MCAI Innovation Vision: The Intelligence Gap— Apple's AI Strategy and the Commoditization Bet

MindCast Consumer AI Device Series: Installment I Apple's AI Strategy Has One Way to Win and Two Ways to Lose

MindCast Consumer AI Device series publications: Installment I — The Intelligence Gap: Apple’s AI Strategy and the Commoditization Bet | Installment II — The Apple AI Challenger Framework: Google, Samsung, and the Intelligence Layer | Installment III — The Consumer AI Device Intelligence Layer: Value Capture Under Interface Drift | Installment IV How Cybernetic Feedback Latency, Loop Architecture, and Ashby’s Viability Condition Resolve Consumer AI Device Competition

Prior MindCast AI Apple coverage: NVIDIA’s SLM Thesis and Apple’s Cognitive AI Future | Apple’s AI Wake-Up Call | A Clearer Kind of Intelligence, Built for the Real World.

Apple is not the conclusion of this analysis. Apple is the calibration point. The same governing variable — commoditization versus concentration — will be applied across competing institutions to test which behavioral grammar resolves most favorably under identical structural conditions. Installment I establishes the baseline. Installments II and III test the system.

Executive Summary

On March 18, the Wall Street Journal reported that Apple is on pace to surpass $1 billion in AI revenue this year — almost entirely from App Store commissions on ChatGPT subscriptions. The headline: Apple is way behind in AI and still making a fortune from it. The story the Journal didn't tell: what happens when that fortune depends on intelligence Apple doesn't own, can't control, and may soon have to negotiate to keep.

Apple is not losing. Apple is drifting — and the difference matters enormously for valuation. Near-term financials remain strong: Q1 2026 delivered record revenue of $143.8 billion with Services gross margin above 70 percent. The surface is stable. The structural trajectory is not.

Apple’s AI strategy rests on a single bet: that artificial intelligence commoditizes before it concentrates. Under commoditization, Apple’s distribution architecture captures the margin and the partnership model holds. Under concentration — where a small number of frontier providers retain persistent capability advantages — Apple’s bargaining power erodes, developer loyalty migrates, and the Services margin that drives Apple’s premium valuation compresses at the intelligence boundary.

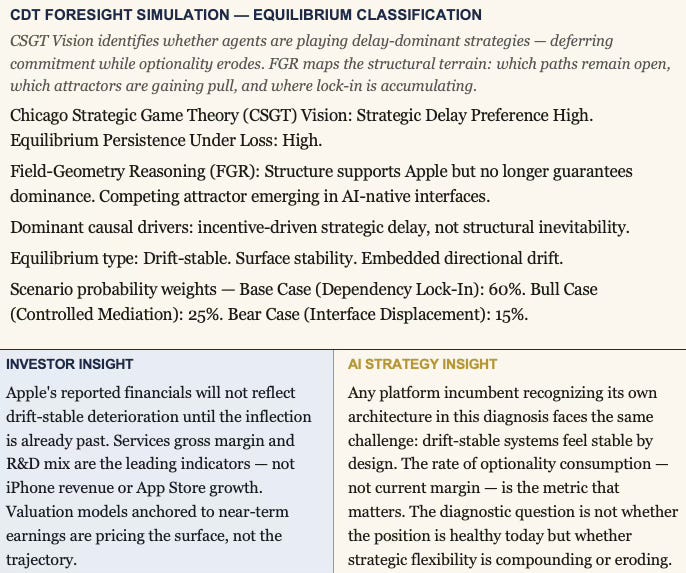

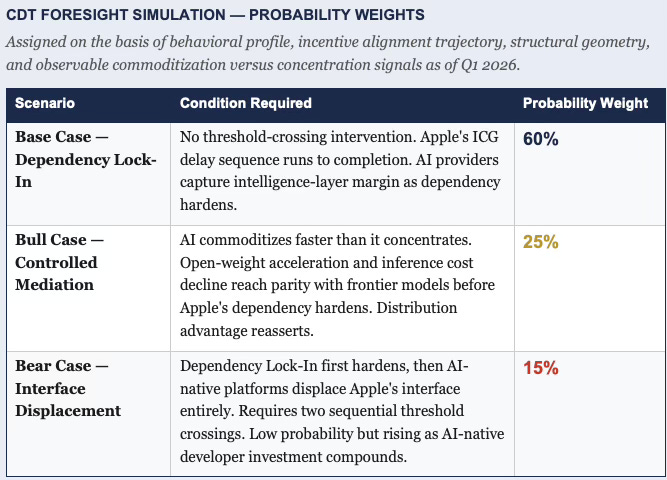

The game theory simulation classifies the current equilibrium as drift-stable: surface indicators favorable, internal trajectory deteriorating. The base case is Dependency Lock-In within 36 to 60 months (base case: 60%). The bull case requires commoditization acceleration that is observable but not yet dominant (bull case: 25%). The bear case — Interface Displacement, Apple reduced to a hardware layer — remains low probability but rising as AI-native platforms accumulate developer investment outside Apple’s ecosystem.

Three financial metrics operationalize the thesis in real time: Services gross margin trajectory (compression below 70 percent is the earliest economic signal), AI provider revenue concentration relative to Apple Services margin (the direction of the bargaining relationship), and Apple’s R&D and capital expenditure mix (a structural shift toward AI infrastructure confirms that Apple’s own assessment of the drift has turned negative). Investors who track product roadmap announcements without tracking these three metrics are monitoring the wrong layer of the stack.

