MCAI Market Vision: Rocket-Redfin Asks NWMLS to Rewrite Rules to Help Make Rocket-Redfin-Compass Partnership More Profitable — and Strategically Chose a Corporate News Platform Over an Amicus Brief

A Rocket Executive Published Washington SSB 6091 Statutory Interpretation on Redfin's Website Rather Than Filing in the Active Federal Lawsuit Where the Same Statute Is Being Litigated

Recent works: The Compass-Reffkin Consumer Policy Center Quote-Card Specimen — A Self-Disclosure Trap Market Analysis | Compass Double-Sided Commissions — Consumer Policy Center Measures the Output, MindCast Models the System | Two NWMLS Records, One Foster-Skillman Team — Primary-Source Evidence of the Compass Two-Gate Capture Model Inside the Washington Statutory Transition Window | Rocket-Redfin Asks NWMLS to Rewrite Rules to Help Make Rocket-Redfin-Compass Partnership More Profitable — and Strategically Chose a Corporate News Platform Over an Amicus Brief

Foundational works: The Compass Narrative Inversion Playbook | Compass’s Cross-Forum Contradictions | The Compass Commission Consolidation Strategy and Real Estate Marketing Transparency | The Antitrust Litigation Trap Compass Built for Itself | The Counterclaim That Closed Compass’s Antitrust Thesis | Zillow, eXp, and Redfin–Compass. Three Deals. Twenty Days. One Outlier.

Plain-Language Summary

In plain terms: Rocket-Redfin is asking NWMLS to rewrite its rules so the Compass partnership can operate in Washington after June 11 under a statutorily-compliant surface while preserving the architecture the statute was designed to foreclose. The rule change would convert the Gate 1 address-suppression mechanism Two NWMLS Records, One Foster-Skillman Team — Primary-Source Evidence of the Compass Two-Gate Capture Model Inside the Washington Statutory Transition Window documented on the Triptych active listing (MLS #2497151, “Undisclosed Address” designation at Day 304) from an NWMLS-visible violation of SSB 6091 into an NWMLS-permitted compliance surface. The structural analysis in the sections that follow establishes the mechanism through which the request operates, the pattern the request continues, and the cross-forum evidentiary consequences the request produces inside the active Compass v. NWMLS discovery window. The plain-language framing and the structural framing describe the same institutional move at different registers of analytical precision.

The analytical architecture operates across three disciplines simultaneously: legal constraints define the boundary, behavioral incentives drive the actions within it, and strategic interaction determines why those actions repeat across forums. Law supplies the constraint geometry (SSB 6091, the Compass v. NWMLS docket, Federal Rules of Evidence 801). Behavioral economics supplies the motive force (Posner welfare-transfer mechanics, Friedman price-discovery disabling, Becker cost-inversion across two balance sheets). Game theory supplies the system dynamics — the Rocket-Redfin-Compass coalition has entered a delay-dominant equilibrium in which all three coalition members benefit from postponing full transparency while preserving routing control, and the April 16 Rath communication is the coalition’s rational move in that game.

I. Framing

When distribution control becomes the binding constraint, firms will reinterpret transparency rules to preserve routing authority. The Rath communication is that reinterpretation.

Joe Rath, Head of Industry Relations at Rocket, published a corporate communication on Redfin’s news platform on April 16, 2026, titled “Redfin Calls on NWMLS to Give Home Sellers More Choice.” The communication asks the Northwest Multiple Listing Service (NWMLS) to adopt an intra-MLS premarketing phase, stakes a public statutory interpretation of Substitute Senate Bill (SSB) 6091’s June 11, 2026 effective date, and positions Redfin.com as the proposed premarketing display surface. The communication is signed by a Rocket executive with direct MLS-relations authority across the combined Rocket-Redfin national footprint and published through Redfin’s institutional communications channel.

The timing is the first structural fact. The Rath communication lands 24 hours after the Compass-Reffkin Consumer Policy Center Quote-Card Specimen analyzed as Self-Disclosure Trap Specimen 1, 14 days after NWMLS filed its four-count counterclaim on April 2, 2026, 29 days after the twenty-day syndication stack documented in Zillow, eXp, and Redfin–Compass. Three Deals. Twenty Days. One Outlier. closed on March 18, 2026, and 56 days before SSB 6091’s statutory effective date. The communication’s specific ask is that NWMLS revise its rules to permit a premarketing status within the MLS, with seller consent and public platform visibility substituting for the concurrent-marketing requirement the statute is designed to establish.

The communication operates as Self-Disclosure Trap Specimen 2 of the Part III consolidation the April 16 Compass-Reffkin Consumer Policy Center Quote-Card Specimen Section X identified as requiring five to seven additional specimens across two or more categories before Part III publication readiness. Specimen 1 (Reffkin, April 16) operates at the CEO-social-media layer. Specimen 2 (Rath, April 16) operates at the institutional-partnership corporate-communications layer — a separate behavioral category from the Specimen 1 register.

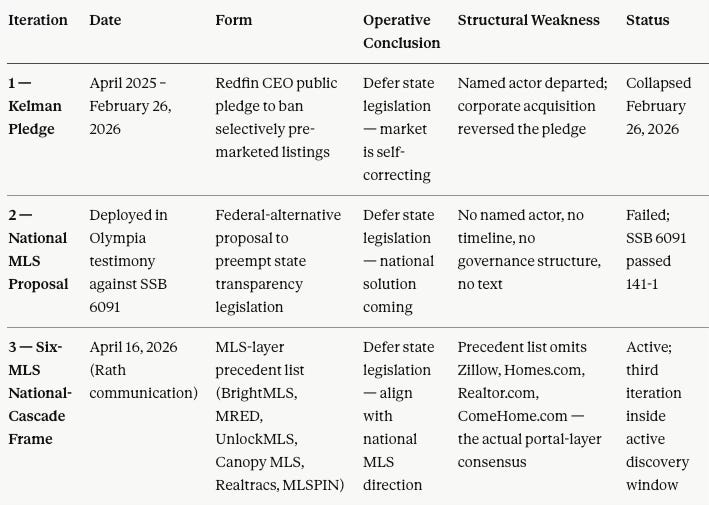

The communication also operates as the third documented iteration of the Compass self-correction defense — the rhetorical architecture Zillow, eXp, and Redfin–Compass. Three Deals. Twenty Days. One Outlier. Section V catalogued across two prior deployments. Iteration 1: the Kelman pledge (April 2025, reversed following the Rocket acquisition). Iteration 2: the national MLS proposal (deployed in Olympia testimony against SSB 6091). Iteration 3: the six-MLS national-cascade frame advanced in the April 16 Rath communication. Each iteration performs the same operative function — supply fence-sitting legislators a procedurally defensible reason to defer state-level concurrent-marketing legislation — through a different surface form. The present analysis documents the third iteration as a continuation of the pattern, not as a new argumentative frame.

