMLS while Compass simultaneously pulls Internet Data Exchange (IDX) data from compliant brokerages to populate its own platform. Price discovery in Phase 1 derives its value from the broader MLS price signal. Compass extracts that signal while refusing to contribute to it during the phase when extraction generates dual-commission capture advantage. As The Law and Behavioral Economics of Compass vs. NWMLS — Procedural Survival Is Not Substantive Victory NWMLS Litigation Playbook established in Section XII.IV: the mechanism is precise, Reffkin’s testimony establishes it, Compass’s IDX data consumption establishes the extraction, and Compass cannot produce market-wide consumer welfare evidence at scale. That combination is the summary judgment kill condition.

The CPA counterclaim runs on a parallel track: degradation of NWMLS platform value through inaccurate listing data does not require resolving the antitrust question. Showing that buyers relied on NWMLS data Compass made misleading is sufficient.

The Three-Attack Convergence

Three structural vulnerabilities compound simultaneously at summary judgment. Presenting them together, rather than sequentially, denies Compass the ability to compartmentalize its defense — each requires a different legal theory to answer, and no single theory answers all three coherently at once.

The internal contradiction: if selective listing exposure constitutes anticompetitive harm when NWMLS imposes it through Rule 2, what makes selective listing exposure an innovation when Compass imposes it through Phase 1? Compass’s theory requires the court to hold that the more restrictive distribution arrangement — Phase 1, Compass agents only — is procompetitive, while the less restrictive arrangement — mandatory MLS sharing with all 30,000+ licensed agents — is anticompetitive. An inversion of that structure is a legal inconsistency, not a factual dispute. It does not resolve more favorably for Compass on a developed record than it does at the pleadings stage.

The cross-forum market definition inconsistency: Compass argued national market in Zillow and argues Seattle/King County in NWMLS for the same 3PM strategy and the same conduct. Absent a coherent economic basis for that distinction — which Compass has not produced — NWMLS trial counsel holds either a judicial estoppel motion or a credibility attack on Compass’s market definition expert. Both are available on a fully developed record.

The consumer harm failure: Compass bears the burden of demonstrating harm to competition, not harm to Compass. On the current record, Compass has produced seller-level transaction statistics. Ninety-four percent of 3PM listings eventually reach the MLS regardless. Output has not been reduced. Prices have not been shown elevated market-wide. All three channels of competition harm that Rule of Reason step one requires remain unestablished — and the CPA counterclaim adds a parallel track reaching the same consumer harm question through a lower evidentiary threshold.

Contact mcai@mindcast-ai.com to partner with us on Predictive Cognitive AI in Law and Behavioral Economics. To deep dive on MindCast work in Cognitive AI upload the URL of this publication into any LLM and prompt ‘reconstruct MindCast framework with three degrees of cited sub links.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure.

Recent projects: MindCast AI Emergent Game Theory Frameworks | Google’s Deep-Thinking Ratio Measures Effort, Not Structure | The Cognitive AI Response to Apple’s “The Illusion of Thinking | Triadic Calibration and the Acceleration of Metacognition | The Runtime Causation Arbitration Directive | Runtime Geometry, A Framework for Predictive Institutional Economics | The Ninth Circuit on April 16 as System Convergence — The First Measurable Test of Prediction Market Structure

III. Impact on Investors

The counterclaim’s investor consequences run on two tracks simultaneously — public markets repricing of the Compass acquisition thesis and adjacent firms, and private market due diligence implications for buyers and owners of assets that passed through Compass’s pre-MLS marketing architecture. Both tracks are materially affected by the same filing.

III-A. Public Markets: COMP and the Layer 3 Impairment

Understanding what the counterclaim’s paragraph 43 means for Compass investors requires first understanding what the Anywhere Real Estate acquisition actually bought. The The Compass Commission Consolidation Strategy and Real Estate Marketing Transparency — What Seattle Region Ultra-Luxury Records Reveal About Price Discovery and Market Control developed the Three-Layer Acquisition Hierarchy that separates what survives transparency legislation from what does not.

