MCAI Economics Vision: The Prediction Markets Rule Architecture Series, A Boundary Rule with a Functional Core

Installment I: A two-step framework for CFTC authority over event contracts under the Commodity Exchange Act

MindCast Series, The Prediction Markets Rule Architecture: The Prediction Markets Rule Architecture Series, A Boundary Rule with a Functional Core | The Prediction Markets Rule Architecture Series, Competitive Federalism | Kalshi Loses Federal Forum — The Washington Remand Order and the Jurisdictional Layer of the Prediction Markets Boundary Rule

Executive summary

The Commodity Exchange Act already draws the line between hedging and wagering. Current disputes exist because the rule operationalizing the line remains incomplete. The framework below restores the rule.

Contracts based on contests — competitive games whose outcomes depend on play for stakes — fall outside the federal derivatives system as a presumptive matter. Contracts based on consequences — real-world events with measurable economic and operational effect — face evaluation under a five-factor functional override. The override admits contracts performing genuine risk transfer for participants who already face the underlying exposure. The override excludes contracts synthesizing exposure within the contract itself or exposing the market to misappropriation by participants holding non-public government, military, regulatory, institutional, or athlete information.

The structure stands as an administrable standard that survives independent statutory review under Loper Bright Enterprises v. Raimondo — defensible for regulators on a contemporaneous record, and falsifiable on the evidence. No alternative standard currently offered in the public record satisfies both the statutory boundary CEA § 5c(c)(5)(C) draws and the evidentiary requirements Loper Bright imposes on agency interpretation; the framework presents itself as the default rule on those constraints rather than as one option among several. Failure to adopt the framework triggers regulatory arbitrage and offshore migration as structural consequences — the equilibrium failure mapped in MindCast: Kalshi, Prediction Markets and the Conflict Architecture of Regulation and the cross-forum convergence documented in MindCast: Prediction Markets Litigation Stack — Federal, Private, and State Enforcement Converge. Former CFTC Chairman Gary Gensler — principal architect of the Dodd-Frank swaps regime — told Barron’s in April 2026 that the swap definition was not intended to encompass sports event contracts and that betting on sports is gaming. The Van Dyke insider-trading indictment unsealed April 23, 2026 — the first criminal charges in the United States for misappropriation trading on a prediction market — places informational integrity at the center of any defensible regulatory architecture. The April 30, 2026 joint comment filed in the same docket by the five major North American players associations places athlete safety, athlete due process, and athlete-information misappropriation on the public record the rule must address.

The line is not the problem. The rule is.

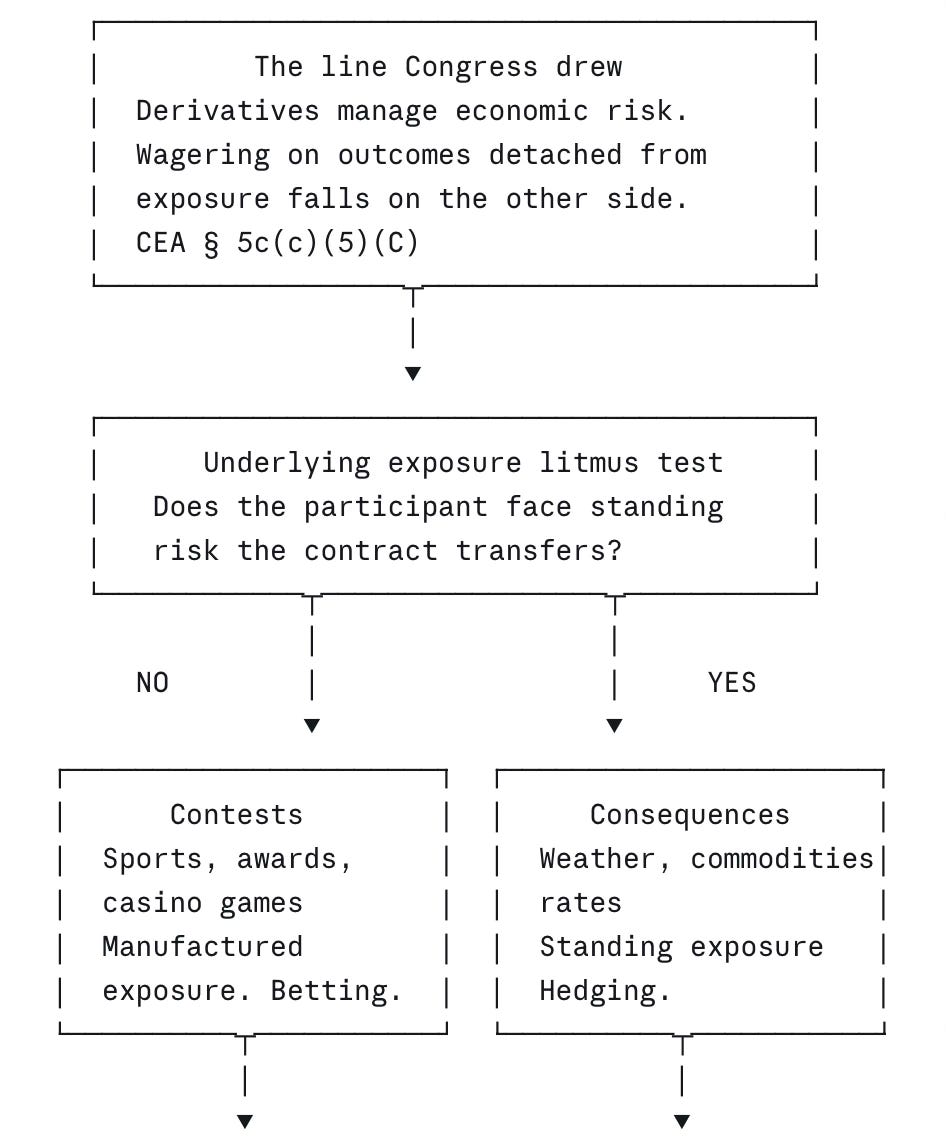

I. The line Congress drew: contest versus consequence

The CEA’s boundary rests on purpose. Derivatives manage economic risk; pure wagering on outcomes detached from exposure falls on the other side. CEA § 5c(c)(5)(C) gives the Commission authority to stop “gaming” contracts contrary to the public interest. The Rule 40.11 gap blocking that authority appears in MindCast: Defining “Gaming” Under the Commodity Exchange Act, The Rule 40.11 Gap Driving the Nationwide Kalshi Litigation Web — Congress supplied the statutory boundary; the agency has failed to operationalize it.

Event labels cannot draw the line. Election outcomes drive trillions in capital allocation. Weather outcomes underwrite agricultural hedging across continents. Sports outcomes do not create standing operational exposure of the kind derivatives law exists to hedge. The label fails to predict the function. The operative question runs deeper: does a contract transfer economically material uncertainty affecting capital allocation?