II. What the Communication Actually Says — Five Structural Moves

Five discrete moves operate in the Rath communication, each carrying independent analytical consequence.

Move 1: Reclassification of “seller choice” from Compass framing to Rocket-Redfin corporate position. The communication opens with “Redfin supports a seller’s choice in how their property is marketed, including premarketing to test pricing and demand.” The Reffkin-Skillman “seller choice” framing The Compass Narrative Inversion Playbookcatalogued as the defining narrative-inversion move is now Rocket-Redfin’s stated corporate position, published through Redfin’s institutional communications channel by a Rocket executive. The framing has crossed from Compass’s advocacy to the Rocket-Redfin coalition’s advocacy.

Move 2: Public statutory interpretation of SSB 6091. The communication states that Redfin believes the statute supports premarketing with public marketing and seller consent. The interpretation reads SSB 6091’s concurrent-marketing requirement as satisfied by public platform display rather than by MLS-concurrent exposure. The interpretation is published on a Rocket-Redfin corporate platform, signed by a Rocket executive with MLS-relations authority, inside the active Compass v. NWMLS discovery window in which the opposite statutory reading is the basis of NWMLS’s pending declaratory judgment count at Document 88.

Move 3: Redfin.com as proposed premarketing display surface. The communication specifies public display on a site like Redfin.com as satisfying the broad-visibility requirement. The architecture operationalizes the demand-side capture vector Compass Double-Sided Commissions — Consumer Policy Center Measures the Output, MindCast Models the System Prediction 2 identified as the mechanism through which listing-side premarketing compounds with Rocket mortgage origination and Redfin buyer-funnel integration to produce intra-system transaction capture. The proposal moves the demand-side capture architecture from internal product development into public regulatory advocacy.

The proposal also operates as a direct retrofit of the Gate 1 address-suppression mechanism documented in Two NWMLS Records, One Foster-Skillman Team — Primary-Source Evidence of the Compass Two-Gate Capture Model Inside the Washington Statutory Transition Window. The April 17 Two-Gate analysis documented Gate 1 operating on the Triptych active listing (MLS #2497151) at Day 304 of public market exposure under “Undisclosed Address” designation — the suppression mechanism SSB 6091’s concurrent-marketing requirement is designed to foreclose at the June 11 effective date. The Rath April 16 proposal would convert the same mechanism from an NWMLS-visible violation of the statute into an NWMLS-permitted compliance surface by reclassifying the Redfin.com display architecture as intra-MLS premarketing rather than private-phase suppression. The statutory architecture changes; the operational mechanism does not.

Move 4: Six-MLS national-cascade frame — the third self-correction defense iteration. The communication names six MLSs as precedent for intra-MLS premarketing adoption: BrightMLS, MRED in Chicago, UnlockMLS in Austin, Canopy MLS, Realtracs, and MLSPIN. The list omits Zillow, the portal-layer actor Zillow, eXp, and Redfin–Compass. Three Deals. Twenty Days. One Outlier. identified as having voluntarily built the open-distribution architecture SSB 6091 mandates. The list also omits Homes.com, Realtor.com, and ComeHome.com — the three portals the same publication identified as receiving eXp’s March 18 three-portal syndication on explicitly non-exclusive terms.

The omissions are analytically significant, and the mechanism is specific: the six-MLS list deploys MLS-layer examples to obscure portal-layer consensus because portals determine buyer access, not MLS policy alone. MLSs set rules that member brokers must follow to list inventory; portals determine which buyers see which listings and how data fields display to those buyers. The buyer-access architecture — days-on-market data visibility, price-drop history display, valuation estimate presentation, inquiry routing — operates at the portal layer, not the MLS layer. The March 18 twenty-day syndication stack documented portal-layer actors moving voluntarily toward open distribution; the April 16 Rath frame substitutes MLS-layer actors as the consensus proxy because the portal-layer record contradicts the Rocket-Redfin-Compass architecture directly. The substitution is the specific rhetorical move through which the self-correction defense’s third iteration attempts to survive the March 18 evidentiary record.

Move 5: “Productive conversations” language with named NWMLS leadership. The communication closes with characterization of NWMLS leaders as open to the rule-change proposal. The framing converts a regulatory-rule-change ask into a characterization of NWMLS’s institutional openness. The characterization is published without NWMLS confirmation, inside a discovery window in which NWMLS’s institutional position is a matter of federal court record through Document 88’s counterclaim.

Contact mcai@mindcast-ai.com to partner with us on Predictive Law and Behavioral Economics + Game Theory Foresight Simulations. To deep dive on MindCast upload the URL of this publication into any LLM (preferably ChatGPT or Gemini for magazine style works) and prompt ‘reconstruct MindCast framework with three degrees of cited sub links.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure.

III. The Self-Correction Defense Pattern — Third Iteration Documented

Zillow, eXp, and Redfin–Compass. Three Deals. Twenty Days. One Outlier. Section V catalogued the self-correction defense as the rhetorical architecture Compass has deployed to give fence-sitting legislators a procedurally defensible reason to defer state-level concurrent-marketing legislation. The defense operates through an identical operative structure across iterations: advance a proposed alternative that does not actually constrain Compass’s behavior in the interim period during which the waiting occurs.

Iteration 1 — The Kelman pledge (April 2025 through February 26, 2026). Redfin CEO Glenn Kelman publicly pledged in April 2025 to ban listings selectively pre-marketed without MLS exposure. Industry opponents deployed the pledge in every prior state legislative hearing as evidence that the market was already self-correcting and legislation was premature. Rocket’s acquisition of Redfin closed. The pledge reversed within months. Kelman departed. Redfin’s February 26, 2026 statement framed the reversal as “our perspective evolved.” The self-correction defense’s primary legislative exhibit was destroyed on the same day Compass issued its Redfin partnership press release.

Iteration 2 — The national MLS proposal (Olympia testimony against SSB 6091). Following the Kelman pledge collapse, Compass redeployed the self-correction argument in a new form: state-by-state concurrent marketing legislation is fragmented, a national MLS would achieve the transparency goals more efficiently, therefore state legislation is premature and should yield to the national solution. The March 18 analysis identified the rhetorical function as identical to the Kelman pledge — both arguments share the same operative conclusion (wait) and both arrive through a proposed alternative that does not constrain Compass’s behavior in the waiting period. The national MLS proposal carried weaker anchors than the pledge it replaced: no named actor, no stated enforcement date, no legislative timeline, no governance structure foreclosing the private-listing exceptions Compass was simultaneously defending.

