MCAI Lex Vision: The Compass-Redfin Alliance, Market Self-Correction Is Dead

What the February 2026 Rocket–Compass–Redfin Partnership Means for State Legislators and Attorneys General

See companion publications Platform-Mediated Price Discovery, A Runtime Measurement Framework for the Compass–Redfin–Rocket Architecture, The Compass Collapse– A Post Washington SSB 6091 Passage Reckoning series

On February 26, 2026, Rocket Companies, Compass International Holdings, and Redfin announced a three-year strategic alliance. Compass Coming Soon listings began appearing on Redfin immediately, with Private Exclusives to follow. Sixty million monthly visitors. Leads flowing exclusively to Compass agents. No days on market. No price history. No valuation estimates. No referral fee.

George Stigler wrote in 1971 that regulation is “acquired by the industry and is designed and operated primarily for its benefit.” Rocket acquired Redfin. Call it what it is: a balance-sheet response to a closing regulatory window — executed at zero cash cost by a firm carrying $3 billion in post-merger debt — and it eliminates the only remaining argument against transparency legislation: that the market would self-correct.

Two frameworks predicted this outcome before it materialized. Tirole's two-sided market architecture identified why the pledge was structurally unstable: Redfin monetizes buyer lead volume, not listing data quality, so accepting information-stripped listings costs the platform nothing while serving Compass's commission capture model. Jean Tirole & Jean-Charles Rochet, Platform Competition in Two-Sided Markets, Journal of the European Economic Association, Vol. 1, No. 3, pp. 990–1029 (June 2003). Competitive pressure was never pointing toward enforcement of the pledge — it was pointing toward the deal announced February 26. The Nash-Stigler constraint The Dual Nash-Stigler Equilibrium Architecture identified why voluntary firm-level correction cannot substitute for legislation: the strategy that generates sufficient revenue to matter is the strategy that generates sufficient evidence to end it, but ending it voluntarily requires forfeiting the revenue permanently. No firm sustains that. Rocket's acquisition didn't create the structural instability in Kelman's pledge. It removed the reputational constraint that had temporarily obscured it.

Every prior MindCast analysis predicted the structural logic that produced this announcement. The timestamps prove it. What follows documents what the announcement means for state legislators, state attorneys general, and the litigation calendar that was already running before February 26.

If the structure persists, then:

The state ratchet closes the Layer 3 window jurisdiction by jurisdiction, eliminating the operating condition the Anywhere acquisition premium requires.

The Redfin platform pivot buys Compass one to two earnings cycles of narrative cover — but not structural relief.

Goodwill impairment becomes a timing question, not a conditional one.

The cross-forum litigation posture weakens with each quarter the contract runs.

Multi-state AG coordination becomes analytically rational, with Washington’s evidentiary record as the shared foundation.

I. The Reversal That Ends the Debate

In April 2025, Redfin CEO Glenn Kelman pledged publicly to ban listings selectively pre-marketed without MLS exposure. Redfin set a September 2025 enforcement date. Rocket’s $1.75 billion acquisition closed, and the pledge reversed within months. Kelman departed. Redfin’s February 26 statement: “Our perspective evolved.”

Stigler’s capture theory — The Theory of Economic Regulation, Bell Journal of Economics and Management Science, 1971 — predicts exactly this sequence. Regulatory behavior tracks ownership, not stated mission. Redfin didn’t abandon its transparency pledge because its values changed. Rocket acquired the institution, and the institution’s behavior realigned with Rocket’s interest structure. The institution changed. The pledge reversed. The mechanism confirmed.

MindCast AI’s Tirole Phase Analysis, published January 23, 2026, framed the same dynamic through Tirole’s two-sided market architecture: Redfin monetizes buyer lead volume, not listing data quality, so accepting information-stripped listings costs Redfin nothing while serving Compass’s commission capture model. The Tirole framing explains why the deal is rational for Redfin economically. The Stigler framing explains why the pledge reversal was predictable institutionally. Both mechanisms confirmed simultaneously.

The significance extends beyond Redfin specifically. The self-correction argument has a specific procedural function in state legislative hearings — and February 26 destroys that function, not merely its credibility.

In every prior session where concurrent marketing legislation was introduced, industry opponents deployed market self-correction as the primary defense for inaction. The argument worked because it gave fence-sitting legislators a procedurally defensible reason to defer: the market is already moving, voluntary action is underway, legislation is premature. Redfin’s April 2025 pledge was the argument’s primary exhibit. Compass opponents cited it in Washington’s January 2026 Senate hearing. Legislative staff referenced it in committee analysis. Kelman’s own words — a sitting CEO of the second-largest portal publicly committing to ban the practice — gave the self-correction argument the institutional weight it needed to justify delay.

Now trace what happened to that exhibit. Kelman recognized the consumer harm — the pledge itself is an admission that harm exists. Rocket acquired Redfin. The pledge reversed within months. The reversal had nothing to do with new evidence about consumer welfare. Ownership changed, and the institution’s behavior followed ownership — exactly as Stigler’s 1971 framework predicted. A committee chair who invokes self-correction today must defend the proposition that a pledge that reversed four months after a corporate acquisition represents ongoing voluntary market discipline. No legislator can hold that position once handed the Kelman timeline in a hearing.

The Compass partnership compounds the destruction. Redfin didn’t merely reverse its pledge. Redfin became the primary national distribution infrastructure for the practice it pledged to ban — under a three-year contract, at zero cost to Compass. The self-correction argument required believing that competitive market pressure would discipline information suppression. February 26 produced the largest single-day expansion of information suppression infrastructure in the industry’s history, executed by the platform that was supposed to be the market’s corrective mechanism.

Every state legislature that has faced the “market self-corrects” argument now has the answer in a press release dated February 26, 2026. The second-largest real estate search portal became the primary distribution infrastructure for the practice the first platform is still banning. The argument doesn’t lose credibility. It loses its primary exhibit and acquires a contradicting one — a signed three-year contract, in the opposite direction, published by the exhibit itself.

II. What the Partnership Actually Proves

The contract terms are worth reading carefully, because they reveal the architecture precisely.

Per Compass’s own partnership page, Compass listings on Redfin display with no days on market, no price drop history, and no home valuation estimates. Those are not the seller’s data points. They are the buyer’s. Stripping them from the buyer serves the brokerage’s commission capture architecture — not the seller’s interest in maximizing competitive exposure. All buyer inquiries route directly to Compass agents with no referral fee. Rocket Mortgage preferred pricing — a 1-point first-year rate reduction or up to $6,000 lender credit — is available exclusively to Compass clients. One million buyer leads flow to Compass agents over the partnership term at zero acquisition cost.

Wider distribution of an information-stripped inventory — all lead flow captured internally, mortgage origination bundled exclusively to Rocket’s platform.

The Compass Commission Consolidation Strategy, published February 19, quantified what that architecture produces at the transaction level: $4.2 million in captured buyer-side commission from Seattle’s ultra-luxury market across 130 transactions over thirteen months. The Category D analysis in that publication identified the specific mechanism the Redfin partnership now targets at national scale — transactions where Compass held the listing and an independent broker won the buyer-side commission because the listing reached the open market. Windermere East won that competition seven times in the dataset. Under the Redfin architecture, those same buyers contact a Compass agent first through the Redfin platform, eliminating Windermere’s competitive entry point before the property ever reaches the MLS. The Redfin partnership is a direct structural attack on every Category D outcome in the dataset — not just in Seattle, but across 35 major markets simultaneously.

