MCAI Market Vision: Kalshi's Institutional Push Is Building the Case Against Itself

Why the Infrastructure Prediction Markets Build to Win Institutional Capital Is the Same Infrastructure That Wins the Regulators' Case

Abstract for litigators, rulemaking staff, and institutional allocators. The institutional infrastructure prediction-market platforms began building in 2026 — FCM membership, clearing, block trades, and prime-broker intermediation — supplies evidence relevant to the classification question already at issue in the pending Kalshi proceedings. Kalshi’s first bespoke institutional block trade, a hedge on the clearing price of California’s May 2026 carbon allowance auction, structured through a clearing member with a dedicated liquidity provider, performs economic risk transfer rather than wagering on a contest. The transaction is usable as economic-purpose evidence under the screen proposed in the MindCast CFTC public comment on RIN 3038-AF65. One trade does not fix the dominant character of a venue; the relevant claim is narrower and more durable — institutional infrastructure shifts the evidentiary and classification posture of the venue, even where individual contracts still require separate analysis under the contest-versus-consequence boundary. Federal clearing does not displace state police-power authority absent clear congressional displacement, so institutional onboarding widens rather than closes the federal-state split. Practitioners may treat the block-trade structure as a discrete fact pattern; the analysis below situates it.

Prediction markets crossed an invisible line in May 2026. The moment institutional prime brokers, clearing infrastructure, and liquidity intermediaries entered the market, the industry’s growth strategy began strengthening the exact derivative characterization the platforms spent two years resisting in court.

Reuters reported the build-out on May 27, 2026. Clear Street became the first institutional Futures Commission Merchant to join Kalshi’s exchange and clearing house. Marex started building the infrastructure connecting investors to both Kalshi and Polymarket. Jump Trading began routing institutional flow toward the venues. Analysts framed the open question as liquidity — shallow order books cannot absorb the size that hedge funds move.

Liquidity is the surface problem. The deeper movement runs the other direction.

Prediction markets now face a structural inversion: the infrastructure required to attract institutional capital strengthens the derivative characterization the platforms previously resisted. Retail markets survived on ambiguity. Institutional markets cannot. Every layer added to satisfy institutional capital moves the instruments closer to the regulators’ case and reshapes the evidentiary posture across the nationwide Kalshi litigation web in the Commodity Futures Trading Commission’s favor. Growth and legal exposure no longer oppose each other. The two now move together.

I. The Phase Transition Changes the Legal Geometry

Retail prediction markets survive on ambiguity, novelty, and low systemic significance. A thin venue trading small contracts on contested classification poses little to the financial system and little to a court’s sense of urgency. Ambiguity protects the platform.

Institutional prediction markets require the opposite. Standardized intermediation, clearing reliability, liquidity depth, compliance architecture, and counterparty trust become non-negotiable the moment a hedge fund considers routing real size. Each requirement pulls the instrument toward the structure of a traditional derivatives market.

The two phases carry opposite legal incentives, and the reversal is the whole story.

A platform that spent two years arguing it does not run derivatives must now build derivatives infrastructure to grow. A venue can still host individual contracts that fall outside proper CEA scope — the contest-versus-consequence boundary continues to sort them. The general posture, however, grows harder to hold with every layer added: the more the platform looks and clears like a derivatives market, the steeper the climb to argue it is not one.

Growth does not merely scale the platform. Growth changes the classification problem itself.

II. The Block Trade Instantiates the Economic Purpose Test

Kalshi executed its first bespoke institutional block trade in May 2026. Greenlight Commodities brokered the deal. A Houston environmental hedge fund took the position. Jump Trading supplied liquidity. The contract resolved on the clearing price of California’s May carbon allowance auction.

Speculation alone would not change anything. Hedge funds speculate in nearly every asset class without converting those assets into regulated derivatives. The classification pressure emerges from a different source: the architecture surrounding the trade, not the appetite for risk inside it.

