MCAI Lex Vision: The Law and Behavioral Economics of Compass vs. NWMLS

Procedural Survival Is Not Substantive Victory

Companion publications Compass v. NWMLS — The Counterclaim That Closed Compass’s Antitrust Thesis | Visual Synthesis: The Antitrust Litigation Trap Compass Built for Itself | Zillow v. MRED and Compass — Residential Real Estate Enters Infrastructure Sovereignty Conflict

Executive Summary

Compass is not winning — it is sequencing. The denial of the motion to dismiss in the NWMLS case reflects procedural survival, not validation of the antitrust theory Compass advances. Compass pursued aggressive, high-risk injunctive relief against Zillow, where courts demanded proof and exposed structural weaknesses across all three Sherman Act theories. Compass then shifted to a lower-risk procedural posture in the NWMLS case, preserving claims without evidentiary testing.

Washington’s passage of Senate Bill (SSB) 6091 alters the governing structure. As documented in the MindCast enforcement analysis, Multiple Listing Service (MLS) rules alone could not police the pre-MLS marketing window — MLS governance holds jurisdiction only over listings already submitted, not over marketing that occurs before submission. SSB 6091 supplies the statutory backstop that closes the gap, reframes the NWMLS dispute as a transparency response rather than a private restraint, and shifts the legislative record into the judicial interpretation layer at summary judgment.

The MindCast AI Proprietary (MAP) Cognitive Digital Twin (CDT) Foresight Simulation — the MAP CDT — routes the litigation structure through six Vision Functions. All six converge on a single output: Compass operates against system-level constraints that favor transparency, coordination, and broad access. Fragmentation delays failure. Fragmentation does not alter system trajectory.

If Compass cannot demonstrate market-wide consumer welfare gains from selective exposure, the litigation converges toward NWMLS at summary judgment. The current probability distribution reflects that outcome: conditional on no new empirical harm evidence entering the record, the MAP CDT assigns P50–P70 probability to NWMLS prevailing or the case settling on terms that preserve mandatory-sharing architecture. The forward-lock condition is evidentiary, not procedural — Compass survived the pleading stage, but survival does not supply the proof the merits stage requires.

The governing posture is a delay-dominant but converging equilibrium. Courts have not validated Compass’s theory. They have deferred it.

I. Procedural Survival Is Not Substantive Victory

On March 19, 2026, Judge Jamal N. Whitehead denied NWMLS’s motion to dismiss in Compass, Inc. v. Northwest Multiple Listing Service (NWMLS), Case No. 2:25-cv-00766-JNW. Robert Reffkin treated the ruling as vindication. The ruling established only that Compass pleaded enough to proceed — nothing more.

A Rule 12(b)(6) motion tests one thing: whether the complaint states a claim that is plausible on its face. The court accepts all factual allegations as true and draws all reasonable inferences in the plaintiff’s favor. No evidence enters. No expert is cross-examined. No internal document is produced. The court’s own conclusion was explicit: the denial should not be read as expressing any view on the ultimate merits of the parties’ competing theories.

Under Twombly and Iqbal, the plausibility standard is the lowest merits-adjacent threshold in federal civil litigation. Every plaintiff who survives a motion to dismiss wins by exactly that measure. Compass cleared it. Market definition remains unresolved. Competitive effects are untested. NWMLS’s procompetitive justifications remain untested. The factual record Compass must produce does not yet exist.

Compass alleged enough to proceed. Proceeding is not prevailing.