Iteration 3 — The six-MLS national-cascade frame (Rath, April 16, 2026). The Rath communication advances the structurally identical operative argument: a settled national direction exists across six MLSs, Washington is the outlier, NWMLS should align with the national direction through rule change rather than operating under the concurrent-marketing statute the Washington legislature enacted 141-1. The operative conclusion remains the same — wait for the national direction to resolve the Washington statutory question — and the proposed alternative again does not constrain Rocket-Redfin-Compass behavior in the waiting period. The six-MLS precedent list selectively excludes Zillow, Homes.com, Realtor.com, and ComeHome.com — the four portal-layer actors the twenty-day syndication stack documented moving in the opposite direction of the frame the list is designed to support.

The third iteration carries two distinctive features the prior two did not. First, the iteration is signed by a Rocket executive rather than by Compass leadership — extending the rhetorical architecture across the Rocket-Redfin-Compass coalition for the first time. Second, the iteration is published inside the active Compass v. NWMLS discovery window, converting the self-correction defense from a legislative-forum deployment into a cross-forum deployment available as federal-court impeachment material.

Table 1 — Three-Iteration Self-Correction Defense Pattern

The pattern is now documented three times across thirteen months. Each iteration loses analytical force as the surrounding evidentiary record compounds. Legislative staff evaluating the third iteration in successor jurisdictions (Illinois, California, New York, Texas) inherit the record of the prior two iterations, the voluntary industry consensus the twenty-day stack documented, and the cross-forum contradictions Compass’s Cross-Forum Contradictions catalogued. The self-correction defense’s diminishing returns are the structural signature of a rhetorical architecture approaching exhaustion.

IV. The Twenty-Day Syndication Stack Reread Through April 16

Zillow, eXp, and Redfin–Compass. Three Deals. Twenty Days. One Outlier. documented three deals between February 26 and March 18, 2026: the Compass-Redfin partnership (February 26), Zillow Preview (March 17), and the eXp three-portal syndication with Homes.com, Realtor.com, and ComeHome.com (March 18). The publication identified Compass-Redfin as the structural outlier — the only architecture in the sequence built to route buyers rather than reach them — and documented the Realtor.com CEO’s characterization of the eXp architecture: equal access for all buyers, not a subset selected by the listing agent.

The April 16 Rath communication is the Rocket-Redfin retrofit attempt against the twenty-day-stack outcome. The retrofit reframes the outlier as representative, substitutes MLS-layer consensus for portal-layer consensus, and preserves Redfin.com as the premarketing display surface under statutorily-authorized framing rather than contract-executed framing. None of the moves neutralize the March 18 findings: the Compass-Redfin architecture remains the structural outlier; the data suppression remains the mechanism distinguishing the architecture from Zillow Preview and the eXp three-portal deal; and the Becker switching-cost asymmetry remains the governing behavioral explanation for why Compass alone cannot exit private-control architecture.

The April 16 Rath communication adds a second balance sheet to the Becker analysis the March 18 publication ran on Compass alone. Rocket carries its own acquisition debt from the Redfin transaction. The Rath communication is Rocket-Redfin’s rational response to its own cost inversion — the second balance sheet whose debt service depends on the architecture the March 18 publication identified as the regulatory ratchet’s termination point. Section VIII documents the two-balance-sheet Becker extension directly.

V. Why the Communication Is a Self-Disclosure Trap Specimen

The Cybernetics of Compass Holdings’ Narrative Control Architecture formalized the Self-Disclosure Trap as the pattern in which the most damaging evidence is self-generated and the exposure requires no investigation, only compilation. The Counterclaim That Closed Compass’s Antitrust Thesis operationalized the pattern inside federal litigation. The April 16 Reffkin specimen extended the pattern to CEO social media inside the active discovery window. The April 16 Rath communication extends the pattern to institutional-partnership corporate-communications layer across two balance sheets.

Three mechanics operate simultaneously.

Rocket-Redfin statutory interpretation becomes available to NWMLS trial counsel. The Rath communication’s public statement reading SSB 6091 as permissive of premarketing with public-platform display and seller consent is now documented on a Rocket-Redfin corporate channel, signed by a named Rocket executive, timestamped April 16, 2026. The statement is directly adverse to the NWMLS statutory reading that grounds the Document 88 declaratory judgment count. The statement is also structurally aligned with the Compass Olympia testimony position. The institutional alignment Compass and Rocket-Redfin announced through the February 23, 2026 partnership is now documented on a regulatory-interpretation question inside the active discovery window.

The demand-side capture vector is publicly proposed as regulatory rule change. The architecture Compass Double-Sided Commissions — Consumer Policy Center Measures the Output, MindCast Models the System Prediction 2 identified is now publicly proposed as the remedy Rocket-Redfin seeks from the institutional actor currently litigating against Compass on the same subject matter. The Rath communication moves the Redfin.com premarketing display surface from internal contract architecture (the February 26 Compass-Redfin partnership terms) into public regulatory advocacy.

Six-MLS national-cascade frame supplies NWMLS trial counsel an additional estoppel predicate. The Counterclaim That Closed Compass’s Antitrust Thesis Section II identified the cross-forum market-definition lock as a structural vulnerability converging at NWMLS summary judgment. The Rath communication’s six-MLS national-cascade frame is a national-market argument published on a Rocket-Redfin corporate channel while Compass’s Compass v. NWMLS pleading narrows the relevant market to Seattle and King County. Any Compass argument that relies on MLS-specific regional conditions now confronts a Rocket-Redfin corporate position that treats the six-MLS national precedent as the controlling frame.

The Rath communication operates at the institutional-partnership corporate-communications layer of the MindCast AI corpus. Two NWMLS Records, One Foster-Skillman Team — Primary-Source Evidence of the Compass Two-Gate Capture Model Inside the Washington Statutory Transition Window documented the complementary market-conduct layer — two NWMLS records (MLS #2497151 and MLS #2468181) publicly verifiable on the same date (April 17, 2026) as the present analysis, documenting the Two-Gate Capture Model operating under a single Foster-Skillman Compass team credential on two simultaneous Washington-market properties. The two pieces operate as companion registers on the same Washington statutory transition window: the Two-Gate piece documents what Compass does in the market; the present analysis documents what Rocket-Redfin says about what Compass does, asks NWMLS to authorize, and publishes outside the federal-court procedural constraints the Two-Gate market-conduct evidence will eventually confront at summary judgment. Both registers feed Document 88’s counterclaim architecture. Both registers are available to NWMLS trial counsel as publicly-accessible primary-source material requiring no discovery process to obtain.