The Address Suppression Calculus, published February 22, identified the Nash-Stigler constraint governing address suppression at the team level: “The strategy that generates sufficient revenue to matter is the strategy that generates sufficient evidence to end it.” No price threshold existed where Team Foster’s architecture simultaneously generated revenue material to Compass’s debt service and avoided the detection threshold that triggers NWMLS enforcement. The Redfin partnership is Compass attempting to escape that trap by moving from team-level routing to platform-level distribution — substituting Redfin’s 60 million monthly visitors for the address field suppression that NWMLS constraints made untenable at scale. The Nash-Stigler constraint doesn’t disappear at the platform level. It migrates upward to the state legislative and federal enforcement tiers where the Redfin contract now operates.

The operational confirmation arrived the same day as the press release — from inside the suppression architecture the Address Suppression Calculus documented.

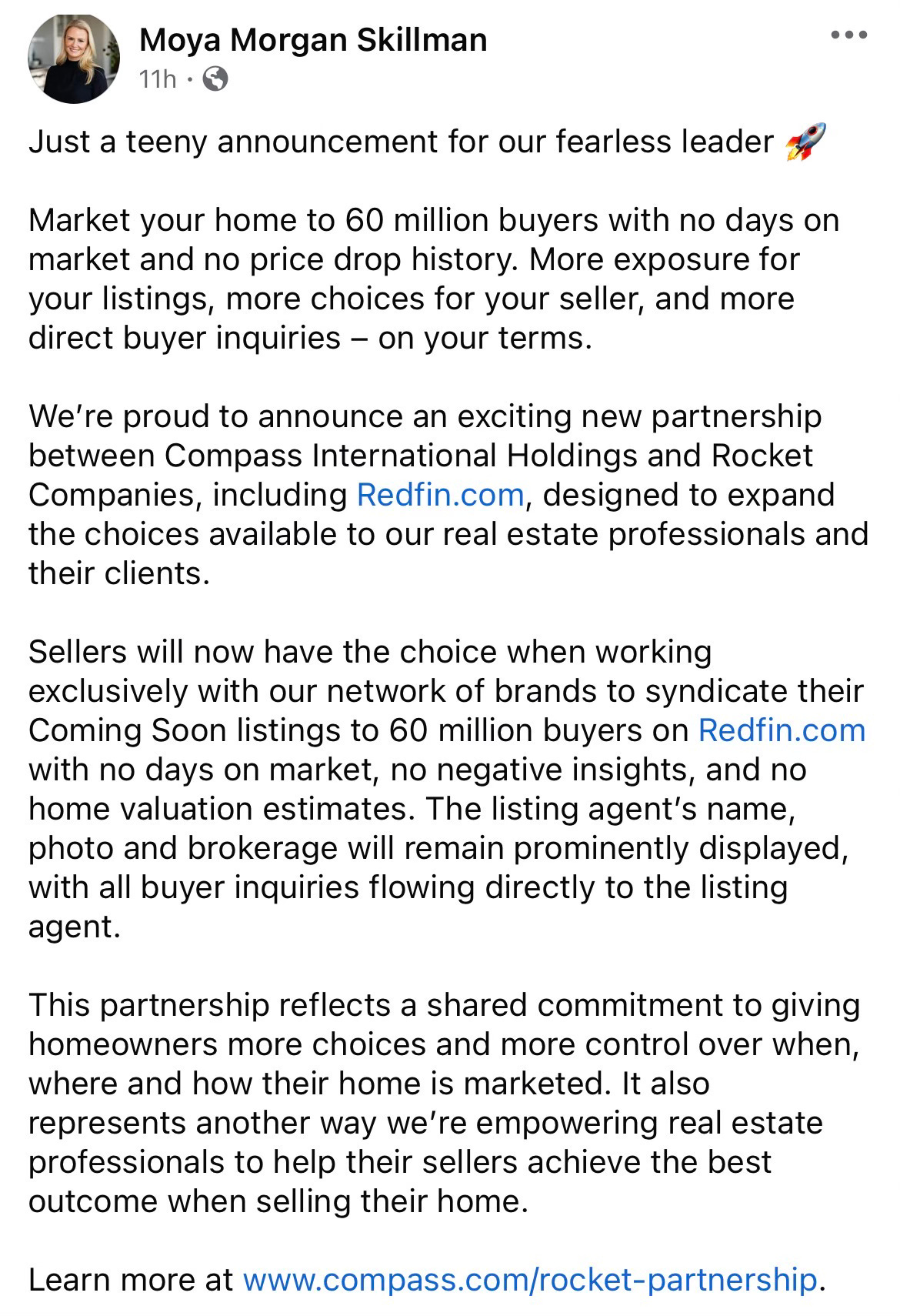

Moya Morgan Skillman, a Team Foster agent, posted two items on February 26. The first announced the Compass-Redfin partnership to her network with language that reveals the intended audience: “More direct buyer inquiries — on your terms.” No days on market. No price drop history. No negative insights. “Your terms” is agent-facing framing, not seller-facing. Sellers seeking maximum competitive exposure don’t need to be told their listing will display without negative insights. Agents seeking to control buyer information do.

