MCAI Lex Vision: The Compass–Zillow Antitrust Litigation Arc Is Closed. Here Is What the Record Shows.

How Compass Spent Two Years and Millions in Legal Fees Generating the Evidentiary Record Used Against It — and What Reffkin's LinkedIn Post Is Hiding This Morning

Companion publications: Compass's Coasean Coordination Problem Part IV — Platform Routing, Portal Power, and the Zillow Litigation | The Compass Antitrust Self-Destruction Sequence | The Compass Narrative Inversion Playbook | Compass’s Cross-Forum Contradictions | Compass Rhetorically Reframing Seller Choice to Launch Jurisdictional Attack on MLSs | Compass’s Consumer Choice Framing as a Control Mechanism

Robert Reffkin posted a LinkedIn announcement this morning framing Compass’s voluntary dismissal of its Zillow lawsuit as a consumer-choice victory. “Our goal has always been to give homeowners more choice to decide when, where, and how to market their homes,” he wrote. “We are pleased to see that both other brokerages and portals are now recognizing the strong consumer demand for more options in how they sell their homes.”

Reffkin’s post reframes a legal defeat as a consumer-choice victory. The federal record shows the opposite: Compass lost on every theory it advanced and exited once no path to relief remained after denial of preliminary injunction in Compass, Inc. v. Zillow Group, Inc., No. 25-CV-05201 (JAV), slip op. at 50 (S.D.N.Y. Feb. 6, 2026) (Vargas, J.).

The MindCast Signal Suppression Equilibrium — formally introduced in Prestige Markets as Signal Economies — A Model of Signal Suppression and Institutional Failure — explains the mechanics: when Access Dependence × Reputational Retaliation Risk × Information Fragmentation × Narrative Distortion exceeds Signal Aggregation Capacity (A×R×F×N > S), rational actors suppress the true signal even when they privately observe it.

Reffkin's post meets the condition: broker access dependence on Compass's network, reputational risk of contradicting the CEO's framing, the opinion's 50-page length fragmenting its distribution, and the consumer-choice narrative distorting how the loss is interpreted — together overwhelming a signal that requires reading a federal ruling to access.

MindCast published the analytical framework for this outcome before the Zillow complaint was filed. The Brief of MindCast AI LLC as Amicus Curiae in Support of Defendant Zillow identified the central structural problem: Compass sought to compel a high-integrity coordination actor to transmit inventory that deliberately bypassed coordination requirements. The remedy Compass sought was the harm the law is designed to prevent. Compass’s Coasean Coordination Problem Part IV — Platform Routing, Portal Power, and the Zillow Litigation formalized this as the forced-transmission paradox — Compass’s Causal Signal Integrity score of 0.23 against Zillow’s 0.77, a 3.3:1 asymmetry quantifying why compelling Zillow to distribute coordination-degrading inventory would hollow out the focal point without formally destroying it. Judge Vargas’s February 6, 2026 opinion reached the same conclusion in judicial language.

Here is what the record now shows.