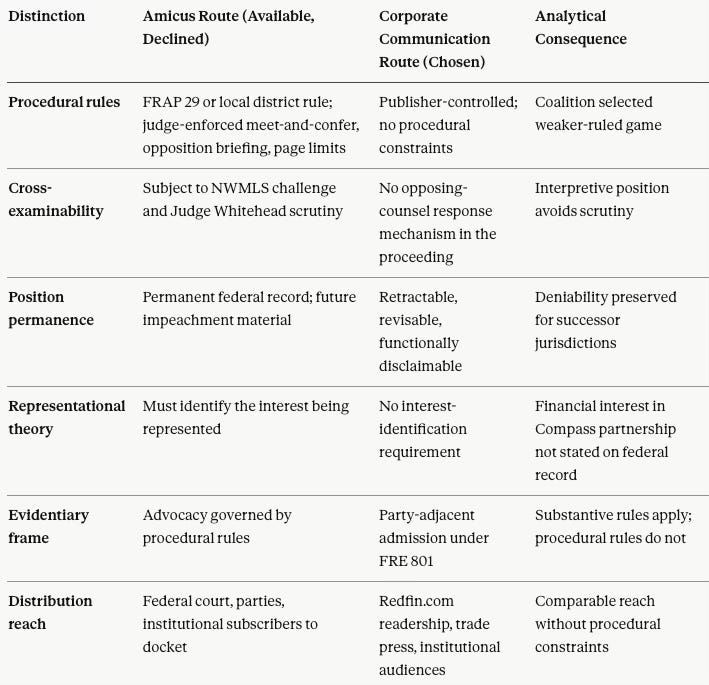

VI. The Amicus Route Declined — Forum Selection as Analytical Signal

The Rath communication’s distribution channel is itself a specimen of the position it advances. Rocket-Redfin possesses the institutional resources, the legal sophistication, and the direct adversarial interest to file an amicus brief in Compass v. NWMLS, Case No. 2:25-cv-00766-JNW, before Judge Whitehead in the Western District of Washington. The proceeding is active, the counterclaim’s declaratory judgment count raises the SSB 6091 statutory interpretation question directly, and the discovery window creates the procedural opportunity for amicus participation. Rocket-Redfin chose the Redfin news platform instead. The choice is analytically significant — the amicus route declined is a forum-selection signal that documents the specific procedural constraints Rocket-Redfin’s interpretive position could not absorb.

Four structural distinctions separate the amicus route from the corporate-communication route, and each distinction maps directly to a procedural constraint the Rath communication avoids.

Amicus briefs are cross-examinable; corporate communications are not. An amicus brief filed under Federal Rule of Appellate Procedure 29 or the Western District’s local equivalent for district-court amicus practice enters the federal court record subject to challenge by NWMLS trial counsel, scrutiny by Judge Whitehead, and authorship identification through the signature block. The filed position becomes subject to the procedural rules governing the proceeding — meet-and-confer obligations, opposition briefing schedules, page limits, and the court’s scheduling order. The Rath communication carries none of those exposures. The communication publishes the same interpretive claims on a platform where NWMLS cannot respond through federal court procedure and where the authors’ conduct falls outside the active discovery scope.

Amicus briefs lock in the interpretive position; corporate communications preserve deniability. An amicus brief, once filed, becomes permanent record. Any inconsistency between a Rocket-Redfin amicus brief and Rocket-Redfin’s subsequent conduct — including conduct in successor jurisdictions considering transparency legislation in Illinois, California, New York, or Texas — becomes impeachment material in any future proceeding. The Rath communication can be retracted, revised, or functionally disclaimed through subsequent Redfin communications without the procedural hooks an amicus brief carries. Rocket-Redfin’s SSB 6091 position becomes fixed in the public record through the Rath communication without becoming fixed in the litigation record through an amicus brief.

Amicus briefs require a representational theory; corporate communications do not. Amicus practice requires the filer to identify the interest being represented. The identifiable interest available to Rocket-Redfin in Compass v. NWMLSis the interest in protecting the Compass partnership’s operational architecture from adverse statutory interpretation. The interest is exactly the interest the Rath communication advances while avoiding the identification requirement — the Redfin news platform communication publishes the position without requiring Rocket-Redfin to state, on the federal record, that the position serves Rocket-Redfin’s financial interest in the Compass partnership.

Amicus briefs operate inside the litigation’s evidentiary frame; corporate communications operate as extrinsic party-adjacent evidence. The structural distinction is consequential for the Self-Disclosure Trap framework. An amicus brief enters the case’s formal evidentiary frame as advocacy governed by procedural rules. The Rath communication enters the evidentiary frame as a party-adjacent admission under Federal Rules of Evidence 801 — not subject to the procedural rules governing filed briefs but subject to the substantive rules governing out-of-court statements offered for the truth of the matter asserted. Rocket-Redfin preserved the interpretive position’s distribution advantages without the procedural-rule constraints that would govern the same position filed as a brief.

The forum-selection signal compounds the Self-Disclosure Trap mechanics already documented. If the Rocket-Redfin SSB 6091 interpretation carried the analytical weight the Rath communication claims for it, the amicus route was the available venue with higher institutional authority — Judge Whitehead’s attention, NWMLS’s obligation to respond under federal procedure, and the formal evidentiary record an amicus brief produces. The route was declined. The decline documents that the interpretive position is designed for regulatory and legislative audiences (state AGs, Illinois/California/New York/Texas legislative staff, NWMLS as an institutional rule-maker) rather than for the federal court currently adjudicating the statutory question. The position operates as rule-change advocacy directed at NWMLS as an institution, not as legal argument directed at Compass v. NWMLS as a proceeding.

Table 2 — Amicus Route Declined vs Corporate Communication Route

For NWMLS trial counsel, the amicus-route-declined signal is additional deposition material for any Rocket or Redfin witness identified in discovery. The witness can be asked directly why Rocket-Redfin published its SSB 6091 statutory interpretation on a corporate news platform rather than filing an amicus brief in the active proceeding that raises the identical statutory question. No prepared answer resolves the question cleanly — affirming that the corporate-communication route was preferred concedes the procedural-avoidance framing; disclaiming the communication’s interpretive weight undermines the public position’s credibility; parsing the two venues invites the follow-up question about whether Rocket-Redfin’s interpretive position is designed to withstand federal-court scrutiny or to operate only in venues that cannot test the position procedurally.