A coherent rule must state the line as a sorting principle: contest versus consequence. A contest is a competitive activity whose outcome depends on play for stakes — sports, awards, casino-style games, and similar competitive performances. Contests fall presumptively within “gaming” under CEA § 5c(c)(5)(C) and belong to state gaming commissions and tribal gaming compacts under the Indian Gaming Regulatory Act, not to federal derivatives markets. A consequence is a real-world event whose outcome carries measurable economic, operational, or policy effects independent of the contract — weather realizations, commodity supply disruptions, interest-rate movements, election outcomes, geopolitical events. Consequences avoid categorical gaming treatment; whether a consequence-based contract belongs inside the federal derivatives system depends on whether the contract performs genuine risk transfer — the question the functional override answers.

Drafting-history evidence: what Congress did

The framework’s reading of CEA § 5c(c)(5)(C) is not a reconstruction. The Dodd-Frank drafting record now contains documented statements from the principal architect of the swaps regime confirming the framework’s reading directly. Former CFTC Chairman Gary Gensler — who served as principal architect of the Dodd-Frank swaps regime and later chaired the SEC — told Barron’s in April 2026 that the swap definition was not intended to encompass sports event contracts: I never once ever heard a member of Congress or their staffs suggest that the law they were writing, acting upon, and voting on was for our little agency, the CFTC, to have oversight over sports betting.

The word gaming in the anti-gaming clause carries high-value drafting-history evidence from a principal Dodd-Frank architect. Gensler told Barron’s the inclusion was a priority for Nevada Senator Harry Reid, then the Democratic Majority Leader, so the CFTC could prohibit it — and that no one in the drafting process intended to preempt state gaming commissions. The textualist swap-definition argument the federal preemption theory relies on faces direct contradiction from documented drafting purpose. Gensler’s closing four-word position carries the weight of the rest: Betting on sports is gaming.

The framework does not depend on drafting history alone. The statutory text already singles out gaming, and the drafting record confirms what the text makes visible. Independent commentary corroborates the analytical posture: gambling-law commentator Daniel Wallach told Barron’s that the courts ruling for Kalshi are wearing blinders and just focusing on the plain language of the statute without taking into account the legislative history and statements made at the time of Dodd-Frank’s enactment. The textualist-blinders framing names the analytical failure the framework’s contest-versus-consequence sort is designed to correct.

The contest-versus-consequence sort operates as the surface threshold. The five-factor test below operates as the substantive override. The dissent in KalshiEX LLC v. Flaherty reads Rule 40.11 in this direction. The framework specifies how the dissent’s reading translates into rule text.

II. Why current practice fails

The Commission’s simultaneous assertion-and-inquiry posture appears in MindCast: Kalshi, Prediction Markets and the Conflict Architecture of Regulation. The Commission asserts authority in three appellate circuits and the District of Arizona while the agency’s own Advance Notice solicits public comment on what “gaming” means. The diagnostic resolves to a single line: authority exercised before deliberation completed. CFTC Chairman Mike Selig, pressed at his Senate confirmation hearing on whether sports event contracts should be defined as gaming, deferred to ongoing lawsuits and stated he would really want the benefit of understanding what the judges think about the issue — as reported in Barron’s. The current Commission Chairman declines to affirm the position the statute’s principal architect states is the actual statutory meaning.

The split produces four structural failures.

Over-exclusion. Categorical reasoning blocks legitimate risk-transfer mechanisms tied to decision-relevant uncertainty by mistaking event type for economic function.

Under-explanation. Orders rely on labels rather than evidence of exposure and transfer. After Loper Bright eliminated the deference previously absorbing the gap, label-based reasoning no longer survives appellate review. Daniel Wallach, a recognized gambling-law commentator tracking the prediction-market cases, has framed the same failure mode as a textualist trap — telling Barron’s that the courts ruling for Kalshi are wearing blinders and just focusing on the plain language of the statute without taking into account the legislative history and statements made at the time of Dodd-Frank’s enactment. The framework’s contest-versus-consequence sort and the drafting-history evidence set out in Section I correct the failure mode at the level the courts can reach under independent statutory analysis.

Cross-forum inconsistency. Positions diverge across CFTC rulemaking, federal enforcement, DOJ Supremacy Clause litigation, and state and tribal actions — the four-track convergence pattern documented in MindCast: Prediction Markets Litigation Stack. The institutional-opposition record now extends across thirty-eight state attorneys general filing jointly in Commonwealth of Massachusetts v. KalshiEX LLC, the Indian Gaming Association and tribal coalition acting through public statements and conference resolutions, the five North American players associations filing jointly in the RIN 3038-AF65 docket, and public-interest organizations including the Project On Government Oversight filing comment in the same docket. A structurally distinct vector now operates alongside the agency-led preemption track: private-party preemptive federal court actions, including Robinhood Markets, Inc. v. Brown filed March 30, 2026 in the United States District Court for the Western District of Washington — Robinhood suing the Washington Attorney General and the Washington State Gambling Commission preemptively, three days after Washington filed against Kalshi in state court. The platform-side preemption track parallels Robinhood’s similar preemptive litigation in Massachusetts and New Jersey, demonstrating a coordinated private-party strategy that operates independently of the CFTC’s own preemption suits and that converts every state enforcement initiative into immediate federal court litigation.

Misappropriation exposure. The Van Dyke indictment — alleging a Special Forces master sergeant used classified operational intelligence about the January 2026 raid that captured Nicolás Maduro to win approximately $400,000 on Polymarket contracts pricing whether U.S. forces would be in Venezuela by January 31 — establishes the prediction-market category sits at the intersection of derivatives regulation, securities-style misappropriation doctrine, and national-security information control. The DOJ filed wire fraud, commodities fraud, theft of nonpublic government information, and unlawful monetary transaction counts. The CFTC filed a parallel civil action seeking disgorgement, civil penalties, and a permanent trading ban. The current rule lacks a surveillance architecture capable of preventing or detecting the conduct charged.

The condition compounds beyond agency posture. MindCast: The Rule 40.11 Paradox — Kalshi, the Third Circuit, and the Class Action the Ninth Circuit Cannot Ignore documents how definitional ambiguity does not pause the system — the ambiguity activates the private enforcement layer under 7 U.S.C. § 25(b), where damages accrue against an unamended federal rule the Commission has acknowledged remains undefined. Deferring classification does not buy peace. Deferring converts ambiguity into liability and, after Van Dyke, into criminal exposure.

Contact mcai@mindcast-ai.com to partner with us on Predictive Cognitive AI + Game Theory in Law and Behavioral Economics. To deep dive on MindCast work in Cognitive AI upload the URL of this publication into any LLM and prompt ‘parse MindCast framework with three degrees of cited sub links.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure.

Recent projects: Where Institutional Capital Moves Under Federal Digital-Asset Control Architecture | Defining “Gaming” Under the Commodity Exchange Act, The Rule 40.11 Gap Driving the Nationwide Kalshi Litigation Web | The Rule 40.11 Paradox — Kalshi, the Third Circuit, and the Class Action the Ninth Circuit Cannot Ignore | Prediction Markets Litigation Stack — Federal, Private, and State Enforcement Converge

III. The mechanism: presumption plus functional override

A coherent regime needs a two-step structure merging administrability with economic fidelity. The structure must hold a clear default while admitting evidence-based exceptions. The structure must operate at the level of contract architecture rather than event taxonomy.