Examine the roles, because each one is a fact a court can find. A hedge fund manages defined exposure to carbon allowance prices. A liquidity provider warehouses the offsetting risk. A clearing house guarantees settlement. A broker intermediates institutional execution. Each participant occupies a defined economic position inside a hedging and liquidity ecosystem — the exact division of labor that regulated derivatives markets exist to support. A carbon-auction hedge built that way does not wager on a contest. The structure performs genuine risk transfer for real capital exposure, and the record of who played which role establishes the function on the face of the transaction rather than by inference.

Earlier MindCast work drew the line the trade crosses. A Boundary Rule with a Functional Core holds that derivatives manage economic risk while wagering on outcomes detached from exposure falls outside the federal derivatives system. The carbon contract sits unambiguously on the derivatives side.

The MindCast CFTC public comment filed April 17, 2026 supplied the screen that sorts the two. Defining “Gaming” Under the Commodity Exchange Act proposed a modified economic purpose test turning on a contract’s function rather than its event label. Reuters described the institutional build-out six weeks later. The platforms, reaching for institutional depth, are now manufacturing the factual record that satisfies the functional-core override the comment specified. The economic purpose test no longer needs a hypothetical. Kalshi supplied one.

One trade does not establish the dominant character of the venue, and the argument does not require it to. A single transaction proves the structure exists and functions as risk transfer. The dominant-character question turns on trajectory, not on one contract — and the trajectory is what the forecast below addresses.

III. The Intermediation Layer Cannot Dissolve the State-Law Question

Clearing, settlement, swap wrappers, and block-trade desks answer one question: how the trade clears. None of the machinery answers a separate question: what the activity is.

Earlier analysis of the Washington remand named the distinction the prime-broker layer cannot collapse. Kalshi Loses Federal Forum established that federal authority over how a trade clears is a different question from state authority over what the underlying conduct is. Kalshi’s removal theory tried to make the first answer the second. The Washington court refused.

A doctrinal anchor states the point plainly. A federally cleared transaction can still constitute prohibited gambling activity under state law unless Congress clearly displaced state police-power authority. Sophistication in the plumbing does not supply that displacement. Clear Street’s FCM membership deepens the federal-derivative characterization of the execution while leaving state police-power claims fully intact.

Balance requires one limiting principle. Congress or future rulemaking could still broaden federal displacement, and a decisive Ninth Circuit ruling could compress state authority sharply. Present statutory structure, however, does not automatically convert federally cleared activity into federally exclusive jurisdiction. Institutional onboarding therefore widens the split between federal-preemption logic and state-classification authority rather than closing it. The more institutional the venue becomes, the stronger both sides of the conflict grow at once.

Contact mcai@mindcast-ai.com to partner with us on Predictive Game Theory AI in Law and Behavioral Economics. To deep dive on MindCast work in Cognitive AI upload the URL of this publication into any LLM (preferably Google AI mode) and prompt ‘reconstruct MindCast framework with three degrees of cited sub links.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure

IV. Growth Accelerates Entry Into the Delay-Dominant Equilibrium

Earlier MindCast work identified the system state the litigation has entered: classification deferred, liability accumulating. The Rule 40.11 Paradox documented the private right of action under 7 U.S.C. § 25(b), which runs directly against designated contract markets and clearing organizations for rule violations with no new regulatory finding required.

Institutional flow compounds the exposure, and the compounding reaches a place retail flow never did. Every increment of notional volume routed through the venues enlarges the base of transactions subject to § 25(b) damages should classification resolve against the platforms. Clearing-house membership and block-trade infrastructure raise the size of each position and the sophistication of each counterparty, which sharpens the liability profile rather than softening it.

A counterintuitive force pulls in the same direction. Institutional capital generally prefers regulated ambiguity to unregulated ambiguity, because regulated ambiguity still supplies supervisory infrastructure, clearing expectations, and counterparty norms. Sophisticated allocators therefore push the platforms toward the very classification the platforms resist — institutional demand itself favors derivative treatment.