Layer 1 is the base operating value of Anywhere Real Estate as a standalone brokerage: 340,000 agents, established brands including Coldwell Banker, Century 21, and Sotheby’s International Realty, and functioning transaction volume across 35 major markets. Layer 1 survives any regulatory change. Concurrent marketing mandates, antitrust verdicts, and transparency legislation do not touch it.

Layer 2 is the scale synergy value created by combining Compass’s technology platform and recruiting infrastructure with Anywhere’s agent network: back-office consolidation, cross-brand referrals, and the competitive advantage the combined entity holds over independent brokerages on service quality and operational efficiency. Layer 2 also survives SSB 6091 intact. Windermere competes at 35% Washington luxury market share entirely on Layer 2 value — without private exclusives, without pre-MLS routing, without the architecture the counterclaim describes. Layer 2 describes a business worth owning.

Layer 3 is the private exclusive infrastructure premium — the $400–800 million of the $1.6 billion acquisition price that exists only if listings can be withheld from the open market long enough for an internal Compass buyer to arrive first, capturing both the listing-side and buyer-side commission on the same transaction. Layer 3 is the layer SSB 6091 eliminates in Washington, paragraph 43 documents as legally expiring on June 11, 2026, and the state-level legislative ratchet replicates nationally with each state that follows. Layer 3 is not a strategic preference. With $2.6 billion in post-merger debt assumed on a firm that has never posted a full-year GAAP profit, Layer 3 is a solvency argument.

The 130-transaction Seattle ultra-luxury dataset from The Compass–Anywhere Address Suppression Calculus quantifies the Layer 3 mechanism at ground level: 16 of 130 transactions produced commission flows entirely inside the combined Compass-Anywhere entity, representing $4.2 million in captured buyer-side commission from one metropolitan market’s monthly top-10 record. Scaled to 35 major markets at 10–15x the top-10 transaction volume, the same internalization rate implies $600 million to $1.5 billion of the acquisition price resting on the single operating condition that SSB 6091 eliminates in Washington and the structural state-level ratchet replicates nationally.

Paragraph 43 of the counterclaim is the first publicly filed federal court document stating, under professional certification, that Compass knows its primary revenue-generating architecture will violate Washington state law. The goodwill recorded at the Anywhere acquisition close assumed the Private Exclusive infrastructure would continue operating.

The auditor testing goodwill assumptions at the next cycle reads paragraph 43, reads the statute quoted at paragraph 40, reads the June 11, 2026 effective date, and determines whether the goodwill assumption still holds. No LinkedIn post manages that inquiry. As the SSB 6091 Has Passed: Here Is What It Now Reaches — and the Compass Enforcement Record It Inherits analysis notes: a firm that outsources its listing suppression infrastructure to a third-party platform for a three-year term because it cannot operate that infrastructure internally at scale has not recovered Layer 3 — it has documented that Layer 3 can no longer be operated internally.

The Debt-Narrative Correlation — established in The Cybernetics of Compass Holdings’ Narrative Control Architecture — Inventory Restriction, Commission Capture, and the Collapse of Audience Separation — is the investor’s primary interpretive key: Compass’s rhetorical intensity tracks balance-sheet constraints, not market conditions. The March 19–20 sequence — Zillow dismissal, SSB 6091 signing, fiduciary duty LinkedIn carousel, open letter naming NWMLS as a retaliatory enforcer — is the most intense single-week escalation in the correlation’s documented history, coinciding with simultaneous closure of both active regulatory forums. The blitz is the financial pressure signal. The counterclaim is the structural constraint that makes the pressure permanent.

The Disclosure Form versus the earnings call is the self-documentation trap that compounds the investor risk. Compass’s own client-facing Disclosure Form states that private exclusive marketing may reduce the number of potential buyers, may reduce the number of offers, and may reduce the final sale price. Reffkin stated on the Q1 2025 earnings call: “There is no downside.” Both documents are public, simultaneous, and about the same product. The gap between those two statements — one issued to clients, one issued to capital markets — is the UDAP deceptive trade practices exposure documented in Death by a Thousand Depositions — A Pre-Foresight Simulation of Compass’s Multi-Vector Regulatory Collapse. No investigation required. Only compilation. An investor pricing Reffkin’s public communications as founder-style brand management is misreading the evidentiary environment in which those communications now operate.