Step one — presumptive boundary

Contests fall outside the federal derivatives system under the CEA’s public-interest and anti-gaming principles. Consequence-based contracts avoid categorical exclusion but face the override below before listing. The presumption protects statutory purpose, administrability, and judicial clarity. The presumption places the burden on the listing party to demonstrate the contract belongs inside the regulated derivatives system — rather than placing the burden on regulators, courts, state attorneys general, or tribal compact holders to chase each new product through litigation.

Step two — functional override

The proponent overcomes the presumption only by affirmative demonstration of economically material risk transfer combined with informational integrity safeguards — the modified economic purpose test, restated in functional terms and extended to address misappropriation risk.

The override turns on a critical distinction: economic impact is not economic exposure. Many outcomes affect markets indirectly. Only some create operational exposure participants can hedge through a contract. The override admits the latter and excludes the former. Even when exposure exists, the override fails if the contract category remains structurally vulnerable to misappropriation by participants holding non-public government, military, regulatory, institutional, or athlete information.

The five-factor test follows below.

IV. The five-factor test

A contract overcomes the presumption only by satisfying all five factors. The proponent bears the burden of demonstration on a developed record at affirmative approval. Each factor operates independently; failure on any single factor defeats admissibility.

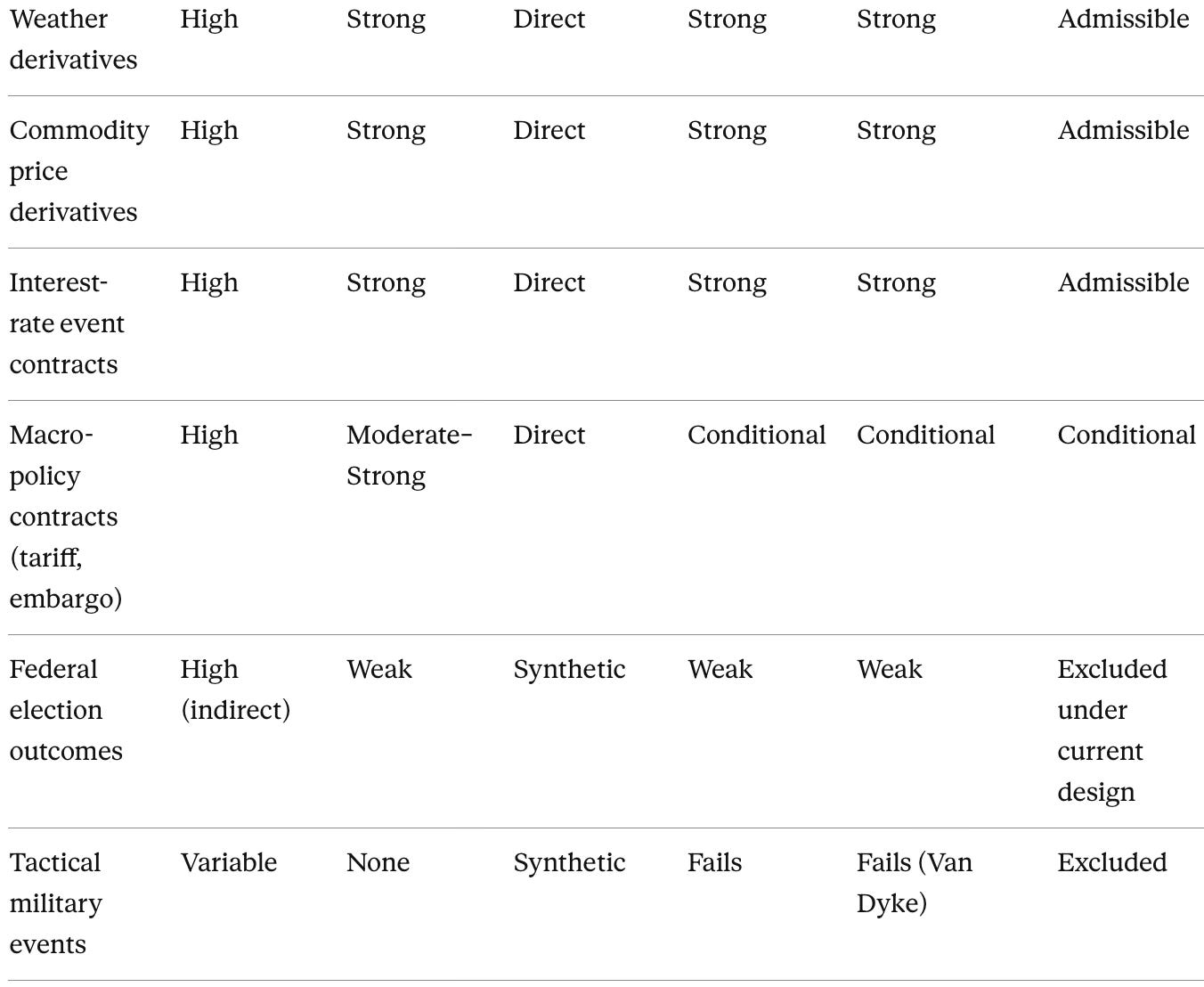

1. Materiality. The outcome measurably moves economic decisions — documented strategy shifts, pricing adjustments, or hedging behavior at scale. Evidence of capital repositioning satisfies materiality. The outcome’s general consequence does not.

2. Participant connection. A meaningful share of participants bear or manage the underlying risk in operational terms. The test operates structurally: the contract must remain available to and designed for participants who face the underlying exposure. Recreational use does not satisfy the factor regardless of volume.

3. Transfer mechanism. The contract redistributes existing uncertainty between counterparties in a manner corresponding to real underlying risk. A contract manufacturing exposure existing only inside the contract itself fails the factor — payoffs must hedge or price uncertainty participants already face, not synthesize uncertainty the contract creates.

4. Design integrity. Structural features prevent recreational, entertainment-driven flow from dominating the market. Design integrity fails where:

Payout structures maximize participation from non-exposed actors rather than hedging counterparties.

Contract sizing aligns with retail speculation rather than commercially meaningful hedging ratios.

Settlement structure has no linkage to operational exposure faced by any identifiable counterparty class.

Marketing and distribution architecture targets recreational participants rather than hedging participants.

5. Informational integrity. The exchange demonstrates active surveillance preventing misappropriation trading by participants holding non-public information. The contract category avoids structural domination by information asymmetries the surveillance architecture cannot reach. Informational integrity fails where:

The exchange lacks a Surveillance Sharing Agreement with relevant federal agencies (CFTC enforcement, DOJ, and where applicable, FBI counterintelligence and Department of Defense channels for security-sensitive event categories).

The exchange lacks documented insider-trading compliance policies, identity verification at the participant level sufficient to support enforcement, and a published referral process for suspected misappropriation.

The contract category remains dominated by information asymmetries held by government, military, regulatory, or institutional insiders no published-information lag or surveillance protocol can mitigate.