The reputational geometry shifts as well. Retail ambiguity scales socially. Institutional ambiguity scales onto regulated balance sheets. Once brokers, custodians, prime intermediaries, and clearing participants enter the system, legal ambiguity stops being a platform’s litigation problem and becomes a counterparty’s balance-sheet risk. The commercial imperative to grow and the legal exposure that growth creates are coupled. Pursuing one deepens the other.

V. The Routing Layer Is Forming in Plain Sight

The CPI Antitrust Chronicle published the recurring analytical move: identify the routing layer, identify the conduct that captures it, and predict where enforcement arrives once the Becker phase of tolerated accumulation closes. The Routing Layer Is the Antitrust Trigger applied the frame to AI infrastructure, and the frame ports onto prediction-market plumbing without modification. Clear Street, Marex, and Jump are positioning across onboarding, custody, execution, and liquidity routing as the gateway through which institutional flow must pass to reach the exchanges.

A prediction follows directly. Once institutional routing centralizes through a small set of intermediaries, surveillance, compliance, and enforcement pressure will concentrate increasingly at the intermediation layer rather than solely at the exchange layer. Control of the gateway determines who captures the economics of institutional adoption — and concentrates the conduct that later enforcement will examine.

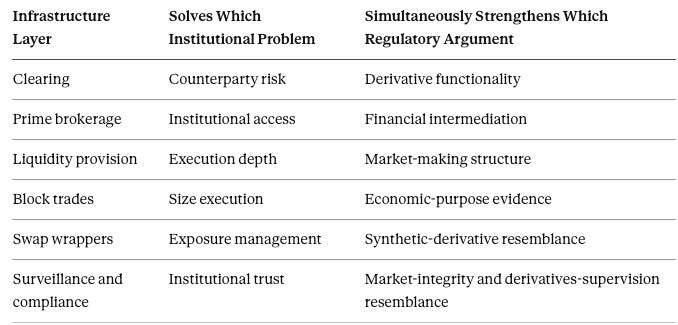

VI. The Infrastructure Matrix

One table converts the thesis from analysis into a deployable frame. Each infrastructure layer solves a real institutional problem. Each simultaneously strengthens a regulatory argument the platforms have been litigating against.

Read the table left to right and the inversion becomes mechanical. Every solution to a growth problem is, in the same motion, a contribution to the case against the platform. The surveillance row carries the sharpest edge — the same monitoring that earns institutional trust generates the insider-trading, election-manipulation, and integrity records that regulators supervising derivatives venues already expect to see.

VII. The Falsifiable Forecast

MindCast states the prediction with explicit falsification conditions.

Forecast. Institutional notional volume on Kalshi and Polymarket and adverse classification pressure will rise together across the next two to four quarters. At least one pending proceeding will cite institutional block-trade structure — the carbon-allowance contract or a successor — as evidence that the instruments perform economic risk transfer rather than gaming.

Probability band: P10 58% | P50 72% | P90 84%. Window: two to four quarters from publication.

Falsification condition: institutional volume grows materially while every court and the CFTC rulemaking record move toward narrowing CEA reach and affirming state gambling authority, with no proceeding invoking institutional trade structure as economic-purpose evidence.

VIII. What the Inversion Means for Each Stakeholder

The structural inversion lands differently on each party watching it, and naming those positions clarifies why the dynamic is stable rather than transitional. No single reader sits outside the geometry.

Litigating attorneys general and plaintiffs’ counsel. The institutional build-out supplies fresh evidence on the classification question already in front of the courts. The carbon-allowance block trade functions as a discrete fact pattern showing economic risk transfer on the face of the transaction, usable alongside the economic-purpose screen from the RIN 3038-AF65 record. Growth in institutional volume enlarges the evidentiary base over time rather than mooting the question.