The counterclaim, SSB 6091, and the voluntary industry consensus documented in Zillow, eXp, and Redfin–Compass — Three Deals. Twenty Days. One Outlier.together produce a single investment thesis recalibration: Compass shifts from a potential distribution-layer disruptor to a high-performing brokerage with technology advantages. The structural ceiling compresses. The operating business remains. What changes is the premium the market can rationally assign to a business model that depends on a regulatory permission structure that three simultaneous institutional forces — federal courts, a state legislature, and voluntary industry consensus — have now withdrawn.

III-B. Adjacent Publicly Traded Firms: Competitive Realignment and the Leverage Inversion

As The Compass Antitrust Self-Destruction Sequence — How Aggressive Federal Litigation Birthed the Legislation That Destroyed the Business Modeldocumented through the Nash-Stigler coalition collapse analysis, Compass’s federal complaints collapsed a fragmented equilibrium into a unified coalition with a single dominant strategy: eliminate the conduct legislatively rather than litigate it bilaterally. The counterclaim completes that coalition’s defensive arc by converting NWMLS from a cost-burdened defendant into an affirmative plaintiff with treble damages claims and fee-shifting potential. For publicly traded firms adjacent to the dispute — Zillow Group (Z/ZG), CoStar Group (CSGP), and any MLS-affiliated or brokerage-affiliated public entity — the counterclaim’s most significant signal is structural stabilization: the transparency-dominant architecture the industry voluntary consensus already endorsed is now being defended by a counterclaim with statutory alignment, bilateral damages claims, and a trial date.

Windermere operates at 35% luxury market share in the Washington market entirely on Layer 1 and Layer 2 value — service quality, agent talent, transaction expertise — none of which SSB 6091 touches. The twenty-day industry sequence documented in Zillow, eXp, and Redfin–Compass — Three Deals. Twenty Days. One Outlier. confirmed the voluntary market consensus: Zillow Preview with full buyer data and open access, eXp’s three-portal non-exclusive syndication, Realtor.com CEO Damian Eales explicitly contrasting “equal access for all buyers” against “a subset selected by the listing agent” — every major industry actor except Compass chose open distribution architecture within twenty days of each other. Competing firms now operate in a market where the industry’s own voluntary judgment endorsed the transparency model that SSB 6091 mandates and NWMLS Rule 2 has always required. For investors in those firms, the consensus is a stability signal: the architecture their portfolio companies built on is the architecture the regulatory and judicial environment is now actively defending.

III-C. Private Real Estate Investors: Due Diligence in a Post-Counterclaim Market

Private real estate investors — buyers, developers, family offices, institutional acquirers, and high-net-worth individuals evaluating residential assets — face a materially different set of counterclaim consequences than public markets investors. The question is not goodwill impairment. The question is whether the assets they have transacted, are evaluating, or may acquire were subject to the information suppression architecture paragraph 23 documents.

The “negative insights” finding is an asset-level due diligence problem, not only a securities disclosure problem. Compass’s own marketing materials confirm that properties passing through the Private Exclusive and Coming Soon phases were marketed to buyers without accurate days-on-market data and without price-drop history. A private investor who purchased a property quietly marketed within the Compass network for weeks or months before formal MLS listing — and who evaluated that property without knowing the pre-MLS marketing duration, the number of offers received and declined, or whether the price had already been adjusted during the private phase — negotiated from a structurally weaker information position than the seller held. The CPA counterclaim names exactly that asymmetry as the deceptive practice at issue. For prior buyers of Compass-handled properties, the finding is a retrospective due diligence flag. For current buyers evaluating active Compass listings, it is a forward-looking analytical prompt.

The post-merger disclosure problem compounds the private investor exposure. As documented in SSB 6091 Has Passed. Here Is What It Now Reaches — and the Compass Enforcement Record It Inherits, the Compass–Anywhere merger closed January 9, 2026, bringing Coldwell Banker, Century 21, Sotheby’s International Realty, ERA, and other Anywhere portfolio brands under the same corporate parent. Any transaction since that date where both the listing agent and the buyer’s agent carry different brand names from the combined Compass-Anywhere portfolio — presented to the buyer as independent competitive representation — is structurally single-enterprise representation dressed in disclosure language that has not been updated to reflect common control. Washington’s RCW 19.86 consumer protection standard for material omission — no intent required, structural deception facially apparent from the disclosure form itself — applies to those transactions.