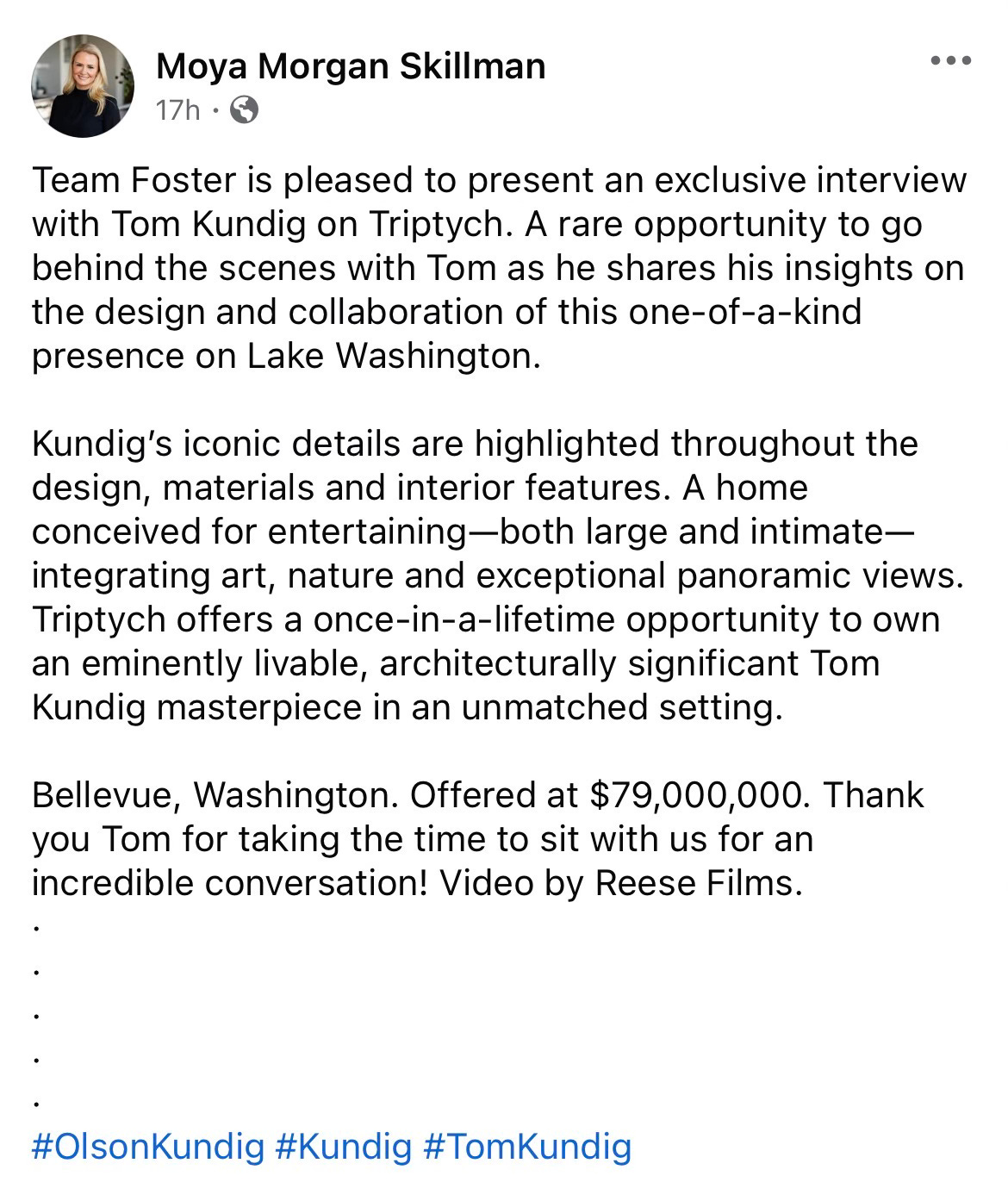

The second post marketed Triptych — MLS #2392995, the $79 million Lake Washington estate documented in the The Address Suppression Calculus as the anchor of Team Foster’s suppression portfolio, listed without a street address — through an exclusive architect interview with Tom Kundig, produced by Reese Films. Sophisticated content marketing designed to generate buyer inquiry through Compass’s internal network before broad MLS exposure. The Redfin partnership is the next distribution layer for exactly this inventory.

Both posts together confirm what the structural analysis predicted: the Redfin partnership is being deployed on the same inventory, by the same agents, using the same suppression architecture the Address Suppression Calculus documented in February — now with 60 million monthly Redfin visitors as the distribution vehicle. The Nash-Stigler constraint didn’t disappear. It scaled.

Compass broker Moya Morgan Skillman, Team Foster, announces the Redfin partnership on February 26, 2026 — framing suppressed buyer data as a seller benefit and routing all inquiries to the listing agent. Public Facebook post.

Skillman markets MLS #2392995 — the $79 million Lake Washington estate documented in the Address Suppression Calculus as Team Foster's anchor suppression listing — through an exclusive architect interview designed to generate internal buyer inquiry before broad market exposure. Public Facebook post, February 26, 2026.

The same broker. The same property. The same suppression architecture. On the same day Compass issued a press release framing the Redfin partnership as a seller-choice initiative, a Team Foster broker posted it to her network as a tool for controlling buyer information — and marketed the Address Suppression Calculus's primary exhibit through content designed to route buyers internally before the market sees it. February 26 didn't just confirm the structural analysis. It confirmed who executes it, on what inventory, and with what pitch.

February 26 didn't just confirm MindCast’s structural analysis. It confirmed who executes it, on what inventory, and with what pitch. Redfin's 60 million monthly visitors aren't an open market — they're the entrance to Compass's walled garden, where buyers arrive stripped of price history, sellers believe they're getting premium exposure, and every inquiry routes to a Compass agent before the market ever sees the property.

III. The Layer 3 Confirmation

MindCast AI’s Three-Layer Acquisition Hierarchy decomposed the $1.6 billion Anywhere acquisition price into three value layers. Layer 1 is standalone brokerage value — agent networks, brands, transaction volume. Survives any regulatory change. Layer 2 is scale synergies — technology integration, cross-brand referrals, recruiting leverage. Also survives transparency legislation. Layer 3 is the private exclusive infrastructure premium — estimated at $400–800 million — which exists only if listings can be withheld from the open market long enough for an internal buyer to arrive first, capturing both commission sides.

Compass just confirmed Layer 3 in its own commercial language, in a signed contract, published in a press release. Robert Reffkin’s statement: sellers deserve the freedom to list without “misleading insights that damage value.” Not brand consolidation language — Layer 3 language — simultaneously available to every auditor testing goodwill assumptions, every state legislature advancing concurrent marketing bills, and every federal court examining Compass’s antitrust claims.

The 42-Day Collapse Framework, published February 21, characterized Layer 3 as a solvency argument, not a seller-choice argument. The Redfin deal makes that characterization unchallengeable. A firm defending a seller-choice preference does not structure a three-year national platform deal around it. A firm defending a balance-sheet necessity does. Compass carries $2.6 billion in assumed Anywhere debt, has never posted a full-year GAAP profit, and has quarterly debt-service obligations compressing its profit horizon. The partnership costs zero cash — the only kind of distribution deal available to a firm in that position.

The merger created the debt. The debt requires the dual commissions. The dual commissions require the private exclusive window to stay open. Each state that closes that window tightens the financial constraint the merger itself created. The Redfin deal is Compass doing the only thing it can afford: trading listing inventory access for distribution reach without writing a check. Solvency geometry — confirmed in Compass’s own press release.

The Redfin deal also provides a market-implied valuation that MindCast’s Seattle dataset didn’t have. Compass just structured a three-year national platform deal anchored entirely on its exclusive listing inventory. If Rocket’s $1.75 billion acquisition of Redfin was premised on the Compass listing inventory as the primary driver of partnership value — which the press release structure strongly implies — the market is implicitly pricing the Layer 3 premium at the upper end of the $400–800 million range, not the lower end. The Stigler Equilibrium, published January 20, draws the precise distinction the Redfin deal makes concrete: captured enforcement enables private coercion to substitute for price competition. Compass isn’t competing on agent quality, listing exposure, or seller outcomes. Compass routes buyers through walled gardens — Redfin’s 60 million monthly visitors feeding Compass agents, Rocket’s mortgage integration bundled exclusively to Compass clients, address suppression at the team level below the detection threshold. Private coercion substituting for price competition, funded by $2.6 billion in acquisition debt that competitive capital markets would never have extended to a firm that has never posted a full-year GAAP profit on competitive merit alone. The debt is the diagnostic: capital markets funded the Anywhere acquisition because the projected return was routing capture, not competitive performance. The Redfin deal is that thesis executing in real time.

Revising the Layer 3 premium upward carries a direct implication for goodwill impairment: the larger the premium, the larger the impairment exposure when the regulatory ratchet closes the window state by state.

IV. The MindCast Prediction Record

The analytical value of MindCast’s corpus is not that it can describe what happened. It is that the structural logic was predictable before the outcomes materialized — and was published with timestamps.

The Shadow Antitrust Trifecta, published February 13, named Deputy AG Todd Blanche, DOJ Chief of Staff Chad Mizelle, and lobbyist Mike Davis by structural role in the Compass-Anywhere merger bypass architecture. The Warren letter named all three in a congressional demand to the Attorney General six days later.

How MindCast AI Predicted the Slater Ouster documented nine of ten falsifiable predictions confirmed on the day Gail Slater was removed from the DOJ Antitrust Division — including the specific prediction that boundary-asserting staff would be removed before structural reform could occur, published nineteen days earlier.

Nineteen Senators, Seventeen Questions, published February 20, mapped the Warren letter’s seventeen questions as a falsification board against the merger clearance process — documenting how each question eliminates the possibility of a coherent institutional defense regardless of how it is answered. The publication named the three March deadlines — AG Bondi’s congressional response due March 5, the Live Nation trial beginning March 2, and the Davis deposition in the Pitts HPE-Juniper proceedings — as simultaneous constraint events. All three are still running.