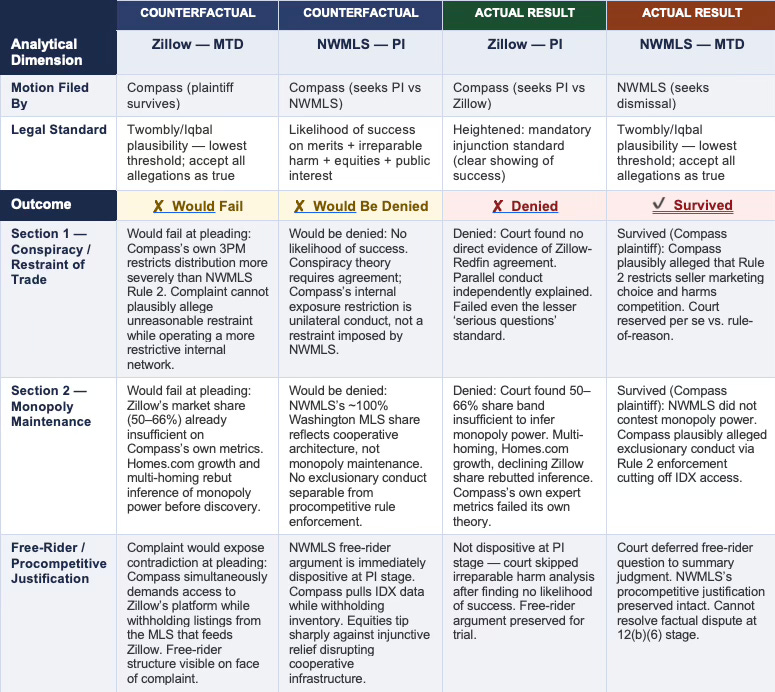

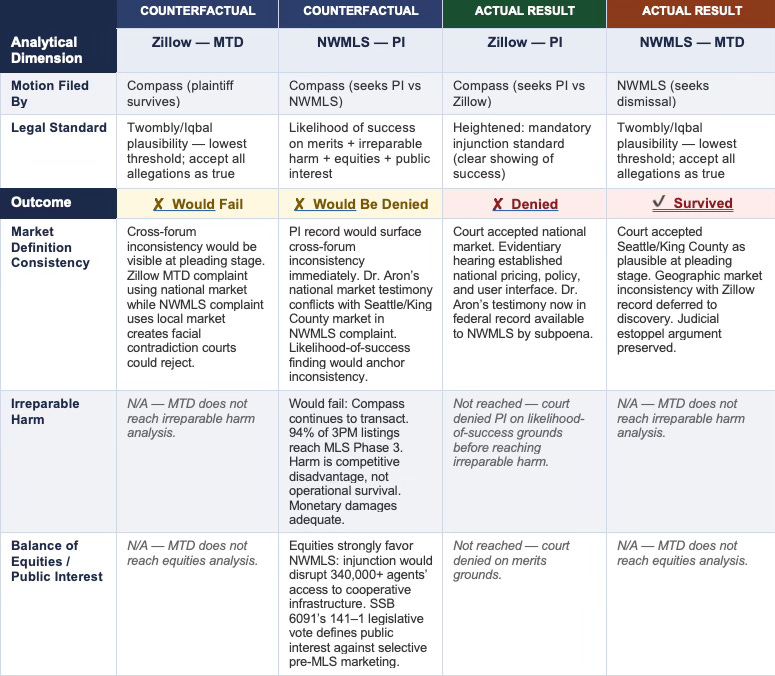

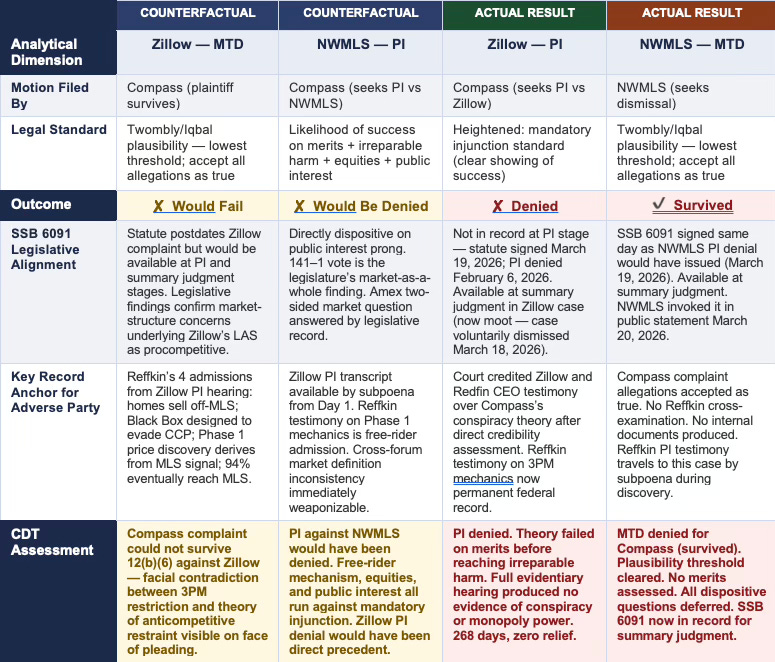

Counterfactual Motion Outcome Matrix: Actual and Modeled Results

Shaded columns = actual outcomes. Unshaded = CDT counterfactual (motion not filed). Analysis applies same legal standards across both cases.

MTD = Motion to Dismiss (Rule 12(b)(6)) · PI = Preliminary Injunction · Counterfactual columns apply the same legal standards as the actual proceedings. Zillow MTD counterfactual assumes Compass filed a parallel 12(b)(6)-stage challenge; NWMLS PI counterfactual applies the four-factor Winter test at the heightened mandatory-injunction standard applied in the Zillow PI proceeding.

II. Self-Inflicted Regulatory Capture: The Litigation That Built the Law Against Itself

The MindCast publication The Compass Antitrust Self-Destruction Sequence documented a pattern it termed self-inflicted regulatory capture: a firm’s own litigation providing opponents the statutory blueprint to regulate it. The sequence has fully resolved.

Before April 2025, Compass operated Private Exclusives quietly within a legal gray zone. NWMLS rules governed listing submission timing and accuracy after a property entered the MLS. NWMLS rules hold jurisdiction only over listings that agents have already submitted — pre-submission marketing falls entirely outside their reach. A listing agent could market a $43.8 million waterfront property privately for 84 days — routing it through the brokerage’s internal network, generating buyer interest among affiliated agents, and narrowing the competitive buyer pool to people whose agents had network access — and submit a fully compliant MLS listing on day 85. Nothing in NWMLS’s rulebook had been violated. The harm was complete before enforcement authority began.

In April 2025, Compass filed a federal antitrust complaint against NWMLS. In June 2025, Compass escalated with a second complaint against Zillow. By broadcasting the mechanics of its shadow market through public federal complaints, Compass handed Washington State legislators, regulators, and opposing industry actors a fully developed analytical and evidentiary framework for statutory intervention. As the MindCast analysis established: Compass’s elite antitrust counsel drafted, with billable precision, the operative definition of ‘public marketing’ that SSB 6091 codified.Washington’s drafters did not need to invent a regulatory framework.

Compass filed one in federal court, and the Legislature applied it 141–1.

SSB 6091 passed the Washington State Senate 49–0 on February 10, 2026, cleared the House 92–1 on March 3, 2026, and was delivered to the Governor. The combined bicameral record stands at 141–1. Compass spent an estimated $2 to $4 million in legal fees to generate the evidentiary record that legislators, regulators, and opposing counsel then deployed against it.

Compass’s own antitrust counsel wrote, with billable precision, the definitions SSB 6091 codified. The Legislature applied them 141–1.

III. The Internal Contradiction Compass Must Answer

Compass’s antitrust theory contains a structural contradiction that discovery will expose. Compass challenges NWMLS’s Rule 2 as an anticompetitive restriction on how brokerages may market properties before MLS submission. Compass’s own 3-Phased Marketing Strategy operates as a graduated restriction on listing distribution — Phase 1 restricts access to Compass agents exclusively, Phase 2 expands exposure selectively on Compass’s own platform, Phase 3 releases the listing to MLS platforms and public portals.

Selective exposure constitutes innovation when Compass controls it and anticompetitive harm when a rule operates against Compass. Discovery will test whether that distinction survives adversarial scrutiny.

Reffkin testified under oath at the Zillow preliminary injunction hearing that homes can and do sell during Phase 1 without ever reaching the MLS. He acknowledged that the Black Box feature on Compass.com was deliberately structured to market Private Exclusives without triggering Clear Cooperation Policy (CCP) rules. He enumerated four advantages of off-MLS marketing: privacy, pre-marketing momentum, feedback collection, and price discovery. That sworn testimony now sits in the federal record in the Southern District of New York. NWMLS’s counsel can subpoena it.

Every admission Reffkin made about the mechanics of Phase 1 maps directly onto NWMLS’s free-rider argument — the argument the court deferred at pleading stage but did not dismiss.

IV. Litigation Fragmentation as Risk Containment

The MindCast framework for Litigation v. Leverage identifies three non-merit litigation types: tactical litigation (aimed at draining resources), structural litigation (exploiting legal asymmetry to suppress weaker parties), and symbolic litigation (recasting narratives through the authority of legal form). Compass’s NWMLS filing exhibits characteristics of all three — a regional cooperative without the resources for decade-long federal defense, an asymmetric venue selection favoring federal antitrust over cooperative governance channels, and a public narrative that instrumentalized the complaint as a seller-choice manifesto.