The transparency restoration SSB 6091 enforces beginning June 11, 2026 is a positive structural signal for private investors evaluating Washington residential assets going forward. Accurate days-on-market data flows correctly. Price-drop history is visible from the first day of public marketing. Pre-MLS buyer-pool selection that compressed competitive bidding during the private phase is eliminated. For any private investor who relies on market comparables — appraisers, lenders, institutional buyers evaluating deal basis, developers assessing comparable sales — the systemic data integrity improvement the counterclaim and SSB 6091 together enforce improves the quality of the market signal being bought from.

The practical due diligence checklist for private investors in Compass-active markets follows directly from the enforcement analysis in SSB 6091 Has Passed. Here Is What It Now Reaches — and the Compass Enforcement Record It Inherits. Pull the Cumulative Days on Market (CDOM) versus Days on Market (DOM) gap on any active Compass listing: the delta between those figures on Compass’s own platform is the platform’s own admission of pre-MLS marketing duration. Verify co-listing agent affiliations against the post-January 9, 2026 Compass-Anywhere corporate structure before signing any engagement agreement. On any Redfin display of a Compass listing, check whether days-on-market, price-drop history, and valuation estimates are present — their absence while present on every adjacent listing is the two-tiered information architecture the SSB 6091 enforcement analysis identified as an independent consumer protection issue. These are not litigation postures. They are market analysis tools the counterclaim’s factual record made publicly accessible.

IV. Public Perception in the Real Estate Industry

The PR blitz is not managing the narrative. Every statement Compass makes feeds the judicial record that will resolve the case — and the general public possesses a closed evidentiary record operating independent of any single publication or proceeding.

As Compass Rhetorically Reframing Seller Choice to Launch Jurisdictional Attack on MLSs established: Compass is no longer fighting for listing visibility. After securing national distribution through the Redfin partnership, Compass targets MLS enforcement authority directly — the open letter published March 19, the same day SSB 6091 was signed, naming NWMLS by name as a retaliatory enforcer and pledging institutional resources to fund agent resistance to MLS enforcement actions. Compass, joined by Rocket and Redfin, attempts to convert seller preference into a legal override of MLS rules, positioning agents as constrained actors caught between client instruction and institutional enforcement. Framing the conflict that way masks the structural reality: control over listing exposure determines control over buyer flow, pricing signals, and market structure.

“Compass is no longer fighting for listing visibility. It is attempting to replace the authority that governs it.”

— Compass Rhetorically Reframing Seller Choice to Launch Jurisdictional Attack on MLSs

The Blitz as Self-Documentation

The The Cybernetics of Compass Holdings’ Narrative Control Architecture — Inventory Restriction, Commission Capture, and the Collapse of Audience Separation analysis named the eighth emergent pattern across the full Compass corpus as the Self-Disclosure Trap: Compass’s most damaging evidence is self-generated. The PR blitz accelerates the trap rather than escaping it — every statement made to every audience operates inside a judicial and legislative record that inverts its intended meaning.