I. What Compass Asked For and What the Court Found

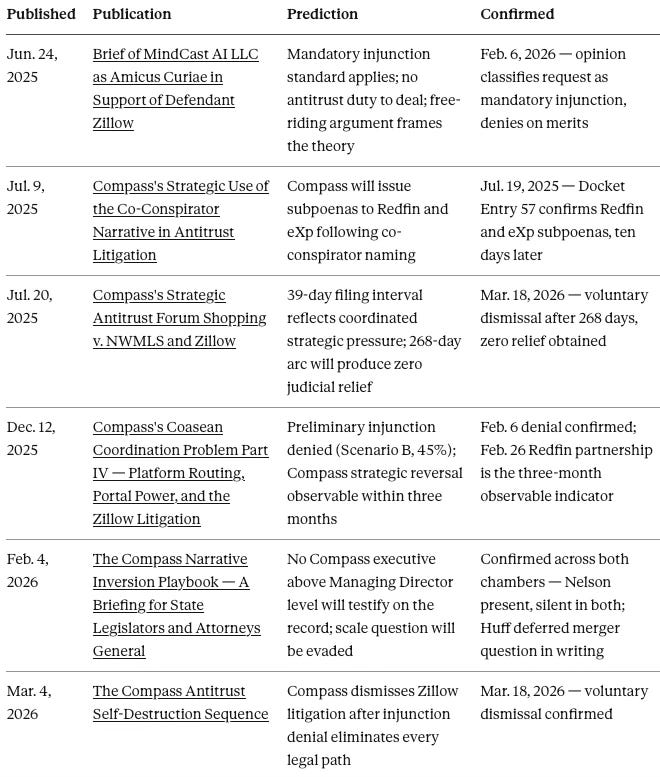

Compass filed its complaint against Zillow on June 23, 2025 — thirty-nine days after filing against NWMLS in the Western District of Washington. The timing was not coincidental. Compass’s Strategic Antitrust Forum Shopping v. NWMLS and Zillow — Compass Litigates, Fragments, Reframes for Market Share, published July 20, 2025, identified the 39-day interval as evidence of coordinated strategic pressure rather than independent grievance, and characterized the venue fragmentation — a Seattle-based company sued in New York — as a deliberate mechanism to prevent any single court from evaluating the cumulative pattern. The prediction is confirmed by the dismissal arc: 268 days from filing to voluntary withdrawal, zero judicial relief obtained at any stage.

The complaint sought a preliminary injunction prohibiting Zillow from enforcing its Listing Access Standards against listings marketed off-MLS before syndication. Judge Vargas denied the motion on February 6. She did not reach irreparable harm. Compass’s entire public narrative — harm to sellers, harm to agents, harm to competition — was never evaluated because the legal theory collapsed first.

The failure was total across all three theories. On Section 1, the conspiracy claim, the court found that “Compass has not presented any direct evidence of an anticompetitive agreement between Zillow and Redfin” and that “contemporaneous communications… indicate that Zillow and Redfin independently developed and announced their policies.” (Compass v. Zillow, Op. p. 29) Compass’s Strategic Use of the Co-Conspirator Narrative in Antitrust Litigation, published July 9, 2025, had predicted that Compass would issue subpoenas to Redfin and eXp as the next tactical move after naming them as conspirators — confirmed ten days later through Docket Entry 57. The subpoenas produced nothing that survived the evidentiary hearing. The court found “Zillow’s conduct is most plausibly explained as its own independent response… [and] Redfin’s conduct is most plausibly explained as an independent response.” (Op. p. 33) Both CEOs’ denials were credited after direct observation. Supporting Zillow Against Compass’s Forum Fragmentation and Co-Conspirator Strategies — MindCast AI Foresight, Predicting and Catching Compass in the Act had identified this outcome as structurally overdetermined once the conspiracy theory was stress-tested against actual communications: “The side that deploys coordination vocabulary controls the expert narrative.”

On Section 2, the court found that “even assuming arguendo that the Court could rely on these figures, Zillow’s market share… would still only lie somewhere between 50 and 66%” — a band that “can occasionally show monopoly power” but required supporting evidence of actual control that Compass could not produce. (Op. pp. 46–47) “Compass has not provided sufficient evidence from which it can be inferred that Zillow has monopoly power.” (Op. p. 50) Multi-homing destroyed the network effects argument: “Consumers use multiple online home search platforms simultaneously at little or no cost.” (Op. p. 49) “Recent entry of competitors… suggests not only that Zillow is unable to exclude competition… but also that barriers to entry have not precluded meaningful new entrants.” (Op. pp. 49–50) Homes.com had grown from 2.4 to 19 percent audience share in four years. Zillow’s own share declined from 62 to 50 percent between May 2024 and June 2025. Compass’s Coasean Coordination Problem — Platform Routing, Portal Power, and the Zillow Litigation had placed the preliminary injunction denial at Scenario B with 45 percent probability, with the observable indicator that Compass would reduce Private Exclusive marketing emphasis within three months of denial. The Redfin partnership announced February 26 — twenty days after the denial — is that indicator firing on schedule: routing control migrated from inventory suppression to platform-level buyer capture, exactly the strategic reversal Scenario B predicted.

On exclusion, the court was precise: “Home sellers can still choose to list properties for sale through premarketing strategies like 3PM… albeit at the cost of foregoing exposure for those listings on Zillow.” (Op. pp. 39–40) That is a voluntary tradeoff, not exclusion. “There is no evidence that any brokerage stopped offering such strategies to consumers after Zillow announced its LAS.” (Op. p. 39) The numbers that make the harm narrative untenable: “only .011% [of listings] were removed: roughly 1 in 10,000” and “the 48 removed listings accounted for just 0.06%… of new listings.” (Op. p. 41) Compass described this enforcement as existential. The court’s arithmetic made that description numerically false on the face of the opinion.