Compass did not pursue a preliminary injunction (PI) against NWMLS. That omission is the most analytically significant strategic signal in the entire litigation posture. Against Zillow, Compass moved for a preliminary injunction immediately. Against NWMLS, Compass allowed the motion to dismiss to run its course at the pleading stage — the lowest-burden procedural vehicle in the litigation sequence.

The Zillow preliminary injunction loss forced Compass to avoid early merits testing in NWMLS. Compass learned from Zillow what a merits-tested motion produces. Judge Vargas held a four-day evidentiary hearing in November 2025 with live witness testimony including Reffkin himself. After reviewing the full record, she found that Compass failed to meet even the “serious questions” threshold — the standard below likelihood of success. The court denied the preliminary injunction on February 6, 2026. Had Compass sought a preliminary injunction against NWMLS and lost, the likelihood-of-success finding would have entered the record before discovery.

Compass contained risk by separating procedural survival from substantive testing — a maneuver that preserved the public narrative while leaving the legal theory structurally unchanged.

Contact mcai@mindcast-ai.com to partner with us on Predictive Cognitive AI in Law and Behavioral Economics. To deep dive on MindCast work in Cognitive AI upload the URL of this publication into any LLM and prompt ‘reconstruct MindCast framework with three degrees of cited sub links.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure.

Related MindCast AI Research: Run-Time Causation — Causal-signal arbitration framework; institutional evaluation of competing causal narratives. Nash–Stigler Equilibria — Equilibrium concept explaining how institutional incentives stabilize inefficient outcomes. Predictive Institutional Cybernetics — Markets as feedback systems governed by signal processing, delay, and equilibrium stabilization. Cybernetics Foundations — Theoretical lineage from Wiener through Ashby, Beer, Bateson, and Hayek into MindCast’s CDT/Vision architecture. Double-Sided Rational Ignorance (DSRI) — How market participants fail to perceive aggregate harm when information remains fragmented.

V. The Zillow Arc: What the Voluntary Dismissal Record Shows

The MindCast publication The Compass–Zillow Antitrust Arc Is Closed documented Reffkin’s LinkedIn announcement framing voluntary dismissal as a consumer-choice victory. The federal record shows the opposite: Compass lost on every theory it advanced and exited once no path to relief remained after denial of preliminary injunction.

Section 1: No Agreement Found

Compass predicated its Section 1 claim on an alleged conspiracy between Zillow and Redfin to jointly adopt Listing Access Standards (LAS) targeting Compass’s 3-Phased Strategy. After a four-day evidentiary hearing with testimony from both Chief Executive Officers (CEOs), Judge Vargas found the parallel conduct was independently explained. No direct evidence of an anticompetitive agreement existed. The circumstantial evidence was, in the court’s language, ambiguous at best and affirmatively contradicted by credible witness testimony and contemporaneous documents. Compass failed to meet even the serious-questions standard on its core Section 1 theory — not the higher likelihood-of-success threshold, but the lesser standard below it. After a full evidentiary record.

Section 2: Compass’s Own Numbers Were Insufficient

Compass introduced three separate market share metrics generated by its own expert, calculating Zillow’s share at 50 to 66 percent. The court found that market share band insufficient to infer monopoly power given countervailing market characteristics. Multi-homing was ubiquitous. Homes.com grew from 2.4 percent audience share in 2021 to 19 percent by May 2025. Zillow’s own share declined from 62 to 50 percent between May 2024 and June 2025. The theory failed on its own evidentiary terms.

268 days from filing to voluntary withdrawal. Zero judicial relief obtained at any stage. The MindCast Causal Signal Integrity score assigned to Compass’s Zillow theory at filing — 0.23 against Zillow’s 0.77, a 3.3:1 asymmetry — confirmed by Judge Vargas’s February 6 opinion.

Reffkin framed a legal defeat as consumer-choice momentum. Judge Vargas’s 50-page opinion recorded the actual result: 268 days of litigation, zero judicial relief, and voluntary withdrawal once the injunction pathway closed.

VI. The Cross-Forum Market Definition Contradiction

In the Zillow case, Compass defined the relevant geographic market as national. Online home search platforms operate nationally — national pricing, national user interface, national policy implementation. Compass needed a national market to make Zillow’s share appear sufficiently concentrated. The court accepted it.

In the NWMLS case, Compass defined the relevant geographic market as Seattle and King County, Washington. NWMLS controls nearly 100 percent of MLS services in that hyper-local geography. Compass needed a local market to establish NWMLS’s dominance. Both cases involve the same 3-Phased Marketing Strategy, the same underlying conduct, and the same product. Compass argued national market architecture to one court and local market architecture to another, calibrating the definition to whichever framing made market power allegations plausible in each jurisdiction.

NWMLS’s counsel will place Dr. Aron’s national market testimony from the Zillow hearing directly alongside Compass’s Seattle/King County allegations in the NWMLS complaint. Courts apply judicial estoppel when a party successfully asserts a position in one proceeding and takes a clearly inconsistent position in a later proceeding. The contradiction becomes a summary judgment weapon regardless of whether estoppel formally applies.

Compass calibrated its geographic market definition to whichever framing made market power allegations plausible in each jurisdiction. Discovery will surface the inconsistency.

VII. The Free-Rider Argument and the Per Se Reservation

The Free-Rider Mechanism

NWMLS raised the free-rider argument in its motion to dismiss. The court correctly deferred it at the pleading stage. At summary judgment, the argument becomes NWMLS’s strongest weapon, and Reffkin’s sworn testimony establishes its evidentiary foundation without NWMLS lifting a subpoena. Compass’s Phase 1 strategy withholds listing inventory from NWMLS while Compass simultaneously pulls Internet Data Exchange (IDX) data from compliant brokerages to populate its own platform. Price discovery in Phase 1 derives its value from the broader MLS price signal. Compass extracts that signal while refusing to contribute to it.

The Per Se Reservation

Judge Whitehead identified the core distinction that dooms Compass’s per se group boycott theory: Compass is a member brokerage, not a rival listing service. PLS.com involved an MLS being boycotted by other MLSs at the same market level. Compass is a broker seeking to withhold listings from the cooperative infrastructure it belongs to — while simultaneously extracting the IDX data that cooperative’s compliant members generate. The court wrote that it had reservations about whether PLS.com’s per se group boycott analysis extends to this case given the meaningful factual differences identified. Judicial reservation language is intentional. At summary judgment, on a developed record, that reservation becomes a ruling.

VIII. SSB 6091 and the Statutory Realignment

The MindCast enforcement analysis SSB 6091 Has Passed. Here Is What It Now Reaches documented why legislative action was necessary rather than MLS rule enforcement alone. Three distinct constraints prevented NWMLS from closing the gap independently: the scope gap (MLS rules cannot reach pre-submission marketing by design), the litigation constraint (enforcement actions during active antitrust litigation became exhibit material for Compass’s exclusion narrative), and the structural conflict (NWMLS’s broker-owned governance structure created competitive alignment problems in enforcing against its largest member’s top listing teams).