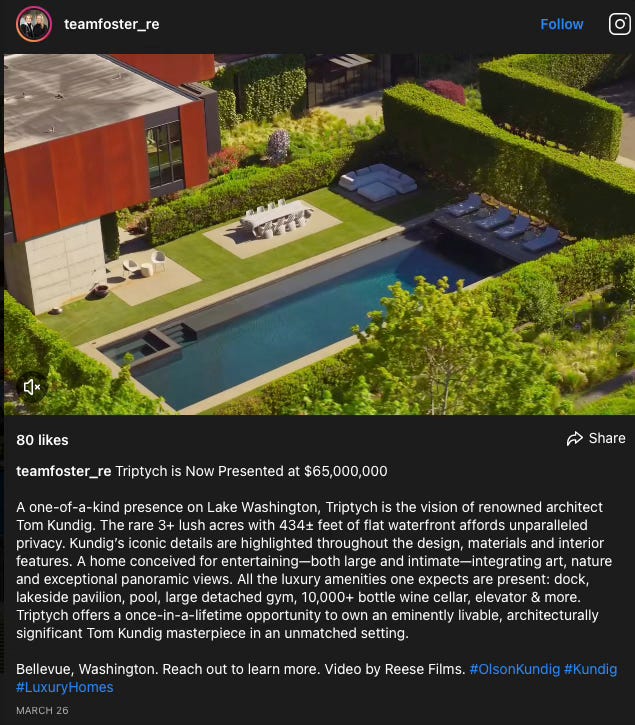

Reffkin’s post-Zillow LinkedIn post — framing 268 days of litigation and zero judicial relief as consumer-choice momentum — is a party admission under FRE 801(d)(2). The open letter naming NWMLS as a retaliatory enforcer is a party admission. The Redfin partnership press release framing buyer data suppression as seller benefit is a party admission. The agent messaging campaigns generating the 17:1 Astroturf Coefficient — documented in The Astroturf Coefficient: Manufactured Opposition in the SSB 6091 Legislative Record — are discoverable. Every deponent in the October 2026 trial was a participant in some layer of the blitz. Nelson was present and silent at both Washington legislative hearings while directing broker-level messaging. Huff carried the seller-choice narrative before the legislature and could not answer the merger’s competitive consequences on the record. Skillman’s February 26 social media posts — framing buyer data suppression as seller benefit while representing the Triptych estate on Lake Washington, Bellevue, then listed without a street address and previously marketed at $79 million before being presented publicly at $65 million on March 26 — are timestamped, public, and in the record.

The Skillman Moment

The Skillman Moment — an established analytical marker in The Cybernetics of Compass Holdings’ Narrative Control Architecture — Inventory Restriction, Commission Capture, and the Collapse of Audience Separation and Compass Rhetorically Reframing Seller Choice to Launch Jurisdictional Attack on MLSs — names the precise point at which Compass’s internal narrative grammar fails to export beyond its own incentive structure. Moya Skillman, principal of the Foster-Skillman Compass team and co-director of the Eastside luxury listing architecture documented in The Compass–Anywhere Address Suppression Calculus, applied Reffkin’s “seller choice” framing — developed to challenge MLS mandatory-sharing rules — to SSB 6091, a state licensing conduct statute, in public social media commentary on February 26, 2026. The same day the Redfin partnership was announced. While representing the Triptych estate — a Tom Kundig-designed property on Lake Washington in Bellevue, Washington — then privately marketed at $79 million without a publicly listed street address.

By March 26, 2026 — one month after the February 26 posts, four days before Washington AG Nick Brown filed the state’s Kalshi complaint, and twenty-five days after Compass filed its NWMLS counterclaim response window opened — Team Foster’s Instagram account announced: “Triptych is Now Presented at $65,000,000.” A $14 million reduction. Eighteen percent off the private marketing price. The price drop is not incidental detail. The “negative insights” the counterclaim names are specifically days-on-market accumulation and price-drop history that Compass strips from NWMLS listings after the Private Phase concludes. The Triptych listing is the live transaction-level demonstration of that mechanism: a buyer encountering Triptych on the MLS at $65 million on March 26 would see the current ask without knowing the property had been privately marketed at $79 million, without knowing how long it had circulated within the Compass network before the price adjustment, and without the suppressed days-on-market record that would otherwise have informed their negotiating position. The Disclosure Form warned this outcome was possible. Reffkin said there was no downside. The listing documented both simultaneously.

The category error in Skillman’s February 26 posts is structurally significant independent of the price drop. “Seller choice” is a market-level vocabulary built to contest cooperative governance rules — whether an MLS can require universal listing submission. SSB 6091 is a conduct statute enacted by 141 of 142 Washington legislators. Applying the former to the latter is not a rhetorical miscalculation. It is evidence that the cognitive grammar Compass’s internal communications infrastructure runs on does not recognize the distinction between a private cooperative rule and a state law. Inside the Compass incentive structure, the framing resolves the compliance tension emotionally for agents — “we’re protecting your client’s right to choose.” Outside that structure, in a legislative transcript, a deposition, or a jury pool, the framing reads as a challenge to a law the speaker presumably knows exists. The posts are timestamped. The law had already passed. The listing subsequently documented the suppressed-data mechanism in real time. The Skillman Moment is not an isolated social media post. It is the Cognitive Grammar mismatch made visible at the individual agent level — the same mismatch Section V’s integrated system output identifies at the institutional level.