Contact mcai@mindcast-ai.com to partner with us on Law and Behavioral Economics foresight simulations. To create your own game theory simulation of data on Compass address suppression and private exclusives, upload the URL of this publication to any LLM (ChatGPT, Claude, Gemini, Grok, Perplexity) and prompt ‘develop MindCast framework with 3 degrees of cited sub links.’ Thereafter, all new information you upload is training data for your AI system. See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure and MindCast Predictive Cybernetics Suite for more info.

MindCast AI’s analytical work on SSB 6091 — transaction methodology, opposition modeling, testimony framework, and game theory prediction record — is available for deployment in any state considering real estate transparency legislation. Washington’s record does not need to be rebuilt. It needs to be applied.

Recent projects: The Compass Commission Consolidation Strategy, The Compass–Anywhere Address Suppression Calculus, Death by a Thousand Depositions: The 42-Day Compass Collapse Framework, The Compass Collapse– A Post Washington SSB 6091 Passage Reckoning (3 part series)

II. The Mandatory Injunction Classification

The most analytically significant holding received almost no public attention: the court’s classification of Compass’s request as a mandatory injunction rather than a prohibitory one. A prohibitory injunction preserves the status quo. A mandatory injunction alters it, triggering the heightened “clear or substantial likelihood” standard. The court classified Compass’s request as mandatory because “directing Zillow to enjoin the implementation of the LAS on its platforms to accommodate Compass’s 3PM and other premarketing or private listing strategies would alter Zillow’s and Compass’s positions vis-à-vis the other.” (Op. p. 22) Zillow would have been required to distribute listings on Compass’s terms, restructuring a commercial relationship that never existed in that form.

The classification names precisely what Compass was doing. Compass was not defending a right it possessed. It was demanding a structural accommodation it had never had. The antitrust framing — Zillow as monopolist, Compass as excluded competitor — obscured that the relief sought was not restoration but compulsion. The Brief of MindCast AI LLC as Amicus Curiae in Support of Defendant Zillow had argued this directly a year before the hearing: “The requested injunction is the coordination harm.” The court reached the same conclusion through mandatory injunction doctrine. “Because the Court concludes that Compass has not shown a likelihood of success on the merits… it need not reach the question of irreparable harm.” (Op. p. 22) Compass’s entire public harm narrative was rendered procedurally irrelevant before it was weighed on substance.

III. What Reffkin’s Testimony Established on the Record

The preliminary injunction was not resolved on briefs alone. From November 18 to 21, 2025, Judge Vargas held an evidentiary hearing at which Reffkin testified under oath. Reffkin’s testimony from those four days is now permanent federal record.

Reffkin testified that 94 percent of listings using Compass’s 3-Phase Marketing Strategy proceed to the third phase — MLS submission and Zillow syndication. The number is not Zillow’s characterization. It is the CEO’s sworn description of his own model. The temporal arbitrage architecture Compass built terminates in Zillow distribution by the CEO’s own account in 94 of every 100 cases. Compass’s Coasean Coordination Problem identified this as the core admission that collapses the narrative: “Compass wanted distribution without Zillow’s informational framing.” The 94 percent figure confirms the model required Zillow at the back end. Reffkin established that under cross-examination.

Reffkin also described the Black Box structure on Compass.com — the front-page interface advertising Private Exclusives without specific listing details, requiring buyer contact with a Compass agent to access property information — and testified that Compass structured it specifically to avoid running afoul of NAR and MLS rules. The court found the Black Box violated Zillow’s LAS. Compass built a mechanism to circumvent MLS transparency requirements, testified to that design on the record, and then argued the resulting enforcement was anticompetitive.

The Coming Soon phase description completes the picture. The complaint described Phase 2 as publicly launching listings on Compass.com “without displaying days on market, price drop history, or other negative insights.” That language — Compass’s own characterization in a sworn federal pleading — established that data suppression was the feature, not a side effect. The Compass Antitrust Self-Destruction Sequence documented this as one of three definitional layers Compass’s own counsel drafted that SSB 6091 subsequently codified: “Compass acknowledged, in a sworn federal pleading, that Coming Soon is a public launch visible to all agents and consumers on the internet. SSB 6091’s concurrent marketing trigger activates when any marketing occurs. The admission is in the complaint.”