SSB 6091 moves the compliance clock to the moment marketing starts — not the moment of MLS submission. The 84-day pre-MLS window documented in MindCast’s transaction analysis is no longer lawful in Washington.

Three Structural Effects on the Litigation

First, NWMLS moves from private justification to policy alignment. As the MindCast statutory analysis in WA SSB 6091: Real Estate Marketing Transparency established, the statute’s core objective is concurrent, transparent marketing as the default condition for Washington residential real estate. NWMLS now defends a rule that the Washington legislature independently determined reflects pro-competitive market architecture. The legislative record supplies the factual predicate for NWMLS’s procompetitive justification at summary judgment.

Second, Compass’s narrative compresses. The “seller choice” framing Compass has deployed publicly illustrates how Compass’s internal narrative functions for agents operating inside the commission incentive structure — and why it fails when exposed to judicial or regulatory scrutiny. SSB 6091 reframes selective exposure not as seller empowerment but as opacity risk — a reframe the 141–1 legislative record makes extremely difficult to contest.

Third, the Amex two-sided market question the NWMLS court deferred now carries legislative weight. SSB 6091’s findings establish that the Washington legislature determined mandatory listing transparency benefits the market as a whole — the precise framing the Amex “market as a whole” inquiry requires. Courts weighing the Amex framework will encounter a legislative record that pre-answers the dispositive question in NWMLS’s favor.

The Redfin Partnership as Litigation Accelerant

On February 26, 2026 — while the House Rules Committee held the scheduling gate on SSB 6091 — Rocket Companies, Compass, and Redfin announced a three-year strategic alliance. Compass Coming Soon listings began appearing on Redfin immediately. Private Exclusives to follow. The announcement killed the only remaining legislative argument against the bill: that the market would self-correct. Redfin’s CEO had pledged publicly in April 2025 to ban listings selectively pre-marketed without MLS exposure. Rocket acquired Redfin. The pledge reversed. The same platform that was the primary exhibit for voluntary market discipline became the primary national distribution infrastructure for the practice it pledged to ban.

As the MindCast circumvention analysis in Compass Plan B: Structural Circumvention After SSB 6091 documents, post-passage adaptation paths carry their own evidentiary risk. Workaround strategies weaken Compass’s litigation posture by signaling business-model preservation rather than consumer protection. Courts interpreting the procompetitive justification for NWMLS’s rules will weigh post-enactment behavior. A brokerage that constructs operational workarounds to a transparency statute within weeks of enactment supplies evidence that the challenged conduct’s purpose is structural, not incidental.

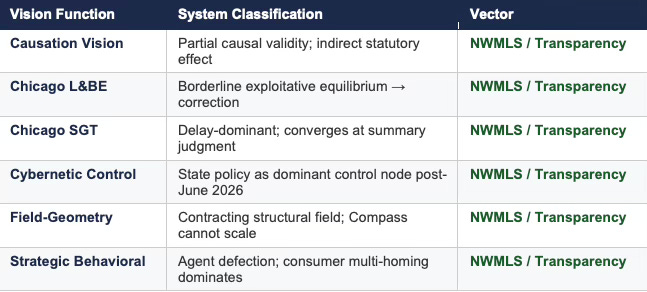

IX. MindCast AI Proprietary Cognitive Digital Twin Foresight Simulation: Six Vision Functions

MindCast’s MAP CDT architecture routes each institutional analysis through signal intake and filtering, hypothesis formation, causal inference, causal signal integrity validation, Vision Function routing, dominance resolution, and recursive foresight simulation. Each actor is modeled as a Cognitive Digital Twin encoding its objective function, constraint stack, adaptation velocity, and feedback sensitivity. What follows is the published output of the simulation run across six Vision Functions applied to the Compass litigation system.

VISION FUNCTION I Causation Vision

CDT Causal Signal Integrity Test

System Interpretation

Causal Signal Integrity testing confirms that SSB 6091 strengthens NWMLS’s litigation position — but through an indirect mechanism, not a direct legal determination. The statute does not determine legal outcomes directly but alters the weighting of procompetitive justification narratives and consumer harm burden allocation. The strongest causal link is indirect: legislation changes judicial interpretation context rather than outcome mechanics.

Compass over-attributes causality to legal doctrine and systematically underweights structural and behavioral constraints. Compass’s own litigation generated the regulatory record that SSB 6091 applied. Compass must now produce empirical consumer harm evidence to overcome the causal deficit its evidentiary record created in New York.

CDT Foresight Predictions

Courts cite market structure and evidence more than the statute itself at summary judgment

Legislative alignment increases NWMLS success probability but is not independently determinative

Compass must produce market-wide consumer harm evidence to overcome the causal deficit the Zillow PI record established

VISION FUNCTION II Chicago Law & Behavioral Economics

Coase → Becker → Posner Chain

System Interpretation

Coase layer: MLS functions as coordination infrastructure with high trust density and low transaction cost for shared listings. Compass’s Private Exclusive model was built entirely on top of cooperative infrastructure Compass does not own and cannot replace. The coordination-cost foundation for that analysis — distinguishing MLS coordination infrastructure from transaction-cost pricing friction — is developed in the MindCast Coasean Coordination Problem Part III.

Becker layer: Compass exploits gaps in coordination by introducing selective exposure strategies that increase private payoff at the cost of aggregate market information quality. Phase 1 is individually rational for Compass and collectively inefficient for the market.

Posner layer: The legal system evaluates whether exploitation produces net harm or net efficiency gain. Compass’s 3-Phased Marketing (3PM) statistics — 2.9% higher close price, 20% faster offers — describe seller-level outcomes, not market-wide welfare. Compass cannot sustain a Posner-layer defense without producing measurable consumer welfare evidence at market scale. System classification: borderline exploitative equilibrium shifting toward legal correction.

CDT Foresight Predictions

Legal correction is likely if courts find selective exposure reduces market-wide efficiency

Compass’s strategy survives only if it produces net welfare gains at market scale, not seller-level statistics

MLS cooperative structure remains the dominant equilibrium regardless of litigation outcome

VISION FUNCTION III Chicago Strategic Game Theory

Delay-Dominant Equilibrium Classification

System Interpretation

The system exhibits a delay-dominant equilibrium. Compass fragments litigation to avoid correlated failure. NWMLS defers to the procedural posture Compass selected. Courts delay merits resolution through standard sequential adjudication. All players avoid early loss while preserving optionality — a posture that serves Compass’s narrative interests more than NWMLS’s evidentiary interests.