The blitz’s enforcement mechanism has now broken down in the most publicly visible form available: industry professionals across LinkedIn are sharing — and joking about — being blocked by Reffkin. “Blocked by Reffkin” has become a running industry punchline. Analytically, the joke is not trivial. The Prestige Markets as Signal Economies — A Model of Signal Suppression and Institutional Failure the MindCast corpus formalizes requires four conditions to hold simultaneously: Access Dependence × Reputational Retaliation Risk × Information Fragmentation × Narrative Distortion exceeding Signal Aggregation Capacity. The PR blitz’s foundational assumption was that Reputational Retaliation Risk — the career cost of publicly contradicting a CEO whose network controls listing access, referral flows, and recruiting infrastructure — would suppress broker-level dissent. Blocking critics was the visible enforcement of that assumption. When blocking becomes an industry punchline rather than a deterrent, the Reputational Retaliation Risk condition has failed. The suppression architecture loses its enforcement function the moment the threat is no longer credible as a career consequence.

Brokers publicly sharing their block status as a badge are simultaneously signaling two things NWMLS trial counsel will note: first, that Compass’s network access no longer carries sufficient professional leverage to suppress their public commentary — the Access Dependence condition has weakened alongside the Retaliation Risk condition; second, that the critique that earned the block is professional testimony from people operating inside the system the counterclaim describes. Every broker who jokes about being blocked is vouching, with professional identity attached and publicly, for the authenticity of what they observed. No deposition required. LinkedIn is aggregating that signal in real time, at scale, beyond Compass’s ability to suppress or manage. The Signal Suppression Equilibrium’s formula — A×R×F×N > S — has inverted: Signal Aggregation Capacity now exceeds the suppression product. The counterclaim accelerated that inversion by giving every blocked broker a federal court document validating what they said when they got blocked.

What the General Public Now Knows

Public opinion shifts. What the general public now possesses about Compass is a closed evidentiary record in multiple publicly accessible forums simultaneously — and assembling it required no coordination. Three facts anchor that record in their simplest form.

First, “negative insights.” Compass internally labeled the information a buyer needs to negotiate as “negative insights” and systematically stripped it from NWMLS listings before public submission. Quoted in a federal court counterclaim, the phrase requires no legal translation.

Second, the Disclosure Form versus the earnings call. Compass’s own client-facing Disclosure Form states that private exclusive marketing may reduce the number of potential buyers, may reduce the number of offers, and may reduce the final sale price. Reffkin stated on the Q1 2025 earnings call: “There is no downside.” Both documents are public, simultaneous, and about the same product. As the Death by a Thousand Depositions — A Pre-Foresight Simulation of Compass’s Multi-Vector Regulatory Collapse analysis established, the gap between those statements is the UDAP deceptive trade practices exposure — no investigation required, only compilation.

Third, 141–1. Washington’s legislature voted 141–1 to make Compass’s core marketing practice illegal — in the same state where Compass filed its antitrust complaint characterizing the identical practice as a consumer protection innovation. As The Compass Antitrust Self-Destruction Sequence — How Aggressive Federal Litigation Birthed the Legislation That Destroyed the Business Model established, 141–1 is not a legal argument. It is the simplest possible legislative signal about what the practice actually is.

The fair housing dimension compounds the public record’s durability. SSB 6091’s legislative history states directly: “One study found that hidden listings may be reinforcing racial divides.” The “Call for Address” mechanism — documented in The Compass–Anywhere Address Suppression Calculus through the Triptych estate on Lake Washington in Bellevue, privately marketed at $79 million without a publicly listed street address before being presented publicly at $65 million on March 26, 2026 — is a gatekeeper that disproportionately disadvantages buyers who lack the network connectivity to identify which Compass agent to contact. A brokerage running a PR blitz framing buyer data suppression as seller empowerment, while operating a “Call for Address” mechanism, manages a consumer narrative against a statutory record that 141 elected legislators characterized as a fair housing intervention.