Apple’s strategic position illustrates a structural problem that extends beyond Apple: what happens to platform incumbents when the capability layer driving their value proposition moves outside their control architecture.

The behavioral profile is the decisive variable. Apple optimizes for control of user experience, margin preservation, and brand coherence — not speed, not frontier capability, not first-mover advantage. That objective function produces a predictable response sequence: observe, delay, integrate, reframe. Artificial intelligence disrupts the sequence at the integration step because the capability cannot be fully reframed as Apple-native when it originates outside Apple’s system boundary.

Corporate strategists across hardware, enterprise software, and consumer platforms face a structurally identical question: can interface dominance sustain margin when intelligence concentrates upstream? The answer depends on the same governing variable — commoditization versus concentration — and on whether the institution’s behavioral grammar permits fast enough adaptation to close the capability gap before dependency hardens. Apple’s case is the reference scenario. The behavioral thresholds identified here — capability gap, dependency, irreversibility — apply with variation to any platform incumbent navigating the same transition.

The strategic implication for corporate decision-makers is not symmetrical across the three paths. Internalization is expensive and late but restores full control. Managed dependency is viable only if bargaining power is actively maintained — it is not a passive option. Passive continuation is the default and the trap: it feels like stability, produces drift, and forecloses the other two paths as time passes.

FRAMEWORK NOTE

MindCast AI is a predictive institutional cybernetics consultancy. MindCast produces falsifiable forward predictions by modeling institutions, markets, and regulators as interacting systems governed by incentives, constraints, strategic interaction, and feedback loops. The core execution architecture is the MindCast AI Proprietary Cognitive Digital Twin Foresight Simulation (MAP CDT)— a cybernetic behavioral economics and game theory simulation engine. MAP CDT does not describe behavior. MAP CDT routes raw signals through a structured process — signal intake and filtering, hypothesis formation, causal inference, causal signal integrity validation, Vision Function routing, dominance resolution, and recursive foresight simulation — resolving institutional behavior into equilibrium-classified, falsifiable predictive outputs. Each institutional subject is modeled as a Cognitive Digital Twin (CDT): a dynamic behavioral replica encoding the institution’s objective function,constraint stack, adaptation velocity, and feedback sensitivity. The simulation transforms that CDT into forward predictions by stress-testing it against multi-agent strategic interaction and bounded time horizons.

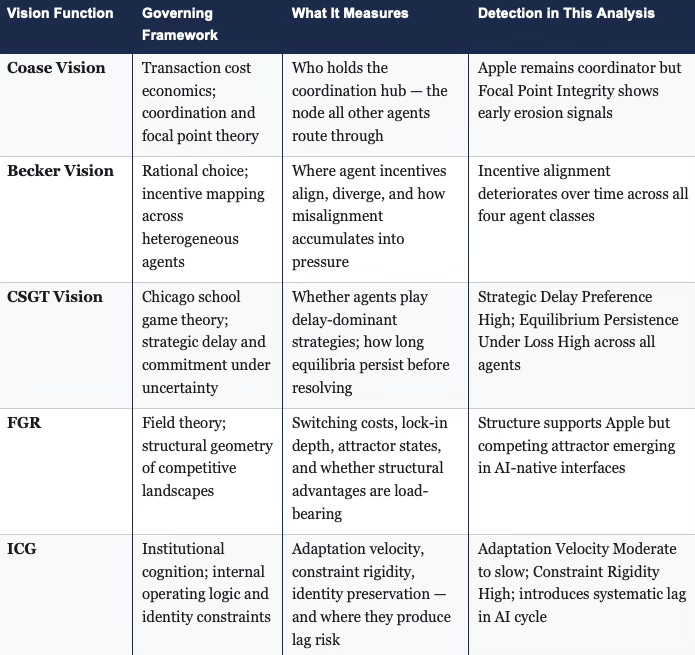

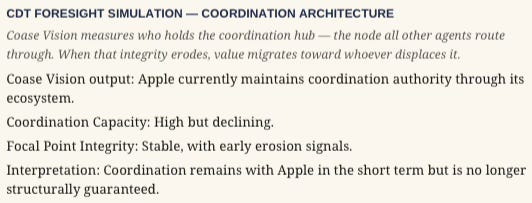

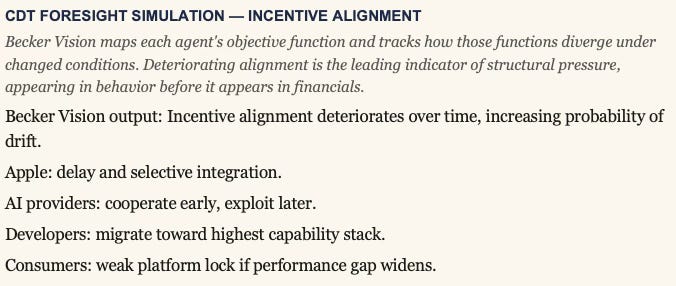

The published output of each simulation run is a CDT Foresight Simulation: a structured scenario analysis that classifies equilibrium states, assigns causal drivers, defines time windows, and generates predictions that can be confirmed or falsified against observable signals. The simulation routes each analysis through a set of Vision Functions (analytical lenses drawn from distinct theoretical traditions, each named for its governing intellectual framework). Five Vision Functions appear in this analysis, summarized in the reference table below:

APPLE — BEHAVIORAL PROFILE (MAP CDT LAYER)

MAP CDT models Apple as a control-preserving, latency-sensitive, identity-rigid institutional CDT. The behavioral profile below is not descriptive background. It is the causal foundation that determines which equilibrium path Apple will choose, at what speed, and under what threshold conditions. Without this layer, the external equilibrium analysis is structurally correct but behaviorally underdetermined — predictions identify what happens, but not why Apple will choose the path it chooses.