The contract category remains dominated by information asymmetries involving non-public athlete health information, biometric or performance data, injury reports, training-staff knowledge, or league-internal disciplinary information. State-law protections identified by the National Football League Players Association, Major League Baseball Players Association, National Basketball Players Association, National Hockey League Players’ Association, and Major League Soccer Players Association in their April 30, 2026 RIN 3038-AF65 comment — including Massachusetts C.23n §§ 3, 4, and 11; Missouri 11 CSR 45-20.350 and 45-20.370; Illinois 25-80; and Virginia § 58.1-4030 — establish the floor any federal informational integrity standard must meet.

The contract architecture creates the conditions for the conduct charged in United States v. Van Dyke — wagers tied to outcomes whose timing and substance are controlled by classified operational decisions or by analogous non-public institutional information.

Informational integrity carries the second load-bearing role in the test. The Van Dyke case demonstrates how prediction-market contracts can monetize misappropriated classified information at velocity exceeding any post-hoc enforcement response. The Players Associations’ filing establishes how the parallel misappropriation problem extends to non-public league, medical, and athletic-staff information no exchange surveillance architecture can plausibly reach without symmetric data-sharing obligations the current rule does not impose. Surveillance architecture must operate at listing rather than after damage. A contract category failing informational integrity ex ante does not become admissible through enforcement actions ex post.

The operational threshold is testable on the record: a contract category fails informational integrity where enforcement latency exceeds the payoff resolution window. If misappropriation can be detected only after the contract has paid out, the surveillance architecture cannot reach the conduct the framework is designed to prevent. The Van Dyke contract architecture — payoff resolution within days of the underlying classified operation, enforcement latency measured in months — fails the threshold by orders of magnitude.

Design integrity prevents engineered workarounds at the level of contract structure. Informational integrity prevents misappropriation at the level of participant access. Both factors operate together.

The inquiry shifts from what type of event is this to does uncertainty here move capital, does the contract transfer the risk, and can the market resist informational misappropriation.

Per-se exclusion: negative-outcome and individual-targeting contracts

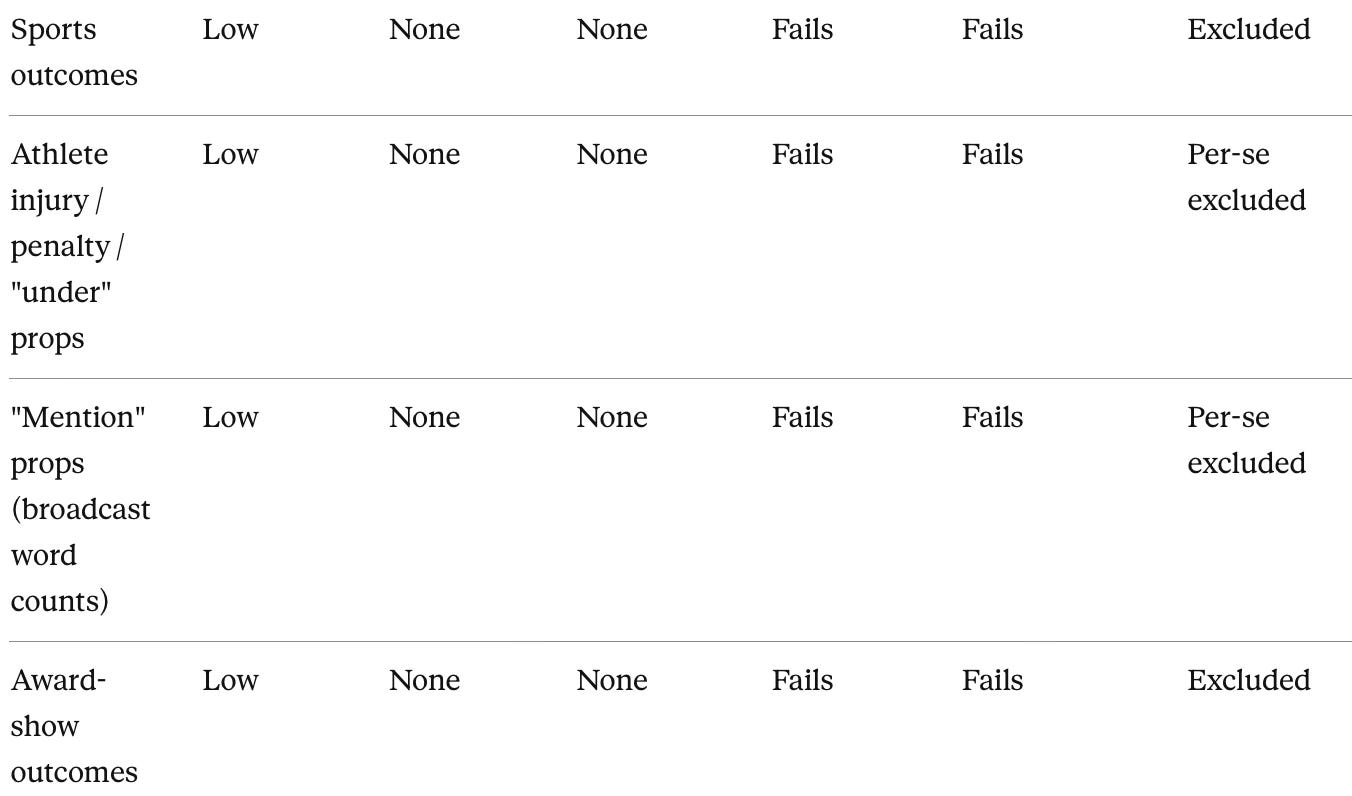

Independent of the five-factor analysis, the rule must categorically exclude contracts engineered to pay out on negative events affecting identifiable individuals. The category covers four contract types:

“Under” bets and negative-performance contracts paying out when a named individual fails to meet a specified statistical threshold.

Injury and penalty props paying out on whether a named individual is injured, ejected, suspended, or otherwise penalized.

“Mention” props paying out on whether a specified word or phrase — including injury-related, conduct-related, or disciplinary terminology — is spoken during a live broadcast.

Any contract whose payout structure creates a financial incentive for participants to wish, encourage, or facilitate harm to a named individual.

The categorical exclusion of these contracts appears on the public record through the April 30, 2026 joint comment filed in the RIN 3038-AF65 docket by the National Football League Players Association, Major League Baseball Players Association, National Basketball Players Association, National Hockey League Players’ Association, and Major League Soccer Players Association. The Project On Government Oversight filed a parallel public comment in the same docket urging the Commission to specify that event contracts on death, political events, and electoral outcomes — and contracts creating incentives for government officials to trade on material non-public information — are contrary to the public interest under CEA § 5c(c)(5)(C). The framework reaches the same exclusion result for political and electoral contracts through the five-factor test rather than per-se categorical exclusion: the five-factor test produces the exclusion through documented analytical reasoning that survives independent statutory review under Loper Bright, while preserving analytical room for any future contract structure that could in principle satisfy the override. The per-se exclusion in this section covers negative-outcome and individual-targeting contracts because the contract architecture itself creates the public-interest harm CEA § 5c(c)(5)(C) was designed to prevent. The exclusion does not depend on the contest-versus-consequence sort or the five-factor test. A registered entity listing such contracts violates Rule 40.11 on the face of the listing regardless of any other admissibility analysis.