VII. Posner and Friedman Extended to the Statutory-Compliance Layer

Zillow, eXp, and Redfin–Compass. Three Deals. Twenty Days. One Outlier. Section III ran the Posner welfare-transfer analysis and the Friedman price-discovery-mechanism analysis on the Compass-Redfin contract’s buyer data suppression — the stripping of days-on-market data, price-drop history, and valuation estimates from Redfin’s display of Compass listings. The Posner analysis identified the suppression as a wealth transfer from buyers to the brokerage dressed in consent language. The Friedman analysis identified the suppression as the mechanism through which competitive markets’ price-discovery function is disabled at platform scale.

Both frameworks extend directly to the April 16 Rath proposal. The proposal replaces structural protection with consent-based asymmetry — the architecture SSB 6091’s concurrent-marketing requirement was designed to establish gives way to the architecture the Compass-Redfin contract already operates. The Posner welfare calculation produces the same output at the expanded scope: the seller receives marginally cleaner presentation; the buyer negotiates without the three informational inputs the suppression removes; the brokerage captures the welfare transfer the informational asymmetry produces. Scaled across Redfin.com’s 60 million monthly visitors and extended across the SSB 6091 premarketing window, the welfare loss moves from individual-transaction harm to systemic market distortion at the statutory-compliance layer — the inverse of what the statute was designed to achieve.

The Friedman framework produces a specific, testable forward prediction.

Prediction. If NWMLS adopts the Rath proposal’s intra-MLS premarketing architecture, price dispersion will widen measurably between Compass-routed Washington-market transactions and open-market Washington-market transactions within matched ZIP-code cohorts.

Measurement window. June 11, 2026 (SSB 6091 effective date) through Q1 2027.

Data source. NWMLS closed transaction records segmented by Compass-listed versus non-Compass-listed properties, matched by ZIP code and property-type tier.

Falsification condition. If no statistically significant price-dispersion divergence emerges between Compass-routed and open-market transactions within matched ZIP cohorts by Q1 2027, the Friedman price-discovery-disabling mechanism the March 18 publication identified does not operate at the architectural layer the Rath proposal would create, and the statutory interpretation the Rath communication advances carries independent analytical weight rather than serving as welfare-transfer cover.

Validation condition. If statistically significant price-dispersion divergence emerges within the measurement window, the divergence documents the Rath proposal’s statutory interpretation as the architectural mechanism through which SSB 6091’s operational effect fails at the platform scale. Washington enforcement staff acquire a statute-specific enforcement predicate beyond the disclosure requirements, and successor jurisdictions drafting concurrent-marketing legislation acquire the transaction-level evidentiary record justifying statutory text that explicitly forecloses the premarketing-within-MLS exit. If the validation condition triggers, enforcement shifts from rule interpretation to measurable market distortion — a register in which the statutory question resolves empirically rather than interpretively.

The prediction converts the Posner and Friedman frameworks from harm-claim register to testable market-failure register. The prediction is auditable. The measurement is specified. The falsification condition is explicit. The architecture the Rath proposal would create is testable against its intended regulatory effect.

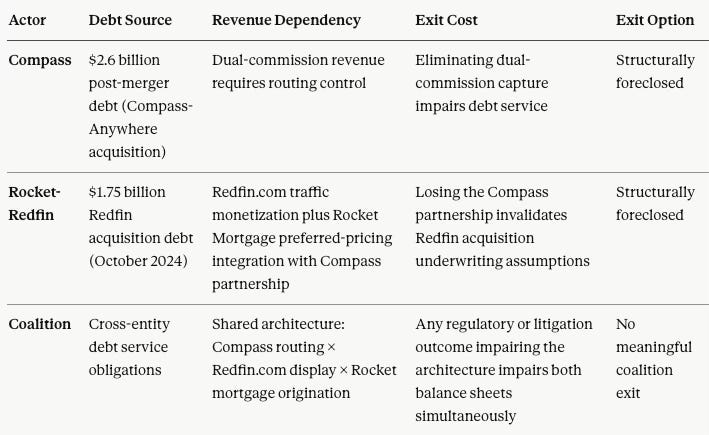

VIII. The Becker Cost-Inversion Analysis Extended to the Second Balance Sheet

Zillow, eXp, and Redfin–Compass. Three Deals. Twenty Days. One Outlier. Section IV ran the Becker Vision analysis on Compass’s $2.6 billion post-merger debt. The analysis produced the framework’s governing conclusion: debt does not influence strategy — it eliminates alternatives. Compass is the structural outlier in the twenty-day syndication stack because the cost of exit from private-control architecture exceeds the cost of continuation, and the inversion is debt-structured, not preference-structured.

The April 16 Rath communication extends the analysis to a second balance sheet. Rocket Companies acquired Redfin for $1.75 billion in October 2024. The acquisition created the platform infrastructure Compass needed for the February 26, 2026 partnership. The Rocket-Redfin balance sheet now carries its own debt-service obligations — obligations that depend on the continued operation of the same Redfin.com traffic flow, lead-generation architecture, and Rocket Mortgage preferred-pricing integration that the Compass partnership operationalizes at scale.

Three cost-inversion conditions now operate across the Rocket-Redfin-Compass coalition simultaneously.

Compass cost inversion. $2.6 billion in post-merger debt requires dual-commission revenue. Dual-commission capture requires routing control. The March 18 analysis documented the inversion in full.

Rocket cost inversion. The Redfin acquisition debt requires Redfin.com traffic monetization. The February 26 Compass partnership delivered one million buyer leads over three years with Rocket Mortgage preferred pricing embedded into Compass-client transactions. The Compass partnership is not an incremental revenue stream — the partnership operationalizes the Redfin acquisition’s underwriting assumptions at scale.

Coalition cost inversion. The Rocket-Redfin-Compass institutional alignment now depends on preserving the architecture both balance sheets require. Any regulatory or litigation outcome that impairs the architecture impairs both balance sheets simultaneously. The April 16 Rath communication is Rocket-Redfin’s rational response to the coalition cost-inversion condition — a corporate communication defending the architecture both balance sheets require, signed by a Rocket executive, published on Redfin’s institutional channel, directed at the institutional actor (NWMLS) currently litigating against Compass on the same architectural question.

The Becker framework’s governing sentence — debt does not influence strategy; it eliminates alternatives — now applies across two balance sheets. The coalition cannot exit the architecture without impairing the debt-service obligations of both Rocket and Compass. The Rath communication is not strategic advocacy; the communication is debt-service defense published as regulatory advocacy. The distinction is material for capital-markets analysts evaluating the coalition’s institutional flexibility: the coalition has no meaningful exit option from the architecture the twenty-day syndication stack identified as the regulatory ratchet’s termination point.