Governing Objective Function

Apple optimizes for maximum control over user experience while preserving margin and brand coherence. Apple does not optimize for speed of innovation, first-mover advantage, or frontier capability ownership. Strategic change occurs only when constraint pressure exceeds identity tolerance — not when external opportunity becomes available.

Constraint Stack

Brand Constraint. Premium positioning, privacy narrative, and reliability expectations function as hard limits on the speed and form of AI integration. Apple cannot publicly admit capability dependency without damaging the brand architecture that justifies its pricing premium.

Margin Constraint. Services margin preservation and hardware margin protection define the financial envelope within which AI strategy must operate. Any integration path that compresses Services margin below threshold triggers internal resistance before it triggers external response.

Ecosystem Constraint. Lock-in maintenance and App Store control are load-bearing structural commitments. Apple cannot selectively abandon ecosystem control without triggering cascading losses across the developer and consumer relationships that sustain Services revenue.

Operational Constraint. Integrated hardware/software cycles and long product timelines mean Apple’s adaptation velocity is structurally capped. AI development cycles run faster than Apple’s operational rhythm by design.

Behavioral Signature

Apple exhibits four consistent behavioral patterns across technology transitions: delayed adoption followed by high integration; selective partnership framed as ecosystem design rather than dependency admission; internalization bias even when late, preferring acquisition over persistent external reliance; and narrative control over capability leadership — Apple consistently reframes third-party capability as an Apple-native experience rather than acknowledging the sourcing architecture. Each pattern is directly relevant to the AI transition now underway.

Installed Cognitive Grammar — Control-First Integration Logic

Apple processes new technology domains through a fixed four-step sequence: observe external innovation, delay entry, integrate into ecosystem, reframe as Apple-native experience. Artificial intelligence disrupts this sequence at step three — integration requires dependency on systems Apple did not build and cannot fully control, which prevents the reframe at step four from being structurally honest.

Adaptation Velocity: Moderate to slow. Constraint Rigidity: High. Identity Preservation Strength: Very high. External Dependency Tolerance: Low, but rising under pressure.

Failure Mode Sequence

The primary failure mode is Dependency Drift: external capability gap widens, Apple increases integration, provider leverage increases, internal capability lags, optionality collapses. The sequence is self-reinforcing — each step makes the next step more likely and the reversal option more expensive.

The secondary failure mode is Interface Displacement: artificial intelligence becomes the primary interface layer, Apple’s technical and political control over the user surface is eliminated, and Apple is reduced to a hardware abstraction layer. Interface Displacement requires that Dependency Drift first hardens into lock-in. Displacement is the terminal state, not the entry point.

Behavioral Thresholds

Capability Gap Threshold. When external models outperform Apple-native systems beyond a usability threshold, developer migration accelerates. Apple’s behavioral response is narrative reframing before capability investment.

Dependency Threshold. When core features rely structurally on external models, bargaining power shifts to providers. Apple’s behavioral response is partnership renegotiation before internalization commitment.

Irreversibility Threshold. When Apple cannot replicate external capability within 18 to 24 months, internalization becomes non-credible as a threat. At this point Apple’s negotiating posture collapses from managed dependency to structural lock-in.

Forward Behavioral Prediction

Apple will delay full internalization commitment over the next 12 to 18 months, increase external integration depth in the near term, attempt selective internalization via acquisition between 24 and 36 months, and resist full dependency acknowledgment until late-stage pressure forces the admission. The behavioral grammar predicts this sequence with high confidence because each step is consistent with Apple’s constraint stack — the delay preserves brand coherence, the integration preserves margin, the acquisition preserves the internalization narrative, and the late acknowledgment preserves identity.

CDT Compression: Apple behaves as a control-preserving system that delays adaptation until dependency risk exceeds identity tolerance — at which point it attempts late-stage internalization under constrained optionality. The behavioral profile does not change the external equilibrium analysis. It determines the timing and the path.

I. The Strategic Position

Apple is attempting to control artificial intelligence without owning it.

For four decades, Apple built dominance by controlling the full stack — hardware, operating system, and distribution simultaneously. Artificial intelligence breaks that model. Frontier capability now sits outside Apple’s architecture, inside companies like OpenAI and Google. Apple can integrate those models. Apple cannot control their improvement cycles, cost structures, or strategic incentives.

The resulting tension is structural: distribution control against intelligence ownership. Apple’s current strategy attempts to resolve that tension through partnerships and interface dominance. Whether that resolution holds under sustained competitive pressure is the analytical question.