The Tirole Phase Analysis predicted the Redfin reversal mechanism before Redfin reversed. The 42-Day Collapse Framework characterized the deal’s structure before the deal existed. The Layer 3 solvency argument quantified the balance-sheet necessity that the Redfin press release confirmed in Compass’s own language. The Redfin partnership is Day 48 of the 42-day framework. The depositions have not yet begun.

V. Is the Partnership Currently Legal in Washington?

The short answer: probably yes as structured today. The more important answer: SSB 6091 changes that calculus materially across three specific legal friction points.

The partnership’s own language is designed for legal defensibility. Written seller consent is required. Listings are publicly marketed on two platforms. Compass claims MLS compliance. Deliberate legal architecture produced that threading of the needle — nothing incidental about it. Under current Washington law, a listing displayed on two platforms with seller consent doesn’t meet the traditional definition of a pocket listing.

SSB 6091 shifts the analysis on three points.

First, if the bill establishes that withholding days on market and price history from buyers constitutes a material omission, then Redfin displaying Compass listings stripped of that data — while showing it for every other listing — creates a two-tiered information environment that could constitute an unfair or deceptive trade practice under the CPA. The disparate treatment is the legal hook, not just the omission itself. Washington courts have found CPA violations where the deceptive act is structural — and this architecture qualifies.

Second, Washington’s agency disclosure requirements under RCW 18.86 create exposure when Compass agents receive all buyer leads from Redfin inquiries. When those same agents represent sellers whose listings are information-suppressed, the prior disqualification problem the Commission Consolidation Strategy documented in the Mercer Island Exhibit Transaction — four role designations, two agents, both sides — replicates at platform scale. SSB 6091’s transparency provisions tighten that exposure further by establishing what disclosure was required.

Third, the Rocket Mortgage integration — preferred pricing exclusively through Compass agents, mortgage products embedded into Compass’s platform, buyer leads routed from Redfin — is a vertical tying arrangement. Washington’s CPA has been used in tying arrangements where market power is leveraged to foreclose consumer choice. Rocket is the nation’s largest residential lender. The tying question is worth scrutiny under that framework independent of RESPA.

Legal today. Potentially actionable under SSB 6091 and potentially actionable under existing law on the tying theory regardless of what the legislature does.

VI. Redfin’s Liability Architecture

Redfin’s exposure from this partnership is multilayered and arguably greater than Compass’s. Redfin operates in Washington as a licensed brokerage — not merely a passive platform — while simultaneously serving as a national search portal. Liability attaches at every level the partnership touches — compounded by the Kelman reversal documentary record Redfin cannot retract.

Washington Consumer Protection Act. A licensed brokerage actively curating a two-tiered information environment — Compass listings stripped of buyer data while every other listing displays it — is participating in information suppression, not merely hosting it. The Kelman reversal is the evidentiary anchor: Redfin’s own former leadership recognized the consumer harm publicly, then reversed course for commercial reasons after a corporate acquisition. Defending that sequence under RCW 19.86 is a difficult task. Washington’s AG Civil Rights Division confirmed UDAP enforcement authority exists for exactly this category of structural conduct at the January 2025 Senate hearing — a permanently discoverable legislative transcript now available to every AG office examining the same business model.

The Posner consumer welfare inversion and the pricing market distortion. Richard Posner’s Economic Analysis of Law(1973) established the framework Washington courts use to evaluate whether a challenged practice enhances or reduces total market welfare — not merely whether individual actors consented to it. The test isn’t whether the seller agreed. The test is whether the practice produces a net welfare gain or loss across all parties to the transaction.

Private exclusives fail that test structurally. A listing withheld from the MLS during a pre-marketing window produces information asymmetry by design. The seller’s agent controls timing, exposure, and competing offer generation. Buyers who arrive through the private channel negotiate without the market signal that MLS exposure produces — no competing bids, no days-on-market clock, no price reduction history. The brokerage benefits twice: first by controlling buyer access, then by capturing the buyer-side commission when an internal agent closes the deal. Posner’s framework identifies this as a wealth transfer dressed as a service — the seller believes they’re getting a curated, premium experience; what they’re actually getting is a constrained auction with fewer bidders and a predetermined buyer pipeline.

The Redfin partnership scales this mechanism nationally and makes it invisible. Every Compass listing on Redfin displays without days on market, without price history, without valuation estimates — while every competing listing on the same platform displays all three. Buyers comparing properties on Redfin don’t see suppressed data. They see a blank field where market intelligence should be. The information asymmetry isn’t disclosed. It’s designed into the platform architecture, normalized by the interface, and invisible to a buyer who has never seen what a complete listing looks like.

Stripping days-on-market data and price history from buyers isn’t a neutral act. Sellers already possess that information. Removing it from buyers transfers economic value from buyers to the brokerage by degrading the buyer’s price-discovery capacity. A buyer who cannot see that a listing sat for 90 days and dropped $200,000 negotiates from a structurally weaker position — and the commission differential that results flows to the brokerage, not back to the seller. Reffkin’s “no downside” framing inverts Posner’s consumer welfare standard directly — claiming that a practice which demonstrably reduces buyer information produces no welfare loss. That argument requires believing that degrading one party’s negotiating capacity, systematically, at platform scale, across 60 million monthly visitors, is welfare-neutral because the other party consented. Posner’s framework rejects that framing on efficiency grounds independent of statutory analysis. The welfare loss is real. The transfer is measurable. The Redfin contract just made it national.

RESPA Section 8. The Rocket Mortgage integration creates a three-party referral arrangement in settlement services that RESPA Section 8 was specifically designed to reach: Redfin routes buyer leads exclusively to Compass agents; those agents connect buyers to Rocket’s preferred pricing bundle; Rocket’s products are embedded into Compass’s platform. RESPA reaches “thing of value” exchanges, not only cash payments. One million buyer leads routed exclusively to Compass agents over three years is a quantifiable thing of value. CFPB enforcement authority is the operative instrument. Whether the arrangement triggers a formal enforcement action would depend on regulator analysis of the specific referral mechanics — but the structural predicate for scrutiny is present on the face of the contract. Adding a sixth enforcement sovereign to the architecture the 42-Day Collapse Framework identified — federal consumer financial regulation, operating independently of state legislative and antitrust proceedings.

Fiduciary duty to buyer clients. Redfin buyer’s agents in Washington are now structurally positioned to breach their RCW 18.86 duty on every Compass listing they show, because the information suppression is built into the platform infrastructure. The agent may not know they’re doing it, which does not eliminate liability — it amplifies it as a systemic practice. Systemic fiduciary breach at platform scale is a regulatory enforcement action, not individual case management.

The antitrust record reversal. Compass sued Zillow for antitrust conspiracy and named Redfin as a co-conspirator, alleging that coordination to ban private listings from search platforms harmed consumers. Redfin is now Compass’s distribution partner for those same listings. A plaintiff’s antitrust attorney challenging the Compass-Redfin structure — representing independent brokerages excluded from the preferred placement and lead flow — has Compass’s own litigation filings available to establish market power and anticompetitive effect. Redfin sits at the center of both sides of that record simultaneously. Redfin now sits at the center of both sides of that record simultaneously — a structural liability in the Southern District of New York case scheduled for trial in July 2026, not merely a credibility problem.

VII. What the Partnership Does to Active Litigation

Three active proceedings are directly affected by the Redfin announcement, and the effect runs in different directions for each.