IV. The Narrative Inversion the Record Now Forecloses — And What Happened in Olympia

Between the filing of the Zillow complaint in June 2025 and the dismissal this morning, Compass maintained two structurally incompatible positions across two institutional forums. The Compass Narrative Inversion Playbook — A Briefing for State Legislators and Attorneys General, published February 4, 2026, documented the mechanism: “Compass argues in federal court that restricted listing visibility harms consumers and forecloses competition. In state legislatures, Compass argues the opposite — that restricted visibility is benign seller choice. Both positions cannot be true.”

The dual-position conflict. The Washington State Senate hearing on SSB 6091 on January 23, 2026 placed both positions on the public record simultaneously. Huff’s prepared testimony targeted Zillow directly: “It is not the homeowner. It is the dominant third-party platform providers whose business models rely on the harvesting of data of every available listing. The state should not be legislating to protect the data-scraping interests of tech platforms at the expense of homeowners’ rights.” (Transcript 43:12) Compass was simultaneously litigating in the SDNY, arguing in a sworn federal complaint that Zillow’s platform restrictions constituted anticompetitive exclusion and demanding the federal judiciary force Zillow to distribute Compass listings. In Olympia, the same platform was a data-scraping villain. The Narrative Inversion Playbook documented this as Argument 4: “In federal court, Compass demands platform access and calls platform restrictions anticompetitive. In Olympia, Compass frames platform access as a problem. These positions cannot coexist.”

The hearing dynamics. Compass’s designated witness was Brandi Huff, Managing Director for Washington — not Cris Nelson, Compass’s Regional Vice President, who was present in the hearing room for both the Senate and House proceedings and declined to testify in either chamber. The Narrative Inversion Playbook documented Nelson’s posture as the executive buffer strategy: “Present at both hearings but declined to testify in either chamber, maintaining executive buffer from the legislative record.” Her silence was not incidental. Compass sent its Managing Director to absorb cross-examination that its Regional VP was present to observe but protected from answering. The Compass Astroturf Coefficient at the Washington State Senate — How Coordinated Non-Disclosure Distorted the Legislative Record at Washington’s SB 6091 Hearing documented that 162 Compass-affiliated individuals registered opposition at the same hearing — with only 9 disclosing their affiliation. The Astroturf Coefficient reached 17:1. Huff’s disclosed testimony was the visible tip of a coordinated apparatus whose depth the sign-in record was designed to obscure. The inversion held through prepared remarks. It collapsed when Senator Alvarado asked a single follow-up on the Anywhere merger: what does layering an exclusive network on the largest Wall Street-backed brokerage mean for competition? Huff’s answer: “That is probably above what I feel comfortable speaking to because my job currently is to support the brokers in our community. As far as the merger and acquisition and higher level business model, that’s probably above. But I’m happy to put those things in writing too at a later date.” (Transcript 45:37) No written submission appeared before the House voted 92–1. Senator Bateman followed with the fair housing enforcement question. Huff acknowledged: “I’ll acknowledge that that is still sometimes a problem.” (Transcript 48:07) The Narrative Inversion Playbook’s Prediction 1 had forecast exactly this: “No Compass executive above Managing Director level will testify on the record.” Confirmed twice across two chambers, with Nelson present and silent in both.

The structural implication. Compass approved the anti-Zillow framing, the homeowner autonomy argument, and the Wisconsin opt-out reference. Compass could not simultaneously support its own designated witness answering the merger’s competitive consequences — because any honest answer would have validated SSB 6091. The forward lock holds after today: the Zillow complaint has been dismissed, but the sworn pleadings remain in PACER. Every state that advances a concurrent marketing bill after March 18, 2026 inherits both the SDNY opinion and the complaint that preceded it — Compass’s own counsel’s sworn description of why visibility restrictions harm consumers, now permanently available as primary source material for any legislative record that follows.

V. Validated Predictions: The MindCast Analytical Record

The following predictions were published before the events they describe. Each is drawn from a timestamped MindCast publication and confirmed against the public record as of March 18, 2026.

Four predictions remain active and falsifiable: NWMLS Notice of Supplemental Authority citing the eXp deal (deadline April 4, 2026); California no-opt-out concurrent marketing bill citing the Redfin contract (Q3 2026); CFPB RESPA preliminary inquiry into the Rocket–Compass–Redfin structure (Q3 2026); Anywhere acquisition goodwill impairment as a timing question at the next audit cycle. Each will either confirm or falsify the framework publicly and on the record.