V. Admissibility matrix (applied)

The framework’s discipline becomes visible at the level of contract analysis. The matrix below applies the five factors and the per-se exclusion to representative contract categories. Readers can deploy the matrix directly in regulatory submissions, judicial briefing, or compliance review.

Worked walk-through — the election case

The election outcome contract presents the framework’s hardest classification case. Sophisticated readers press the conventional objection first: institutional investors do reposition portfolios based on election outcomes, satisfying materiality — does the framework not pull election contracts inside the override on that basis?

Materiality alone cannot create CFTC admissibility. Otherwise every politically salient fact becomes a derivative, and the boundary CEA § 5c(c)(5)(C) draws collapses into a single-factor test the statute does not contemplate. The override requires all five factors to hold; materiality is the gateway, not the destination. Indirect exposure through policy sensitivity — corporate hedging against regulatory, tax, or trade-policy outcomes — does not constitute hedgeable risk because the exposure lacks a measurable payoff function tied to the contract. A corporation worried about election-driven tax policy faces tax-code risk, not election-outcome risk; the hedging instrument the framework recognizes addresses the tax code directly, not the proxy outcome that may or may not produce a tax change.

The objection fails. Election outcomes influence markets, but the outcomes do not create operational exposure participants hedge through a contract. The contract does not transfer an underlying risk faced by participants; the contract manufactures exposure existing only within the contract itself. A utility hedges weather risk because the utility hasweather exposure on its operations regardless of whether the contract exists. A trader buying an election contract has no analogous standing exposure — the trader’s election “risk” arises through the act of buying the contract, not through transfer of an existing risk. Participant connection fails because no operational election-outcome exposure exists in the way operational weather-outcome exposure exists. Transfer mechanism fails because payoffs synthesize exposure rather than redistribute it. Design integrity fails because position sizing, contract framing, and flow patterns align with recreational wagering rather than hedging — the recreational-flow versus hedging-flow asymmetry quantified in MindCast: Kalshi Found the One Gap in American Gaming Law Nobody Closed. Informational integrity fails because election-outcome information asymmetries — campaign internal polling, candidate health information, undisclosed staff knowledge — sit outside the surveillance architecture any exchange can plausibly maintain.

Excluded under the current architecture — and the exclusion holds against the materiality objection because the framework distinguishes economic impact from economic exposure on the face of the test. A future contract structure could in principle satisfy the override by demonstrating verified exposure linkage among hedging counterparties, not by reframing the same recreational-flow architecture in different language. The burden sits with any proponent seeking the override.

Worked walk-through — the geopolitical case

Geopolitical and security-related contracts occupy the framework’s third-rail category. Informational integrity does the most work in this category because the underlying information sits closest to classified or non-public institutional channels. The walk-through divides the category into broad macro-policy contracts and narrow tactical military-event contracts.

A broad macro-policy contract — for example, a contract paying out on whether a specified tariff schedule remains in effect on a given date, or whether a particular sanctions regime stays active — can satisfy the override conditionally. The outcome carries measurable supply-chain and capital-allocation consequences hedging participants face on their operations. Tariff and sanctions information, while sometimes non-public during a window, generally falls under publication requirements and procedural lag the surveillance architecture can accommodate. Conditional admissibility follows, contingent on the exchange demonstrating an SSA with relevant agencies and a published-information lag protocol.

A tactical military-event contract — for example, a contract paying out on whether a specified individual is captured by a specified date, or whether U.S. forces are present in a specified country by a specified date — fails the override decisively. Van Dyke’s contract category fits exactly here. Materiality runs variable. Participant connection falls to none — no operational counterparty class faces standing tactical-event exposure the contract redistributes. Transfer mechanism fails because the contract synthesizes exposure rather than transferring it. Design integrity fails because the category remains structurally engineered for speculation on classified outcomes. Informational integrity fails on the most acute available evidence: the United States indicted a participant in Operation Absolute Resolve for using classified planning information to win on the exact contract type. No exchange surveillance architecture can reach the universe of cleared personnel with operational knowledge of classified missions in real time. The category fails the override.

The framework does not ask whether the exchange detected Van Dyke after the fact — Polymarket cooperated with the investigation, and the cooperation credits the platform’s compliance posture without substituting for ex ante exclusion. The framework asks whether the contract category remains admissible at listing. Tactical military-event contracts do not.

Worked walk-through — the sports case

Sports outcome contracts fail at the threshold. Sports outcomes meet the definition of contests: competitive activities whose outcomes depend on play for stakes. Sports outcomes sit on the state-and-tribal side of the federal derivatives boundary regardless of how the four substantive factors apply. Materiality runs minimal, no meaningful population of participants faces underlying sports-outcome risk in the operational sense, and design integrity aligns with recreational flow by construction.

Presumptively and definitively excluded.

Worked walk-through — the weather case

A contract paying out on cumulative heating degree days passes all five factors. Utilities, agricultural operators, and energy traders measurably reposition capital based on temperature realizations. The contract remains structurally available to and designed for hedging participants with operational exposure. Payoffs correspond to underlying weather risk faced by counterparties — risk existing independent of the contract. Position limits and settlement align with hedging function. Weather-data sources remain public, and informational asymmetries reduce to forecasting expertise rather than misappropriated insider information.

Belongs inside the regulated system.

VI. What each actor does Monday morning

The framework converts theoretical structure into operational instructions. Each constituency gains a specific action set tied to existing legal authority and existing institutional capacity. The instructions below assume the Commission adopts the framework through Rule 40.11 rulemaking and Rule 40.3 procedural conversion; pending that adoption, the same instructions apply as preparation for the affirmative approval pathway courts will increasingly demand under Loper Bright.

For regulators

Move boundary-implicating consequence-based contracts from Rule 40.2 self-certification to Rule 40.3 affirmative approval within 90 days — at minimum, all novel, retail-accessible, politically sensitive, sports-related, or security-sensitive event contracts. Self-certification was never designed to carry the weight of distinguishing hedging instruments from wagering products at the boundary, and the Van Dyke case has demonstrated self-certification cannot carry the weight of distinguishing surveillance-capable contract categories from misappropriation-vulnerable ones. Affirmative approval generates the contemporaneous record Chenery, State Farm, Encino Motorcars, and Loper Bright require. Establish a parallel CFTC–DOJ Insider Trading Task Force to police the new markets, using the Van Dyke commodities-fraud and misappropriation theories as the enforcement template. Publish factors and evidentiary expectations for the five-factor test, with worked examples drawn from the matrix above.

For courts

Where the Commission has not applied a structured test, remand for application of a presumption-and-rebuttal framework rather than redefining the statute through abstraction. Adopt the contest-versus-consequence sort as the threshold and the five-factor test as the substantive standard. Review agency decisions for consistency, evidentiary support, and reasoned explanation. The framework gives panels exercising independent judgment under Loper Bright a doctrinal handhold avoiding any need to rewrite the CEA.