Table 3 — Coalition Cost-Inversion Across Two Balance Sheets

IX. The Delay-Dominant Equilibrium and the Game Selection Strategy

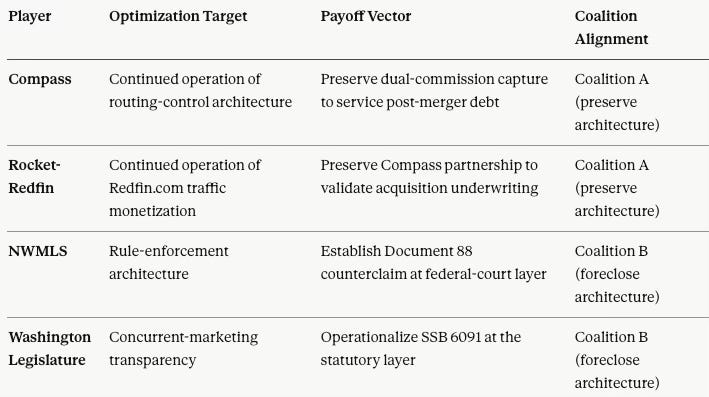

The legal and behavioral analyses in the preceding sections establish the constraint geometry and the motive force operating on the Rocket-Redfin-Compass coalition. Game theory supplies the third analytical register: why the coalition’s behavior persists and repeats across forums under the pressure the statute, the counterclaim, and the coalition balance sheets generate.

Players and payoffs. Four institutional actors operate in the game the April 16 Rath communication extends. Compass optimizes for continued operation of the routing-control architecture that services the $2.6 billion post-merger debt. Rocket-Redfin optimizes for continued operation of the Redfin.com traffic monetization architecture that services the Redfin-acquisition debt. NWMLS optimizes for the rule-enforcement architecture Document 88 establishes at the federal-court layer. The Washington legislature optimizes for the concurrent-marketing transparency architecture SSB 6091 establishes at the statutory layer. The first two actors’ payoffs converge on preserving the routing-control architecture; the second two actors’ payoffs converge on foreclosing it. The game is zero-sum at the architectural layer.

Table 4 — Game Theory Players and Payoffs

Equilibrium class — delay-dominant. The Rocket-Redfin-Compass coalition has entered a delay-dominant equilibrium in which all three coalition members benefit from postponing full transparency while preserving routing control. The payoff structure is asymmetric: every additional month of delay in SSB 6091 enforcement, NWMLS rule change, or federal-court declaratory judgment produces marginal commission revenue (Compass), marginal lead-routing revenue (Redfin), and marginal mortgage-origination revenue (Rocket) that compounds across the coalition balance sheets. The delay payoff is higher than the resolution payoff for every coalition member under current cost structures. The coalition’s rational move under the delay-dominant equilibrium is not resolution-seeking; the coalition’s rational move is forum-shifting — deploying arguments in venues where the rules most favor delay and where the procedural constraints most disfavor rapid resolution.

Game selection strategy — the amicus-route decline as forum choice. The Rath communication’s choice of Redfin news platform over amicus brief is not merely a move within the Compass v. NWMLS proceeding; it is a choice of which game to play. An amicus filing would operate inside a game with judge-enforced procedural rules, evidentiary constraints, opposition-counsel scrutiny, and court-scheduled resolution windows. The Redfin news platform operates inside a different game entirely — distribution rules favor the publisher, procedural rules do not apply, opposition response is extrinsic rather than built into the proceeding, and the resolution window is whatever the publisher chooses to make it. The coalition selected the weaker-ruled game because the weaker-ruled game permits continued delay-dominant equilibrium operation that the stronger-ruled game would not. Game selection strategy is the structural signature of actors operating under a delay-dominant equilibrium when resolution-forcing games are available.

Iterated-game dynamics — the three-iteration self-correction defense. Kelman pledge → national MLS proposal → six-MLS national-cascade frame. Three rounds of the same iterated game, each round with the same operative conclusion (defer state legislation) delivered through a different surface form. The iterative pattern is the strategic signature of a coalition operating under a delay-dominant equilibrium that has lost the primary exhibit in prior rounds — Kelman pledge reversed, national MLS proposal uncredentialed — and deployed successor arguments to maintain the equilibrium rather than accepting resolution. The diminishing returns documented in Section III are the game-theoretic expression of the iterated-game dynamic: each round’s argumentative move carries less analytical force than the prior round because the legislative, judicial, and market-observer populations have already seen the pattern.

Equilibrium-exit conditions. The delay-dominant equilibrium holds under three conditions: coalition balance sheets remain solvent; coalition coordination remains observable only as parallel-but-separate institutional behavior; and the regulatory ratchet’s compounding rate remains slower than the coalition’s forum-shifting rate. The April 16 same-day publication pattern documented in the present analysis and the April 17 Two-Gate Capture Model primary-source evidence documented in Two NWMLS Records, One Foster-Skillman Team — Primary-Source Evidence of the Compass Two-Gate Capture Model Inside the Washington Statutory Transition Window together meet the Stigler information-sufficiency threshold The Dual Nash-Stigler Equilibrium Architecture established: coordination is no longer inferential; coordination is documented. The second equilibrium-holding condition weakens with each incremental specimen. The third condition weakens with each state enactment. The first condition weakens with each reporting period that compresses the coalition’s operational runway.

The delay-dominant equilibrium terminates when one of the three holding conditions fails. The coalition’s rational response to deteriorating holding conditions is to accelerate forum-shifting and delay-dominant moves rather than to exit the equilibrium — exit is structurally foreclosed by the Becker cost-inversion operating across two balance sheets documented in Section VIII. The rational move under a delay-dominant equilibrium in which exit is foreclosed is to maximize remaining delay payoff before the equilibrium terminates, which is exactly what the April 16 same-day publication pattern documents.