Compass v. NWMLS — trial set June 8, 2026 in the Western District of Washington. Compass’s antitrust theory against NWMLS rests on the claim that NWMLS’s restrictive listing policies exclude Compass listings from market visibility, harming consumers and foreclosing competition. Securing distribution to 60 million monthly Redfin visitors weakens that theory materially. The “exclusion from market” argument becomes difficult to sustain when Compass voluntarily partnered with the second-largest portal. NWMLS’s lawyers will file a Notice of Supplemental Authority on the Redfin announcement before the week is out — following the same playbook they ran on February 6 when they cited the Compass v. Zillow preliminary injunction denial within hours of that ruling. Discovery is running live right now. Whatever NWMLS’s internal documents reveal about its listing policies will land in the public record on a timeline running parallel to SSB 6091’s House floor decision.

MindCast AI’s Litigation-Acquisition Monopolization Strategy analysis, published December 2025, predicted precisely this dynamic: “If blocked: Compass pursues alternative opacity strategies through portal partnerships.” Compass was not blocked — the merger cleared through a bypass architecture now under congressional investigation — but the prediction held anyway. The Redfin partnership is the portal partnership the December analysis forecast, executing on the same three-prong strategic logic: NWMLS litigation clears the mandatory submission requirement, Zillow litigation forces portal distribution of private listings, Anywhere acquisition provides national agent scale. The Redfin deal is the fourth node, converting predicted strategic fallback into operational platform architecture.

Compass v. Zillow — trial scheduled July 2026 in the Southern District of New York. The SDNY already denied Compass’s preliminary injunction on February 6, finding that “considered holistically, the record fails to show that Zillow possessed the power to exclude competition from the online home search market.” The Redfin deal compounds that finding: Compass has now demonstrated it can secure national platform distribution for its exclusive listings independently of Zillow. The exclusionary monopolization theory doesn’t survive a defendant showing the plaintiff just signed a competing distribution deal at scale.

Washington AG v. Zillow and Redfin — the FTC filed antitrust claims against Zillow and Redfin on September 30, 2025, over their rental market agreement, with Washington as one of five co-plaintiff states. Washington’s AG is simultaneously a plaintiff against Redfin in federal court and watching Redfin become the primary distribution infrastructure for the information suppression SSB 6091 was designed to prevent. The Stigler Equilibrium names what the DOJ clearance represents structurally: an Enforcement Capture Equilibrium producing outcomes with market aesthetic but without market function — behavioral remedies designed to evaporate, temporal arbitrage that let the merger consolidate before review concluded, information routing through Compass’s lobbying apparatus. The clearance wasn’t institutional error. It was the equilibrium output of a single decisive chokepoint facing concentrated merger benefits and diffuse consumer costs. Washington’s AG, operating outside that chokepoint entirely, is the institutional competition the Stigler framework identifies as the structural remedy.

No coincidence — the convergence is the structural argument for AG-level engagement with the Redfin partnership as a consumer protection matter independent of the federal antitrust proceeding. The AG office that is already litigating against Redfin federally has both the institutional standing and the factual record to act on the February 26 partnership domestically.

Contact mcai@mindcast-ai.com to partner with us on Law and Behavioral Economics foresight simulations. To create your own game theory simulation of data on Compass address suppression and private exclusives, upload the URL of this publication to any LLM (ChatGPT, Claude, Gemini, Grok, Perplexity) and prompt ‘develop MindCast framework with 3 degrees of cited sub links.’ Thereafter, all new information you upload is training data for your AI system. See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure for more info.

Related works: The Compass Commission Consolidation Strategy and Real Estate Marketing Transparency, How Compass Bought Its Antitrust Clearance, Dual Nash-Stigler Equilibrium Architecture, The Compass Narrative Inversion Playbook, Chicago School Accelerated: The Integrated

VIII. What the Partnership Means for SSB 6091

SSB 6091 passed the Washington State Senate 49-0 on February 10. Bipartisan. Zero amendments. Zero opt-outs. Zero absences. The House Rules Committee holds the only remaining gate.

The February 26 Compass-Redfin announcement provides every Rules Committee member a concrete, same-week example of exactly the market behavior the bill targets. Scheduling the bill clean carries lower political risk today than it did on February 25. The committee that delays it hands Compass the calendar death its lobbying operation failed to achieve through amendment — after the entire Washington State Senate declined to give it.

The bill’s opponents argued in committee that market self-correction was underway. Redfin’s pledge was the primary evidence. Today that evidence is a signed three-year contract in the opposite direction.

The Compass-Redfin architecture also creates a specific enforcement question that didn’t exist before February 26. Redfin operates in Washington as a licensed brokerage. A Redfin buyer’s agent in Washington showing a client a Compass listing is now showing that client a listing stripped of days on market and price history — data the agent knows exists, because every other listing on the same platform displays it. RCW 18.86 imposes a duty to disclose material facts. The suppression is built into the platform infrastructure. Systemic fiduciary exposure — not individual agent error — defines what Redfin has built. SSB 6091 closes the underlying mechanism. Without it, the exposure is structural and ongoing on a platform reaching 60 million monthly visitors.

The SSB 6091 Cross-Forum Analysis, published February 10, tracked the convergence of the 49-0 Senate vote and the SDNY preliminary injunction denial in the same calendar week — two institutional forums reaching the same structural conclusion independently. The Redfin announcement is the third forum, same week. Three simultaneous institutional confirmations of the same structural finding, in the same seven-day window, while the House Rules Committee holds the scheduling decision.

IX. Multi-State Legislative Implications

The Compass-Redfin partnership accelerates state legislative activity through three specific mechanisms that are more precise than political momentum.

The scale of the announcement eliminates the “niche practice” defense that has killed transparency legislation in prior sessions. Compass is no longer a brokerage-level actor defending a local market practice. It is the anchor tenant of a national platform architecture backed by Rocket’s balance sheet, covering 340,000 agents across six major brands, operational immediately across 60 million monthly visitors. Legislative staff in any state can open the Redfin website and see the suppressed listings. The harm is no longer theoretical. It is demonstrable with a browser and two tabs.

Rocket’s involvement as the nation’s largest residential lender changes the federal preemption question. RESPA exposure at the federal level — with CFPB as the enforcement vehicle — creates the same dynamic that has historically accelerated state legislative action: when federal enforcement is plausible but uncertain, states move their own legislation as a hedge. Expect AG offices in consumer-protection-active states — California, Illinois, Colorado, Minnesota — to be watching this closely. California is the most obvious accelerant: the California Association of Realtors and the state AG already have active tension with Compass over Private Exclusives, and a formal Redfin partnership triggering 500,000 suppressed listings provides the specific legislative hook California consumer advocates have been waiting for. Illinois matters because Chicago is Compass’s second-largest market and @properties — now a CIH subsidiary — has deep political connections in Springfield. Legislators who deferred to @properties on local real estate matters now must reckon with the fact that @properties is part of a national information suppression architecture controlled from New York.

The information asymmetry is now visible and measurable at the platform level. Prior legislative efforts against exclusive listings failed partly because the harm was diffuse and hard to quantify. The Compass-Redfin structure makes the suppression explicit: the same Redfin platform shows days on market for every listing except Compass’s. A legislative staffer can demonstrate that in a committee hearing with a laptop. Concrete, demonstrable harm moves votes in ways that theoretical arguments don’t.