VI. The Root Cause of Why Compass Dropped the Case

After the injunction denial, the case was effectively over. “Because Plaintiff has not shown a likelihood of success on the merits, Plaintiff’s motion for a preliminary injunction is DENIED.” (Op. p. 50) After February 6, Compass no longer had a viable path to relief. The court rejected every theory required to sustain the case — no conspiracy, no monopoly power, no exclusion. The only remaining characterization of Zillow’s conduct was a voluntary tradeoff: “Home sellers can still choose to list properties for sale through premarketing strategies like 3PM… albeit at the cost of foregoing exposure for those listings on Zillow.” (Op. pp. 39–40) That framing eliminates antitrust liability as a matter of law. Without a surviving claim, no injunctive leverage, and an evidentiary record that had already produced party admissions — the 94 percent figure, the Black Box design rationale, the Coming Soon data suppression concession — available to defendants in future proceedings, continued litigation would only deepen the structural disadvantage the case had already exposed. Reffkin’s sworn testimony is now a permanent exhibit. The rational move was to exit before discovery compelled more of the same.

VII. What the Dismissal Actually Means

Reffkin’s post frames the dismissal as a consumer-choice victory because Zillow reversed the specific policy Compass called anticompetitive. Reffkin’s framing requires ignoring what the litigation cost and what the reversal actually produced.

The Compass Antitrust Self-Destruction Sequence documented the cost precisely: Compass spent an estimated two to four million dollars in legal fees generating the primary evidentiary record used against it — in the legislative proceedings that produced SSB 6091’s 141–1 bicameral vote, and in the federal judicial record that now characterizes its injury as a voluntary tradeoff. “Washington’s drafters did not need to invent a regulatory framework. Compass filed one in federal court, and the Legislature applied it.” The Compass Commission Consolidation Strategy — Private Exclusives, Address Suppression, and the Architecture of Dual-Commission Capture established the underlying market failure that SSB 6091 addressed: across 130 Seattle ultra-luxury transactions totaling $1.08 billion, 16 produced commission flows that stayed entirely inside the combined Compass-Anywhere entity. The Compass–Anywhere Address Suppression Calculus modeled the revenue and detection consequences and found the two objectives structurally incompatible at scale — a finding the Redfin partnership’s architecture now confirms, having migrated the suppression mechanism from listing-level to buyer-routing-level rather than abandoning it.

What Zillow’s reversal actually produced: Zillow modified its LAS to allow premarket listings if broadly accessible — not selectively accessible. Compass gained timing flexibility. Compass lost structural control over the buyer interaction layer. Zillow vs. Redfin–Compass, Premarket Control Under Expanding Transparency Laws — How Compass Turned Its Own Lawsuits Into the Legislation That Destroyed Its Business Model — and What Zillow Built While Compass Was Losing in Court, published this morning, put it directly: “Compass gained timing flexibility but lost structural control.” Reffkin’s “choice vs. control” framing describes gaining the former while the record documents losing the latter.

Zillow, eXp, and Redfin–Compass. Three Deals. Twenty Days. One Outlier. — How the Pre-Market Syndication Stack Exposed Compass–Redfin as the Only Architecture Built to Route Buyers — Not Reach Them, also published this morning, places the dismissal in the twenty-day industry context that isolates Compass as the structural outlier. Zillow launched Zillow Preview on March 17 with Keller Williams, REMAX, HomeServices of America, and Side — open distribution, full buyer data, no internal routing requirement. eXp announced three-portal syndication on March 18 on explicitly non-exclusive terms, with the Realtor.com CEO stating publicly: “equal access for all buyers, not a subset selected by the listing agent.” Compass dismissed its Zillow lawsuit on the same day and announced it through a consumer-choice LinkedIn post. The voluntary industry consensus toward open distribution makes Compass’s architecture the outlier not by regulation alone but by the market’s own judgment — exactly what the Becker Vision CDT Foresight Simulation predicted: “The market can move where Compass cannot.”

The NWMLS October 2026 trial proceeds in the Western District of Washington, where the jury pool will be drawn from the same state whose legislature voted 141–1 to mandate exactly what Compass sued NWMLS for enforcing. Reffkin’s sworn testimony on the 94 percent figure, the Black Box design, and the Coming Soon data suppression architecture is now available to NWMLS trial counsel as party admissions under FRE 801(d)(2). The cross-forum record — SDNY docket, Washington legislative transcript, LinkedIn post — constitutes a unified evidentiary record no forum compartmentalization strategy can now separate.

Reffkin posted about homeowner choice. Nelson was in the room in Olympia and said nothing. The depositions have not yet begun.