The equilibrium breaks at summary judgment, where deferred factual questions cannot be avoided. The cross-case strategic interdependencies between the NWMLS and Zillow litigations — and why they must be evaluated as a unified coordination-degrading strategy rather than isolated disputes — are formally developed in the MindCast Coasean Coordination Problem Part V. Compass abandons fragmentation only if early adverse signals accumulate to the point where maintaining multiple litigation fronts exceeds the benefit of narrative preservation. The 39-day interval between the NWMLS and Zillow filings — identified in prior MindCast analysis as evidence of coordinated strategic pressure rather than independent grievance — confirms that fragmentation was the deliberate architecture.

CDT Foresight Predictions

Litigation converges at summary judgment in the NWMLS case, approximately 18 to 24 months from current posture

Compass abandons fragmentation strategy if pre-summary-judgment adverse signals accumulate

NWMLS maintains stable defensive posture and benefits from delay as the factual record develops

VISION FUNCTION IV Cybernetic Control Vision

Closed-Loop Institutional Feedback

System Interpretation

The system exhibits closed-loop control architecture: Compass innovation triggers NWMLS restriction, which triggers legislative response, which triggers Compass adaptation, which restarts the loop. Control authority has progressively shifted from private actors toward the institutional layer as each cycle completes. SSB 6091 represents the state policy layer asserting control node dominance.

Compass’s adaptation velocity — the seven circumvention vectors documented in MindCast’s Plan B analysis — generates its own evidentiary record that feeds back into the judicial interpretation of intent and purpose. Feedback latency decreases as enforcement mechanisms mature post-June 2026.

CDT Foresight Predictions

State policy becomes the dominant control node post-June 2026 enactment

Feedback latency decreases as SSB 6091 enforcement accumulates observable signals

Compass post-enactment circumvention behavior enters the judicial record as intent evidence during discovery

VISION FUNCTION V Field-Geometry Reasoning

Structural Constraint Mapping

System Interpretation

Outcomes in the Compass litigation are governed primarily by structural field geometry rather than strategic intent or narrative strength. The dominant structural constraints are MLS network effects, Zillow’s demand concentration in the online home search layer, and legal transparency pressure crystallized into statutory form through SSB 6091.

Compass cannot scale the selective exposure model under current market structure. The Private Exclusive strategy requires a demand-side aggregator willing to surface Phase 1 listings to buyers. Zillow’s LAS removes that aggregator. NWMLS’s Rule 2 removes the supply-side infrastructure. SSB 6091 removes the regulatory permission structure. The Compass-Redfin-Rocket partnership inserts a substitute aggregator — but one whose prior public commitments contra Compass’s model are already in the legislative and judicial record. The Part V joint-evaluation framework establishes why granting relief in either the NWMLS or Zillow case raises coordination costs across the entire residential real estate market, not merely within the forum where relief is sought.

CDT Foresight Predictions

Compass cannot scale the selective exposure model under current structural geometry

Market converges toward full-disclosure equilibrium driven by platform, MLS, and statutory pressure simultaneously

Litigation outcome follows structural constraints, not narrative strength or procedural wins

VISION FUNCTION VI Strategic Behavioral Coordination

Agent-Level Behavioral Dynamics

System Interpretation

The behavioral layer shows consistent patterns across agent types. Sellers prefer broad exposure over controlled exposure when forced to choose under uncertainty. Brokers follow dominant platforms and defect from strategies that create listing removal risk. Buyers gravitate toward aggregated visibility platforms with comprehensive inventory.

Compass adoption of 3PM declined from 39 percent of sellers in April 2025 to 22 percent in July 2025 following Zillow’s LAS announcement — a 44 percent adoption drop driven entirely by platform-level behavioral pressure before any court ruled on the merits. Post-SSB 6091 enforcement compounds that pressure further, eliminating the regulatory permission structure on which 3PM’s Phase 1 mechanics depend. Agent defection risk increases as regulatory uncertainty compounds platform-level disincentives.

CDT Foresight Predictions

3PM adoption continues declining under combined enforcement and platform pressure

Broker defection from 3PM increases if summary judgment timeline signals adverse outcome

Consumer multi-homing behavior reinforces comprehensive-inventory platforms as dominant, compressing Compass’s differentiation window

X. Integrated System Output: Convergence Classification

All six Vision Functions converge on a single system classification. Compass operates against structural, behavioral, statutory, and institutional constraints that uniformly favor transparency, coordination, and broad market access. No Vision Function identifies a dominant pathway to Compass prevailing on the merits at the current trajectory.

Falsifiable Predictions

The MAP CDT Foresight Simulation generates the following falsifiable forward predictions, each subject to confirmation or disconfirmation against observable signals:

Compass fails to establish monopoly power or per se group boycott on a developed factual record in the NWMLS case at summary judgment

NWMLS prevails at summary judgment or the case settles on terms that preserve MLS mandatory-sharing architecture

The cross-forum market definition inconsistency surfaces as a contested issue in NWMLS summary judgment briefing within 12 months

Compass’s 3PM adoption rate in Washington declines below 15 percent within six months of SSB 6091’s June 2026 effective date

Reffkin’s Zillow PI testimony is introduced in NWMLS discovery or summary judgment proceedings as evidence of Phase 1 mechanics and intent

Falsification Condition

The simulation output is falsified if Compass produces empirical evidence of measurable market-wide consumer welfare gains from selective listing exposure at scale — not seller-level transaction statistics, but welfare gains distributed across the full buyer-seller-agent system. No such evidence exists in the current record.

Probability Compass wins on the merits at summary judgment: Low to moderate. Probability NWMLS prevails or settlement preserves MLS architecture: High. Key trigger: empirical proof of consumer harm at market scale.

XI. The Structure Is Not Open

The litigation has not reached truth. Compass cleared the plausibility threshold — the procedural floor, not a merits finding. Procedural survival at the pleading stage is what Rule 12(b)(6) produces when allegations are facially coherent. Compass’s allegations were facially coherent. Compass survived.

The Zillow preliminary injunction denial demonstrates what happens when Compass’s theory faces adversarial testing on an actual evidentiary record. 268 days from filing to voluntary withdrawal. Zero judicial relief obtained at any stage. The Section 1 conspiracy theory collapsed for lack of agreement evidence after four days of witness testimony. The Section 2 monopoly theory collapsed because Compass’s own expert metrics were insufficient to establish the monopoly power element.