For market participants

Contracts unable to demonstrate participant exposure linkage and informational integrity at listing should not be filed. Design contracts demonstrating exposure linkage and transfer mechanics. Implement controls aligning trading with hedging and price discovery rather than recreational flow. Adopt insider-trading compliance policies, identity verification protocols sufficient to support enforcement, and Surveillance Sharing Agreements with relevant federal agencies before approaching affirmative approval. The compliance posture aligns with the institutional capital preferences mapped in MindCast: How Institutional Capital Moves Under Federal Digital-Asset Control, where capital flows toward compliant, low-latency infrastructure rather than classification-dependent models.

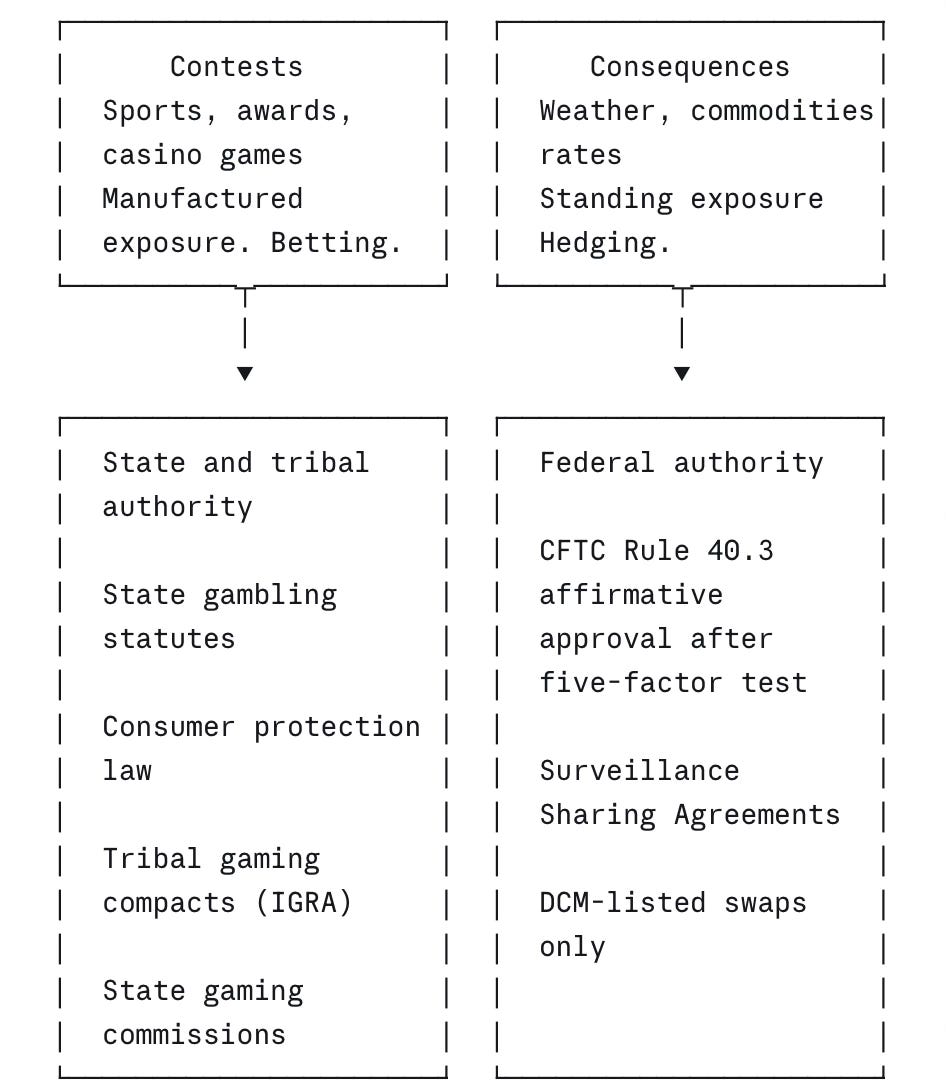

For state regulators and tribal gaming authorities

The framework preserves jurisdiction over conduct historically belonging to state and tribal authority. Contests sit on the state and tribal side of the federal derivatives boundary. The federal framework occupies the field of derivatives regulation and does not occupy the field of gaming regulation. The three-layer sovereign argument — Montana v. Blackfeet Tribe, Chenery, and Loper Bright — operates independently of swap classification, and the rule preserves it on its face. The competitive federalism architecture below specifies the operational interface under conditions where no sovereign will defer to the others.

VII. Competitive Federalism: the federal-state-tribal allocation under concurrent sovereignty

A vague non-displacement clause cannot carry the weight of the current state-federal collision pattern. Federal authority asserts exclusive jurisdiction through CFTC enforcement actions and amicus briefs, thirty-eight state attorneys general have filed jointly against the federal preemption theory, and tribal compact rights face displacement by a federal statute that never contemplated the IGRA collision. The dynamic is competitive federalism rather than cooperative federalism — three sovereignties asserting authority over the same conduct, with no expectation that any sovereign will concede ground to another. The architecture below specifies the equilibrium terms under which each sovereign retains authority within its sphere against encroachment by the others. The framework operates without requiring federal-state-tribal coordination that the current regulatory environment cannot produce.

Jurisdictional architecture. The Commission’s exclusive jurisdiction extends to the execution of swaps on designated contract markets. State and tribal authorities retain jurisdiction over unregulated wagering and over contests as defined in Section I. Federal authority over the trade does not displace state authority over the activity.

Dual-Gate Reporting. Registered entities listing consequence-based contracts whose payouts reference state-specific or tribal-jurisdiction-specific outcomes must file Dual-Gate Reports with the relevant state regulator or tribal gaming authority. Reports document participant geographic distribution, volume by jurisdiction, and any settlement events with potential to overlap state lottery or tribal compact economic interests. Reporting does not function as a license; reporting operates as a transparency mechanism giving state and tribal authorities the data they need to evaluate displacement risk and to coordinate enforcement where their jurisdiction is implicated.

Geofencing protocols. Where a registered entity lists a contract category overlapping with state-licensed gaming or tribal compact exclusivity, the entity must implement geofencing or comparable participation restrictions respecting state and tribal regulatory boundaries. Federal authorization to list a contract is not federal authorization to market or transact in jurisdictions where the underlying activity remains reserved to state or tribal authority.

Non-displacement of IGRA compact rights. Express text confirms the Commission’s authority under the CEA does not displace, override, or condition rights established under tribal gaming compacts negotiated under the Indian Gaming Regulatory Act. The federal derivatives framework occupies the field of derivatives regulation. The framework does not federalize gaming regulation through derivatives law.

Coordination protocol. The Commission establishes a published coordination channel with state attorneys general, state gaming regulators, and tribal gaming authorities for cases where consequence-based contracts may have downstream effects on state- or tribal-regulated activity. Coordination does not surrender federal jurisdiction. Coordination prevents the federal-state collision pattern from regenerating after rulemaking.