CFTC and rulemaking staff. The build-out instantiates the economic-purpose distinction the ANPRM record was assembled to address. A venue developing FCM membership, clearing, and block-trade capacity demonstrates the functional core the modified economic purpose test screens for — converting a definitional debate into an observable market fact.

Institutional investors, accredited investors, and family offices. Allocators evaluating entry occupy the exposure the analysis describes, not a vantage outside it. Routing flow through a prime broker into a venue whose classification remains contested carries a private-liability tail under 7 U.S.C. § 25(b) and a reputational exposure that scales onto the allocator’s own balance sheet rather than staying with the platform. The classification uncertainty is a diligence input, and sophisticated capital generally prefers regulated ambiguity precisely because supervisory infrastructure, clearing expectations, and counterparty norms attach to it — which means allocator demand itself pushes toward the derivative characterization the platforms resist. The point here is structural, not a recommendation on whether to allocate; the exposure exists regardless of the entry decision.

Prime brokers, FCMs, and liquidity providers. Intermediaries positioning across onboarding, custody, execution, and liquidity routing capture the economics of institutional adoption and, in the same motion, concentrate the conduct that later enforcement examines. The gateway role is a revenue position and a supervisory-attention position at once.

The platforms. Kalshi and its peers face the bind the paper names throughout: the infrastructure required to grow strengthens the characterization litigated against for two years. The strategic question is no longer whether to build institutional capacity but how to build it without manufacturing the record that resolves the classification against them.

IX. Bottom Line

Prediction markets face a single problem wearing two faces. Solving the liquidity problem requires intermediation. Intermediation proves the economic-purpose case. The infrastructure built to win institutional capital is the same infrastructure that wins the regulators’ case for them.

A reusable principle sits underneath the prediction-market specifics. Institutional infrastructure does not merely support a market — institutional infrastructure determines what kind of market regulators and courts believe they are observing. The machinery built to attract serious capital rewrites the regulatory question rather than answering it, and the same dynamic governs AI compute markets and tokenized-asset venues no less than prediction markets.

A venue cannot grow into legitimacy without growing into the classification it has spent two years litigating against.

Appendix: Related MindCast Publications

The publications below extend the analysis along adjacent lines. None is load-bearing for the argument above, and none duplicates the works cited in the body. Each is grouped by the question it answers.

Why the conflict is structural rather than accidental

Kalshi, Prediction Markets and the Conflict Architecture of Regulation — models overlapping federal, state, and tribal jurisdiction and real-time market feedback as producing regulatory conflict as an equilibrium outcome rather than an accident; develops the deference stack underlying the post-Loper Bright posture.

The Full Arc of Prediction Markets — traces the jurisdictional architecture from the election-contract dispute forward, situating the CFTC-versus-state-gambling tension the Kalshi cases brought into open conflict.

How the litigation is distributed across forums

Prediction Markets Litigation Stack — Federal, Private, and State Enforcement Converge — maps the four-track convergence of federal enforcement, private § 25(b) actions, state attorneys general, and tribal challenges, and identifies Washington as the highest-density convergence node.

The National Kalshi Prediction Market Litigation Map — charts enforcement actions across multiple state jurisdictions and appellate circuits producing conflicting rulings on identical statutory text; develops the removal-asymmetry and cascade mechanics.

The Ninth Circuit on April 16 as System Convergence — frames the consolidated oral argument as the first synchronized observable test of prediction-market structure and the narrowest-ground incentive driving appellate panel behavior.

Why delay is the platform’s strategy

The Computational Era Operationalizes Cybernetics and Predictive Game Theory — names the Kalshi delay-dominant architecture directly: the platform litigates to extend the timeline until the rule changes, not to win the existing rule.

Why infrastructure status changes the governance question

Innovation Becomes Governance — Why MindCast Analyzes Infrastructure Rather Than Disruption — argues that enforcement against the present operator may harden the event-contract category for a future operator rather than dismantle it, and locates surveillance and informational-integrity questions as consequences of infrastructure status.