SSB 6091 accelerates structural convergence by aligning NWMLS with Washington’s legislative judgment and compressing Compass’s argument space. The Reffkin testimony creates a durable evidentiary anchor available to opposing counsel across both cases. The cross-forum market definition inconsistency creates a summary judgment vulnerability that discovery will surface. Compass’s own litigation generated the statutory framework now deployed against it in both the legislative and judicial arenas.

Six Vision Functions applied through the MAP CDT architecture converge on the same output: the system favors transparency, coordination, and broad access. Compass is operating against that structure, not within it. Compass must prove real market harm, resolve internal contradictions across forums, and overcome statutory alignment. If Compass cannot, the theory collapses at summary judgment with a more developed record, a more expensive litigation posture, and a public narrative that procedural wins built and substantive losses will dismantle.

The outcome remains open. The structure is not.

NWMLS LITIGATION PLAYBOOK

How to Force Compass’s Theory to Confront Its Own Record

A CDT Strategic Architecture for the Compass v. NWMLS Litigation Sequence

NWMLS’s optimal strategy is not to out-argue Compass. The governing objective is to convert Compass’s theory from plausible to testable to contradictory — and to control when and how truth is tested. Surviving the motion to dismiss preserves every defense, keeps the case in the Western District of Washington, and avoids any premature merits commitment — the correct first-move posture. The game now is a structured delay in which NWMLS allows Compass to accumulate record, then strikes decisively when the contradictions are fully locked.

NWMLS does not need to out-argue Compass. It needs to let Compass prove its own case — and fail doing it.

XII.I. Stay in the Rule-of-Reason Lane

NWMLS must avoid per se framing at all costs. Judge Whitehead already signaled doubt: Compass is not a rival listing service, and the classic group boycott hallmarks from PLS.com do not translate to a member brokerage seeking to withhold listings from the cooperative it belongs to. The per se path is where Compass’s theory is strongest, because it does not require a developed factual record. The rule-of-reason path is where NWMLS wins, because it requires Compass to prove market-wide harm on evidence.

Under rule-of-reason analysis, NWMLS’s procompetitive justification is cooperation, platform utility, and market-wide information efficiency — precisely the factual record that SSB 6091’s legislative findings have now pre-populated. NWMLS should emphasize at every procedural juncture that the MLS functions as infrastructure, not a gatekeeper: the entity that compels universal listing access so every licensed agent in Washington can compete for every property. That framing, sustained consistently, positions NWMLS as the neutral coordinator and Compass as the selective extractor.

XII.II. Expand the Factual Record: The Discovery Kill Zone

Compass has already created the evidence NWMLS needs. The discovery phase is not where NWMLS generates facts — it is where NWMLS surfaces the facts Compass generated and forces them into a single coherent record. Three primary discovery targets carry the most analytical weight.

Target 1: The Zillow PI Record

Reffkin testified under oath at the Zillow preliminary injunction hearing on four critical points that map directly onto the NWMLS case. He acknowledged that homes sell during Phase 1 without ever reaching the MLS. He confirmed that the Black Box architecture was deliberately designed to market Private Exclusives without triggering CCP rules. He enumerated the benefits of off-MLS marketing in terms that constitute a textbook free-rider admission — Phase 1 price discovery derives its value from the MLS pricing signal that Compass withholds inventory from generating. And he acknowledged that 94 percent of listings proceed to Phase 3 MLS listing, which establishes that the MLS is the destination Compass needs even when it withholds from it during Phases 1 and 2. The full Zillow preliminary injunction transcript is available by subpoena and positions as a natural target for discovery production.

Target 2: Internal Compass Documents

Compass’s internal strategy documents, pricing logic, and buyer-routing architecture are the evidentiary core of the free-rider and selective-extractor arguments. The MindCast Narrative Control Architecture publication documents that Compass operates a three-layer control system: operational restriction (staged visibility, internal buyer routing, dual-commission capture), linguistic translation (restriction reframed as seller choice and innovation), and institutional calibration (different language in courts, legislatures, investor calls, and consumer-facing channels). The divergence between those layers generates contradictory factual claims about the same business practice. Discovery requests should target the following: the internal MLS restrictiveness ranking (where NWMLS rated most restrictive on a 1–5 scale), the Anywhere acquisition integration strategy as it relates to Private Exclusive scaling, Q4 earnings guidance that treats Private Exclusive adoption as a revenue metric, and the consumer-facing Disclosure Forms that the MindCast analysis identifies as making factually inconsistent claims about buyer access.

Target 3: Adoption and Behavioral Data

Compass’s own adoption data confirms the behavioral thesis. 3PM adoption declined from 39 percent of sellers in April 2025 to 22 percent in July 2025 following Zillow’s Listing Access Standards announcement — a 44 percent behavioral reversal triggered entirely by platform-level pressure, before any court ruled on the merits. Compass’s argument that the 3-Phased Marketing Strategy (3PM) generates seller-choice value is undermined when sellers abandon it the moment a platform signals listing-removal risk. That behavioral pattern constitutes direct evidence that Compass’s strategy generates value only when all distribution channels are available — meaning Phase 1 is not an independently valuable seller service but a routing mechanism that depends on eventual MLS distribution for its commercial viability.

The discovery target is not to find damaging facts. The discovery target is to surface the facts Compass already created — across depositions, internal documents, and public filings — and force them into a single coherent record.

XII.III. The Deposition Layer: Nelson, Huff, and Skillman

The MindCast Narrative Control Architecture analysis identifies three individuals whose depositions carry specific strategic value for NWMLS in the Compass v. NWMLS litigation. As the analysis states: the Washington record captures the Compass institutional system operating without its managed messaging layer — making these witnesses analytically valuable precisely because they are local actors in a regional legislative fight, not national strategists managing enterprise exposure.

Cris Nelson — Pacific Northwest Regional Vice President

Nelson is the senior Compass executive who was present at both Washington State SSB 6091 legislative hearings on January 23 and January 28, 2026, and who chose not to testify while deploying Brandi Huff as Compass’s named witness. Nelson is the author of the documented public statements that form the core of the Compass seller-choice narrative in the Pacific Northwest — including the claim that 36 percent of Seattle homeowners working with Compass chose to pre-market as a Private Exclusive. Her deposition should establish: the internal decision-making process for who testified at SSB 6091 hearings and why Nelson did not; the content and purpose of Compass agent messaging campaigns deployed during the legislative fight; the internal ranking of NWMLS as most restrictive on the 1–5 scale and what operational decisions that ranking drove; and the relationship between Private Exclusive adoption metrics and Nelson’s performance incentives as Regional VP. Nelson’s public record establishes the Compass institutional position. Her deposition establishes whether that position reflects genuine seller-protection reasoning or commission-capture architecture.