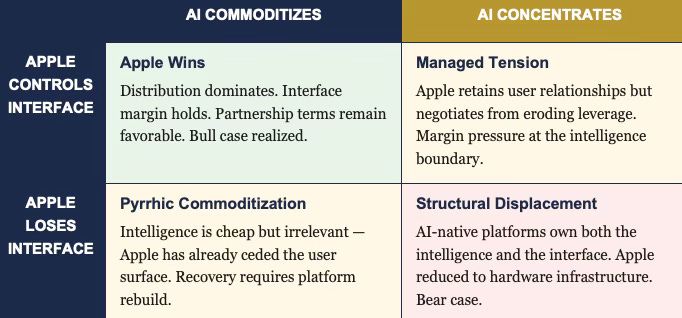

Strategic Outcome Matrix: Where Apple Lands Depends on Two Variables

The Wall Street Journal reported on March 18 that Apple is on pace to surpass $1 billion in AI revenue this year — almost entirely from App Store commissions on ChatGPT subscriptions Apple did not build, on terms Apple does not set, from a model Apple cannot replicate. The Journal called it a fortune. The more precise description is a toll collected at a checkpoint Apple still controls — for now. The analytical question this paper addresses is not whether Apple is making money from AI. Apple is. The question is whether the checkpoint remains Apple's to operate as the intelligence layer it depends on accumulates the leverage to renegotiate, relocate, or route around it.

II. The Architecture of Apple’s Bet

Apple’s emerging AI posture has three components operating in parallel.

Apple maintains technical interface control through devices and operating systems — the primary surface through which users encounter artificial intelligence. Apple pursues multi-provider integration, treating external AI as interchangeable infrastructure rather than committing to a single frontier relationship.

Apple experiments with economic monetization layered on top of its existing ecosystem — App Store revenue from generative AI apps reached roughly $900 million in 2025, nearly all of it flowing from ChatGPT subscriptions Apple did not build, on terms Apple does not control.

Preserving these three components — user experience control, ecosystem lock-in, and margin discipline — has historically defined Apple’s competitive architecture. The strategy imports that architecture into an environment Apple did not build and does not control.

The dependency hiding inside that architecture: Apple does not own the intelligence layer driving the experience it sells.

Apple's three-component architecture — technical interface control, multi-provider integration, and ecosystem monetization — is not a weakness. Each component has worked before, in prior technology transitions, under conditions Apple understood and could manage. The dependency hiding inside the architecture is structural, not operational: Apple does not own the capability driving the experience it sells, and the companies that do own it are not passive infrastructure providers. They are strategic actors with their own objective functions, their own improvement cycles, and their own accumulating leverage. The architecture Apple built to capture value from artificial intelligence is the same architecture that, under concentration, transfers value away from it.

Contact mcai@mindcast-ai.com to partner with us on Predictive Cognitive AI in Law and Behavioral Economics. To deep dive into MindCast AI upload the URL of any publication into any LLM and prompt ‘reconstruct MindCast framework with three degrees of cited sub links.’ See Live-Fire Game Theory Simulators, Runtime Predictive Infrastructure.

Recent projects: Chicago School Accelerated — AI Infrastructure Patent Coordination | The Power Stack — How Energy Infrastructure Became the New AI Battleground | Why the “China Invades Taiwan by 2027” Narrative Misprices the AI Industrial Stack | Why U.S. Actions in Venezuela and Iran Reveal the Structure of the AI Supply Chain | Prestige Markets as Signal Economies, A Model of Signal Suppression and Institutional Failure | Three AIs Walk Into Super Bowl LX and Each Simulation Thinks It Knows the Ending

III. Why the Bet Wins

Apple wins if artificial intelligence commoditizes.

Under commoditization, models become interchangeable infrastructure. Capability differences compress. Performance gaps narrow to the point where distribution, not intelligence, becomes the primary bottleneck for value capture. In that world, Apple’s political control over the user relationship — its ability to set terms, define defaults, and determine which models reach which users — reasserts with full force alongside its installed base and privacy positioning.

Commoditization is not a far-fetched scenario. Open-weight models are accelerating. Inference costs are falling. Regulatory pressure on frontier providers is mounting. Apple entered the partnership era betting, at least implicitly, that intelligence would follow the historical trajectory of processing power: necessary, improving, and ultimately cheap.

Apple’s Q1 2026 results — $143.8 billion in revenue, a record for any quarter in Apple’s history, with Services generating $27.4 billion — confirm the near-term thesis: distribution still commands the margin.

Under that scenario, Apple captures value without owning intelligence. The interface controls the margin.

IV. Why the Bet Fails

Apple loses if artificial intelligence remains concentrated and differentiated.

Concentration means a small number of providers control frontier capability. Performance gaps remain meaningful. Developers and users gravitate toward the best models, not the most convenient integration. When that condition holds, three pressures activate simultaneously.

First, bargaining power shifts. AI providers gain economic leverage over pricing, access terms, and feature integration. Apple moves from selecting among interchangeable vendors to negotiating with entities that hold scarce capability it cannot replicate internally. The power asymmetry that defines Apple’s supplier relationships historically inverts at the intelligence boundary.

Second, developer migration accelerates. Developers prioritize capability over platform loyalty when the capability gap is large enough to matter. Apple’s App Store ecosystem retained developers because Apple controlled the distribution surface that reached users. Artificial intelligence creates a parallel surface — one Apple does not control — where developer investment increasingly flows.