Washington’s evidentiary record travels to every state that follows. The Astroturf Coefficient — 17:1 ratio of undisclosed to disclosed Compass affiliates at the January 23 Senate hearing — the cross-forum contradiction between Compass’s federal court positions and its state legislative testimony, the delegation downshift from Cris Nelson to Brandi Huff, the twelve-word opt-out amendment: every state legislature advancing a transparency bill inherits that record without needing to generate it from scratch. The Compass Narrative Inversion Playbook and State Power vs. Compass Private Exclusivesdocument the full playbook and why it fails under simultaneous institutional scrutiny. Each state that holds hearings generates a permanently discoverable evidentiary record available to every other legislature, regulator, and opposing counsel that follows.

The Parker v. Brown ratchet accelerates with each adoption. Each state that enacts a no-opt-out concurrent marketing requirement reinforces the “clearly articulated state policy” standard, making federal preemption challenges progressively weaker as the state count rises. Wisconsin enacted in December 2025. Illinois reintroduced in February 2026. Washington passed 49-0. Five states with no-opt-out concurrent marketing requirements is not a regulatory headwind. It is a material assumption failure in the Anywhere acquisition underwriting that triggers goodwill impairment review.

X. The Drafting Template: What Other States Should Enact and What Their AGs Can Do Now

The Compass-Redfin partnership creates two distinct legislative problems that require two distinct statutory responses. States drafting their own concurrent marketing legislation need to address both — and AGs in every consumer-protection-active state have enforcement vectors available right now, before any bill passes.

The listing-side provision: replicate SSB 6091’s core.

SSB 6091’s operative requirement is concurrent marketing: a residential property listed for sale must be submitted to the regional MLS within one business day of any public marketing, with no opt-out. The “no opt-out” language is the load-bearing provision. Every prior version of this legislation in Washington and other states allowed seller opt-out — and Compass deployed seller consent as the primary defense against pocket listing restrictions for three years. SSB 6091 eliminates that defense entirely. State legislatures drafting concurrent marketing bills should replicate three specific elements: the one-business-day submission trigger, the no-opt-out structure, and a definition of “public marketing” broad enough to cover Coming Soon designations, agent network announcements, and brokerage website postings. All three are necessary. A bill with opt-out is not SSB 6091 — it is the bill Compass’s lobbying operation already knows how to defeat.

The “public marketing” definition is where Compass will fight the implementation battle — and the Redfin partnership reveals exactly how.

Compass’s consistent legislative argument, advanced through its Washington lobbying operation, is that private exclusive marketing is seller-authorized conduct. The seller signed a consent form. Therefore the brokerage isn’t suppressing anything — it’s executing the seller’s instructions. That argument killed prior versions of this legislation for three years.

SSB 6091's no-opt-out structure eliminates that defense for MLS submission. But Compass will immediately redeploy it for the Redfin display architecture. The pattern is already documented: at the January 23 Senate hearing, Compass's Washington lobbying operation delegated testimony from Cris Nelson to Brandi Huff — a downshift that signaled Compass was managing exposure rather than engaging on the merits. The partnership's own language leads with "written seller consent required" — deliberate legal positioning, not boilerplate. Compass's compliance argument after SSB 6091 passes will be straightforward: the seller authorized the listing arrangement, the listing appears on two public platforms, MLS submission occurred within one business day. The bill is satisfied. The fact that Redfin displays the listing without days on market, price history, or valuation estimates is a platform display decision executed under seller authorization — outside SSB 6091's operative trigger.

That argument works unless enforcement authorities treat platform display suppression as a distinct act from listing authorization. Seller consent to list is not seller consent to deceive the buyer. Washington's AG and the Department of Licensing should treat those as two distinct enforcement targets — the MLS submission obligation under SSB 6091, and the platform display suppression as a separate CPA violation under RCW 19.86 independent of what the bill requires.

Washington's AG has the enforcement authority, the legislative transcript, and now the Redfin contract as primary evidence — the House vote converts a supportive posture into an actionable one.

The distribution-side provision: what SSB 6091 doesn’t cover and the Redfin deal makes necessary.

SSB 6091 targets the listing practice — withholding a property from MLS submission. The Compass-Redfin partnership creates a second harm that requires a second provision: a licensed brokerage operating as a consumer-facing search platform cannot display listings with selectively suppressed buyer data fields when it displays that data for all other listings on the same platform. Redfin is a licensed brokerage in every state where it operates. Displaying Compass listings without days on market, price history, or valuation estimates — while showing all three fields for every competing listing — is a two-tiered information architecture on a licensed brokerage’s platform. State legislatures writing new bills should add a platform display provision: licensed brokerages operating search platforms must display material listing data fields uniformly across all listings. No field suppression for preferred partner inventory. Adding that provision closes the Redfin architecture before it replicates in the next partnership Compass signs.

The Kelman reversal as legislative record.

Every state committee that holds a hearing on a concurrent marketing bill will face the same primary defense: the market is self-correcting, voluntary industry action is underway, legislation is premature. February 26, 2026 killed that defense. The Kelman reversal timeline — public pledge in April 2025, Rocket acquisition closes, pledge reverses within months, Kelman departs, February 26 statement reads “Our perspective evolved” — is now a permanently documented sequence available to any committee chair who wants to defeat the self-correction argument with primary evidence rather than economic theory. Legislative staff in any state can enter the Redfin press release, the Kelman pledge, and the acquisition timeline into the committee record as three exhibits. No state needs to generate that evidentiary record from scratch. Washington already did.

The state AG enforcement map: three vectors available pre-legislation.

State AGs in consumer-protection-active states have enforcement authority that does not depend on a concurrent marketing bill passing. Three vectors are available now, in any state where Redfin operates as a licensed brokerage and has signed the Compass partnership.

Vector 1 — State UDAP. Every state has a consumer protection statute modeled on the FTC Act’s unfair or deceptive acts or practices standard. Redfin operates as a licensed brokerage displaying a two-tiered information environment: Compass listings stripped of days on market, price history, and valuation estimates, while every competing listing on the same platform displays all three. A licensed brokerage that actively curates information suppression for a preferred commercial partner while presenting itself to consumers as a neutral search platform is participating in structural deception. The Kelman reversal provides the intent evidence: Redfin’s own prior leadership recognized the consumer harm and pledged to prohibit it, then reversed after a corporate acquisition. State UDAP enforcement does not require proving intent — the structural deception is facially apparent from a side-by-side comparison of any Compass listing against any non-Compass listing on the same Redfin page. But the Kelman record makes intent available anyway.

Vector 2 — State agency disclosure law. Every state that licenses real estate agents imposes fiduciary or statutory disclosure duties on buyer’s agents. Redfin buyer’s agents in every state are now structurally positioned to show clients Compass listings stripped of material data fields the agent knows exist, because the same platform displays them for every other listing. A buyer’s agent who shows a client an information-suppressed listing without disclosing the suppression has potentially breached the disclosure duty the license imposes. State AG consumer protection divisions with real estate licensing oversight authority — or state real estate licensing boards — can issue guidance requiring Redfin buyer’s agents to disclose when a listing’s data fields have been suppressed by platform agreement. Guidance costs nothing legislatively and creates the enforcement predicate for pattern investigations if Redfin buyer’s agents fail to disclose.

Vector 3 — State mortgage broker and consumer lending law. The Rocket Mortgage integration — preferred pricing exclusively through Compass agents, mortgage products embedded into the platform, buyer leads routed from Redfin — is a vertical tying arrangement in settlement services. RESPA Section 8 is the federal predicate, with CFPB as the enforcement vehicle. But every state with consumer lending and mortgage broker licensing statutes has independent authority over settlement service referral arrangements. State AG consumer finance divisions should examine whether the Rocket-Compass-Redfin referral structure satisfies state anti-kickback and anti-tying provisions independent of any federal CFPB action. The three-party structure — lead routing, exclusive preferred pricing, platform integration — is precisely the arrangement state mortgage broker regulations were designed to reach. Filing a state inquiry before CFPB acts establishes independent state enforcement posture and creates a coordination vehicle with other state AGs examining the same contract.