Brandi Huff — Compass’s Named SSB 6091 Legislative Witness

Huff served as Compass’s designated broker-witness at both SSB 6091 legislative hearings — the individual Compass placed before the legislature to embody the seller-choice narrative. The MindCast Narrative Control Architecture analysis documents that the 17:1 undisclosed-to-disclosed affiliation ratio in SSB 6091 testimony reflects deliberate apparatus design: Compass operated coordinated lobbying infrastructure including pre-drafted agent messaging campaigns. Huff’s deposition should establish: whether her legislative testimony was scripted, coordinated, or reviewed by Compass legal or communications staff before delivery; what she was told about the purpose of her appearance and what Compass expected her testimony to accomplish; her understanding of Compass’s Private Exclusive commission economics at the time of her testimony; and whether she received any direct or indirect benefit from Compass in connection with her legislative appearance. Huff’s testimony before the legislature is already in the public record. Her deposition establishes whether that testimony was independent advocacy or managed institutional output — a distinction directly relevant to Compass’s procompetitive justification narrative.

Moya Skillman — Team Foster Luxury Broker, Compass Network

Skillman represents the transaction layer. As co-lead of Team Foster — the high-volume luxury brokerage team whose transactions form the ground-level evidentiary core of MindCast’s dataset, including MLS #2362507 (the $15M transaction in which Team Foster captured both listing and buyer-side commission simultaneously) and MLS #2392995 (the $79M Triptych marketed as “Call for Address”) — Skillman’s professional activity sits at the intersection of the commission-capture architecture and the seller-choice narrative. Her public statement to the Puget Sound Business Journal applying Reffkin’s MLS-targeted “seller choice” framing to SSB 6091 — a state licensing statute, not an MLS rule — illustrates how the Compass institutional narrative exports to agents without the category correction that enterprise-level messaging would supply. Skillman’s transaction-level activity provides a pathway for opposing counsel to test the mechanics of how Team Foster identifies, routes, and closes buyer leads during Phase 1 and Phase 2; the commission structure on dual-capture transactions including MLS #2362507; what disclosure, if any, seller clients received about the buyer-routing architecture before signing listing agreements; and whether Skillman’s understanding of “seller choice” aligns with what Compass’s federal antitrust filings describe as the purpose of the Private Exclusive model. Skillman’s testimony connects the transaction-level data to the corporate narrative — and tests whether the narrative survives contact with the commission economics it describes.

Nelson, Huff, and Skillman are not peripheral witnesses. Each occupies a different layer of Compass’s three-layer control system — and each operated without enterprise-level message management in the Washington legislative fight. Their roles encode the contradictions. Discovery surfaces them.

XII.IV. Lock In the Free-Rider Framing

The free-rider argument is NWMLS’s strongest weapon at summary judgment and the one Compass is least equipped to rebut. The mechanism is precise: Compass withholds listing inventory from NWMLS during Phase 1 while simultaneously consuming the MLS price discovery signal through IDX data feeds. Phase 1 price discovery derives its value from the market-wide pricing baseline that mandatory sharing generates. Compass extracts that baseline signal without contributing to it during the phase in which extraction matters most.

The Chicago School doctrinal framing supports NWMLS: anti-free-riding rules imposed to protect cooperative investment are procompetitive under rule-of-reason analysis when the restriction is reasonably tailored to the coordination problem. NWMLS’s Rule 2 is precisely that restriction — mandatory contribution to the shared listing infrastructure as the condition of accessing shared listing data. Reffkin’s sworn testimony establishes the mechanism. Compass’s own IDX data consumption establishes the extraction. The Coase-layer analysis supports the infrastructure framing: MLS functions as a high-trust coordination mechanism with low transaction costs for shared listings. Compass’s selective-exposure model degrades that coordination infrastructure while continuing to benefit from it.

The free-rider argument structures naturally into three sequential steps at summary judgment: first, establish the mechanism from Reffkin’s testimony (Phase 1 withholds inventory; Phase 1 price discovery uses MLS signal; Compass pulls IDX while withholding); second, establish the procompetitive justification for Rule 2 using SSB 6091’s legislative findings as the market-structure predicate; third, require Compass to demonstrate that the net welfare effect of Phase 1 at market scale — not seller-level transaction statistics — outweighs the coordination cost. Compass has not produced that evidence. Compass cannot produce that evidence on the current record. That is the summary judgment kill condition.

XII.V. Deploying SSB 6091 — The Right Frame

SSB 6091 is a powerful evidentiary asset if deployed correctly and a credibility risk if deployed incorrectly. NWMLS should not argue that the statute makes its rules legally correct — that argument conflates legislative policy with antitrust doctrine and invites Compass to litigate preemption. NWMLS should instead argue that SSB 6091 confirms the market-structure concerns that justify Rule 2 as a procompetitive constraint.

The argument runs as follows: the Washington legislature conducted hearings, received testimony, reviewed transaction data, and made a finding that concurrent public marketing of residential listings is required to protect market-wide information efficiency. That legislative finding is not controlling on the antitrust question, but it constitutes a market-structure determination by a co-equal branch of government with access to the same transaction record NWMLS is introducing. Under the Amex framework, Compass must demonstrate anticompetitive effects on the market as a whole — not just on Compass as a competitor. The legislature’s 141–1 finding is the market-as-a-whole determination. Compass must rebut it with empirical evidence, not narrative.

SSB 6091 also carries a timing argument that NWMLS should preserve. The Compass-Redfin-Rocket partnership announced February 26, 2026 — while the House Rules Committee held the SSB 6091 scheduling gate — eliminated the market self-correction argument Compass had been running in legislative forums. The same week Compass announced a 60-million-user distribution partnership for Private Exclusives, the legislature voted 92–1 to ban the practice. That simultaneous timing is not coincidence. The legislative record reflects it — and that record is already in evidence as a matter of public law.

XII.VI. Attack on Three Fronts Simultaneously at Summary Judgment

Compass’s three structural vulnerabilities — the internal contradiction, the cross-forum market definition inconsistency, and the consumer harm failure — are mutually reinforcing. Presenting them simultaneously, rather than sequentially, denies Compass the ability to compartmentalize its defense and forces the court to confront the pattern rather than the arguments in isolation.