Consumers do not parse MLS rules. They rely on simple expectations: listings should be visible, information should be complete, and retaining a buyer’s agent should mean the buyer’s agent is actually working for the buyer. Compass’s model challenges each expectation through staged visibility, stripped data fields, and dual-commission routing. NWMLS’s counterclaim translates those mechanisms into intuitive terms — hidden listings, missing data, “negative insights” — and files them in federal court. Once consumers ask why they did not see a listing, why the price history was absent, or why the days-on-market counter started on the day public marketing began rather than the day private marketing began, trust erodes. Trust does not require full knowledge to erode. Three facts in plain English — the “negative insights” phrase, the Disclosure Form versus the earnings call contradiction, and the 141–1 vote — are sufficient. The general public now possesses all three.

Broker Recruitment: The Architecture Is Expiring

Agents respond to risk faster than courts resolve cases. Paragraph 43 delivers a specific and personal message to every Compass agent in Washington and every prospective recruit evaluating the Compass proposition nationally: the architecture being recruited to operate will be unlawful in Washington after June 11, 2026, and the corporate backstop’s track record in Washington is zero judicial relief across two proceedings.

The counterclaim introduces three compounding risk vectors that change how agents advise clients and evaluate brokerage affiliation. The compliance vector: three concurrent enforcement tracks operate independently and simultaneously after SSB 6091’s effective date — Washington Department of Licensing (DOL) Real Estate Program enforcing through RCW 18.85 against individual licensees, the Attorney General’s (AG’s) consumer protection division under RCW 19.86, and NWMLS governance enforcement. Personal license suspension or revocation is the exposure, not a corporate fine Compass covers. The open letter’s “we have your back” pledge has no documented mechanism for absorbing personal license discipline. The visibility vector: Zillow’s LAS and Redfin’s platform architecture penalize listings not broadly exposed. An agent whose listing strategy generates platform removal risk cannot serve clients as effectively as agents operating on fully open-distribution terms. The reputation vector: the “negative insights” phrase is now in a federal court counterclaim. Any Compass agent who explains their pre-market strategy to a client sophisticated enough to search the case docket faces a conversation the open letter cannot script.

Even small increases in perceived risk change behavior at the agent level. Agents hedge. They avoid strategies that might reduce listing exposure or trigger platform penalties. As The Cybernetics of Compass Holdings’ Narrative Control Architecture — Inventory Restriction, Commission Capture, and the Collapse of Audience Separation established through the Agent as Enforcement Vector pattern: Compass captures the revenue upside of the routing architecture; agents absorb the compliance downside. Confidence returns to the market when agents believe the rules will hold — and the counterclaim, SSB 6091, and the voluntary industry consensus documented in Zillow, eXp, and Redfin–Compass — Three Deals. Twenty Days. One Outlier. all signal the same direction simultaneously. Windermere, John L. Scott, and REMAX agents operating in Washington face none of these three vectors. Their value proposition survives SSB 6091 entirely intact.

The Feedback Loop: How Public Perception Becomes System Pressure

Public perception of Compass’s conduct does not stay in the consumer domain. It feeds back into the institutional system through four sequential transmission mechanisms — each reinforcing the next, each making the prior stage harder to reverse.

Consumer distrust triggers agent hesitation. When buyers ask why they did not see a listing, why the days-on-market counter appears to have reset, or why price history is absent on a Redfin display of a Compass property, agents face those questions at the transaction level. An agent whose explanation requires defending a practice the general public now associates with the phrase “negative insights” — in a federal court counterclaim — cannot manage that conversation as efficiently as an agent operating on fully transparent terms. Hesitation at the agent level does not require a regulatory event to produce behavioral change. Consumer awareness is sufficient.