Due process in event-contract manipulation investigations. CFTC Division of Market Oversight Staff Letter No. 26-08, March 12, 2026, recommends designated contract markets coordinate with sports leagues on contract development, settlement integrity, information-sharing arrangements with integrity monitoring organizations, official league data settlement, and league-led manipulation investigations. The architecture creates a CFTC–DCM–league–integrity-monitor information channel that, as filed by the Players Associations in their April 30, 2026 RIN 3038-AF65 comment, can operate to the exclusion of the individual whose career, reputation, and livelihood form the subject of the investigation. The framework closes the gap. Any individual whose conduct becomes the subject of an event-contract manipulation investigation involving information-sharing among the Commission, a registered entity, an integrity monitoring organization, or a sports league receives symmetric and contemporaneous access to the information being shared. Affected players appear through their certified bargaining representative where applicable. The clause preserves the cooperation among regulators, exchanges, leagues, and integrity monitors effective enforcement requires while restoring the procedural symmetry the affected individual deserves under fundamental due process principles. The CFTC, DOJ, and registered entities retain their full enforcement authority. The clause adds the affected individual to the information loop without subtracting anyone from it.

The architecture answers the institutional concerns raised by tribal gaming authorities, state gaming regulators, state attorneys general, and athlete representative organizations without surrendering the federal derivatives framework. The architecture defines what competitive federalism looks like in operation when no sovereign will defer to the others.

VIII. Implementation path

The framework maps onto existing regulatory structure without requiring statutory amendment. Each component below identifies the operational mechanism, the time horizon, and the authority under which the Commission can act. Sequencing matters; the Commission can begin the rulemaking conversion before completing the per-se exclusion list, and can run enforcement coordination in parallel with rulemaking.

Rulemaking. The presumptive boundary lives in Rule 40.11 through definitional rulemaking adopting the contest-versus-consequence distinction and resolving “gaming” with the precision the statute requires. The four-element architecture — definitional rulemaking, modified economic purpose test, affirmative approval pathway, non-displacement clause — appears in MindCast: Defining “Gaming” Under the Commodity Exchange Act. The framework specifies what those four elements look like in operation, extended to address informational integrity and federal-state-tribal coordination.

Affirmative approval. The functional override lives in Rule 40.3. Consequence-based contracts move out of self-certification under Rule 40.2 and into affirmative approval, where the public interest determination Congress required gets made on a developed record including design integrity and informational integrity evidence.

Competitive Federalism Architecture. Express text in Rule 40.11 implements the Section VII architecture: jurisdictional clarity, Dual-Gate Reporting, geofencing protocols, IGRA non-displacement, the published coordination protocol, and the due process clause for event-contract manipulation investigations.

Per-se exclusions. Express text in Rule 40.11 codifies the categorical exclusion of negative-outcome and individual-targeting contracts specified in Section IV — under bets, injury and penalty props, mention props, and any contract whose payout structure creates a financial incentive for participants to wish, encourage, or facilitate harm to a named individual.

Enforcement coordination. A CFTC–DOJ Insider Trading Task Force institutionalizes the Van Dyke enforcement template across consequence-based contract categories, with FBI counterintelligence channels available for security-sensitive categories.

Pilot listings and record building. Approve a limited set of contracts meeting the standard with enhanced reporting. Collect data on participant composition, hedging use, price informativeness, and surveillance performance — the evidence the five-factor test requires.

Adjudication. Apply the framework consistently across enforcement and listing decisions to withstand arbitrary-and-capricious review.

A consequence the architecture produces automatically: completing Rule 40.11 supplies registered entities with a definitional standard against which the Commission can measure compliance, closing the prospective private enforcement exposure under 7 U.S.C. § 25(b) MindCast: The Rule 40.11 Paradox identifies as the residual liability track surviving any preemption ruling.

IX. Foresight and falsification

The framework generates testable predictions about what each regulatory path produces. Each prediction ties to mechanism — constraint, behavior, outcome. Each prediction carries an explicit falsification window and an observable signal MindCast will track post-publication.

Prediction A — pure bright-line. If regulators maintain categorical exclusions, economically material risk-transfer activity will migrate to adjacent or offshore venues within 12–24 months — because exclusion removes regulated pathways while leaving demand intact. The migration pattern fits the regulatory arbitrage dynamics mapped in MindCast: Federal Digital-Asset Control, where infrastructure positioning rather than classification determines effective jurisdiction.

Falsification: No measurable migration or emergence of substitutes in adjacent venues by T+24 months.

Prediction B — pure functional without boundary. If regulators adopt an open-ended functional approach without a presumption, courts will reject the regime within 12–18 months of challenge — because Loper Bright requires independent statutory analysis and an unbounded functional regime supplies no limiting principle for the panel to apply.

Falsification: Courts uphold an unbounded functional regime on merits review.

Prediction C — informational-integrity gap without surveillance architecture. If regulators adopt a functional standard without an ex ante informational integrity factor, additional misappropriation cases will surface within 6–12 months — because the Van Dyke indictment establishes both the enforcement template and the contract-architecture vulnerability, and follow-on conduct represents the predicted equilibrium response to a surveillance gap platforms cannot close unilaterally.

Falsification: No additional charged misappropriation cases involving cleared personnel, regulatory insiders, or other category-vulnerable participants within 12 months.

Prediction D — hybrid adoption. If regulators implement the hybrid framework with the five-factor test and the Competitive Federalism Architecture, the market will converge on a smaller set of defensible contracts within 18–30 months — because design integrity at listing prevents engineered workarounds, informational integrity prevents misappropriation-vulnerable categories from entering the system, affirmative approval generates the contemporaneous record courts credit, and Dual-Gate Reporting forecloses the state-federal collision pattern driving the multi-forum litigation web. The convergence corresponds to the Trajectory A configuration under a completed Rule 40.11 in MindCast: Prediction Markets Litigation Stack — the only configuration allowing the regulatory system itself to resolve. The framework names the resulting state Admissibility-Constrained Market Equilibrium — a market populated by contracts that survive both the contest-versus-consequence sort and the five-factor functional override, traded on infrastructure that meets the informational integrity threshold, with state and tribal authority preserved over conduct on the contest side of the boundary.

Falsification: Persistent cross-forum inconsistency and high reversal rates of agency decisions after T+30 months — the equilibrium signature mapped in MindCast: MCAI Lex Vision Visual Companion.

X. Why this reconciles the camps

The framework reconciles five analytical camps without surrendering any of their core commitments. Each camp’s strongest argument finds operational expression in the rule architecture above. The reconciliation operates structurally rather than rhetorically: each camp gains text on the face of the rule rather than acknowledgment in the preamble.

The bright-line camp remains correct that the Commodity Exchange Act cannot become a general license for wagering on any event with informational value. The functional camp remains correct that modern economic exposure does not always appear on the face of the event. The enforcement camp remains correct that surveillance architecture must operate at listing rather than after damage. The federalism camp remains correct that state and tribal authority over gaming and consumer protection cannot be displaced by a federal statute that never contemplated the collision. The athlete-protection camp remains correct that contract architecture engineered to monetize harm to identifiable individuals — and information channels that exclude the affected individual from investigations adjudicating their own conduct — represent failures of fundamental due process the rule must address.

A coherent legal standard requires all five: a contest-versus-consequence sort, a five-factor functional override including informational integrity reaching athlete and league information, an affirmative approval pathway, a competitive federalism architecture with Dual-Gate Reporting, and per-se exclusion of negative-outcome and individual-targeting contracts coupled with symmetric due process for affected individuals. The framework above operates at all five levels simultaneously.