Front 1: The Internal Contradiction

Compass must answer a question it cannot answer coherently: if selective exposure is anticompetitive harm when NWMLS imposes it, what makes selective exposure innovation when Compass imposes it? The 3PM strategy restricts listing distribution to Compass agents during Phase 1. Rule 2 requires universal sharing. Compass’s theory requires the court to hold that the more restrictive distribution arrangement — Compass’s internal-only Phase 1 — is procompetitive, while the less restrictive arrangement — mandatory MLS sharing with all licensed agents in Washington — is anticompetitive. That inversion is the heart of the contradiction. The contradiction frames as a legal inconsistency, not a factual dispute — a distinction that matters for how the court resolves it.

Front 2: The Market Definition Inconsistency

Compass argued national market in Zillow — online home search platforms operate nationally, national pricing, national policy. Compass argues Seattle/King County market in NWMLS. Both cases involve the same 3PM strategy, the same conduct, and the same product. Dr. Aron’s national market testimony from the Zillow preliminary injunction hearing sits in the federal record available by subpoena. The judicial estoppel argument is available as a motion, and in the alternative, the inconsistency functions as a credibility attack on Compass’s market definition expert — a plaintiff whose geographic market theory shifts between forums based on which framing produces market power allegations has defined a litigation-convenient market, not an economically coherent one. A plaintiff whose geographic market definition shifts between national and hyper-local based on which framing produces market power allegations has defined a litigation-convenient market, not an economically coherent one.

Front 3: The Consumer Harm Failure

Compass bears the burden of demonstrating harm to competition — not harm to Compass. The antitrust laws protect competition, not competitors. On the current record, Compass has produced seller-level transaction statistics showing higher close prices and faster offers for 3PM listings — data that describes outcomes for individual sellers, not welfare effects across the full market. NWMLS should demonstrate that those statistics do not establish market-wide consumer welfare effects. 94 percent of 3PM listings eventually reach the MLS, establishing that MLS listing is the terminal condition for virtually all Compass sellers. Output has not been reduced — listings still reach the market. Prices have not been elevated — Compass’s own data shows that 3PM listings close higher, which benefits sellers but says nothing about buyer welfare or market-wide information efficiency. Quality has not been diminished on the evidence Compass has produced. All three channels of competition harm that Rule of Reason step one requires are unestablished on the current record.

XII.VII. Procedural Timing: Delay, Then Strike Decisively

NWMLS should not rush summary judgment. The record improves for NWMLS with every month of discovery. Compass’s contradictions accumulate in documents, deposition testimony, and public statements — including Reffkin’s ongoing social media output, which the MindCast analysis establishes meets the Signal Suppression Equilibrium (SSE) condition for narrative distortion: Access Dependence × Reputational Retaliation Risk × Information Fragmentation × Narrative Distortion > Signal Aggregation Capacity. Every LinkedIn post Reffkin publishes characterizing litigation outcomes is a potential party admission under Federal Rule of Evidence 801(d)(2).

The optimal timing strategy is full discovery followed by a comprehensive summary judgment motion that collapses all three Sherman Act theories simultaneously. Section 1 fails because no unreasonable restraint exists under rule of reason once the free-rider mechanism, the procompetitive justification, and SSB 6091’s market-structure findings are in the record. Section 2 fails because NWMLS’s market power, even at near-100 percent of the Washington MLS market, does not constitute monopoly maintenance when the market’s dominant architecture is cooperative infrastructure with mandatory sharing rules that benefit all members. The tortious interference claims fail because NWMLS’s enforcement of Rule 2 is, at worst, good-faith enforcement of contractual obligations Compass accepted as a member — and the legislative record now confirms the enforcement as a statutory transparency obligation.

XII.VIII. Settlement Architecture

NWMLS holds settlement leverage that increases with time. Compass carries approximately $2.6 billion in post-merger debt following the Anywhere Real Estate acquisition and has never posted a full-year GAAP profit. The litigation cost of a multi-year federal antitrust case — estimated at $2 to $4 million expended in the Zillow case alone over eight months — compounds against a balance sheet that depends on Private Exclusive revenue as a solvency mechanism. As the MindCast analysis documents, Compass’s rhetorical intensity tracks balance-sheet constraints: narrative escalation marks the sequential exhaustion of forums as each closes.

An optimal settlement preserves mandatory-sharing architecture, gives Compass narrow operational flexibility as a face-saving concession, and forecloses adverse per se precedent that would constrain both parties in future Washington MLS governance disputes. NWMLS’s leverage is not that it will win at trial — though the structural analysis suggests that is the most probable outcome. NWMLS’s leverage is that Compass cannot afford to lose, and the record that discovery generates makes losing progressively more probable with each passing month.

NWMLS’s leverage increases with time. Compass’s balance sheet, its debt service obligations, and its accumulating evidentiary record all move in NWMLS’s favor as the litigation clock runs.

XII.IX. What NWMLS Must Avoid

Overplaying cooperative power: NWMLS should never frame itself as a gatekeeper. The consistent positioning is infrastructure — the neutral coordinator that ensures every licensed agent in Washington can compete for every listing. Any tone that reads as anti-Compass rather than pro-market undermines the framing and hands Compass the narrative it needs.

Moral arguments: Fairness rhetoric is a losing register in antitrust litigation. NWMLS should stay in the efficiency, coordination, and output vocabulary throughout. The argument is not that Compass is wrong. The argument is that Compass is free-riding on shared infrastructure while claiming the infrastructure is anticompetitive.

Early summary judgment: A premature motion risks an incomplete record and missed contradictions. The full value of the Nelson, Huff, and Skillman depositions, the internal Compass documents, and the post-SSB 6091 circumvention behavior requires time to develop. Patience is the strategic asset.

Litigating the per se question: The per se path gives Compass its best theory. NWMLS should consistently push toward rule-of-reason analysis, where the procompetitive justification is strong and the consumer harm burden falls on Compass.

XII.X. Synthesis: The Clean Architecture

NWMLS’s optimal strategy is a four-phase execution: stay in the rule-of-reason lane and let Compass litigate the weaker per se theory; expand the factual record through targeted discovery of the Zillow PI transcript, internal Compass documents, and the Nelson/Huff/Skillman deposition sequence; deploy SSB 6091 as market-structure confirmation rather than legal authority; then strike at summary judgment with all three Sherman Act theories collapsing simultaneously under the weight of the accumulated record.

Compass’s theory survives the pleading stage because courts accept allegations as true. Discovery transforms that survival into a liability: the record Compass already generated constrains the defenses it can now raise. At summary judgment, the internal contradiction, the cross-forum market definition inconsistency, and the consumer-harm failure converge simultaneously — and no single legal theory can answer all three coherently at once. Compass built the trap. NWMLS needs only to close it.

Convert Compass’s theory from plausible to testable to contradictory. Control when and how truth is tested. Let Compass prove its own case — and fail doing it.