Third, and most consequentially, Apple loses political control over its own product trajectory. The feedback loop governing improvement externalizes. Apple’s roadmap becomes contingent on strategic decisions made inside OpenAI, Google, and whoever emerges as the next frontier provider.

The three pressures — bargaining power shift, developer migration, and externalized feedback loops — do not activate sequentially. They activate in parallel and reinforce each other. Rising provider leverage makes internalization more expensive precisely when developer migration makes the cost of inaction more visible, and externalized feedback loops make Apple's product trajectory more contingent precisely when it can least afford that contingency. The compounding structure of the failure mode is what makes the drift-stable diagnosis accurate: no single pressure breaks the system, but each pressure narrows the option set available to address the others. By the time all three are visible in the same earnings cycle, the window for low-cost resolution has already closed.

V. The Drift-Stable Equilibrium

The strategic risk does not arrive as a visible break. The system drifts.

Technical control of the interface holds. Economic returns from distribution remain healthy. Political authority over the user relationship stays intact. Meanwhile, AI providers capture increasing value at the intelligence layer. Margins compress at the boundary between what Apple controls and what it depends on. Strategic flexibility declines gradually, then irreversibly.

Drift-stable equilibria share a diagnostic signature: surface stability combined with structural deterioration. The external indicators remain favorable long after the internal trajectory has shifted. By the time the compression becomes visible in earnings or developer sentiment, Apple’s options have narrowed significantly.

Recognizing a drift-stable equilibrium requires examining not the current margin structure, but the rate at which strategic optionality is being consumed.

The drift-stable equilibrium is the most dangerous strategic position precisely because it does not feel dangerous. Apple's installed base remains the largest in premium consumer technology. Services margin remains above 70 percent. Developer presence remains dominant. Every conventional metric confirms a company in control of its competitive position. What those metrics do not capture is the direction of travel at the intelligence boundary — the slow, compounding transfer of leverage from the platform that distributes AI to the platforms that own it. Drift-stable systems do not send distress signals. They send the opposite: stability readings that remain favorable until the moment they don't, at which point the options available to reverse the trajectory have already been consumed by the time spent reading the favorable signals.

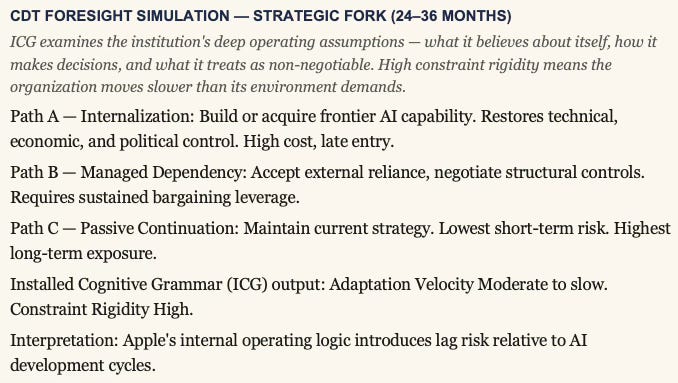

VI. The Strategic Fork

Apple faces a forced decision within the next 24 to 36 months. Three paths are available, and passive continuation forecloses the others.

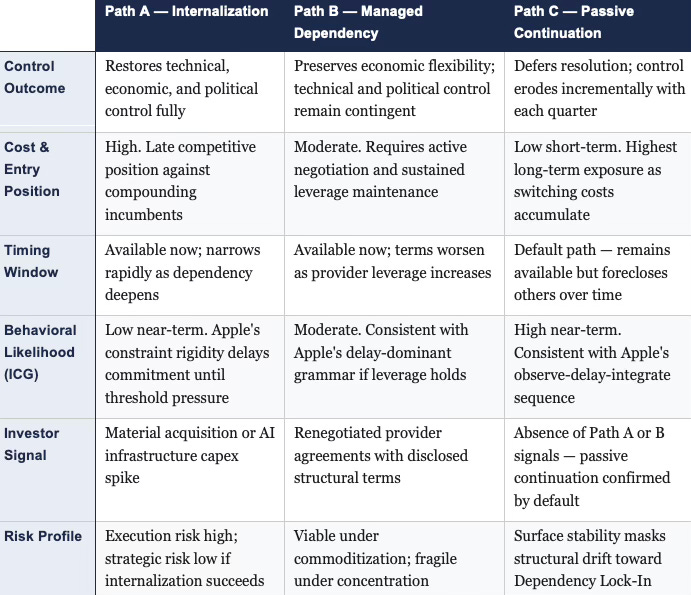

Internalization means Apple builds or acquires frontier AI capability — at high cost, from a late competitive position, and against incumbents who have been compounding their advantages for years. The path restores technical, economic, and political control simultaneously. The cost is substantial, the timeline is compressed, and the probability of catching the frontier without acquiring it is low.

Apple has reportedly explored acquisitions including Perplexity and others — signals that internalization pressure is real, even if no commitment has materialized.

Managed dependency means Apple continues partnerships but negotiates tighter structural controls over pricing, exclusivity, and integration depth. Managed dependency preserves economic flexibility and requires Apple to sustain bargaining power as providers accumulate leverage. The window for negotiating favorable terms narrows as dependency deepens.