Agent hesitation shifts listing strategy. Agents who hedge away from pre-MLS routing reduce the inventory flowing through Compass’s Phase 1 and Phase 2 architecture. Reducing inventory through those phases is not merely a compliance response to SSB 6091. It is a market signal. Sellers whose agents recommend against private exclusives — because the compliance, visibility, and reputation vectors make the strategy harder to execute without friction — encounter the open-distribution model as the default rather than the alternative. Each listing that enters the MLS without a private phase is a data point restoring the price discovery signal the “negative insights” architecture suppressed.

Listing strategy shifts reinforce platform architecture. As more listings enter the MLS concurrently with public marketing, the Zillow Preview and eXp non-exclusive syndication architectures — both built for transparent premarket visibility — become the dominant distribution infrastructure by default. Platform algorithms optimize for engagement. Listings with full buyer data, accurate days-on-market, and complete price histories generate stronger engagement signals than listings with stripped fields. The voluntary industry consensus documented in Zillow, eXp, and Redfin–Compass — Three Deals. Twenty Days. One Outlier.becomes self-reinforcing as the platform layer rewards the behavior SSB 6091 mandates.

Platform reinforcement produces legal validation. As the transparency architecture becomes the market default — endorsed by consumer behavior, agent practice, and platform design simultaneously — the procompetitive justification for NWMLS Rule 2 and SSB 6091 accumulates observable confirmation in real market data. Every quarter of post-June 11 transaction records in Washington is a quarter of evidence that mandatory concurrent marketing did not harm sellers, did not reduce market activity, and did not produce the negative consequences Compass’s complaint predicted. That evidence enters the NWMLS summary judgment record, every subsequent state legislature’s hearing record, and the goodwill impairment analysis auditors apply to the Anywhere acquisition premium.

The loop is self-reinforcing and, absent a countervailing structural force, irreversible. Consumer awareness generates agent behavior change. Agent behavior change restores data integrity. Restored data integrity validates platform architecture. Platform validation produces legal confirmation. Legal confirmation deepens consumer awareness. The counterclaim did not create the loop. It accelerated it by filing the “negative insights” phrase in federal court — the single most publicly legible expression of what the loop was always about.

Conclusion

NWMLS’s April 2 counterclaim did not introduce new variables into the Compass v. NWMLS proceeding. It closed the escape pathways that had kept the system’s governing structure ambiguous. Five analytical domains now converge on the same structural verdict: the litigation thesis is exposed at summary judgment by the frame inversion, the free-rider mechanism, and the three-attack convergence; the investor thesis rests on a Layer 3 premium that paragraph 43 documents as legally expiring; the public record is closed against narrative management by three facts any buyer understands without legal training; the industry response is governed by a Behavioral Drift Factor that predicts escalation before the strategic team decides on it; and the system itself has crossed the classification threshold from contested to convergent.

The MindCast Simulation’s transparency-dominant convergence regime classification carries specific meaning for each audience this publication addresses. Investors evaluating Compass’s acquisition thesis now hold a federal court document — signed under professional certification — establishing that the operating condition on which $400–800 million of the Anywhere acquisition premium rested will be unlawful in Washington after June 11, 2026. Private real estate buyers in Compass-active markets hold a due diligence checklist anchored in the counterclaim’s own factual record. Agents evaluating brokerage affiliation hold three compounding risk vectors — compliance, visibility, and reputation — that activate simultaneously after June 11 and that the corporate backstop’s track record of zero judicial relief across two proceedings cannot absorb. Institutional actors watching the October 2026 trial calendar hold a settlement architecture analysis identifying the Nelson-Huff-Skillman deposition sequence as the specific trigger that opens and closes the settlement window.

Three observable events will confirm or falsify the simulation’s classification before the end of 2026. June 11, 2026: SSB 6091 takes effect and the first enforcement cycle begins. The 3PM adoption rate in Washington within six months of that date is the primary broker defection gate condition. The discovery calendar between now and October 2026: each deposition deepens the record NWMLS holds as leverage and narrows the settlement window. And the October 2026 trial itself, or the settlement that forecloses it: whichever arrives first resolves the central falsification question — whether Compass can produce market-wide consumer welfare evidence the simulation’s P10 scenario requires. MindCast Premium subscribers receive real-time simulation updates as each event activates.