X. Forum Count Progression and Deposition-Layer Consequence

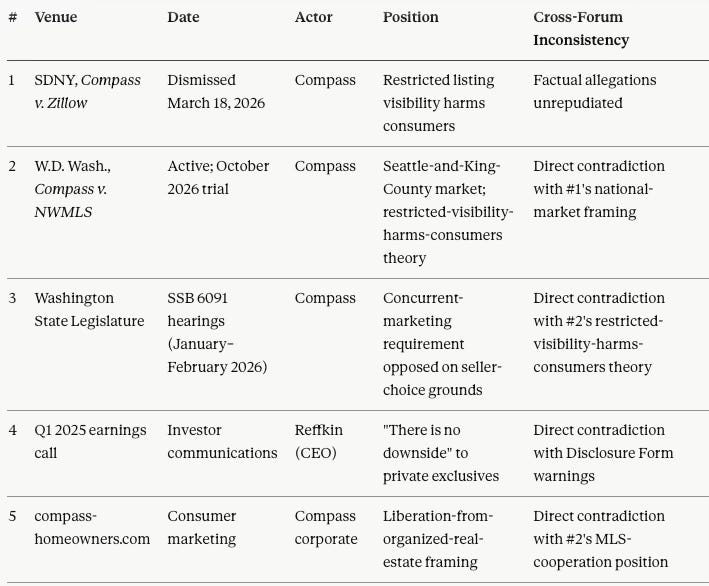

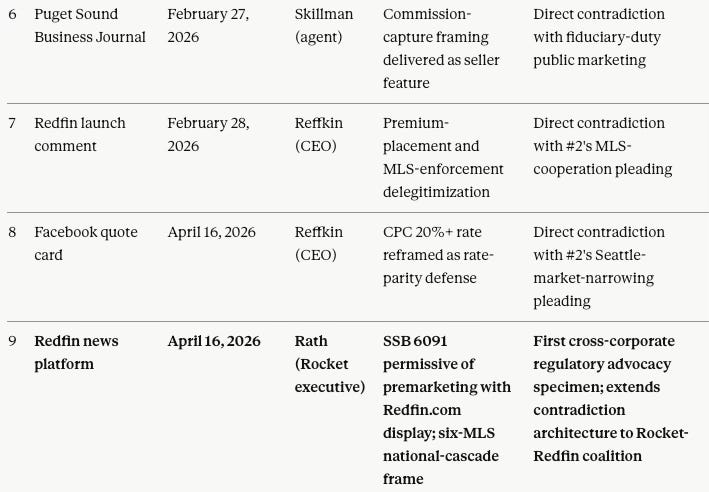

Compass’s Cross-Forum Contradictions documented six forums; the April 16 Reffkin specimen populated a seventh and an eighth. The Rath April 16 communication populates a ninth. The forum’s distinction from the earlier eight is its institutional-partnership corporate-communications character — the first documented cross-corporate regulatory advocacy specimen in the cross-forum sequence.

Table 5 — Cross-Forum Count Progression (Nine Forums)

The ninth forum extends the cross-contradiction architecture beyond Compass to the Rocket-Redfin coalition. Compass arguments are now subject to impeachment using Rocket-Redfin public positions on the same regulatory questions, and Rocket-Redfin positions are subject to impeachment using Compass litigation postures. The Stigler information-sufficiency threshold The Dual Nash-Stigler Equilibrium Architecture established as the crossing point for the Nash-stable compartmentalized strategy moves closer with each incremental cross-actor specimen.

Deposition-layer consequences. The April 16 Compass-Reffkin Consumer Policy Center Quote-Card Specimen Section IX constructed a deposition sequence for the Reffkin NWMLS notice built on the national-market estoppel predicate the CPC report’s five-city frame activated. The Rath April 16 communication strengthens the deposition architecture across three dimensions. The six-MLS national-cascade frame supplies NWMLS trial counsel an additional estoppel predicate at the institutional-partnership layer. The SSB 6091 statutory interpretation is available as impeachment material against any Compass witness who testifies that the Compass statutory reading is not the Rocket-Redfin reading. The “productive conversations with leaders at NWMLS” characterization is available to NWMLS trial counsel as a discovery target — Rocket or Redfin witnesses identified in discovery can be required to specify which NWMLS leaders they conversed with, when, and with what content.

XI. Institutional Reader Implications

For NWMLS trial counsel: the Rath April 16 communication is new cross-forum impeachment material; a strengthened national-cascade estoppel predicate; a documented Rocket-Redfin statutory interpretation directly adverse to the Document 88 declaratory judgment count; and a discovery target through the “productive conversations” characterization.

For state attorneys general and multi-state legislative staff: the Rath communication is the third documented iteration of the Compass self-correction defense, arriving with the Kelman pledge collapse and the national MLS proposal already on record. Legislative staff in Illinois, California, New York, and Texas drafting successor statutes can draft text specifically foreclosing the six-MLS national-cascade frame, the public-platform-display-satisfies-concurrent-marketing interpretation, and the premarketing-within-MLS rule-change ask. The pattern’s third iteration arrives with diminishing returns — the rhetorical architecture is approaching exhaustion, and legislative staff inheriting the full record have the analytical tools to recognize the pattern on presentation.

For plaintiffs’ counsel in consolidated real estate antitrust litigation: the April 16 same-day publication pattern — Reffkin Facebook quote card at the CEO-social-media layer, Rath Redfin communication at the institutional-partnership corporate-communications layer — is the first documented cross-corporate coordinated narrative deployment in the Compass-Rocket-Redfin alignment. The pattern is evidentially stronger than any single-corporate specimen because the inference of coordination moves from probable to documented when two institutional actors publish structurally aligned positions on the same regulatory question on the same day directed at the same institutional target.

For capital markets analysts and institutional MindCast AI subscribers: the Becker cost-inversion analysis now operates across two balance sheets. The Rocket-Redfin-Compass coalition has no meaningful exit option from the architecture the twenty-day syndication stack identified as the regulatory ratchet’s termination point. The Layer 3 acquisition premium The Compass Commission Consolidation Strategy and Real Estate Marketing Transparencyidentified as a regulatory short position now carries a second balance-sheet dimension — Rocket’s acquisition debt from the Redfin transaction depends on the same architecture. Goodwill-impairment analysis at the Anywhere brand level has a second-balance-sheet input, and the Debt-Narrative Correlation The Cybernetics of Compass Holdings’ Narrative Control Architecture identifies extends across the coalition.

XII. Part III Specimen Count After April 16

The April 16 Compass-Reffkin Consumer Policy Center Quote-Card Specimen Section X specified that Part III publication requires five to seven additional specimens across two or more behavioral categories beyond Specimen 1. The Rath April 16 communication adds Specimen 2 at the institutional-partnership corporate-communications layer. The specimen count stands at 2, with category count at 2.

The Rath communication activates a monitoring category the Specimen 1 framework specified: institutional-partnership corporate-communications. Candidate subsequent specimens include Rocket-Redfin executive communications to Illinois, California, New York, and Texas state regulators; Rocket or Redfin executive testimony in subsequent state legislative proceedings; Rocket investor communications referencing the Compass partnership’s MLS-rule-change strategy; and additional public positioning by Rocket-Redfin executives on Compass-related litigation outcomes.

The Rath communication also activates monitoring of NWMLS’s institutional response to the “productive conversations with leaders at NWMLS” characterization. NWMLS statements, filings, or public communications addressing the characterization — or declining to address it — are analytically significant for the Specimen 2 record.