The Parker v. Brown sequencing argument.

State legislatures and AGs deciding whether to move now or wait face a specific strategic calculus that the Redfin partnership changes. Each state that enacts a no-opt-out concurrent marketing requirement reinforces the “clearly articulated state policy” standard under Parker v. Brown, making federal preemption challenges progressively weaker as the state count rises. Wisconsin enacted in December 2025. Washington passed 49-0 in February 2026 and is one House Rules Committee scheduling decision from enactment. A third state becomes a pattern. A fifth state becomes a standard. States that move early shape the preemption landscape for every state that follows. States that wait inherit a stronger federal preemption argument as Compass’s counsel documents the growing state count as evidence of state regulatory overreach rather than convergent consumer protection judgment.

The AG coordination dynamic runs parallel. Washington’s AG is already a plaintiff against Redfin in federal court and has domestic enforcement authority over Redfin as a Washington-licensed brokerage — a dual position no other state AG currently holds. But the factual predicate Washington’s AG has already established — the legislative transcript confirming UDAP enforcement authority, the Reffkin “no downside” versus the Compass Disclosure Form contradiction, the Kelman reversal record — is available to every other AG without independent investigation. Federal Inaction Has Elevated State Authority and Judicial Process as Competitive Federalism document the structural argument: when federal enforcement gaps are structural rather than episodic, state authority substitutes rather than supplements. The Compass-Redfin partnership is a structural federal enforcement gap operating in real time. The AGs who move first write the enforcement record that every AG who follows inherits.

XI. The Goodwill Impairment Question

The Anywhere acquisition recorded goodwill — premium above book value — that must be tested annually against the assumptions used to justify it. The $400–800 million Layer 3 premium rested on a single regulatory assumption: that private exclusives could be deployed at national scale without legislative or judicial interference sufficient to close the window.

The Redfin deal updates the impairment calculus in two directions simultaneously. On one side, it gives Compass a quantifiable new revenue stream to set against impairment testing: one million buyer leads over three years at zero referral cost, Rocket mortgage integration revenue, platform placement fees. Auditors can treat Platform Capture Value as a partial substitute for Private Exclusive Infrastructure Premium, potentially delaying the impairment trigger by one annual cycle.

On the other side, the deal formally documents — in Compass’s own commercial language, in a binding contract, in a press release — that the private exclusive inventory was the strategic rationale for the acquisition. When the regulatory environment closes the window state by state, Compass has no internal substitute mechanism. Outsourcing listing suppression infrastructure to a third-party platform for a three-year term is not a Layer 3 recovery strategy. It is evidence that Layer 3 can no longer be operated internally at the scale the acquisition required.

The internal contradiction vector compounds this. Anywhere CEO Ryan Schneider called the private listings approach “short-sighted” on Anywhere’s February 2025 earnings call. Coldwell Banker CEO Kamini Lane wrote that private listings ignore the law of supply and demand. ERA President Alex Vidal said the practice didn’t exist “in the field.” Every statement is timestamped, published, and available to auditors evaluating the goodwill assumptions recorded at close. Those same brands are now enrolled, by corporate decision, in a national information suppression contract. Auditors testing the goodwill assumptions now have: acquired leadership skepticism on the record, a signed contract confirming the mechanism is the strategic rationale, and a state legislative ratchet systematically eliminating the operating condition the premium requires. The impairment question is when — not whether.

XII. The Cross-Forum Contradiction: Now Contractually Locked

The Compass Narrative Inversion Playbook documented the cross-forum contradiction as the one vector Compass cannot fix: the firm is on record in federal court arguing that restricted listing visibility harms consumers and forecloses competition, while arguing in state legislatures that restricted listing visibility protects consumers through privacy and seller choice. Three positions, three forums, zero compatibility.

The Redfin partnership converts that rhetorical contradiction into a contractual one. Compass is now obligated — by contract — for three years to display listings on Redfin with no days on market and no price history: the exact “value killers” Reffkin named as the mechanism’s rationale. Every state legislative hearing during that window can reference the contract. Every deposition in the Zillow and NWMLS trials can reference it. Every congressional record update references it. The cross-forum contradiction is no longer a credibility argument. It is a three-year business obligation operating simultaneously against Compass’s own federal court positions.

Compass cannot settle its way out of the contradiction while the contract runs. It cannot amend the contract without disrupting the Rocket mortgage integration and the lead flow that justifies the deal’s economics. The window the 42-Day Collapse Framework identified as “Severe, Irresolvable” just became irresolvable by contract for three years.

XIII. The AG Strategy

Washington’s AG office holds a specific structural advantage that no other state AG currently has: simultaneous plaintiff status against Redfin in federal court and domestic enforcement authority over Redfin as a Washington-licensed brokerage. The February 26 partnership activates both simultaneously.

The UDAP enforcement authority Washington’s AG Civil Rights Division confirmed on the legislative record — recognizing the Reffkin “no downside” earnings call statement versus the Compass Disclosure Form’s acknowledgment that private exclusive marketing may reduce sale prices as an actionable gap — now applies to a national platform architecture producing the same suppression at 60 million monthly visitors. The gap between what the CEO says publicly and what the company’s own disclosure form tells clients is documented, public, and irreconcilable. Washington’s AG doesn’t need a new investigation to establish the factual predicate. The legislative transcript already did.

Three enforcement vectors are available independent of SSB 6091’s House vote. First, RCW 19.86 UDAP — the two-tiered information architecture on a licensed brokerage’s platform is structural deception under the standard Washington courts have applied. Second, RCW 18.86 fiduciary duty — Redfin buyer’s agents showing information-stripped Compass listings are systemically positioned to breach disclosure obligations at platform scale. Third, the RESPA tying analog under Washington’s Consumer Loan Act and mortgage broker regulations, independent of CFPB federal enforcement.

Multi-state AG coordination shares a common evidentiary foundation: the same contract terms, the same Kelman reversal documentary record, the same Rocket Mortgage tying structure, and the same MindCast analytical corpus available to all simultaneously through publicly accessible publications. Federal Inaction Has Elevated State Authority and Judicial Process as Competitive Federalism document why, when federal enforcement gaps are structural rather than episodic, state authority doesn’t merely supplement federal action — it substitutes for it. The Compass-Redfin partnership is a structural federal enforcement gap: CFPB has jurisdiction but has not yet acted, DOJ cleared the underlying merger through a bypass architecture under congressional investigation, and the FTC’s separate Zillow-Redfin action addresses a different market. State AGs are the enforcement mechanism available now.