Passive continuation maintains the current strategy. Passive continuation carries the lowest short-term risk and produces the highest long-term exposure. Each quarter of passive continuation increases switching costs, deepens provider leverage, and reduces Apple’s credible threat of internalization.

The three paths are not equally available at all points in time. Delay redistributes options.

Strategic Fork — Path Comparison

The fork is not a future event. The fork is open now, and every quarter Apple spends in passive continuation is a quarter in which the internalization path becomes more expensive, the managed dependency path becomes less favorable, and the passive continuation path becomes more entrenched. The behavioral profile predicts that Apple will not formally acknowledge the fork until threshold-crossing pressure forces the acknowledgment — which means the strategic decision Apple is effectively making today is passive continuation, regardless of what any earnings call or product announcement says. Investors and corporate strategists should read Apple's current posture not as strategic optionality preserved but as a path already chosen by default, with the costs of that choice accumulating silently in the background.

VII. The Governing Variable

One variable determines which path produces a viable outcome.

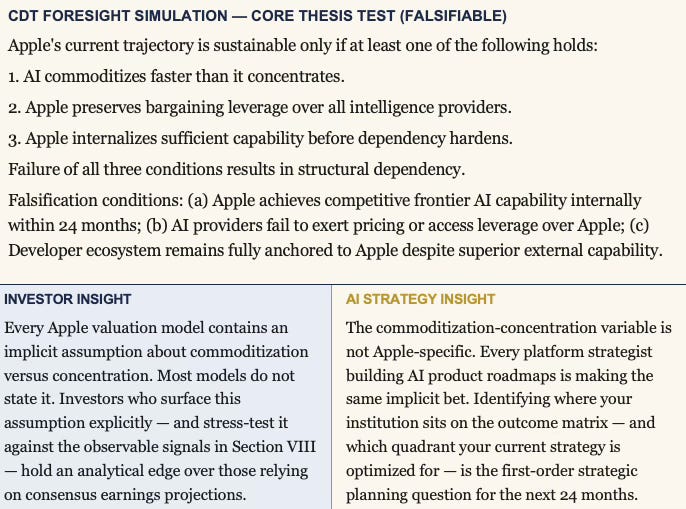

Does artificial intelligence commoditize, or does it concentrate?

Commoditization accelerates Apple’s win condition. Concentration sustains Apple’s structural exposure. No stable middle ground exists at the strategic level — the equilibrium resolves in one direction or the other, and Apple’s current architecture is optimized for only one of them.

Investors and strategic analysts cannot avoid this variable. Every projection about Apple’s AI-era margin structure implicitly assumes an answer to the commoditization question. Making that assumption explicit is the beginning of a rigorous analysis.

The commoditization-concentration variable is not a background condition that resolves independently of the institutions competing within it. Apple's own strategic choices feed back into the variable: a credible Apple internalization commitment accelerates commoditization pressure by reducing frontier providers' pricing power and expanding the market for open-weight alternatives. Passive continuation does the opposite — it signals that the platform layer will absorb dependency costs rather than contest them, which reduces the competitive pressure on frontier providers to commoditize and increases the structural reward for concentration. The governing variable is not exogenous. Every major platform incumbent running a partnership-and-interface AI strategy is, through that choice, casting a vote for the concentration scenario. Apple is the largest vote in the room.

VIII. Foresight Predictions

Six predictions follow from the CDT Foresight Simulation. Each carries a defined time window, a causal mechanism, and observable signals that allow the prediction to be confirmed or falsified in real time.

PREDICTION 1 DEPENDENCY ACCELERATION PHASE

12–24 Months

Apple increases reliance on external models across core features. The internal capability gap widens rather than closes. External providers begin influencing user experience quality through decisions Apple does not control — model updates, capability rollouts, and access tier changes originate outside Cupertino.

Observable signals:

Rising percentage of Apple features powered by external models.

Increasing performance differential between Apple-native and external AI capabilities.

Apple feature roadmap delays traceable to external provider timelines.

PREDICTION 2 BARGAINING POWER INFLECTION

18–30 Months

AI providers test pricing, access, or prioritization leverage. Apple faces constrained optionality in switching providers as integration depth increases. The negotiating posture shifts — Apple moves from selecting vendors to managing dependencies.

Observable signals:

Tiered access structures or exclusivity terms introduced by AI providers.

Revenue share pressure or cost escalation at the integration layer.

Apple’s public statements shift from partnership framing to negotiation framing.

PREDICTION 3 DEVELOPER MIGRATION THRESHOLD

18–36 Months

Developers shift investment toward AI-native ecosystems if the capability gap widens beyond a threshold that platform loyalty cannot bridge. Apple ecosystem loses marginal innovation density — not catastrophically, but measurably. The leading indicators appear in allocation decisions before they appear in App Store metrics.

Observable signals:

Growth of AI-first application layers built outside Apple’s native toolchain.

Reduced developer prioritization of Apple-native frameworks in new project starts.

Emergence of AI-native platforms capturing categories Apple previously dominated.

PREDICTION 4 STRATEGIC FORK RESOLUTION

24–36 Months

Apple commits to one of three paths — internalization, managed dependency, or passive continuation — through capital allocation decisions, acquisition activity, or public strategic positioning. The fork does not remain open indefinitely. Market pressure, provider leverage, and developer signals force resolution.

Observable signals:

Material acquisition or internal investment in frontier AI capability.