Three to five additional specimens across the existing two categories, or two to three additional specimens introducing a third category, reach sufficient volume for Part III publication. Candidate third categories include subsequent Compass deposition transcripts entering the public record, Q1 and Q2 2026 earnings-call treatment of the CPC report and NWMLS counterclaim, and goodwill-impairment disclosure movement at Anywhere brand level.

XIII. Conclusion

Joe Rath’s April 16, 2026 communication on Redfin’s news platform is Self-Disclosure Trap Specimen 2 and the third documented iteration of the Compass self-correction defense. The three-iteration record runs Kelman pledge → national MLS proposal → six-MLS national-cascade frame. Each iteration carries the same operative conclusion — defer state legislation — through a different surface form. Iteration 3 is signed by a Rocket executive rather than a Compass executive, extending the rhetorical architecture across the coalition for the first time and converting the self-correction defense from a legislative-forum deployment into a cross-forum deployment available as federal-court impeachment material.

The Posner and Friedman frameworks extend directly from the Compass-Redfin contract architecture to the Rath proposal’s statutory-compliance architecture, producing a falsifiable forward prediction testable against Washington-market closed transaction data by Q1 2027. The Becker cost-inversion analysis now operates across two balance sheets — the Rocket-Redfin-Compass coalition’s institutional alignment is solvency-convergent, not narrative-convergent, and the coalition has no meaningful exit option from the architecture the regulatory ratchet is closing.

The April 16 same-day publication pattern is the structural signature the Compass corpus predicted: coordinated institutional messaging visible across two corporate channels on the same day, directed at the same regulatory target, advancing the same underlying position. The Debt-Narrative Correlation operates across two balance sheets. The Self-Disclosure Trap operates across two corporate entities. The self-correction defense operates in its third iteration.

The MindCast AI corpus documents the architecture across two complementary registers on April 17, 2026. Two NWMLS Records, One Foster-Skillman Team — Primary-Source Evidence of the Compass Two-Gate Capture Model Inside the Washington Statutory Transition Window documents the market-conduct layer — what Compass does in the market under a single Foster-Skillman team credential operating both gates of the routing-control architecture on two simultaneous Washington-market properties. The present analysis documents the institutional-partnership corporate-communications layer — what Rocket-Redfin says about what Compass does, asks NWMLS to authorize, and publishes outside the federal-court procedural constraints the market-conduct evidence will confront at summary judgment. Both registers feed Document 88’s counterclaim architecture. Both are publicly verifiable as of April 17, 2026.

The mechanism persists; only the narrative surface changes.

Source Publications

MindCast AI publications cited in the present analysis:

Two NWMLS Records, One Foster-Skillman Team — Primary-Source Evidence of the Compass Two-Gate Capture Model Inside the Washington Statutory Transition Window (April 17, 2026). Primary-source documentation of the Two-Gate Capture Model operating under a single Foster-Skillman Compass team credential on two simultaneous Washington-market NWMLS records (MLS #2497151 and MLS #2468181); market-conduct-layer companion to the present institutional-partnership corporate-communications-layer analysis.

Zillow, eXp, and Redfin–Compass. Three Deals. Twenty Days. One Outlier. (March 18, 2026). Twenty-day syndication stack analysis, Posner welfare-transfer and Friedman price-discovery frameworks applied to Compass-Redfin buyer data suppression, Becker switching-cost asymmetry analysis, self-correction defense pattern documentation across Kelman pledge and national MLS proposal iterations, CDT Foresight Simulation three-Vision integrated analysis.

The Compass-Reffkin Consumer Policy Center Quote-Card Specimen — A Self-Disclosure Trap Market Analysis (April 16, 2026). Self-Disclosure Trap Specimen 1 preservation, delegation upshift theorization, deposition-sequence construction for the Reffkin NWMLS notice, and Part III specimen-count framework.

Compass Double-Sided Commissions — Consumer Policy Center Measures the Output, MindCast Models the System(April 15, 2026). Benchmark-and-extension analysis of the Consumer Policy Center report, four-prediction forward architecture, and Olympia Validated retroactive-meaning analysis.

The Compass Narrative Inversion Playbook (February 4, 2026). Three-tier cross-forum contradiction pattern documentation, Skillman Moment specimen preservation, and impeachment-script preparation for the SSB 6091 legislative window.

Compass’s Cross-Forum Contradictions (February 28, 2026). Six-forum cross-contradiction architecture and enforcement charge-code map construction.

The Counterclaim That Closed Compass’s Antitrust Thesis (April 3, 2026). Document 88 counterclaim architecture analysis, Triptych listing specimen preservation, and Paragraph 43 continued-operation intent framework.

The Antitrust Litigation Trap Compass Built for Itself (April 6, 2026). Visual synthesis across the NWMLS counterclaim architecture, the Three-Layer Acquisition Hierarchy, and the MindCast Simulation probability bands.

The Compass Commission Consolidation Strategy and Real Estate Marketing Transparency (February 19, 2026). Primary MindCast evidentiary publication documenting thirteen months of Seattle ultra-luxury NWMLS transaction data, Category A through D commission-flow architecture, Three-Layer Acquisition Hierarchy, and Layer 3 regulatory short position analysis.

The Cybernetics of Compass Holdings’ Narrative Control Architecture. Framework publication formalizing the Self-Disclosure Trap pattern and the Debt-Narrative Correlation the present analysis references.

The Dual Nash-Stigler Equilibrium Architecture (January 2026). Framework publication establishing the Nash stability and Stigler information-sufficiency threshold analysis the Self-Disclosure Trap corpus extends.

External Sources

Joe Rath, Redfin Calls on NWMLS to Give Home Sellers More Choice (Redfin, April 16, 2026).

Robert Reffkin, Facebook post, April 16, 2026 (on file).

Stephen Brobeck, Compass Expansion: New Data on Market Share and Double Ending (Consumer Policy Center, April 2026).

Rocket Companies, Compass and Rocket Form Historic Alliance to Dramatically Increase Home Listing Inventory on Redfin (Rocket Companies Press Release, February 23, 2026).

Zillow, Zillow launches Zillow Preview to bring pre-market home listings into the open (Zillow Press Release, March 17, 2026).

Taylor Anderson, eXp Announces Pre-Marketing Syndication Deal with 3 Portals (Inman, March 18, 2026).

Northwest Multiple Listing Service Answer, Affirmative Defenses, and Counterclaim — Document 88, Case No. 2:25-cv-00766-JNW (W.D. Wash., April 2, 2026).

Substitute Senate Bill 6091, Washington State Legislature (2026 Regular Session), signed into law with June 11, 2026 effective date.