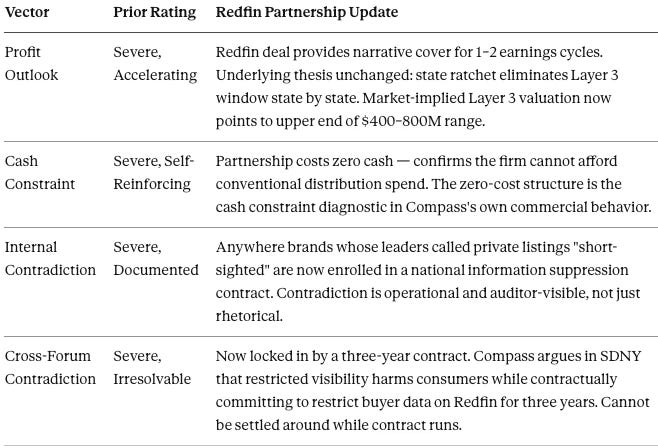

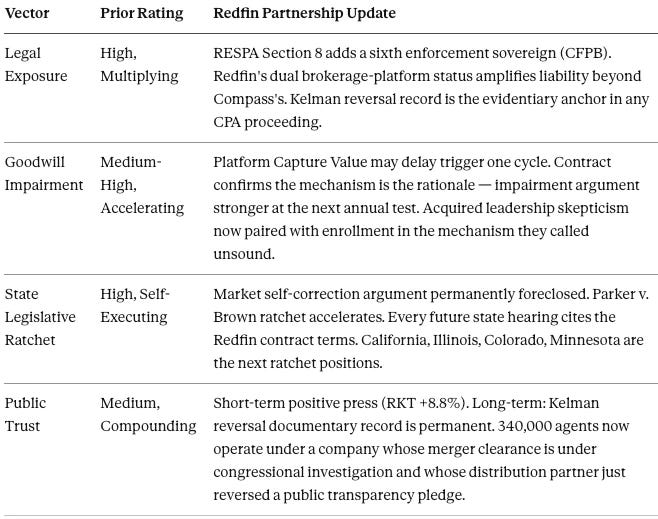

XIV. The Eight-Vector Update: Day 48

The 42-Day Collapse Framework identified eight compounding vectors — each severe on its own, collectively self-reinforcing — that define Compass-Anywhere’s structural position as the regulatory ratchet closes. Day 48 is today. The Redfin partnership updates four vectors toward Severe and accelerates the remaining four. No vector improves. The framework below tracks where each stands as of February 26, 2026 and what the partnership changes.

The first four vectors govern the firm’s internal financial and narrative architecture — the balance-sheet constraint, the contradiction record, and the solvency geometry that the Redfin deal confirms rather than resolves.

The second four vectors govern the external enforcement and institutional landscape — the legal exposure multiplying across six sovereigns, the goodwill impairment timeline, the state legislative ratchet, and the public trust trajectory. Each accelerates independently of whether Compass's internal contradictions resolve.

Eight vectors. No exits. The internal architecture confirms the solvency constraint; the external architecture confirms the enforcement trajectory. The Redfin partnership moves all eight simultaneously — buying narrative cover on two while accelerating the remaining six. The framework was never a countdown. Day 48 is the day the countdown became a contract.

XV. Forward Predictions

Four falsifiable predictions follow directly from the partnership’s structural logic, each observable against a specific trigger.

Within 7 calendar days: NWMLS files a Notice of Supplemental Authority citing the Redfin partnership in support of its pending motion to dismiss Compass v. NWMLS — arguing that Compass’s claimed harm from Washington’s restrictive listing policies is substantially mitigated by national Redfin distribution reaching 60 million monthly visitors. NWMLS ran this same playbook on February 6 within hours of the Compass v. Zillow preliminary injunction denial. The Redfin announcement is a stronger factual predicate.

By Q1 2026 earnings: Compass frames the Redfin deal as a Layer 3 pivot — platform distribution replacing state-by-state private exclusive windows — rather than a Layer 3 retreat. Watch for Reffkin to deploy the 60 million visitor figure and the 1 million buyer lead commitment as the investor-facing answer to state legislative ratchet losses. If the earnings call instead acknowledges the state ratchet as a material headwind without naming the Redfin partnership as a structural solution, the Layer 3 pivot thesis weakens and goodwill impairment accelerates to the next annual test cycle.

A second state — California most likely — advances a no-opt-out concurrent marketing bill citing the Redfin contract terms as evidence that voluntary market correction is insufficient. The Kelman reversal becomes the legislative record anchor for the necessity argument in every subsequent state hearing. The specific California hook: the CAR and state AG already have active Compass tension, and 500,000 suppressed listings on Redfin provides the precise legislative catalyst the prior sessions lacked.

CFPB opens a preliminary inquiry into the Rocket–Compass–Redfin referral arrangement under RESPA Section 8. The three-party structure — lead routing, exclusive preferred pricing, platform integration — is precisely what the CFPB’s enforcement mandate was designed to reach. The trigger is a consumer complaint or AG referral, both of which are now structurally available given the partnership’s terms.

The falsifiable test already running: seven active Team Foster listings documented in The Address Suppression Calculuson February 19 — $136 million in inventory, $3.4 million in buyer-side commission at stake, including MLS #2392995, the $79 million Lake Washington estate listed without an address — will produce closing records in NWMLS. When each closes, the MLS records who represented the buyer. If the internalization pattern documented in the Mercer Island Exhibit Transaction repeats, the Layer 3 model holds. If independent brokers win the buyer side at open-market rates, the regulatory pressure is already reshaping behavior before SSB 6091 formally takes effect. The Redfin contract terms make the same falsifiable test available at national scale: when Compass’s quarterly earnings disclose buyer lead conversion rates through the partnership, the Layer 3 revenue contribution becomes quantifiable against the state legislative ratchet losses.

XVI. Conclusion

The Compass-Redfin contract is Exhibit A.

Compass built its Anywhere acquisition premium on private exclusives — amplified by $2.6 billion in assumed debt and 340,000 acquired agents — to convert network density into commission capture at national scale. The Redfin partnership confirms that mechanism is the firm’s primary commercial asset, in its own language, in a binding contract, published today. The merger created the debt. The debt required the dual commissions. The dual commissions required the private exclusive window. The Redfin deal is what a firm does when the window starts closing — not a pivot, a last available play executed at zero cash cost because no other play exists.

MindCast AI predicted the Tirole Phase Transition that produced the Redfin reversal. Named the bypass actors before the congressional record named them. Quantified the Layer 3 mechanism in Seattle transaction data before the Redfin press release confirmed it nationally. Characterized the solvency argument before the zero-cash deal structure proved it. Published the cross-forum contradiction before the three-year contract locked it in place.

The prediction record is not background. It is the evidentiary foundation for why the forward predictions above deserve legislative and enforcement attention before the outcomes materialize rather than after.

SSB 6091 passed the Washington State Senate 49-0. The House Rules Committee holds the gate. The Redfin contract — signed today — is the most concrete single-day validation of why the bill’s sponsors were right. Every state legislature and AG office that reads the contract terms, reads the Kelman reversal record, and reads the RESPA tying structure is looking at the same architecture Washington’s Senate already voted to close.

Death by a thousand depositions is not a metaphor. It is the operational description of what happens when eight compounding vectors share a single evidentiary substrate — and none of them stop running.

The depositions have not yet begun.

Validated Foresight Predictions

Prior MindCast publications cited in this analysis:

The Stigler Equilibrium: Regulatory Capture and the Structure of Free Markets | The Compass-Anywhere Litigation-Acquisition Monopolization Strategy | The Compass-Anywhere Address Suppression Calculus | The Tirole Phase Analysis of Advocacy-Driven Antitrust Inaction | The Compass Commission Consolidation Strategy | Death by a Thousand Depositions: The 42-Day Collapse Framework | Nineteen Senators, Seventeen Questions | The Shadow Antitrust Trifecta | How MindCast Predicted the Slater Ouster | SSB 6091 Cross-Forum Analysis | The Compass Narrative Inversion Playbook | State Power vs. Compass Private Exclusives | Federal Inaction Has Elevated State Authority | Judicial Process as Competitive Federalism, The Dual Nash-Stigler Equilibrium Architecture,