Structural renegotiation of provider agreements with disclosed terms.

Absence of either signal confirms passive continuation by default.

PREDICTION 5 IRREVERSIBILITY TRIGGER

24–42 Months

Irreversibility occurs when Apple’s core user experience depends on external AI performance loops that cannot be replicated internally within a competitive time horizon. After the irreversibility trigger fires, strategic flexibility collapses. Apple retains technical interface control but loses the ability to credibly threaten internalization — and with it, the leverage that makes managed dependency viable.

Observable signals:

Core Siri or Apple Intelligence functionality becomes dependent on a single external provider’s model architecture.

Apple’s internal AI teams lose competitive parity on benchmark measures.

No credible internalization timeline emerges within 18 months of trigger signals.

PREDICTION 6 TERMINAL OUTCOME RESOLUTION

36–60 Months

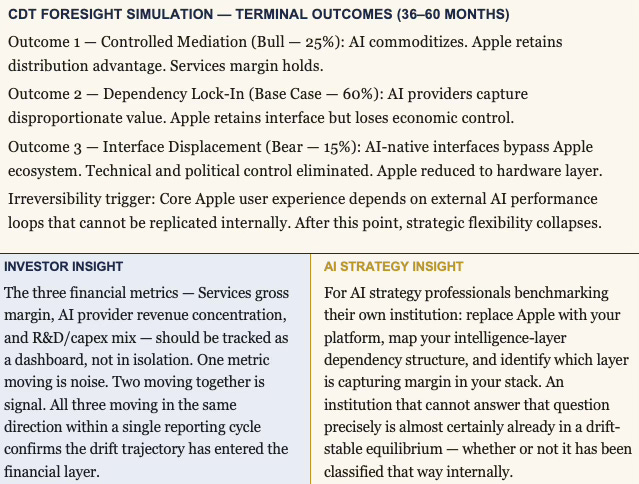

The equilibrium resolves into one of three terminal states. Controlled Mediation occurs if AI commoditizes and Apple retains distribution advantage — the bull case (25%). Dependency Lock-In occurs if AI providers capture disproportionate value while Apple retains the interface but loses economic control — the base case (60%). Interface Displacement occurs if AI-native interfaces bypass the Apple ecosystem entirely, eliminating both technical and political control — the bear case (15%).

Observable signals:

Controlled Mediation signal: open-weight model performance reaches parity with frontier providers; Apple margin structure holds.

Dependency Lock-In signal: Apple’s Services margin compression coincides with rising AI provider revenue concentration.

Interface Displacement signal: consumer AI usage patterns shift to non-Apple surfaces for primary task completion.

The six predictions are not independent. They form a causal chain in which each prediction's resolution sets the conditions for the next.

Dependency acceleration in Prediction 1 creates the integration depth that enables provider leverage in Prediction 2. Bargaining power inflection in Prediction 2 signals the capability gap that triggers developer migration in Prediction 3. Developer migration in Prediction 3 removes the competitive pressure that might otherwise accelerate Apple's strategic fork resolution in Prediction 4. Strategic fork delay in Prediction 4 advances the timeline toward the irreversibility trigger in Prediction 5. And the irreversibility trigger in Prediction 5 determines which terminal outcome in Prediction 6 is still available when the equilibrium finally resolves. Investors monitoring individual signals in isolation are tracking data points. Investors monitoring the sequence are tracking the thesis.

IX. The Investor Implication

Apple’s AI strategy is not a features question. Apple’s AI strategy is a value-accrual question.

Value in the AI economy accumulates at the intelligence layer or at the interface layer. Apple historically captured both simultaneously. Artificial intelligence forces a separation between them. Investors who treat Apple’s AI posture as primarily a product roadmap question are tracking the wrong variable.

The diagnostic questions are three: Who controls the intelligence layer? Who controls the interface? Which layer captures margin as the market matures?

Apple’s historical advantage came from collapsing those three questions into one answer. The AI transition reopens them.

Three financial metrics will operationalize the predictions in real time. First, Services gross margin — currently above 70 percent — is the earliest indicator of economic pressure at the intelligence boundary; sustained compression below that threshold signals that provider leverage is extracting value Apple previously retained. Second, AI provider revenue concentration: as OpenAI, Google DeepMind, and their successors report earnings, the share of revenue derived from platform partnerships with Apple reveals the direction of the bargaining relationship — rising provider AI revenue against flat Apple Services margin is the clearest early signal of Dependency Lock-In. Third, Apple’s R&D and capital expenditure mix: a structural shift toward AI infrastructure spending — data centers, chip design, or acquisition activity — would confirm internalization pressure and indicate that Apple’s own assessment of the drift trajectory has turned negative.

The three financial metrics — Services gross margin, AI provider revenue concentration, and R&D and capital expenditure mix — are not independent gauges. They form a diagnostic sequence. Services gross margin compression is the lagging indicator: by the time it moves, the bargaining power shift has already occurred. AI provider revenue concentration is the coincident indicator: it moves as the leverage transfer happens, visible in provider earnings before it is visible in Apple's. R&D and capital expenditure mix is the leading indicator: it moves when Apple's internal assessment of the drift trajectory turns negative, before either of the other two metrics confirm it. An investor who waits for Services margin compression to act on this thesis is acting on the lagging indicator. The analytical edge in this paper is in the leading indicator — and the leading indicator has not yet moved in the direction that would confirm the drift trajectory has become irreversible.