The framework also reconciles two analytical postures inside the MindCast corpus itself. MindCast: Defining “Gaming” Under the Commodity Exchange Act names the Rule 40.11 definitional gap as the institutional vulnerability driving the litigation web; the present publication takes Congress as having supplied the statutory boundary and specifies the rule architecture that closes the operational gap. Both arguments converge on the same regulatory action — completing Rule 40.11 — at different levels of articulation. The Van Dyke indictment confirms the cost of further deferral now includes criminal misappropriation exposure the current rule cannot prevent.

XI. Bottom line

The Commodity Exchange Act does not fail to draw the line. The system fails because the rule that enforces it remains incomplete. The framework above restores the rule in a form courts can apply, regulators can administer, markets cannot evade, insiders cannot exploit, and contract architects cannot engineer to profit from harm to identifiable individuals.

Citation architecture (two-degree support)

Degree one — direct foundations

MindCast: Defining “Gaming” Under the Commodity Exchange Act, The Rule 40.11 Gap Driving the Nationwide Kalshi Litigation Web — establishes the economic-purpose screen and Rule 40.11 stabilization logic the framework operationalizes.

MindCast: The Rule 40.11 Paradox — Kalshi, the Third Circuit, and the Class Action the Ninth Circuit Cannot Ignore — demonstrates how definitional ambiguity creates compounding private liability under 7 U.S.C. § 25(b) rather than regulatory pause.

MindCast: Federal Digital-Asset Control — situates prediction markets within a broader control system governed by feedback latency and execution constraints; anchors Prediction A’s migration mechanism.

MindCast: How Institutional Capital Moves Under Federal Digital-Asset Control — shows capital preference for compliant, low-latency infrastructure over classification-dependent models; supports the market-participant compliance posture the design integrity and informational integrity factors incentivize.

Degree two — structural extensions

MindCast: Kalshi, Prediction Markets and the Conflict Architecture of Regulation — maps the Regulatory–Market Feedback Loop, develops the full Loper Bright–Chenery–State Farm–Encino Motorcars deference stack, and explains why unresolved jurisdiction becomes an equilibrium state.

MindCast: Prediction Markets Litigation Stack — Federal, Private, and State Enforcement Converge — demonstrates four-track cross-forum interaction; supplies the trajectory architecture against which Prediction D is mapped.

MindCast: MCAI Lex Vision Visual Companion — provides structural visualization of the litigation stack and institutional interaction dynamics; supports the falsification-signal architecture for Prediction D.

MindCast: Kalshi Found the One Gap in American Gaming Law Nobody Closed — quantifies the recreational-flow versus hedging-flow asymmetry anchoring the worked-example analysis of the federal election outcome contract under design integrity.

External primary references

Nick Devor, Gary Gensler Paved the Way for Prediction Markets. Sports Betting Wasn’t Part of the Plan, Barron’s, April 15, 2026 — supplies high-value Dodd-Frank drafting-history evidence from a principal architect of the swaps regime. Former CFTC Chairman and SEC Chairman Gary Gensler states on the record that the swap definition was not intended to encompass sports event contracts; that the inclusion of the word gaming in CEA § 5c(c)(5)(C) was a Reid-driven priority so the CFTC could prohibit it; and that betting on sports is gaming. The interview supplies a principal-author response to the textualist swap-definition argument the federal preemption theory relies on.

United States v. Van Dyke, indictment unsealed April 23, 2026 (S.D.N.Y.), and parallel CFTC civil action — establish the misappropriation enforcement template the informational integrity factor and the CFTC–DOJ Insider Trading Task Force institutionalize.

National Football League Players Association, Major League Baseball Players Association, National Basketball Players Association, National Hockey League Players’ Association, and Major League Soccer Players Association, joint comment to RIN 3038-AF65, April 30, 2026 — establishes the athlete-protection and due-process record the framework’s per-se exclusion of negative-outcome contracts, the extension of informational integrity to athlete and league information, and the due process clause in Section VII operationalize.

Brief of the States of Nevada, Ohio, and 36 other Amici States in Commonwealth of Massachusetts v. KalshiEX LLC, No. SJC-13906 (Mass. Sup. Jud. Ct. Apr. 24, 2026) — establishes the bipartisan thirty-eight-jurisdiction record that the Commodity Exchange Act does not preempt state gambling regulation and that state and tribal authority over the activity coexists with federal authority over the trade. The brief supports the framework’s contest-versus-consequence sort, the Competitive Federalism Architecture’s jurisdictional allocation, and the Dual-Gate Reporting and geofencing protocols.

Indian Gaming Association statement, 29th Annual Western Indian Gaming Conference, February 2026, and IGA Chairman David Bean public testimony — establishes the tribal sovereignty institutional position on the IGRA collision the framework’s non-displacement clause addresses.

Project On Government Oversight, Public Comment to CFTC RIN 3038-AF65, April 28, 2026 — establishes the public-interest organization record supporting categorical exclusion of contracts on death, political events, and contracts creating material non-public information incentives for government officials. The framework reaches the same exclusion result for political and electoral contracts through the five-factor test, supporting the framework’s per-se exclusion architecture for negative-outcome and individual-targeting categories and the framework’s informational integrity factor for the MNPI dimension.

KalshiEX LLC v. Flaherty, No. 25-1922 (3d Cir. Apr. 6, 2026) — the Third Circuit dissent reads Rule 40.11 in the contest-based direction the framework adopts; the majority’s silence on Rule 40.11 is the doctrinal space the framework’s definitional rulemaking fills.

CFTC Division of Market Oversight Staff Letter No. 26-08, March 12, 2026 — establishes the CFTC–DCM–league–integrity-monitor information-sharing architecture the framework’s due process clause renders symmetric for affected individuals. CFTC announcement at CFTC Press Release 9193-26.

CFTC ANPRM, Prediction Markets, 91 Fed. Reg. 12516 (Mar. 16, 2026) — the open rulemaking docket the framework’s definitional and procedural elements respond to. CFTC announcement at CFTC Press Release 9194-26.

Appendix — Competitive federalism allocation diagram

The structural diagram below shows how authority is allocated between federal, state, and tribal sovereigns under the framework. The line Congress drew sits at the top as the operating constraint. The underlying-exposure litmus test operates as the sorting mechanism. Contests route to state and tribal authority. Consequences route to federal authority subject to the five-factor functional override and Rule 40.3 affirmative approval. The allocation operates without requiring federal-state-tribal coordination; each sovereign retains authority within its sphere on its own statutory and constitutional grounds.

Each sovereign retains authority within its sphere. Operable without federal-state-tribal coordination.

The diagram operates as a partner-facing reference tool. State and tribal partners can paste the diagram into internal briefings, council resolutions, attorney general memos, or legislative findings without modification. The allocation it specifies does not depend on CFTC adoption of any framework, federal court ruling on any pending case, or congressional amendment to any statute. The allocation specifies the equilibrium each sovereign can defend within its existing authority.

The publication responds to ongoing public dialogue across federal, state, and tribal forums on the statutory boundary question and the implications of federal prediction-market preemption for state and tribal authority.