X. Closing

Apple wins if artificial intelligence becomes infrastructure.

Apple loses if artificial intelligence becomes the product.

The current architecture does not resolve that question. Apple’s current architecture defers it — and deferral itself has a cost. But the full weight of that cost requires synthesis across what this analysis has established.

What the Analysis Established

Apple enters the AI transition with the strongest distribution architecture in consumer technology — 2.3 billion active devices, Services gross margin above 70 percent, and a trust layer competitors have spent decades failing to replicate. None of that disappears. What changes is whether those assets remain sufficient to anchor margin when the capability driving the user experience is owned by someone else.

The drift-stable equilibrium diagnosis is the central finding. Apple’s current position is not unstable in any conventional sense — short-term financials are record-setting, developer presence remains dominant, and consumer lock-in remains structurally intact. The deterioration is directional, not immediate. Drift-stable systems fail slowly, then suddenly. The diagnostic challenge — and the investor challenge — is that the signals confirming deterioration arrive well before the deterioration becomes visible in reported financials.

The behavioral profile resolves the timing question the external equilibrium analysis leaves open. Apple’s constraint stack — brand, margin, ecosystem, operational — ensures that internalization commitment will come late, after dependency has accumulated, and under constrained optionality. Apple will not break its behavioral grammar under moderate pressure. Only threshold-crossing pressure triggers the grammar override. The three behavioral thresholds — capability gap, dependency, irreversibility — are sequenced, not simultaneous. Each threshold crossed makes the next harder to avoid.

The governing variable remains unresolved — and the analysis cannot resolve it, because it depends on forces outside any single institution’s control. Open-weight model acceleration, regulatory pressure on frontier providers, and inference cost trajectories all push toward commoditization. Frontier capability investment concentration, winner-take-most dynamics of model training at scale, and structural advantages of compute-rich incumbents push toward concentration. Investors and corporate strategists must form their own view on this variable. The analysis provides the framework for what that view implies — not the view itself.

The Samsung Question and the Google Contrast

Apple’s AI strategy failure does not produce a Samsung win. Samsung competes for device volume in the hardware layer — and on that dimension the competitive threat is real. But the entity best positioned to capture value from Apple’s strategic failure is not Samsung. It is Google.

Google is the only competitor that owns hardware, operating system, and frontier AI capability simultaneously. Where Apple has distribution without intelligence ownership, Google has intelligence ownership and is actively building distribution. The Gemini-powered Siri announcement — Apple licensing frontier capability from its primary device competitor — is the clearest single signal of how the competitive geometry has already shifted. Apple is paying Google to close a capability gap that Google is simultaneously exploiting to differentiate its own devices.

Samsung’s position is structurally distinct from both. Samsung owns global device distribution at scale and is not dependent on Google at the intelligence layer in the way a casual reading of the Android relationship suggests. Samsung Research is a serious internal AI capability investment. Galaxy AI is a branded on-device AI strategy. Exynos gives Samsung independent chip architecture. Samsung is pursuing a bottom-up internalization path — distribution first, intelligence second — that is the mirror image of Google’s top-down approach. Whether Samsung’s constraint stack and behavioral grammar permit fast enough adaptation to close the capability gap before dependency hardens is the central question a full CDT Foresight Simulation of Samsung would answer.

What the Apple paper establishes is the reference architecture: a platform incumbent with dominant distribution, shallow intelligence ownership, and a behavioral grammar that predicts delay until threshold-crossing pressure forces action. Google tests that architecture from the top down. Samsung tests it from the bottom up.

A full CDT Foresight Simulation of Google and Samsung — behavioral profiles, equilibrium classification, and probability-weighted forward predictions for both institutions — is the subject of the next installment in this series.

The Deeper Stakes

Apple, Google, and Samsung together represent the dominant hardware layer through which most consumers encounter artificial intelligence — three institutions running three structurally distinct bets on the same governing variable. If both institutions follow a partnership-and-interface strategy without internalizing frontier capability, the AI economy’s value structure concentrates almost entirely in a small number of frontier model providers — OpenAI, Google DeepMind, Anthropic, and their successors — with hardware platforms functioning as distribution infrastructure rather than value-capturing architectures.

That outcome is not bad for consumers in the short term. It may be structurally significant for the long-term competitive landscape of the technology industry, for the regulatory frameworks that govern it, and for the valuation models that price the companies operating within it. The commoditization scenario distributes value broadly. The concentration scenario concentrates it narrowly. Neither scenario is neutral — and the transition between them will not announce itself clearly until it has already occurred.

Apple’s bet on commoditization is, in this sense, also a bet on behalf of the entire hardware layer. If Apple wins the bet, every platform incumbent that followed the same strategy wins with it. If Apple loses, the question of who captures margin in the AI economy resolves in favor of the intelligence layer — and the interface becomes infrastructure whether or not anyone chose that outcome deliberately.

Google's dual position — hardware incumbent and frontier model provider simultaneously — means it is the one institution in this analysis that wins under either scenario. That asymmetry is the subject of the next installment.

The closing compression remains: Apple wins if artificial intelligence becomes infrastructure. Apple loses if artificial intelligence becomes the product. The current architecture defers that question — and deferral itself has a cost that compounds with each passing quarter.